“The Fed should get out of the business of trying to juice our economy and simply be focused on sound money and monetary stability, ideally tied to gold.” —Ted Cruz, Oct. 28, 2015

Texas Senator and Republican presidential candidate Ted Cruz supports returning to a gold standard, and half of the other Republican candidates do not reject the idea.1 This level of interest makes the proposal worth a serious look.

The gold standard attracts people because gold is tangible. The classical gold standard—a period of 35 years before World War I when most trading economies ran a pure gold standard arrangement—exhibited long-run price stability. Nostalgia may play a role in gold’s allure.2 In addition, the credibility of modern central bank policies took a strong blow in the global financial crisis, with pointed criticism of efforts to stimulate inflation through low interest rates and unconventional monetary policies.

Why hasn’t any country gone back on the gold standard since President Richard Nixon closed the gold window in 1971? If it worked then, why not today?

To preview the conclusion, this issue brief agrees with the consensus of economists that the current money system works much better than the gold standard would. We are much better off allowing an independent central bank to respond dynamically to economic conditions than anchoring our money supply to the whims of a global commodity market.

Metrics for a Good Monetary System

Until aspiring bitcoin successors get the kinks worked out, there is no avoiding governments meddling in money.3 What would be the characteristics we should look for in a government-run system?

- Price stability: Economists generally find that inflation between zero and 5 percent avoids the pitfalls of deflation while minimizing the volatility induced by inflation.4 Most major economy central banks have chosen an inflation target around 2 percent to keep inflation contained in the optimal range.

- Growth stability: Economists generally agree that achieving the first goal is about the best monetary policy can do to facilitate stable growth. But if growth drops well below potential, monetary policy can play a role in helping return the economy to health, consistent with the inflation target.5

- Financial stability: Most importantly, central banks need a monetary arrangement that allows them to act as a lender of last resort in a crisis, providing liquidity to solvent financial institutions whose failure would otherwise jeopardize the economy.

- Minimal government interference: In a campaign year dominated by calls for shrinking the shadow of the federal government on the economy, minimizing the scope of government manipulation belongs on the list of desirable characteristics.

Horse Race: Current System vs. Gold Standard

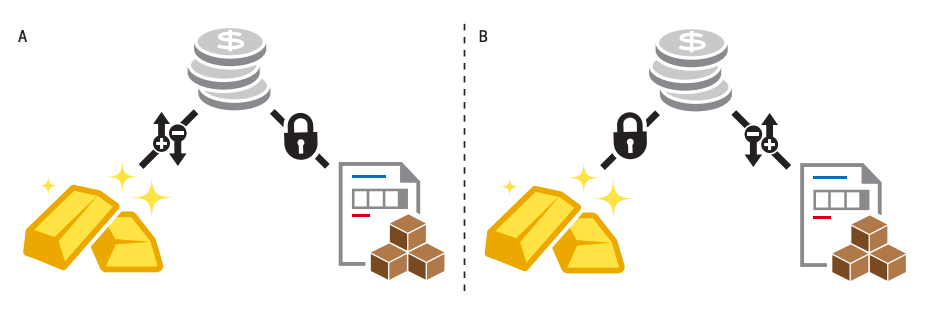

The big question in this horse race is what should be the objective for issuing money? Under the current system the Federal Reserve (“Fed”) primarily issues money on the basis of maintaining domestic price stability. That is, the value of the goods and services Americans buy should rise relative to the value of the dollar (i.e., inflation) by about 2 percent per year. The dollar price of gold makes no difference (Figure 1a).

Figure 1 — Current System (A) vs. Gold Standard (B)

Under a gold standard, on the other hand, the U.S. government (presumably the Fed) would maintain a constant dollar price of gold. This eliminates any scope for discretionary monetary policy. The value of the dollar relative to things Americans buy floats in response to gold market intervention (Figure 1b).

It is important to note that gold is a global commodity. The Fed must target the global price of gold. If Indian demand for gold collapses, or if China limits gold exports, the Fed would make up the difference by buying or selling gold, respectively, to maintain a constant dollar price.

