Introduction1

Global economic integration has increased dramatically in recent years. The current wave of globalization has been characterized by two interrelated processes: a sharp drop in barriers to trade and the expansion of global production networks built around multinational corporations (MNCs), which are the central actors in the global trading system. U.S. MNCs, for instance, account for over 80 percent of the value of goods and services traded across national borders. The formation of these production networks is made possible by lowering tariffs and other restrictions on the flow of goods and services. Efforts at liberalizing international trade have been supported by international cooperation and have been institutionalized in multilateral, regional, and bilateral trade agreements. Most countries in the world are members of the World Trade Organization (WTO), the quintessential multinational institution designed around the principles of nondiscrimination and reciprocity.

The formation of the WTO was the result of the Uruguay Round of the General Agreement on Trade and Tariffs, which was concluded in 1994. The lengthy deadlock of the Doha Round of the multilateral trade regime, which was launched after the conclusion of the Uruguay Round, has motivated numerous countries to liberalize trade by joining bilateral or regional trade agreements, which are known as preferential trade agreements (PTAs) because they provide preferential market access to the signatories. To date, there are more than 600 trade agreements in force, and every WTO member country is also a signatory of (at least) one preferential trade agreement.2 Despite their prevalence, the effects of PTAs on everything from trade, to foreign investment, to economic reform, to wages, to employment are hotly debated.

The Consequences of Preferential Trade Agreements

Preferential tariff cuts and other provisions included in PTAs promote deeper economic integration. PTAs have contributed to the formation of regional and global production networks, where inputs can be shipped across borders multiple times to take advantage of lower production costs, availability of local resources, and economies of scale. The costs of integrating production between parent companies and their affiliates across national borders—as in the case of the Mexican maquiladoras—would be prohibitive due to the presence of higher tariffs and other trade costs. For this reason, many countries, including the United States and its regional partners, have negotiated lower tariffs with their preferential trading partners.

