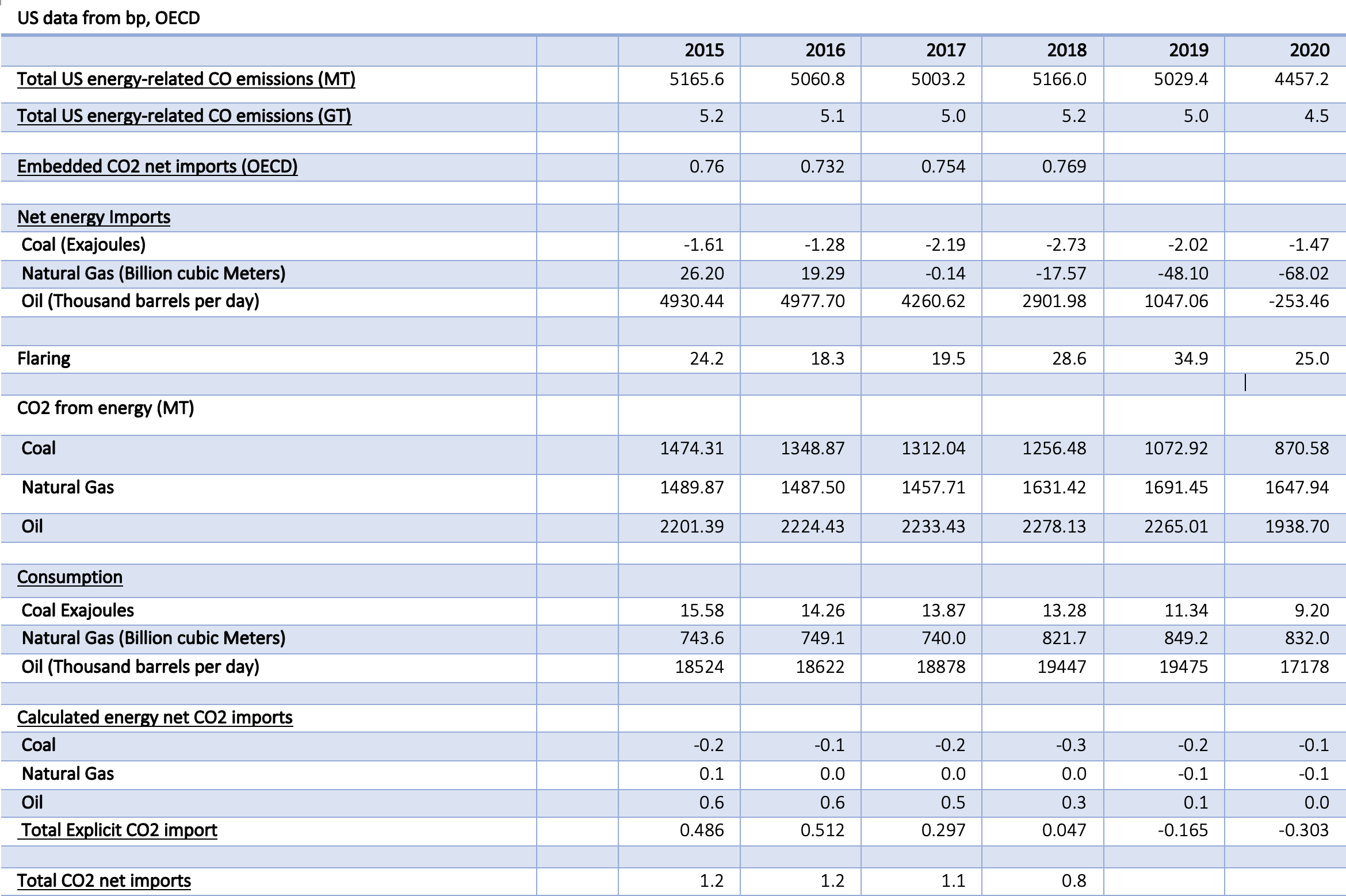

Introduction/Summary

Recent moves by the European Union and other nations highlight the growing interest in carbon border adjustments as a policy tool to protect economies that pursue relatively aggressive climate policies, while also encouraging broader international adoption of such strategies. Carbon border adjustments (CBAs) are trade policies designed to “level the playing field” for domestic producers. The underlying idea is to impose a tax/fee on imports based on the emissions profile of the good in question to reflect the domestic cost of climate policy on a similar good. In addition, a rebate can be given for the exports of goods based on the environmental regulatory costs in the host country, so as not to disadvantage domestic producers in a global marketplace with less rigorous climate policies.

Much of the public discussion and analysis has focused on the implications of such measures for carbon-intensive manufacturing industries. As a result, the carbon content associated with fossil fuels has been neglected. While the final form of the adjustment measures under consideration remains highly uncertain, a comprehensive border adjustment mechanism would also apply to fossil fuel trade. Accordingly, a full assessment of the macro- and micro-economic implications of a border adjustment must include trade in both implicit and explicit carbon—i.e., trade in carbon embedded in manufactured goods as well as direct trade in fossil fuels.

Broadening the frame of reference to include both dimensions of international trade in carbon yields interesting insights. China—the largest emitter of CO2 globally—is the world’s leader in net exports of carbon embedded in manufactured goods, but also the world’s largest importer of fossil fuels. Europe is a large importer of both embedded carbon and fossil fuels. The United States is the world’s leading importer of embedded carbon, but—due to the shale revolution—has moved from being the world’s largest fossil energy importer to being a net exporter. These relative differences, and especially the large shift in US net carbon trade in recent years, could have significant ramifications when analyzing the impact of a carbon border adjustment.

Motivations for Carbon Border Adjustments and Overview of Existing Literature

One motivation behind CBAs is to prevent the creation of “pollution havens,” and, in particular, “carbon leakage,” which happens when producers shift their output to countries that have lax climate policies. By imposing taxes on imported carbon emissions and rebates on exports, domestic industries would be protected, and there would be no incentive for manufacturers to relocate to “pollution havens.” With exceptions granted to goods produced in countries with similarly robust climate policies, such measures would also provide an incentive for trading partners to adopt similar policies (Campbell, McDarris, and Pizer 2021). Recently the European Union has been pushing for a carbon border adjustment mechanism that imposes a carbon tax on imports that do not meet their emissions standards. On March 15, the European Council reached an agreement to implement carbon border adjustments on the following industries: cement, aluminum, fertilizers, electricity energy production, iron, and steel. However, there are still uncertainties regarding the exact timing and scope of the EU’s plans (Council of the EU 2022).

In the US, a similar bipartisan proposal is being discussed in the Senate. Initially the Democratic party proposed a bill that measures the cost of carbon based on “domestic environmental damages” for carbon-intensive goods (PwC 2021). Members of the Republican party have also recently endorsed the idea of a CBA to curtail Russia’s influence over Europe and the US (Joselow and Montalbano 2022).

One limitation of the current discussion on CBAs is that the focus has been on “embodied carbon,” or the carbon associated with the production of a good, which in this analysis we will refer to as embedded or implicit carbon.

With this limited perspective, we see that developed countries like the US and Europe are net importers of embedded carbon at 0.75 gigatonnes (Gt) and 0.52 Gt respectively in 2018 (the most recent year for which such analysis is available—see OECD). Meanwhile China, with its large trade surplus in energy-intensive manufactured goods, is the world’s largest exporter of embedded carbon at 0.9 Gt in 2018. This framework is frequently used to indicate that countries and regions like the US and Europe are responsible for greater emissions than are immediately apparent when considering only direct emissions from fossil fuel combustion. The reverse is true for net exporters of energy-intensive goods like China.

The measurement and impacts of embedded carbon have also garnered increasing attention in recent economic literature. For example, Sato provides an overview of how input-output tables[1] are used to estimate the amount of embedded carbon in international trade (2013, 834).

Another recent example is an OECD paper by Yamano and Guihoto (2020) that utilizes the OECD inter-country input-output tables and the IEA’s carbon intensities of production to calculate the total amount of traded embodied carbon. Using linear algebra and compiling the information into matrices, Yamano and Guihoto decompose the types of energy used in intermediate stages of production from the final demand. Next, with a matrix of emissions per unit of production, they calculate the emissions that are associated with the final demand of a country. During this process, they account for trade by introducing a trade matrix between different countries. Thus, each country’s carbon emissions are tracked for domestic consumption, as well as embedded carbon in exports and imports of goods from foreign countries. To have a complete measure of carbon emissions, Yamano and Guihoto also add carbon emissions that arise from the transportation of the products.

But What About Trade in Explicit Carbon?

However, to view the complete picture of international carbon flows, there needs to be an equal focus on “explicit” carbon or the carbon content of trade in fossil fuels. The trade patterns of explicit carbon are significantly different from that of embodied carbon. For Europe and China, we can see that explicit carbon imports have generally been increasing. On the other hand, the opposite is happening in the US, in large part due to its transition from a net importer of fossil fuels to a net exporter in late 2019.

To be sure, this approach does not change global analysis or calculation of CO2 emissions (nor do we include other greenhouse gasses in our analysis). Except for specific analyses referred to later, embedded CO2 emissions are generally accounted for within the country of origin for the manufacturing process, unlike explicit CO2 emissions, which are measured at the point of consumption/combustion.

Moreover, since there is no border adjustment mechanism currently in place in any country (the EU plan is slated to start phasing in next year), the final form of such mechanisms is unknown. Proposals so far in the EU focus on the protection of certain energy-intensive manufacturing sectors, not on managing all carbon trade.

A complete picture of both implicit and explicit carbon flows is necessary to understand the impact of a comprehensive border adjustment.

This paper introduces a conceptual framework for measuring the total impact of a comprehensive carbon border adjustment by adding both implicit and explicit carbon trade for key economic blocs.

Explicit CO2 trade estimates are derived using public data from the bp Statistical Review of World Energy, along with unpublished bp data (used with permission) on country-level CO2 emissions by fossil fuel type. We first estimate each country’s/bloc’s net trade in each fossil fuel. We then create an estimate of explicit CO2 trade using conversion factors based on the carbon content of that country’s/bloc’s consumption of each fossil fuel. Admittedly, this is a massive simplification in that we assume all trade in coal and oil (including crude and refined products) has only one country-specific conversion factor. For example, China imports high-energy coking coal (used, for example, in steel manufacturing), which has a very different energy/emissions profile than China’s domestic coal. Similarly, the United States exports light, sweet crude oil and imports heavy, sour crude (which has greater energy content and therefore carbon density) to better match the configuration of domestic refineries. The US also imports gasoline and exports surplus distillates including diesel fuel (which again, is denser/more carbon intensive). These quality differences can be significant—for example, the energy density of different types of coal and different refined products can vary by more than a factor of two. A more complete analysis would incorporate such differences, but it is beyond the scope of this paper.[2]

A Review of Trade in Explicit Carbon

There have been different trends in the net trade of explicit carbon between the United States and Europe and China.[3] In particular, the US has become a net exporter of explicit carbon, while China and Europe have been increasing their net imports of explicit carbon.

