Author(s)

To access the full report, use this PDF link: CHINA-pub-PolicyReport57.pdf

Overview

Social media sites, while currently treated as an “audiovisual product”1 by the Chinese government under the World Trade Organization’s (WTO) trade policy, have outgrown this construct and instead have become the “ports”2 of the twentyfirst century. Taking into consideration the global trade significance of social media as a locus of international trade in advertising, information, and increasingly other types of commercial goods, it is essential that the United States continues to pursue WTO action to encourage China to open trade in social media infrastructure. This, in turn, would ensure long-term global competitiveness in the information communication and technology sector. In May 2012, following a multi-year appellate process in the WTO Dispute Settlement Body (DSB), the Chinese government asserted that it had met its WTO obligations to open its media markets. At the same point, the US government signed a memorandum of understanding, signaling the Chinese government had made progress, but had not completely resolved the initial United States WTO complaint.3 The US response to the memorandum of understanding in the May 24, 2012, meeting of the WTO DSB highlighted that improvement in market access brought “significant progress, but not a final resolution.”4 This policy paper will argue that there are several additional steps that need to be taken in order to continue making progress toward more open media markets and to assure the long-term health of global media and technology markets.

The need for increased development of fair digital media markets has emerged out of the rapidly changing nature of digital distribution practices. In 2007, when the United States leveraged its initial WTO complaint against China, the terms of the debate were substantially different than they are now. Seven years ago, audiovisual materials were much more easily decoupled from their digital distribution sites.5 However, in the current environment, delivery portals are so deeply entwined with the dispersal of content that it has become nearly impossible to make cogent international policy based on distinctions between digital “audiovisual products” and digital distribution sites.6,7 Indeed, because these sites have become so central to the experience of media consumption, as well as a host of other activities ranging from commerce to social life, it is essential to take into account these complexities when legislating trade related to digital media. For example, it is nearly impossible to completely separate videos that are primarily distributed through the Chinese digital video portal Youku from the videos themselves. Similarly, separating the content of tweets on the Chinese social media portal Weibo from the platform itself fails to take into account the significance of the platform as well as its ubiquitous nature. As such, it is unrealistic to separate the platform from the content in regulatory policy. Instead, guidelines should be focused on maintaining the openness of twenty-first century digital ports of trade.

When China entered the WTO in 2001, it (rightly) requested protections for its media industries from global markets, as the majority of the country’s media industries were state-owned enterprises that served an almost exclusively Chinese population. Even in 2014, radio and television remain largely domestic industries. The PRC government’s control of radio and television industries still fits clearly within the initial WTO agreements on audiovisual products. PRC film import quotas, while frustrating to Hollywood producers and lobby groups like the Motion Picture Association of America, are consistent with WTO policy regulations on audiovisual products. However, dynamism of the global media industries over the past 12 years has fundamentally changed the tapestry of global media in such a way that Chinese media entities have become players in the global digital media sphere. It is within this context that I would argue for an expansion of Chinese media policy, particularly with regard to international media access within the Chinese market.

Evolving from a nationally owned and distributed infrastructure, the Chinese digital media landscape has developed to become one in which private Chinese companies are taking a substantive role in the global stage, rivaling other global digital media firms based in the United States and Europe. The international explosion of communication platforms like Weibo and Weixin underscore the broad, innovative impact of Chinese digital media corporations in the contemporary social mediascape. Chinese Internet companies like Sina and Sohu have become power players in the growth of global digital culture, with stocks publicly listed on the Nasdaq stock market. When Chinese digital media companies operate openly and globally across a broad range of industries (e.g., social media, e-commerce, gaming, and entertainment, among others), there is a significant trade incongruity, as foreign companies can only compete with those companies outside of China.

