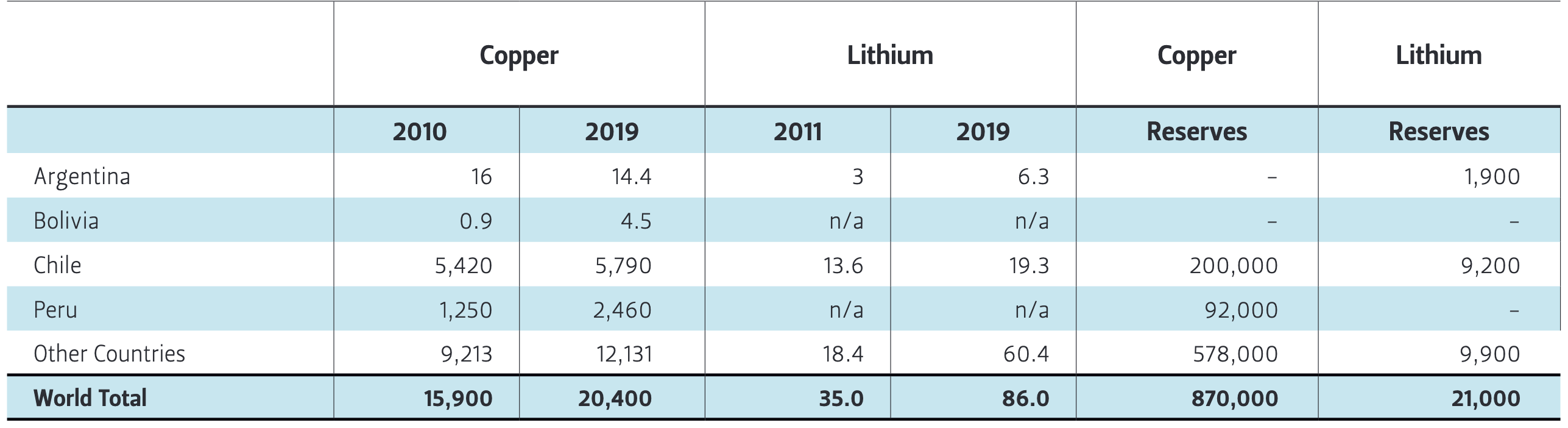

Latin America seems well positioned to enable the energy transition, with major reserves and producers of critical metals for the manufacturing of electric cars and batteries. Significant copper and lithium reserves are located in Argentina, Bolivia, Chile, and Peru (Table 1). Bolivia has the highest amount of lithium resources in the region according to the U.S. Geological Survey, although, with no commercial production yet, its reserves are not listed by the agency. Chile, on the other hand, has significant lithium production and reserves. The country has the potential to leverage these resources with the high quality and quantity of solar radiation in its northern region and onshore wind in its extreme South, which would lower the carbon intensity of copper and lithium mining and potentially parts of the supply chain downstream of its mines. These advantages present an opportunity for Chile to become one of the most cost-effective producers of “green hydrogen,” as the government has stated in its national hydrogen strategy and as is discussed in an earlier Baker Institute brief, Chile’s Energy Transition and the Role of Green Hydrogen.1

Mining and Energy Highlights

Chile is abundant in mineral resources, but not hydrocarbons. Historically, the country has been dependent on energy imports, i.e., natural gas pipelines from Argentina and liquified natural gas (LNG) import terminals in the northern and central regions in addition to coal and oil imports. Hence, energy security and competitiveness have been major challenges, particularly for the country’s energy-intensive mining operations. These challenges have led to decarbonization initiatives and a focus on renewable resources. As solar and wind technologies developed and became economically viable, the country aggressively pursued the building of generation capacity sourced on solar and wind (accounting for approximately 20% of electricity capacity).2 As a result, the country appears focused on decarbonizing its industry, mining, and economy at large.

