Abstract

This brief argues that, in contrast to the pessimism and ongoing recession in Latin America generated by the collapse of commodity prices, there are reasons for optimism in the area of external financing. In fact, we may be in the midst of the first crisis in Latin American history in which resource transfers through the capital account would continue to be positive, a remarkable historical fact. The closure of financial markets has been weak and temporary, FDI continues to make positive resource transfers, and China is providing additional resources.

The tendency of global finance to behave in a procyclical way vis-à-vis emerging and developing countries, generating on many occasions boom-bust cycles, has been a subject of extensive discussion in the economic literature in recent decades.1 Viewed by historical standards, however, the crisis generated by the collapse of commodity prices since mid-2014 (referred to below simply as the current crisis) may be the first in the region’s history in which there will be no “sudden stop”2 in external financing—or it would be a feeble one. Although there have been disturbances in financial flows to the region, reflected in periods of increases in sovereign risk spreads and reduced availability of financing, they have been weak compared to those experienced during previous crises. Foreign direct investment (FDI) has continued to flow into the region, and a new source of finance, China, has made strong inroads. The net effect has been persistent positive net resource flows through the capital account. This is, of course, in sharp contrast to the severe trade shock associated with the collapse of commodity prices the region has experienced in recent years.3

Explanations for this recent pattern must mix external and regional factors. Among the former, the most important by far is the low-interest environment that has characterized all developed countries since the 2008–2009 North Atlantic financial crisis.4 Regional factors include the significant changes in the external balance sheets of Latin American countries, particularly the improvement that took place during the first phase of the commodity boom (2004 to mid-2008), as well as major changes in the behavior of financial flows and FDI that have occurred since the early 2000s.

External Financing to Latin America: A First, Broad Look

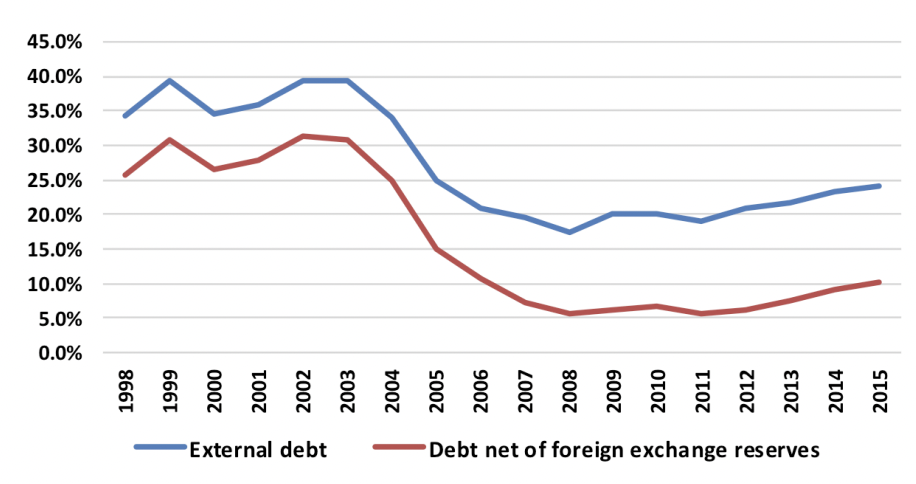

Figure 1 — Gross and Net External Debt, 1998–2015 (% GDP)

The evolution of external financing to Latin America has had novel features over the past decade. The most important result of these trends has been the significant moderation in the region’s vulnerability to fluctuations in external capital flows. This reflects global trends, particularly the boom in financing to emerging markets prior to the North Atlantic financial crisis. The boom led to the lowest risk spreads on record, achieved in 2006 and in 2007 until the outbreak of the US subprime crisis in the (northern hemisphere) summer of 2007. In turn, a new boom in external financing toward emerging economies unfolded since late 2009, about one year after the worst single shock experienced during the North Atlantic crisis—the collapse of Lehman Brothers in September 2008. This new boom was associated with strong “push factors,” particularly the low interest rate environment that has characterized advanced countries—including a growing share of assets yielding negative interest rates—but also the risks associated to investments in some high-income countries (the European periphery) or sectors (energy investments in recent years).

