A central goal of the Affordable Care Act (ACA) is to provide access to affordable health insurance coverage for millions of Americans. The inclusion in the insurance markets of young adults, who are generally healthier than older adults, helps the system as a whole by offsetting the costs of health services used by the older and less healthy populations.

In this brief, we examine the health insurance experiences of Texans ages 18 to 34, the so-called “Young Invincibles,” between 2013 and 2016. The Young Invincibles term was coined by the health insurance industry to describe young people who were expected to forego health insurance based on the belief they were too healthy to warrant the cost. Prior to the implementation of the ACA, the Young Invincibles were less likely to be insured than their older counterparts.

Our data show that the uptake of health insurance by Young Invincibles has increased significantly from 2013 to 2016. The uninsured rate for this group has fallen by more than one-third, from 32.7% to 21.3%. The increase is significantly attributable to the Young Invincibles’ coverage through employer-sponsored insurance plans (21% increase). The largest sub-groups of Young Invincibles who remain uninsured are Hispanic and low income.

About the Survey

The Health Reform Monitoring Survey (HRMS) is a quarterly survey of adults ages 18-64 that began in 2013. It is designed to provide timely information on implementation issues under the ACA and to document changes in health insurance coverage and related health outcomes. HRMS provides quarterly data on health insurance coverage, access, use of health care, health care affordability, and self-reported health status. The HRMS was developed by the Urban Institute, conducted by GfK, and jointly funded by the Robert Wood Johnson Foundation, the Ford Foundation, and the Urban Institute. Rice University’s Baker Institute and The Episcopal Health Foundation are partnering to fund and report on key factors about Texans obtained from an expanded, representative sample of Texas residents (HRMS-Texas). The analyses and conclusions based on HRMS-Texas are those of the authors and do not represent the view of the Urban Institute, the Robert Wood Johnson Foundation or the Ford Foundation. Information about the sample demographics of the cohort is available in Issue Brief #1. This Issue Brief is a summary of data extracted from the HRMS Surveys in Texas administered between September 2013 and March 2016. We will continue to report on survey data through additional Issue Briefs and future surveys.

Changes in the Rates of Uninsurance Among Young Invincibles

Historically, younger adults have had lower rates of health insurance coverage than their older counterparts. The ACA offered four mechanisms to encourage the coverage of more young adults: (1) allowing those up to age 26 to be covered through their parents’ individual and employer-sponsored health insurance plans; (2) providing income-based tax subsidies to support the purchase of individual health plans through the ACA Marketplace; (3) mandating that large employers offer affordable coverage to their employees; and (4) expanding Medicaid to cover low income childless adults, a population that often includes young adults. We have been tracking the health insurance status of Texas’ Young Invincibles since 2013, prior to the opening of the Marketplace and the implementation of the large employer mandate, to identify and understand changes in coverage levels. Our data show that the health insurance status of Texas’ Young Invincibles has changed substantially for the better since 2013.