Copper

Globally, Chile is the No. 1 copper producer, and demand is likely to increase, as copper in “wind turbines, solar farms, and their transmission networks use[s] up to 12 times as much of the metal as nonrenewable energy systems.”3 Electric grids, electric cars, and car-charging stations, in addition to the post-pandemic economic recovery, are expected to further increase demand.4 According to the Department of Industry, Science, Energy and Resources (DISER) in Australia, the global copper-demand outlook for 2026 is 28 million metric tons and 31.1 million metric tons for 2030, while in 2019, worldwide consumption was 24 million metric tons.5

Table 1 — Production & Reserves: Copper and Lithium in Selected Countries (in ’000 Metric Tons)

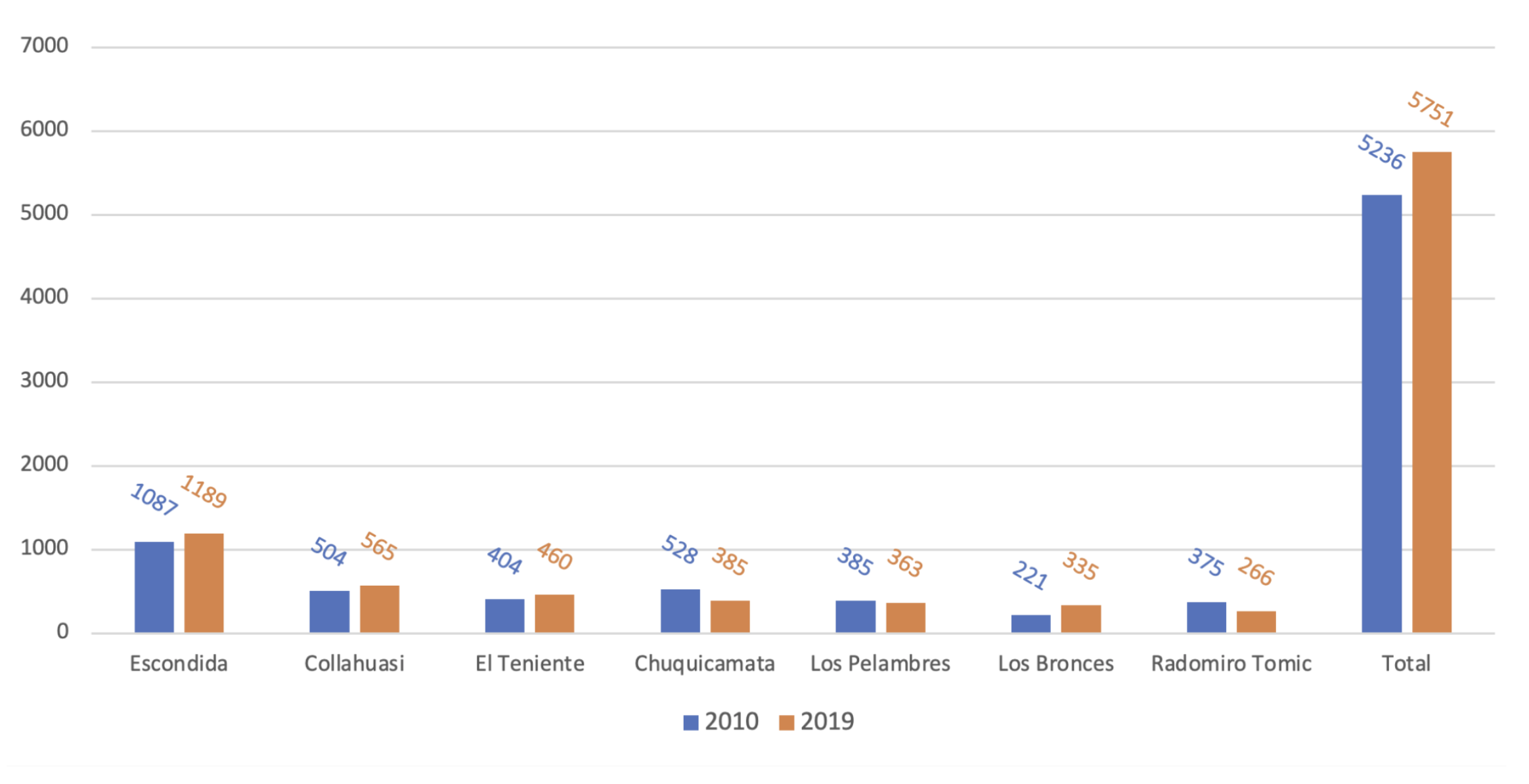

As the world’s top copper producer, Chile is well positioned to take advantage of this trend. Currently, the country is responsible for 28% of global production. Chile’s state-owned copper mining company, Corporación Nacional del Cobre (CODELCO), produces close to 30% of the country’s total output (see Figure 1 for its largest copper mines). Private producers, both domestic and international, include BHP, Rio Tinto, and Anglo American Sur.

Figure 1 — Chile’s Copper Production by Largest Mines, 2010 and 2019 (in ’000 Metric Tons)