Other factors are, however, regional in character. The most important is the significant improvement in the external balance sheets of Latin American countries that took place during the first phase of the commodity boom, from 2004 to mid2008, which was associated with a massive reduction in the external debt net of foreign exchange reserves as a proportion of GDP—a very simple measure of such balance sheets.

As Figure 1 shows, it fell from around 30 percent in 2002–2003 to 6 percent in 2008. The counterpart in the balance of payments was a five-year period of current account surpluses (2003–2007), a very unusual outcome for a region that has been characterized by a history of current account deficits. Since 2008, the region returned to its traditional pattern of running current deficits and the improvement in the net external debt ceased, but the net external debt continued to be low as a proportion of GDP, even in recent years, when it again has experienced a small upward trend. This has been the main “pull factor” at work, as it has made the region a relatively safe destination for financial flows. Another feature that has contributed to risk reduction is exchange rate flexibility in most of the largest economies of the region, which reduces the lags in exchange rate adjustments that characterized all economies up until the crisis of East Asia in 1997, which then spread to the rest of the developing world (referred to below as the crisis of the late twentieth and early twenty-first centuries).

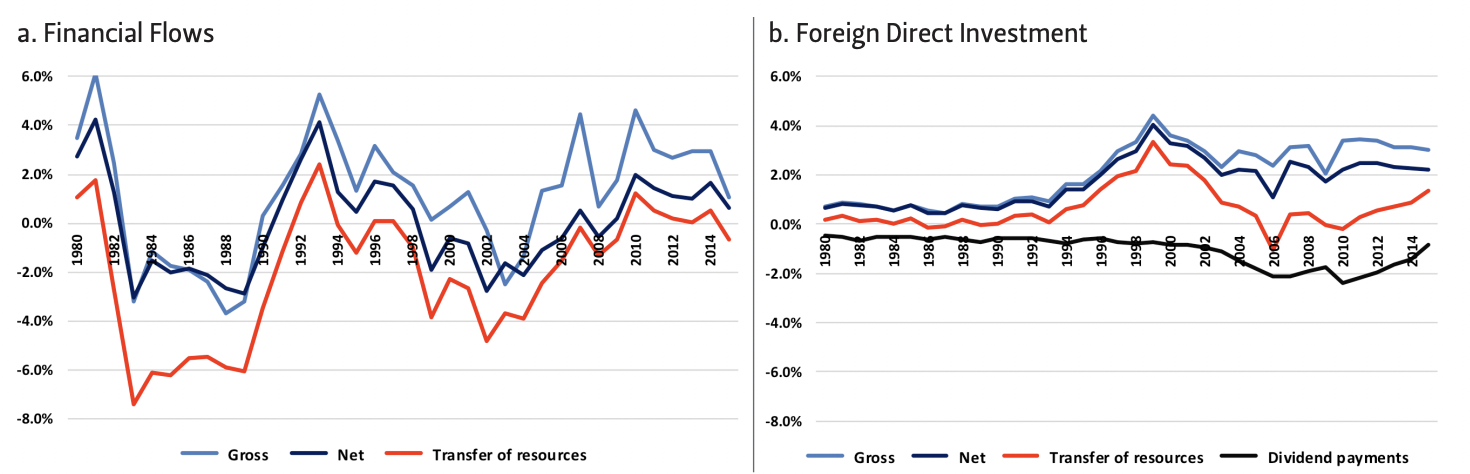

The main reflection of the joint effect of the “push” and “pull” factors has been the moderation of negative external shocks, as measured in particular by the net resource transfer through the capital account, which is the result of subtracting the debt service and FDI dividends from net capital flows. As Figure 2a shows, the large negative resource transfer through financial flows that characterized the intense and long external debt crisis of the 1980s was followed during the next crisis by a fairly long period of large negative financial resource flows after the outbreak of the East Asia crisis in 1997 and its spread to a broad group of emerging markets, including Argentina, Brazil, and other Latin American countries. However, this period of negative resource transfers was moderated in its early phase (1998– 2000) by the very high positive resource transfer through FDI (Figure 2b), but hit with full force in the early 2000s.