The US: Moving from Importer of Explicit Carbon to Exporter

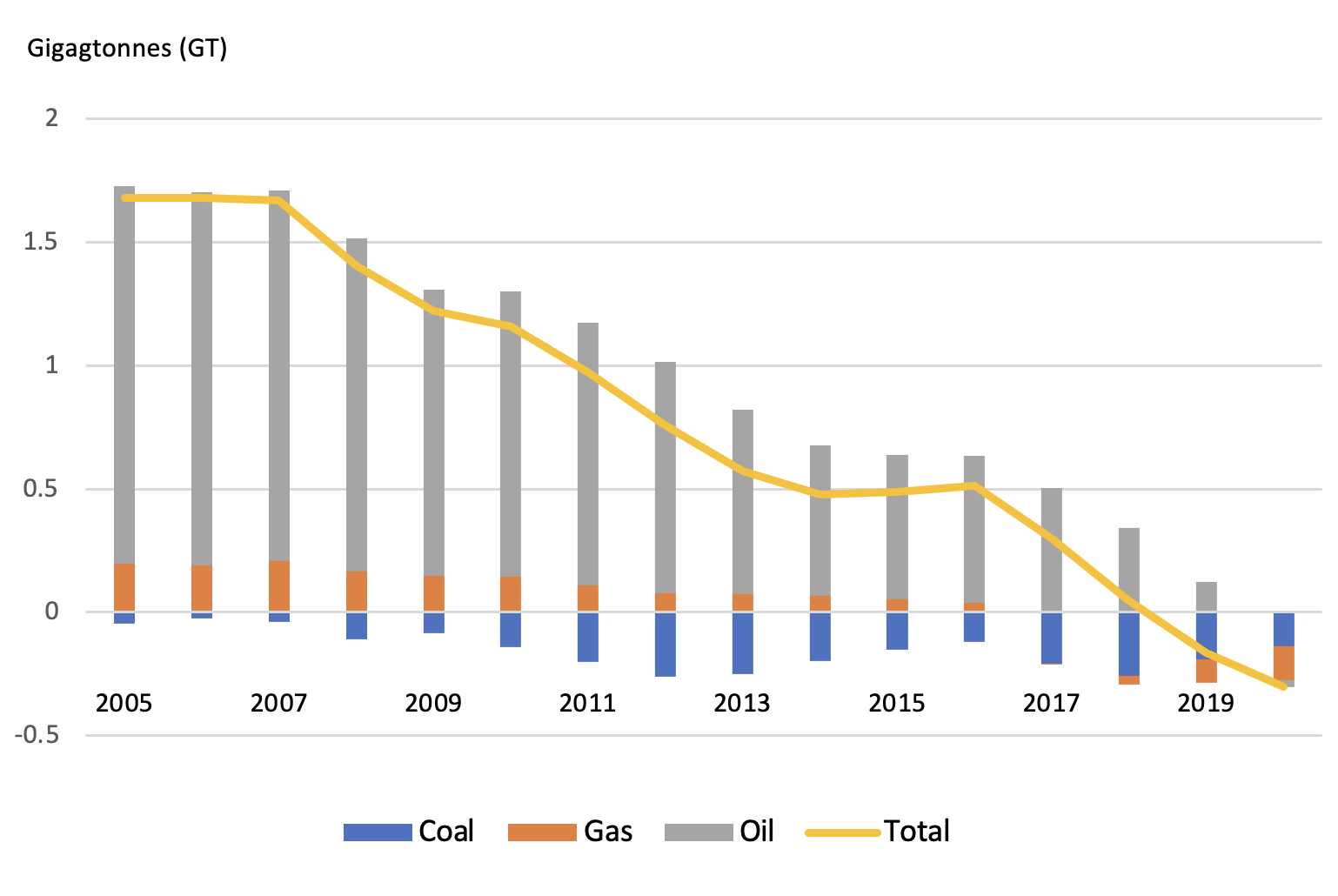

As it can be seen from the figures below, the US became a net exporter of fossil fuels, and therefore of explicit carbon, in 2019—for the first time since at least 1950.

Figure 1 — US Explicit Carbon Trade, 2005-2020[4]

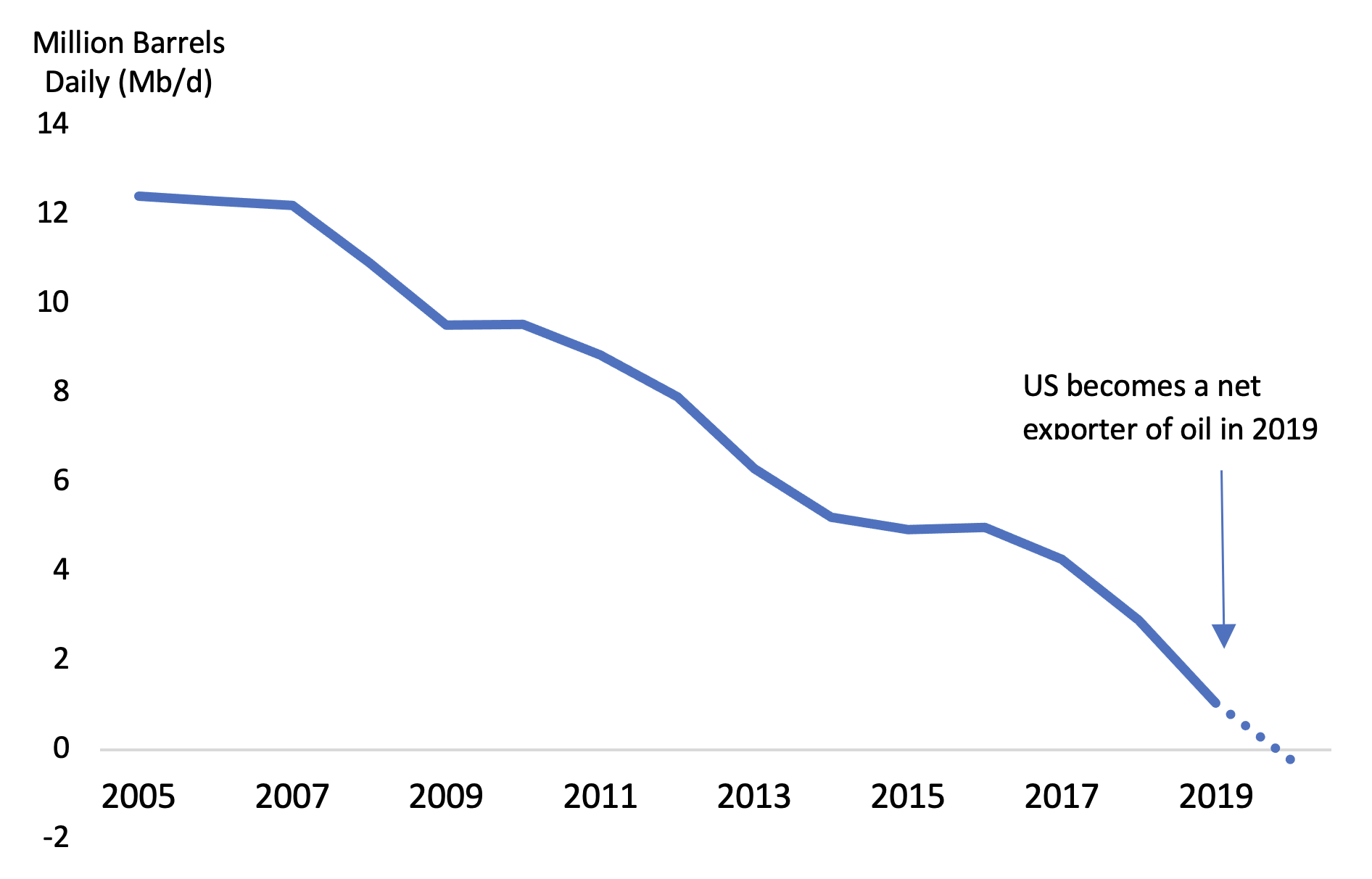

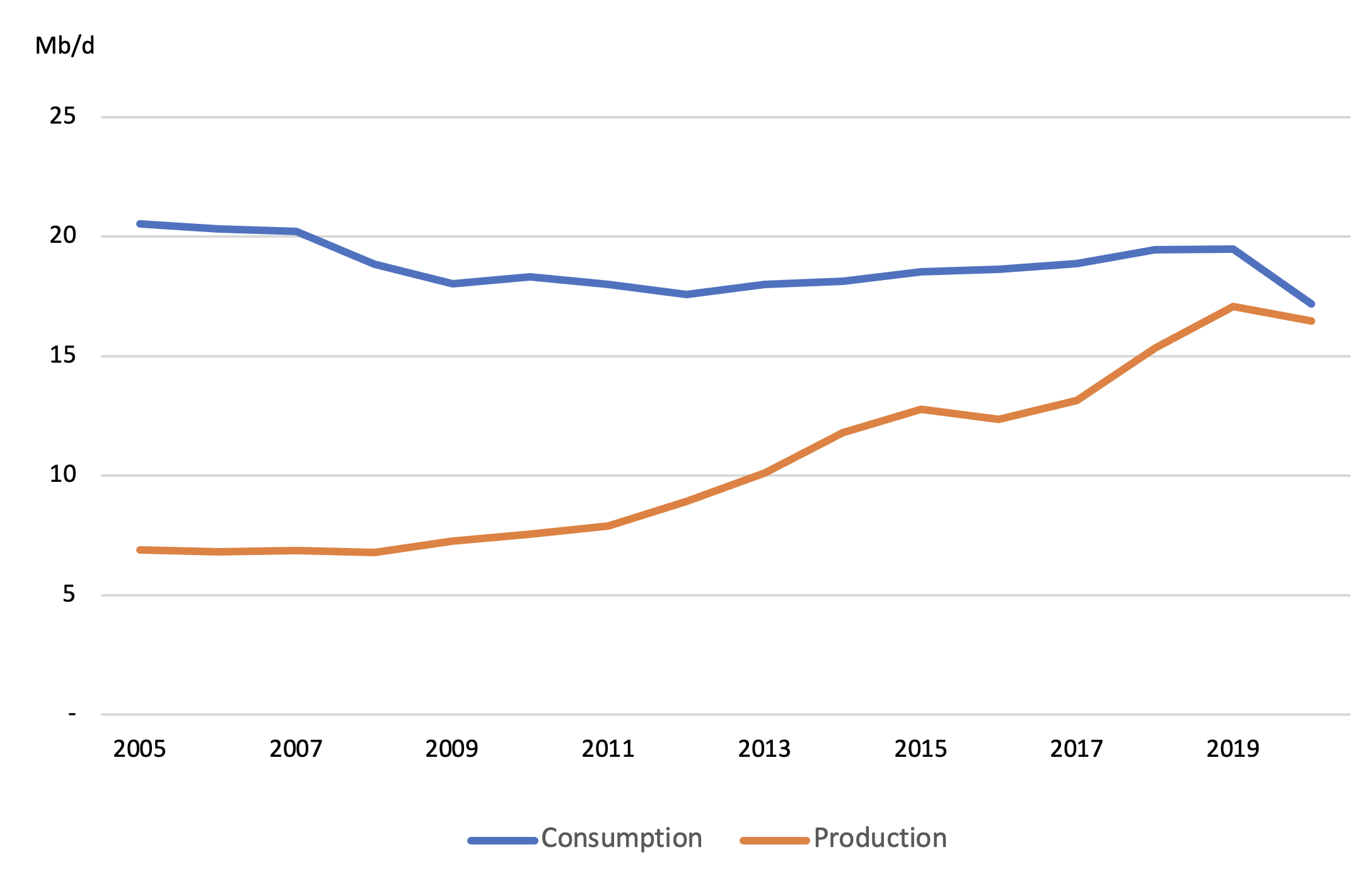

By far the most important contributor to this change was that the US became a net exporter of oil in November of 2019. This represents a dramatic shift, since the US in 2005 was by far the world’s largest oil-importing country, at that time importing over 12 million barrels per day, or more than 60% of domestic consumption.

