Author(s)

The energy transition is taking different paths around the world — particularly now, given the uncertainty in the supply of energy and commodities critical for the transition away from fossil fuels, as well as issues in the supply chains of staples for daily consumption, including fertilizers, and consequent price increases.

In this context, commodity producers/ exporting countries are likely to benefit—that is, if they are able to exploit their comparative advantage. Brazil and Chile, for example, can profit from their role as iron ore, copper, and lithium producers given the need for those minerals for renewable energy production, including but not limited to the manufacture of electric vehicles. Significant hydro and renewable resources also play into their positioning as potential “green” miners and producers of green hydrogen.

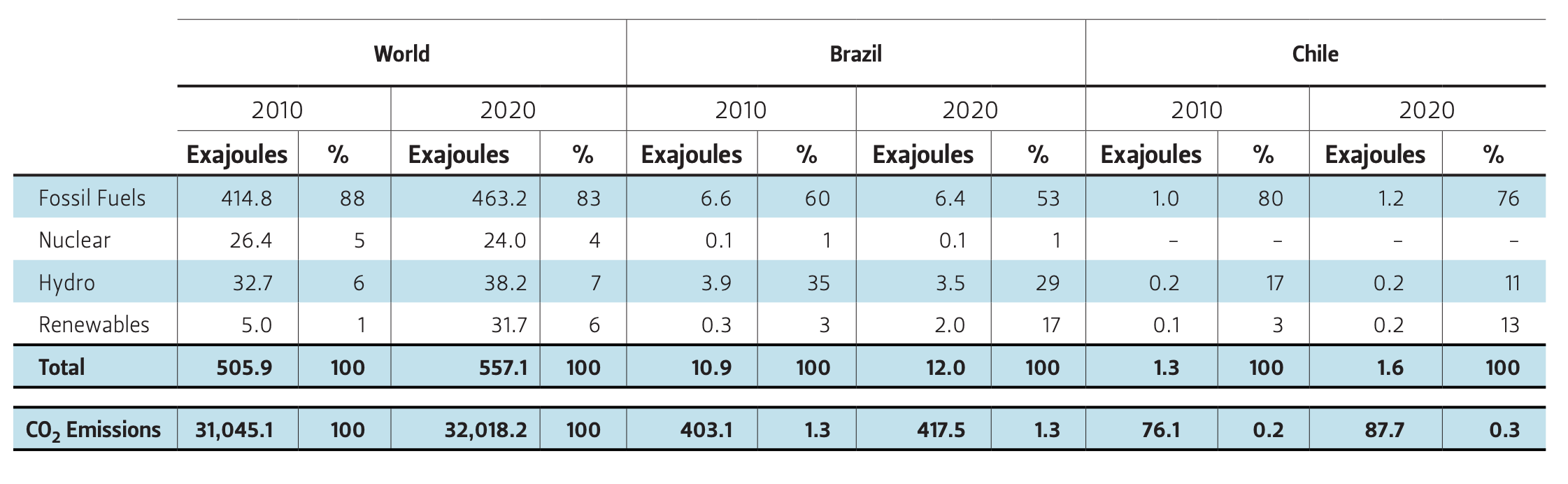

With major developments in solar and wind power playing to their strengths, Brazil and Chile generate hydro and renewable energy at 46% and 24%, respectively (see Table 1). But in spite of their favorable position and the impact of COVID-19, both countries increased their greenhouse gas (GHG) emissions between 2010 and 2020 at a higher rate than the world as a whole. Mining activity is likely to explain the increase in GHG emissions for both countries (with deforestation also contributing to the increase in Brazil).

Although they are very different countries, Brazil and Chile have significant hydro and renewable resources in common, and are both major mining operators and exporters. Reducing GHGs in their mining operations is therefore a challenge and an opportunity. Becoming “green iron ore” and “green copper” producers and exporters would give them a competitive advantage while reducing emissions in their domestic economies. Hence, diversifying their energy portfolios and technology development, with the objective of having cleaner energy available for their economies while reducing their CO2 emissions and meeting their net-zero commitment by 2050, is and should be important for both countries.