In contrast to these two long and intense periods of negative resource transfers, the effect of the North Atlantic financial crisis on external financing to Latin America was weak, leading to only short and very moderate negative net resource transfers through financial flows (2008 and 2009), which were not compensated by positive transfers through FDI. In turn, the recent crisis has been characterized so far by the persistence of positive resource transfers in 2014, 2015, and (most likely) 2016. There were negative transfers through financial flows in 2015, but again at very low levels by historical standards, and they were amply compensated by the large positive transfers through FDI. This is quite a remarkable feature in light of Latin America’s economic history.

External Financing to Latin America: A Detailed Look

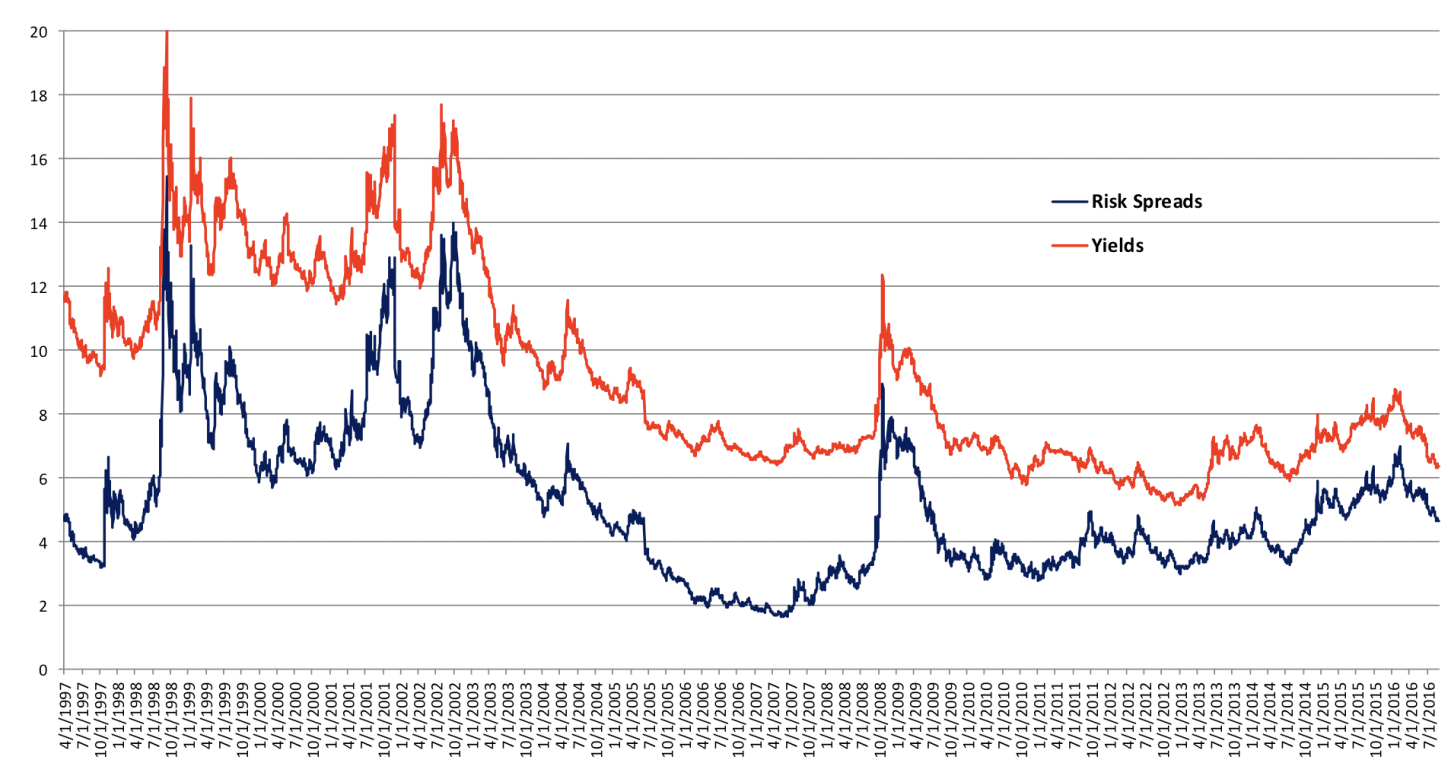

The reduced external vulnerability can be seen in four additional dimensions. The first is in the costs and access to international bond markets. The increased availability of external financing and the improvement in external balance sheets were behind the sharp reduction in risk spreads that took place from 2003 to 2007, which stopped as a result of the subprime crisis in the United States in the (northern hemisphere) summer of 2007, but only moderately so. The increase in risk spreads that occurred after the collapse of Lehman Brothers was sharp, but less intense than that which took place on several occasions between 1998 and 2002. Even more importantly, the time period of high spreads was very short— about one year, versus six years during the crisis of the late twentieth and early twenty-first centuries (Figure 3).

