Introduction

The BRICS hold their seventh summit in Ufa, Russia this week.1 At the summit, members will continue to define the shape of their New Development Bank (NDB), also known as the BRICS Bank. They have established a rough outline of the bank’s aim, size, and governance, but many important details remain, including agreement on four critical issues: voter representation, political influence, lending practices known as conditionality, and market strategies known as additionality.

While the BRICS may seek to establish a new model for development banks, they should still look to established banks for practical advice on designing a new institution. From national development banks like Brazil’s BNDES to regional and global multilateral development banks (MDBs) like the Asian Development Bank (ADB) and the World Bank, the BRICS can draw from a deep reserve of experience. By examining lessons to be learned from three development banks at different levels of government, we not only can glean the environment into which the NDB will be entering, but also envision a framework for a new type of development bank.

Voter Representation

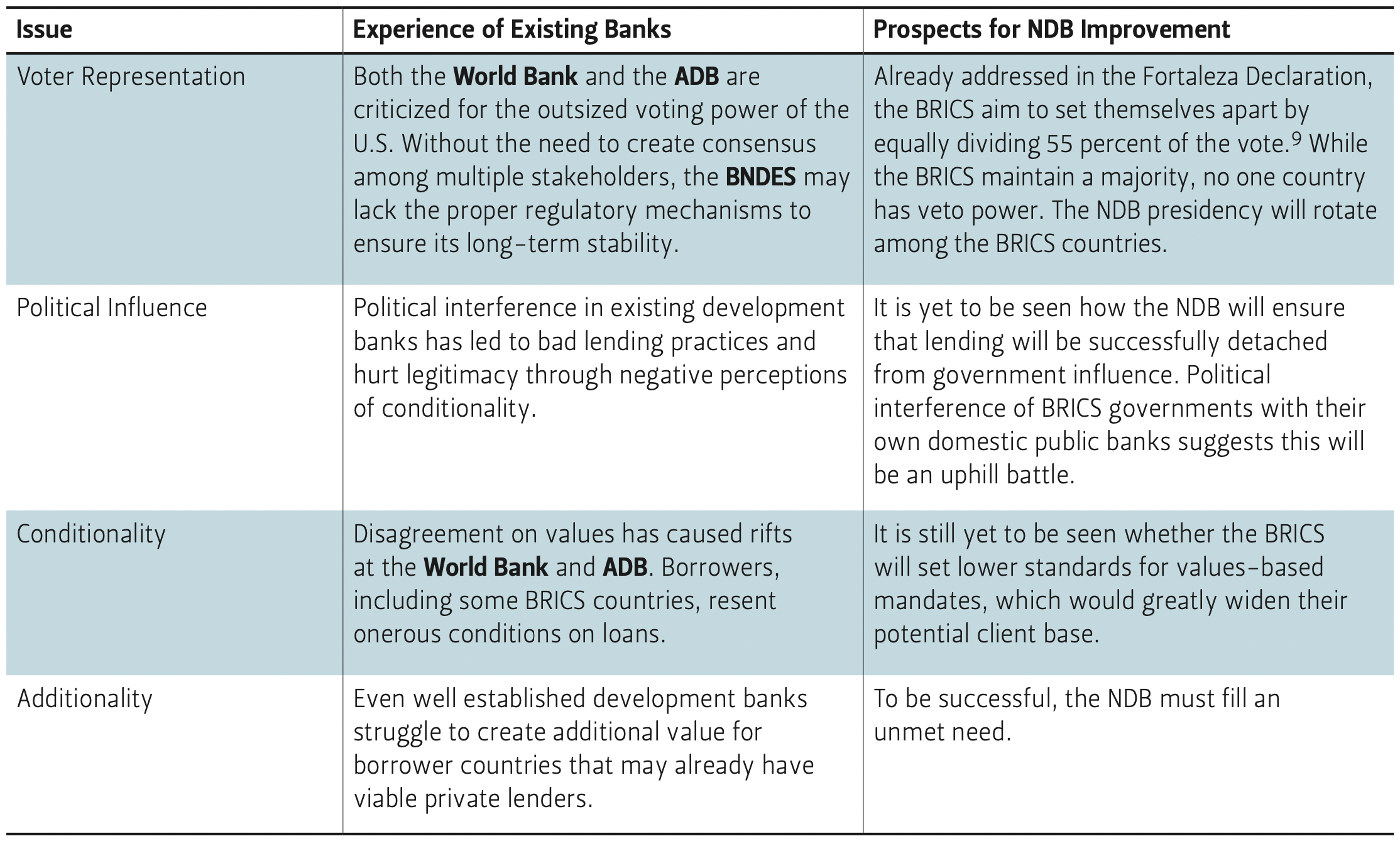

Voter representation has been a key issue for the newly founded NDB. Both the World Bank and its affiliated regional bank, the Asian Development Bank, have received criticism for underrepresenting later- developing countries. Critics complain that the dominance of established Western powers crowd out alternative voices in institutional governance. During the 2013 summit in South Africa, the BRICS called “for the reform of international financial institutions to make them more representative and to reflect the growing weight of BRICS and other developing countries.”2 This highly visible issue helped motivate the creation of both the NDB and the Asian Infrastructure Investment Bank (AIIB).

Brazil’s BNDES demonstrates the other side of the coin, with highly centralized control by the president. Not only is BNDES one of the largest and most profitable development banks, it is also one of the most efficient, with profits per employee approximately 10 times that of the World Bank.3 This derives in part from its efficient governance structure; fewer checks and balances can result in fewer complications. Despite the potential gains for efficiency, this can be a dangerous strategy. Not only may stakeholders abandon the institution, but lending practices may stray from the bank’s long-term interests.

The BRICS will rotate NDB leadership—a good start at avoiding excessive control by individual members. The BRICS have also tried to create a voting distribution scheme that is more representative by giving each of the five founding countries an equal voting share. Nonetheless, their joint 55 percent voting share has raised concerns about a guaranteed majority should they vote together.4 However, the BRICS are diverse in their interests and political standpoints. It seems just as likely that regional alliances may form in the NDB. The BRICS have already made strides in addressing voter representation issues, but with so much diversity within the founding members, maintaining an equal voice among them will remain critical to the NDB’s success.

