Introduction

For many decades, academics, researchers, and policymakers have debated the role of foreign direct investment (FDI) in economic and social development. This subject has been difficult to elucidate. Not only has the discussion been colored by many ideological positions, but the fundamental characteristics of cross-border investment have evolved over time. Moreover, the features of FDI flows have recently diverged from traditional paradigms. First, over the last five decades, FDI was typically visualized as a flow of capital moving from big multinational enterprises (MNEs) in industrialized countries in the north to developing countries in the south; this FDI traditionally aimed at exploiting natural resources in the south (e.g., Chile and Peru) or substituting trade as a means to serve their domestic consumption markets (e.g., Mexico and Colombia). Today, FDI no longer just flows from “north” to “south,” but also from “south” to “south” and from “south” to “north.” FDI is not only carried out by large MNEs, but also by relatively smaller firms in developing countries that are investing beyond their home countries.

Further, until the 1980s, FDI was conceived of as an alternative to trade in serving a market, in the sense that exporting firms could either export from their home country or locate their factories in their target markets. Today, FDI is no longer a substitute for trade; it is quite the opposite. FDI has become part of the process of international production by which investors locate in one country to produce a good or a service that is part of a broader global value chain (GVC). Investors, then, have become traders and vice versa.

Last but not least, another key shifting paradigm relates to the modalities through which investment is carried out. Cross-border investment is no longer only about portfolio investment and FDI. International patterns of production are leading to new forms of cross-border investment in which foreign investors share their intangible assets, such as know-how or brands, in conjunction with local capital or tangible assets owned by domestic investors. This is the case of non-equity modes of investment (NEMs) such as franchises, outsourcing, management contracts, contract farming, or manufacturing (e.g., instead of establishing a manufacturing affiliate in a foreign location, companies can outsource production to an independent manufacturer that will produce under the specifications provided by the buyer in exchange for a commitment of the latter to acquire the production manufactured under the contract).

As stated above, today most developing countries are becoming sources of FDI. However, this phenomenon has not yet been studied in detail, as most research on FDI has been focused on flows from developed countries. This is due to the fact that historically, advanced economies have hosted the vast majority of transnational corporations, whereas developing countries have been mostly recipients rather than exporters of FDI. A number of researchers have acknowledged that outward foreign direct investment (OFDI) encourages economic cooperation and global integration between the source and host countries. This cooperation results in technology and skill transfers, the sharing of knowledge, access to international brand names and global markets, and global resources and income generation for the home country.1 The key question that naturally arises with the surge of OFDI, particularly in emerging economies, is whether the current internationalization of firms will help these economies sustain long-run economic growth and, if so, to what extent. It is common knowledge that inward FDI is an effective instrument in the creation of domestic production and employment in an economy. The question is how home countries can benefit from OFDI and use it as a tool to further integrate their economies into GVCs and generate more and better jobs.

This brief focuses on Latin America. Its objective is not to answer the broad question of the impact of OFDI on emerging and developing countries in terms of development, which is a new area of research yet in development.2 The goal is to describe the phenomenon and to highlight some of the areas where policymakers should focus in order to reap the benefits of OFDI. Moreover, given the relevance of economic integration in trade and investment flows, the focus of this brief is on the dynamics between the four countries of the Pacific Alliance,3 namely, Mexico, Colombia, Peru, and Chile.

Motivations Driving OFDI in Latin America

According to several studies,4 there have been several waves of internationalization by firms from developing economies. The first wave, in which Latin American countries participated (specifically Argentina, Brazil, Colombia, Mexico, and Venezuela), took place in the 1960s and 1970s. Most of the operations undertaken by Latin American firms targeted regional economies for their expansion and generally sought a local partner to be able to serve internal markets. Frequently, the operations were preceded by exports to the receiving country and were motivated by existing barriers to trade of different kinds (both de jure and de facto).

