Experiments in Fiscal Governance: The Economic Reform Agenda in the GCC

The decline in oil prices in late 2014 precipitated a torrent of fiscal policy changes across the Gulf Arab states. These reforms covered sensitive issues such as labor market reform; financial sector liberalization; the introduction of consumption and land taxes; and removal or reduction of subsidies on electricity, water, and fuel. As a result, it is reasonable to expect some reconfigurations of state-society relations in the Gulf states. Yet there are few signs of public unrest or protest, even with higher costs of living and limited availability of public-sector jobs.

This muted reaction is a puzzle, at least as a short-term observation. But the shifts under way are structural, and society—both citizens and foreign residents—will likely take some time to fully absorb the impact.

At the same time, a number of global and regional political currents have strengthened authoritarian governance and diminished incentives for risk-taking in civil society. The outbreak of conflict related to the Arab Spring uprisings in Syria, Libya, Yemen, and Egypt has demonstrated the high risk of revolution and change in government. Shifts in American and European politics since 2016 have also reinforced negative perceptions of democracy and given rulers in the Gulf states (and across the Middle East and North Africa region) an opportunity to promote their own versions of nationalist growth agendas without external pressure on their methods of governance.

In effect, what we have witnessed since late 2014 is a new period of policy experimentation in which the ends of a diversified economy less reliant on oil exports justifies the means of achieving a radical break in a system of social welfare, changing employment preferences and practices, and establishing a new role for the state in prescribing an agenda for growth. The state remains central to the conception and execution of economic development, while Gulf citizens and residents are expected to either seize the opportunity, leave, or be left behind. This brief sets out some of the major structural reforms to taxes, subsidies, and debt issuance in the GCC that are shifting financial burdens from the state to its citizens and residents.

