Abstract

Property tax is a vital and stable source of revenue for many local governments. One reason for the stability of this revenue is the tendency of tax levies to increase automatically with property values. However, this same characteristic can have negative economic consequences and pose a hardship for property owners if unchecked, especially in states that rely heavily on property tax as a source of revenue. As a result, many states have adopted truth-in-taxation measures to highlight tax increases and give citizens the opportunity to express opposition through the democratic process, whether at a public meeting, through a ballot measure or at the next election of government officials.

Drawing on past research, we assert that truth-in-taxation measures, while successful in other states, have failed to constrain the property tax burden in Texas to the satisfaction of property owners. We also examine ways to enhance the efficacy of truth-in-taxation measures in Texas and suggest changes to the new digital tax rate notice implemented in 2020 and 2021. These recommendations, based on cognitive load theory, could lead to an increase in popular understanding of tax rate notices in Texas as well as increased citizen participation in decisions involving proposed property tax rates.

Introduction

Property tax is a necessary evil as it provides a reliable source of revenue for local governments (Goodman 2018). State and local governments can maintain financial autonomy and fiscal stability because of the revenue they collect in the form of property tax (Fischel 2001). Although some experts hold a positive attitude toward property tax, taxpayers who observe a consistent rise in property tax levies maintain a less positive view. In other words, no candidate wins an election by vowing to collect more property tax. In fact, candidates are more likely to gain traction if they promise to reduce the property tax burden (Cornia and Walters 2006). In an attempt to slow the growth of property tax, state legislatures have adopted full-disclosure policies and truth-in-taxation measures. These measures are intended to help property owners hold elected officials accountable for the taxes they impose and, either directly or indirectly, to curtail increases in property tax.

In this paper, we examine ways to enhance the efficacy of existing truth-in-taxation notices in the state of Texas. In order to identify which format of the notice furthers understanding or comprehension among property owners, we adopted an experimental survey design and systematically varied elements of the notice across four different conditions. The findings from the project will inform the policies of states that want to adopt truth-in-taxation measures or increase the efficacy of existing measures.

Background on Truth-in-Taxation and Disclosure Measures

A common notion is that, as the market value of real property increases, accompanying increases in taxable value inevitably lead to a rise in property tax levies (Lyman 2006). In reality, this is true only when government officials choose not to decrease tax rates in response to an increase in property values. The lack of downward adjustment of tax rates in the face of higher property values results in a windfall of revenue to taxing units and an irritation to taxpayers. Even though the windfall may not fully capture the increase in property values, recent research investigating the relationship between home prices and property tax levies demonstrates that local policymakers do incorporate a portion of housing value increases in proposed tax levies (Goodman 2018).

In order to curtail unwarranted increases, a variety of policies are used to deter the escalation of property tax levies. Explicit policies include tax and expenditure limits (commonly known as TELs) that are adopted by state governments and imposed on local taxing units. In other words, taxing units are unable to adopt a tax rate that exceeds the specified tax limit (Cornia and Walters 2006). Past research notes that property tax limits tend to have unintended negative consequences. For example, in places where property taxes fund K-12 education, a decrease in property tax revenue adversely impacts educational initiatives and limits the efficiency of school administrators (Eom and Rubenstein 2006). Contrarily, news articles in Texas reported that, in response to TELs that took effect in 2020, local elected officials imposed property tax rates for 2019 in excess of those needed to fund current needs (Ramsey 2019). Similarly, a reduction in income from property tax prompts local governments to make up the lost revenue by increasing other forms of taxes such as excise taxes (Shadbegian 1999).

In addition to these explicit policies, truth-in-taxation and full-disclosure laws are often implemented in an effort to decelerate the rise in property tax. While these policies are less researched, Cornia and Walters (2006) concluded that full-disclosure and truth-in-taxation laws are less likely to trigger the negative consequences of TELs and provide more flexibility to local officials who determine budgets for local taxing units. These laws dictate that residents within a taxing unit be notified about any proposed increase in property tax levies. The notice to residents must be published in a public medium (e.g., the local newspaper) and provide the venue and time of public meetings during which residents may voice their opinions on whether or not local elected officials should increase the property tax. Research notes that after the adoption of full-disclosure laws in Utah, counties responded by reducing their tax rates in relation to an increase in real estate prices (Cornia and Walters 2006). Similarly, recent research that investigated the rise and decline of property tax across all U.S. states from 1998 to 2012 corroborates Cornia and Walter’s findings. Findings from this research indicate that states that adopted truth-in-taxation requirements were able to apply political pressure on local officials to slow the growth of the property tax burden (Goodman 2018).

Current Research On Enhancing Existing Truth-in-Taxation Measures

Substantial evidence demonstrates that full-disclosure policies or truth-in-taxation laws adopted by state legislatures have the potential to stall or prevent the drastic elevation of property tax. Goodman (2018) suggests that there may not be a need to apply real political pressure on local officials; instead, the fear of negative consequences (such as being voted out of office in the next election) is sufficient to inspire officials to reduce tax rates when housing prices escalate. In essence, these policies are restoring strength in the democratic process by allowing residents to approve or disapprove an increased tax levy.

