Introduction

In the wake of the 2008 financial crisis, the U.S. Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“the Dodd-Frank Act”). While the intent of the act was to reduce risk-taking by the largest banks to prevent another financial crisis, many of the regulations were unfairly applied to small banks or had other unintended consequences.

In every year since, Congress has proposed and debated bills to reform the Dodd-Frank Act. One of the most important questions in those debates is if, and to what degree, Dodd-Frank increased the costs of regulatory compliance for U.S. banks. In a recent paper, my coauthor Scott Burns and I estimate the effects of the Dodd-Frank Act on U.S. bank expenses.1 This brief summarizes three key findings of that study:

- Banks’ total noninterest expenses increased by an average of more than $50 billion per year after the passage of Dodd-Frank.

- Increases occurred both in salary expenses from hiring new workers and in non-salary expenses such as auditing, consulting, and legal fees.

- Smaller banks were disproportionately affected by larger increases in salary and non-salary expenses.

The Dodd-Frank Act

Enacted July 10, 2010, the Dodd-Frank Act is, according to the U.S. Department of the Treasury, “the most comprehensive set of reforms to our financial system since the Great Depression.”2 The act made sweeping changes throughout the financial regulatory system including new regulations for systemically important financial institutions (Title I), a new framework for liquidating failing financial companies (Title II), added rules for the insurance (Title V) and mortgage (Title XIV) markets as well as new agencies for financial research (Title I) and consumer protection (Title X). This single act created more regulations than all other legislation under the Obama administration combined, making it what “may be the biggest law ever.”3

