Author(s)

Last month, China’s National Development and Reform Commission (NDRC) released its 14th Five-Year Plan (FYP) (2021-2025) for the energy sector. Clean, low-carbon, safe and efficient are the keywords in the energy plan, consistent with the outline released in March last year. The 2025 targets in the FYP can be categorized into two themes: (1) Enhance energy security by ramping up domestic production, and (2) peak carbon emissions by 2030 and reach carbon neutrality by 2060. Given that currently half of China’s installed electricity generation capacity is coal, the latter target would imply phase-out of coal generation, wouldn’t it?

Well … not so fast.

As of February 2022, China has 2,390 GW installed capacity, which, besides coal, includes 17% hydro (390 GW), 14% wind (330 GW), 14% solar (320 GW), 5% natural gas (108 GW), and 2% nuclear (53 GW). Coal’s dominance is even more pronounced when one considers actual electricity generation, a whopping two-thirds of which comes from burning coal.

The latest FYP plans on an increase of total installed electric generation capacity to 3,000 GW by 2025. China also plans to increase the share of non-fossil fuels in total electricity generation to 39% and increase the percentage of electricity in total final consumption to 30%.

To decarbonize the electricity mix, the FYP sets the capacity target for the two zero-carbon fuel sources, hydro and nuclear respectively at 380 GW and 70 GW by 2025, which would be 12% and 2% of the 3,000 GW capacity target respectively. In other words, hydro would account for a smaller share of total fuel mix and nuclear remains the same as it is today. It seems like the country is well on its way, as China exceeded its 2025 goal for hydropower already, with 390 GW of installed capacity providing 15% of the country’s power supply in 2021.

Nuclear is at 75% of the 70 GW target. While only 2 GW of nuclear capacity became operational last year, the country has been ambitiously developing nuclear power projects with 14 GW of confirmed capacity under construction and additional 47 GW announced.

But for installed capacity to reach 3,000 GW by 2025, China will need to fill the remaining 610 GW with renewables and more coal.

Admittedly, China is rapidly expanding its renewables. It is currently the largest wind power producer globally and shows no signs of slowing its capacity additions. The government has recently announced plans to add 450 GW of wind and solar in the Gobi Desert in northern China.

However, renewables like wind and solar rely on the weather and cannot be stored at scale with existing technology. This results in a significant disconnect between installed capacity and actual power generation that renewables provide. For example, in 2021, wind accounted for 14% of China’s installed capacity but only generated 7% of the electricity. The intermittency of growing renewable capacity also means that there is an increase in for balancing by a stable and dispatchable baseload such as coal or natural gas. The former is the more likely choice for China, since China is the world’s largest producer, importer and consumer of coal. In fact, China’s coal consumption has more than doubled since 2000. And while coal’s share in the total energy mix has declined, it still constituted over 55% in 2020. Petroleum, natural gas and non-fossil-fuel sources accounted for 18.9%, 8.4% and 15.9%, respectively. Besides, coal consumption is not decreasing in absolute terms. The actual volume of coal consumed in China has been increasing since the seeming plateau around 2015, and just saw its largest annual growth of 4.6% in a decade.