Although the research discussed above demonstrates the efficacy of full-disclosure policies in reducing the property tax burden in states such as Utah and Florida, the same cannot be said for Texas. Research on the implementation of truth-in-taxation measures in 1982 notes that these measures did not reduce the real per household tax burden. Instead, the implementation of the truth-in-taxation measures caused local residents to experience a modest increase in their property tax burden over the four-year period examined (Bland and Laosirirat 1997). Research also suggests that current truth-in-taxation measures in Texas do not prompt taxpayers to participate in the tax rate decisions of local taxing authorities. The number of witnesses who attended tax rate hearings across the five most populous counties in Texas in 2016 ranged from zero to 16 people (Rabb 2019). The contrasting experiences of Texas and Utah with truth-in-taxation measures suggest that the procedures utilized in Texas could be enhanced to increase their efficacy.

We argue that the ineffectiveness of truth-in-taxation measures in Texas is a consequence of the confusing information presented to taxpayers, and we assert that tax rate notices that present less confusing information can enhance understanding among taxpayers. Comprehension of the tax rate notice is critical because if taxpayers do not understand the information provided in the notice, they are unable to successfully act on that information — i.e., participate in public tax rate hearings or other civic debates. In other words, a tax rate notice that is published to inform citizens and enhance awareness serves its purpose only if the notice can be readily understood by the public.

These assertions are rooted in accepted theory and supported by scholars in the field of public administration who note that simply granting citizens a wider access to policy information does not guarantee enhanced understanding of the policy (O’Neill 2002). Alternatively, focusing on the elements of information and how those elements are presented to the public enhances the public’s understanding of a given policy (Mansbridge 2009). Furthermore, cognitive load theory asserts that individuals find it easier to comprehend a message when they are required to exert less mental effort to process it. Enhanced understanding of the message also makes it easier to use the information embedded in it (Paas, Renkl, and Sweller 2003). Past research notes that government entities are successful in encouraging citizens to sponsor or participate in civic activities when they can easily understand public policies and are able to educate themselves about how certain policies are likely to impact them (Thomsen and Jakobsen 2015).

Another characteristic of truth-in-taxation measures in Texas is the provision of information on tax increases only at the collective level (e.g., county or city) and not at the individual level. Specifically, from 1982 to 2019, tax rate notices provided information for a taxing unit as a whole and merely gave instructions to taxpayers about how to calculate the effect of the proposed tax rate for their own properties (Texas Tax Code §26.06). According to cognitive load theory, property owners in Texas were required to exert a substantial amount of mental effort to understand how a notice showing a tax increase at the collective level applied to their individual cases. This format of presenting a tax increase, where the financial impact on the individual citizen is not obvious, delivers the information in a manner that is not salient to individual citizens. Research on political participation illustrates that citizens’ willingness to attend to a specific issue and to actively engage is contingent on the extent to which they perceive the issue at hand as salient to themselves (Verhoeven 2009 as cited in van Eijk and Steen 2014). Therefore, from the perspective of usefulness and ease of understanding, truth-in-taxation notices in Texas from 1982 through 2019 were less likely to elicit participation among citizens.

To address this shortcoming, in 2019, Texas enacted a new requirement that all counties deliver individualized tax rate notices to property owners digitally (Texas Property Tax Reform and Transparency Act 2019). The new law, which took effect in 2020 for counties with a population of 200,000 or more, and in 2021 for all other counties, also prescribed the content of the individualized digital tax rate notice. However, while the digital notice is required to include complex legal constructs such as the “no-new-revenue tax rate” and the “voter-approval tax rate” (essentially jargon for most citizens), it does not require a simple comparison between the amount of tax paid last year and the amount proposed for the current year. Hence, the new digital notice is still likely to require citizens to exert a substantial level of mental effort and is less salient than it could be.

Our research aims to enhance the efficacy of the newly-implemented truth-in-taxation measure in Texas. We investigate what kind of information presented in the digital tax rate notice of a county enhances understanding of a tax increase and prompts participation among property owners on the digital platform. Specifically, we intend to examine whether the presence of explicit language that states a tax increase and the clarity of the notice (operationalized as a lack of jargon) impact property owners’ understanding of the tax rate notice. Our research question and hypotheses are outlined below, followed by an overview of the two studies we conducted to test the hypotheses.

Research question: What information presented in the digital tax rate notice helps property owners identify a tax increase?

Hypothesis 1: Explicit terms in a tax rate notice indicating a tax increase will be positively associated with participants’ comprehension of the notice.

Hypothesis 2: Clarity of a tax rate notice will be positively associated with participants’ comprehension of the notice.

Hypothesis 3(a): Explicit terms in a tax rate notice indicating a tax increase will be positively associated with participants’ decisions to give feedback to the county.

