Author(s)

Overview

The Arab Gulf states have officially pledged to achieve net-zero greenhouse gas emissions. Meanwhile, however, they face ongoing criticism for watering down climate agreements and delaying international action. Some observers have contended they are using their vast financial resources to influence climate negotiations and gain concessions that serve their own economic interests.

How significant is the influence of the Arab Gulf states — whose economies remain dominated by oil and gas — on the world’s pathway to net-zero emissions? This report aims to answer that question by evaluating the Gulf’s energy diplomacy and financial reach, including the state of its markets and its contributions to the world economy (and to global financial institutions in particular).

So far, trends in the financing of fossil fuel projects imply that the pathway to net zero will involve continued investment in oil and gas, an increase in the share of clean energy in the energy mix, and the integration of clean technologies into the energy sector. This report finds that although this is the pathway preferred by the Gulf states, they are not necessarily its only proponents. Rather, their strategy aligns with the world's pursuit of economic growth and, accordingly, of secure, reliable, and stable energy sources.

Introduction

Together, the Arab Gulf states — Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) — have become a global power. Led by Saudi Arabia and the UAE, and to some extent Qatar, they have a major influence on the world’s energy, financial, political, and, consequently, environmental affairs. This gives rise to the question: How big a role do the Arab Gulf states play in steering the global climate change agenda?

In January 2023, the UAE announced Sultan Ahmed al-Jaber as chair of the 28th United Nations Climate Change Conference of the Parties (COP28), to be held in Dubai in November 2023.[1] Al-Jaber is the UAE’s minister of industry and advanced technology and special envoy for climate change, as well as the CEO of the Abu Dhabi National Oil Company (ADNOC).

Al-Jaber's appointment as chair of COP28 was met with criticism by some Western legislators. More than 100 members of the U.S. Congress and the European Parliament called for al-Jaber's removal from the chair position, arguing that his role as CEO of ADNOC would threaten the integrity of the negotiations.[2] Similar objections had been made during COP27, which was held in Egypt in November 2022. In that case, critics protested the attendance of fossil fuel lobbyists at the conference, which resulted in a final declaration that only pledged to phase out coal, and not oil and gas fuels.[3]

Some Western leaders, however, have welcomed al-Jaber’s appointment. Frans Timmermans, the European Commission’s president for climate affairs, said, “Al-Jaber is extremely well placed to lead us into a successful COP because of his involvement in renewable energies.” Timmermans stressed the need for the participation of oil and gas companies in the energy transition, stating that discounting them would obstruct progress toward climate change goals.[4]

John Kerry, the U.S. climate envoy and former secretary of state, also expressed approval of al-Jaber’s appointment, saying: “I think that Dr. Sultan al-Jaber is a terrific choice because he is the head of [a] company ... that knows it needs to transition.”[5]

Along with al-Jaber’s appointment as COP28 chair, a number of factors have prompted this research into the role — direct or indirect — the Gulf states may play in steering the global energy transition agenda along a particular path of interest. These include the 2011 decision by the International Renewable Energy Agency (IRENA) to make the UAE, whose economy is dominated by oil exports, the site of its permanent headquarters; the Gulf states’ plans to increase their oil and gas production capacities; and the continued financing by Gulf states of global fossil fuel projects, which reached an accumulative $5.5 trillion in 2022.[6]

Complex geopolitical and economic dynamics generally obscure the specific roles any particular region plays in the global energy transition and pursuit of net zero. But, by examining a region’s exports and imports, investments, funds, and other indicators of economic growth, we can more easily assess its role in global economic development. Because economic growth — a mainstream objective among developed and developing countries alike — relies on a stable supply of energy, in doing so we can determine, at least partially, the region’s influence on the energy sector and the energy transition agenda.

In a world of increasing interdependence between net importers and exporters of energy, multilateral rules can provide a more balanced and efficient framework for international cooperation. This research paper aims to contribute to the literature by promoting the international cooperation on energy necessary to face the challenges of the energy transition and reach the net-zero greenhouse gas emissions goal.

1. Methodology

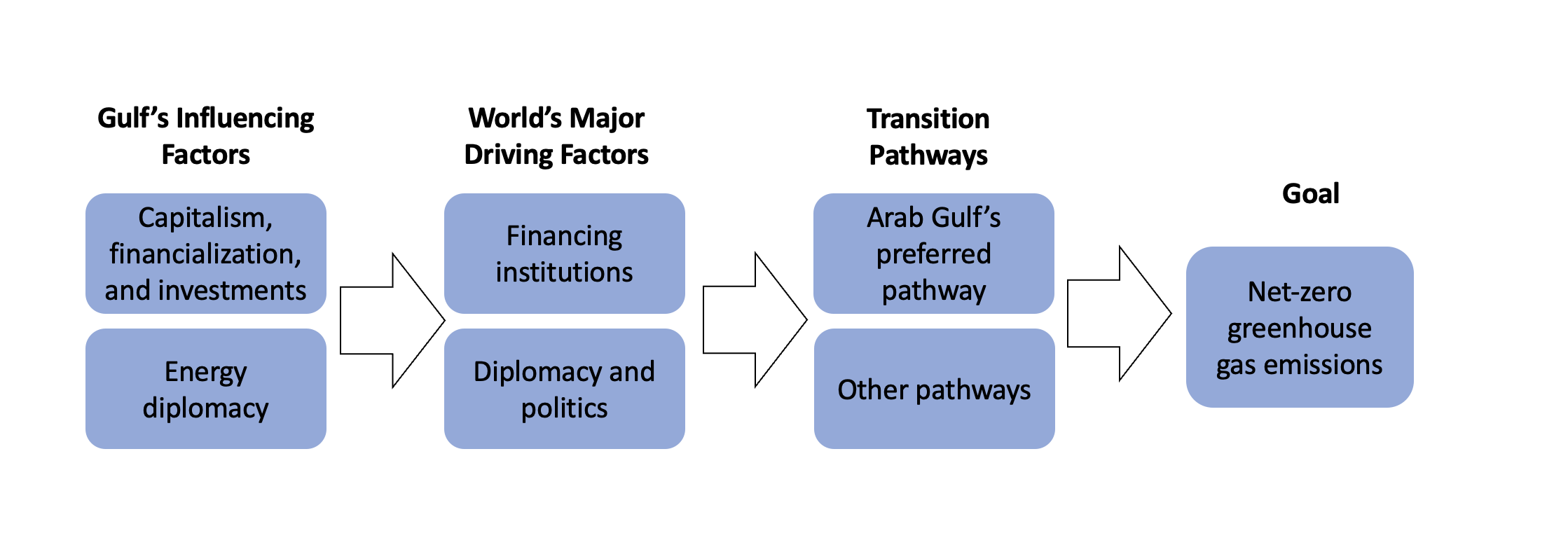

To trace the Gulf states’ influence on the energy transition agenda, I first review transition pathways in Section 2 and attempt to determine whether trends in world financing suggest a particularly favored pathway to the net zero goal. I review two options: the pathway preferred by the Gulf states, and a pathway proposed by the International Energy Agency (IEA), which represents the mainstream among developed nations (Figure 1).

Next, I examine the major factors driving the energy transition globally in Section 3, and then assess the two main factors behind the Gulf states’ influence on the net zero goal — financial reach and energy diplomacy — in Section 4.

The financialization of the Gulf has made it a prominent player in the global financial sector; its capital and investments partially feed the world’s banks and capital markets, which in turn impact the development of energy technologies, resource extraction and consumption, and related governance. Meanwhile, the Gulf states employ their soft power, or diplomacy, to secure their interests in the global arena. Their energy diplomacy influences the demand for their oil and gas products.

In Section 5, I discuss the Gulf states’ energy diplomacy. The paper ends by discussing the global push for economic growth and its relation to energy supply and consumption.

Figure 1 — Methodology Used to Track the Gulf States’ Influence on the Energy Transition Agenda

2. The Energy Transition from the Gulf Perspective

Through the Paris Agreement, countries at COP21 in 2015 pledged to limit the global temperature increase to 1.5 degrees Celsius above preindustrial levels by the end of this century. According to the Intergovernmental Panel on Climate Change (IPCC), roughly 65% of global greenhouse gas emissions causing the global temperature increase can be attributed to CO2 from fossil fuel combustion and industrial processes.[7]Through its executive secretary, Patricia Espinosa, the United Nations Framework Convention on Climate Change (UNFCCC) called for “a swift and broad transition to renewable energy.” Espinosa stated that the transition would be “essential to achieve the emission reduction goals laid down by the Paris Agreement.”[8]

Though United Nations subsidiary and member organizations have not explicitly called to phase out oil and gas from the global energy system, some international agencies have openly supported phasing out all fossil fuels — coal, oil, and gas — to achieve the net zero goal. For example, IRENA defines the energy transition as “a pathway toward a transformation of the global energy sector from fossil-based to zero-carbon by the second half of this century.”[9]

