In this brief, we examine the changes in the rates of uninsurance among Texans ages 18-64 from September 2013, before the opening of the first open enrollment period of the Affordable Care Act’s (ACA) Health Insurance Marketplace, and March 2016, after the close of the third open enrollment period. We also examine the demographic characteristics of the uninsured and the changes in rates of uninsurance among various demographic groups. The data show that from 2013 to 2016, the rate of uninsured Texans ages 18-64 dropped by nearly one-third (30% decrease). Of ten demographic sub-groups examined, all showed decreases in rates of uninsurance, ranging from 15% to 51%. The steepest percentage decreases were experienced by Texans ages 50-64 (51% decrease) and Texans with incomes between 139% and 399% of the federal poverty level (42% decrease). The largest percentage point decreases were experienced by Hispanics (11.9 percentage points) and Texans ages 50-64 (10.8 percentage points). We conclude that the ACA has contributed significantly to reducing the rate of uninsured Texans ages 18-64.

About the Survey

The Health Reform Monitoring Survey (HRMS) is a quarterly survey of adults ages 18-64 that began in 2013. It is designed to provide timely information on implementation issues under the ACA and to document changes in health insurance coverage and related health outcomes. HRMS provides quarterly data on health insurance coverage, access, use of health care, health care affordability, and self-reported health status. The HRMS was developed by the Urban Institute, conducted by GfK, and jointly funded by the Robert Wood Johnson Foundation, the Ford Foundation, and the Urban Institute. Rice University’s Baker Institute and The Episcopal Health Foundation are partnering to fund and report on key factors about Texans obtained from an expanded, representative sample of Texas residents (HRMS-Texas). The analyses and conclusions based on HRMS-Texas are those of the authors and do not represent the view of the Urban Institute, the Robert Wood Johnson Foundation or the Ford Foundation. Information about the sample demographics of the cohort is available in Issue Brief #1. This Issue Brief is a summary of data extracted from the HRMS Surveys in Texas administered between September 2013 and March 2016. We will continue to report on survey data through additional Issue Briefs and future surveys.