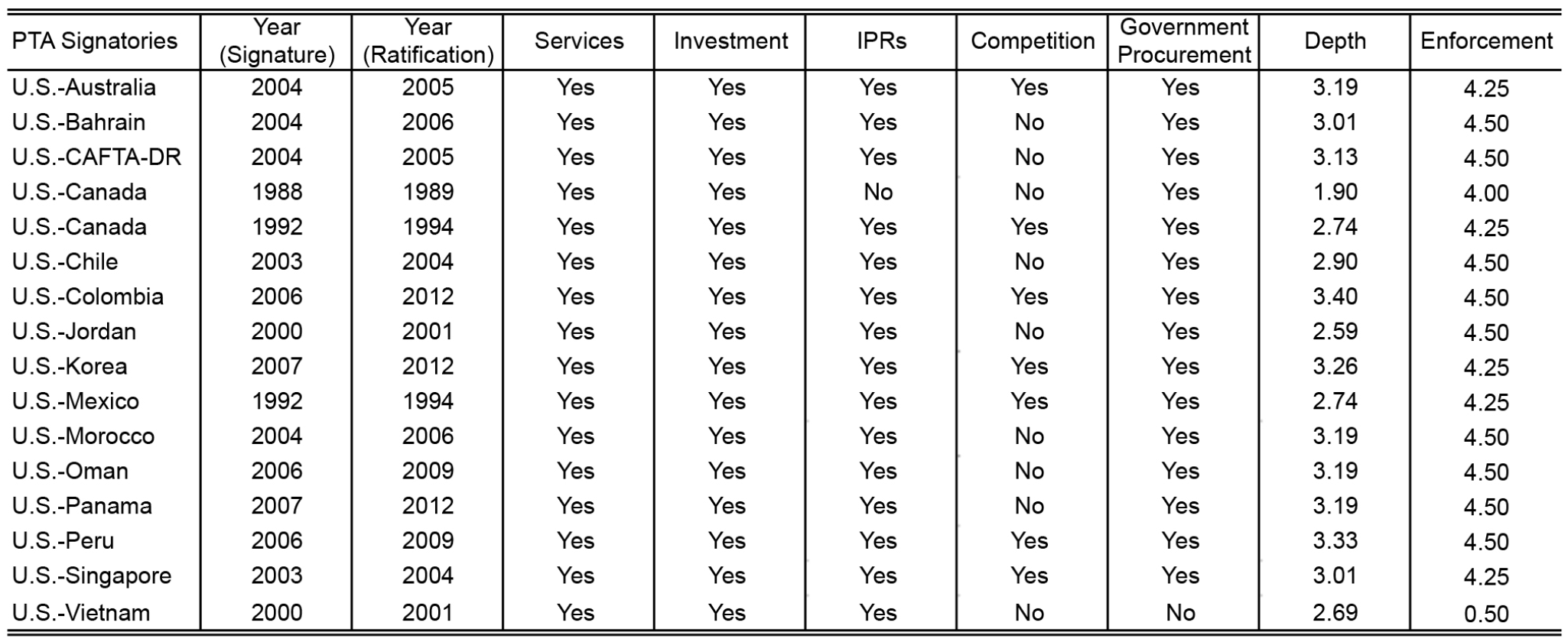

PTAs are increasingly complex arrangements that cover a host of issues, including intellectual property rights (IPRs) and investor dispute settlement. Once the main advocate for multilateral liberalization, the U.S. has preferential trade agreements in force with 20 countries. Table 1 presents a list of the PTAs that the U.S. has signed with other nations, and their main provisions.3