Political Influence

To the greatest extent possible, the political influence of large shareholders must not impede prudential decision-making. No development bank has successfully exorcised this demon—though some are more professionally run than others—and all have suffered as a result. Politically charged lending or conditionality can have negative effects in two ways. It can limit good projects that would yield high development benefits and raise the reputation of the NDB. It can also cause the bank to take on loans that would otherwise be stalled, leading to the approval of lower-quality projects.5

Political influence can affect loan quality as well as the legitimacy of the entire organization. For example, the BNDES’ close political affiliation gives it easy access to funds, as well as fewer opposing views within the bank, but it also ties the fate of the bank to that of the government. The current government is burdened with a scandal involving the state-owned oil company, Petrobras. Unfortunately for BNDES, it lent the company $22 billion in 2010 alone.6 This association with Petrobras threatens to undermine the credibility of the bank because of the perception of political influence in its lending activities. The BRICS must learn this lesson and seek to establish institutional autonomy for the NDB in order to protect its legitimacy.

Conditionality

One of the main challenges development banks face is remaining fiscally responsible when trying to fund projects too risky for the private sector. Conditionality, referring to the requirements placed on borrowers to meet prudential performance benchmarks, like market assessments and audits on the use of funds, and values-based performance benchmarks, like requiring social and environmental impact studies. These protect the financial security and ethical use of loan money. Inadequate conditions can affect the financial security of loans and also lead to negative perceptions of the bank as a whole. The plethora of conditions placed on loans from the ADB and the World Bank has caused debate about whether they have become too onerous.

The NDB faces a particular challenge in reaching agreement on its approach to values-based mandates.7 On one hand, the bank can be seen as an alternative to the Western-based conditionality of existing institutions. MDB loan conditions are often called excessive or even hypocritical when requirements exceed the actions of the lender at a similar point of development. On the other hand, if it supports projects with controversial environmental, social, or corruption concerns, the NDB is left open to criticism. With the public’s negative perception of relaxed standards among banks in their home countries, the BRICS may struggle to avoid scrutiny on this issue. Making sure that conditionality is prudential, rather than political, is a prerequisite. However, the future of NDB’s values-based conditionality is more ambiguous.