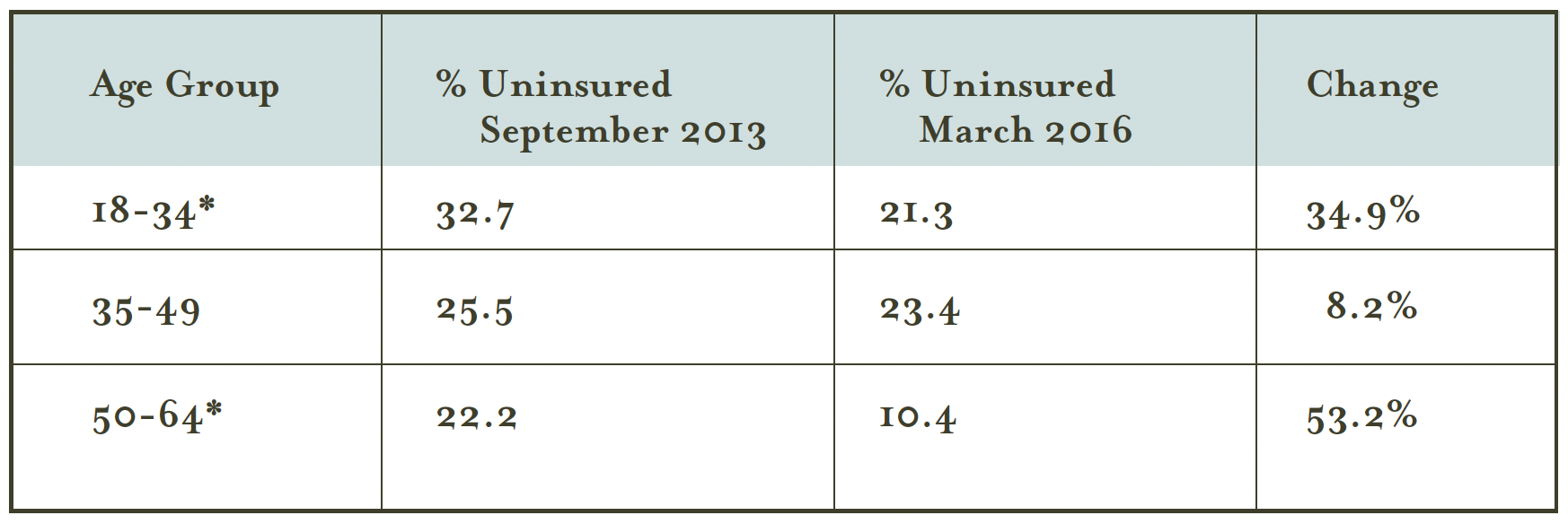

As Table 1 shows, all non-elderly Texas adults achieved reductions in their rates of uninsurance between September 2013 and March 2016. The uninsured rate for Texas’ Young Invincibles fell 11.4 percentage points, from 32.7% to 21.3%, a 34.9% drop. As of March 2016 the Young Invincibles had a lower rate of uninsurance than their middle-aged counterparts. Not surprisingly, the oldest group, those ages 50-64, made the greatest gains and remain the group with the lowest uninsurance rate.

Table 1 — Changes in Uninsured Rate by Age Group, September 2013 to March 2016

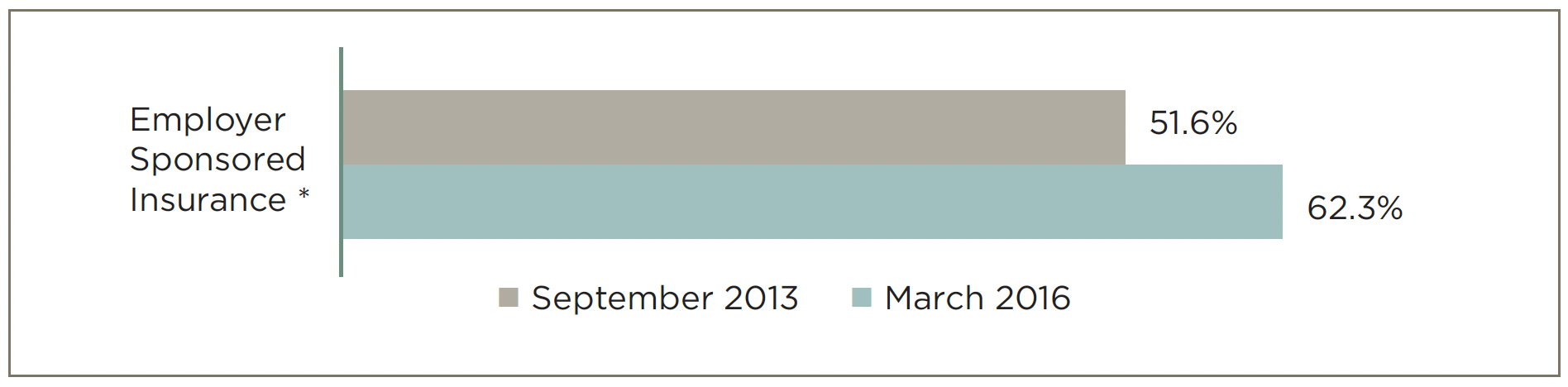

We further examined the data to see if we could understand why and how the improvement in coverage occurred. For those Young Invincibles who are insured, we examined their sources of insurance in 2013 and 2016. While the raw data showed an increase in coverage through the Marketplace and a decrease in coverage through public plans such as Medicaid, these changes were not statistically significant, so they are not reported in this issue brief. Figure 1 below shows the large and statistically significant increase in coverage through employer-sponsored insurance plans. This is likely attributable to a combination of factors including a strong Texas economy through 2015 leading to overall increases in employment, the January 2016 implementation date for the ACA provision requiring large employers to make affordable coverage available to employees, and the ability of those up to age 26 to remain on their parents’ employer-sponsored plans. Because Texans in older age groups also benefited from the first two factors, the ability of many Young Invincibles to remain on their parents’ plans likely explains the substantial decrease in uninsurance.