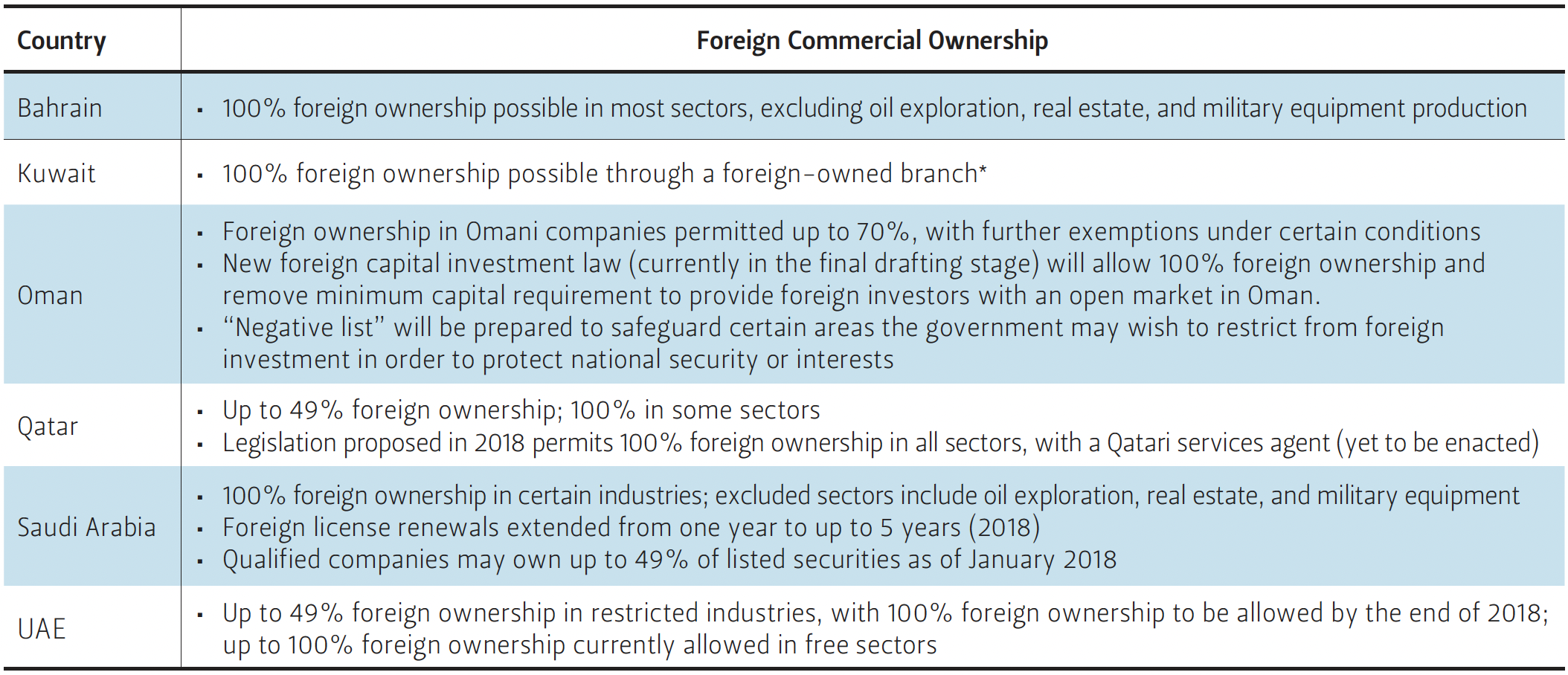

Figure 1 — Foreign Commercial Ownership Reforms in the GCC

Sources 2017 EU-GCC Investment Report; 2016 EY Global Tax Alert Library; Emirates News Agency.

Structural Barriers to Reform and Economic Growth

The grievances that motivated many of the Arab Spring uprisings were economic in nature: lack of social and economic mobility, corruption, and exclusion from opportunity. New research by scholars at the World Bank on the sources of the grievances, the demographic profile of protestors, and the puzzle of mobilization1 reveals how little has changed in terms of the structural barriers to inclusion that persist across the Gulf and the wider MENA region.2

Employment opportunities and lack of affordable housing remain key problems,3 especially for the current generation of young, media-savvy Arabs. The fiscal reform agenda has only heightened anxieties around public sector employment, while the cost of living has risen throughout the Gulf Arab states due to the imposition of new taxes and fees as well as reduced energy and water subsidies.

In this period of policy experimentation, we also find variation across the Gulf states in the implementation of reforms (particularly regarding the value added tax, which only the United Arab Emirates [UAE] and Saudi Arabia have instituted thus far), and also in the perception of the value of foreigners as workers and members of society.

All of the Gulf states aim to increase national employment in the private sector, but the policy prescriptions for how to create job opportunities have varied significantly. Saudi Arabia and Oman have seen an exodus of expatriate workers4 because of rising visa fees and higher costs of living, including school fees.5 Other states like Bahrain, the UAE, and Qatar have created more liberal policies to welcome foreign investors as long-term residents and to facilitate the retention of existing expatriates as a labor resource.

As governments in the region compete by offering stimulus packages and enticements to make their business environments more welcoming to foreign investors,6 they are weakening one of the key wealth redistribution tools utilized over the past 40 years: the commercial agency structures that required investors to partner with local citizens in order to establish franchises and foreign-owned firms.7

Jobs Crisis: Protecting and Creating Jobs for Nationals

Whereas foreigners are less welcome in Saudi Arabia, we see an acceleration in protection schemes for national employment. Saudization, or the reservation of certain jobs and sectors for Saudi nationals, is part of the government’s effort to reduce the public wage bill and transform its private sector. In January

2018, the government announced that it would expand its growing list of Saudi-only jobs to include sellers of watches, eyewear, medical equipment and devices, electrical and electronic appliances, auto parts, building materials, carpets, cars and motorcycles, home and office furniture, children’s clothing and men’s accessories, home kitchenware, and confectioneries.8

The experimental nature of Saudization raises questions about why certain sectors are targeted, and how smaller businesses will be able to assume the higher wage costs of hiring nationals. In theory, the policy should create opportunities for all Saudis, but its potential to increase jobs for Saudi women is especially promising. Yet few expect that Saudi citizens will be eager to take low-wage and menial jobs,9 particularly in construction.