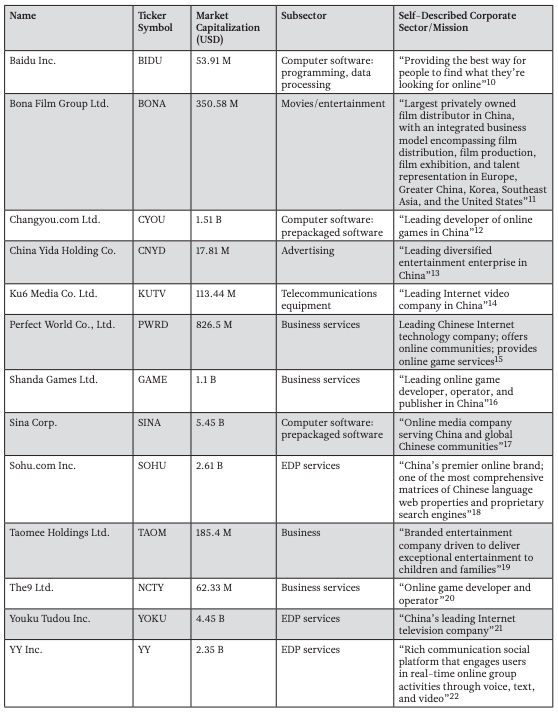

In order to highlight the scope of Chinese digital media and technology companies that have raised money on global capital markets, I have compiled a list of recent Nasdaq IPOs as well as each company’s stated mission on their investor relations page. Both the market capitalization8 and the nature of the business as described to shareholders— the individuals most (literally) invested in the company’s future—highlight the growth of a large sector of Chinese companies that have raised funds in US capital markets and are also pursuing global media and technology expansion strategies. The chart on page 3 showcases some of the major players, and the following analysis highlights implications of their activities with regard to current WTO audiovisual policy in China.

The companies listed in Table 1 have not only raised capital on international markets, but have also developed highly global business models with growing influence outside of China. For example, Changyou.com, a leading developer of online games in China, operates subsidiaries in not only the United States, but also in the European Union and Malaysia.23 While the company’s initial market is in China, it is making a strong play for international market share by operating subsidiaries in two of the largest global markets and one of the largest markets in Southeast Asia. China Yida is a leading diversified entertainment enterprise in China. While most of its business focuses on the growth of the Chinese tourism market, the company’s advertising segment focuses largely on the growth of television and digital media. The combination of a focus on tourism with a growing digital media business sector situates the company as a digital port for disseminating tourist information. While this is significant for Yida’s market share, it also highlights the way the company is no longer a strictly domestic player.

In the realm of digital film distribution, a practice that has dramatically increased online since the 2007 US WTO memorandum filing,24 companies like Bona Film Group Limited, which is also listed on the Nasdaq stock market, have become global players in both theatrical film distribution and digital distribution.25 Before digital distribution became standard practice in China, there was a clear policy rationale for preventing foreign companies from entering the Chinese media market. As a protected domestic industry, theatrical film distribution is located within PRC borders and legally does not have to be opened to outside competition. However, by raising capital on international markets as well as developing international digital distribution as a sector of its business, Bona is operating as a global media company with the protections from foreign competition negotiated for a media company that is only operating within a national context. The growth of Bona is stunning and has made dynamic impacts on the global media sphere. In November 2013, Yu Dong, the company’s chairman, offered rich insights into the process of US-China collaboration at Asia Society’s annual US-China Film Summit. The company’s participation in such events, its development of global distribution practices, and raising money on global markets highlights the fact that Bona is indeed a global company that other global companies should be able to compete with in China.

Table 1: Global Chinese Media Companies Listed on the NASDAQ Stock Market in 20139

The execution of Chinese soft power with regard to media policy creates a substantive inequality that is impacting the long-term competitiveness of global companies in what is poised to become the largest media market in the world.26 Because Chinese digital media industries are no longer exclusively focused on domestic media communications to domestic audiences, it follows that regulations of the country’s media market would also take into consideration the fact that Chinese digital media is closely entwined with the global market and open up a globally competitive playing field. The United States and China still have much to learn from one another and can both benefit from increasing openness in digital media platforms. Increasing the facility with which US and Chinese digital media companies can develop long-term collaborations leads to a potential for greater innovation on both sides.

Moreover, long-term cybersecurity on both sides is based on more than heading off acute attacks on infrastructure: It must also focus on the continuous growth of a digital sphere in which social networks and infrastructure can expand globally with transparency. This level of openness creates a global digital public sphere in which increasingly dominant commercial security apparatuses can be tested in multiple markets, where users can choose Internet security practices, and where governments and corporations alike can have an understanding of who is handling their data and how. Incongruity in the global development of digital infrastructure—even for entertainment purposes—represents a longterm structural weakness because it will fail to strengthen Internet safety and transparency policies in an open global market. This is bad for users because it limits their legal options to access social media platforms with safe and transparent user policies; it is bad for governments because users are at the mercy of corporations that may or may not report back with transparency to government regulators; and it is bad for corporations whose global market shares will be limited by increasingly draconian regulations on global trade in digital media. And indeed, despite Chinese government oversight of the digital sphere, there is still the potential for corporations to take advantage of the knowledge gap between technology workers and government technocrats to the disadvantage of both consumers and governments.