Table 1 — Design of U.S. PTAs

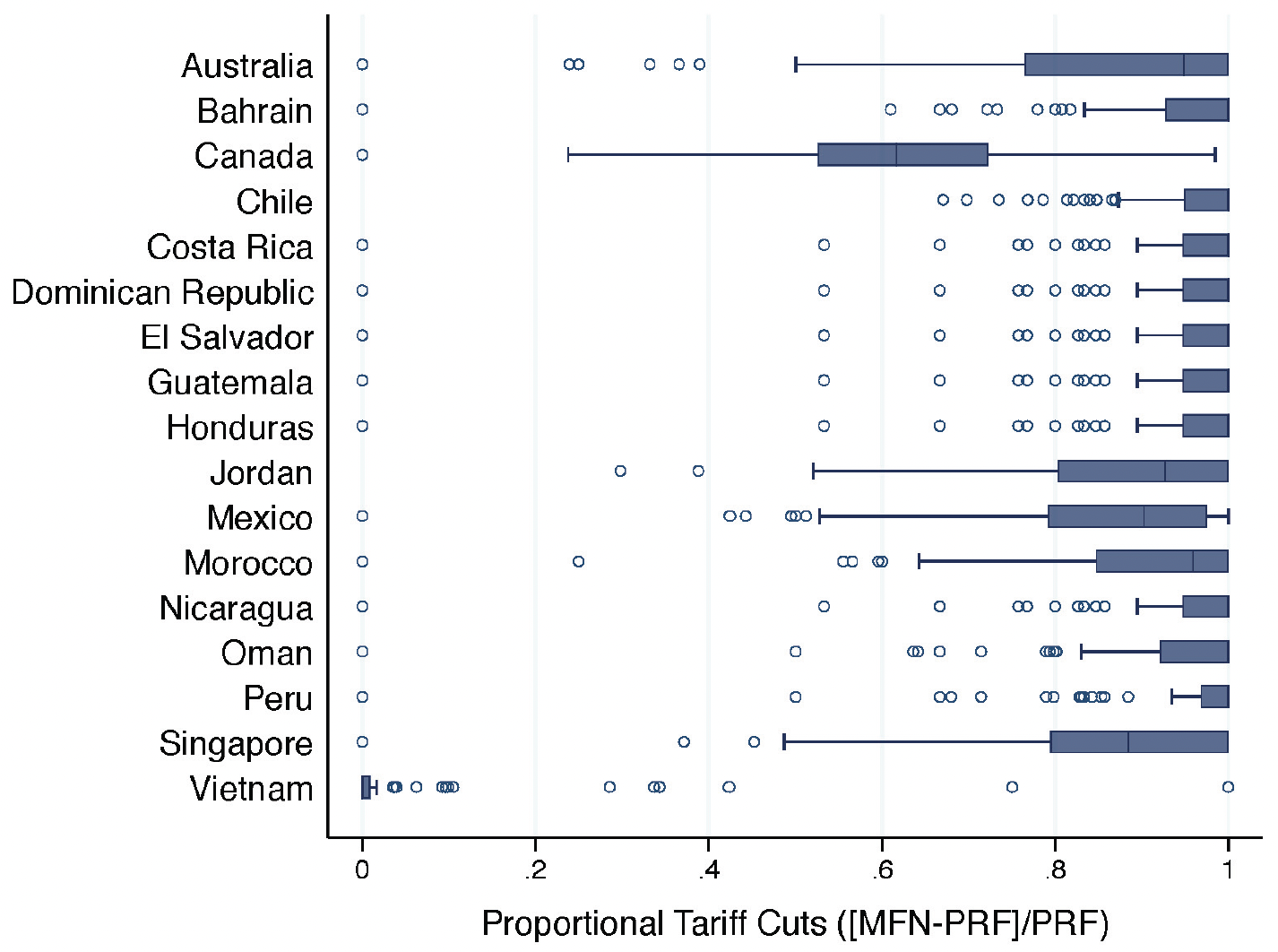

Figure 1 — Tariff Reductions in U.S. PTAs Since 1990

Notes The figure displays the distribution of proportional tariff cuts (MFN-PRF)/MFN—namely, the difference between the tariff offered to all countries on most favored nation terms (MFN) and the preferential tariff resulting from the PTA (PRF) implemented by the U.S. for the 17 PTAs signed after 1990. Higher proportional cuts reflect a greater difference between the prevailing tariff rate and the PTA rate. Data come from World Integrated Trade Solution (2014) and are at a highly disaggregated tariff line. Each tariff line corresponds to a specific group of products; the digit level reflects the level of detail of the products included in the category, depending on their characteristics. The HS 6-digit level follows the international standard known as the Harmonized System.

Figure 1 illustrates the magnitude of preferential tariff cuts offered by the United States in all PTAs it has signed since 1990. Latin American nations figure prominently in this selective list of U.S. preferential trading partners: Mexico (NAFTA, 1994); Chile (2004); Costa Rica, the Dominican Republic, El Salvador, Guatemala, Honduras, and Nicaragua (CAFTA-DR, 2005); Peru (2009); Colombia (2012); and Panama (2012). Figure 1 shows the distribution of preferential tariff cuts for each trading partner under a PTA: the shaded boxes mark the interquartile range and the median of the distributions of tariff cuts, and the hollow circles mark more extreme values. The figure suggests that there is a large degree of variance in the level of cuts within each PTA. According to the U.S. Census Bureau, 79 percent of U.S. trade with Latin American countries is covered by a PTA (that number increases to 88 percent if Canada is included).4

Political Backlash Against PTAs

Trade agreements between the United States and Latin American countries such as the North America Free Trade Agreement (NAFTA), the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR), and the now-defunct Trans-Pacific Partnership (TPP) were a source of heated controversy in the 2016 U.S. presidential campaign. These agreements were alleged to deliver lopsided benefits in favor of U.S. trading partners, displacing American blue-collar workers from their jobs.

The argument is politically expedient, particularly in battleground states battered by the decline of American manufacturing employment.5 But the debate overlooks the direct effect of PTAs on the activities of MNCs. It is therefore very important to understand which firms benefit from PTAs and why. We expect MNCs to be the big winners from the wave of preferential agreements, but there is reason to believe that those benefits will be unevenly distributed.

