Author(s)

To access the full paper, download the PDF on the left-hand sidebar.

Introduction

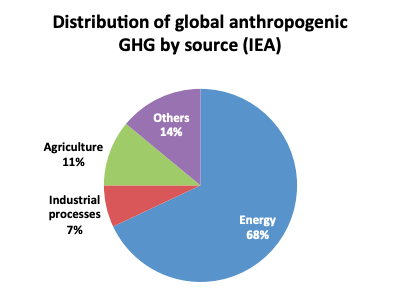

Burning coal, oil and natural gas is responsible for two-thirds of the world’s emissions of greenhouse gases. These same fuels also represent the economic mainstay of resource-rich countries and the world’s largest firms. Any steps humanity takes to reduce climate-warming emissions will damage commercial opportunities. Relief for the climate means danger for the fossil fuel business. Given the stakes, it bears asking: What, exactly, are the risks? How are they manifested and distributed?

Luminaries such as the US president and the governor of the Bank of England have called for leaving large portions of oil, gas, and coal reserves in the ground. International Energy Agency director Fatih Birol has said that two-thirds of known fossil fuel reserves can never be burned if humanity is to prevent average global temperatures from rising by more than 2°C. 1 Pope Francis, the leader of the world’s 1.2 billion Catholics, has called for “swift and unified global action” on climate change.2 For fossil fuel businesses, such statements represent existential threats. By Citicorp’s estimate, large-scale resource abandonment translates into an eye-watering $100 trillion in foregone fossil fuel revenues by 2050.3

Figure 1 — Fossil Fuels Were Responsible for Two-thirds of Global Greenhouse Gas Emissions in 2010

While the consequence of these statements—and the likelihood of earth’s warming lingering below the 2°C threshold—remain in doubt, it is clear that climate action will make life increasingly difficult for businesses that profit from fossil fuels. For the industry, a new set of risks has come to the fore. These range from legal and shareholder actions pertaining to big international oil companies (IOCs), government moves to block export pipelines, 4 and assessments that divide fossil fuel reserves into usable and “stranded” portions.5

The risk burden across the sector—for firms dealing in coal, oil, and natural gas—will not be shared uniformly. While much of the focus has been on oil companies and countries harboring large crude oil reserves, the most damaging effects have fallen upon businesses based on coal, the most polluting and carbon-intense of the fossil fuels. At the other end of the spectrum, the natural gas industry has benefited from climate action. Lower-carbon gas is widely accepted as a preferential replacement for coal and a “bridge” toward decarbonized electricity markets.

Decarbonization risks are also higher in the mature OECD economies, where abatement actions and government regulation is more common and robust. In much of the developing world, fossil fuel demand growth remains high. Governments can be expected to insulate state-owned energy businesses from some risks outlined here.

There are four main categories of climate risk for the fossil fuel industry:

- Policy risk: Government policies, regulations, and pledges that reduce carbon emissions; or policies that support competing technology

- Demand risk: Decline in global fossil fuel demand due to climate and other factors

- Divestment risk: Shareholder or grassroots activism that seeks to influence producer companies (and possibly countries) through financial or reputational means; or investor avoidance of fossil fuel shares

- Competition risk: Rivalry for market share among producers seeking to monetize reserves before they are rendered unburnable; competition between fossil and noncarbon sources of energy

Additionally, there are fuel-specific risks that are not shared equally among the three6 fossil fuel types.

Below, this paper compiles and describes the risk types affecting fossil fuels. I do not attempt to measure or quantify these risks or estimate their effects on future carbon emissions or companies’ balance sheets.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.