In addition to Saudization, the kingdom has introduced a range of reforms10 to rationalize fuel and electricity costs, established a new value-added tax, and targeted cash support to lower income families through the Citizen’s Accounts Program. All of these measures have disrupted the economy, leaving families to try to establish a new monthly baseline for expenses. Energy prices have increased two-to three-fold in Saudi Arabia, and there was an 80 percent11 increase in gasoline prices at the end of 2017.12 Consumer sentiment among Saudis and foreigners alike is apprehensive. Just as the image of a Saudi woman soldier is testing the limits of popular culture, there is an unsettled sense of “What next?” in consumer confidence.13

The Reuters Ipsos consumer sentiment index from late 2017 for Saudi Arabia showed consistent negative expectations about jobs, investment, and growth.14 Indexes by IHS Markit and Emirates NBD indicate a sharp drop in the Purchasing Managers’ Index, declining from 57.3 in December 2017 to 53.0 in January 2018, the lowest reading in the survey’s history.15

This malaise is all the more troubling as it has been accompanied by the largest fiscal outlays in recent Saudi history. The Saudi budget expanded for 2018; combined with additional investment spending from the Public Investment Fund, approximately 340 billion riyals (about US$90.66 billion) in investment spending is planned for 2018.

For good measure, the government has delayed its commitment to a balanced budget until 2023. But spending its way out of the current slump includes inherent risks.

One key factor driving consumer sentiment, especially within the private sector, is the expatriate population—the unwitting victim of Saudi Arabia’s reforms. For those who stay, the rise in the cost of living has been substantial. And for those who leave, their absence is compounding weak economic activity. And many are leaving.

Expatriates, who make up one-third of the population in Saudi Arabia, are facing price increases without the cushion of the Citizen’s Accounts16—a program that offers direct cash transfers to low- or middle-income households—or the reinstatement of public sector allowances17 (issued by decree for 2018 only). And foreign workers are subject to a range of additional fees18 for dependents19 as well as other levies20 that citizens do not have to pay.

The rationale for the increased fees and taxes is to create an alternate stream of government revenue to offset losses in oil revenue that have been compounding since late 2014. Even though Saudi Arabia’s 2018 budget21 is its largest ever, it still features some cost-savings measures. Examples include price rationalization in the energy sector; attempts to cut the public wage bill; new taxes on tobacco and sugary drinks; plans to introduce road tolls; the implementation of a VAT on Jan. 1, 2018; new efforts to retroactively collect zakat (Islamic tax) from financial institutions;22 and a push to seize assets from public officials and members of the ruling family as well as large business conglomerates through an anti-corruption campaign.23

The UAE has also struggled to create jobs for citizens in the private sector, but its approach to expatriate workers has been very different from the Saudi “tax and levy” policy. Efforts to extend long-term residency,24 introduce new protections for investor’s rights, and even allow home-based businesses are designed to boost a private sector heavily reliant on foreigners as business owners and innovators.

Within the UAE, there is also competition for foreign expertise and investment. Abu Dhabi recently created a stimulus package25 for investment within the emirate to rival the vibrant private sector in Dubai.

Likewise, Bahrain has moved to allow long-term foreign residency,26 end its kafala system of requiring workers to have an employer sponsor their visa permits by allowing self-sponsorship (especially for lower wage workers), and introduce a number of reduced subsidies and increased fees for citizens.