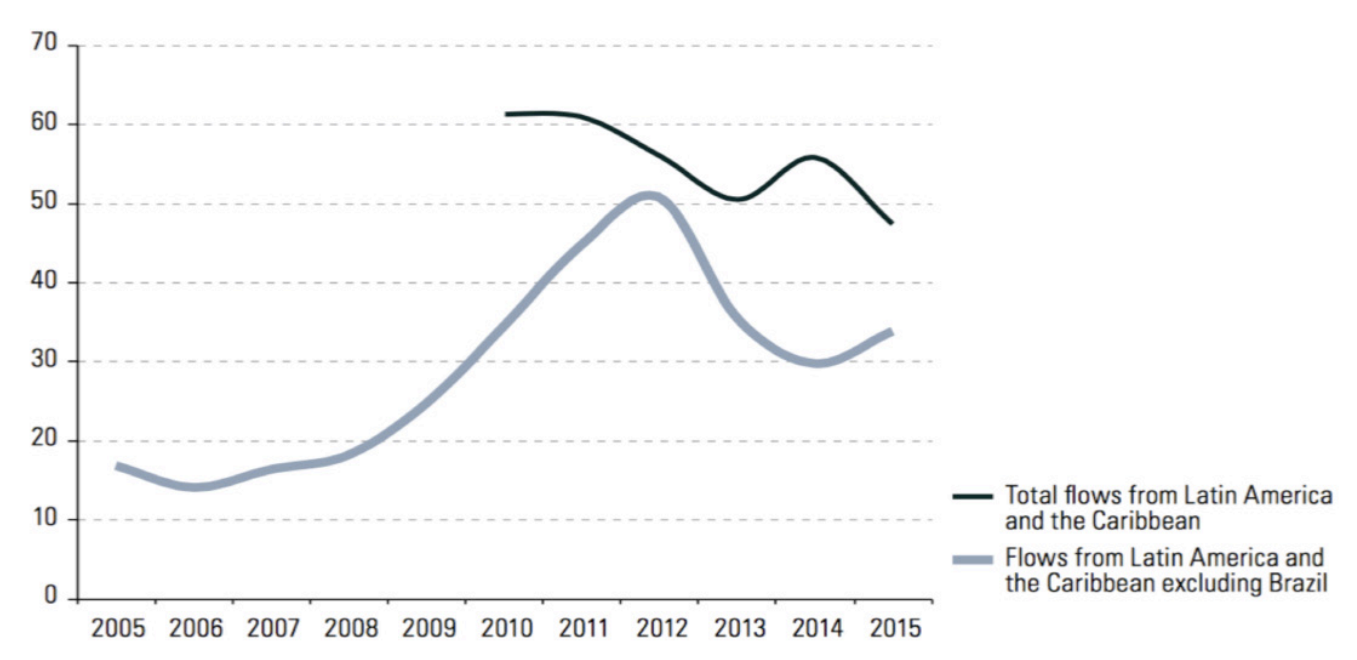

Figure 1 — Latin America and the Caribbean: Outward FDI Flows, 2005–2015 (Billions of Dollars)

Source Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of official figures and estimates as of May 27, 2016.

During the 1980s, Latin America went through a deep debt crisis, structural adjustments, and stabilization policies. These made the region miss the second wave of internationalization led by Asian countries like Singapore, South Korea, and Malaysia. From the 1990s until the early 2000s, the region received large amounts of FDI following the reform and liberalization processes of the previous decade. This increased competition in Latin American economies—and the rise of domestic enterprises’ performance—positively affected OFDI flows since companies were more prepared to face new challenges, which increased the number of Latin American companies investing abroad.

Economists have developed different theories explaining the emergence of firms in developing countries, e.g., the eclectic paradigm of John H. Dunning, the internationalization theory, and the investment development path (IDP) theory.