Hypothesis 3(b): Clarity of a tax rate notice will be positively associated with participants’ decisions to give feedback to the county.

Study 1

Methods

This study adopted a 2x2 between-subjects design and aimed to measure the efficacy of the truth-in-taxation notices that are delivered to property owners in Texas. Study 1 sought to test the hypotheses and to survey participants for their opinions and preferences on tax rate notices and the property tax burden. Study 2 sought to test the same hypotheses, while eliminating a confounding variable present in Study 1.

Procedure

We submitted an open records request to the appraisal district offices of 27 counties in Texas to obtain an appraisal roll containing names and mailing addresses of both residential and business property owners. To ensure that all geographic areas of Texas were represented in the sample pool, we set out to select the most populous county from each of the 31 state Senate districts in Texas that would also result in a unique county from each district. The vagaries of Senate district lines necessitated some departures from the methodology, which ultimately yielded 27 unique, geographically dispersed counties.[1]

We adopted a cluster stratified sampling method to recruit our participants. Participants were either residential and/or business property owners and were randomly recruited from 27 counties in Texas. Potential participants received letters via the U.S. Postal Service providing a website link and unique key. Participants entered the key in the designated website to securely log into our study’s online survey. Since potential participants may not be familiar with our organization — the McNair Center for Entrepreneurship and Economic Growth at Rice University’s Baker Institute for Public Policy — we enlisted support from the Texas Association of Appraisal Districts (TAAD) to lend credibility to our request for participation in the survey. TAAD is a voluntary, nongovernmental, statewide membership organization of appraisal districts and property tax officials across Texas. The letter from TAAD was intended to bolster the confidence of a potential participant who might be unsure of the veracity or legitimacy of the survey invitation letter.

Participation in the survey was entirely voluntary, and participants were compensated for survey completion with digital Amazon gift cards worth $25 each. Data was collected in a confidential manner, and the research team sought approval from Rice University’s Institutional Review Board (IRB) before beginning data collection.