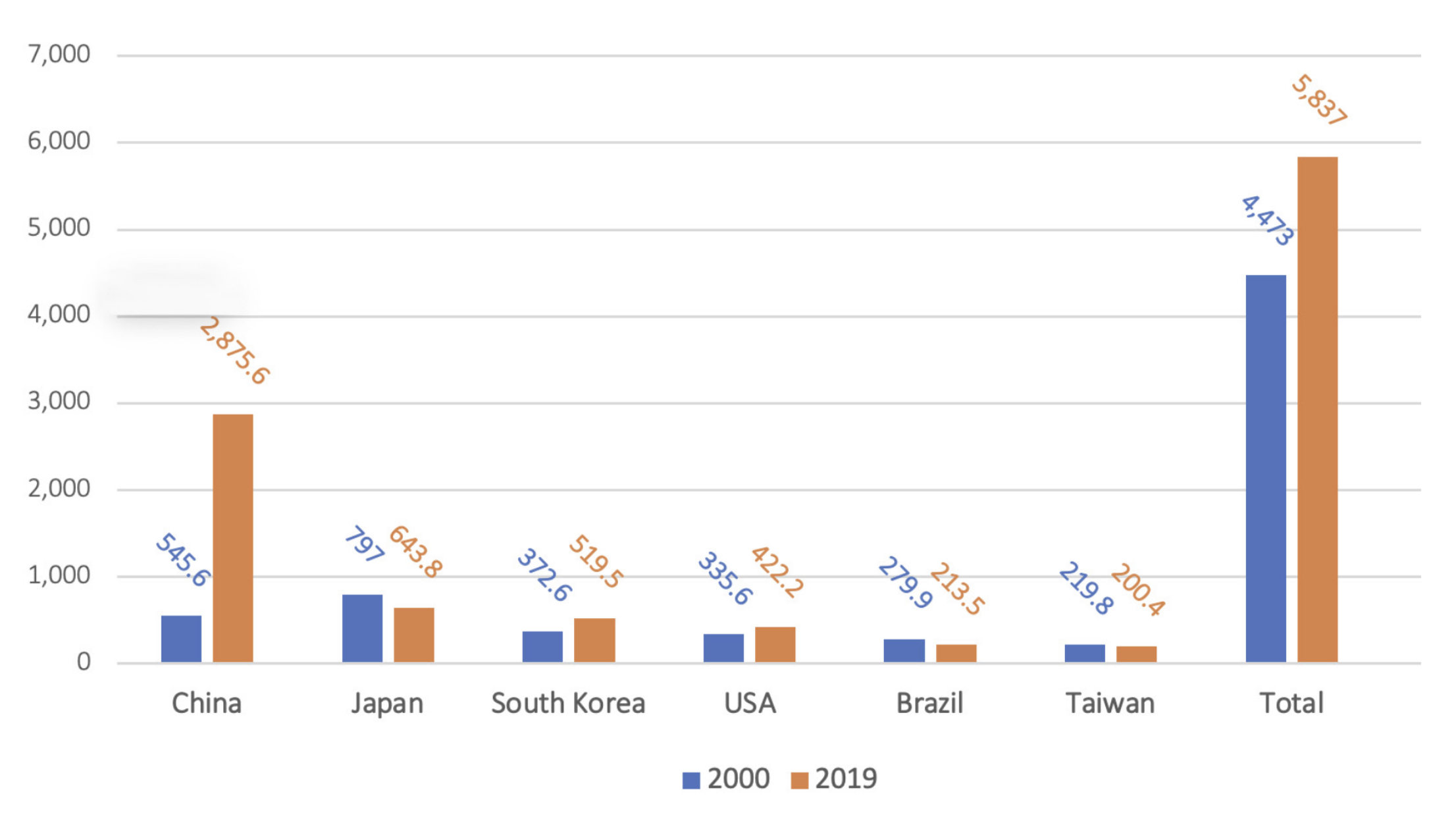

However, Chile’s production is not increasing fast enough to meet the expected demand. Some producers are struggling to expand operations due to falling productivity, declining ore grade, and long cycle times to open new mines, among other reasons. As a result, Chile’s contribution to global production decreased from 34% of worldwide production in 2010 to 28% in 2019.6 A variety of factors, including COVID-19 and the uncertainty of upcoming constitutional revisions, are delaying foreign investment in copper production. However, CODELCO increased its production by 1.2% between 2019 and 2020, according to its 2020 annual report.7 Most production is exported as raw material since copper manufacturing in Chile is minimal, as demonstrated by the fact that production and export volumes nearly match. Its export destinations in the last 20 years have dramatically changed, with China capturing close to 50% of total Chilean copper production in 2019 (see Figure 2). The shift in production destination presents an opportunity for Chile to primarily be a copper supplier for the manufacture of electric vehicles, construction, and multiple industrial applications in the Western Hemisphere, rather than chiefly transport the metal across the world; having the Americas as the primary export destination would also reduce carbon emissions, given the shorter travel distances.