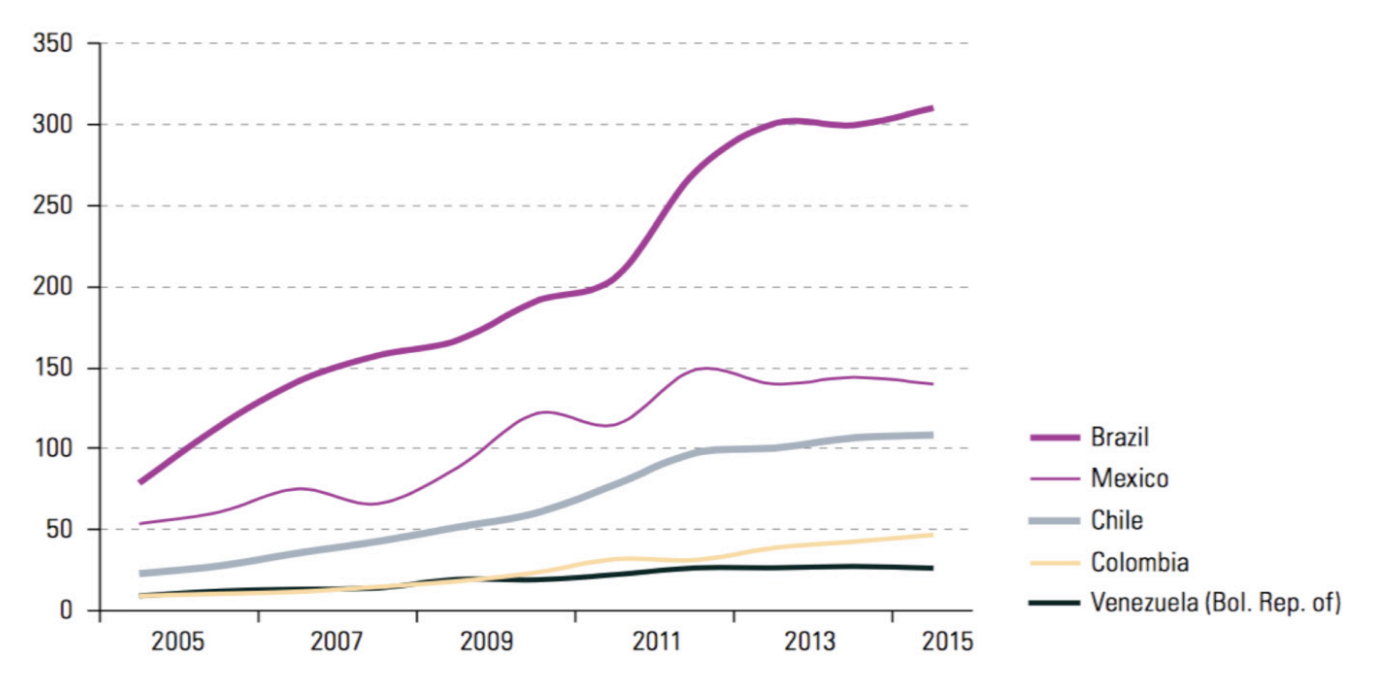

Figure 2 — Selected Latin American Countries: Stock of FDI Abroad, 2005–2015 (Billions of Dollars)

The eclectic paradigm (also called the “OLI paradigm”) suggests that firms invest when three conditions are satisfied: ownership advantages (O), location advantages (L), and internationalization advantages (I).5 The internationalization theory (or “Uppsala model”)6 focuses on the different stages of a firm’s internationalization process based on the idea of “incremental learning”: (i) no exports but increased knowledge of a foreign market; (ii) occasional exports through an agent; (iii) transactions in the foreign market through agents or subsidiaries; (iv) establishment of a subsidiary in a foreign market; and (v) production in a foreign market. This theory further suggests that a firm with a competitive advantage in its domestic market will seek to move abroad to exploit that advantage. According to this model, firms usually invest in a particular country or region with characteristics similar to their domestic markets.7