Furthermore, at the same time the imbalance of Chinese and American media and technology companies is growing in China, the financial stakes are increasing. The immediate effect of long-term restriction of film, social media, and other technology companies in the Chinese market lacks the hacker mystique and immediacy of cyber attacks, yet it poses a credible challenge to US long-term economic competitiveness with China. The incongruity of US corporate activity in the Chinese digital media space with Chinese corporate activity in the US digital media space highlights a potential future imbalance in global technology influence between China and the United States. Indeed, Chinese is poised to take over as the most common language of the Internet by 2015.27 If Chinese companies were not expanding the reach of their digital tools globally, if they were not raising capital on US markets, then it would make sense to consider Chinese digital information policy exclusively a domestic concern. However, this is not the case, and it is important for US policymakers to take into consideration the growing inequality in this sphere.

Indeed, social media activity in China already demonstrates a serious trade imbalance between China and the United States. Major US social media companies like Facebook and Twitter are not legally allowed to operate in China, with the exception of a recent move that allows Facebook access in the new Shanghai Free Trade Zone.28 Yet, China is rapidly becoming the world’s largest digital media market. By contrast, Chinese social media companies not only operate within the United States, but the major firms have also raised capital within US financial markets. This list includes market leaders like media portal Sina, which runs the major microblog site Weibo, as well as “infotainment web platform” Sohu.com. Both firms are listed on the Nasdaq. The social media platform Renren is listed on the New York Stock Exchange, as is the social video site and YouTube competitor Youku Tudou.29 Together these Chinese web and social media companies have raised over USD 43 billion from US-based capital markets.30 These are not state-owned companies and are global in scope like their American competitors, yet equivalent American firms are not allowed to operate within China.

Investment restrictions in social media have created undue complications for Chinese companies. Chinese social media firms that have raised capital within the United States rely on a complex, quasilegal system to raise money on foreign capital markets. This business structure, called a variable interest entity (VIE), requires Chinese companies like Sina to establish a US-based consulting company that raises capital. After its establishment, the company then pays its Chinese counterpart. The structures through which companies raise capital underscore the incongruities already existing within capital markets. A combination of WTO and Chinese government policy changes can help to increase the transparency of capital markets with regard to raising capital between China and the United States. Along with a liberalization of WTO regulations regarding the distribution of audiovisual products in order to decrease protections for global Chinese social media companies, there will be increased transparency in international Chinese media industries.

Major Chinese Internet companies that have raised capital in the United States are rapidly increasing the profile of Chinese social media in the global marketplace. They are providing important services for both English language and Chinese language users, including messaging, streaming video, e-commerce, and social networking. Both Sina Weibo and Youku have become international Internet superstars. Social media giant Tencent recently inked strategic partnerships with four major Hollywood studios to establish online video distribution in the Chinese market, made possible by preexisting restrictions on foreign companies.31 However, the intensive protectionism in the Chinese digital media sphere does not reflect this massive push toward globalization by Chinese digital media companies. With the global social media market poised to reach USD 34 billion by 201632 and social media sites serving as platforms for future economic activity, the United States has a lot to lose from this unequal playing field.

At the same time, gaming companies, which offer their own platforms for social commerce through the sale of premium content within and surrounding the games, still require a Chinese partner with a majority stake in the product in order to enter the market. While the growth of these industries was once inchoate, the Nasdaq listed Shanda Games’ 2012 annual revenue at USD 751.5 million, with USD 58 million being generated outside of its core area of online gaming in China. The internationalization of Chinese digital media and entertainment companies presents an exciting growth trend in the market and shows the ways Chinese companies can act as global leaders in the marketplace. Simultaneously, the international market growth and international capital investment in Chinese companies that are funded by global capital on stock exchanges in the United States highlight the ways in which these companies are no longer functioning as part of a domestic industry. As such, media policy in China should reflect the global significance of these industries and institutions by opening up markets.

Yet, at the same time, US media companies have encountered complications at multiple turns when entering the Chinese market. Google withdrew from the mainland Chinese market after the government blocked many of its landmark services, from Blogger to YouTube.33 As previously noted, Twitter and Facebook are both currently blocked in the country.34 The blocking of US-based services in China while there is open access for China-based services in the United States reflects a deep and growing trade imbalance that I would argue is stretching WTO regulations.