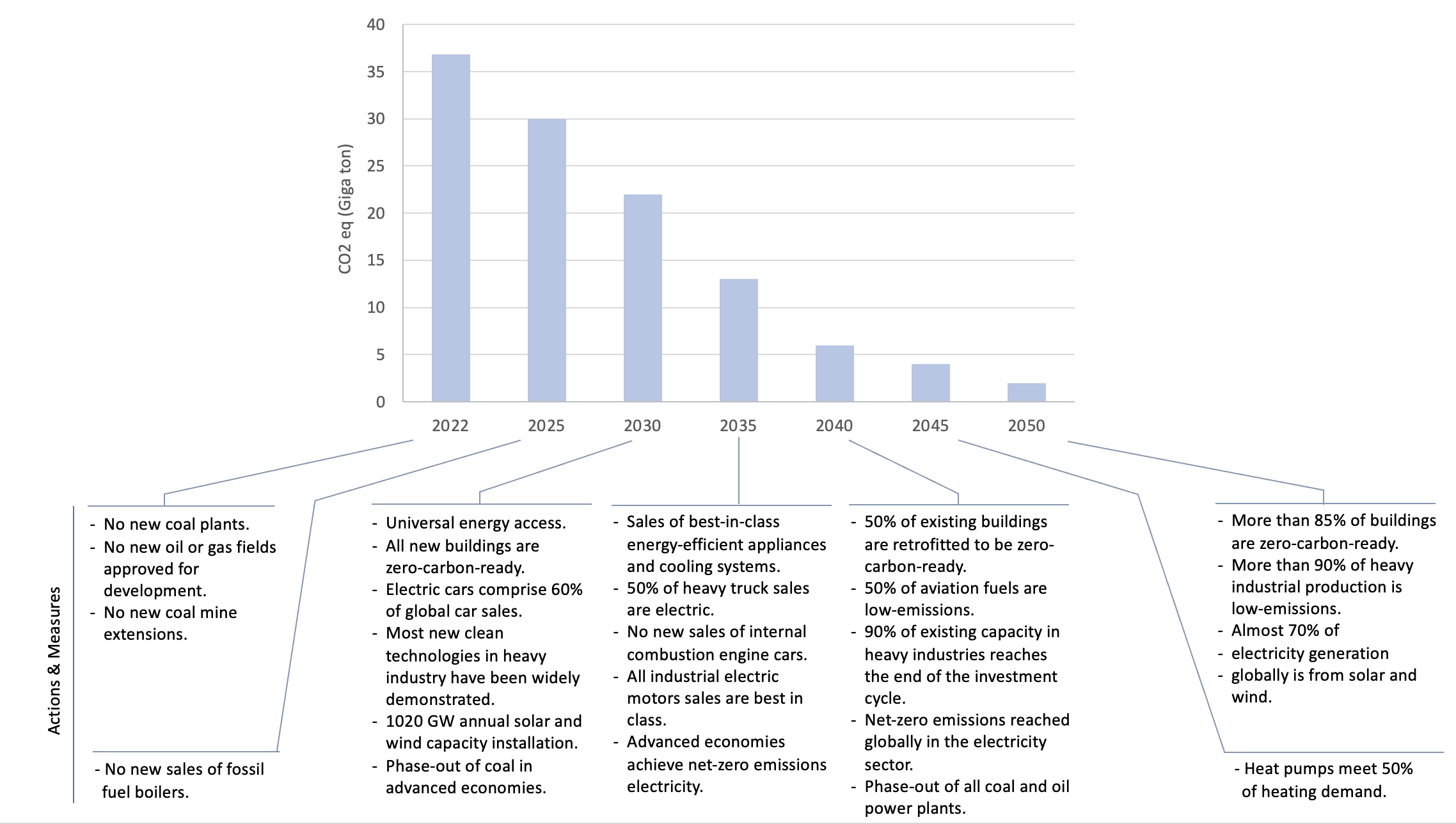

The IEA previously proposed a pathway to net-zero carbon emissions by 2050 that would see investment in coal mines, oil, and gas fields banned by 2021 and completely rule out fossil fuels by 2025 (Figure 2).[10] While acknowledging that 2.6 billion of the world’s 7.9 billion people have no access to electricity or clean cooking options, the IEA assumes that energy and electricity will be available to the world’s entire population by 2030 — an assumption that depends on meeting the challenge of rapidly deploying clean technology infrastructure, development, and availability. (The IEA has pointed out that its proposed strategy is a pathway and not the pathway to the net zero goal.)

By contrast, the Arab Gulf states have quite a different perspective concerning the pathway to net zero. For the Gulf states, monetizing hydrocarbon assets is a top priority for maintaining national security.[11] As such, their strategy is to maximize hydrocarbon exports to sustain the stability of their local economies and related international political and economic affairs.[12] Despite their ambitious transition energy projects and goals, economic structures in the Gulf states — i.e., their hydrocarbon-based economies — essentially remain unchanged. Thus, an energy transition agenda that phases out fossil fuels, particularly oil and gas, is not favored by the Gulf states.

Figure 2 — The IEA's Proposed Pathway for Achieving Net-zero Emissions by 2050

The leaders of the Arab Gulf states have outlined their approach to reaching near- or net-zero carbon emissions on several occasions.[13] It can be summarized into three main pillars:

- Do not disrupt oil and gas markets. The Gulf states have stressed the importance of adopting a “balanced” approach to climate change that promotes sustainability, energy security, and economic prosperity. They argue that developing nations need reliable and affordable energy sources to achieve their developmental goals, and moreover that developed countries need stable energy markets to fuel their economies.

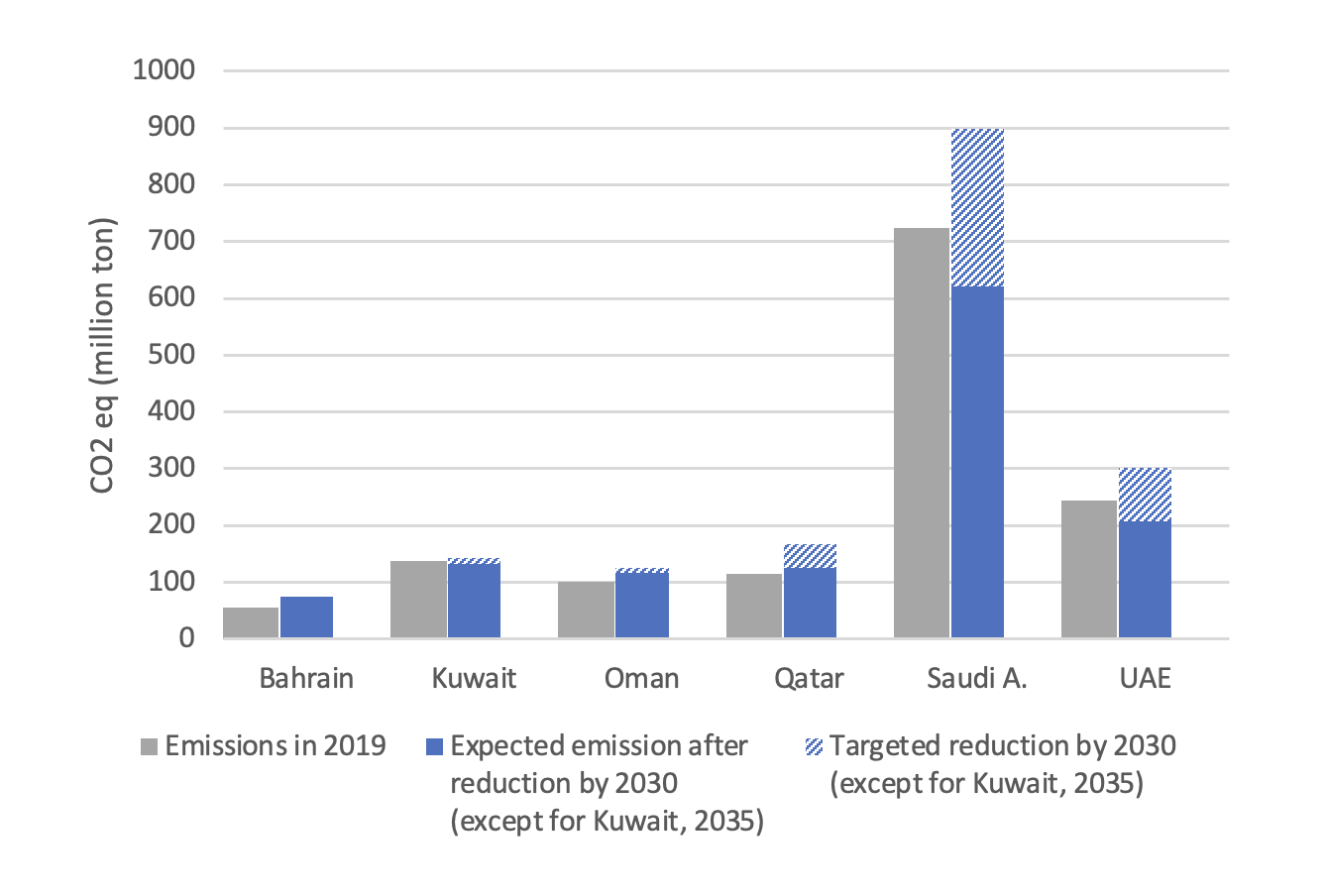

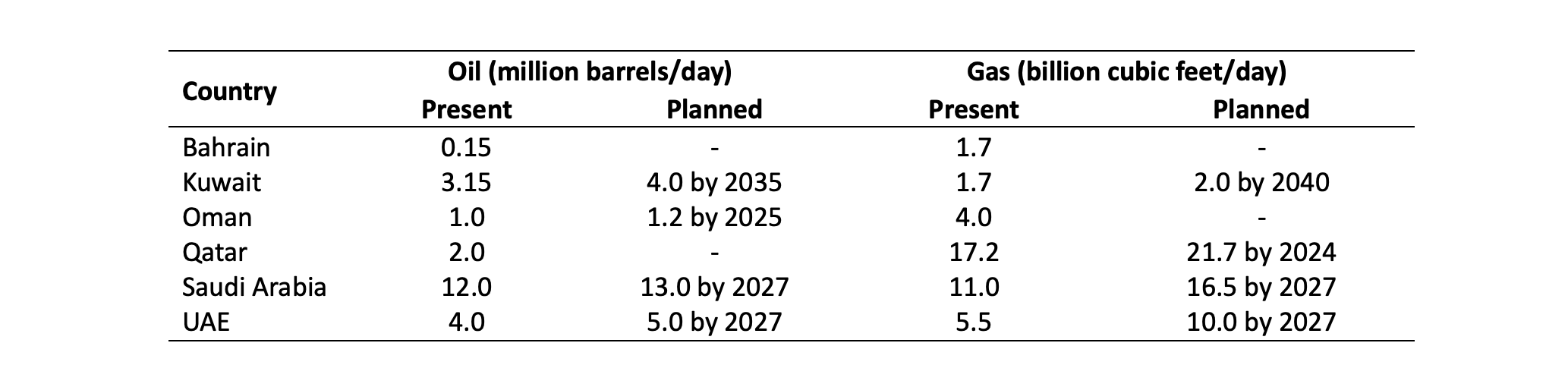

As such, from their perspective, it is vital for the Gulf states to continue to invest in oil and gas and avoid jeopardizing global energy security and increasing inflation — which would eventually slow the transition to a sustainable clean energy system. Although they have announced ambitious climate targets (see Figure3), the Gulf states are keen to expand their oil and gas production capacities to meet their economic and developmental goals (Table 1).

Moreover, the Gulf states believe developed countries must fulfill their climate finance pledges if they seek a faster transition to clean energy in developing countries. In 2009 at COP15, leaders of developed nations committed to mobilize $100 billion annually by 2020 to assist developing countries in addressing climate change. To date, the promised annual climate finance fund — which experts have since found insufficient to meet the needs of developing nations[14] — has not been met.

- Transition Gradually. The Gulf states have also disputed the call to immediately replace oil and gas with alternative renewables and clean fuels, contending that the world should first achieve a practical and realistic transition using its current energy sources. This was expressed by al-Jaber at the Copenhagen Climate Ministerial Meeting in March 2023: “The work focus should be on stopping emissions and not abandoning the current energy system before the future energy system is ready.”[15]

Transitioning from the present conventional system to a net- or near-zero emissions energy system requires supporting infrastructure, competent technology, and committed financing. The latter is vital to assure an effective transition without disrupting economic development globally.