Finding Revenue: Experimental Fiscal Policy

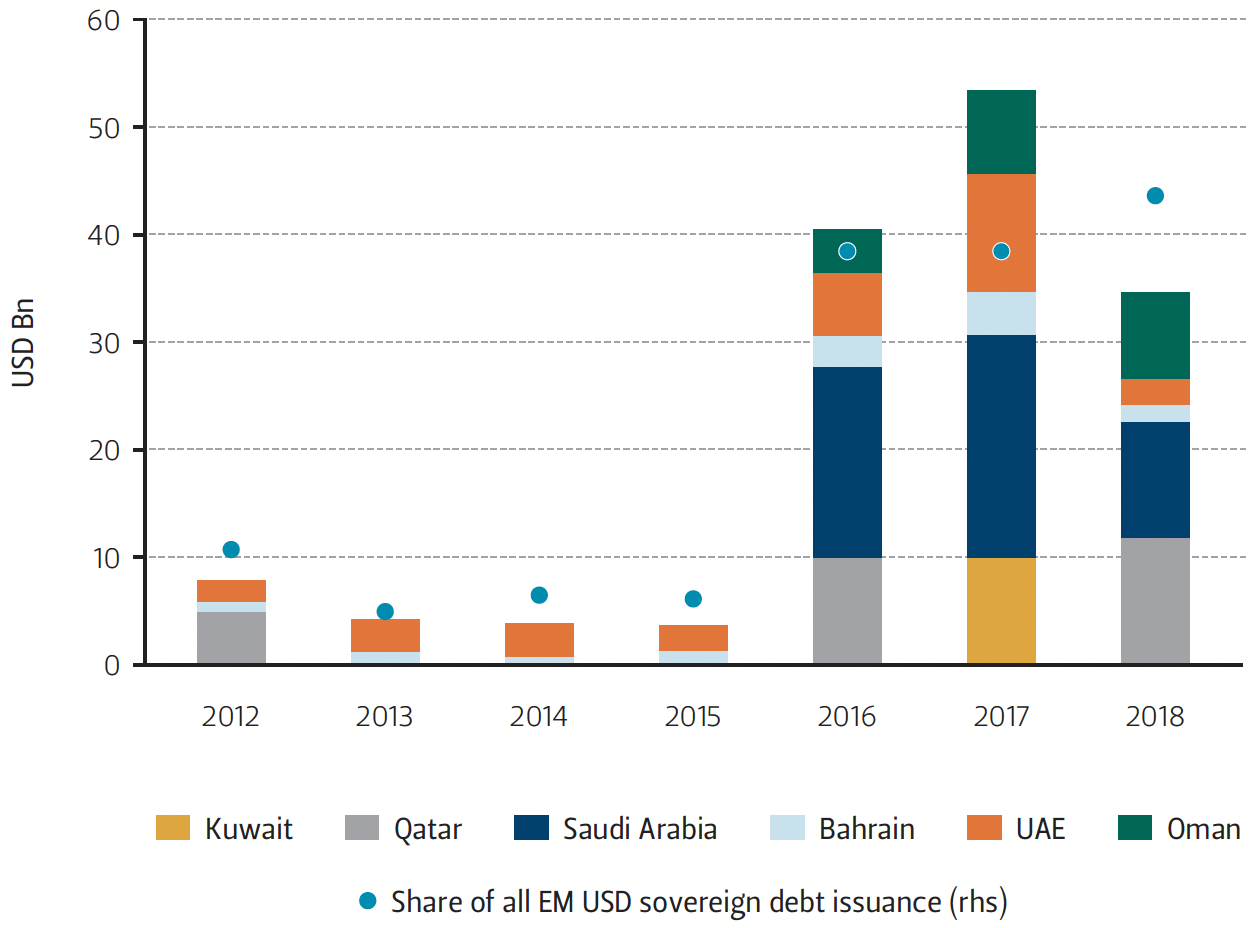

Fiscal policy experimentation has required innovation to create new sources of revenue as well as the issuance of debt. After decades of fiscal surplus and a very low debt-to-GDP ratio, Gulf states now find themselves heavily indebted, not just to their local banking sectors but to international banks and bondholders.

Moreover, the ability to access debt capital markets has created some competition among governments. Saudi Arabia and Qatar had dueling debt issuances in March 2018,27 with each attempting to one-up the other in the amount they could borrow.