Figure 2 — US Oil Net Imports, 2005-2020

As shown in Figure 2, starting from 2007, net US oil imports started to decrease sharply. A major driving force behind this trend was the advancement in hydraulic fracturing and horizontal drilling, which enabled the US to develop shale oil and gas. Between 2005 and 2015, oil production in the US increased by 75% due to advancements in technology (Cook and Perrin 2016). Domestic oil consumption declined after about 2007[5] but has been rising in recent years (with the exception of the COVID-related decline in 2020). In other words, the net shift in US import dependence (and therefore in net CO2 trade) has been largely a supply-side story.

The most recent decline in oil imports can be attributed to COVID-19 and the associated economic shutdowns, which led to a sharp contraction in US oil demand. This is reflected in the decrease in the consumption of oil in 2020 but has largely been offset by a strong recovery in 2021 and so far, this year.

The US has remained a small net oil exporter throughout the pandemic and recovery. While the outlook remains very uncertain, the US Energy Information Administration projects that the US will remain a net exporter of oil through 2050 (Ricker and Painter 2020).

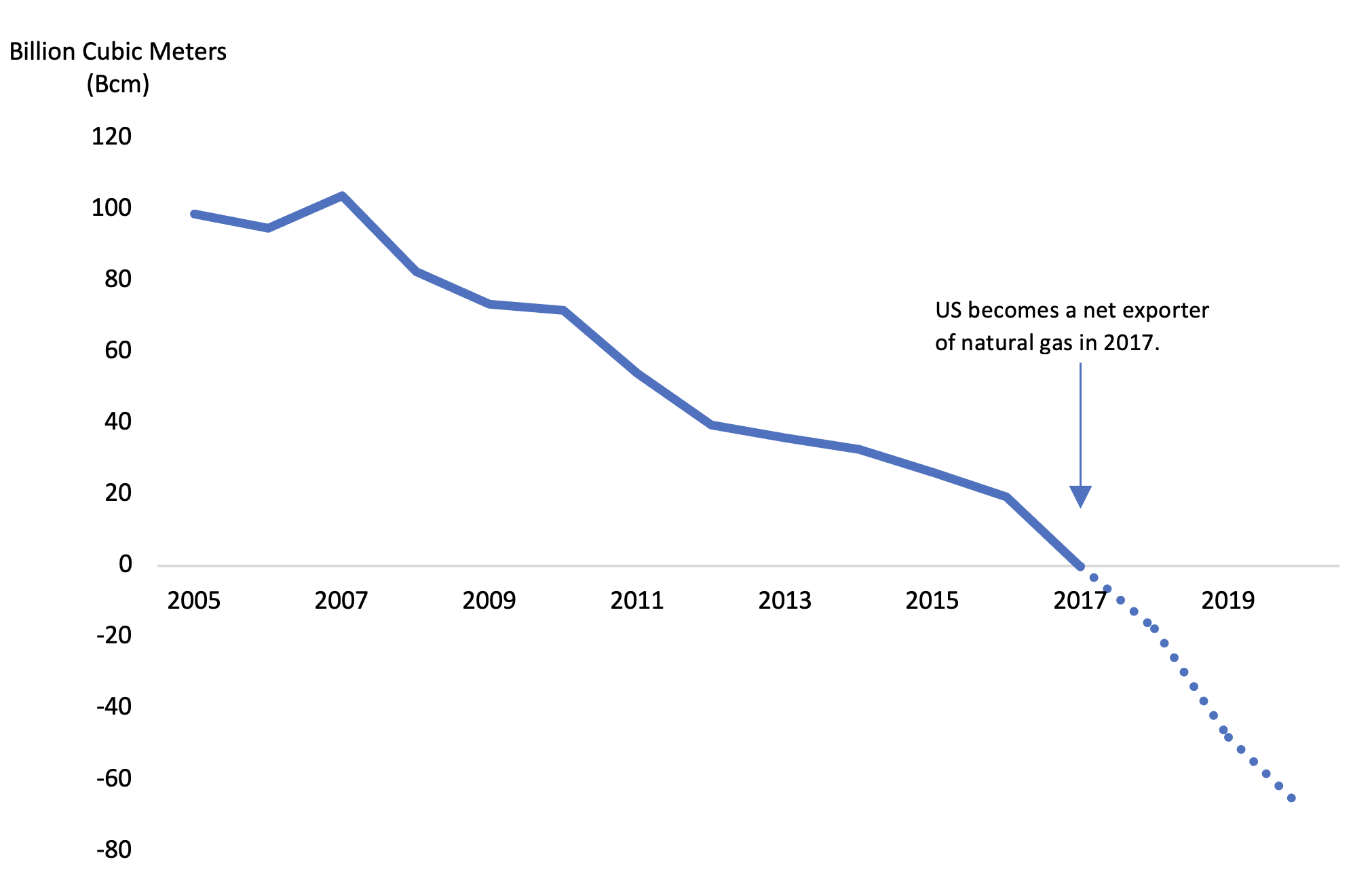

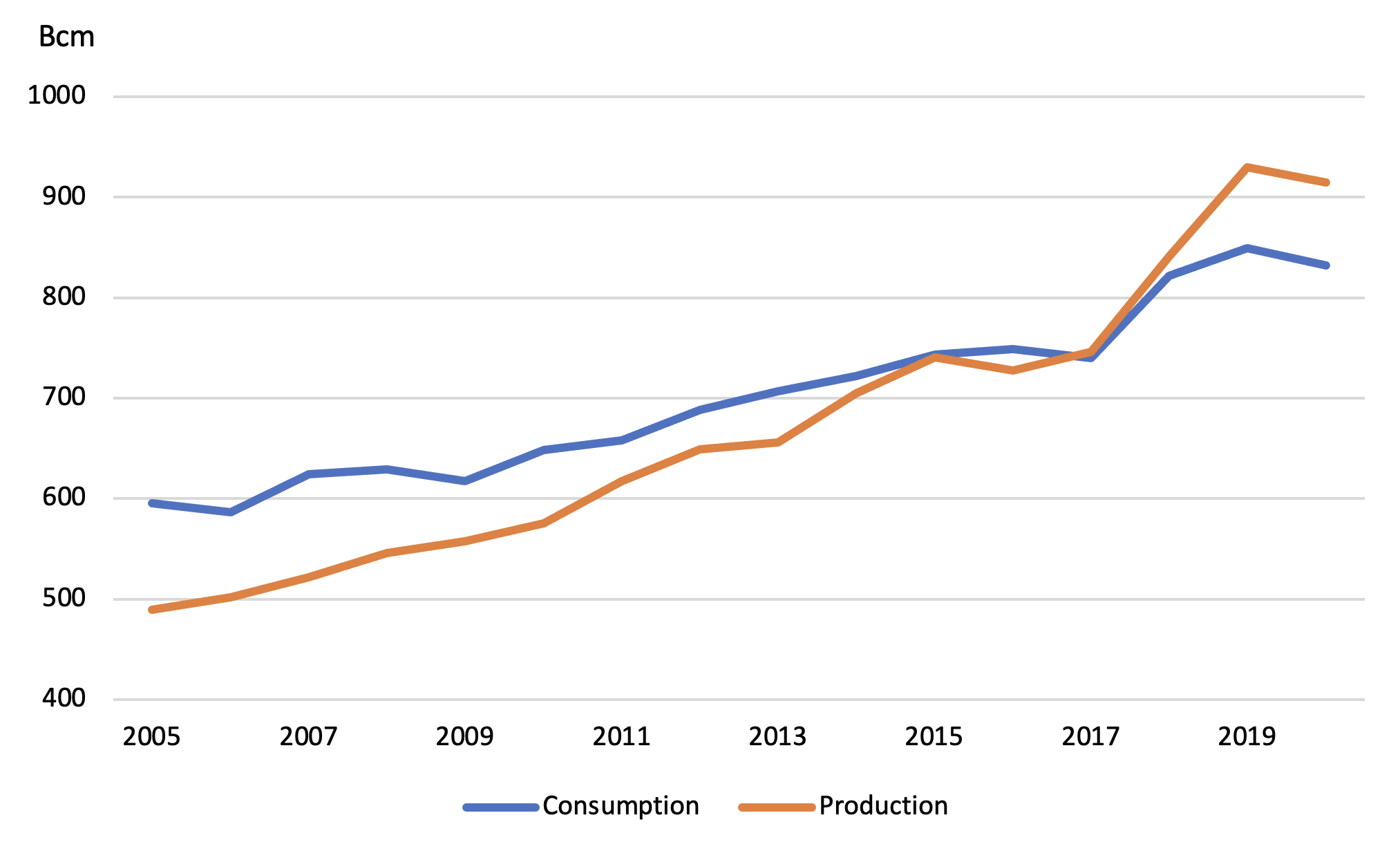

For the same reasons, the US has also moved from being a net importer of natural gas to being a large net exporter. Natural gas production increased, along with oil, with the technological advancements in hydraulic fracturing and horizontal drilling. In 2017, production started to overtake consumption of natural gas, and the US became a net exporter. As a result, it can be seen that natural gas net imports follow a similar trend as oil net imports, with exports continuing to grow as new facilities are commissioned, especially for liquefied natural gas.