Figure 2 — Net Resource Transfers Through the Capital Account, 1980–2015 (% GDP)

After the North Atlantic crisis, Latin American risk spreads never returned to the very low levels of 2006–2007, but the costs of financing fell thanks to the low interest rate of 10-year US treasury bonds, which are used as a reference to estimate the risk spreads of Latin American bonds. Shocks affecting the cost of financing have continued, but their effects have been moderate and temporary. This is true of the Eurozone crisis of 2011–2012, which had very small effects on Latin America—and only when Italy and Spain risk spreads increased. Later shocks have had stronger effects, including: the May 2013 announcement by the US Federal Reserve that it would start to wind down its expansionary monetary policies; the collapse of commodity prices in the second semester of 2014 (the shock with stronger and more lasting effects); the volatility in Chinese stock markets in mid-2015 and the (small) devaluation of the Renminbi in August of that year; the downgrade of Brazilian sovereign debt to junk status by Standard & Poors in September 2015 and by other rating agencies soon afterward; and the broader turmoil in global capital markets in late 2015 and early 2016. However, the intensity of these shocks has been moderate relative to past patterns —including the North Atlantic crisis—and all have been partially or totally reversed soon after. This is, for example, what is reflected in the sharp reduction in risk spreads between March and August 2016.5

Figure 3 — Risk Spreads and Yields of Latin American Sovereign Bonds, 1997–2016

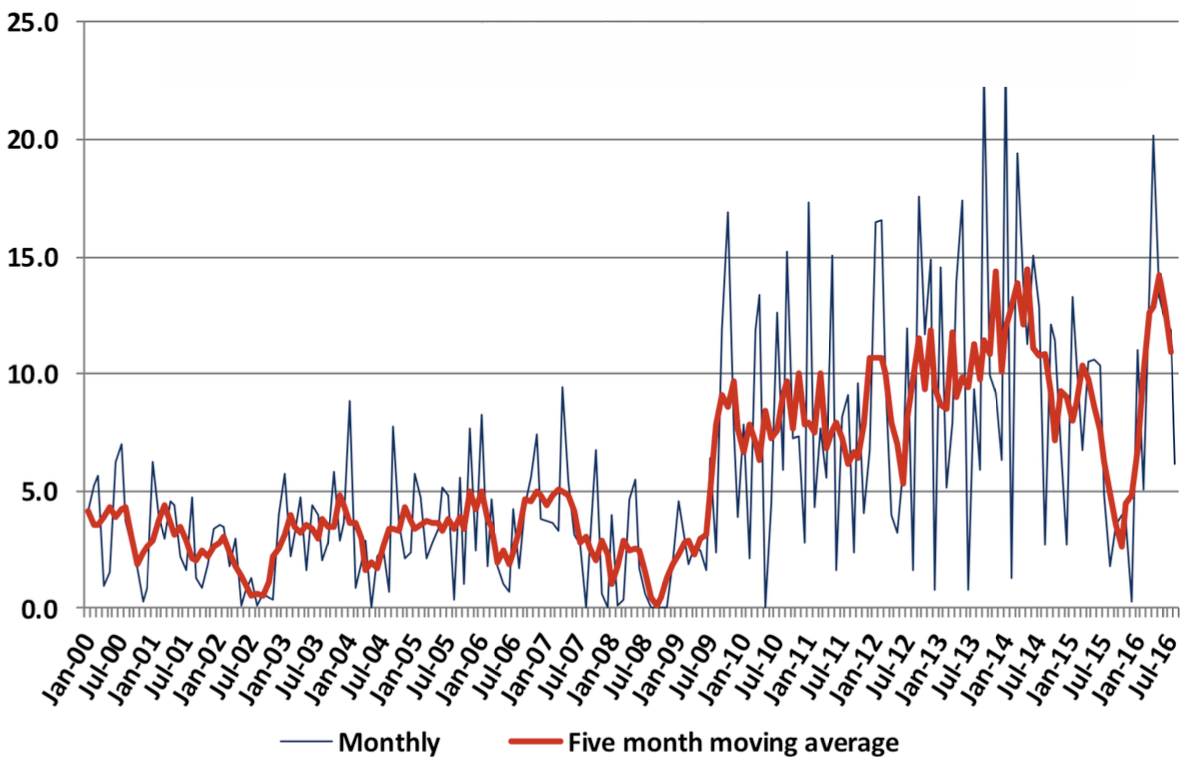

The evolution of access to bond markets tells a similar story. Indeed, in this case, there was a very intense boom after the North Atlantic crisis, reflecting the strong push and pull factors mentioned above. It started as the reduction in risk spreads in late 2009, about a year after the Lehman Brothers collapse, and more than duplicated the bond issuances that were typical before the North Atlantic crisis. Issuances reached a peak from mid-2013 to mid-2014 to levels that were 3.5 times the monthly levels of 2003–2007 (Figure 4). Reduced access was particularly strong during the period of global capital market volatility in the second semester of 2015 and early 2016, but even then there was no full interruption of access—i.e., no full “sudden stop.” Due to the later recovery, bond issuances between January and August 2016 reached levels that are comparable to the peaks achieved after the North Atlantic financial crisis and 36 percent higher than those reached in the same period of 2015 (12.3 percent higher if we exclude the large issue by Argentina in April 2016, to which I refer below). There are, of course, risks. They include the effective beginning of increases in US interest rates once the Federal Reserve decides to move in that direction, as well as possible additional downgrades in credit ratings.