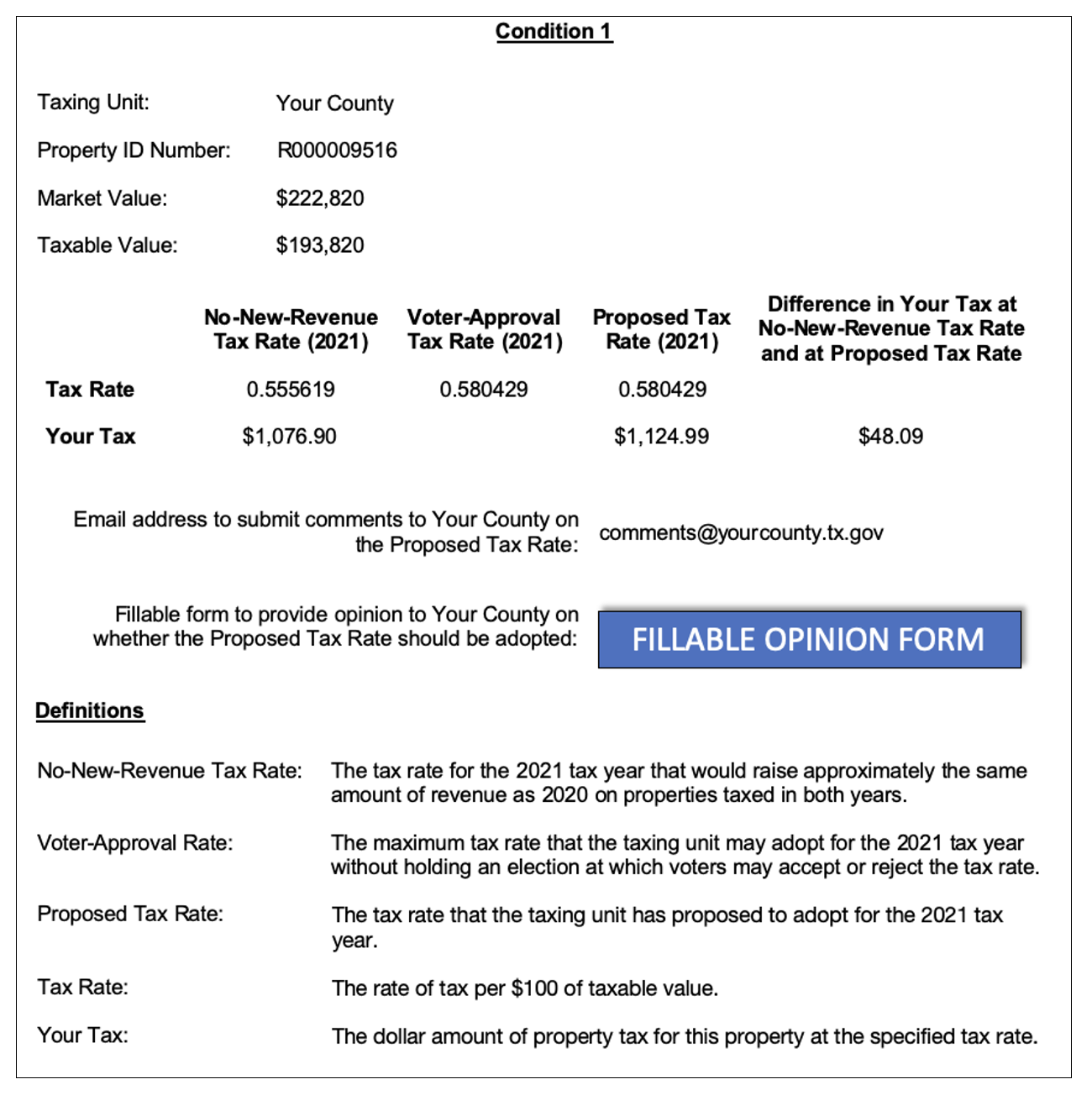

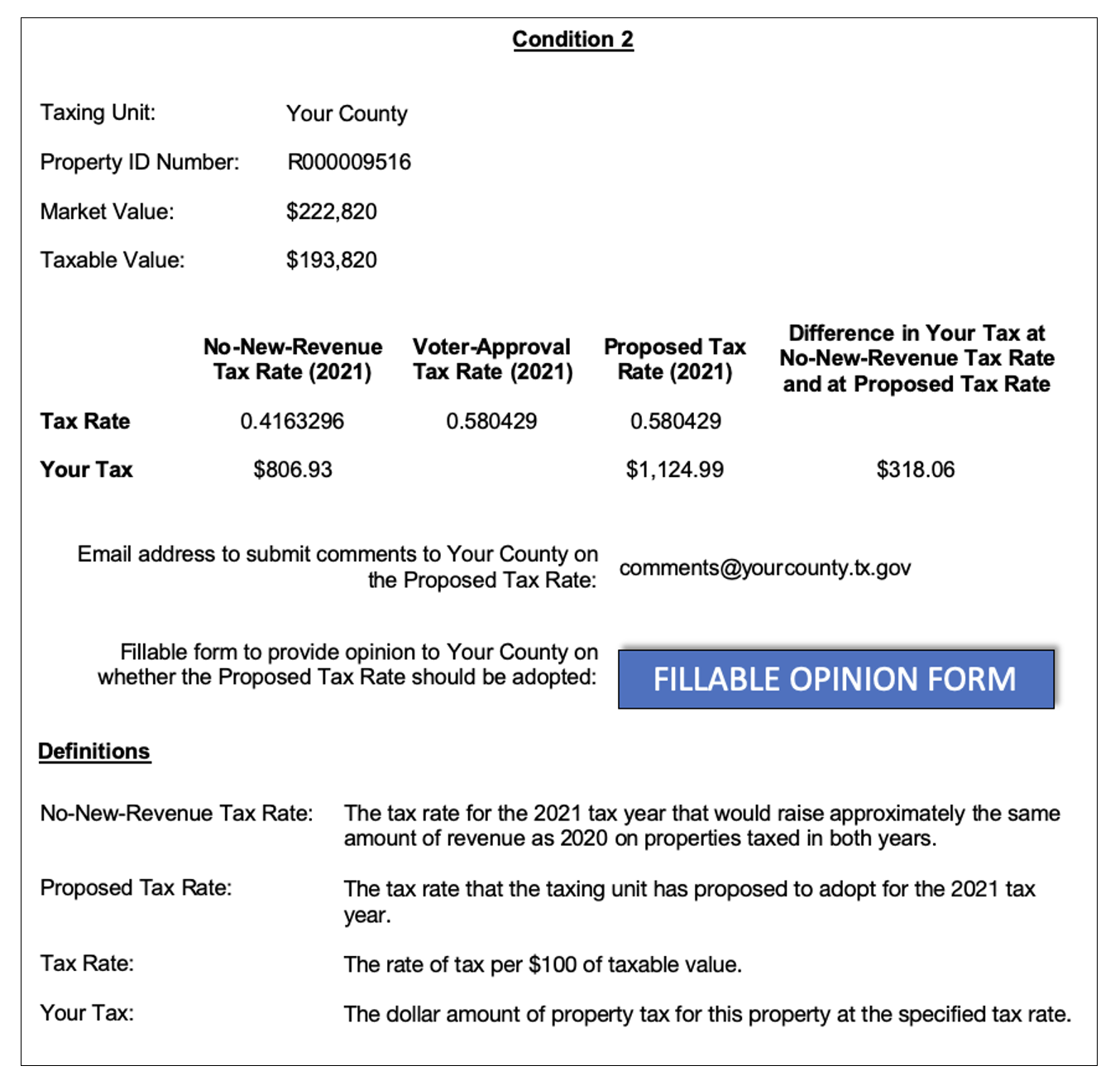

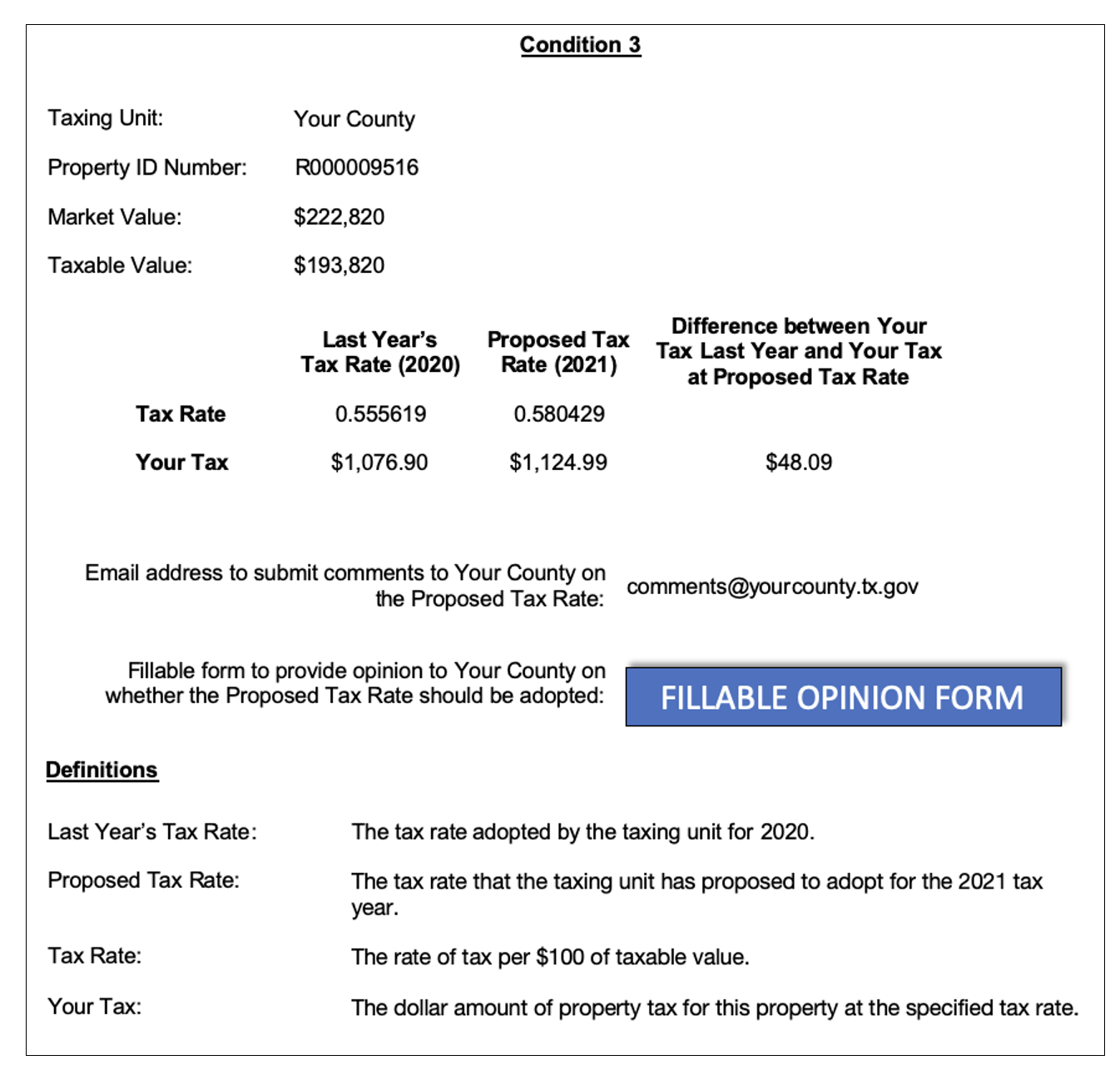

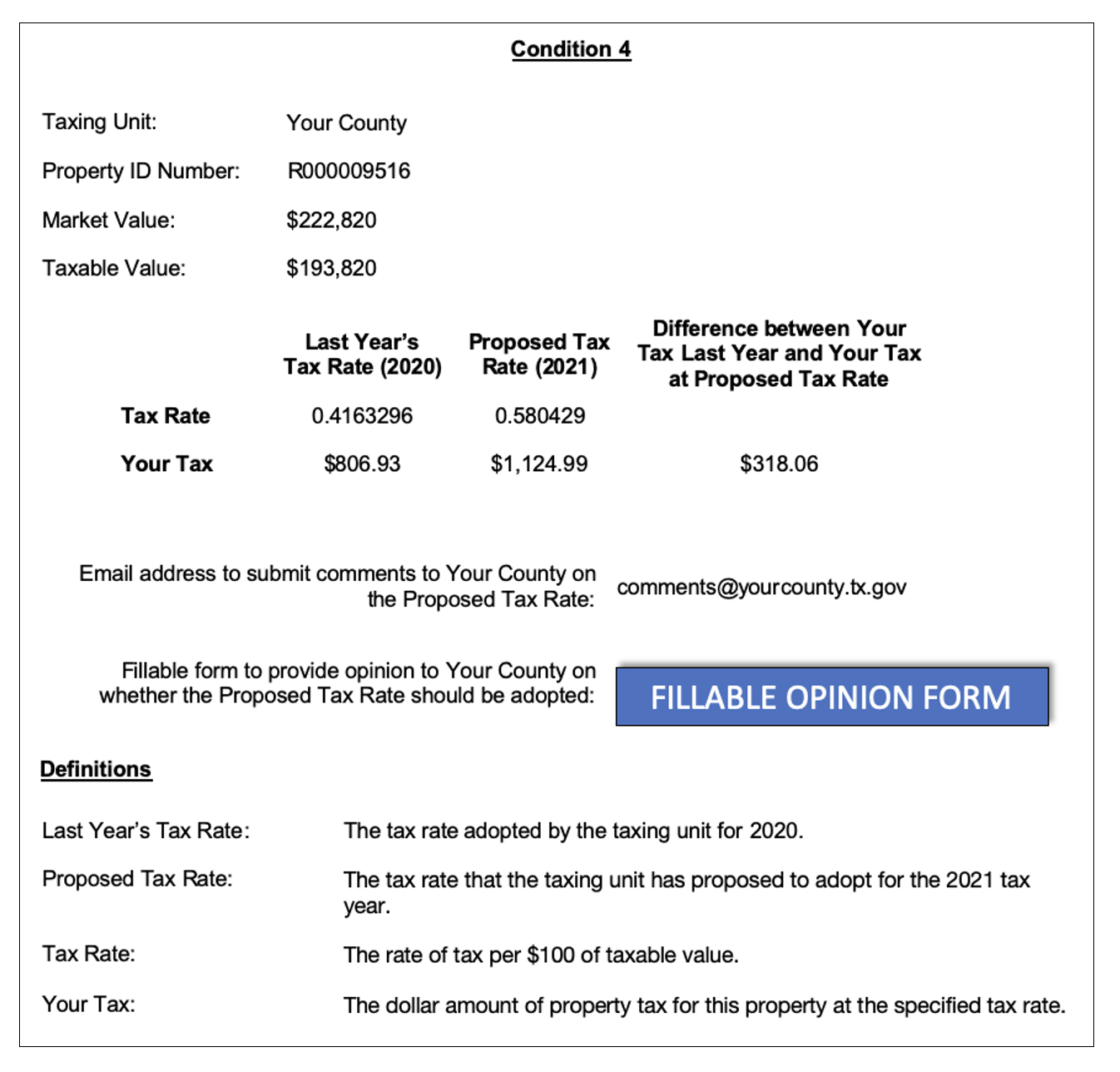

The two variables manipulated in this study were (i) use of explicit language to indicate a tax increase and (ii) clarity, meaning the absence of jargon. The study utilized the following four conditions: explicit language/high clarity; explicit language/low clarity; no explicit language/high clarity; no explicit language/low clarity. Each participant was randomly assigned to one of the four conditions. In each condition, participants read a hypothetical tax rate notice that presented both a higher tax rate and a higher tax levy compared to the prior year — in other words, a tax increase.