1. Price Stability

It is difficult to construct a good comparison between the two options, since we can’t ever run both under identical circumstances. Economic models that attempt a direct—but theoretical—comparison generally find that while a gold standard produces good long-run price stability, year-to-year short-run volatility is higher than what a modern inflation targeting monetary policy produces.6

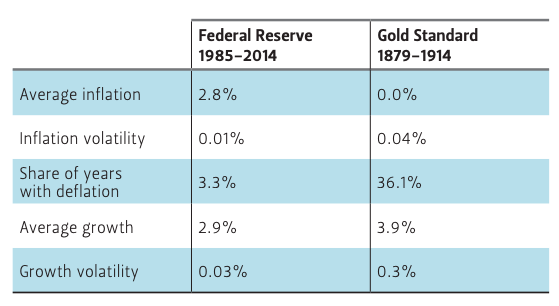

Historical comparisons can also yield some insight. The clearest comparison is between the period of the classical gold standard in the U.S. (1879-1914), and the modern era of inflation targeting, which began in the mid-1980s.7 Table 1 indicates that inflation was indeed lower on average during the classical gold standard, but at the cost of higher year-to-year volatility. Further, the U.S. experienced deflation more than one-third of the time during the classical gold standard.

Table 1 — Historical Inflation Performance Under a Gold Standard and Modern Monetary Policy

The famous gold rushes of the 19th century illustrate the difficulty with locking money supply to gold. A slowing of global demand for gold below the pace of new gold production (or a surge of supply beyond demand) requires the Fed to purchase gold to keep the market balanced at the pegged price. This raises the U.S. money supply, which is stimulative, and inflation tends to increase. Accordingly, gold demand above supply causes a contractionary monetary policy and downward pressure on inflation.

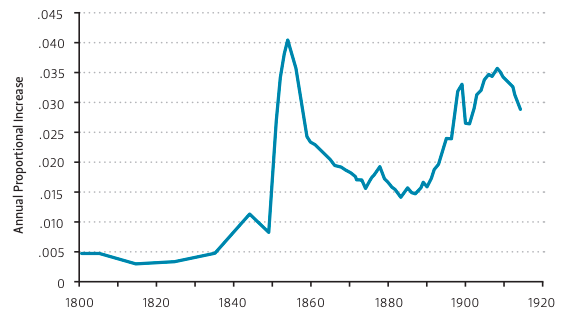

It is no coincidence that the major gold rushes of the 19th century occurred in two clusters, first in California (1849) and Australia (1851), and then in South Africa (1886) and the Alaskan Klondike (1896). Gold production slumped for about a decade in the 1840s, and for about two decades beginning in 1870. (Figure 2) In both cases central banks around the world were forced to sell gold, reduce their money supply, and induce deflation. Deflation meant gold could buy more real goods. Prospecting for gold became a more profitable enterprise, and eventually major new gold supplies were found. All of them were inspired by deflation caused by the gold standard.

Figure 2 — Rate of Increase of Global Mined Gold Stock

What do current trends suggest would happen today? Real GDP is a good proxy for gold demand for nonmonetary purposes.10 The IMF forecasts world GDP growth above 3 percent for the next few years.11 The global gold supply grew at a remarkably steady rate of 1.6 percent per year in the 20th century and has continued that pace of growth in this century, according to U.S. Geological Survey data.12

If the U.S. were the only country on a gold standard, the imbalance between global supply growing at 1.6 percent and demand growing above 3 percent would require the Fed to reduce the U.S. money supply at a pace of at least 1.4 percent of global gold stocks, or 2.4 percent of the U.S. monetary base, every year.13 As long as the U.S. economy grows about 1.5 percent annually, a back-of-the-envelope calculation suggests that would cause relentless 4 percent deflation.14

2. Growth Stability

Economic growth was undoubtedly higher on average during the classical gold standard than in the past 30 years, but that would be an unfair comparison, as monetary policy cannot impact growth in the long run, only prices.