Figure 1 — Change in Employer Sponsored Insurance Coverage, Young Invincibles, September 2013 and March 2016

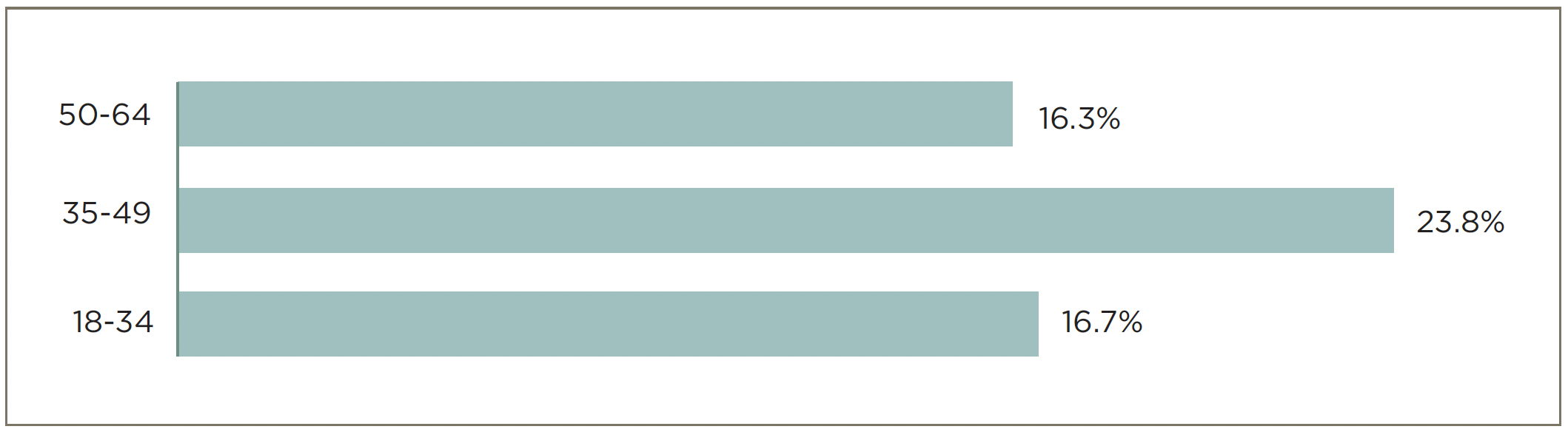

Health insurance coverage is important because it helps provide affordable access to health services. To determine whether the Young Invincibles found health services affordable, we asked survey respondents whether they or anyone in their family had problems paying or were unable to pay any medical bills in the past 12 months. As Figure 2 shows, among the Young Invincibles as well as the oldest group, fewer than 17% reported having trouble paying medical bills. The higher rate reported by the middle-aged group may reflect the fact that they have the highest rates of uninsurance in 2016 among the three groups.

