By Shao-Chee Sim, Elena Marks, Vivian Ho and Philomene Balihe

In September 2015, just before the third open enrollment period of the Affordable Care Act’s (ACA) Health Insurance Marketplace was about to open, we surveyed insured Texans ages 18 to 64 to assess their confidence level in understanding the basic terminology about health insurance plans and in how they use their health insurance plans. Our data show that, as compared to Texans with employer-sponsored insurance (ESI) and those with public health insurance, Texans with individual plans were more likely to lack confidence in understanding health insurance terminology. Texans with individual plans also expressed more difficulty in understanding how to use their health insurance plans.

About the Survey

The Health Reform Monitoring Survey (HRMS) is a quarterly survey of adults ages 18-64 that began in 2013. It is designed to provide timely information on implementation issues under the ACA and to document changes in health insurance coverage and related health outcomes. HRMS provides quarterly data on health insurance coverage, access, use of health care, health care affordability, and self-reported health status. The HRMS was developed by the Urban Institute, conducted by GfK, and jointly funded by the Robert Wood Johnson Foundation, the Ford Foundation, and the Urban Institute. Rice University’s Baker Institute and The Episcopal Health Foundation are partnering to fund and report on key factors about Texans obtained from an expanded, representative sample of Texas residents (HRMS-Texas). The analyses and conclusions based on HRMS-Texas are those of the authors and do not represent the view of the Urban Institute, the Robert Wood Johnson Foundation or the Ford Foundation. Information about the sample demographics of the cohort is available in Issue Brief #1. This Issue Brief is a summary of data extracted from the HRMS Surveys in Texas administered between September 2013 and September 2015. We will continue to report on survey data through additional Issue Briefs and future surveys.

Texans With Individual Health Plans Were Most Likely to Lack Confidence in Understanding Health Plan Terminology