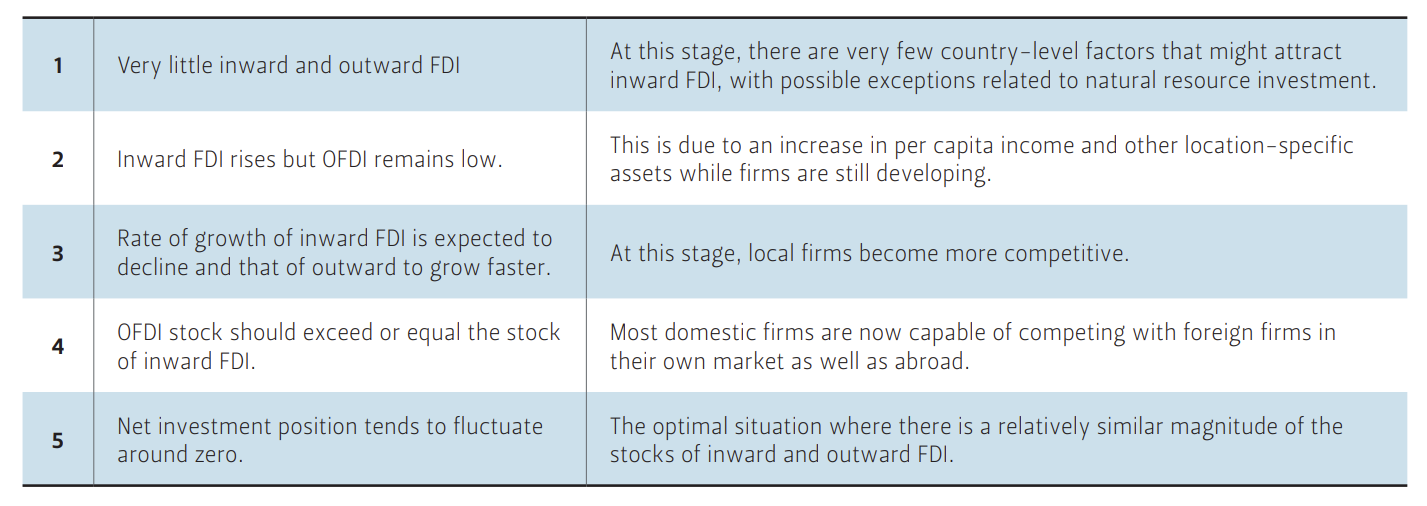

Finally, the IDP theory argues that as countries become more industrialized or developed, their firms are likely to build up company-specific advantages and so are able to compete more effectively at the international level.8 The IDP theory suggests that countries tend to go through five stages as outlined in Table 1.

Table 1 — Investment Development Path Stages

OFDI Trends in Latin America and the Pacific Alliance

OFDI is no longer a phenomenon restricted to developed economies; rather, it is an emerging trend in economies in development. OFDI from emerging economies was almost nonexistent 20 years ago. This has changed dramatically. In 2015, according to the United Nations Conference on Trade and Development’s (UNCTAD) 2016 World Investment Report,9 OFDI from developing and transition economies accounted for USD409 billion, representing 27.7 percent of the total FDI flows worldwide. In the case of Latin America, according to the same source, OFDI reached USD10 billion a year in the late 1990s, increasing to an average of USD36 billion between 2006 and 2012. Between 2013 and 2015, in a difficult economic period for the region, OFDI from south of the Rio Grande has slightly increased, from USD31 billion in 2013 to USD$33 billion in 2015.10

Today, more than 90 percent of OFDI from Latin America comes from only four countries: Chile, Brazil, Mexico, and Colombia. In 2015, Chile was the leading source of OFDI with USD15.8 billion, followed by Brazil with USD13.5 billion, Mexico with USD1.2 billion, and Colombia with USD4.2 billion.11 The increase of OFDI, from these four countries in particular, can be explained by the following factors: (i) sustained economic growth in the region; (ii) access to natural resources at a time of high commodity prices; (iii) regional economic integration efforts through the negotiation of Free Trade Agreements (FTAs); and (iv) a regulatory framework that has remained open to both inward and outward FDI in generally all sectors.