What is equally remarkable is the fact that countries that did not have access to private capital markets have been able to issue bonds successfully in recent years. This is the case of Ecuador, which did so in 2014 and 2015 and simultaneously experienced a sharp reduction in risk spreads. In turn, Argentina returned to capital markets in April 2016 with a massive issuance of $16.5 billion, which was used to pay holdout investors with whom it successfully renegotiated its debt. Argentine risk spreads have also fallen sharply over the past two years. The city of Buenos Aires and several Argentinean provinces and firms had already accessed the market since March. Brazil, which has been negatively affected by domestic political events and by the downgrade in its ratings, was also able to access international capital markets in March and July 2016; so did Petrobras in May and July, as well as other Brazilian firms. It can even be argued that Venezuela would access the market if a sensible macroeconomic policy was put in place.

An additional factor that has contributed to reduced financial volatility is the importance of FDI as a source of financing since the mid-1990s (see again Figure 2b). As already indicated, the massive resource transfers generated by this initial boom in FDI helped significantly moderate the procyclical outflows of financial capital during the crisis of the late twentieth and early twenty-first centuries. The extraordinary levels of these transfers disappeared during the 2004–2008 boom, due both to the dividend remittances by foreign investors (some of which are reinvested and therefore included as new inflows of FDI) and the investments by Latin American multinationals (multilatinas) abroad. Both effects, but particularly the first one, have had a stabilizing effect on net resource transfers during the recent crisis. The basic reasons are foreign investors’ falling profits in the oil and mining sectors, after peaking in 2010, and the reduced dollar value of profits in non-tradable goods and services sectors generated by the depreciation of currencies in several countries.

A third factor is, interestingly, the greater freedom of Latin Americans to move their capital abroad as well as the aforementioned investment by multilatinas, which has also contributed to the moderation of the cycle of net capital flows. A simple explanation is that these capital outflows are also procyclical. Financial outflows were particularly intense in 2005–2007 and 2010–2013. They therefore helped moderate the two most recent inflow booms, but also help moderate the two most recent downswings of capital inflows, including the current one (see again Figure 2a).