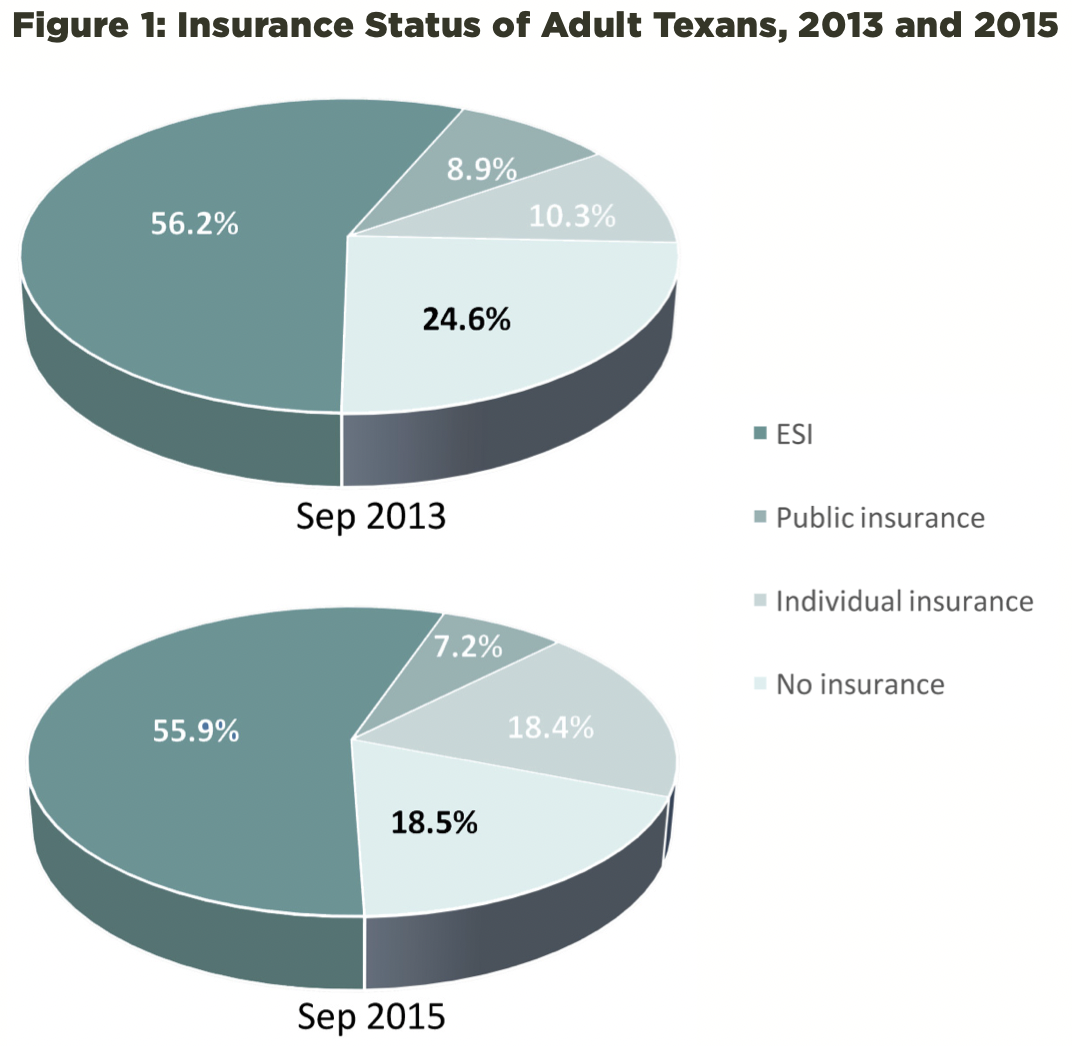

One of the main goals of the Affordable Care Act (ACA) was to enable more Americans to obtain health insurance coverage. Since the opening of the Health Insurance Marketplace and the expansion of Medicaid in many states in January 2014, millions of Americans have obtained health insurance. As we reported in Issue Brief #16, from 2013 to 2015, the rate of uninsured adults ages 18-64 dropped by 41% across the country and by 21.4% in Texas. As shown in Figure 1 below, the significant drop in the percentage of uninsured Texans is primarily attributable to a 78% increase in the percent of Texans covered by individually purchased plans, including the nearly one million who had purchased Marketplace plans by the end of 2015.