Brazil

Fossil fuels represented 53% of Brazil’s energy matrix in 2020, down from 60% in 2010. The country’s carbon emissions have risen slightly in absolute terms (403.1 million metric tons versus 417.5 million metric tons, per Table 1) but have been stable at relative levels, constituting 1.3% of the worldwide total.

Table 1 — Primary Energy Consumption and Carbon Emissions (Millions of Metric Tons)

Brazil has a long history with nonfossil fuels, with two resources at the center: First, thanks to its access to the Iguazu Falls, which are shared with Argentina and Paraguay, Brazil’s electricity generation is dominated by hydro resources, which represent more than 60% of its electricity generation. Second, Brazil is a leader in biogasoline/ethanol and biodiesel production, with mandatory ethanol blending since 1931.

Brazil has a diverse electricity generation matrix, composed of 14% fossil fuels, 2.5% nuclear power, 64% hydro power, and 19.4% renewables, which include wind, biomass, and solar power.1

According to its National Electric Energy Agency (ANEEL), Brazil’s entire northeast coast is very windy, with 82% of the country’s 653 wind farms found in the Northeast. The state of Ceará is the country’s third-largest producer of wind power, behind the states Rio Grande do Norte and Bahia.

In fact, the rise in Brazilian wind power generation has prevented what otherwise would be a dip in the renewable share of primary energy. Overall, renewables and hydro already accounted for 46% of its primary energy sources in 2020, more than 8% over its 2010 share, despite hydro declining (see Table 1). In fact, excluding hydro, the consumption of renewables for power generation increased from 34.1 terawatt-hours in 2010 to 120.3 terawatt-hours in 2020. Wind power represented 47% and solar power represented 7% of the energy sources used to generate electricity.

In this context of substantial “green” power resources, the development of green hydrogen and ammonia and associated chemical products is being considered for local consumption and export.

For example, in March 2021, the state of Ceará signed an agreement with Australian firm Enegix Energy to invest $5.4 billion into expanding green hydrogen in the state. Under the terms of the deal, Enegix will build the world’s largest green hydrogen plant, capable of producing over 600,000 tons per year from 3.4GW of combined baseload wind and solar power. Construction is expected to take up to four years.

Additionally, in the domestic market, hydrogen is being targeted as a possible means of running factories with zero carbon emissions. Considering that Brazil is the no. 2 producer worldwide of iron ore, after Australia, and that iron and steelmaking are responsible for 11% of global CO2 emissions,2 there is a big incentive to curb these emissions. For example, per the Wall Street Journal, the Brazilian iron ore producer Vale SA wants to cut net Scope 3 emissions (from steel manufacturers’ use of iron ore and metallurgical coal) by 15% by 2035,3 with hydrogen potentially playing a significant role in substituting for coal. Furthermore, there are opportunities for similar emission reductions in Brazil’s production of silicon, graphite, nickel, tantalum, and lithium, among other minerals.

Ahead of the 2021 United Nations Climate Change Conference, also known as COP26, in October 2021 Brazil’s environment minister announced a National Green Growth Program to advance sustainable development and promote forest conservation, with objectives to reduce greenhouse gas emissions and protect biodiversity. The operational plan is expected by September 2022.

Unlike Chile, Brazil is blessed with significant oil and gas resources, which pose a challenge for decarbonization. Current oil production in the country — the top oil producer in Latin America — is about 3 million barrels/day. At the IEA Ministerial Meeting in Paris on March 24, 2022, Brazil’s minister of energy offered to increase production by 300,000 b/d to assist with the global oil supply crunch. The country also produces 127 million cubic meters of natural gas per day, although it imports Bolivian gas and LNG to meet domestic demand.

As such, as an oil producer, and having committed to increase renewable power generation and eventually produce green hydrogen, the country has an opportunity to increase oil exports for its own benefit while decarbonizing its domestic economy and mineral exports.