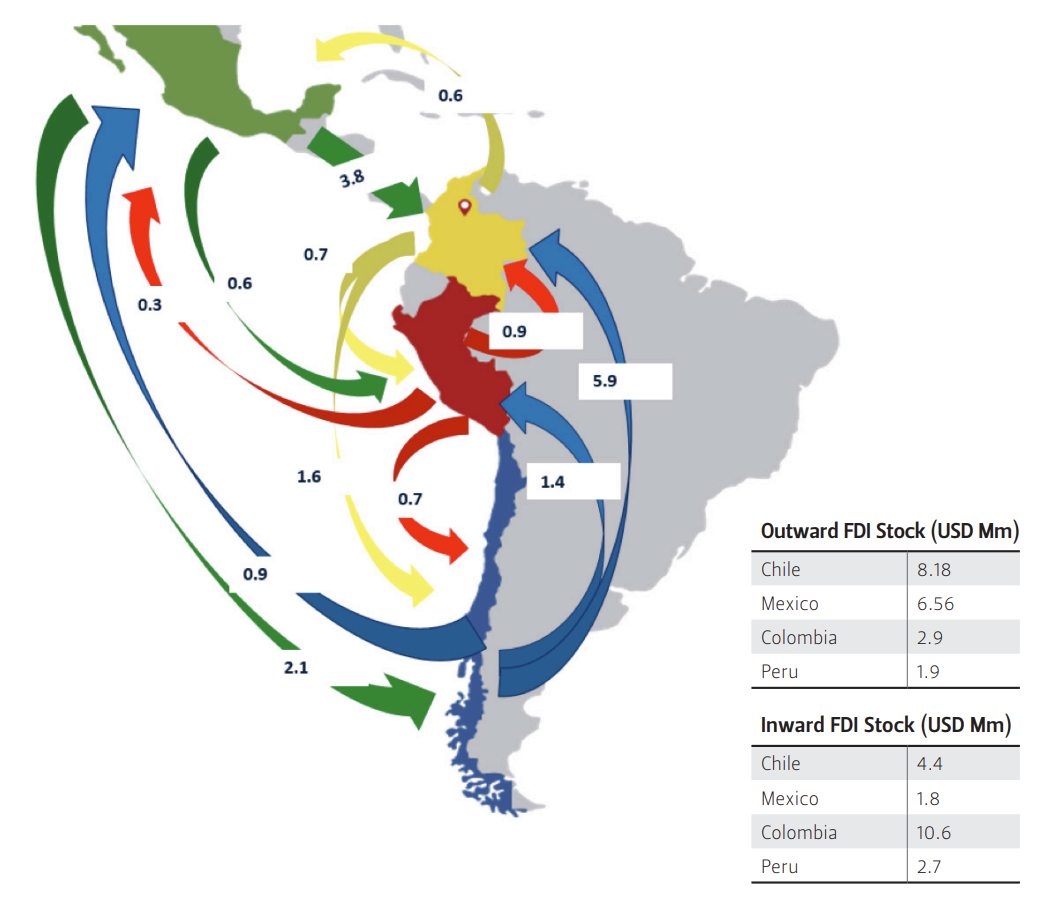

Figure 3 — Bilateral Stock of FDI in the Pacific Alliance Country Members

Source Authors’ calculations.

One of the most recent regional integration initiatives in Latin America is the Pacific Alliance. It commits the four member states to in-depth integration aimed at the free circulation of goods, services, capital, and people by facilitating trade and investment. The Pacific Alliance ranks as the eighth largest economy in the world in terms of GDP; it received more than 44 percent of FDI to Latin America in 2013.12

The analysis of intra-Alliance FDI data shows the following main trends: First, Colombia stands as the main receiver of FDI, with an FDI stock from Alliance members of close to USD10.6 billion. Chile, Peru, and Mexico follow, with stock values of USD4.4, USD2.7, and USD1.8 billion, respectively. If we turn our attention to the outward dimension of FDI, Chile is the country with the largest stock of outward FDI compared to other members of the Alliance. In 2015, this stock reached USD8.2 billion, which was above the outward stock of Mexico (USD6.6 billion), Colombia (USD2.9 billion) and Peru (USD1.9 billion).

Notwithstanding the previous trends, intra-Alliance FDI remains a modest share of the FDI received by all member countries. In Colombia, the country with the largest relative exposure to FDI from Alliance countries, the share of intra-Alliance FDI is 8 percent of total inward stock. Chile and Peru are at a distant second and third, with 3.8 percent and 3.5 percent, respectively. Finally, the same share in Mexico is virtually negligible, at 0.4 percent of FDI stock.

Intra-Alliance FDI flows were very limited until the mid-2000s, with sporadic peaks associated with single FDI operations of relatively high value. Within this general pattern, Chile has exhibited a more stable pattern, particularly as an outward investor in other Alliance countries. Intra-alliance FDI shows a substantial degree of heterogeneity across investment types. First, market-seeking investments generally appear as the driving motivation for a large share of intra-Alliance FDI. Beyond this general trend, there is a noticeable divide between South American members and Mexico. Resource-seeking FDI is of relatively high importance in South America; in contrast, inflows from Alliance members in Mexico involve a wide array of manufacturing industries, under both efficiency and market-seeking investment types.

The Pacific Alliance’s Framework Agreement declares that, as a fundamental part of the plan to achieve its objectives, efforts should be directed toward the free trade of goods and services, the free movement of people and capital, and the development of cooperation mechanisms to encourage investment. With this in mind, the member countries of the Alliance in early 2014 signed an Additional Protocol to the Pacific Alliance Framework Agreement. The protocol defined the actions and guidelines needed to achieve the proposed objectives. As part of this effort, Pacific Alliance member countries are reviewing and completing their legal framework in order to promote the achievement of these goals, based on four fundamental pillars of the Framework Agreement;13 this includes creating an investment climate that will enable an increase in the intra-Alliance FDI flows.14

Concluding Remarks

In today’s international economic context, most Latin American countries—in particular members of the Pacific Alliance—are showing an increase in OFDI flows. The motivation of firms to invest abroad could be to access new markets by getting closer to their customers, to obtain advanced technologies that otherwise would take too much time and too many resources to develop, or to seek lower production costs by adopting regional strategies. From a policymaking perspective, it is fundamental to understand the internationalization path of firms so that governments can design and implement policies that will foster OFDI with the ultimate objective of creating linkages and spillovers in the local economy, particularly in terms of domestic investment and exports.