Figure 1 — Insurance Status of Adult Texans, 2013 and 2015

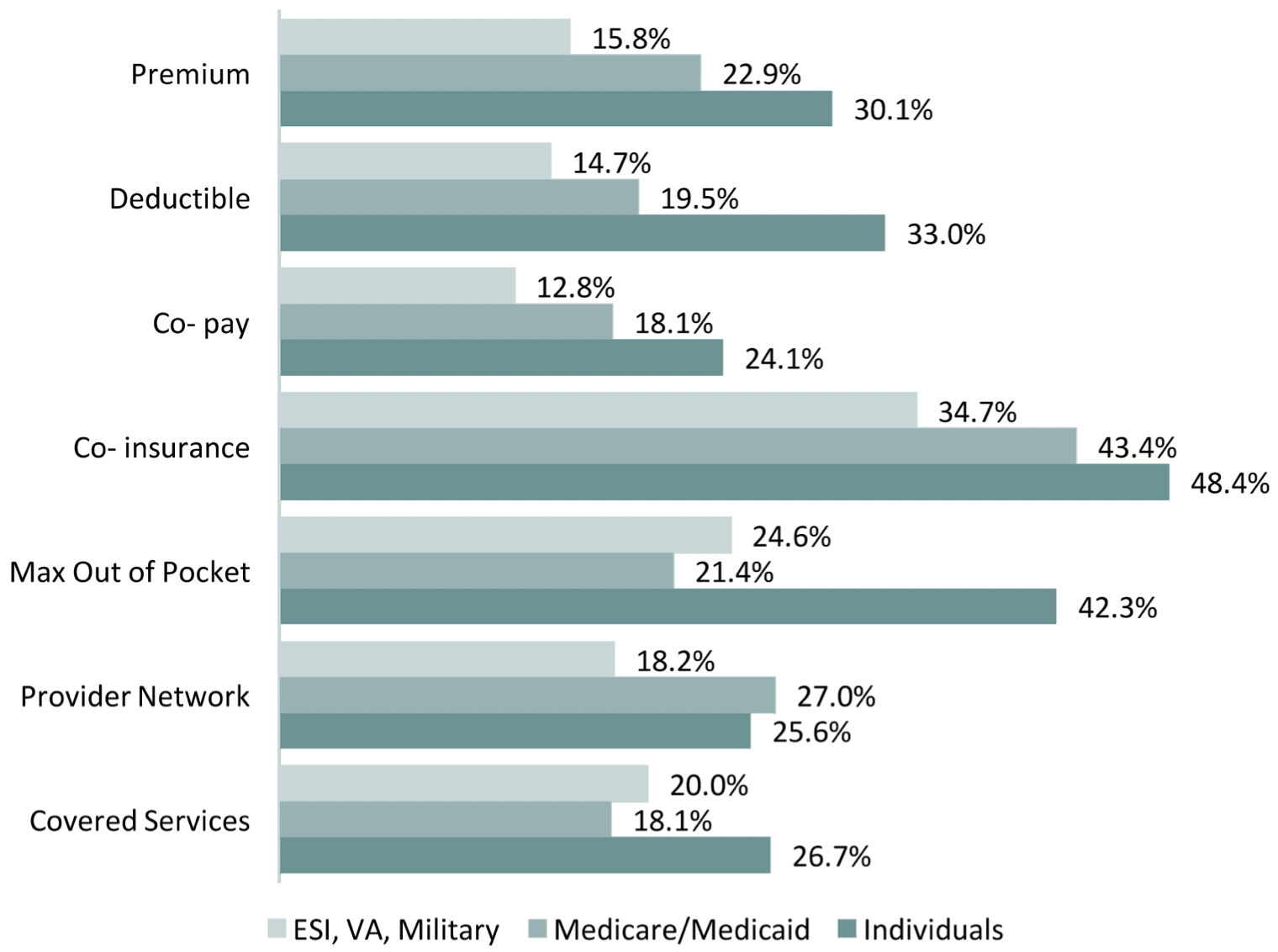

As we reported in Issue Brief #19, approximately 25% of insured Texans stated that they lacked confidence in their understanding of basic health plan terminology. When we stratified the data according to the type or source of insurance, we learned that those who had purchased individual plans were much less confident about their understanding of the terms of those plans, as compared to those with public insurance (primarily Medicaid and Medicare) or employer-sponsored insurance (including military and public sector employees). Specifically, about 4 in 10 Texans with individual plans expressed lack of confidence in understanding “co-insurance” and “maximum out of pocket expenses.”

Chart 1 — Lack of Confidence* in Understanding Health Insurance Terms Among Insured Texans Ages 18-64 by Coverage Type, September 2015