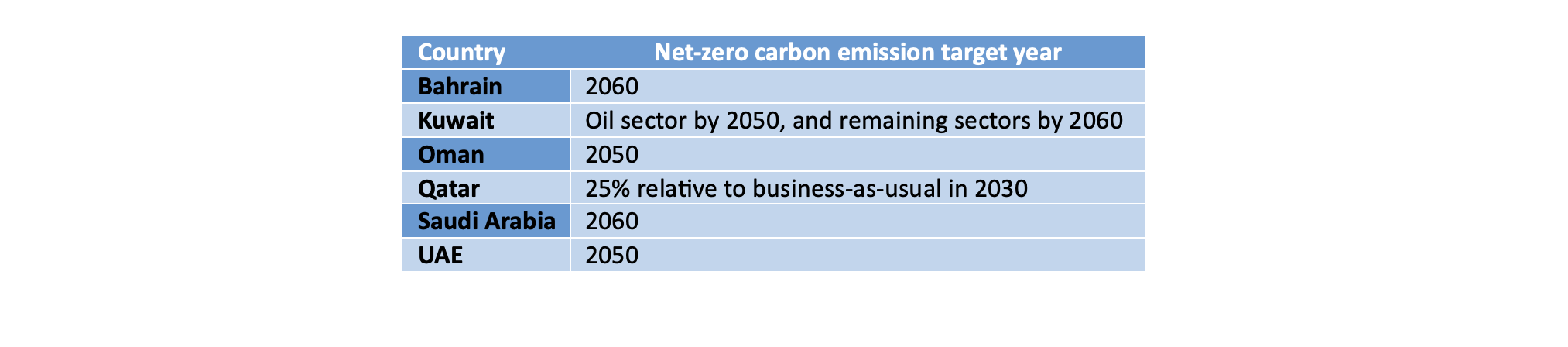

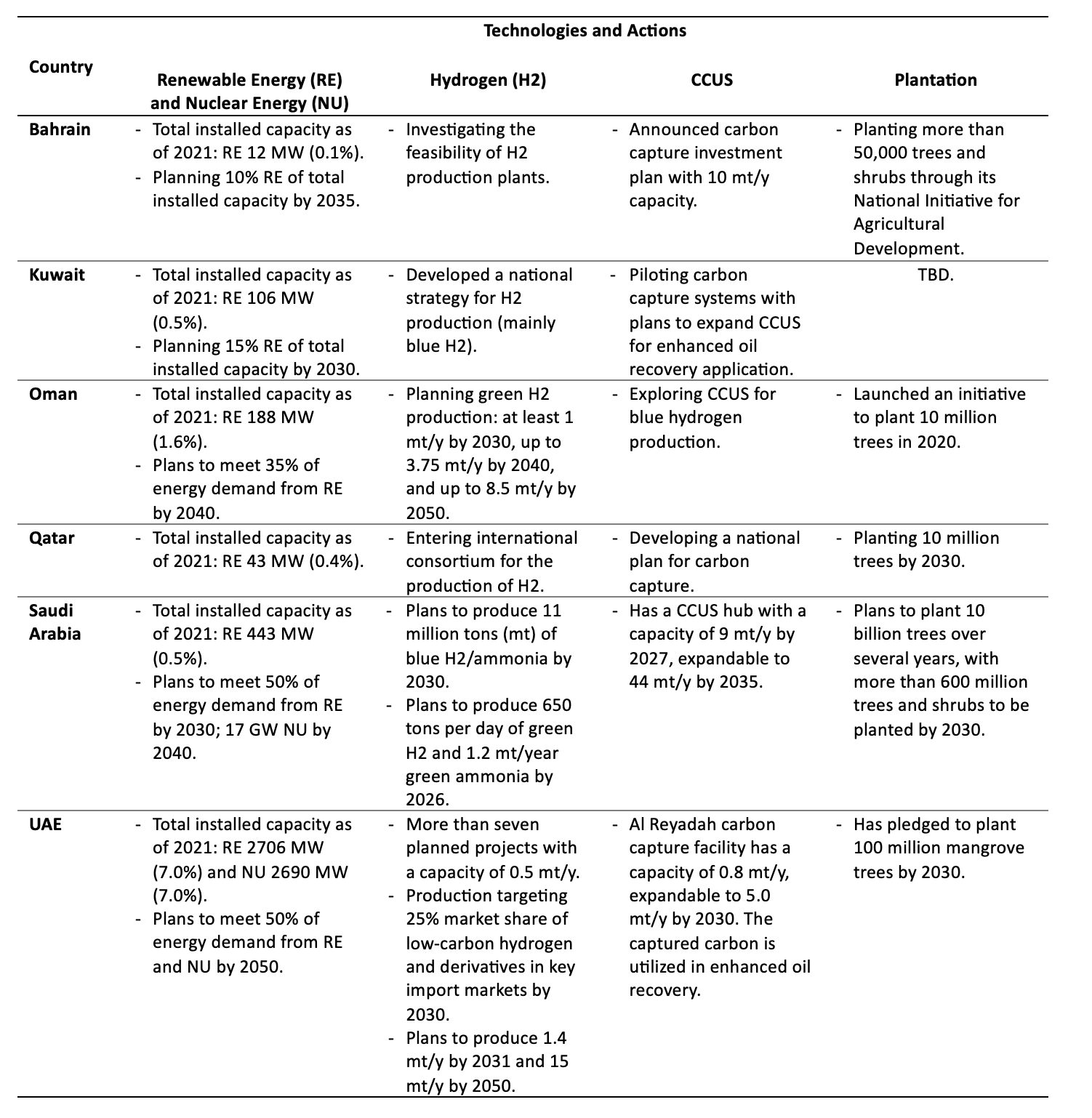

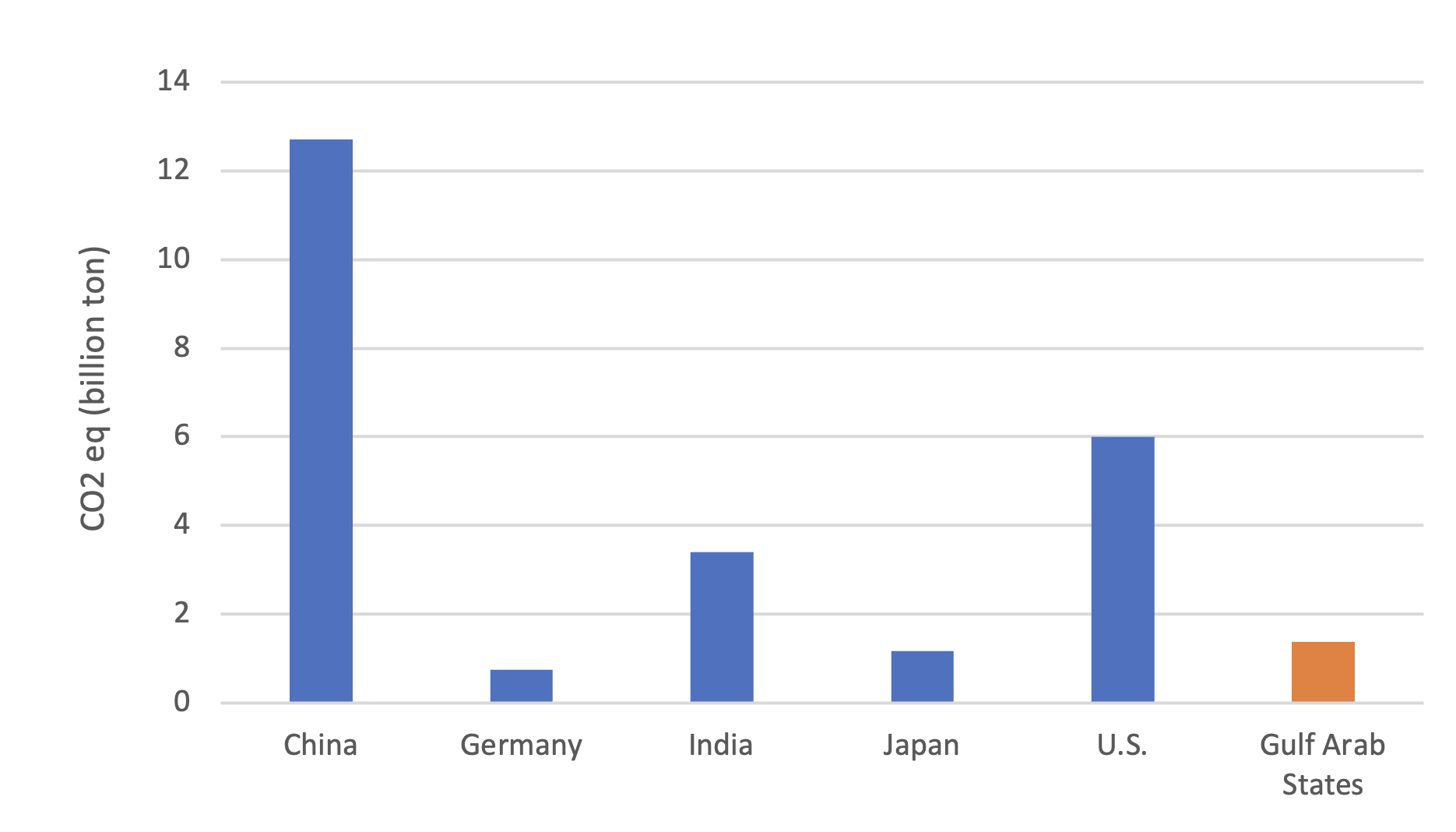

- Integrate clean technologies into energy systems. The Arab Gulf states do not intend to give up the fuel resources that make up their current energy system, including oil and gas. Rather, their strategy for mitigating carbon emissions is to integrate hydrocarbon-fired facilities with clean energy systems and diversify the energy mix, using renewables, hydrogen, nuclear power, plantations, and carbon capture, utilization and storage (CCUS). Although greenhouse gas emissions in the Gulf states are relatively low (Figure 4), they have already begun work to achieve their announced targets (Table 2).

In summary, while the Gulf states support the world's endeavor to limit the global temperature increase to 1.5 degrees Celsius above preindustrial temperatures, their plans for achieving this target differ from those of many developed nations. Given their high economic dependence on hydrocarbon exports, the Gulf states are not motivated to rule out oil and gas from their ventures — local or global — to reach the net-zero emissions goal. This is accordingly reflected in their foreign policy.

Figure 3 — Greenhouse Gas Emission Plans of the Arab Gulf States: (a) Historical and Expected Future emissions; (b) Net-zero Carbon Emissions Targets[16]

(a)

(b)

Table 1 — Present and Planned Oil and Gas Production Capacity

Table 2 — Endeavors to Integrate Clean Technologies and Mitigate Emissions Among the Arab Gulf States[17]

Note MW = megawatts; GW = gigawatts; mt/y = megatons (1 million tons) per year.