Changes in Rates and Characteristics of the Uninsured

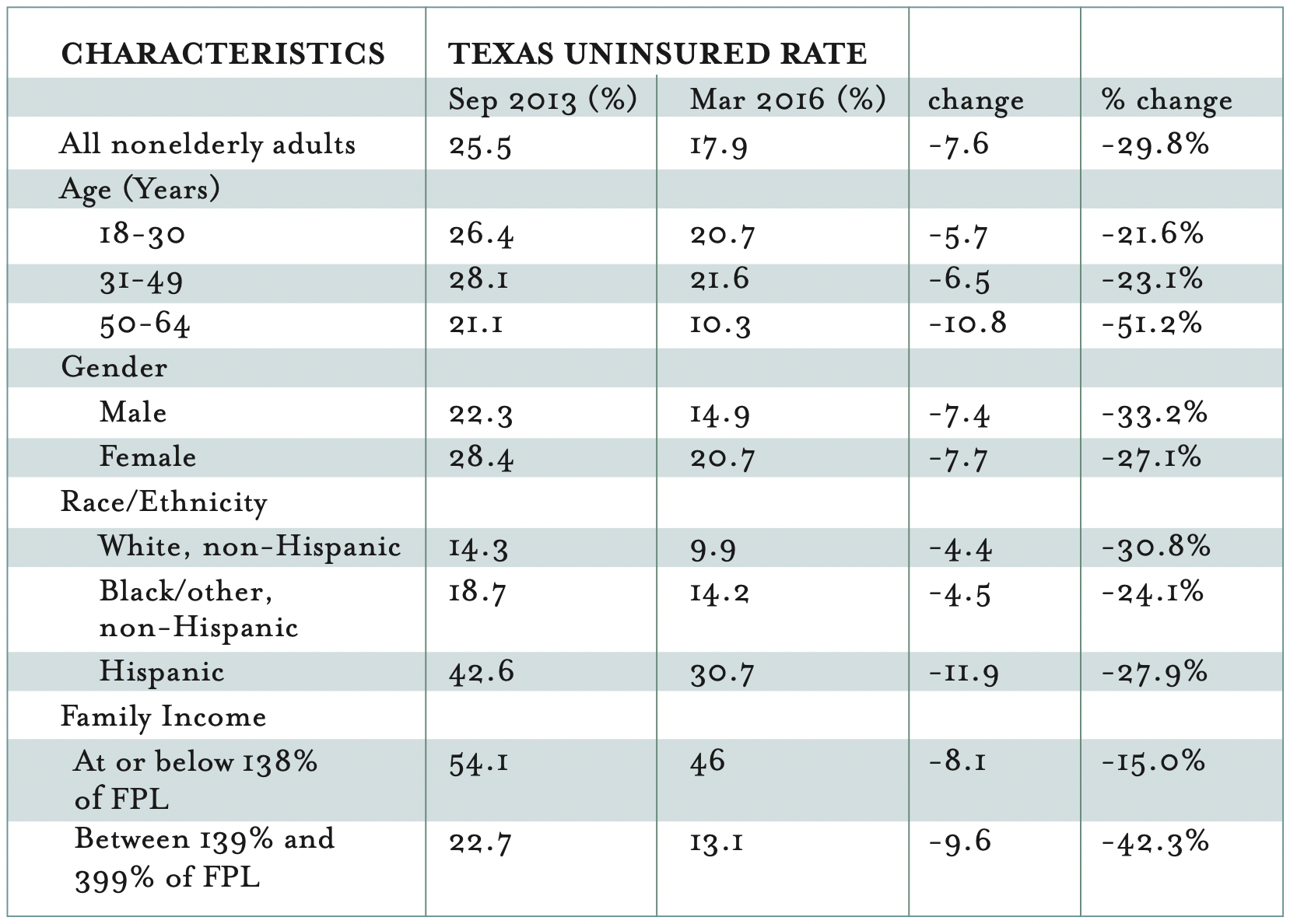

Table 1 below shows the rates of uninsured Texans ages 18-64 as a whole and among ten demographic sub-groups as reported in response to the HRMS-Texas surveys taken in September 2013 and March 2016. Previous HRMS issue briefs have chronicled the steady decline in the rate of uninsured Texans ages 18-64 from 2013 through 2015. As of March 2016, our survey shows that the rate of uninsured Texans ages 18-64 was 17.9%, down seven percentage points since September 2013. Our findings are consistent with recent trend data reported by the US Centers for Disease Control and Prevention showing a decrease of 5.9 percentage points from 2013 to 2015 for this group of Texans (See Table XVII at page A22).

Table 1 — Uninsured Rates by Group, Texas Adults 18–64

As a group, Texans ages 18-64 experienced a 30% decrease in the rate of uninsurance, from 25.5% in September 2013 to 17.9% in March 2016. While gains varied among the ten demographic sub-groups we examined, all groups experienced improvements, ranging from 15% to 51%. Older Texans, ages 50-64, experienced the greatest reduction in the rate of uninsurance (51%) followed by those with incomes between 139% and 399% of the federal poverty level (42%). The 30% overall reduction and the even larger reductions for older and low-to-moderate income Texans are most likely attributable to the implementation of the Affordable Care Act.

For the older group (ages 50-64), the ACA made health insurance more affordable by prescribing premium rate bands. The premium rate bands limit the variability in premiums based on age, so that older adults could no longer be charged more than triple the cost for the same plans as younger adults. Because of the premium rate bands, many Texans ages 18-64 could afford health coverage that was previously out of reach.1

For those in the low-to-moderate income group (139% to 399% of the federal poverty level), the ACA’s Marketplace provided premium subsidies which made coverage affordable for many who could not have purchased plans without this assistance. In addition to premium subsidies, for those with incomes between 133% and 250% of the federal poverty level, additional cost-sharing benefits were available. The popularity of the Marketplace plans among Texans is readily apparent—1.3 million Texans had enrolled in these plans as of early 2016. Of those, 84% received premium subsidies and 57% of those received additional cost-sharing benefits.

Among different income groups, those with incomes between 139% and 399% of the federal poverty level experienced a 42.3% decline in the rate of uninsurance and now have an uninsured rate of only 13.1%, well below the overall rate for 18-64 year olds. This is likely attributable to the ACA’s health insurance marketplace which offered premium subsidies and cost-sharing benefits for individuals in this income.

For the lowest income Texans whose uninsurance rate remains stubbornly high at 46%, the ACA, as implemented in Texas, offers little hope. This group of Texans earns too much to qualify for traditional Medicaid (which only covers parents with annual incomes up to $3,000 and does not cover non-disabled childless adults at all) but not enough to qualify for ACA Marketplace subsidies. The ACA’s plan for covering this group of Americans was through Medicaid expansion. Because Texas opted not to expand Medicaid, this population, estimated by the Kaiser Family Foundation to include 766,000 Texans, most of whom are people of color in working families, is in a “coverage gap” without access to affordable individual insurance coverage. Unless Texas expands Medicaid or devises an alternative system of coverage for this population, they will remain uninsured.