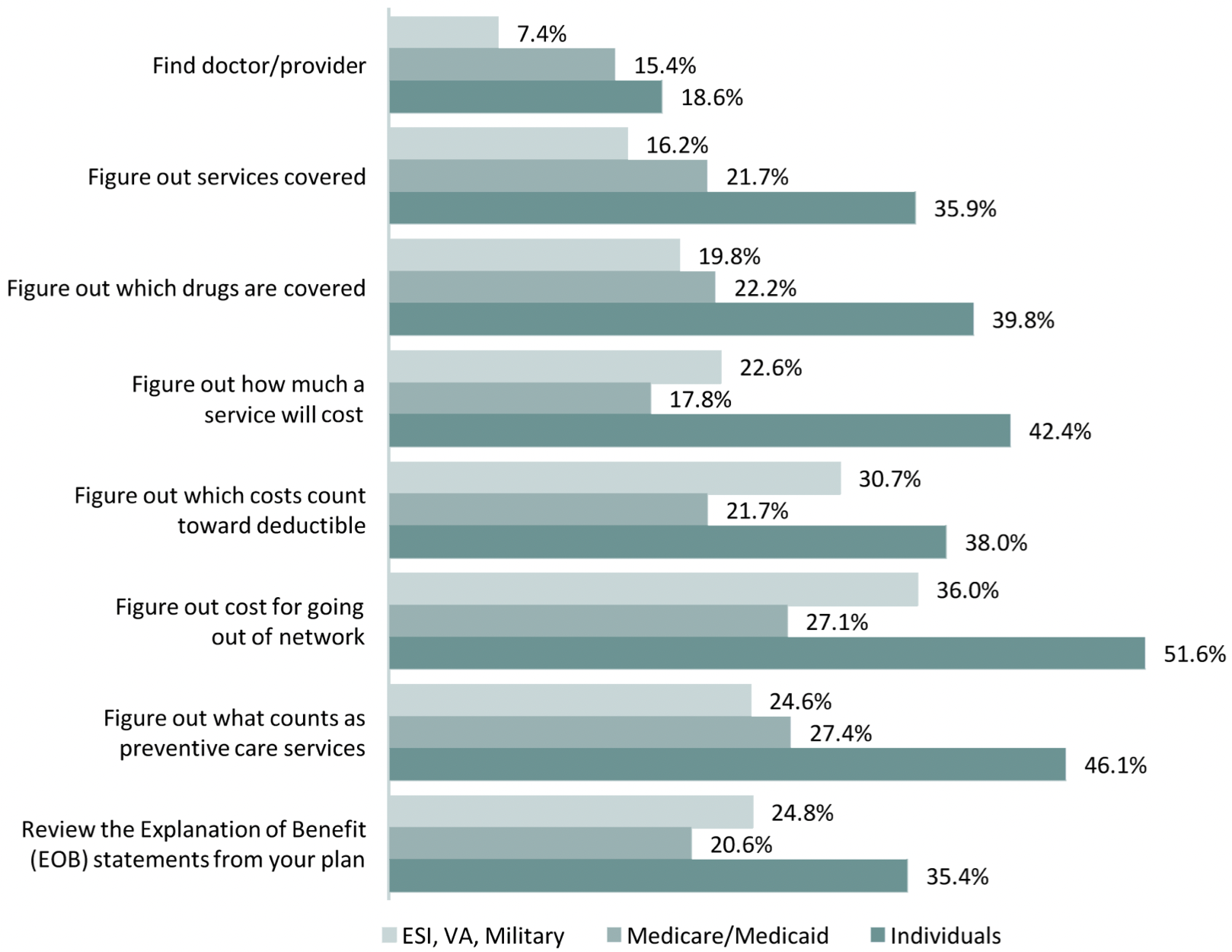

As shown in Chart 2 below, Texans with individual plans also expressed more difficulty in understanding how to use their health plans. While most with individual plans were confident of their ability to find providers, more than one-third of the respondents were not confident that they could figure out what services (36%) or drugs (40%) were covered by their plans. Nearly half (46%) did not understand what counts as preventive services, many of which are provided at no additional cost. Large percentages of respondents reported that they lacked confidence in understanding the actual cost of covered services (42%), which costs count toward the deductible (38%), and how much it would cost to go out of network (51%).

Chart 2 — Lack of Confidence* in Using Health Insurance Among Insured Texans, by Coverage Type, September 2015

The unfortunate irony is that those with individual plans are the least likely to understand plan terminology and how to use their plans but, they are in fact the very ones who are in greatest need of understanding. People with public or employer-sponsored plans have comparatively few choices to make regarding which plan they have. Public plans like Medicaid and Medicare generally have standardized plans with limited opportunities for beneficiaries to make decisions about their coverage. Most employer-sponsored insurance programs offer participants only one or two plan options. In addition to having a broader set of options from which to choose, those purchasing an insurance plan in the individual market, unless heavily subsidized through the Marketplace, bear all of the costs of their plans, while those covered by public and employer plans generally pay a comparatively small share of the costs. Therefore, their need to understand what they are buying is critical.

Conclusions

The long-term success of the ACA depends on people buying, using, and experiencing satisfaction with health insurance. The lack of understanding about the basic financial and coverage provisions of health plans expressed by so many insured can lead to surprise, frustration, and disillusionment, which can undermine efforts to increase coverage. Our national conversation about health insurance—its costs and benefits—has largely taken place among industry, government, and policy experts until relatively recently. This research highlights the importance of health insurance literacy from the healthcare consumer perspective. It will be important for all Americans to gain a basic understanding of this complex system in order for them to participate fully and make the best decisions about health insurance and healthcare choices for themselves and their families. Those who have worked diligently to expand enrollment in health coverage must help the newly insured understand their plans.

Looking Ahead

Later this Spring, we will report on data collected in the March 2016 HRMS survey. Those briefs will include information about the 2016 status and recent experiences of Texans in accessing and using health care and health insurance.

Methodology

Each quarter’s HRMS sample of nonelderly adults is drawn from active KnowledgePanel® members to be representative of the US population. In the first quarter of 2013, the HRMS provided an analysis sample of about 3,000 nonelderly (age 18–64) adults. After that, the HRMS sample was expanded to provide analysis samples of roughly 7,500 nonelderly adults, with oversamples added to better track low-income adults and adults in selected state groups based on (1) the potential for gains in insurance coverage in the state under the ACA (as estimated by the Urban Institute’s microsimulation model) and (2) states of specific interest to the HRMS funders.

Although fresh samples are drawn each quarter, the same individuals may be selected for different rounds of the survey. Because each panel member has a unique identifier, it is possible to control for the overlap in samples across quarters. For surveys based on Internet panels, the overall response rate incorporates the survey completion rate as well as the rates of panel recruitment and panel participation over time. The American Association for Public Opinion Research (AAPOR) cumulative response rate for the HRMS is the product of the panel household recruitment rate, the panel household profile rate, and the HRMS completion rate—roughly 5 percent each quarter.

While low, this response rate does not necessarily imply inaccurate estimates; a survey with a low response rate can still be representative of the sample population, although the risk of nonresponse bias is, of course, higher.

All tabulations from the HRMS are based on weighted estimates. The HRMS weights reflect the probability of sample selection from the KnowledgePanel® and post-stratification to the characteristics of nonelderly adults and children in the United States based on benchmarks from the Current Population Survey and the Pew Hispanic Center Survey. Because the KnowledgePanel® collects in-depth information on panel members, the post-stratification weights can be based on a rich set of measures, including gender, age, race/ethnicity, education, household income, homeownership, Internet access, primary language (English/Spanish), residence in a metropolitan area, and region. Given the many potential sources of bias in survey data in general, and in data from Internet-based surveys in particular, the survey weights for the HRMS likely reduce, but do not eliminate, potential biases.

The design effect for the Texas data in September 2015 is 2.243 and the MOE is +/- 3.7. The survey fielded from September 1-25.