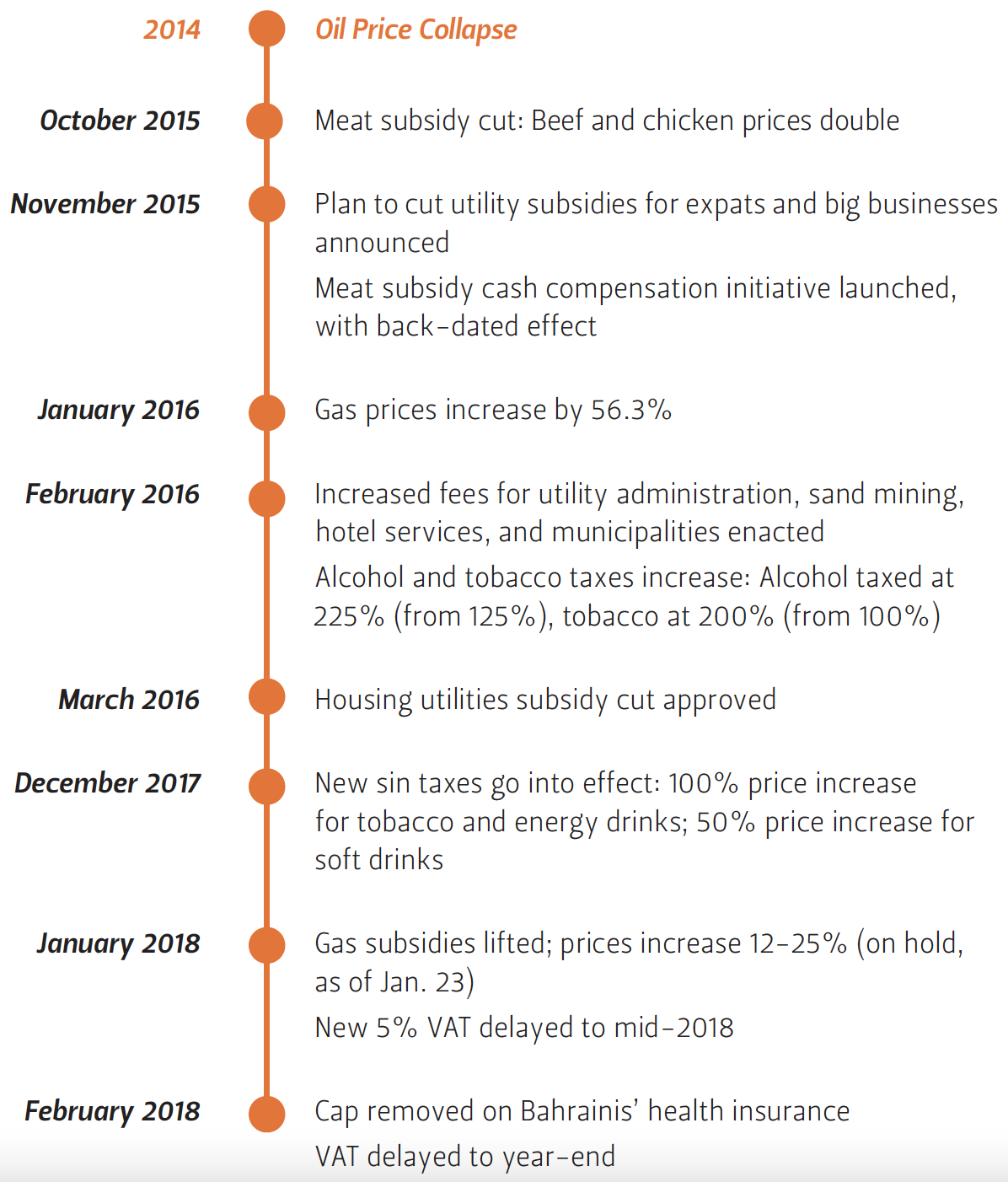

Figure 2 — Timeline of Economic Reforms in Bahrain

Meanwhile, for weaker economies like Bahrain and Oman, efforts to issue bonds and borrow from international banks have been complicated by assurances of support from regional backers. For instance, questions about financial support it received from Saudi Arabia affected Bahrain’s ability to issue a bond in March 2018. The conventional bond issue was canceled at the last minute,28 while a sukuk issue went to market.