Figure 4 — Comparison of CO2 Equivalent Emissions: Arab Gulf States Versus Developed/Industrialized Countries, 2019

3. Transitioning to Net Zero as Fossil Fuel Financing Continues

The international community has come to the consensus that the only way to combat global warming effectively is to reduce greenhouse gas emissions. Through annual conferences like the United Nations Climate Change Conference of the Parties (COP), governments and other stakeholders have come together to negotiate and propose solutions to achieve this goal.

The 2015 Paris Agreement was a major milestone that saw countries in attendance adopt a legally binding treaty on climate change. The agreement, which entered into force in November 2016, established a framework for countries to commit to reducing their emissions and work together to limit global warming to well below 2 degrees Celsius above preindustrial levels. Some developed countries (mainly in Europe) have prominently called to limit global warming by phasing out fossil fuels from the energy sector.

COP27, held in Sharm El Shaikh, Egypt, in November 2022, only partially addressed the fossil fuel issue. Instead, the meeting focused primarily on establishing a dedicated fund to finance developing countries facing the catastrophic effects of climate change.[18] At COP15 in Copenhagen in 2009, rich, developed countries pledged $100 billion for climate action in low-income, developing countries. The commitment was supposed to be met by 2020, but only $83.3 billion had been delivered by 2020 — falling $16.7 billion short of the target.[19]

Currently, there are two distinct energy transition pathways. One, which has been advocated for by some developed nations, seeks to end the activities that cause climate change and, to a lesser extent, finance efforts to mitigate climate change-related damages in developing nations. The other pathway has been promoted mainly by developing countries, including net fossil fuel exporters. It prioritizes efforts to finance climate change loss and damage and to mitigate emissions by integrating clean technologies into the energy sector to sustain developmental economic plans. Financing is therefore critical for both pathways, whether the aim is to continue investing in the fossil fuel sector or not.

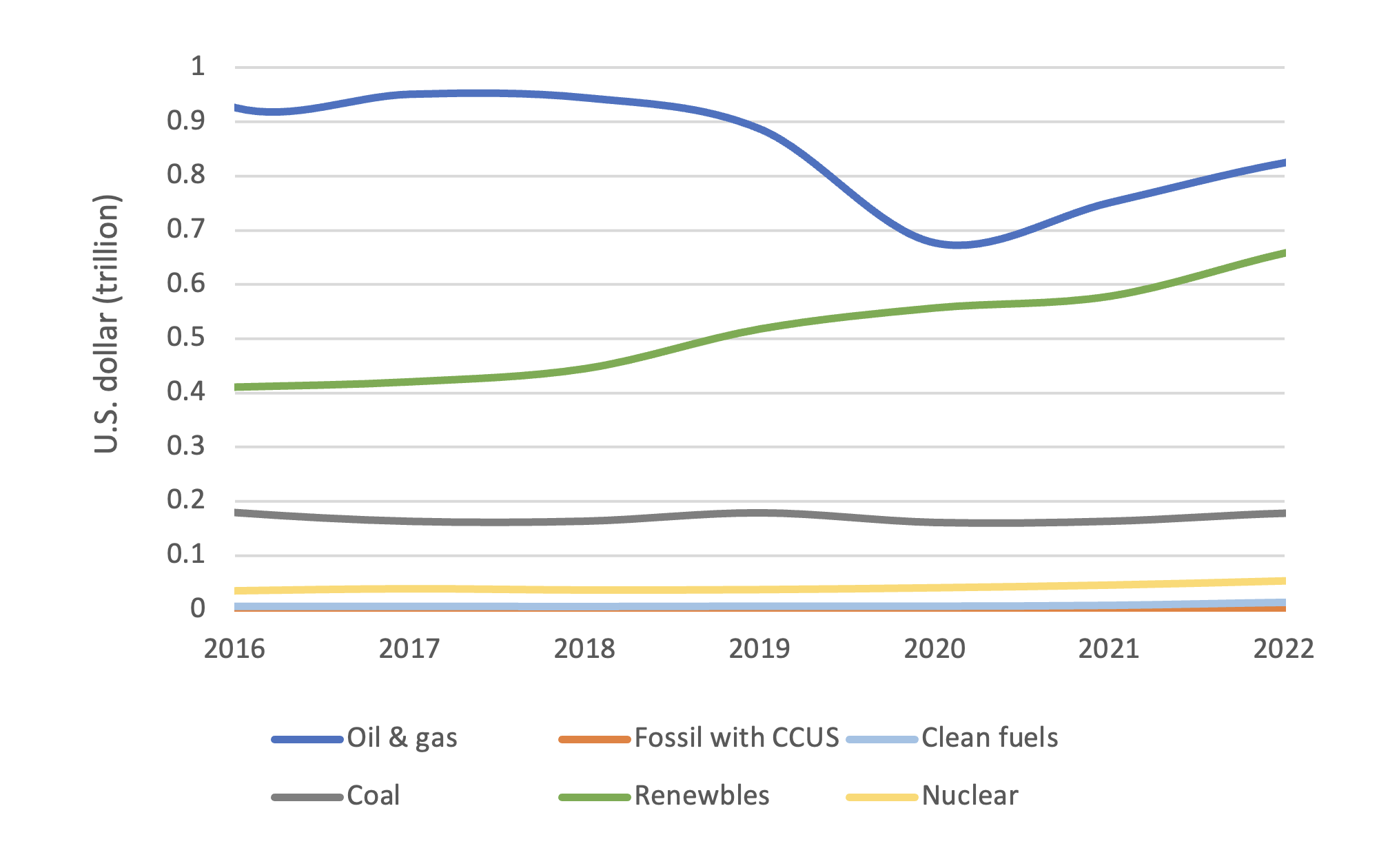

Since the Paris Agreement entered into force in 2016, the level of investment in fossil fuels has remained relatively stable (Figure 5). Oil and gas investments plateaued, dipped during the COVID-19 pandemic, and then increased after 2021. From 2016-2022, accumulated investments in oil and gas, including upstream, midstream, and power applications, were $5.9 trillion. Investments in 2023 are estimated at $869 billion.[20]

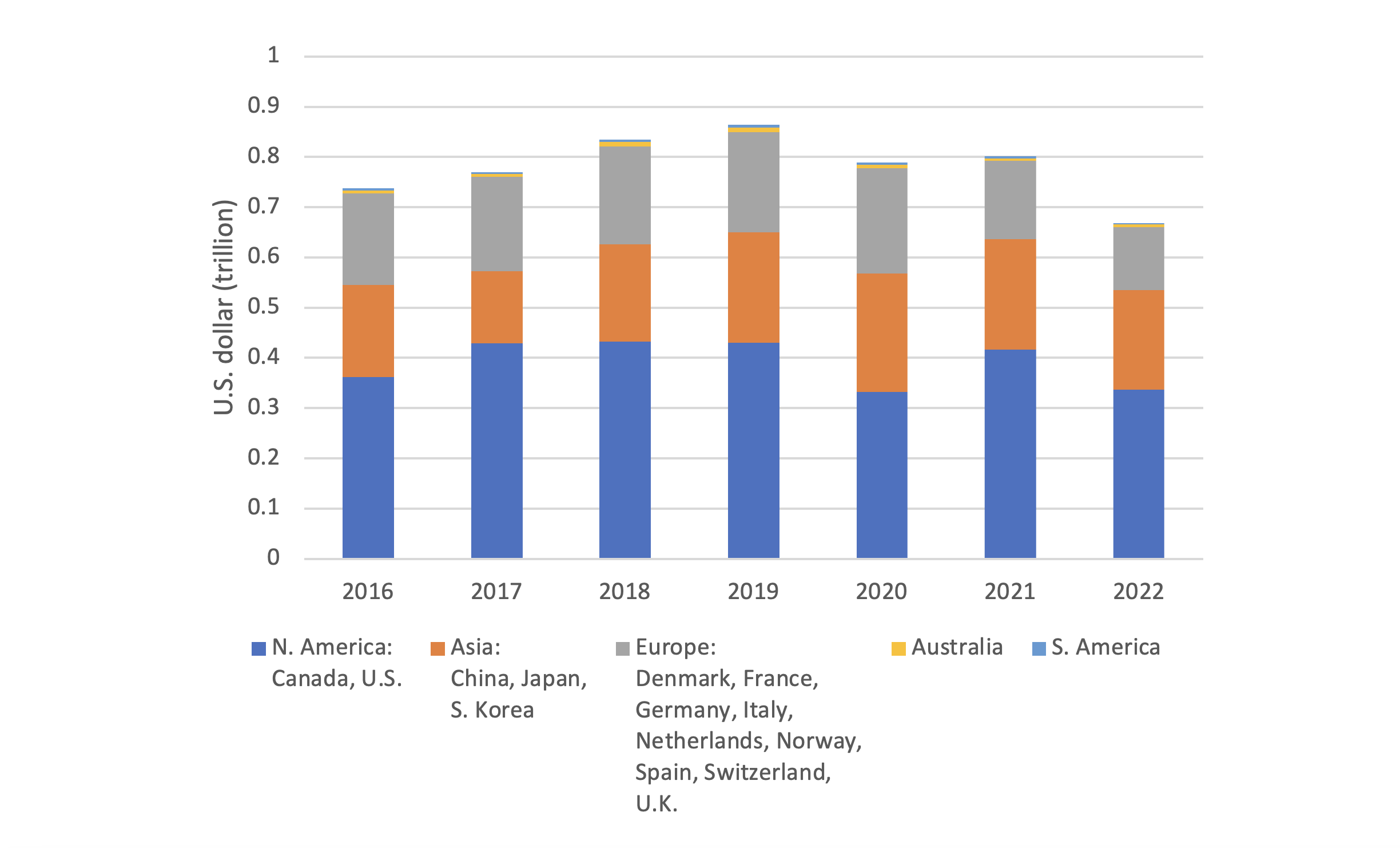

The headquarters of the top 60 financial institutions and banks that finance fossil fuel projects are primarily located in developed and industrialized countries, with the vast majority of funds coming from North America (50%), Asia (25%), and Europe (23%) (Figure 6).[21] Most of these banks have announced policies to restrict financing for fossil fuel projects, but to date the policies have either proven ineffective or not been executed.

Notably, most of the major banks that finance fossil fuel projects are in countries whose governments persistently advocate for phasing out fossil fuels from the global energy sector. These banks, however, are highly influenced by their shareholders, who mostly push for profit maximization and economic growth.

The Arab Gulf states contribute significant amounts of capital to banks and global financial institutions. Their international investments are recognized for driving economic growth and providing liquidity to the global financial system. As previously discussed, their financial capital is mainly fueled by oil and gas revenues, and thus their interest is in pursuing a pathway to net zero that sustains the use of oil and gas to meet the world's energy needs.