Figure 3 — US Natural Gas Net Imports, 2005-2020

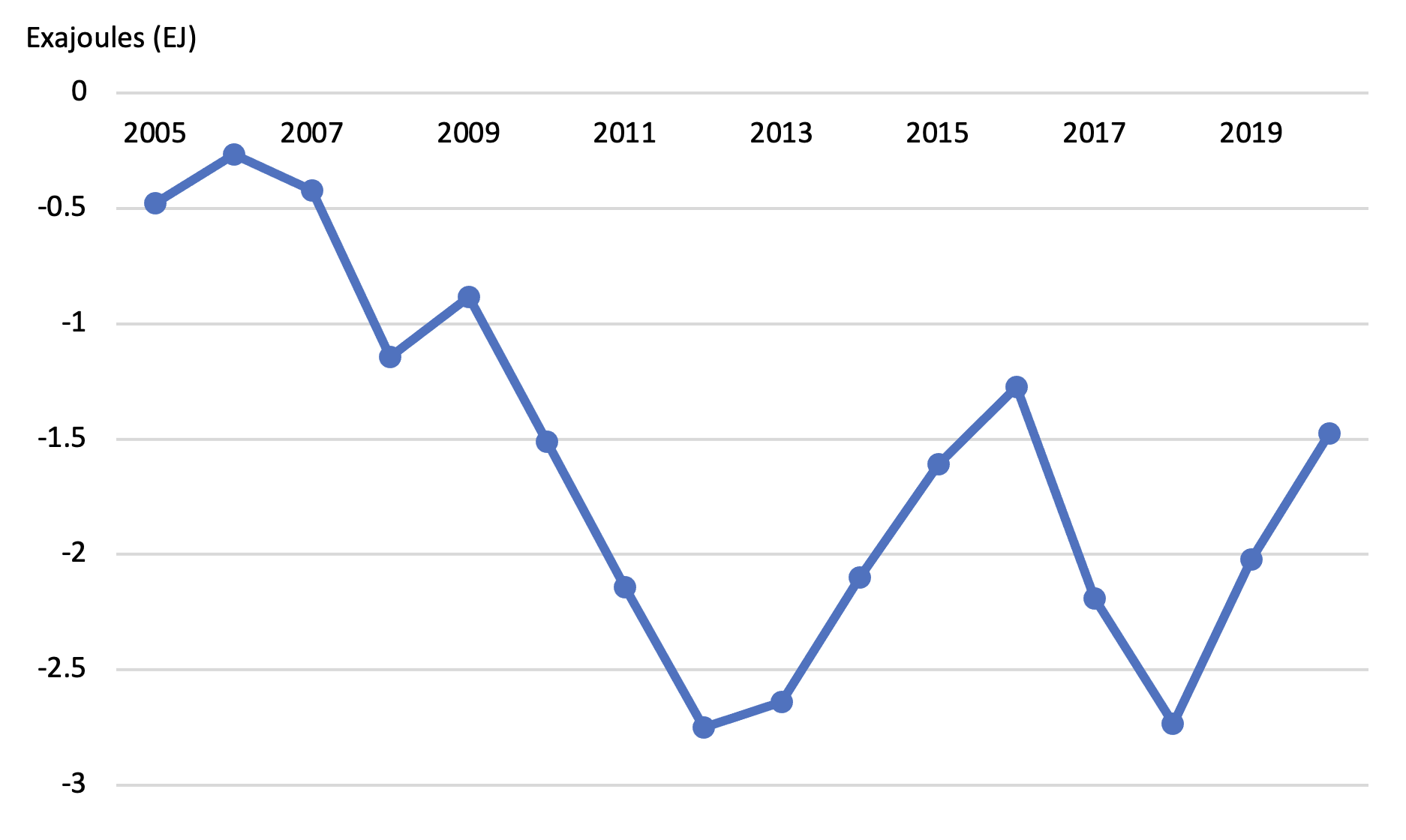

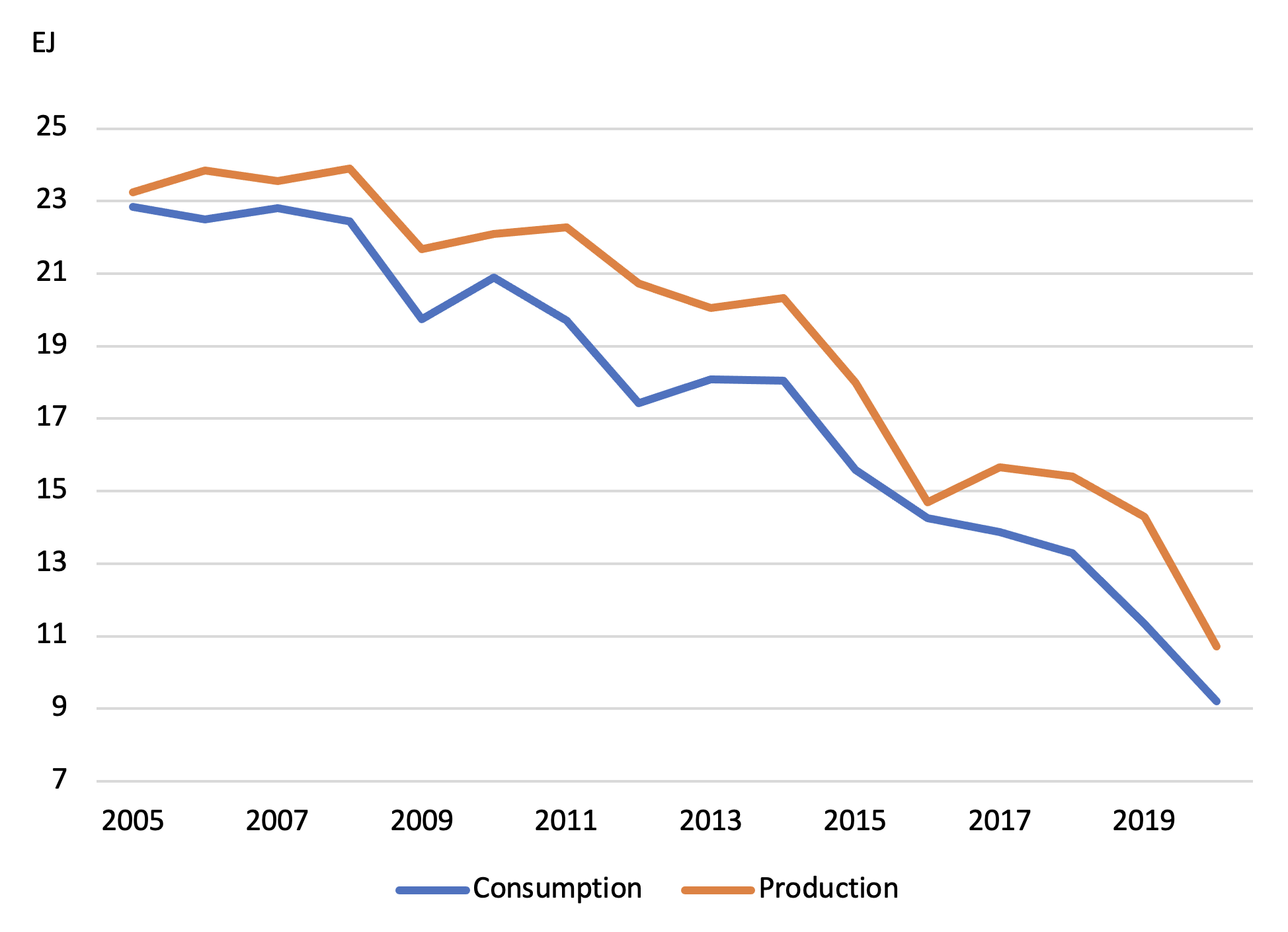

The trend for net coal trade has been less dramatic, but the US has been a net exporter of coal throughout the period under examination. Despite a steady decrease in US coal consumption and production, there does not seem to be a clear trend in the net exports of coal. The recent decrease in net exports can be attributed to the contraction of the global economy—and therefore of coal consumption and trade—due to the pandemic.

Figure 4 — US Coal Net Imports, 2005-2020

The dramatic shift in US net trade in explicit CO2 emissions can be calculated from these energy trends. The largest contributor to this change has been the shift in oil net imports—both because the volumetric shift in energy content is greatest, and because the carbon density of oil is greater than that of natural gas.