In a recent paper published in International Organization, we examine the impact of preferential liberalization on the activities of MNCs.6 Our results are drawn from analyzing firm-level data regarding the activities of nearly all multinational companies based in the U.S., and highly disaggregated tariff schedules offered on preferential and nonpreferential terms. We find strong evidence that tariff reductions offered by the U.S. to its preferential trading partners has led to a significant expansion of the global supply chain activities of the largest and most productive firms. Smaller and less productive firms, on the other hand, are squeezed out of the market following preferential liberalization, as firms operating in the liberalizing market are forced to lower their prices to remain competitive. The expansion of the most productive firms, in turn, results in higher real wages and production costs.7 The net result of this reallocation of sales from the smallest to the largest MNCs is higher market concentration in sectors with higher tariff cuts.

To understand these results, we need to focus on the role of firms in the global economy, particularly the prominent place occupied by MNCs. As central actors in the international economy, MNCs engage in two types of foreign investment: horizontal and vertical.8 Horizontal investment seeks to reach customers in host markets. Vertical investment, central to global supply chain production, occurs when MNCs seek resources abroad by setting up affiliates to produce intermediate or final goods. These intermediate and final goods, in turn, are then exported back to the home market or to third countries, either for consumption or for further processing. We contend that preferential liberalizations should promote export-oriented sales by lowering trade costs.

Yet based on our analysis, it seems that not all MNCs gain from lower preferential tariffs—only the largest and most productive firms do. These findings are in line with recent contributions in the field of international economics that identify differences in firms’ productivity as central determinants of trade performance. International expansion through exports and investment abroad demands extra costs that only the most productive firms can afford.9 Lower costs resulting from trade liberalization should thus benefit the largest and most productive MNCs.