Figure 5 — Global Energy Sector Investments

Figure 6 — Headquarter Locations of Major Banks Financing Fossil Fuel Projects

4. The Key Role of Arab Gulf States in Global Financial Sector

The Gulf states have become key actors that cannot be overlooked in the international arena. Their robust financial position (Figures 7 and 8) has given them a soft power vehicle to protect their interests and achieve their national security goals. Within the Middle East and North Africa (MENA), the Gulf states’ capitalism and financing tools — e.g., financial aid, infrastructure investments, and equity shares in local financial and commercial institutions — allow them to influence, both directly and indirectly, the political economies of various countries and territories, including Egypt, Lebanon, Palestine, Sudan, Tunisia, and Yemen.[22]

These tools enable the Gulf states to expand their influence beyond the Middle East and reach most of the globe. However, they use their roles and leverage differently in developed and industrialized nations. There, they pursue other goals, mainly to support their political stability and economic prosperity.[23]

The Arab Gulf states’ political economies and international political influence have been the subject of extensive study.[24] Below, I use findings from this research to help evaluate the Gulf states’ influence on the global energy transition.

From the late 1980s to the early 2000s, the U.S. was the world’s dominant political and economic power. By the 2010s, China and India had emerged as new competitors. In this new era, the Gulf states have increased their hydrocarbon exports to the East, maintaining Asia's goods production renaissance. For example, China's oil imports increased from 0.68 million barrels per day (mb/d) in 1993 to 12.7 mb/d in 2021, while its natural gas imports rose from 1 billion cubic meters (bcm) in 2006 to 94 bcm in 2020. In 2021, about 28% and 14% of China’s oil and natural gas imports, respectively, were sourced from the Gulf region.[25]

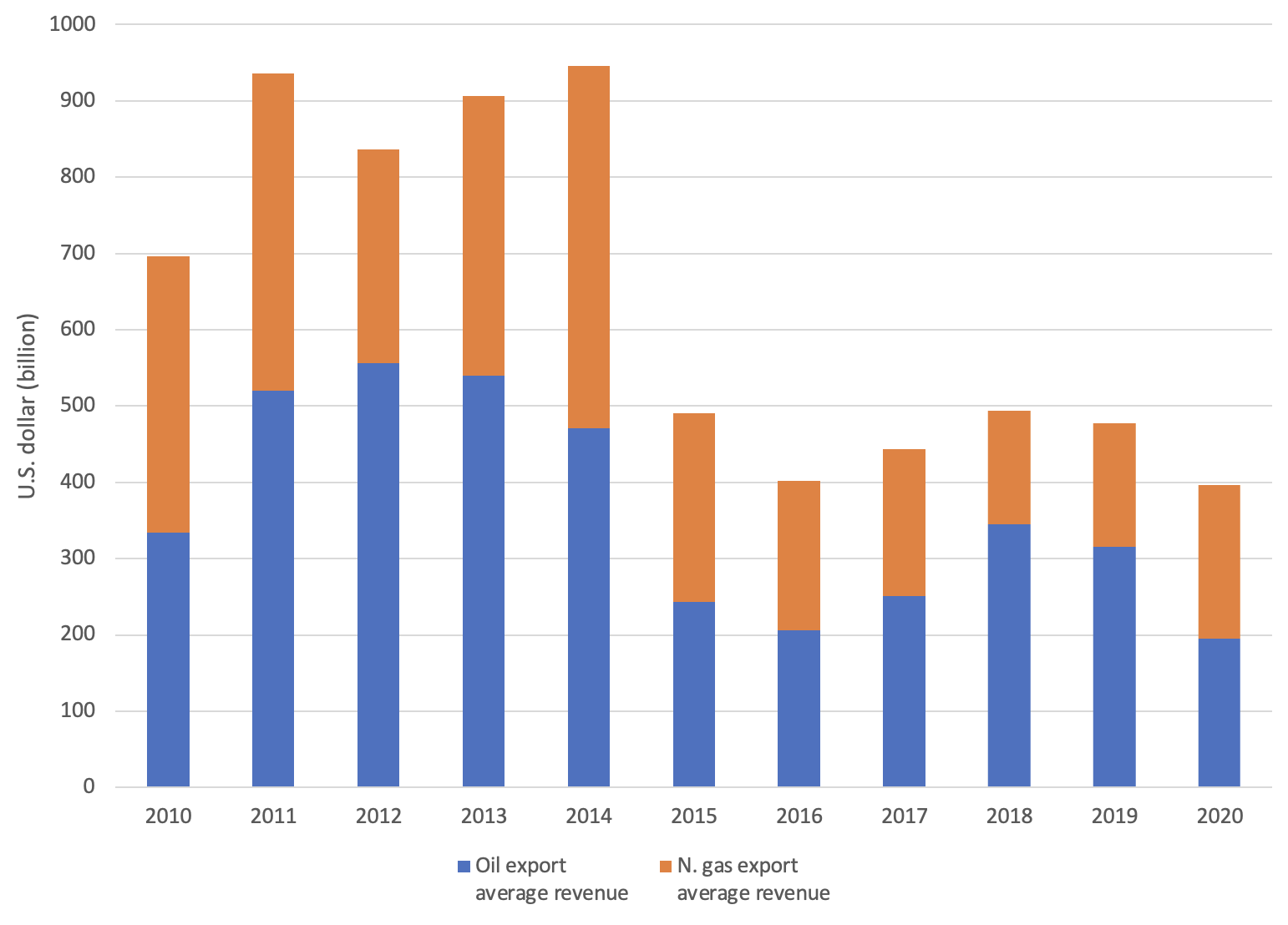

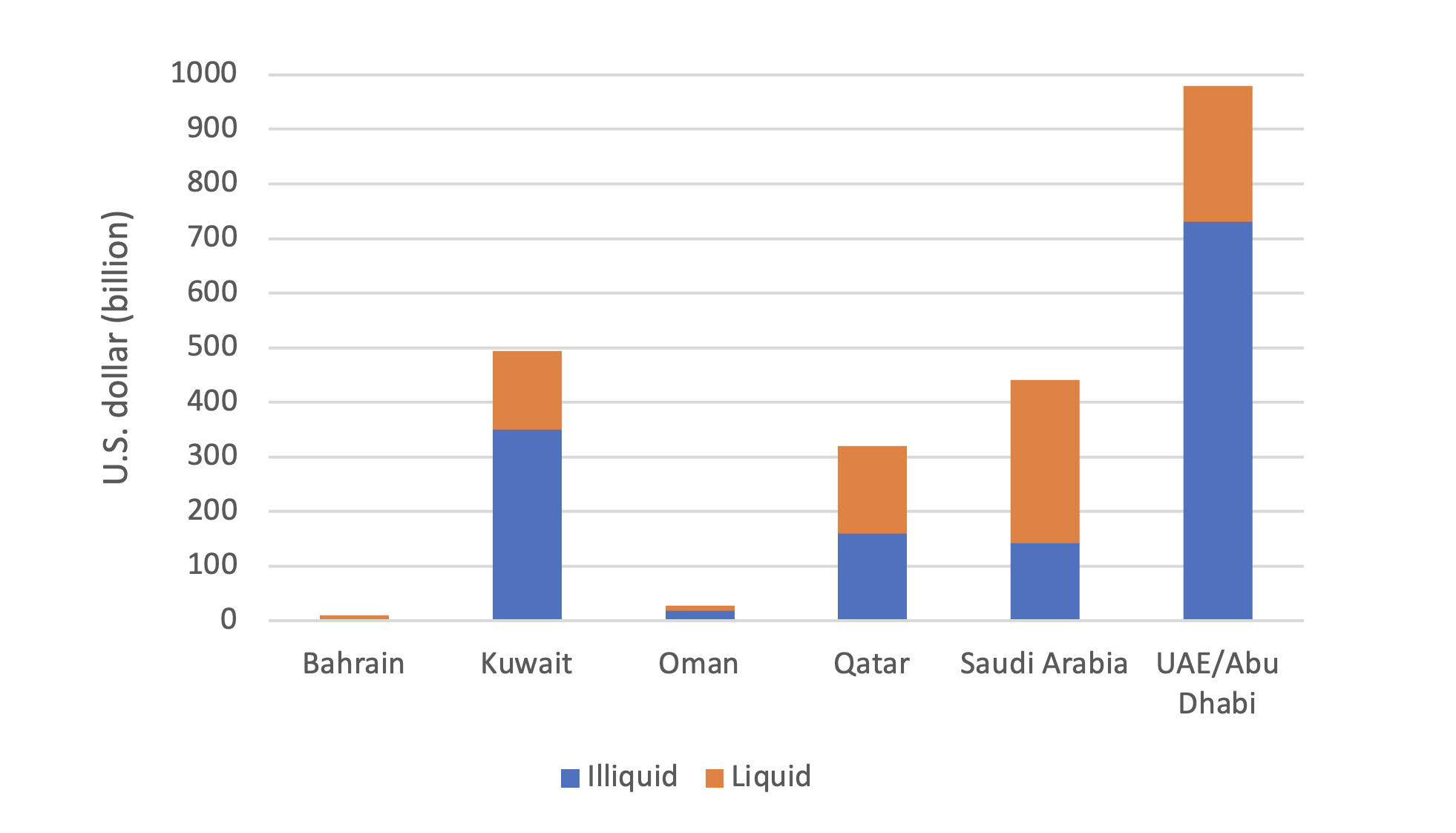

The Gulf has become a pivotal force in the world economy. Its petrodollars have helped maintain the stability of global economic balances, the supremacy of the U.S. dollar, and the central role of the U.S. economy in global consumption. Petrodollar flows have been used in U.S. and European financial markets to make loans and purchase stocks, bonds, real estate, and other assets.[26] Accumulated revenues from oil and gas exports between 2010 and 2020 are estimated at more than $7 trillion (Figure 7). These revenues are the primary source of the Gulf states’ sovereign wealth funds (SWFs), which are an active component of the region’s international investments. These investments are estimated at $2.3 trillion (Figure 8). The Gulf’s investments are roughly distributed as follows: 50% in the U.S., 20% in Europe, 15% in Asia, and 15% in the MENA region.[27]