This policy experimentation, coupled with very public efforts to raise capital, has somewhat lifted the veil of secrecy that has shrouded the fiscal affairs of Gulf governments. International bond issuances require some transparency; a bond prospectus should declare existing debt, possible avenues of growth, and government liabilities in spending. This information is public, which raises the possibility that citizens might access greater details about government expenditures and weigh that information against their own perceptions of service delivery and benefits.

Sensitive Benefits: Scaling Back the Welfare State

The wave of economic liberalization continues to spread across the region, opening paths to greater ownership stakes for foreign investors; allowing longer term residency permits untethered to employers; breaking down state subsidies on energy, fuel, and water; trimming public sector wage bills; and introducing consumption and “sin” taxes.29 Still, some social benefits30 deemed too sensitive to withhold remain.

Figure 3 — GCC Sovereign USD Debt Issuance (2012–2016)

Housing is perhaps the most sensitive of these social benefits and remains one of the key levers of domestic policy for Gulf monarchies. In the Gulf states, a number of factors have escalated the housing shortage and made housing less accessible for citizens, such as rapid population growth, a rising cost of living, and lifestyle expectations in a culture of wealth. In addition, an entrenched system of elite land ownership and state-led megaproject development has excluded average citizens from accessing finance and mortgage markets.

Increasing economic mobility, pathways to home ownership, and a sense of social mobility cannot be sustained without reforms to subsidies31 and cash transfers that address underlying inequalities.32 These include access to opportunity, increased land availability, access to financing, discouraging monopolies and state-linked corrupt firms, and protection of property owners’ rights.

Home ownership embodies the tension of inclusion and mobility, the underlying grievances that have motivated unrest across the MENA region. And across the Arabian Peninsula, from Kuwait33 to Oman, this tension has been simmering for years.

According to Reuters and property consultant firm Jones Lang LaSalle, the cost of a roughly 2,600-square-foot home in a major Saudi city is $186,000 to $226,000. This is 10 times the annual salary of a low-income family in the Gulf states. For example, Saudis who receive the Citizen’s Accounts stipend make about $2,660 per month, which is the average monthly salary in the kingdom.

The Citizen’s Accounts Program is mandated annually; thus, neither the next year's allocation nor who may qualify for the benefit is clear.34 In January, King Salman bin Abdulaziz granted additional stipends of $260 per month for all public sector employees for 2018 to offset cost of living increases.35

A 2014 study by Strategy& identified a demographic-driven surge in housing demand in the GCC states.36 The report estimated that based on the age distribution in Gulf states, with a median age of 29, young people considering marriage and families would trigger a housing shortage of 1 million units by 2018.

But more important than the large youth population in the Gulf is the problem of how and where young people are working, and how they are included in plans for job growth and productivity. Unfortunately, they have been excluded from economic opportunities, with high rates of unemployment blocking them from attaining financial independence.37 The Strategy& report states that in 2012, the average residential home in Kuwait was priced at 30 times the average gross income for a person between the ages of 25 and 29. In comparison, the average home price was 11 times the average young adult’s salary in Norway, and six times more than such workers’ earnings in the United States.

Implications

Economic inclusion in the Gulf states is a public policy priority. In housing and employment opportunities, Gulf governments are now forced to become more innovative in their policy choices by either mandating hiring of nationals or finding ways to incentivize foreigners to grow new businesses. How society will respond is still a very open question.

For now, Gulf citizens and expatriates have embraced change (or left the region). For those who stay, there will begin a new conversation about belonging and contributing to society in meaningful, financially productive ways. These are discussions that governments can dictate or choose to facilitate. The variation in approach across the Gulf could also be substantial.