Europe and China: Growing Imports of Explicit Carbon … For Now

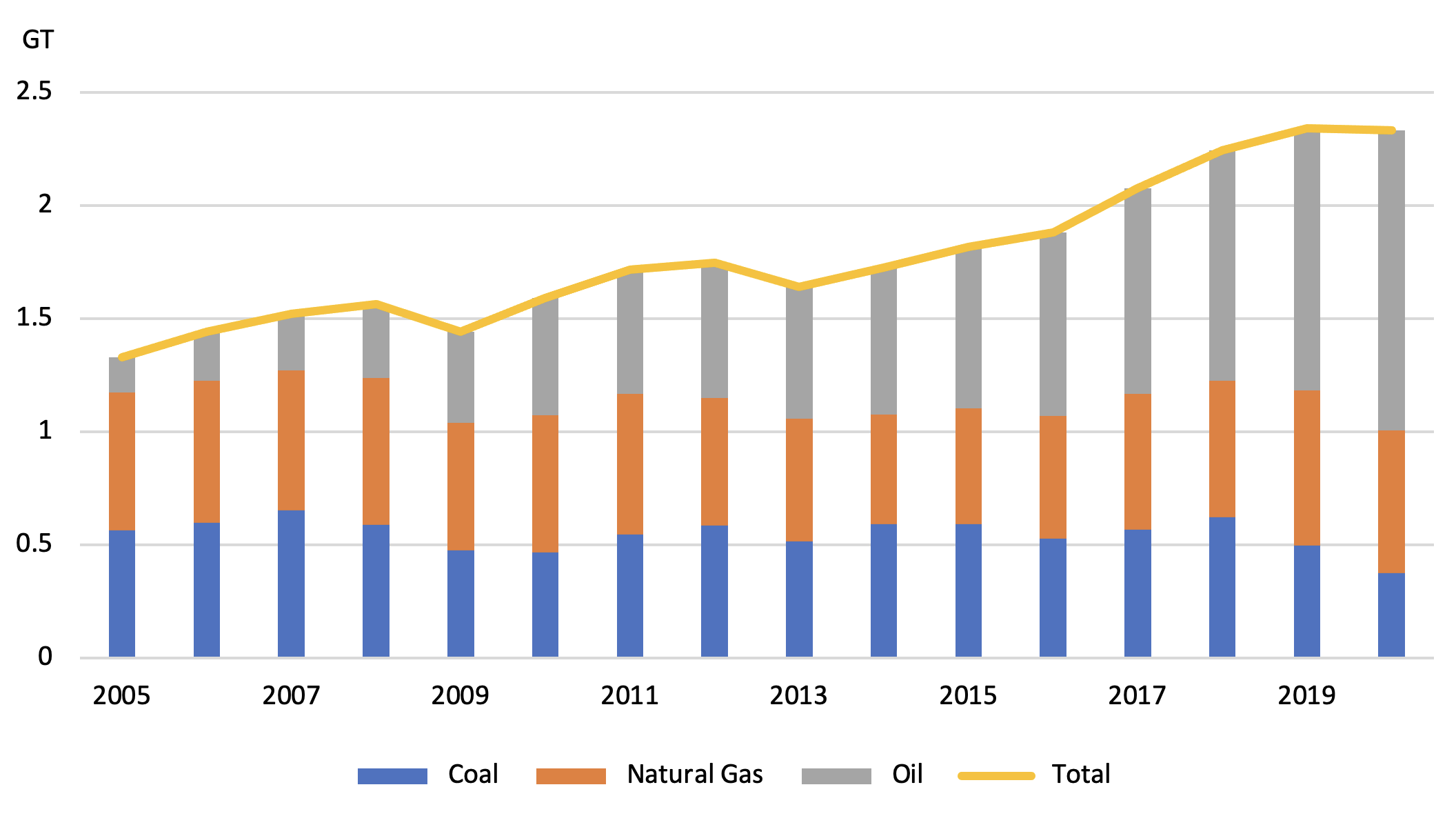

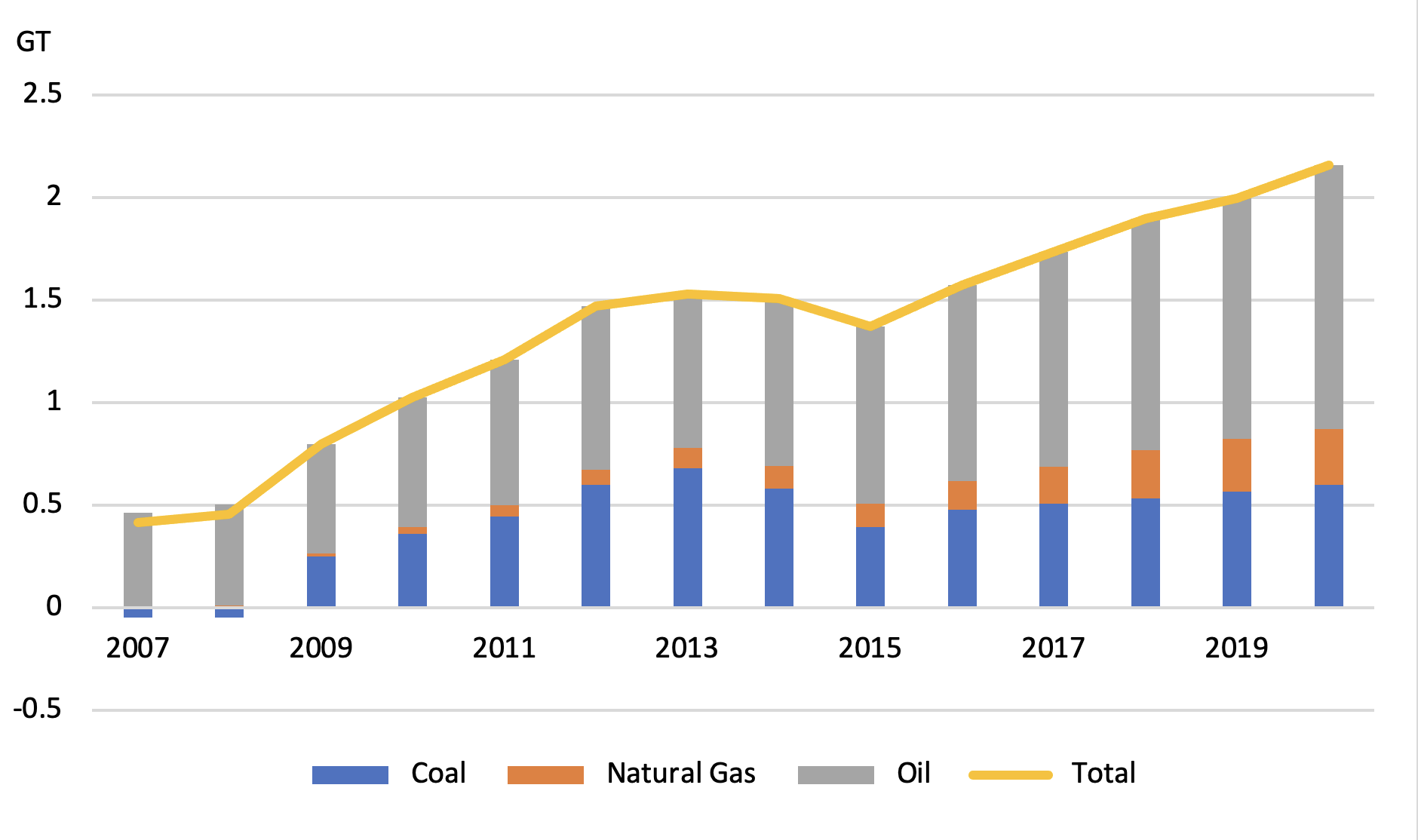

In contrast to the US, the explicit carbon trade trends for Europe and China are very different—though similar to each other. First, looking at Europe, we can see that net “explicit” carbon imports have been increasing, even as overall energy consumption has been declining—the fall in the bloc’s fossil fuel production has been greater than the decline in consumption.

Figure 5 — Europe Explicit Carbon Net Imports, 2005-2020

With China we see a similar trend but with a much sharper increase in the amount of imported explicit carbon, on the back of rapid growth in domestic fossil fuel consumption.

Figure 6 — China Explicit Carbon Net Imports, 2005-2020

Combining Explicit and Implicit Carbon Trade

To get a holistic picture of carbon traded, and thus to understand the overall macroeconomic impact of a comprehensive carbon boarder adjustment, net trade in explicit carbon needs to be combined with net trade in embodied carbon.

For the embodied carbon in trade, the OECD (previously cited) has data published on the embodied carbon associated with international trade. The net embodied carbon in international trade is calculated by combining the OECD’s inter-country input-output tables with the International Energy Agency’s CO2 emissions from fuel combustion statistic.

The net imported embodied carbon (according to the OECD study) and the total carbon (including our estimates of explicit carbon trade) are presented below for the US, the EU, and China. Note that the analysis of embodied/implicit carbon trade is lagged by several years due to data reporting; the most recent year covered in the OECD’s latest analysis is 2018.