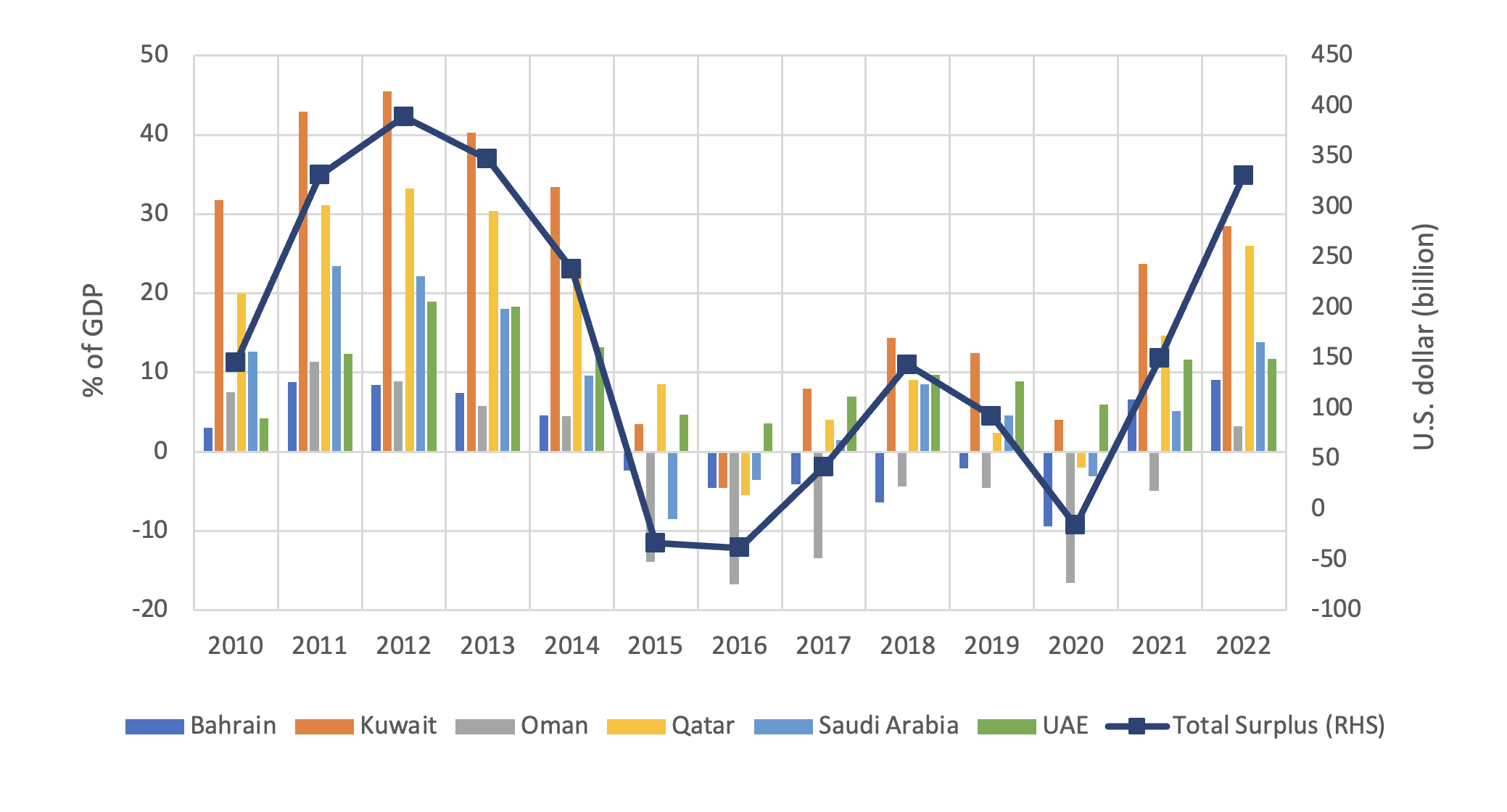

It is essential to note that part of the Gulf states’ petrodollar surpluses (Figure 9) flow into global financing institutions, particularly in the U.S. and Europe. These institutions include Barclays, Citigroup, Credit Suisse, the New York Stock Exchange, and the London Stock Exchange.[28] The condition of the global financial and monetary system is closely linked to global market performance. Hence, when markets face risks such as inflation, pandemics, geopolitical tensions, and crashes, the financial system is the main backbone mitigating the negative impacts. The Gulf states’ petrodollar surpluses have played a vital role in backing up the global financial system and stabilizing world markets, at least partially.

Thanks to their financial solvency — and resulting economic development, infrastructure projects, and high levels of wealth — the Gulf states offer attractive market opportunities for international banks. As a result, major international banks have established a strong presence in the region to tap into these opportunities and benefit from the Gulf’s financial markets, corporate clients, and wealthy individuals.[29]

The engagement and influence of the Gulf states in the international financial system is sustained by their large oil and gas revenues, resulting trade, and large international investments made possible by account surpluses.[30] Economic or financial instability in the Gulf would have ripple effects on major international financial institutions; as such, oil price fluctuations, regional conflicts, geopolitical tensions, and other developments in the Gulf can impact the stability of the global financial system.

Gulf financing plays a key role in financial markets, and, accordingly, impacts the pathways chosen by international financing institutions.

Figure 7 — Average Annual Oil and Gas Export Revenues Among the Arab Gulf States

Figure 8 — Sovereign Wealth Fund Estimated Assets in the Gulf

Figure 9 — Account Surplus Profiles Among Arab Gulf States, 2010-2022

5. The Gulf States’ Energy Diplomacy

Energy diplomacy refers to diplomatic and strategic endeavors to manage and influence the international production, distribution (export and import), and consumption of energy resources.[31] It involves cooperation and competition between nations to secure access to energy supplies and markets, promote energy security, and pursue national interests in the energy sector.

The energy diplomacy of the Gulf states has primarily revolved around ensuring a steady flow of hydrocarbon exports at prices that can support their fiscal budget, strategic economic growth, and national security. As such, they do not support the energy transition pathway to net zero — which would see policies adopted to phase out fossil fuels — and instead utilize diplomacy to seek a pathway that instead keeps oil and gas in the energy sector and focuses on integrating clean technologies to mitigate the impacts of climate change.

The Gulf states also employ their energy diplomacy to maintain their desired hydrocarbon price range. This is evident through their leadership in OPEC and OPEC+, a group of oil-producing nations that has allied with OPEC since 2016 (Saudi Arabia is a leader among both groups). Because net exporters of oil — including the Gulf states —interpret a rise in oil stocks as a sign of slack in supply/demand, and a fall in oil stocks as a sign of supply/demand tightness,[32] the region’s diplomacy has manifested to balance the oil market between supply and demand and avoid accumulation in the oil stock in order to serve its interests. Moreover, the Gulf states’ influence on production levels, prices, and the international response to energy crises is similarly apparent through its influence on the Gas Exporting Countries Forum (GECF)[33] and the IEA.[34]

The Gulf states’ energy diplomacy is also demonstrated by the continued demand for their hydrocarbon resources. The region secures demand by investing in and partnering with global downstream facilities to ensure its products are prioritized. For example, national oil company Saudi Aramco is strengthening its operations in Asia and Europe by pursuing various expansions, including acquiring a 30% share in a refinery in Gdansk, Poland (with a daily capacity of 210,000 barrels), and sole ownership of an associated wholesale business. The company has also entered into an agreement involving a 50% stake in a joint venture with BP for marketing jet fuel in Poland. Saudi Aramco also aims to participate in the development of a significant integrated refinery and petrochemical complex in China.[35]

Similarly, the UAE’s ADNOC has entered into an oil refining partnership with Italian multinational company Eni and Austrian company OMV. Eni and OMV have acquired 20% and 15% shares in ADNOC refining, respectively, with ADNOC owning the remaining 65%. In this way, some Gulf states are securing demand from African, Asian, and European markets.[36]

The Gulf region also uses long-term contracts with both traditional and emerging energy markets to ensure stable demand for their resources. For example, Qatar has signed two long-term gas supply deals with China. The most recent deal, a 27-year contract for 4 million metric tons of liquefied natural gas (LNG) annually, was announced in June 2023. The contract was signed between Qatar Energy and China National Petroleum Corporation (CNPC). CNPC will also take an equity stake in the eastern expansion of Qatar’s North Field LNG project. An earlier deal, another 27-year supply agreement for 4 million tons of LNG a year between Qatar Energy and China’s Sinopec, was announced in November 2022.[37] Qatar Energy also signed a 15-year deal with German firms to supply 2 million tons of LNG annually in late 2022, with deliveries set to start in 2026.[38]

As for the emerging markets, in the second quarter of 2023 Qatar Energy signed an agreement with Bangladesh's PetroBangla to supply an additional 1.8 million tons of LNG annually for the next 15 years starting in 2026.[39] Under an existing deal signed in 2017, Bangladesh has been importing 1.82 to 2.5 million tons of LNG annually since 2018.[40]

The Gulf states are aware of the long-term challenges associated with heavy reliance on oil and gas fuels. As part of their energy diplomacy, they seek to diversify their economies by investing in renewable energy sources, promoting sustainable industries, and encouraging foreign direct investment (FDI) in sectors beyond oil and gas. Through these efforts, they aim to reduce their vulnerability to fluctuations in global energy demand and portray themselves as protecting and caring for the environment.