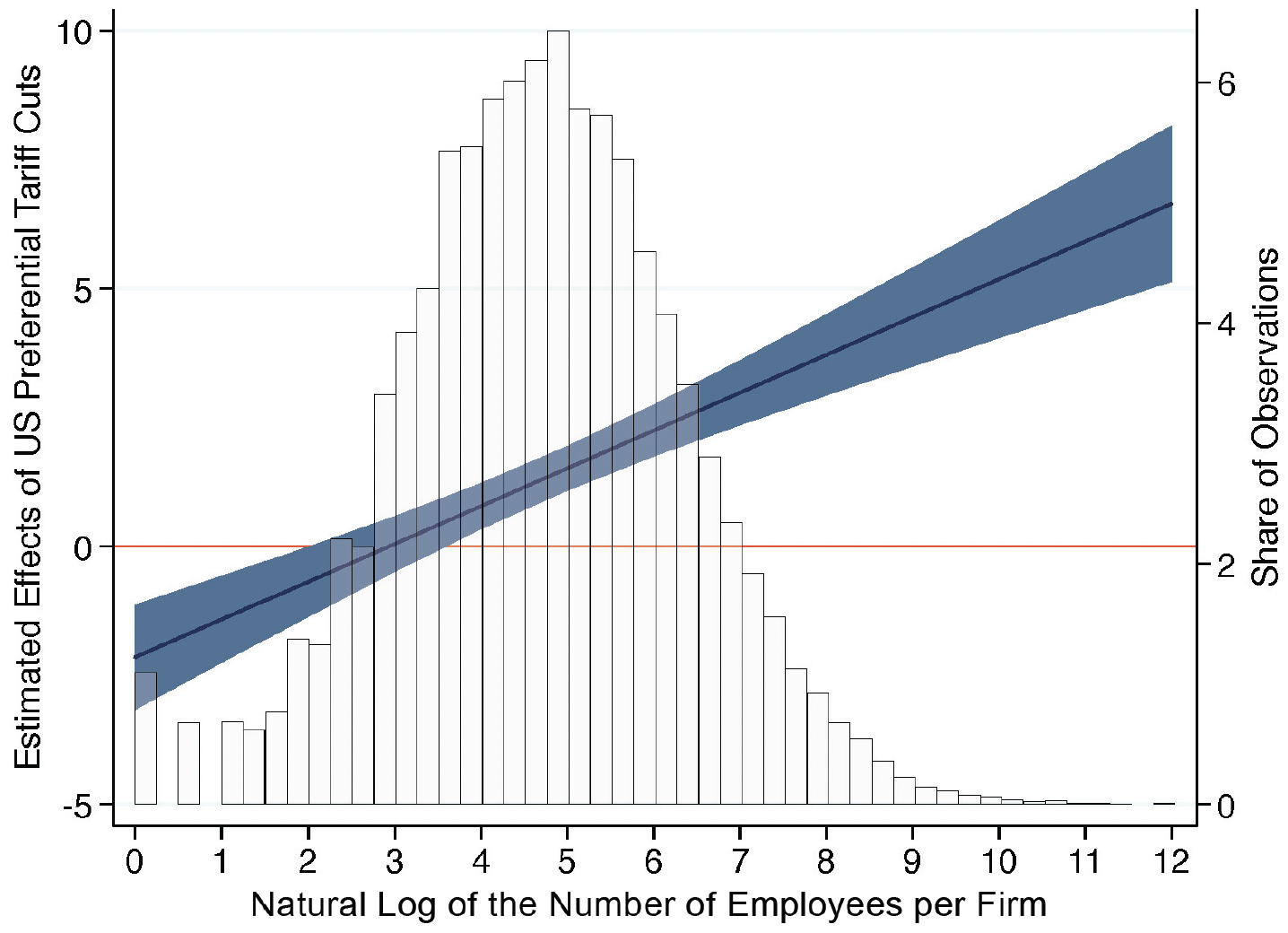

Figure 2 — U.S. Preferential Tariff Cuts and Vertical Sales by Firm Size

Our estimates show that sales from affiliates operating abroad back to the United States increase for larger firms and decrease for smaller firms following preferential tariff cuts implemented by the United States. Figure 2 illustrates the effect of a tariff cut along the range of affiliate sizes estimated in our paper.10 U.S. tariff cuts reduce the vertical sales of smaller affiliates. The effect of preferential cuts on sales turns positive and statistically significant for companies with around 45 employees (corresponding to 3.5 on the horizontal axis), where we estimate that a 10 percent tariff cut is associated with a 6 percent increase in sales to the United States.