A more appropriate comparison would be the volatility of growth, as modern monetary policy often attempts to smooth recessions with low interest rates. The justification is that too low of an economic growth rate would allow inflation to fall below its target. Hence, current central bank stimulus policies are, at the core, motivated by price stability. The figures in Table 1 show that growth volatility has been an order of magnitude smaller in the past 30 years than it was under the classical gold standard.

3. Financial Stability

Financial stability is another criteria that is difficult to compare carefully. For instance, the U.S. had no central bank to serve as a lender of last resort under most of the classical gold standard. That said, financial crises were no less common under gold. The U.S. experienced financial crises in 1884, 1893, 1896, and 1907—roughly once per decade. And the peg to gold constrained the lender-of-last-resort capability in countries with central banks, contributing to financial crisis during the Great Depression.

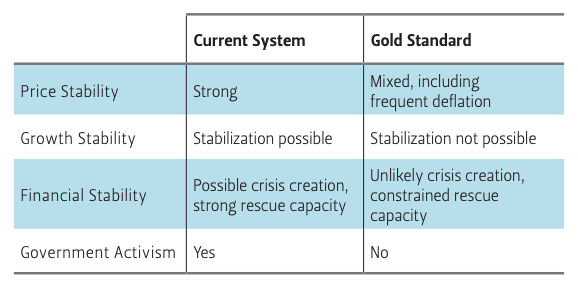

Table 2 — Horse Race

Low interest rates implemented in the pursuit of price stability played a role in the U.S. subprime mortgage crisis, and some worry about asset price bubbles in the current low-interest rate environment. A gold standard would lower the risk that monetary policy contributes to asset price bubbles, at the cost of discarding active price and employment stabilization.

If a bubble can be identified, other instruments exist to restrict lending in those specific markets. Fed Chair Janet Yellen’s June 2015 testimony identifying potential bubbles in equity valuations of smaller firms, social media, and biotechnology firms was enough to cause a correction. But bubbles are notoriously difficult to spot ahead of time.

4. Minimal Government Interference

As the Cruz quote at the top of this brief indicates, one argument to switch to a gold standard is that it removes discretion from the Fed; no longer can monetary policy be used to stabilize economic growth. Some are uncomfortable with the independence of the Fed from elected officials. The traditional argument for gold in this regard is to counteract fear that a central bank might print too much money—either to stimulate the economy or to finance a fiscal deficit—and therefore cause runaway inflation. The slow growth of the global supply of gold puts a lid on potential inflation.

At present the risk of runaway inflation appears low. The preponderance of economic evidence indicates central bank independence is a key ingredient in achieving low inflation.15 Rather, we seem to have the opposite problem of inadequate inflation. If price stability is the first priority, monetary policy should aim to generate more inflation. That means stimulating faster growth.

Critics of current monetary policy cite attempts to boost growth through low interest rates in the early 2000s. But recall that in 2003-4 deflation appeared to be a very real threat.16 Interest rates were lowered for the same reason that they are low today—to protect against deflation.

Conclusion

Whether based on theoretical or historical comparisons, the gold standard appears less likely to deliver superior price stability than the current system. Rather, money supply would be determined by the vagaries of the global gold market, which would only coincide with domestic economic needs by chance. Even if gold markets were perfectly stable, the gold standard would likely induce a damaging level of deflation.

It was precisely the unwillingness of the U.S. to undertake such a destructive monetary policy that lead to the 1971 collapse of the “gold exchange standard” operated under Bretton Woods. Instead, the money supply continued to grow to support moderate inflation, which undermined the tie to gold. Would deflation be more politically acceptable today?

Indeed, price stability is the reason the Fed “juices the economy” to raise inflation up to the target level of 2 percent. Because prices are most stable with moderate, stable growth, monetary policy that actively stabilizes the price level also stabilizes growth better than the gold standard. Could this come at the cost of occasionally contributing to asset price bubbles? Perhaps. But a pure gold standard may limit the lender of last resort capacity of the Fed, so it is not clear that financial stability would improve.

Endnotes

1. Of the remaining candidates, only John Kasich and Marco Rubio have rejected the idea of a gold standard.

2. For example, one of my grandmothers always tried to keep some gold or silver coins in case the Great Depression returned. How many people have similar personal stories?