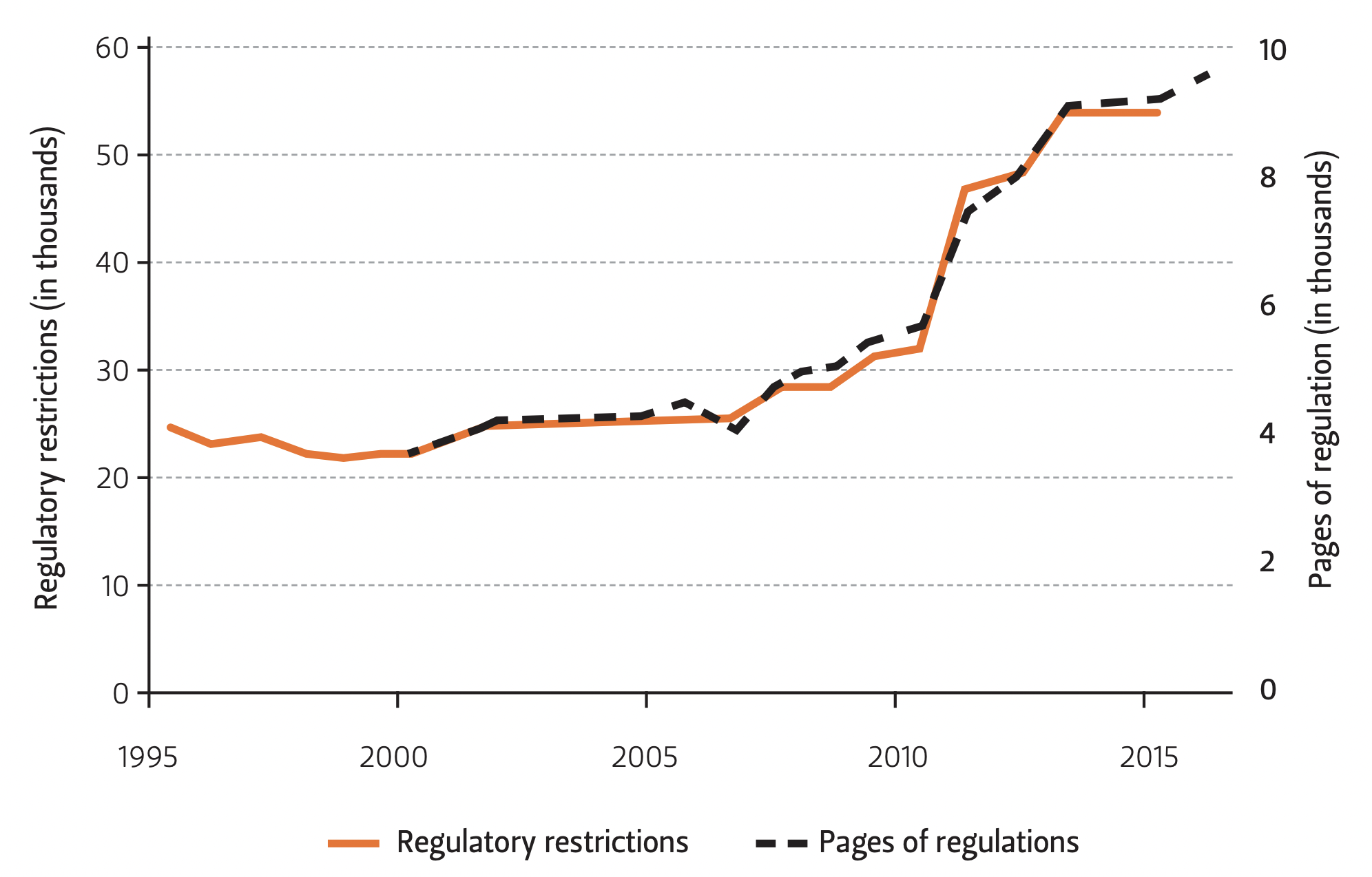

Figure 1 shows two measures of the number of regulations that apply to U.S. banks. The black, dashed line is the number of pages in the Code of Federal Regulation (CFR) Title 12 on Banks and Banking from 2000 to 2017. The orange line shows the number of regulatory restrictions in CFR Title 12 from 1995 to 2016 according to the RegData database, which counts the number of restrictions in regulatory texts based on words such as “must” and “must not” or “shall” and “shall not.”4

Figure 1 — Measures of Regulations in CFR Title 12 on Banks and Banking, 1995-2017

As seen in Figure 1, the years following the Dodd-Frank Act show a massive increase in banking regulations. The number of regulatory restrictions increased from 28,875 in 2009 to 53,974 by 2016, and the number of pages in CFR Title 12 increased from 5,065 in 2009 to 9,601 in 2017. By these measures, Dodd-Frank almost doubled the number of regulations applied to U.S. banks.

Costs of Compliance

Have increases in regulation affected bank expenses? Regulators argue that banks’ compliance costs have not increased,6 while critics, such as former National Economic Council director Gary Cohn, claim they amount to “literally hundreds of billions of dollars of regulatory costs every year.”7 In our recent paper “Has Dodd–Frank affected bank expenses?” published in the Journal of Regulatory Economics, my coauthor Scott Burns and I find that the truth lies somewhere in between.

Regulatory costs typically affect banks’ noninterest expenses, such as hiring new compliance officers or bringing in outside lawyers or consultants. Our analysis finds that total noninterest expenses in the banking system increased after 2010 by an estimated $64.5 billion per year, ranging from a low-end estimated increase of $58.7 billion to a high end of $86.1 billion per year.