United States

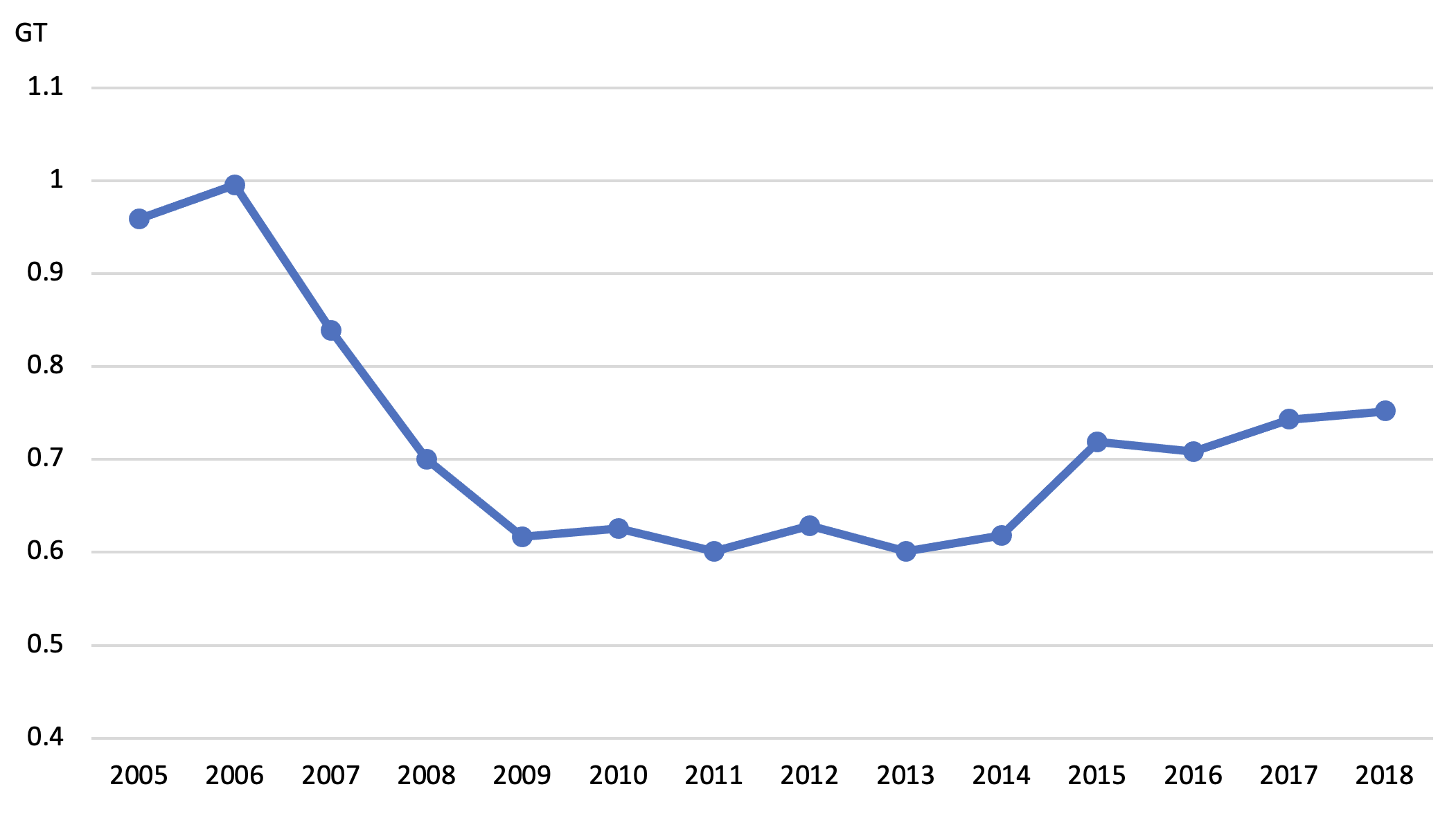

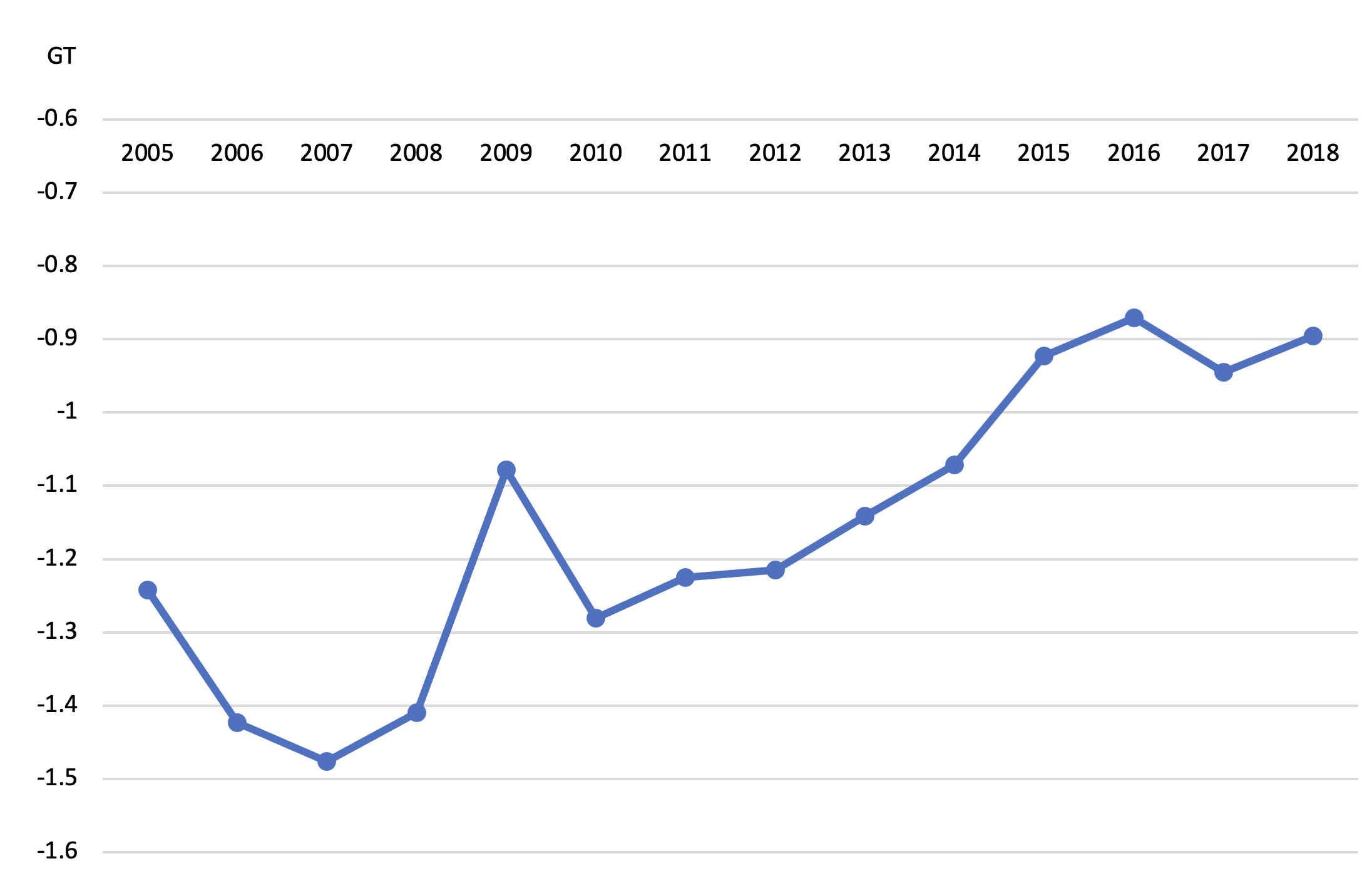

Figure 7 — US Embodied Carbon Net Imports, 2005-2018

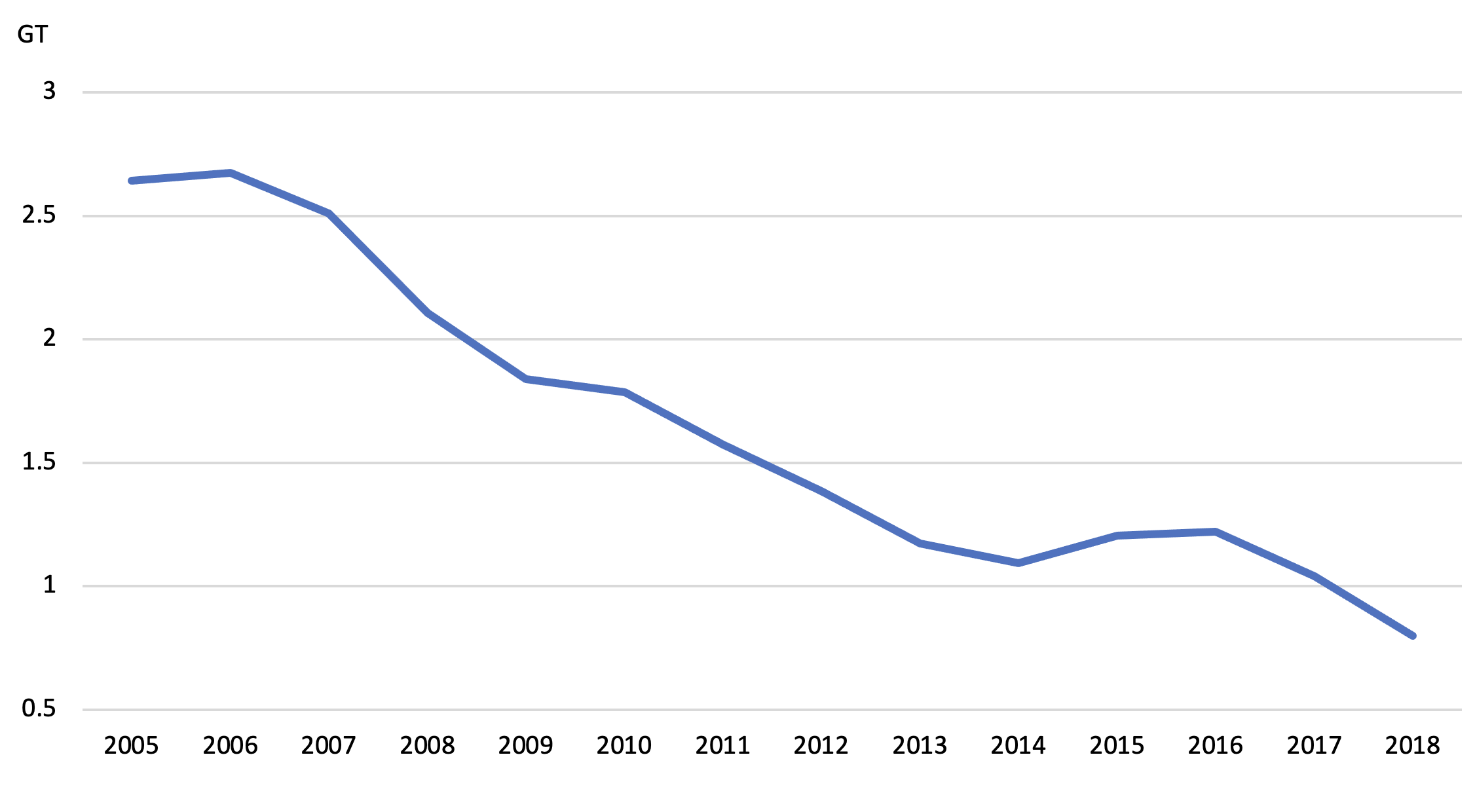

Figure 8 — US Total Carbon Net Imports, 2005-2018

For the US, net imported embodied carbon was steady from 2008 through 2014, and since then has been on a slight increasing trend. However, the significant drop in explicit carbon since 2007 gives the total imported carbon a negative slope. The United States is a still a small net importer of total (embodied and explicit) carbon—but there is a clear negative trend, and the number declined significantly from 2005 to 2018. In general, the US has been decreasing its total carbon imports since 2005.