This brief offers three policy recommendations:

1. Gulf governments must carefully balance short-term labor market challenges, especially among their young adult populations, with a long-term need for diversification and growth. Implementing immigration policy that welcomes foreigners with skills that can be transferred and taught, as well as resources that can be used to grow new businesses on the ground (rather than just in portfolio investments) will be essential. Low-wage foreign workers can be useful, too, but should be granted some flexibility to move between employers (which would generate savings for companies, since they would pay less in recruitment fees and sponsoring workers in holding patterns when business is slow) and build skills that are transferable and can boost productivity. Workers who stay and are able to choose their employers and compete for higher wages will over time build more competitive sectors that can also attract nationals.

2. Most importantly, reforms need staying power, and governments need to build credibility in their reform agendas. Backtracking and reinstating benefits will only make the transition to reduced energy, water, and fuel subsidies more difficult for citizens to bear.

3. As a policy recommendation for working with citizen groups, worker organizations (where they are permitted, as in Bahrain), and industry associations, Gulf states should keep in mind that there is power in transparency. The recent release of budgets by Gulf governments (Saudi Arabia and the UAE in particular) can encourage some dialogue and shared planning between the private sector and the state. Organizing business interests could be a lasting result of the current reform environment.

Endnotes

1. The puzzle being that such widespread political mobilization has overturned governments, but has not yet compelled governments to change their policies to address economic mobility barriers, boost job creation, and combat corruption.

2. Elena Ianchovichina, Eruptions of Popular Anger: The Economics of the Arab Spring and Its Aftermath, MENA Development Report (Washington, D.C.: The World Bank), doi:10.1596/978-1-4648-1152-4.

3. Karen Young, “A Home of One’s Own: Subsidized Housing as a Key Lever of Gulf Domestic Policy,” Market Watch (blog), The Arab Gulf States Institute in Washington (AGSIW), June 15, 2018, http://bit.ly/2wuyhyu.

4. Karen Young, “Saudi Economic Reform Update: Saudization and Expat Exodus,” Market Watch (blog), AGSIW, February 28, 2018, http://bit.ly/2MG7byz.

5. Karen Young, “The Cost of Private Education,” Market Watch (blog), AGSIW, October 3, 2017, http://bit.ly/2PYJ2Bs.

6. Bernd Debusmann Jr., “Revealed: What Abu Dhabi’s $13.6bn Stimulus Really Means for the Capital,” Arabian Business, June 10, 2018, http://bit.ly/2PpklwN.

7. “Bahrain approves new law to allow 100% foreign ownership,” Arabian Business, July 19, 2016, http://bit.ly/2PkPUYH.

8. “Labor Ministry Designates 12 Job Types as Saudi-only,” Arab News, January 30, 2018, http://bit.ly/2LINyka.

9. Margherita Stancati and Donna Abdulaziz, “Saudi Arabia’s Economic Revamp Means More Jobs for Saudis—If Only They Wanted Them,” Wall Street Journal, June 19, 2018, https://on.wsj.com/2MIGyco.

10. “Saudi Reforms,” Gulf Economic Barometer, AGSIW, retrieved July 10, 2018, http://bit.ly/2LP0aX6.

11. Wael Mahdi and Vivian Nereim, “Saudi Arabia Plans to Raise Gas Prices by 80% in January,” Bloomberg, December 11, 2017, https://bloom.bg/2C53c9T.

12. “Saudi Arabia hikes fuel price,” Saudi Gazette, January 1, 2018, http://bit.ly/2LK7NOu.

13. There is some cognitive dissonance and apprehension in Saudi society as changes occur with little public awareness campaigns. The economic effect is that people are less likely to make significant life decisions or even major purchases because of the possibility that major regulatory or labor market reform may affect their livelihoods.

14. “Primary Consumer Sentiment Index,” Thompson Reuters/Ipsos, October 2017, http://bit.ly/2NEuHbT.

15. “Saudi Arabia Purchasing Managers’ Index,” Emirates NBD, February 5, 2018, http://bit.ly/2PkQupl.

16. “Saudi Arabia makes 2 billion riyal payment in citizens account program,” Reuters, December 21, 2017, https://reut.rs/2LHTrOs.

17. “Saudi Arabia restores perks to state employees, boosting markets,” Reuters, April 22, 2017, https://reut.rs/2C5sq87.