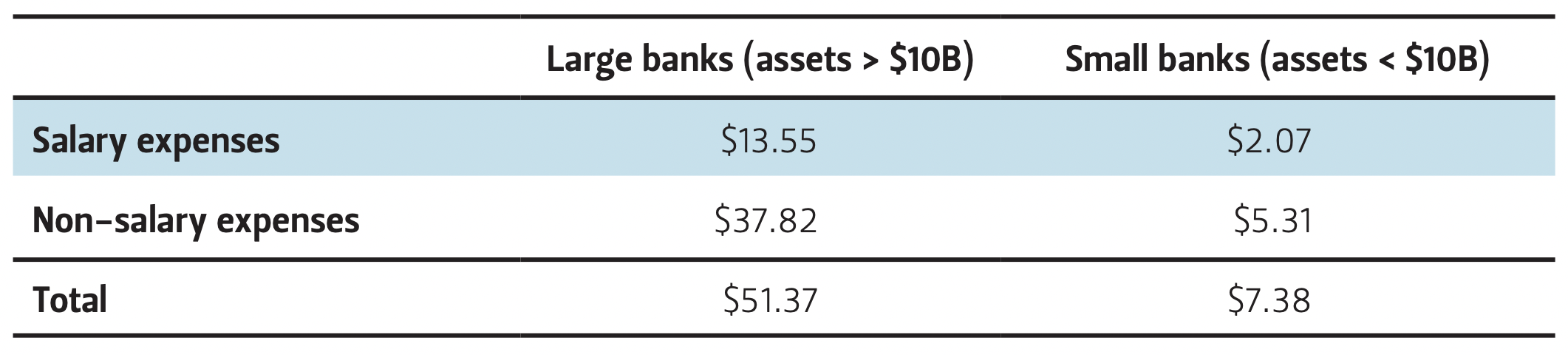

We can break these estimates down by bank size and by the types of expenses. We separate banks into two groups: “large” banks with $10 billion or more in total assets and “small” banks with assets less than $10 billion.8 We break noninterest expenses into separate categories for salary expenses of hiring new workers and non-salary expenses such as consulting and legal fees that might be related to regulatory compliance.

Table 1 shows the results of this breakdown. We see that salary and non-salary expenses increased for both large and small banks. Although the dollar amounts are bigger for large banks, the percentage increases are bigger for small banks, which make up only about 10% of total assets in the banking system.

Table 1 — Expense Increases at Large and Small Banks (Billions of Dollars per Year)

The increases in salary expenses are closely tied to increases in the number of regulations, while increases in non-salary expenses are mostly a one-time event after the passage of Dodd-Frank. Banks began to hire lawyers and consultants when Dodd-Frank was first passed in anticipation of coming regulations, but they did not begin hiring additional full-time employees until the new regulations went into effect.