While the audiovisual products industry in China is growing rapidly, it does not reflect an equitable global trading scheme that mirrors growing Chinese influence in the international media and technology sphere. In 2011, former Chinese President Hu Jintao highlighted the significance of the media and technology industries by identifying them as a “pillar industry” in the country’s 12th Five-Year Plan.35 More recently, President Xi Jinping bolstered the profile of homegrown digital media and technology in his speech on the “China Dream” at the March 2013 National People’s Congress.36 Within both of these conceptual rubrics is a strong emphasis on the protection of domestic media and technology industries as part of a national self-interest. This type of protectionism is legal to the degree that China is protecting national audiovisual products. However, in the case of social media portals that operate as major global gateways for trade, the argument for markets becomes more significant because of their role as ports, not just audiovisual products.

The question then becomes: At what point does domestic media and technology policy turn into a trade barrier? I would argue that China’s dynamic activity in the global social media sphere has reached this stage and that it is important to take clear trade policy-based steps in order to find a workable solution. Chinese protectionism in the digital media sphere has created a major, under-discussed trade gap between China and the United States. The US government must place more pressure on the Chinese government to open up the nation’s media to foreign competition.

Current US policy does not address the seriousness of Chinese digital media industry protectionism either on its own or in tandem with long-term US cybersecurity, or in terms of the country’s economic well-being. Trade negotiations with China have created political hot potatoes in Washington on several recent occasions, in particular with regard to energy and mineral exploration. These tense negotiations have created a difficult platform from which to successfully come to a mutually agreeable policy. However, the stakes for the US economy could not be higher, and Chinese companies can benefit from technology transfer relationships with US corporations.

Policy Recommendations

US policy interventions in the area of digital media can take multiple forms, but I propose starting with the following four:

- Reiterate a global trade policy stating that American companies must follow local laws when operating overseas to reaffirm US commitment to Chinese domestic sovereignty in the expansion of global media markets.

- The US government should register a trade complaint with the WTO because of the preferential market access Chinese companies are receiving within the market.

- The US government should place increased restrictions on Chinese media companies that want to raise capital within US markets until there is greater parity of market access.

- In order to protect US consumers of global social media, the United States should institute a digital transparency reporting policy akin to required financial reporting by the Securities and Exchange Commission.37

Conclusion

In an October 2012 talk at Rice University, US Supreme Court Chief Justice John Roberts highlighted the fact that the most challenging legal issues in the twenty-first century will be driven by the need to keep up with rapid changes in technology, an increasingly difficult task for policymakers. The case for increased WTO action to press China for greater social media market openness, as well as the case for mandated transparency reports in order to protect US consumers in global consumer markets is particularly significant in the post-Snowden era. With collaboration and open markets, China and the United States would have the ability to maximize opportunities for innovation in the digital media sphere. At the same time, increased openness also creates a global marketplace within which consumer choice can facilitate safe and useful digital ports in the twenty-first century.

References

1. World Trade Organization, China—Measures Affecting Trading Rights and Distribution Services for Certain Publications and Audiovisual Entertainment Products, December 21, 2009, AB-2009-3, WT/DS363/AB/R.

2. Google, Enabling Trade in the Era of Information Technologies: Breaking Down Barriers to the Free Flow of Information, November 15, 2010.

3. World Trade Organization, “China—Measures Affecting Trade Rights and Distribution Services for Certain Publications and Audiovisual Entertainment Products,” DISPUTE DS363, accessed May 14, 2013, http://www.wto.org/english/tratop_e/dispu_e/ cases_e/ds363_e.htm.

4. Ibid.

5. Philip M. Napoli, “Navigating ProducerConsumer Convergence: Media Policy Priorities in an Era of User-Generated and User-Distributed Content” (working paper, 2009).

6. Sanjoy Paul, Digital Video Distribution in Broadband, Television and Mobile Convergence (New York: Wiley, 2011), 3.

7. I am referring here to social media applications, web sites, and web portals ranging from Tencent’s Weixin, Sina’s Weibo, and Sina’s web portal to Facebook, Google, and Twitter.

8. This term refers to the value of a company’s outstanding shares.

9. “Companies in China,” Nasdaq, accessed December 4, 2013, http://www.nasdaq.com/ screening/companies-by-region.aspx?region=Asia &country=China&pagesize=150.