18. Sara Khoja and Ahmed Almazed, “KSA: New Fees Applicable for Foreign Employees and Dependents,” Insight and Knowledge (blog), Clyde & Co., January 10, 2018, http://bit.ly/2orHGCJ.

19. Aarti Nagraj, “Saudi’s expat dependent fee: Everything you need to know,” Gulf Business, July 6, 2017, http://bit.ly/2PWdEnd.

20. Chang Lin Zhu, “Expats leaving Saudi must pay new ‘family tax’ up front,” International Adviser, July 5, 2017, http://bit.ly/2MIGRUA.

21. “2018 Saudi Arabia Fiscal Budget,” Jadwa, retrieved July 10, 2018, http://bit.ly/2PTMLA3.

22. Marwa Rashad, Tom Arnold, and Saeed Azhar, “Jump in Islamic tax liabilities worries Saudi banks,” Reuters, February 22, 2018, https://reut.rs/2C3hJTG.

23. Karen Young, “Corruption Purge Overshadows Stalled Reality of Saudi Economy,” Lawfare, November 16, 2017, http://bit.ly/2LJuxOz.

24. “New visa rules in UAE: All you need to know,” Khaleej Times, June 20, 2018, http://bit.ly/2MEK5bM..

25. “Abu Dhabi Stimulus Plan,” Gulf Economic Barometer, AGSIW, retrieved July 10, 2018, http://bit.ly/2MGYtAe.

26. Amany Zaher, “Bahrain Looks To Issue 10-Year Residence Permit for Foreign Investors,” Forbes Middle East, May 31, 2018, http://bit.ly/2CgwJOb.

27. Karen Young, “Trade Wars and Bond-Offs: Side Effects of Tariffs and Tactical Borrowing Hit the Gulf,” Market Watch (blog), AGSIW, April 11, 2018, http://bit.ly/2MHKlq8.

28. Archana Narayanan, “Bahrain Wakes Up to Bond Reality as Secondary Market Hit,” Bloomberg, March 28, 2018, https://bloom.bg/2wuCDpk.

29. “Fiscal Policy Measures: Tax,” Gulf Economic Barometer, AGSIW, retrieved July 10, 2018, http://bit.ly/2ou1vch.

30. International Monetary Fund, Gulf Cooperation Council: How Can Growth- Friendlier Expenditure-Based Fiscal Adjustment be Achieved in the GCC? (Washington, D.C.: International Monetary Fund, 2017), http://bit.ly/2oqKIXH.

31. Elena Ianchovichina and Harun Onder, “Dutch disease: An economic illness easy to catch, difficult to cure,” Future Development (blog), Brookings Institution, October 31, 2017, https://brook.gs/2NE74Aa.

32. Melani Cammett and Ishac Diwan, “The Roll-Back of the State and the Rise of Crony Capitalism,” in The Middle East Economies in Times of Transition, eds. I. Diwan and A. Galal (London: Palgrave Macmillan, 2016).

33. Sharifa Alshalfan, The right to housing in Kuwait: An urban injustice in a socially just system (London: Kuwait Programme on Development, Governance and Globalisation in the Gulf States, London School of Economics and Political Science, 2013), http://bit.ly/2wxHeqK.

34. “How will Saudi Arabia distribute its financial support to its citizens?” Al Arabiya English, December 22, 2016, http://bit.ly/2N3oLfi.

35. “Saudi royal handouts to cost about $13 billion: Minister,” Reuters, January 7, 2018, https://reut.rs/2wwXcS7.

36. “Beyond affordability: Public housing and community development in the GCC,” Strategy&, October 21, 2014. https://pwc.to/2PpGQSu.

37. Rethinking Arab Employment: A Systemic Approach for Resource-Endowed Economies (Geneva, Switzerland: World Economic Forum, 2014), http://bit.ly/2BZOJMt.

Appendix

For an overview of subsidy and tax implementation reforms in the GCC, please see https://bit.ly/2NcklDW.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.