Chile

Chile is the world’s largest copper producer and second-largest lithium producer. However, it does not have hydrocarbon resources. To meet its domestic energy needs, the country has historically relied on imported coal, oil, and natural gas as well as local hydro, where available. Between 2010 and 2020, primary energy consumption grew at 2.4%/year, with carbon emissions growing at the same rate during this period but representing only 0.3% of CO2 emissions worldwide (see Table 1).

The country’s northern region contains the Atacama Desert, which receives the world’s highest levels of solar radiation, while the extreme South has the best onshore wind conditions on the planet. After solar panels and wind turbines became economically viable worldwide, the country, over time, embraced renewables. As a result, the wind and solar share of the country’s primary energy consumption increased from 3% in 2010 to 13% in 2020 (see Table 1).

Installed total power capacity nearly doubled from approximately 16,622 megawatts in 2010 to nearly 31,000 MW in 2021 (see Table 2). This growth was primarily driven by solar and wind capacity, which added close to 9,000 MW during this period. Given the country’s environment, electricity generation is likely to become dominated by solar panels in the northern region and by wind turbines in the South. For example, according to BHP’s Climate Change Report 2020, they established agreements for 100% renewable electricity use in their Chilean operations. In fact, about 120 companies in Chile’s private sector have embarked on campaigns to reach zero emissions.

Table 2 — Chile’s Installed Electricity Capacity and Generation by Source

In this context, the previous administration’s Energy Ministry published an updated National Energy Policy,4 which is currently being reviewed by the new government that took over in March 2022. It primarily includes three objectives:

1. Become carbon-neutral by 2050

2. Use the energy transition as a vehicle to improve the quality of life for all citizens

3. Create a new, productive Chilean identity that integrates clean energy sources into economic activity

By accomplishing these objectives, not only would Chile’s domestic energy production and consumption become more environmentally responsible and competitive, but its exports would as well. Most importantly, Chile is positioning itself to become a major producer and eventually exporter of green hydrogen, ammonia, and methanol, thanks to the competitive cost of electricity generated by solar and wind power plants.

Currently, the northern region is developing initiatives to evaluate the potential growth of the hydrogen industry in the Antofagasta region with participation from industry, academia, and government. Pilot projects include:

- A collaboration in northern Antofagasta between Engie and Enaex, a Chilean explosives manufacturer, to produce blasting chemical ammonia using green hydrogen produced via 1 GW of solar power; this project is set to launch in 2024.

- A project with Air Liquide and partners to produce green methanol

- Several other pilot projects supported by the regional government and private sector

In addition, Chile can also play a significant role in the energy transition as a copper and lithium producer by supporting EV battery production and supplying the copper needed for expansive electrification globally. Chile has the potential to move downstream, producing the batteries locally using renewable energy for home use and export, rather than just exporting the ores.

Conclusion

Both Brazil and Chile are endowed with commodities critical for the global transition toward renewable energy.

They are well positioned to compete and succeed. Whether they use the opportunity will depend on many factors, including the availability of financing to build the necessary infrastructure and the development of a commercial and regulatory framework needed to produce hydrogen, ammonia, and methanol as a new industry. Additionally, hydrogen offers the countries the opportunity to reduce and/or replace the domestic consumption of fossil fuels while becoming “hydrogen exporters.” The first projects to enable these industries are currently in the making. Their success will be indicative of Brazil’s and Chile’s potential role in the energy transition — not only as participants, but as major players and suppliers.

Endnotes

1. BP, Statistical Review of World Energy 2021, 57, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf.

2. Global Efficiency Intelligence, “Global Steel Industry’s GHG Emissions,” https://www.globalefficiencyintel.com/new-blog/2021/global-steel-industrys-ghg-emissions.

3. Vale SA, 2021 Annual Report.

4. Chile Ministry of Energy, Politica Energetica Nacional, Actualizacion 2022, https://energia.gob.cl/energia2050.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.