Additionality

Development banks receive public funds or a de facto public guarantee that allows access to funds at sovereign interest rates. In effect, the taxpayer foots the bill, whether directly or implicitly through guarantees.

Table 1 — Summary of the Key Issues Facing the New Development Bank

In exchange for this bargain, development banks must serve a public purpose: economic development. But as financial markets develop in a wider swath of economies, many companies can borrow in private markets. Development banks should only lend where private banks cannot, instead of crowding out private investments. This is known as additionality because, for instance, the “additional” benefit to society from a subsidized development bank competing with private lenders is small, if not negative.

For example, the BNDES lends primarily to large, established firms despite its mandate to promote innovation.8 This is another major reason for its profitability and efficiency. Almost no other financial institution in Brazil competes with it in long- term finance. The lack of competition may derive from BNDES’s market dominance and low-cost funding base more than some lack of interest among private lenders.

Identifying which projects the private markets can finance is not always clear. The World Bank and Asian Development Bank often see lively debate in their boards between members that are strict (typically net lenders) and loose (typically net borrowers) about requiring additionality in loans.

The risk is that development banks can lose legitimacy, even if they hold themselves to high regulatory standards, if they no longer fill a public purpose in the economy. Beyond its internal structure, the NDB should consider its role in the landscape of existing development banks, and other start-ups such as the AIIB. Even at the global level, with a more varied array of projects to invest in, the NDB will only be useful if it fills an unmet need.

Conclusion

Despite the massive infrastructure needs in places like India—where expenditure needs for infrastructure may amount to $2 trillion over 10 years—the MDBs’ adherence to conditionality and additionality principles causes them to struggle to find enough loanable projects. Borrowers may not be willing to put up with the reviews required to satisfy first-world due diligence standards or the lengthy processing time for debate among the diverse board members.

These issues with the existing development banks, which the NDB seeks to avoid, do not have quick solutions. Some of the issues faced by existing MDBs, like excess influence by legacy powers, are deeply embedded in their architecture. This demonstrates the importance of addressing potential governance problems early on—problems that will become much harder to fix after the doors open. The NDB will succeed if the BRICS can establish an institution that is viewed as legitimate not just by lenders but by borrowers. This means overcoming not only voter representation issues, but also maintaining high standards on political influence, conditionality, and additionality. The NDB presents an opportunity for the BRICS countries to break from the practices of their domestic public banks and demonstrate their commitment to a new, positive force in economic development.

Endnotes

1. The BRICS are Brazil, Russia, India, China and South Africa. They began meeting in 2010 to promote their perspective on global issues as leading emerging economies.

2. See “eThekwini Declaration” at http://www.brics5.co.za/ and “Fifth BRICS Summit–Durban, South Africa,” at http://www.brics5.co.za/fifth-brics-summit-declaration-and-action-plan/.

3. Aldo Musacchio and Sergio G. Lazzarini, Reinventing State Capitalism: Leviathan in Business, Brazil and Beyond (Cambridge: Harvard University Press, 2014), 238.

4. See, for example, C.P. Chandrasekhar, “Banking With a Difference,” Economic & Political Weekly 49, no. 32 (2014): 10-12.

5. For more on this problem in the global institutions, see Ngaire Woods, The Globalizers: the IMF, the World Bank, and their Borrowers (Ithaca: Cornell University Press, 2006), 71.

6. Reinventing State Capitalism, 239.

7. This is discussed further in Russell Green, The New BRICS Bank Raises Tough Questions for Its Founders, July 23, 2014, Rice University’s Baker Institute for Public Policy, Houston, Texas.

8. The Economist, “A ripple begets a flood,” October 19, 2013, http://www.economist.com/news/finance-and-economics/21588133-politically-inspired-surge-lending-weakening-state-owned-banks-latin.

9. The Fortaleza Declaration was the official communiqué from the 6th BRICS Summit in 2014. “Sixth BRICS Summit-Fortaleza Declaration” VI BRICS Summit. http://brics6.itamaraty.gov.br/media2/press-releases/214-sixth-brics-summit-fortaleza-declaration.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.