Figure 2 — Affordability of Health Services in Texas, All Age Groups, March 2016

Characteristics of Uninsured Young Invincibles

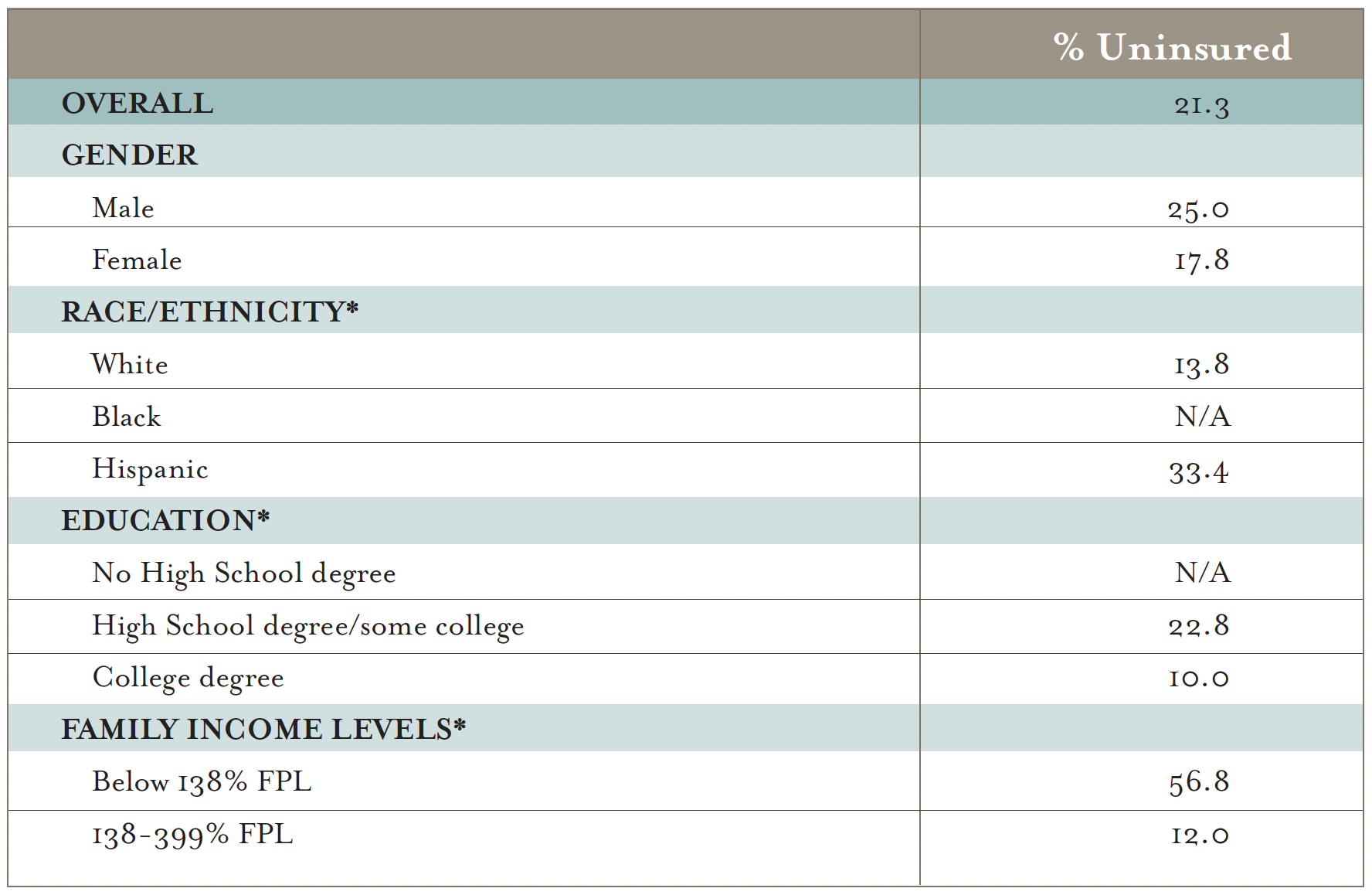

We examined the characteristics of those Young Invincibles who remain uninsured in 2016 to understand what strategies might be best for helping them obtain insurance coverage. As Table 2 shows, 33.4% of Hispanic Young Invincibles remain uninsured. This is only slightly higher than the uninsured rate of 32.2% for all Hispanic, as reported in Issue Brief #22. Hispanics have historically had the lowest rates of health insurance coverage, and while they have made gains in recent years, they still have lower rates of coverage than Whites or Blacks. The majority (56.8%) of the lowest income Young Invincibles remain uninsured. As with the low income population as a whole, Texas’ refusal to expand Medicaid remains an insurmountable barrier for many in this group.

Table 2 — Characteristics of Uninsured Young Invincibles, March 2016

N/A denotes uninsurance rates for “Black” and “No high school degree” were not reported due to insufficient sample sizes.

Conclusions

Our data show that the uninsured rate for Texas’ Young Invincibles dropped significantly from September 2013 to March 2016. When we look at the four aspects of the ACA that could have accounted for the change, our data show that the large employer mandate may have helped Young Invincibles obtain coverage, either through their direct employment or through coverage those ages 18-26 may have through their parents’ employer-sponsored insurance plans. The strength of the Texas economy, through 2015, also likely contributed to rising rates of coverage for the Young Invincibles, as it may have for Texans as a whole.