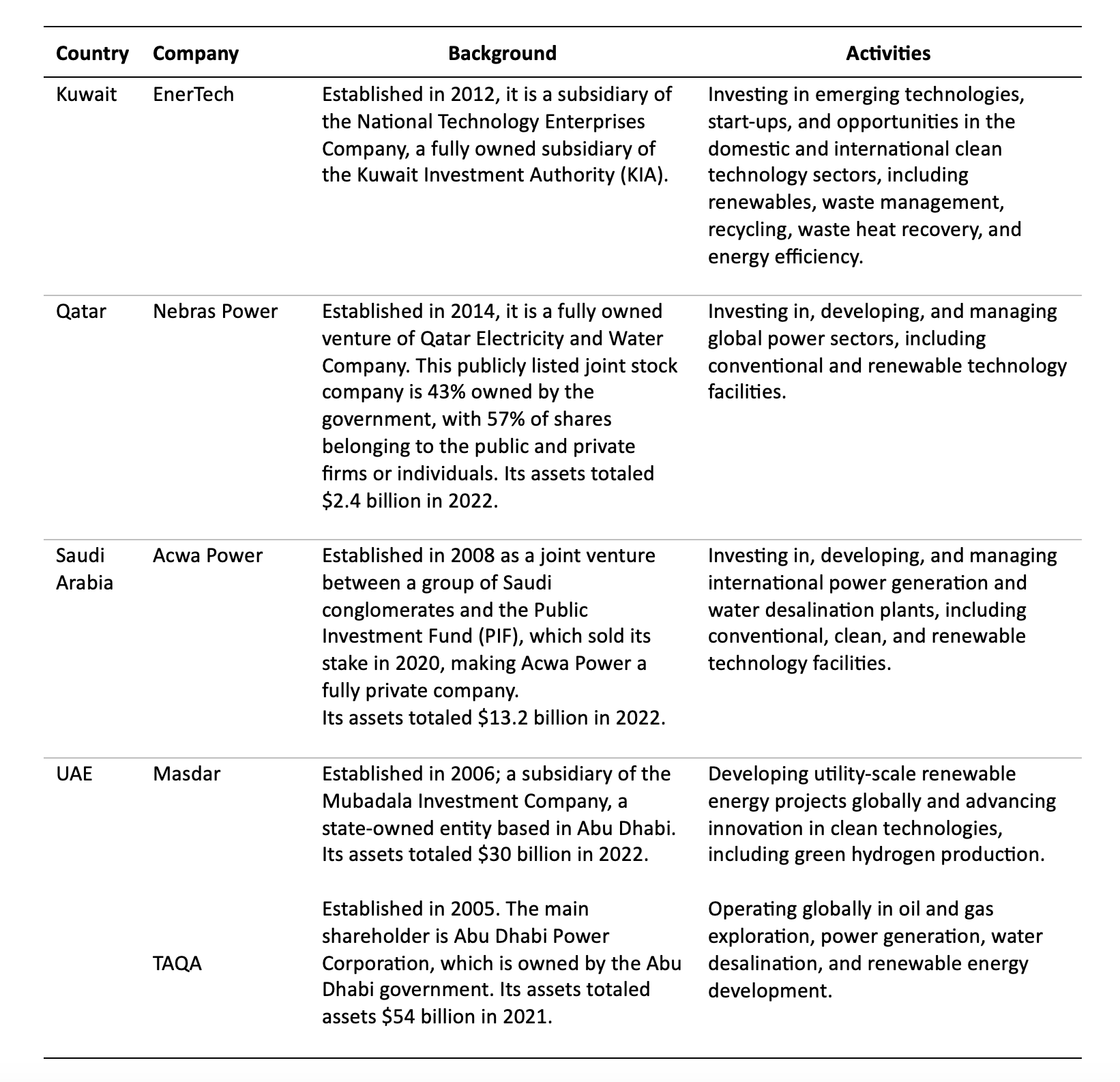

State-owned and national clean energy companies (Table 3) have been established in the Gulf with missions to fulfill the aforementioned goals. These companies develop and deploy sustainable energy solutions and technologies and aim to promote the adoption of renewables, clean energy, and emissions-controlled fossil fuel systems. They operate across various sectors of the clean energy industry, including renewables, hydrogen, energy storage, CCUS, and sustainable urban development.

Meanwhile, the Gulf states are investing in clean technologies and operating environmentally friendly facilities that generate carbon credits — a financial instrument designed to reduce greenhouse gas emissions. One carbon credit represents 1 metric ton of carbon dioxide removed or reduced from the atmosphere; companies can earn credits through a variety of clean energy activities and clean technology projects, such as renewable energy, hydrogen, and CCUS.

In 2022, Abu Dhabi Global Market revealed its intent to establish a carbon-trading exchange and clearinghouse in Abu Dhabi and create the world's first fully integrated platform for carbon trading transactions. This announcement came after Saudi Arabia's Public Investment Fund (PIF) and the Saudi Tadawul Group launched a voluntary carbon credit exchange for certain credits in October 2022.[41]

Table 3 — State-owned and National Clean/Semi-clean Energy Companies in the Gulf

In sum, the energy diplomacy of the Arab Gulf states revolves around maintaining global oil/gas demand, sustaining reasonable oil price levels, promoting clean-fossil integrated systems, and mitigating the effects of climate change.

Discussion

More broadly, the global economy continues to strive for growth — developing nations in particular. Economic growth is not only about maintaining or improving living standards, promoting innovation and technological advancement, and creating jobs and business opportunities. Critically, economic growth also reduces poverty, supplies basic needs to hundreds of millions in the Global South, and sustains social development.

Developed and developing countries alike require stable and affordable energy sources to grow their economies. Accordingly, as the world economy grows, its energy consumption rises, and it thus seeks all possible energy extraction technologies to maximize energy outcomes. In this economic context, the only reason to phase out an energy source is to address inefficiency — i.e., where there is a low energy outcome relative to high input resources.

Banning fossil fuels from the world's energy sector would undermine the world's economic growth goals, at least in the foreseeable future. To date, renewable and clean energy technologies have not replaced or decreased the rate of fossil fuel extraction. Rather, renewables and clean energy have complemented the world's energy mix and prolonged the use of fossil fuels to promote economic growth.[42]

Despite the threat of climate change and the expanding list of energy alternatives to mitigate greenhouse gas emissions, the global economic system will naturally avoid pathways that disrupt its growth process, especially if they rule out a primary, mature, stable, and efficient energy source. Instead, it will seek paths that increase efficiency and reduce greenhouse gas emissions by increasing the proportion of clean energy in the energy mix, integrating clean technologies into the energy sector, and enhancing energy efficiency measures.

Although many banks have embraced net zero commitments as their key approach to tackling climate change, their readiness to finance the fossil fuel value chain (see again the trends in Figures 5 and 6) has persisted due to the “invisible hand,” or the unseen economic forces that continue to demand increasing amounts of energy in order to meet desired growth.[43] The Gulf states’ wealth — comprising SWFs and worldwide investments and assets — is central to growing the world economy. It is not easy to determine the administrative role the Gulf states play in the bank financing of fossil fuel projects (Figure 6). However, they have direct investments in global banks, including some that invest in fossil fuels, such as Barclays, Citigroup, Credit Suisse, and HSBC.[44]

By financing these institutions and large-scale deals, such as infrastructure projects, acquisitions, and corporate expansions worldwide, the Gulf indirectly plays a role in maintaining stability in the financial sector.[45] Moreover, as major trading hubs with strong international trade links, the Gulf states collaborate with international banks on trade finance services. For example, they support cross-border transactions, facilitate trade flows, and provide access to global banking networks.

There is no one region or cluster of nations that can push the world to deviate from its commitment to economic growth. The Gulf states' interest in maintaining demand for their oil and gas products aligns with this mainstream goal, particularly in the Global South. They use their wealth and diplomacy to keep oil and gas in the world’s energy sector. Along with developing nations, the Gulf states indirectly promote a pathway to net zero that does not disrupt global economic growth or jeopardize their national security.

Conclusion

Despite the investments and ambitions for low-carbon emission energy systems of their own countries, some critics — including European and U.S. legislators — have argued that as major producers and exporters of oil and gas, the Gulf states have consistently resisted efforts to set more determined climate goals, instead working to maintain the status quo and protect their economic interests in the oil and gas industry. This research investigated the extent of the Gulf states’ influence on the world’s efforts to achieve net-zero greenhouse gas emissions.

The paper reviewed the Gulf’s two central influencing factors — financial reach and energy diplomacy — and assessed their impacts on the energy transition agenda. The region has become pivotal for the world economy, helping to maintain global economic stability. Between 2010 and 2020, its oil and gas exports generated over $7 trillion, and its SWF investments are distributed worldwide. Its petrodollars have been invested in various financial markets through loans, stocks, bonds, real estate, and other assets.

Some of the Gulf states’ petrodollar surpluses flow into the world’s major financing institutions, mostly in the U.S. and Europe. These institutions are compelled to maximize profits for shareholders, supporting and promoting the goal of growing the global economy. Gulf state investors may not explicitly direct these financial institutions to continue investing in oil and gas projects, but many of them are also shareholders whose goal is to maximize profits. They thus seek to expand the energy sources available to fuel economic growth. As such, it is in the Gulf states’ interest to pursue a pathway to net zero that keeps oil and gas in the energy sector, and their energy diplomacy accordingly serves as another major tool to secure and maintain their interests.

The Gulf states’ energy diplomacy has primarily revolved around ensuring a steady flow of hydrocarbon exports at prices that support their fiscal budget, promote strategic economic growth, and, as a result, safeguard their national security. Their leadership in OPEC and OPEC+ — particularly that of Saudi Arabia — demonstrates their influence over oil prices and ability to maintain prices levels that meet their national interests. Their diplomacy has worked well in securing long-term contracts with both traditional and emerging energy markets to guarantee stable demand for their hydrocarbon products. Moreover, it enables them to strategically invest in and collaborate with downstream facilities worldwide to ensure the steady flow and prioritization of their products.

Recognizing the global political pressure to move toward clean and renewable energy, the Gulf states, mainly led by the UAE, are working through international organizations and partnerships like IRENA and UNFCCC to host clean energy conferences and summits, promote foreign investment in clean technologies, participate in green financing initiatives, support developing countries in technology transfer and capacity building, and invest in carbon credits.

The takeaway: Arab Gulf states employ their wealth and diplomacy to support the continued presence of oil and gas in the world’s energy sector. In doing so, they indirectly promote the adoption of their preferred global pathway to the net zero goal — a pathway that increases the proportion of clean energy sources in the energy mix, continues investment in oil and gas, and integrates clean technologies into the energy sector to mitigate emissions. Most critically, this energy transition agenda is in line with endeavors by developed and developing countries alike to sustain economic growth and development.

Endnotes

[1] Rola AlGhoul and Esraa Esmail, “Following presidential directive, Mansour bin Zayed appoints COP28 UAE President-Designate,” Emirates News Agency-WAM, January 12, 2023, https://wam.ae/en/details/1395303118224.

[2] Gloria Dickle and Kate Abnett, “US, EU lawmakers push to depose UAE's Jaber from climate talks,” Reuters, May 23, 2023, https://www.reuters.com/business/environment/us-eu-lawmakers-push-depose-uaes-jaber-climate-talks-2023-05-23/.

[3] Navin Singh Khadka, “COP28: Why has an oil boss been chosen to head climate summit?,” BBC, January 13, 2023, https://www.bbc.com/news/world-middle-east-64269436.

[4] “EU climate chief defends oil CEO’s appointment as COP28 boss,” EurActiv, January 16, 2023, https://www.eceee.org/all-news/news/eu-climate-chief-defends-oil-ceos-appointment-as-cop28-boss/.

[5] Jon Gambrell, “John Kerry says he backs appointment of UAE oil chief to lead COP28 climate talks,” PBS NewsHour, January 16, 2023, https://www.pbs.org/newshour/world/john-kerry-says-he-backs-appointment-of-uae-oil-chief-to-lead-cop28-climate-talks.

[6] Banking on Climate Chaos, Fossil Fuel Finance Report 2023, https://www.bankingonclimatechaos.org/.

[7] Intergovernmental Panel on Climate Change, Climate Change 2022 – Mitigation of Climate Change (Geneva: IPCC, 2022), https://www.ipcc.ch/report/sixth-assessment-report-working-group-3/.

[8] “The World Needs a Swift Transition to Sustainable Energy,” UN Climate Change News, January 19, 2021, https://unfccc.int/news/the-world-needs-a-swift-transition-to-sustainable-energy.

[9] International Renewable Energy Agency, Global Energy Transformation – A Roadmap to 2050 (Abu Dhabi: IRENA, 2018), https://www.irena.org/publications/2018/Apr/Global-Energy-Transition-A-Roadmap-to-2050.

[10] International Energy Agency, Net Zero by 2050: A Roadmap for the Global Energy Sector (Paris: IEA, 2021), https://www.iea.org/reports/net-zero-by-2050.