Europe

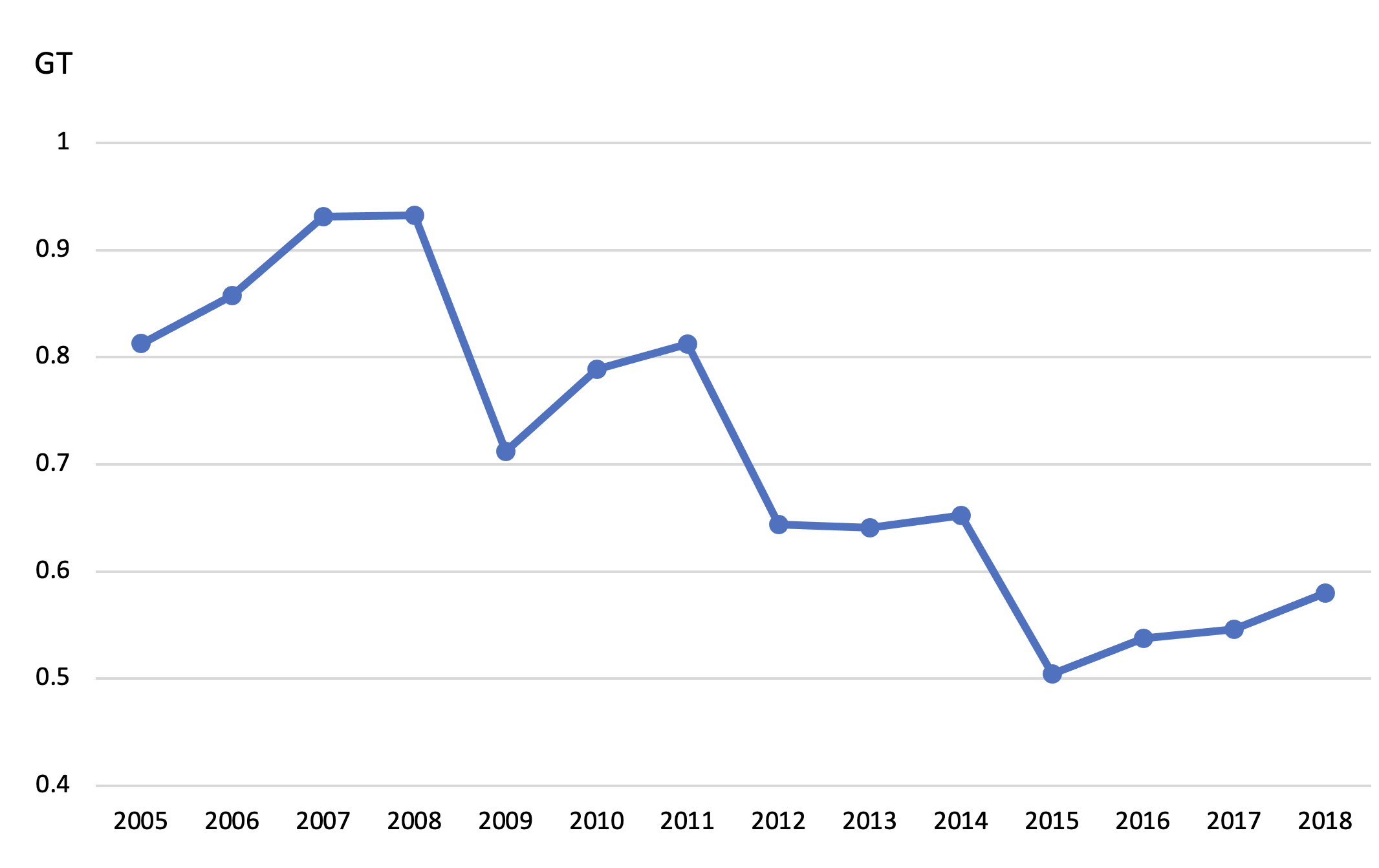

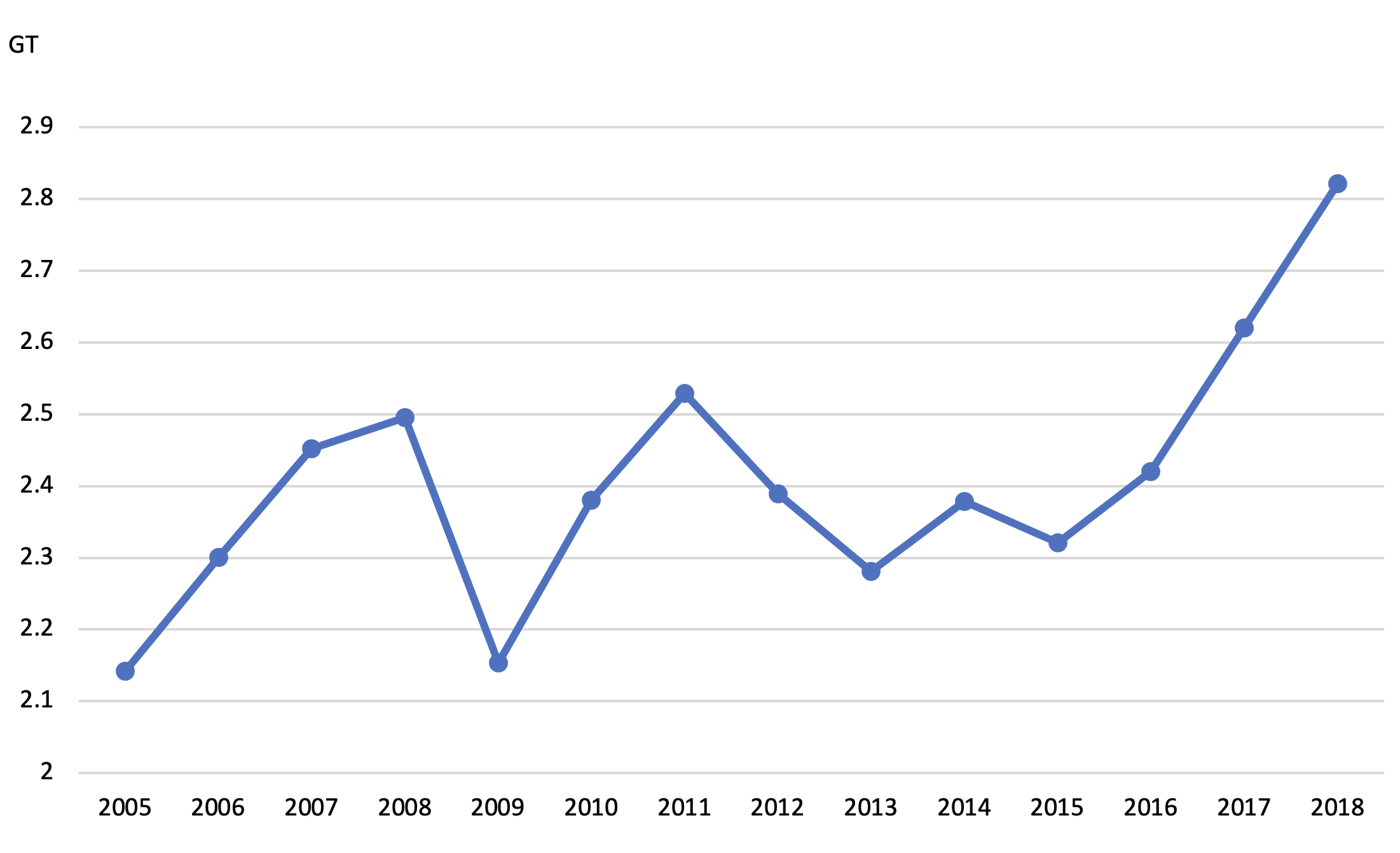

The EU’s embodied carbon trade has been trending lower, but this decline has been more than offset by growing imports of explicit carbon in the form of higher fossil fuel imports. While many analysts expect EU fossil fuel imports to decline sharply in the future due to aggressive climate policies and a desire to reduce dependence on Russia’s fossil fuel exports, for now, fossil fuel imports are an important factor in Europe’s carbon trade balance. (For a discussion of the energy impacts of the Russian invasion of Ukraine, see Collins, Medlock, Mikulska, and Miles 2022; Finley and Krane 2022).

Figure 9 — Europe Embodied Carbon Net Imports, 2005-2018

Figure 10 — Europe Total Carbon Net Imports, 2005-2018

China

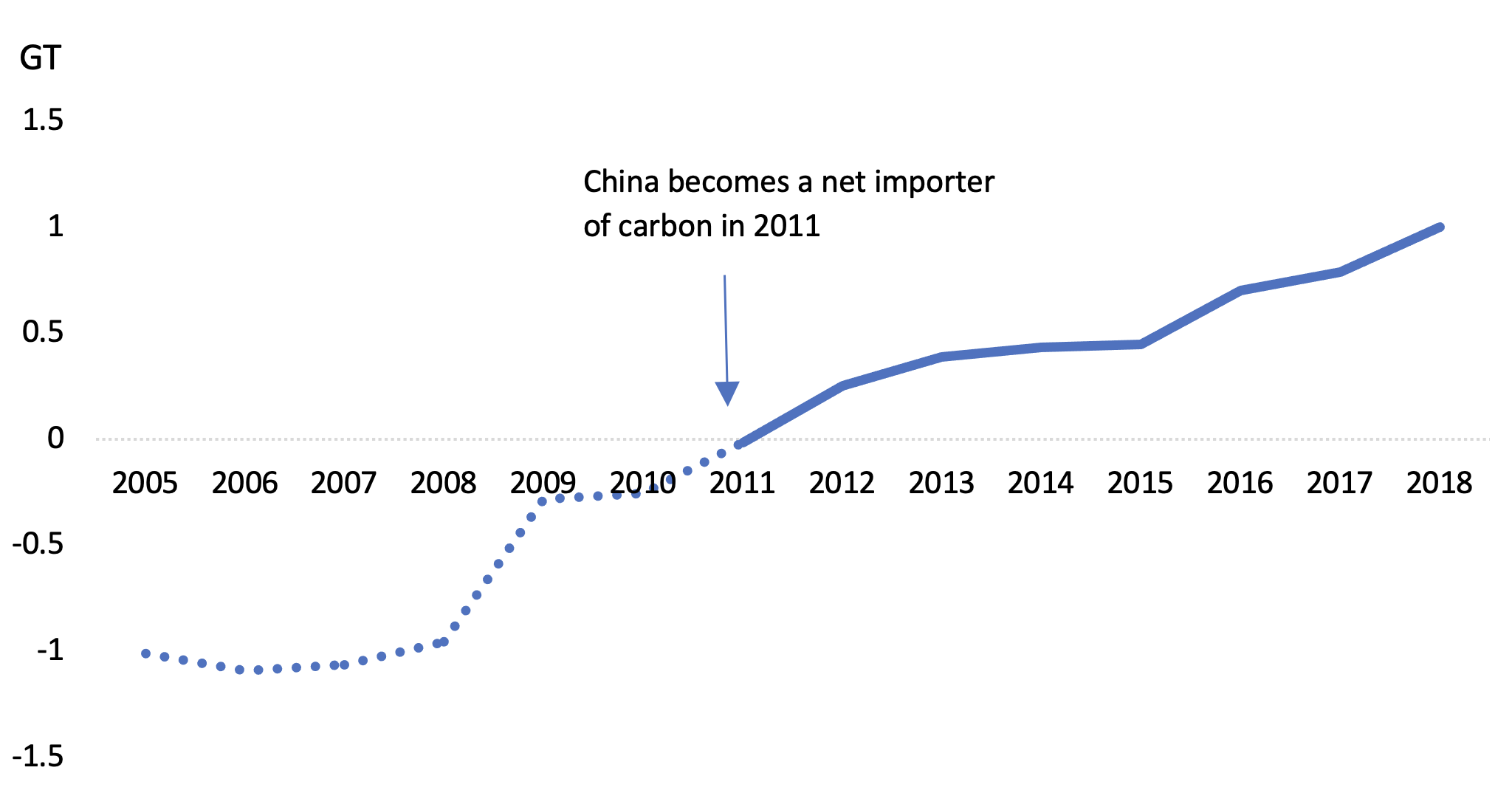

China’s embodied carbon surplus has been gradually decreasing, and this could be attributed to the fact that China is transitioning from a manufacturing economy to a service-based one, combined with a significant decline in coal’s share of domestic energy use (from 73% in 2005 to 59% in 2018). The sharp decrease in 2008 is a result of the contraction in trade following the 2008 financial crisis. Combined with the fact that China’s explicit carbon has been rising strongly, we can see that China’s total carbon trade balance has been shifting in the past decade—and indeed, that China has switched from being a net exporter of carbon to being an increasingly large net importer.

Figure 11 — China Embodied Carbon Net Imports, 2005-2018

Figure 12 — China Total Carbon Net Imports, 2005-2018

Putting These Trends into Context

It is important to put carbon trade—both implicit and explicit—into context. Europe has seen a large decline in direct CO2 emissions in recent years (roughly -30% since 2005) on the back of falling fossil energy consumption. Combined with the modest increase in European net CO2 imports (both implicit and explicit) over that period, net CO2 imports are roughly equivalent to all direct European CO2 emissions. Explicit CO2 imports, moreover, are roughly three times greater than embedded CO2. In 2018[6] Europe’s net CO2 direct imports were 2.24 Gt compared to a 0.58 Gt of embodied CO2 imports. Thus, imposing a comprehensive CBA (i.e., including explicit carbon) would have a much greater impact than just regulating embedded CO2.

US CO2 imports (net of implicit and explicit CO2 trade) were about 0.8 Gt in 2018, equivalent to a much smaller share (about 15%) of domestic CO2 emissions from energy consumption. Note, however, that continued growth of US fossil energy exports after 2018 suggests that US net CO2 imports are likely to have declined further in more recent years. With the US now a net exporter of fossil fuels (and explicit carbon), its net position as a CO2 importer is entirely due to embedded CO2. However, the US is a much smaller net importer than it may seem using only the OECD’s estimate of embedded CO2 trade. Although the magnitude of US explicit carbon trade was a mere 0.047 Gt imported in 2018, there has been a dramatic shift in the numbers since 2005. In 2005, the US imported approximately 1.7 Gt of CO2. If this trend continues, the US is on the road to become a significant exporter of CO2 with significant ramifications for the analysis of the economic impact of a comprehensive CBA.