Currently, as a result of the worldwide economic rebound from the pandemic and a demand surge from China, the price of copper has been rising. In fact, it rose to record highs for the first time in more than a decade, closing at $10,417 per metric ton, or $4.725 per pound, in May.8 On August 6, according to the Wall Street Journal, the price range of the prior 52 weeks was $2.77/lb to $4.89/lb ($6,019/mt to $10,781/mt).

Figure 2 — Chile’s Largest Copper Export Destinations, 2000 and 2019 (in ’000 Metric Tons)10

Legal and Regulatory Framework

Since 1980, Chile has had an evolving competitive legal and regulatory framework for its copper-mining activity. In addition to CODELCO, Chile has attracted private, local, and international mining concerns. However, in May of this year, following the worldwide copper-price increase, Chile’s congress considered a proposed law that would change how copper is taxed. The proposal includes a base royalty rate of 3%. Then the tax would increase progressively to as much as 75% of revenues over $4.00/ lb, or $8,800 per metric ton in additional tax. But Chile’s foreign-owned mines have tax stability clauses in place meant to attract investment, and thus would not be subject to the higher tax until the clauses expire between 2023 and 2032. As a result, affected companies, particularly those whose stability clauses expire in 2023, are delaying and/or stopping their investments until this situation is resolved.