10. “The Baidu Story,” Baidu, accessed December 5, 2013, http://ir.baidu.com/phoenix. zhtml?c=188488&p=irol-homeprofile.

11. “Investor Overview,” Bona Film Group, accessed December 5, 2013, http://ir.bonafilm.cn/.

12. “Company Overview,” Changyou.com, last modified January 9, 2014, http://ir.changyou.com/ about_01.shtml.

13. “About China Yida,” China Yida Holding Co., accessed December 5, 2013, http://www.yidacn. net/html/index.php.

14. “Company Profile,” Ku6 Media Co., Ltd., accessed December 6, 2013, http://ir.ku6.com/ phoenix.zhtml?c=187793&p=irol-irhome.

15. “Company Profile,” Perfect World Co., Ltd., accessed December 6, 2013, http://www.pwrd. com/html/en/about_compro.html.

16. “Company Information,” Shanda Games Limited, accessed December 6, 2013, http:// ir.shandagames.com/.

17. “Company Profile,” Sina, accessed December 6, 2013, http://corp.sina.com.cn/eng/ sina_rela_eng.htm.

18. “Company Overview,” Sohu, accessed December 6, 2013, http://investors.sohu.com/.

19. “About Taomee,” Taomee Holdings Limited, accessed December 6, 2013, http://ir.taomee.com/ phoenix.zhtml?c=243417&p=irol-IRHome.

20. “Welcome to The9 Limited,” The9 Limited, accessed January 13, 2014, http://www.corp.the9. com/.

21. “Corporate Profile,” Youku Tudou Inc., accessed January 13, 2014, http://ir.youku.com/ phoenix.zhtml?c=241246&p=irol-irhome.

22. “Investor Relations,” YY.com, accessed January 13, 2014, http://investors.yy.com/.

23. “Company Overview,” Changyou.com.

24. John Gantz and David Reinsel, The Digital Universe in 2020: Big Data, Bigger Digital Shadows, and Biggest Growth in the Far East (Framingham, MA: International Data Corporation, 2012).

25. “Our Company,” Bona Film Group, accessed December 4, 2013, http://www.bonafilm.cn/ourcompany.aspx.

26. John Horn, “China to become world’s largest media market by 2020, study predicts,” Los Angeles Times, November 28, 2012, http://articles. latimes.com/2012/nov/28/entertainment/la-etct-china-largest-movie-market-20121128.

27. Conrad Quilty-Harper, “Chinese Internet users to overtake English language users by 2015,” The Telegraph, September 26, 2012, http://www. telegraph.co.uk/technology/broadband/9567934/ Chinese-internet-users-to-overtake-Englishlanguage-users-by-2015.html.

28. George Chen, “China to lift ban on Facebook — but only within Shanghai free-trade zone,” South China Morning Post, September 25, 2013, http:// www.scmp.com/news/china/article/1316598/ exclusive-china-lift-ban-facebook-only-withinshanghai-free-trade-zone.

29. “Listings Directory,” NYSE Euronext, accessed May 13, 2013, http://www.nyse.com/ about/listed/lc_all_overview.html.

30. According to Google Finance as of May 13, 2013.

31. “Tencent Adds a Wide Selection of Disney Live-action and Animated Features to its Leading Online Movie Service,” PR Newswire, September 9, 2013, http://www.prnewswire.com/news-releases/ tencent-adds-a-wide-selection-of-disney-liveaction-and-animated-features-to-its-leadingonline-movie-service-222942201.html.

32. “Forecast: Social Media Revenue, Worldwide, 2011-2016,” Gartner Group, June 25, 2012, http:// www.gartner.com/id=2061016.

33. Siva Vidyanathan, The Googlization of Everything (And Why We Should Worry), (Berkeley: University of California Press, 2011).

34. As of May 13, 2013.

35. Yu Hong, “Reading the Twelfth Five-Year Plan: China’s Communication-Driven Mode of Economic Restructuring,” International Journal of Communication 5 (2011): 1045-1057.

36. Ed. Fang Yang, “President Xi delivers speech at closing meeting of 1st session of 12th NPC,” Xinhuanet, March 17, 2013, http://news.xinhuanet. com/english/china/2013-03/17/c_132240367.htm.

37. For a more detailed discussion of the potential role of corporate transparency reports, see http:// www.rankingdigitalrights.org.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.