Figure 4 — Monthly Latin American Bond Issuance, 2000–2016 (Billions of Dollars)

The final factor contributing to positive resource transfers during the current crisis is Chinese financing. It started before the North Atlantic crisis but has boomed since 2009, and actually increased in 2015, in contrast with trends in private capital flows (Gallagher et al. 2012; Myers et al. 2016). Furthermore, an interesting feature of this source is that flows have been destined to countries with more limited access to external private financing (Venezuela, Ecuador, Argentina up until 2015, and Brazil since 2015). In any case, Chinese financing also has benefitted other countries, and three general funds for Latin American countries were approved in 2015, totaling $35 billion. These resources mainly have been used to finance the energy and infrastructure sectors, and are tied to the use of Chinese inputs and, in some cases, Chinese labor in the recipient countries, an issue that has led to strong resistance in the region.

Conclusion

The major conclusion from this brief is that, in contrast to the pessimism that has been generated by the collapse of commodity prices, particularly in South America, there are reasons for optimism in the area of external financing. In fact, as emphasized in this brief, we may be in the midst of the first crisis in Latin American history in which resource transfers through the capital account would continue to be positive—a remarkable historical fact! The closure of financial markets has been weak and temporary, FDI continues to make positive resource transfers, and China is providing additional resources. This will be complemented by the countercyclical financing of multilateral development banks, including the World Bank, the Inter-American Development Bank, the Development Bank of Latin America (CAF), and the Central American Integration Bank (CABEI); however, this issue is not discussed in this brief.

Endnotes

1. See, among many contributions, IMF (2011).

2. This term was coined by Rudiger Dornbusch in a paper on the 1994 Mexican crisis (Dornbusch and Werner 1994), in which he argued that “it is not speed that kills, it is the sudden stop.” The concept’s popularization owes equally to the work of Guillermo Calvo (see Calvo 1998, and Calvo et al. 2004).

3. See, in this regard, the regular analyses by international institutions of Latin American macroeconomic developments (ECLAC 2016a; IMF 2016), as well as Ocampo (2015).

4. I follow some other authors in using this term, rather than that of global financial crisis, because the crisis had global effects but its epicenters were in the United States and Western Europe.

5. For a regular analysis of trends in Latin America’s access to bond markets, see the periodic reports of the Washington office of the Economic Commission for Latin American and the Caribbean (most recently, ECLAC 2016b). See also the excellent historical account of Latin American access to bond markets since the 1980s in Bustillo and Velloso (2013).

References

Bustillo, Inés and Helvia Velloso. 2013. Debt Financing Rollercoaster: Latin America and Caribbean access to International Bond Markets since the debt Crisis, 1982-2012, Libros de la CEPAL No. 119. Santiago: ECLAC.

Calvo, Guillermo A. 1998. “Capital Flows and Capital-Market Crises: The Simple Economics of Sudden Stops.” Journal of Applied Economics 1(1): 35–54.

Calvo, Guillermo A., Alejandro Izquierdo, and Luis-Fernando Mejía. 2004. “On the Empirics of Sudden Stops: the Relevance of Balance-Sheet Effects.” NBER Working Paper No. 10520.

Dornbusch, Rüdiger and Alejandro Werner. 1994. “Mexico: Stabilization, Reform and No Growth,” Brookings Papers on Economic Activity 1:253–316.

Economic Commission for Latin America and the Caribbean. 2016a. Estudio económico de América Latina y el Caribe 2016. Santiago: ECLAC.

ECLAC. 2016b. “Capital Flows to Latin America and the Caribbean: Q1 2016.” Washington, D.C.: ECLAC.

Gallagher, Kevin P., Amos Irwin, and Katherine Koleski. 2012. The New Banks in Town: Chinese Finance in Latin America, Washington, D.C.: InterAmerican Dialogue.

International Monetary Fund. 2011. World Economic Outlook, Washington, D.C.: International Monetary Fund.

IMF. 2016. World Economic and Financial Surveys, Regional Economic Outlook, Western Hemisphere: Managing Transitions and Risks. Washington, D.C.: IMF.

Myers, Barbara, Kevin P. Gallagher, and Fei Yuan. 2016. Chinese Finance to Latin America in 2015: Doubling Down. Washington: Inter-American Dialogue.

Ocampo, José Antonio. 2015. “Latin America’s Recent Economic Turmoil.” Issue brief no. 10.13.15, Rice University’s Baker Institute for Public Policy, Houston, TX. Available at: http://bakerinstitute.org/research/economic-turmoil-latin-america/.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.