[11] Osamah Alsayegh, Kristian Coates Ulrichsen, Jim Krane, and Ana Martín Gil, Exploring the Energy Transition and Net-zero Strategies of Gulf Oil Producers, Conference report no. 05.11.23 (Houston: Rice University's Baker Institute for Public Policy, 2023), https://doi.org/10.25613/1XGY-DF16.

[12] Manal Shehabi, The Hurdles of Energy Transitions in Arab States (Washington, D.C.: Carnegie Endowment for International Peace, 2023), https://carnegieendowment.org/2023/05/03/hurdles-of-energy-transitions-in-arab-states-pub-89518.

[13] Osamah Alsayegh, How Economic and Political Factors Drive the Oil Strategy of Gulf Arab States — And What This Means in the Context of the Global Energy Transition, Research paper no. 01.09.23 (Houston: Rice University's Baker Institute for Public Policy, 2023), https://doi.org/10.25613/KPSA-QK94.

[14] Viktor Tachev, “COP27: Broken USD 100 Billion Promise of Climate Finance but New Hope For Loss and Damage,” Energy Tracker Asia, November 25, 2022, https://energytracker.asia/cop27-broken-usd-100-billion-promise-of-climate-finance-but-new-hope-for-loss-and-damage/.

[15] “Climate Ministers meet in Copenhagen to set the course towards COP28,” State of Green, March 13, 2023, https://stateofgreen.com/en/news/climate-ministers-meet-in-copenhagen-to-set-the-course-towards-cop28/; Saudi Arabia Aramco’s board chair statement at International Petroleum Technology Conference, February 2022, Dharan, Saudi Arabia.

[16] United Arab Emirates Portal, “UAE Net Zero 2050,” https://u.ae/en/information-and-services/environment-and-energy/climate-change/theuaesresponsetoclimatechange/uae-net-zero-2050; “Bahrain announces intention to bring carbon emissions to net zero by 2060,” Bahrain News Agency, October 24, 2021; Saudi and Middle East Green Initiatives, “Paving the way to net zero emissions by 2060,” https://www.greeninitiatives.gov.sa/about-sgi/sgi-targets/reducing-emissions/reduce-carbon-emissions/; The Sultanate of Oman’s National Strategy for an Orderly Transition to Net Zero, Oman’s Vision 2040, November 2022; “Qatar targets 25% cut in greenhouse gas emissions by 2030 under climate plan,” Reuters, October 28, 2021, https://www.reuters.com/business/cop/qatar-targets-25-cut-greenhouse-gas-emissions-by-2030-climate-change-plan-2021-10-28/; “Kuwait committed to reaching carbon neutrality by 2050,” Kuwait News Agency, November 7, 2022, https://www.zawya.com/en/projects/industry/kuwait-committed-to-reaching-carbon-neutrality-by-2050-fm-r3dkoq4b.

[17] Kuwait Foundation for the Advancement of Sciences, Towards a Hydrogen Strategy for Kuwait (Kuwait City: KFAS, 2021); International Renewable Energy Agency, Renewable Capacity Statistics 2022 (Abu Dhabi: IRENA, 2022); UAE Hydrogen Leadership Roadmap (United Arab Emirates Ministry of Energy & Infrastructure, 2021).

[18] United Nations Framework Convention on Climate Change, “Five Key Takeaways from COP27,” https://unfccc.int/process-and-meetings/conferences/sharm-el-sheikh-climate-change-conference-november-2022/five-key-takeaways-from-cop27.

[19] OECD, “Climate Finance and the USD 100 Billion Goal,” September 22, 2022, https://www.oecd.org/climate-change/finance-usd-100-billion-goal/.

[20] International Energy Agency, World Energy Investment 2023 (Paris: IEA, 2023), https://www.iea.org/reports/world-energy-investment-2023.

[21] Banking on Climate Chaos, Fossil Fuel Finance Report 2023.

[22] Karim Mezran and Sabina Henneberg, Gulf Influence in the Maghreb (Washington, D.C.: New Lines Institute for Strategy and Policy, 2022), https://newlinesinstitute.org/north-africa/gulf-influence-in-the-maghreb/; Marcelle M. Wahba, The Role of the Gulf Arab States in a Transforming Middle East (Washington, D.C.: The Arab Gulf States Institute in Washington, 2017), https://agsiw.org/role-gulf-arab-states-transforming-middle-east/; Valeria Talbot, “The Gulf States’ Political and Economic Role in the Mediterranean,” Yearbook 2011 (Barcelona: European Institute of the Mediterranean, 2011), https://www.iemed.org/publication/the-gulf-states-political-and-economic-role-in-the-mediterranean/.

[23] Cinzia Bianco, A Gulf apart: How Europe can gain influence with the Gulf Cooperation Council (European Council on Foreign Relations, 2020), https://ecfr.eu/publication/a_gulf_apart_how_europe_can_gain_influence_with_gulf_cooperation_council/; Rauf Mammadov, Why the Gulf states are investing in Central Asia and the South Caucasus (Washington, D.C.: Middle East Institute, 2019), https://www.mei.edu/publications/why-gulf-states-are-investing-central-asia-and-south-caucasus; Abdullah Baabood, “The Growing Economic Presence of Gulf Countries in the Mediterranean Region,” Yearbook 2009 (Barcelona: European Institute of the Mediterranean, 2009), https://www.iemed.org/publication/the-growing-economic-presence-of-gulf-countries-in-the-mediterranean-region/.

[24] Adam Hanieh, Capitalism and Class in the Gulf Arab States, 2011th ed. (Palgrave Macmillan, 2016); Adam Hanieh, Money, Markets, and Monarchies: The Gulf Cooperation Council and the Political Economy of the Contemporary Middle East (Cambridge: Cambridge University Press, 2018); Jim Krane, Energy Kingdoms: Oil and Political Survival in the Persian Gulf (New York: Columbia University Press, 2019); Kristian Coates Ulrichsen, The Gulf States in International Political Economy (Palgrave Macmillan, 2015); Kristian Coates Ulrichsen, Insecure Gulf: The End of Certainty and the Transition to the Post-oil Era (Oxford: Oxford University Press, 2014); Karen E. Young, The Economic Statecraft of the Gulf Arab States: Deploying Aid, Investment and Development Across the MENAP (I.B. Tauris, 2023).

[25] bp, Statistical Review of World Energy, June 2022, http://www.bp.com/statisticalreview.

[26] Hanieh, Capitalism and Class in the Gulf Arab States; Hanieh, Money, Markets, and Monarchies; Coates Ulrichsen, The Gulf States in International Political Economy; Coates Ulrichsen, Insecure Gulf.

[27] Hanieh, Capitalism and Class in the Gulf Arab States; Hanieh, Money, Markets, and Monarchies.

[28] Hanieh, Capitalism and Class in the Gulf Arab States; Hanieh, Money, Markets, and Monarchies; Coates Ulrichsen, The Gulf States in International Political Economy; Coates Ulrichsen, Insecure Gulf.

[29] Adrian Jimenea and Marissa Ramos, “GCC banks: Key themes to watch for in 2023,” S&P Global Market Intelligence, January 3, 2023, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/gcc-banks-key-themes-to-watch-for-in-2023-73415211.

[30] Jalal Qanas and Malcolm Sawyer, “Financialisation in the Gulf States,” Review of Political Economy, 2022, https://doi.org/10.1080/09538259.2022.2099669.

[31] S. M. Hossein Adeli, “The Contribution of Energy Diplomacy to International Security; with Special Emphasis on Iran,” Iranian Review of Foreign Affairs 1, no. 2 (2010); Steven Griffiths, “Energy diplomacy in a time of energy transition,” Energy Strategy Reviews 26 (November 2019); Hongtu Zhao, “Energy Diplomacy: From “Bilateral Diplomacy” to “Global Energy Governance,” in The Economics and Politics of China's Energy Security Transition, ed. Hongtu Zhao (Academic Press, 2019).

[32] Paul Horsnell and Robert Mabro, Oil Markets and Prices: The Brent Market and the Formation of World Oil Prices (Oxford: Oxford University Press), Oxford Institute for Energy, June 1993.

[33] Bilgehan Alagöz, Iran-Qatar Diplomacy: A Challenge Against Russia? (Ankara: Center for Iranian Studies), February 2022, https://iramcenter.org/en/iran-qatar-diplomacy-a-challenge-against-russia-703.

[34] Maha El Dahan, Dmitry Zhdannikov and Alex Lawler, “Insight: Saudi Arabia leads OPEC decision to drop IEA data as US ties fray,” Reuters, April, 12 2022, https://www.reuters.com/business/energy/saudi-arabia-leads-opec-decision-drop-iea-data-us-ties-fray-2022-04-12/.

[35] International Trade Administration, “Saudi Arabia - Country Commercial Guide,” https://www.trade.gov/country-commercial-guides/saudi-arabia-oil-gas-petrochemicals.

[36] “ADNOC Signs Landmark Strategic Partnership Agreements with Eni and OMV in Refining and Trading,” Abu Dhabi National Oil Company (ADNOC), January 27, 2019, https://www.adnoc.ae/en/news-and-media/press-releases/2019/adnoc-signs-landmark-strategic-partnership-agreements.

[37] “Qatar secures second major LNG supply deal with China,” Al Jazeera, June 20, 2023,https://www.aljazeera.com/news/2023/6/20/qatar-secures-second-major-lng-supply-deal-with-china.

[38] “Germany agrees 15-year liquid gas supply deal with Qatar,” Guardian, November 29, 2022, https://www.theguardian.com/world/2022/nov/29/germany-agrees-15-year-liquid-gas-supply-deal-with-qatar.

[39] Andrew Mills, “QatarEnergy and PetroBangla sign 15-year LNG supply deal, CEO says,” Reuters, June 1, 2023, https://www.reuters.com/business/energy/qatarenergy-petrobangla-sign-15-year-lng-supply-deal-ceo-says-2023-06-01/.

[40] “Deal signed with Qatar to get additional 1.5 MTPA of LNG for next 15 years,” Business Standard News, June 1, 2023, https://www.tbsnews.net/bangladesh/energy/deal-signed-qatar-get-additional-15-mtpa-lng-next-15-years-642374.

[41] Deepika Sriram, “What green finance and carbon markets mean for the GCC,” Middle East Economic Digest, March 31, 2023, https://www.meed.com/what-sustainable-finance-and-carbon-markets-mean-for-the-gcc.

[42] Carey W. King, The Economic Superorganism: Beyond the Competing Narratives on Energy, Growth, and Policy (Springer, 2021), https://doi.org/10.1007/978-3-030-50295-9.

[43] King, The Economic Superorganism.

[44] Banking on Climate Chaos, Fossil Fuel Finance Report 2023.

[45] “APICORP leverages preferred creditor status to launch A/B loan programme,” Gulf Business, June 21, 2022, https://gulfbusiness.com/apicorp-leverages-preferred-creditor-status-to-launch-a-b-loan-programme/.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.