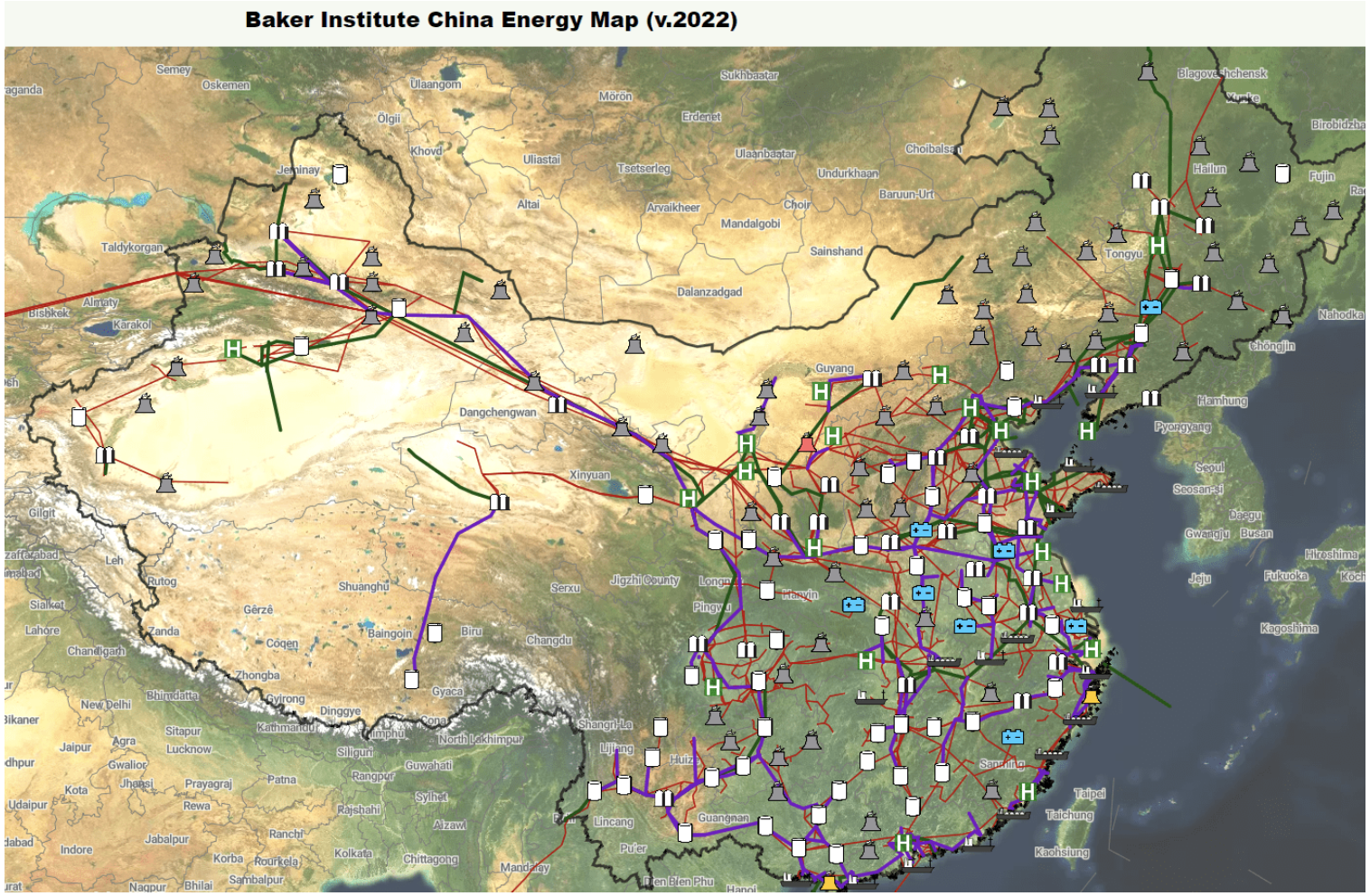

In addition, China’s coal fleet has been growing consistently, with approximately 40 GW of new capacity additions per year since we began mapping it in 2019. Today, the country operates just under 3,000 coal power plants with a 1,110 GW total capacity. (See Figure 1, interactive map available here.) That’s about the size of the United States’ entire power supply. China has added 20 GW to the grid within a year, with 250 GW announced or under construction.

Figure 1 — Baker Institute China Energy Map, version 2022

To ensure reliable supply and avoid power outages like last winter, China is mining more coal than ever. In 2021, China’s coal production reached a record high of 4 billion tonnes, accounting for half of the global output. In addition, the average age of China’s coal fleet is only 14 years old, with at least two decades of life before retirement.

What about the alternatives?

Natural gas can provide residential heating and serves as baseload in countries like the U.S. But in China, natural gas infrastructure development began much later.

For residential heating, China only started converting coal to gas heating to address air pollution (and not CO2 emission!) less than a decade ago. The spiking gas demand from the switch was more than the country’s gas infrastructure was prepared to handle. And while this infrastructure is growing at a high pace, including pipeline gas transmission and liquified natural gas (LNG) terminals, most of the natural gas China will be consuming will need to come from abroad, a significant supply security concern the country will be taking into account when deciding on its energy mix.

The FYP does set out to increase domestic natural gas production to 230 BCM per year by 2025, a 10% increase from the 208 BCM produced in 2021. However, this is a moderate target given that domestic production has been growing at an average of 9% annually since 2017. As a result, natural gas only accounted for 6% of the total energy mix in 2020, in contrast to 68% coal.

Similarly, development of hydrogen economy is unlikely to oust coal in China in the near- to medium-term, at least. Rather, it relies on coal. Today, China produces 33 million tons of hydrogen annually, the largest in the world. Almost 80% comes from fossil fuels (more than 60% from coal and 14% from natural gas), and 20% from industrial by-products. According to a separate hydrogen development plan, China plans to produce 100-200 thousand tons of green hydrogen per year by 2025. But today, the estimated green hydrogen production — using renewables as power sources for electrolysis — is just under 27,000 tonnes per year.

So, how would Beijing manage to peak carbon emissions by 2030, while sustaining its economy and energy security? As discussed, China is actively pushing forward all options, from nuclear and hydro to natural gas and renewables. But, in all cases, coal will remain significant in China’s energy mix for years to come, as none of those can replace coal today as the national power engine just yet. And 2060 is far enough to bet on technology improving the odds to become carbon neutral; China seems to be willing to play those odds.

See the Baker Institute China Energy Map for more detail. We released the 2022 version, tracking over 5,200 infrastructure facilities, including oil and gas pipelines, refineries and storage, LNG terminals, coal, nuclear, and gas power plants, EV battery manufacturers, and hydrogen facilities.

This post originally appeared in the Forbes blog on April 26, 2022.