Lithium

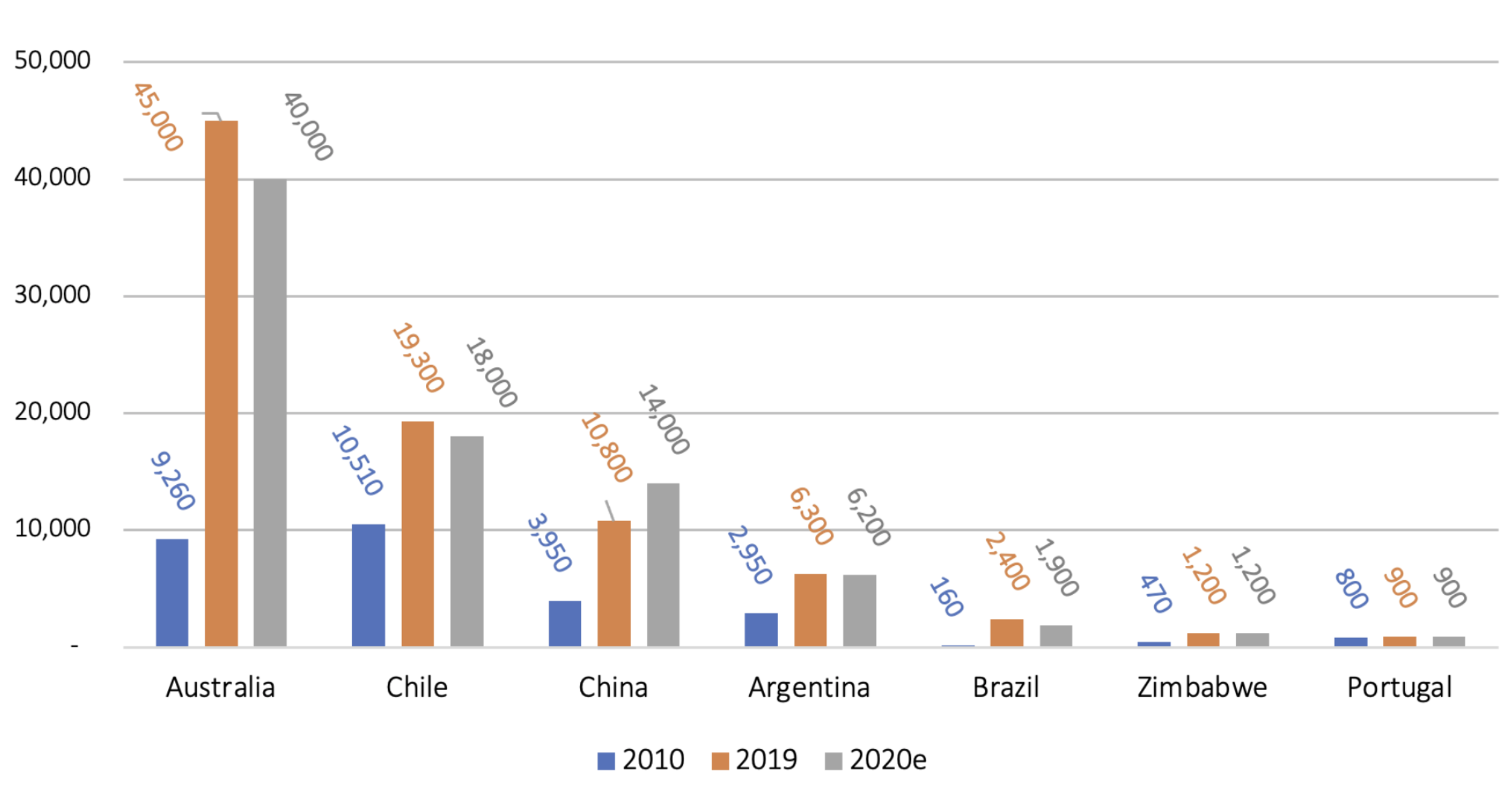

Chile is currently the No. 2 worldwide producer of lithium (Li) after Australia (see Figure 3). It is one of the commodities most expected to benefit from an electric-vehicle boom. However, lithium has already been in use for some time in applications like cell phones and computers; its demand had already more than doubled between 2011 and 2019, from 35,000 metric tons to 86,000 metric tons. Depending on technological advances in Li-ion batteries, the demand for lithium worldwide is expected to be in the range of 4 million metric tons to 10 million metric tons by 2050, according to the World Bank.9 This broad range is the result of technological efforts to reduce lithium content in batteries.

Figure 3 — Global Lithium Production (in Metric Tons)11

Chile’s lithium production is fully destined for export. However, not all lithium is the same; different types are lithium metal, lithium hydroxide and lithium carbonate, which is produced as lithium brine and is the kind primarily produced in Chile. As with copper, the importers of Chilean lithium have also significantly changed in the last 10 years. In 2010 the major importers were Japan, Germany, and South Korea, while in 2019 the major importers were South Korea (+214%) and China (+49%).