We have watched the data closely to see the changes in uninsurance rates among Hispanics. Because this group had the highest rates of uninsurance in 2013 (43%) among all racial/ethnic groups and they are the fastest growing group in the state, the ability of Hispanics to acquire health coverage is critically important to the state as a whole. The March 2016 HRMS-Texas survey shows significant progress for Hispanics. From 2013 to March 2016, Hispanics made the largest percentage point gains in coverage: the rate of uninsured Hispanics dropped by 11.9 percentage points, nearly triple the reduction experienced by Whites (4.4 percentage points) and Blacks (4.5 percentage points). The decline in the rate of uninsured Hispanics (28%) is comparable to the decline experienced by Whites (31%) and greater than that experienced by Blacks (24%). We see the March 2016 data as good news, not only for the reductions in uninsurance rates among Hispanics but also because the gap between Hispanics and other groups is narrowing, reducing the disparities among groups. Despite these gains, we should note that, as of March 2016, the uninsured rate among Hispanics is still at 31%, which is more than double the uninsured rate of Blacks (14%) and triple the uninsured rate of Whites (10%). We will continue to follow the progress of this important demographic group.

Conclusions

The March 2016 HRMS-Texas data shows the continuing downward trend in rates of uninsured Texans that began as the ACA was implemented. For more than a decade prior to the implementation of the ACA, the uninsured rate in Texas remained above 20%, growing to 25% in 2010. Now the uninsured rate is below 1999 levels. Because of the ACA, young adults are able to remain on their parents’ health plans until age 26; those with pre-existing conditions can no longer be denied coverage; subsidies and cost-sharing benefits enable low-to-moderate income families the ability to afford coverage; and large employers are providing health benefits to their employees. However, two key demographic groups, the lowest income Texans and Hispanic Texans, continue to show stubbornly high uninsured rates (46% and 31%, respectively) even with the implementation of the ACA. While we have a long way to go in Texas, including devising a plan for those in the “coverage gap,” this is tremendous progress and the ACA deserves the credit.

Looking Ahead

We will continue to analyze and report on the 2016 data to understand the characteristics and experiences of newly insured Texans and those who remain uninsured.

Methodology

Each quarter’s HRMS sample of nonelderly adults is drawn from active KnowledgePanel® members to be representative of the US population. In the first quarter of 2013, the HRMS provided an analysis sample of about 3,000 nonelderly (age 18–64) adults. After that, the HRMS sample was expanded to provide analysis samples of roughly 7,500 nonelderly adults, with oversamples added to better track low-income adults and adults in selected state groups based on (1) the potential for gains in insurance coverage in the state under the ACA (as estimated by the Urban Institute’s microsimulation model) and (2) states of specific interest to the HRMS funders.

Although fresh samples are drawn each quarter, the same individuals may be selected for different rounds of the survey. Because each panel member has a unique identifier, it is possible to control for the overlap in samples across quarters.

For surveys based on Internet panels, the overall response rate incorporates the survey completion rate as well as the rates of panel recruitment and panel participation over time. The American Association for Public Opinion Research (AAPOR) cumulative response rate for the HRMS is the product of the panel household recruitment rate, the panel household profile rate, and the HRMS completion rate—roughly 5 percent each quarter.

While low, this response rate does not necessarily imply inaccurate estimates; a survey with a low response rate can still be representative of the sample population, although the risk of nonresponse bias is, of course, higher.

All tabulations from the HRMS are based on weighted estimates. The HRMS weights reflect the probability of sample selection from the KnowledgePanel® and post-stratification to the characteristics of nonelderly adults and children in the United States based on benchmarks from the Current Population Survey and the Pew Hispanic Center Survey. Because the KnowledgePanel® collects in-depth information on panel members, the post-stratification weights can be based on a rich set of measures, including gender, age, race/ethnicity, education, household income, homeownership, Internet access, primary language (English/Spanish), residence in a metropolitan area, and region. Given the many potential sources of bias in survey data in general, and in data from Internet-based surveys in particular, the survey weights for the HRMS likely reduce, but do not eliminate, potential biases.

The design effect for the Texas data in March 2016 is 2.7005 and the MOE is +/- 4.1% at the 95% CI. The survey fielded from March 1-22, 2016.

Endnote

1. The ACA’s elimination of health plans’ ability to exclude applicants with preexisting health conditions also enabled more adults of all ages to enter insurance markets from which they were previously barred.