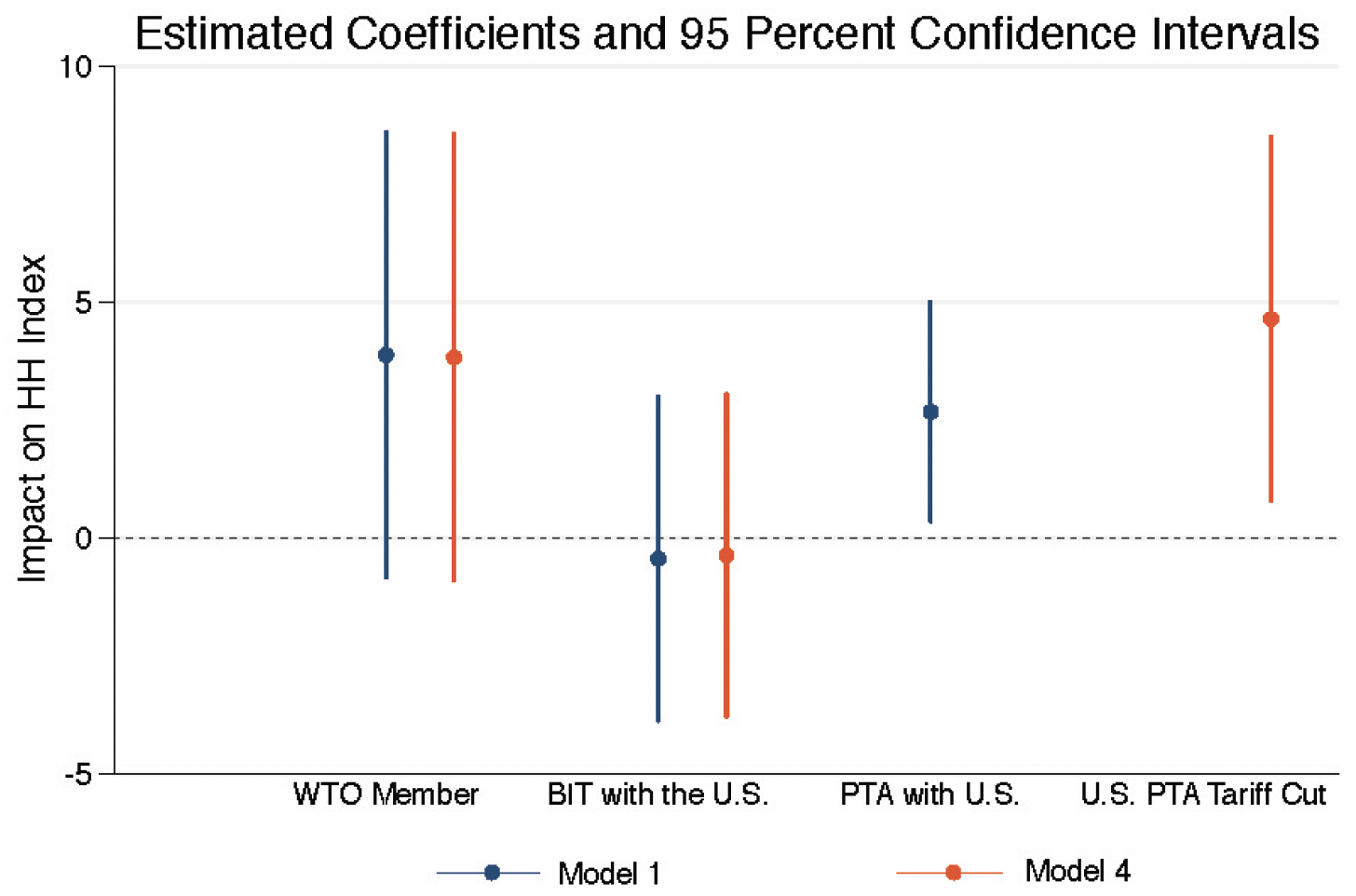

Figure 3 — International Agreements and Concentration of Affiliate Sales

We also find that preferential tariff cuts are associated with increased market concentration; the main results on concentration derived from our paper are reproduced in Figure 3. The figure reproduces the estimated effects of PTAs on sales concentration, which is measured using a Herfindahl-Hirschman (HH) Index of concentration of affiliate sales.11 To illustrate our findings, we selected the estimated coefficients from three variables that measure the impact of three different international institutions on concentration: whether the partner country is a member of WTO, and hence eligible for access to the U.S. under most favored nation tariffs; whether the partner country has a bilateral investment treaty with the U.S.; or whether the partner country has a PTA in effect with the U.S., and hence is eligible for preferential tariffs. The figure shows results from two models in our paper: in Model 1 we used a measure of the existence of a PTA, and Model 4 estimated preferential cuts across different sectors of the PTA. The dots reproduce the estimated coefficients, and the lines mark the 95 percent confidence intervals around those estimates. The magnitude of these effects is sizable: a 10 percent reduction in preferential tariffs is associated with a 0.5-point increase in the HH Index. In sum, the results of our analysis of the sales concentration among U.S. MNCs are consistent with our conjecture that tariff cuts principally benefit the largest firms.