In China, finally, net CO2 imports were equivalent to just 10% of domestic direct CO2 emissions from fossil fuel combustion. Imports of explicit CO2—in the form of fossil fuel imports—are more than double exports of implicit/embodied CO2.

The bottom line is that analysis of net trade in embodied and explicit carbon is essential to understand the full economic implications of potential CBAs. Focusing only on embodied carbon trade could lead policymakers to misjudge the economic impact of a comprehensive border adjustment. Rather, to understand the complete economic implications of a CBA, “total” (explicit + embodied) carbon imports should be the basis for discussion.

Policy Recommendations/Conclusion

It is evident that a carbon border adjustment will have various impacts for different countries. While acknowledging the massive uncertainties around the exact form of potential CBA regimes, we consider the implications of the preceding analysis of a potential comprehensive CBA regime that applies to all forms of CO2 trade—embodied and explicit—as well as targeting both imports (via fees) and exports (via rebates to domestic producers).

In such an example, the EU would benefit from a comprehensive CBA, as it is both an importer of explicit carbon and embodied carbon. Imposing a CBA would help domestic manufacturing industries that face stricter domestic environmental regulations, helping to prevent “carbon leakage.” The domestic fossil energy industry would benefit from fees on fossil energy imports. While the industry is relatively small, it is nonetheless significant, accounting for roughly one-quarter of European oil consumption, 40% of natural gas, and 60% of coal. Moreover, domestic energy production of non-carbon energy forms, which is already growing rapidly, would gain a competitive advantage against imported fossil energy. Finally, the size of the EU net CO2 trade relative to the bloc’s direct emissions suggests that a comprehensive CBA could have relatively large implications for CO2 emissions, trade balances, and potentially currency movements: Net fossil energy imports are roughly equivalent to two-thirds of Europe’s total CO2 emissions from energy use.

On the other hand, the story for the US and China is a bit more complicated. The US is in a unique situation as the country has shifted from being a net importer of explicit carbon to a net exporter, which has driven a steady declining trend for the total net imported carbon. This signifies that a comprehensive CBA, while protecting domestic manufacturing, might also require large rebates to domestic energy exporters (if similar climate policies are not in place with US trading partners) or could entail significant damage to domestic fossil energy producers (if the border adjustment succeeds in spurring widespread adoption of more aggressive climate policies). Moreover, wide regional disparities in manufacturing and energy production mean the economic implications of such measures would vary. Finally, overall trade in carbon (both embodied and explicit) is a relatively small share of the US carbon balance when compared to Europe: Net fossil energy trade is a tiny share of total CO2 emissions from energy use.

China’s situation is the opposite of the US: China is a large exporter of embodied carbon but an even larger importer of explicit carbon. As an exporter of embodied carbon, the Chinese economy would be detrimentally affected if their trading partners started to impose CBAs, if the development of China’s own carbon-pricing program is not deemed sufficiently aggressive by its trading partners. On the other hand, a Chinese border adjustment would benefit Chinese domestic fossil energy producers at the expense of foreign competitors who failed to adopt similar policies. Moreover, policies that dramatically reduced Chinese fossil fuel consumption and imports would improve the country’s balance of trade. Finally, net energy trade is a relatively small share of the country’s overall energy use and CO2 emissions (roughly 25%), though the implications would vary dramatically by fuel, since oil is mostly imported and coal is mostly produced domestically.

Interestingly, this (admittedly simplified) analysis suggests that the US, Europe, and China are all net importers of carbon when both implicit and explicit carbon trade are considered. This indicates a potential high-level alignment of interests regarding future implementation of a potential border adjustment regime.

As governments around the world continue endorsing green policies, interest in CBAs has been growing. The discussion of a CBA is still in its infant stage in the US and globally, but there needs to be careful consideration before moving forward with the issue.

Despite the benefits that a CBA would bring to domestic producers of manufactured goods, there is the question of how the CBA would affect overall trade and social welfare, as well as the fossil energy industry itself. Understanding the trade in both implicit and explicit CO2 is key for both the potential macroeconomic implications of a carbon border adjustment, as well as the industry-specific (microeconomic) impacts.[7]

On a macroeconomic level, a CBA would act as an additional cost for imports based on their carbon content and would reduce the total volume of imports into the country. Further, a comprehensive CBA would refund the cost of domestic climate policies for exporters, potentially boosting exports. Combined, these impacts would result in a net change toward a positive trade balance, which in turn would lead to an appreciation of the nation’s currency—especially if carbon-intensive trade is large relative to the domestic economy.[8]

From a microeconomic perspective, the impact of a CBA would be heterogeneous across differing industries. Overall, there would be a rise in cost, and firms would have to reoptimize their operations. The extent of this impact would depend on how closely the industry is reliant on the goods impacted by the CBA, as well as the respective, industry-specific elasticities of supply and demand that determine the incidence of a tax.

References

bp. 2021. bp Statistical Review Of World Energy 2021. https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf.

Campbell, Erin, Anne McDarris, and William Pizer. 2021. “Border Carbon Adjustments 101.” Resources for the Future, November 10, 2021. https://www.rff.org/publications/explainers/border-carbon-adjustments-101/.

Collins, Gabriel, Kenneth B. Medlock III, Anna Mikulska, and Steven R. Miles. 2022. Send Lawyers, (GAS) and Money: Executive Summary for ‘Strategic Response Options If Russia Cuts Gas Supplies to Europe. Rice University’s Baker Institute for Public Policy, Houston, Texas. February 21, 2022. https://www.bakerinstitute.org/research/send-lawyers-gas-and-money-executive-summary-for-strategic-response-options-if-russia-cuts-gas-suppl.

Cook, Troy, and Jack Perrin. 2016. “Hydraulic Fracturing Accounts for about Half of Current U.S. Crude Oil Production.” Today in Energy, U.S. Energy Information Administration (EIA), March 15, 2016. https://www.eia.gov/todayinenergy/detail.php?id=25372.

Council of the EU. 2022. “Council Agrees on the Carbon Border Adjustment Mechanism (CBAM).” Council of the EU Press Release, European Council, March 15, 2022. https://www.consilium.europa.eu/en/press/press-releases/2022/03/15/carbon-border-adjustment-mechanism-cbam-council-agrees-its-negotiating-mandate/.

Finley, Mark, and Jim Krane. 2022. Reroute, Reduce, or Replace? How the Oil Market Might Cope with a Loss of Russian Exports after the Invasion of Ukraine. Rice University’s Baker Institute for Public Policy, Houston, Texas, March 10, 2022. https://doi.org/10.25613/5DX9-P121.

Friedman, Lisa. 2021. “Democrats Propose a Border Tax Based on Countries' Greenhouse Gas Emissions.” The New York Times, July 19, 2021. https://www.nytimes.com/2021/07/19/climate/democrats-border-carbon-tax.html.

Joselow, Maxine, and Vanessa Montalbano. 2022. “Analysis | Republicans Are Embracing Carbon Border Fees to Counter Putin.” The Washington Post, March 2, 2022. https://www.washingtonpost.com/politics/2022/03/02/republicans-are-embracing-carbon-border-fees-counter-putin/.

Nicholls, Mark. 2022. “CBAM Advances, but Big Battles Remain.” Energy Monitor, April 4, 2022. https://www.energymonitor.ai/policy/cbam-advances-but-big-battles-remain.

OECD (Organisation for Economic Co-operation and Development). “Input-Output Tables.” https://www.oecd.org/sti/ind/input-outputtables.htm.

PwC. 2021. “Carbon Taxes and International Trade: What Are the Key Issues.” August 2021, https://www.pwc.com/us/en/services/tax/library/carbon-taxes-and-international-trade-what-are-the-key-issues.html.

Ricker, Corrina, and Albert Painter. 2020. “The United States Is Projected to Be a Net Exporter of Crude Oil in Two AEO2020 Side Cases.” Today in Energy, U.S. Energy Information Administration (EIA), February 12, 2020. https://www.eia.gov/todayinenergy/detail.php?id=42795.

Sato, Misato. 2013. “Embodied Carbon in Trade: A Survey of the Empirical Literature.” Journal of Economic Surveys 28, no. 5 (2013): 831–861. https://doi.org/10.1111/joes.12027.

U.S. EIA (Energy Information Administration). 2021. “U.S. Energy Facts — Imports and Exports.” May 17, 2021. https://www.eia.gov/energyexplained/us-energy-facts/imports-and-exports.php?fbclid=IwAR2L8l2K-tJyjAePjrAyEOZxDzDd3AgumIRPMjAODuMiuogQP6iFVzTbXCY.

Yamano, Norihiko, and Joaquim Guilhoto. 2020. “CO2 Emissions Embodied in International Trade and Domestic Final Demand.” OECD Science, Technology and Industry Working Papers, 2020. https://doi.org/10.1787/8f2963b8-en.

Endnotes

[1] Input-output tables show the flow of intermediate and final goods within an economy (OECD).

[2] Explicit carbon is defined as carbon content that is associated with the fuel itself. Therefore, carbon emissions associated with producing, transporting, and refining fuels will be associated with embedded carbon. In addition, this paper uses the aggregate carbon emissions associated with each fuel for each country and does not differentiate between different products. For example, Saudi oil production is known to have a low carbon intensity, but this difference in “quality” is not incorporated in this paper’s analysis; again, such a distinction would be treated as embedded in our framework.

[3] Note that we use bp’s designation of “Europe” for this exercise, rather than the EU, because bp fossil fuel trade data does not break down the EU for all forms of fossil fuels.

[4] All data, apart from the embedded carbon (from OECD), is acquired from the bp Statistical Review of World Energy and authors’ calculations.

[5] Graphs of US oil, natural gas, and coal consumption and production are in the appendix.

[6] 2018 is the year of reference, as this is the most recent year provided in the OECD embodied carbon dataset.

[7] The overall effect of a CBA on society is further muddled by the fact that the burden of the tax will depend on the elasticity of demand for the goods that are affected. From a social welfare perspective, there needs to be further discussion on the loss of consumer surplus and the gain of producer surplus from a CBA. Such issues are beyond the scope of this study.

[8] This prospective analysis is premised on a status quo assumption that there are no trade retaliations from the country’s trading partners in response to the institution of a CBA.

Appendices

Appendix 1

Appendix 2

Figure 2a — US Oil Production and Consumption

Source: bp, Statistical Review of World Energy 2021, 70th edition, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf.

Figure 2b — US Natural Gas Production and Consumption

Source: bp, Statistical Review of World Energy 2021, 70th edition, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2021-full-report.pdf.

Figure 2c — US Coal Production and Consumption

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.