Non-salary Expenses

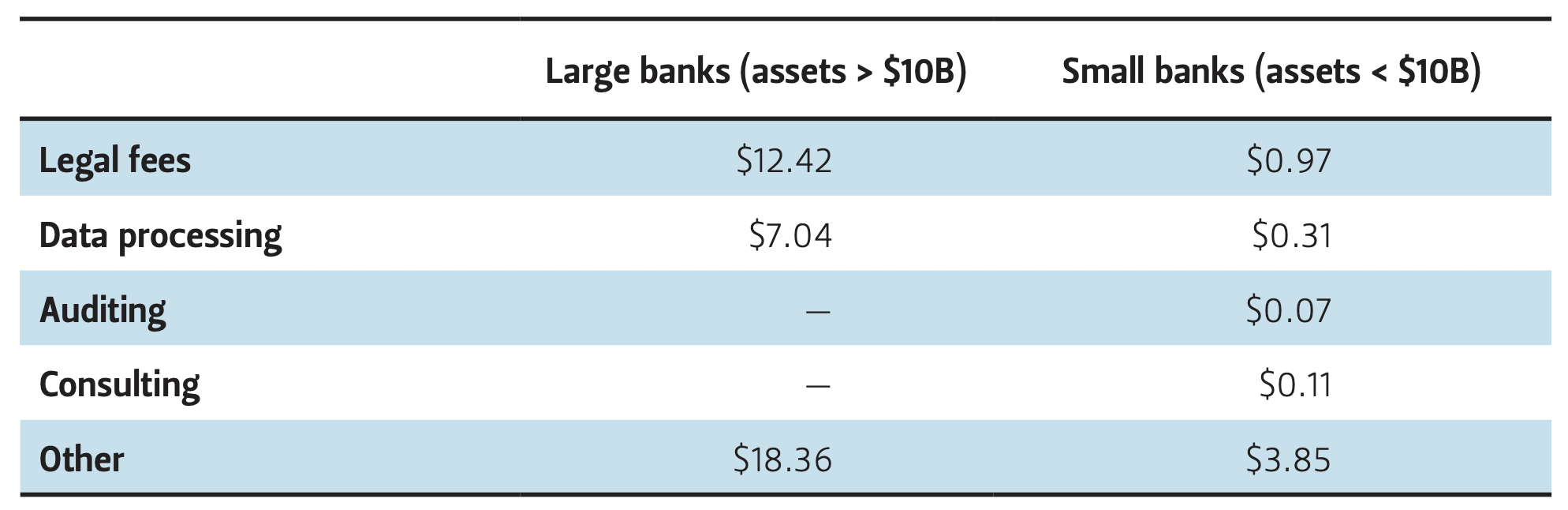

We can also test for increases in four subcategories of non-salary expenses: legal fees, data processing, auditing, and consulting expenses. Table 2 shows the increases for large and small banks in each of these subcategories. Large banks spent an additional $12.42 billion per year on legal fees and $7.04 billion on data processing relative to before the Dodd-Frank Act. Changes in auditing and consulting expenses are not statistically significant. The category “other” expenses, calculated as non-salary expenses from Table 1 minus the other subcategories, makes up roughly half of the total.

Table 2 — Increases in Subcategories of Non-salary Expenses (Billions of Dollars per Year)

Small banks experienced statistically significant increases after Dodd-Frank in all four categories of non-salary expenses. They spent almost $1 billion more per year on legal fees. They increased annual spending on data processing, auditing, and consulting by roughly $310 million, $70 million, and $110 million respectively, and they spent an additional $3.85 billion per year on other non-salary expenses relative to before Dodd-Frank. Compared to large banks, increases in small banks’ non-salary expenses were bigger and more likely to be statistically significant.

Conclusions

The Dodd-Frank act roughly doubled the number of regulations applied to U.S. banks, which increased their compliance costs by more than $50 billion per year. Banks experienced a one-time increase in non-salary expenses, while their salary expenses increased in proportion to new regulations. Small banks experienced disproportionate increases in salary expenses as well as significant increases in auditing, consulting, data processing, and legal fees. U.S. regulators and policymakers may wish to consider these results when developing future regulatory policies.

Endnotes

1. Thomas L. Hogan and Scott Burns, “Has Dodd–Frank affected bank expenses?” Journal of Regulatory Economics (2019) 55: 214-236.

2. Department of the Treasury, The Dodd–Frank act: Reforming wall street and protecting main street, Washington, DC: U.S. Department of the Treasury, January 2017.

3. Patrick McLaughlin and Oliver Sherouse, “The Dodd-Frank Wall Street Reform and Consumer Protection Act May Be the Biggest Law Ever,” Mercatus Center at George Mason University, July 20, 2015.

4. Omar Al-Ubaydli and Patrick A. McLaughlin, “RegData: A numerical database on industry-specific regulations for all United States industries and federal regulations, 1997–2012,” Regulation and Governance 11(2017): 109–123.

5. Data available online at https://quantgov.org/regdata-us/.

6. See, for example, Roisin McCord and Edward Simpson Prescott, “The financial crisis, the collapse of the banking industry, and changes in the size and distribution of banks,” Economic Quarterly, 100(1), 23–50. 2014; and Government Accountability Office, Dodd–Frank regulations: Impacts on community banks, credit unions and systemically important institutions, Washington, D.C.: Government Accountability Office, 2015.

7. Quoted in Michael C. Bender and Damian Paletta, “Donald Trump Plans to Undo Dodd-Frank Law, Fiduciary Rule,” Wall Street Journal, February 3, 2017.

8. Results are similar when the size categories are divided into large banks (assets > $50 billion), regional banks ($10-50 billion in assets), small banks ($1-10 billion in assets), and community banks (assets < $1 billion)

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.