Corollary

To sum up, while academic and popular debates tend to focus on differential benefits and costs of trade across countries or industries, our research highlights winners and losers at the level of individual firms. In short, preferential liberalization produces concentrated benefits among a relatively small number of very large and productive firms. While specific provisions built into preferential trade agreements—such as setting regulatory standards and protecting investment and intellectual property rights—can produce widespread benefits, cutting tariffs on preferential terms has stark distributional consequences across firms of different sizes and levels of productivity.

The linkages between trade, MNC expansion and concentration, and income inequality is an exciting area for future academic research. However, from these results we can draw important lessons on the future of economic and political relations between the U.S., Mexico, and other Latin American countries. Our findings help explain the sharp political backlash against NAFTA, CAFTA, and other preferential trade agreements among U.S. voters, interest groups, and firms. We can predict stronger support for NAFTA from the largest and most productive U.S. firms engaged in global production in Mexico (and Canada), as they reap the lion’s share of the benefits of lowering barriers to trade. In contrast, smaller and less productive firms in the U.S.—particularly those facing higher competition from abroad—tend to oppose the agreement. Moreover, insofar as the wages of workers employed in firms benefiting from preferential liberalization increase more than the wages of workers employed in firms negatively impacted by it, trade agreements may contribute to income disparity in the U.S. This disparate distribution of the costs and benefits of regional trade has taken central stage in political discourse in the United States; thus, the evolution of hemispheric cooperation depends on the ability of negotiators to address these salient conflicts.

Endnotes

1. The statistical analysis of firm-level data on U.S. multinational companies was conducted at the Bureau of Economic Analysis of the U.S. Department of Commerce under arrangements that maintain legal confidentiality requirements. The views expressed are those of the authors and do not reflect official positions of the U.S. Department of Commerce.

2. Andreas Dür, Leonardo Baccini, and Manfred Elsig, “The Design of International Trade Agreements: Introducing a New Database,” Review of International Organizations 9, no. 3 (2014): 353-75.

3. The data come from the Design of Trade Agreements (DESTA) Database, available at http://www.designoftradeagreements.org/.

4. These are our own estimates based on data from the U.S. Census, “U.S. Goods Trade: Imports and Exports by Related Parties 2014,” released on May 5, 2015.

5. See J. Bradford Jensen, Dennis P. Quinn, and Stephen Weymouth, “Winners and Losers in International Trade: The Effects on U.S. Presidential Voting,” International Organization 71, no. 3 (2017): 423-57.

6. Leonardo Baccini, Pablo M. Pinto, and Stephen Weymouth, “The Distributional Consequences of Preferential Trade Liberalization: Firm-level Evidence,” International Organization 71, no. 2 (spring 2017): 373-95.

7. See Pablo M. Pinto, Partisan Investment in the Global Economy: Why the Left Loves Foreign Investment and FDI Loves the Left (Cambridge, UK: Cambridge University Press, 2013); and Pablo M. Pinto and Santiago M. Pinto, “The Politics of Investment: Partisanship and the Sectoral Allocation of Foreign Direct Investment,” Economics & Politics 20, no. 2 (2008): 216–54.

8. Elhanan Helpman,“Trade, FDI, and the Organization of Firms,” Journal of Economic Literature 44, no. 3 (2006): 589-630.

9. Marc J. Melitz and Daniel Trefler, “Gains from Trade When Firms Matter,” Journal of Economic Perspectives 26, no. 2 (2012): 91–118.

10. The upward sloping solid line in the figure graphs the estimated impact of preferential tariff cuts on sales by affiliates of U.S. MNCs back to the U.S. (vertical sales), for firms of different size (measured in terms of employment). The shaded area around that line shows the 95 percent confidence intervals around the estimated effects. The horizontal axis is the natural log of the number of employees by firm. The bars in the background reflect the share of different sizes of firms.

11. The Herfindahl-Hirschman Index is a widely used measure of market concentration. It is constructed by adding up the square of the market share of the firms participating in a sector or economic activity. A higher reading on the HH Index reflects a lower effective number of firms in the market, with each of them amassing a larger market share, and hence greater market power.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.