After peaking in 2017, lithium prices have started to recover as the global economy rebounds and the world pursues an energy transition. According to the U.S. Geological Survey, the price of lithium hydroxide hit a low of $7,000/mt by the end of 2020. In 2021 however, the price has already been recovering above $10,000/ mt, although it remains below what producers seem to require to “incentivize” investment in restoring mothballed mines and processing plants or in new projects, per Macquarie and Credit Suisse.12

Legal and Regulatory Framework

Chilean law has established lithium as a strategic mineral and does not allow for concessions, permitting “only the state, state-owned companies, or private companies operating under partnerships with the Chilean Production Development Corporation (CORFO)” to develop the mineral.13

Lithium brine has significant classification challenges with regard to environmental regulation, since Chilean mining law treats it like a mineral. Indigenous groups and scientists are starting to learn more about its unique impact on freshwater sources and want to classify brine as water instead; what the different classifications mean in terms of the general cost of environmental treatment is uncertain (e.g., which classification would be the costliest).14 On the Atacama salt flat, the sun evaporates the brine pumped from beneath the ground into a concentrate rich in lithium. That this process uses sunlight rather than mechanical power is a major selling point for electric automakers keen on eliminating emissions from supply chains. Chile’s two lithium operators, Albemarle and Chilean SQM, argue that purifying brine water would be challenging and not make sense since it would not impact the surrounding fresh water.15 This is a significant issue that requires both environmental and mining regulatory agencies to assess the implications of lithium-brine depletion and potential freshwater impact. The proposed royalty mentioned earlier also includes a base royalty rate of 3% on lithium sales to fund development and infrastructure in mining regions and underwrite social programs. This charge would be applied only if it is higher than the payment established in the contract.

China’s Role

With China becoming a major player in solar technology, Chile has become very important as a supplier of critical minerals, like copper and lithium. Chile’s commerce with China has grown exponentially in the past two decades. In total, trade grew from $2.3 billion in 2002 to $39.2 billion in 2019, making the People’s Republic of China (PRC) Chile’s No. 1 trading partner.16 Within that same period, China’s exports increased from $1.2 billion to $22.7 billion, and its imports increased from $1.1 billion to $16.5 billion. This growth has been facilitated by a free trade agreement (FTA) between the two countries, which went into effect in 2005, and was expanded to include trade-in-services and other elements in 2017.17 China’s most significant impacts on Chile’s mining sector involve:18

- The PRC’s physical access to Chile’s reserves of lithium, critical for the manufacturing of batteries used to power modern electric vehicles, electronics, and defense technologies;

- A 2017 agreement between CODELCO and China Minmetals Corp. that includes China’s right to explore lithium and acquire rights to mines in Chile in the foreseeable future; and

- The 2019 approval by Chilean regulators of a $4.1 billion deal in which the Chinese firm Tianqi acquired a 24% stake in Chilean SQM, which is involved in the extraction of lithium from the Atacama salt flat.19

As a result, China has gained a position in Chile that supports the long-distance transportation of critical metals, to the detriment of efforts to reduce emissions. Chile should consider attracting investment and technology to create high-level jobs to manufacture batteries in-country, for example, which would require specialized technology and reduce exports to China.

Conclusions

As demonstrated in this brief, Chile has significant copper and lithium production and reserves. However, because of its geographic location, it will face extraordinary supply chain challenges that could counter its resource abundance; acquiring critical elements from the international market for Chile’s industries will test its ability to be competitive and agile.

That said, Chile’s vast natural gifts, including very good solar/wind resources, put it in an advantageous position as the world decarbonizes. Will Chile try to capture some of the supply-chain business downstream of the mine? Chile has had the advantage of stable governments and a generally market-based economic policy over the past several decades that has supported foreign investment in mining. With recent elections hinting at more left-wing policies and the upcoming constitutional revisions, will a changed business environment counteract the country’s natural-resource advantages? This remains to be seen, as history shows that the high political risk of foreign investment has slowed natural-resource development in much of Latin America.