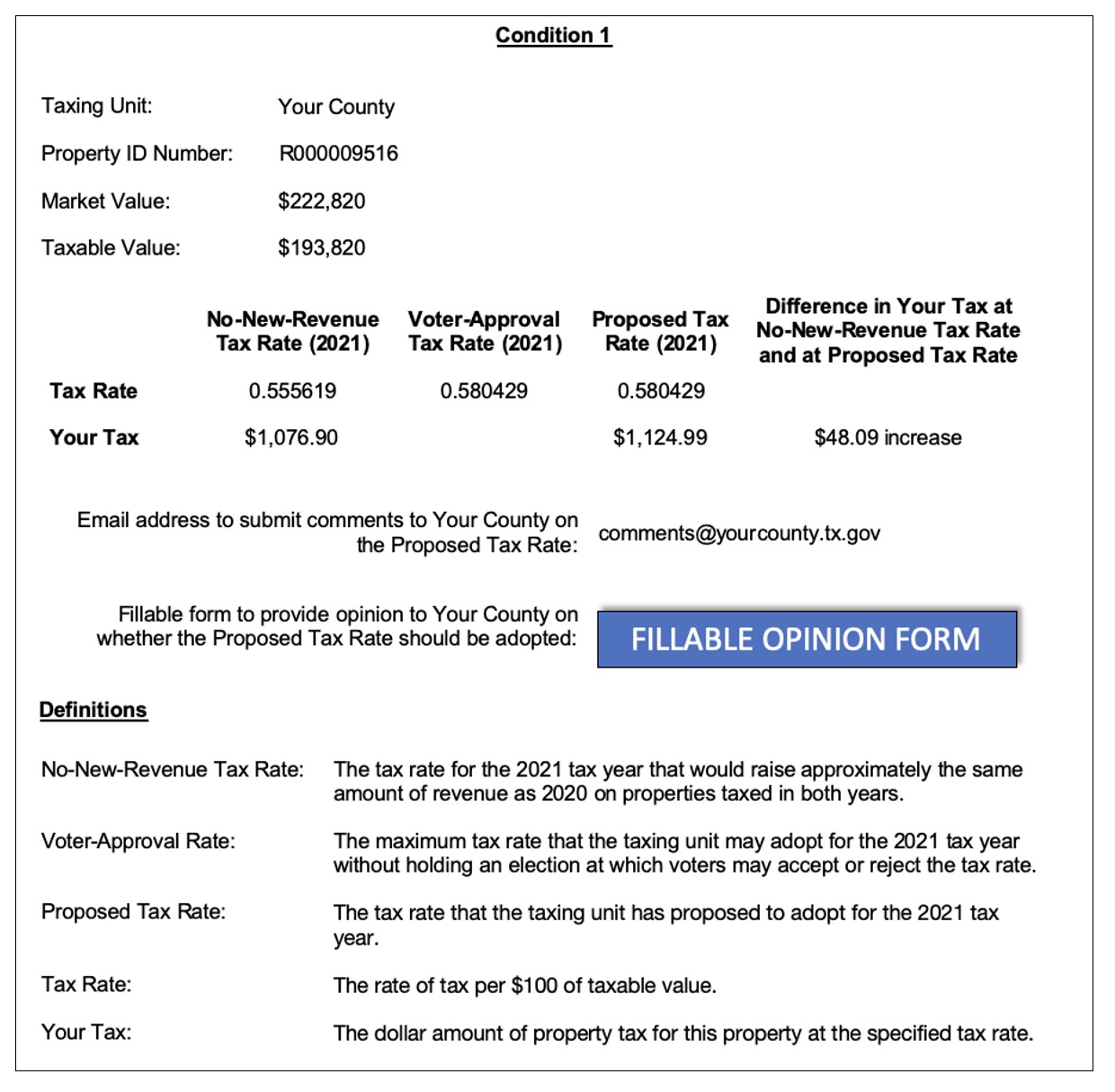

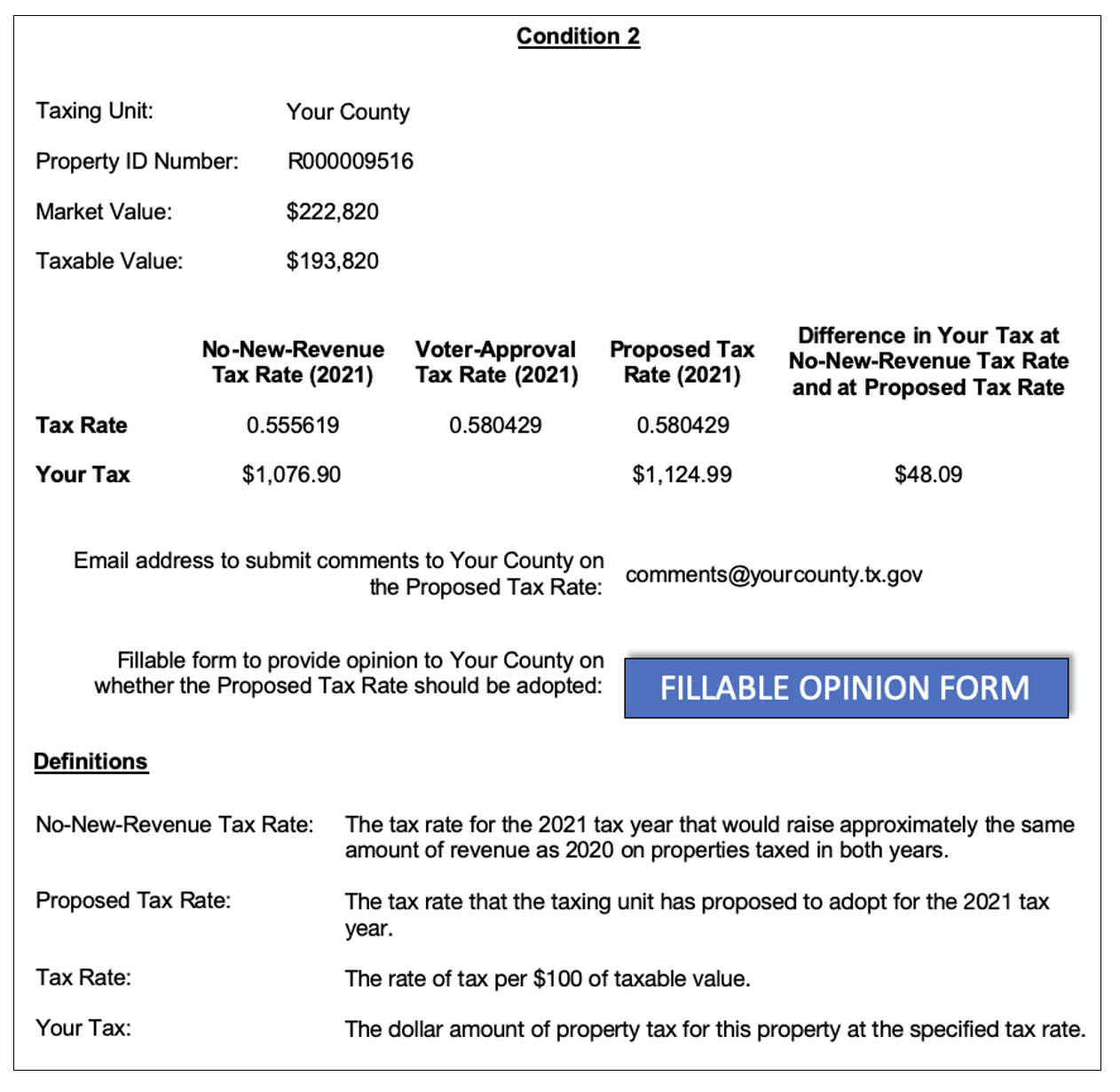