3. Privately issued money is a mess. For instance, until just after the Civil War many different privately issued currencies circulated with a complicated web of exchange rates and discounts. When the federal dollar finally became the undisputed coin of the realm, commerce benefited greatly from reduced transaction costs.

4. Michael Bruno and William Easterly, “Inflation and Growth: In Search of a Stable Relationship,” Federal Reserve Bank of St. Louis Review, May-June 1996: 139–46.

5. “Potential” refers to the maximum rate of economic growth or unemployment at which resources are not so stretched that prices accelerate. Economists consider this to be a stable macroeconomic equilibrium.

6. Michael D. Bordo, Robert D. Dittmar, and William T. Gavin, “Gold, Fiat Money, and Price Stability,” B.E. Journal of Macroeconomics: Topics in Macroeconomics 7, no. 1 (2007), http://search.ebscohost.com/login.aspx?direct=true&db=eoh&AN=0935829&site=ehost-live&scope=site; Gabriel Fagan, James R. Lothian, and Paul D. McNelis, “Was the Gold Standard Really Destabilizing?,” Journal of Applied Econometrics 28, no. 2 (March 2013): 231–49.

7. In between the two comparison periods the U.S. followed a “gold exchange standard” between the world wars (it floated during the wars) and then anchored the Bretton Woods System’s loose link to gold until 1971. Until the mid-1980s the Fed targeted monetary aggregates. Then the Fed gradually abandoned the use of monetary aggregates in favor of the federal funds rate as an intermediary target. The figures in Table 1 do not change materially by changing the starting point by a year or two.

8. For Table 1 historical prices see Lawrence H. Officer and Samuel H. Williamson, “The Annual Consumer Price Index for the United States, 1774-2014,” 2016, https://measuringworth.com/datasets/uscpi/result.php; for historical GDP data Angus Maddison, “Statistics on World Population, GDP and Per Capita GDP, 1-2008 AD,” 2010, http://www.ggdc.net/maddison/Historical_Statistics/horizontalfile_02-2010.xls.

9. Robert B. Barsky and J. Bradford De Long, “Forecasting Pre-World War I Inflation: The Fisher Effect and the Gold Standard,” Quarterly Journal of Economics 106, no. 3 (August 1991): 815–36; for Figure 2 historical prices, see and Lawrence H. Officer and Samuel H. Williamson, “The Annual Consumer Price Index for the United States, 1774-2014,” 2016, https://measuringworth.com/datasets/uscpi/result.php; for historical GDP data see Angus Maddison, “Economic Growth and Structural Change in Advanced Countries,” in Western Economies in Transition: Structural Change and Adjustment Policies in Industrial Countries, ed. Irving Leveson and Jimmy W. Wheeler (London: Croom Helm, 1980).

10. We assume zero gold demand for investment purposes; it would diminish if the U.S. credibly kept the gold price pegged. If gold prices ceased to rise as they did in the 20th century, supply growth might fall, too.

11. “Subdued Demand, Diminished Prospects,” World Economic Outlook Update, International Monetary Fund, January 2016, http://www.imf.org/external/pubs/ft/weo/2016/update/01/.

12. “Gold Statistics,” U.S. Geological Survey, Jan. 30, 2015, http://minerals.usgs.gov/minerals/pubs/historical-statistics/ds140-gold.xlsx.

13. Global gold stocks are worth about $6.8 trillion and the U.S. monetary base is about $3.8 trillion.

14. The quantity equation suggests inflation equals the rate of money supply growth minus the rate of real GDP growth, with the usual assumption of holding money velocity constant.

15. V. V. Chari and Patrick J. Kehoe, “Modern Macroeconomics in Practice: How Theory Is Shaping Policy,” Journal of Economic Perspectives 20, no. 4 (2006): 3–28.

16. Despite average inflation above 2 percent, U.S. CPI presented nine months of (seasonally adjusted) negative inflation during the 2001-2006 period in the context of Japan experiencing five years of deflation.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.