For developing economies, strategic asset-seeking outward direct investment can play a very important role. It facilitates the acquisition of capacities, processes, knowledge, and markets that otherwise would be difficult to acquire. According to a number of studies,15 not many trans-Latin firms have implemented strategies following this approach. Looking for lower cost or more efficient options to manufacture their products has not been an option either.16 The reality is that most of these trans-Latin firms invest in search of new markets (or natural resources), mostly within the region. Their goal is to succeed by implementing business strategies similar to those that already worked in their home economies.

To conclude, OFDI from emerging markets is changing the international investment landscape. It has gradually but decisively grown since the turn of the century, accelerating rapidly following the global financial crisis. It is likely that this trend will continue, and the relative share of emerging markets OFDI in global FDI will only grow. The earlier experience of advanced markets has shown that outward investment can affect home market growth, employment, and domestic investment, but more evidence is needed to examine these effects in the context of emerging markets. Nevertheless, the existing evidence is sufficiently strong such that policymakers may wish to consider how OFDI can be folded into national development strategies, especially by targeting outward investment (depending on the intended home effect) and increasing absorptive capacity (often the main constraint to realizing full benefits for the home economy).

Endnotes

1. United Nations Conference on Trade and Development (UNCTAD),“Developing countries are beginning to promote outward FDI,” UNCTAD investment brief no. 4 (2006a).

2. For example, the Investment Climate Unit of the Trade & Competitiveness Global Practice at the World Bank Group is currently conducting empirical studies on the trends and impacts of OFDI in emerging and developing economies.

3. The member countries of the Pacific Alliance, established April 28, 2011, are Chile, Colombia, Mexico, and Peru.

4. See, for instance, D. Chudnovsky, K. Celso, and A. Bernardo López, Las multinacionales latinoamericanas: sus estrategias en un mundo globalizado, Fondo de Cultura Económica, 1999; E. Rivera Urrutia, N° 15, Empresas multinacionales latinoamericanas: Los casos de Brasil y Chile, 2014. Translation: D. Chudnovsky et al., Latin American multinationals: Their strategies in a globalized world, Economic Culture Fund, 1999; E. Rivera Urrutia, No. 15, Latin American multinational companies. The cases of Brazil and Chile, 2014.

5. John Dunning, “The Eclectic (OLI) paradigm on international production: past, present and future,” International Journal of the Economics of Business 8, no. 2 (2001): 173-90.

6. This theory explains how firms gradually intensify their activities in foreign markets. It was developed by the Swedish researchers Jan Johanson and Jan-Erik Vahlne, whose work was published in the Journal of International Business Studies in 1977.

7. Louis Brennan and Ruth Rios-Morales, “Foreign direct investment from emerging countries: Chinese investment in Latin America,” International DSI/ Asia and Pacific DSI, July 2007.

8. J.J. Duran and F. Ubeda, “The investment development path of newly developed countries,” International Journal of the Economics of Business 12, no. 1 (2005): 123-137.

9. UNCTAD, “World Investment Report,” 2016.

10. Economic Commission for Latin America and the Caribbean, “Foreign Direct Investment in Latin America and the Caribbean,” 2015.

11. Ibid.

12. Ibid.

13. The four pillars of the Pacific Alliance Framework Agreement are the free circulation of goods, services, capital and people.

14. The Investment Climate Unit of the Trade & Competitiveness Global Practice at the World Bank Group is working with Pacific Alliance country members to improve their investment climate in order to foster intra-regional FDI.

15. M. Pérez Ludeña, “Multinational enterprises from Latin America: Investment strategies and limits to growth and diversification,” Transnational Corporations Review 8, no. 1 (2016): 41-49.

16. In 2011, Mexico’s PEMEX unsuccessfully tried to acquire Spain’s Repsol to obtain the Spanish company’s drilling technologies.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.