We know from the Department of Health and Human Services, that during the most recent open enrollment period, 378,798 Texan Young Invincibles were covered by ACA marketplace plans. While our HRMS survey showed an increase in the number of Young Invincibles covered by individual plans, our sample size for this sub-group was too small for us to draw statistically significant conclusions about the impact of the marketplace plans. The participation of Young Invincibles in the marketplace is important to its long-term success. The absence of a sufficient number of Young Invincibles, and other healthier adults, enrolled in the marketplace is cited by some as a factor in the anticipated increases in the 2017 marketplace plan premiums and the withdrawal of large insurance carriers from several state individual insurance marketplaces. The composition of risk pools—including a mix of healthier and less healthy participants—is vital for the long-term sustainability of the marketplace.

The two largest sub-groups of uninsured Young Invincibles are those with incomes below 138% of the federal poverty level and Hispanics. This finding is consistent with the recent report by the Commonwealth Fund which found that Hispanics and low-income young adults (under 35) still lack coverage in a national survey. For the portion of that sub-group with incomes below 100% of the federal poverty level, the ACA’s coverage solution was an expanded Medicaid program. Because Texas has not yet opted to use the federal Medicaid dollars to cover these individuals, it is likely that they will remain uninsured. To encourage uninsured Hispanic Young Invincibles to enroll in the marketplace, culturally appropriate outreach and enrollment assistance are needed.

There are still opportunities to bring more Young Invincibles into coverage. As suggested in a recent CMS memo, outreach and enrollment organizations should develop new approaches to reach young adults, especially those who paid the annually-escalating tax penalty fee for being uninsured. Another promising strategy is to encourage enrollment organizations to assist young adults who are aging out of Medicaid and CHIP and help transition them to Marketplace plans or other coverage. Youth-friendly e-outreach during the upcoming open enrollment period may also be effective. Public-private partnerships involving Lyft, the American Hospital Association, and nonprofits such as Enroll America, Out2Enroll, and Young Invincibles are developing creative ways to reach young adults.

Methodology

Each quarter’s HRMS sample of nonelderly adults is drawn from active KnowledgePanel® members to be representative of the US population. In the first quarter of 2013, the HRMS provided an analysis sample of about 3,000 nonelderly (age 18–64) adults. After that, the HRMS sample was expanded to provide analysis samples of roughly 7,500 nonelderly adults, with oversamples added to better track low-income adults and adults in selected state groups based on (1) the potential for gains in insurance coverage in the state under the ACA (as estimated by the Urban Institute’s microsimulation model) and (2) states of specific interest to the HRMS funders.

Although fresh samples are drawn each quarter, the same individuals may be selected for different rounds of the survey. Because each panel member has a unique identifier, it is possible to control for the overlap in samples across quarters. For surveys based on Internet panels, the overall response rate incorporates the survey completion rate as well as the rates of panel recruitment and panel participation over time. The American Association for Public Opinion Research (AAPOR) cumulative response rate for the HRMS is the product of the panel household recruitment rate, the panel household profile rate, and the HRMS completion rate—roughly 5 percent each quarter.

While low, this response rate does not necessarily imply inaccurate estimates; a survey with a low response rate can still be representative of the sample population, although the risk of nonresponse bias is, of course, higher. All tabulations from the HRMS are based on weighted estimates. The HRMS weights reflect the probability of sample selection from the KnowledgePanel® and post-stratification to the characteristics of nonelderly adults and children in the United States based on benchmarks from the Current Population Survey and the Pew Hispanic Center Survey. Because the KnowledgePanel® collects in-depth information on panel members, the post-stratification weights can be based on a rich set of measures, including gender, age, race/ethnicity, education, household income, homeownership, Internet access, primary language (English/Spanish), residence in a metropolitan area, and region. Given the many potential sources of bias in survey data in general, and in data from Internet-based surveys in particular, the survey weights for the HRMS likely reduce, but do not eliminate, potential biases.

The design effect for the Texas data in March 2016 is 2.7005 and the MOE is +/- 4.1% at the 95% CI. The survey fielded from March 1-22, 2016.