Changes to lithium legislation to attract investment and make it possible to add value to lithium production would be helpful. This will require working closely with the indigenous communities living where lithium resources are located. Addressing the impact of lithium mining on fresh water and the overall ecosystem and undertaking due diligence to obtain the social license to operate in these very isolated areas will be critical for the success of lithium development.

Endnotes

1. Leiss, Benigna C. 2021. Chile’s Transition and the Role of Green Hydrogen. Issue brief no. 04.23.21. Rice University’s Baker Institute for Public Policy, Houston, Texas.

2. “Distribution of installed electricity generation capacity in Chile in 2019, by technology,” Statistica, last modified July 2020, https://www.statista.com/statistics/762291/installed-power-capacity-technology-chile/.

3. Henry Sanderson, “Chilean miners fear struggle to meet copper demand,” Financial Times, April 26, 2021, https://www.ft.com/content/2571df1d-75a9-4352-b621-ee8d85d063d2.

4. Ibid.

5. Vladimir Basov, “Global refined copper demand to rise 31% by 2030 – report,” Kitco, June 08, 2021, https://www.kitco.com/news/2021-06-08/global-refined-copper-demand-to-rise-31-by-2030-report.html.

6. Ibid.

7. Corporación Nacional del Cobre (CODELCO), Annual Results 2020.

8. “Copper hits 10-year high above $10,000 a ton,” Financial Times, April 29, 2021, https://www.ft.com/content/bbd0adc1-442d-4662-bf13-9a641807b378.

9. Kirsten Hund et al., Minerals for Climate Action: The Mineral Intensity of the Clean Energy Transition, The World Bank, 2020, https://pubdocs.worldbank.org/en/961711588875536384/Minerals-for-Climate-Action-The-Mineral-Intensity-of-the-Clean-Energy-Transition.pdf.

10. Cochilco Yearbook: Copper and Other Mineral Statistics, 2000-2019. https://www.cochilco.cl/Lists/Anuario/Attachments/23/AE2019WEB.pdf

11. United States Geological Survey (USGS), Mineral Commodity Summaries, 2012 and 2021, https://www.usgs.gov/centers/nmic/mineral-commodity-summaries.

12. Tim Treadgold, “Lithium Price Tipped To Rise After Warning Of ‘Perpetual Deficit,’” Forbes, July 2, 2021, https://www.forbes.com/sites/timtreadgold/2021/07/02/lithium-price-tipped-to-rise-after-warning-of-perpetual-deficit/?sh=f6bfbfa4ab73.

13. Carla Selman, “Latin American Lithium Promotion,” IHS Markit, April 27, 2018, https://ihsmarkit.com/research-analysis/latin-american-lithium-promotion.html.

14. Dave Sherwood, “Inside lithium giant SQM's struggle to win over indigenous communities in Chile's Atacama,” Reuters, January 15, 2021, https://www.reuters.com/article/us-chile-lithium-sqm-focus/inside-lithium-giant-sqms-struggle-to-win-over-indigenous-communities-in-chiles-atacama-idUSKBN29K1DB; Ian Morse, “Chile’s new constitution could rewrite the story of lithium mining,” Quartz, December 22, 2020, https://qz.com/1948663/chiles-new-constitution-could-rewrite-the-fate-of-lithium-mining/.

15. Ibid.

16. International Monetary Fund, Exports and Imports by Areas and Countries, https://data.imf.org/regular.aspx?key=61013712.

17. “Chile joins China’s Belt and Road Initiative,” Economist, November 22, 2018, http://country.eiu.com/article.aspx?articleid =917372275&Country=Chile&topic=Politics&subtopic=For_5.

18. Evan Ellis, “Chinese advances in Chile,” Global Americans, March 2, 2021, https://theglobalamericans.org/2021/03/chinese-advances-in-chile/.

19. Fabian Cambero, “China’s Tianqi agrees truce in battle over Chilean lithium miner SQM,” Reuters, April 11, 2019, https://www.reuters.com/article/us-sqm-tianqi-lithium/chinas-tianqi-agrees-truce-in-battle-over-chilean-lithium-miner-sqm-idUSKCN1RN2B0.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.