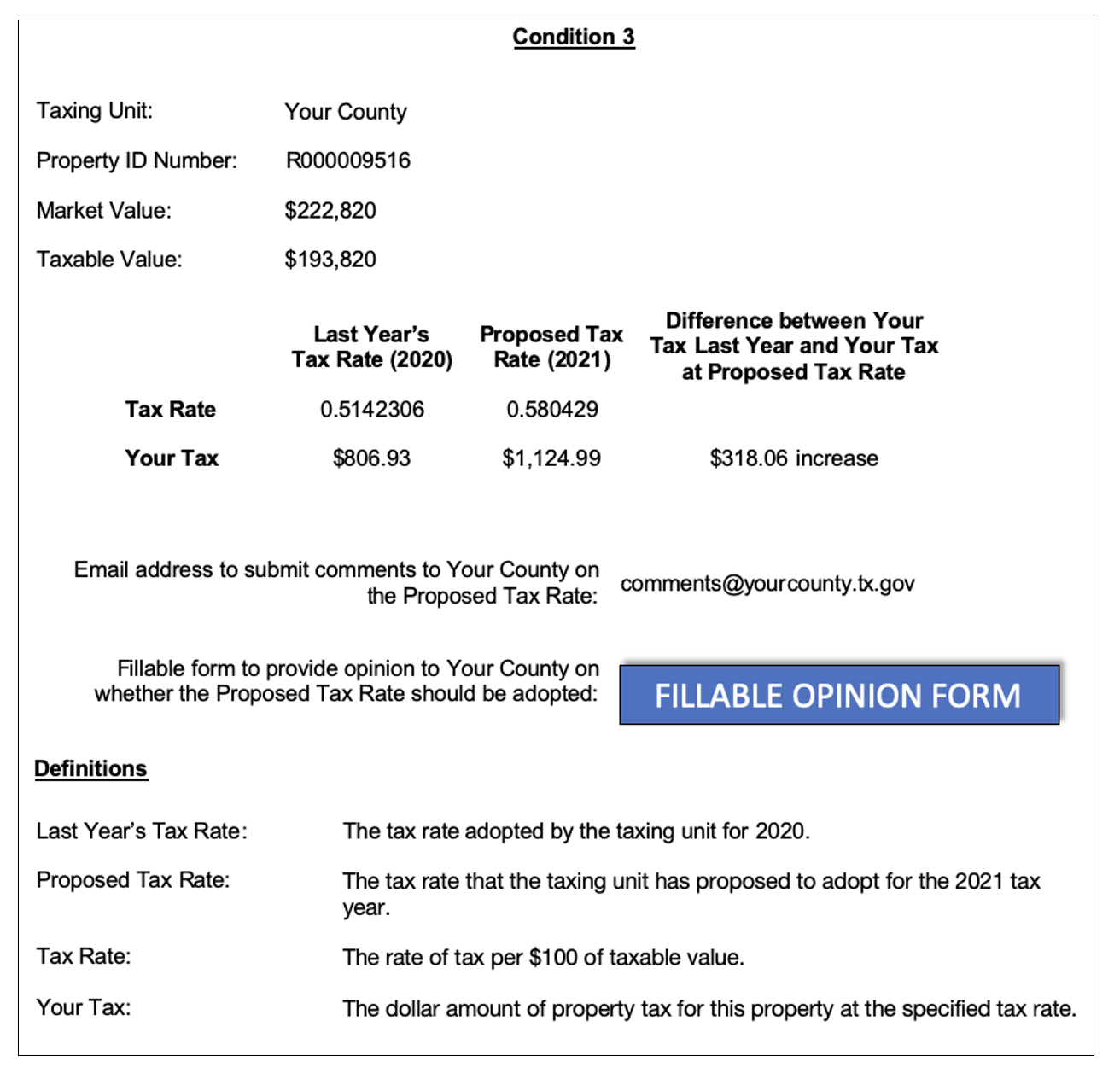

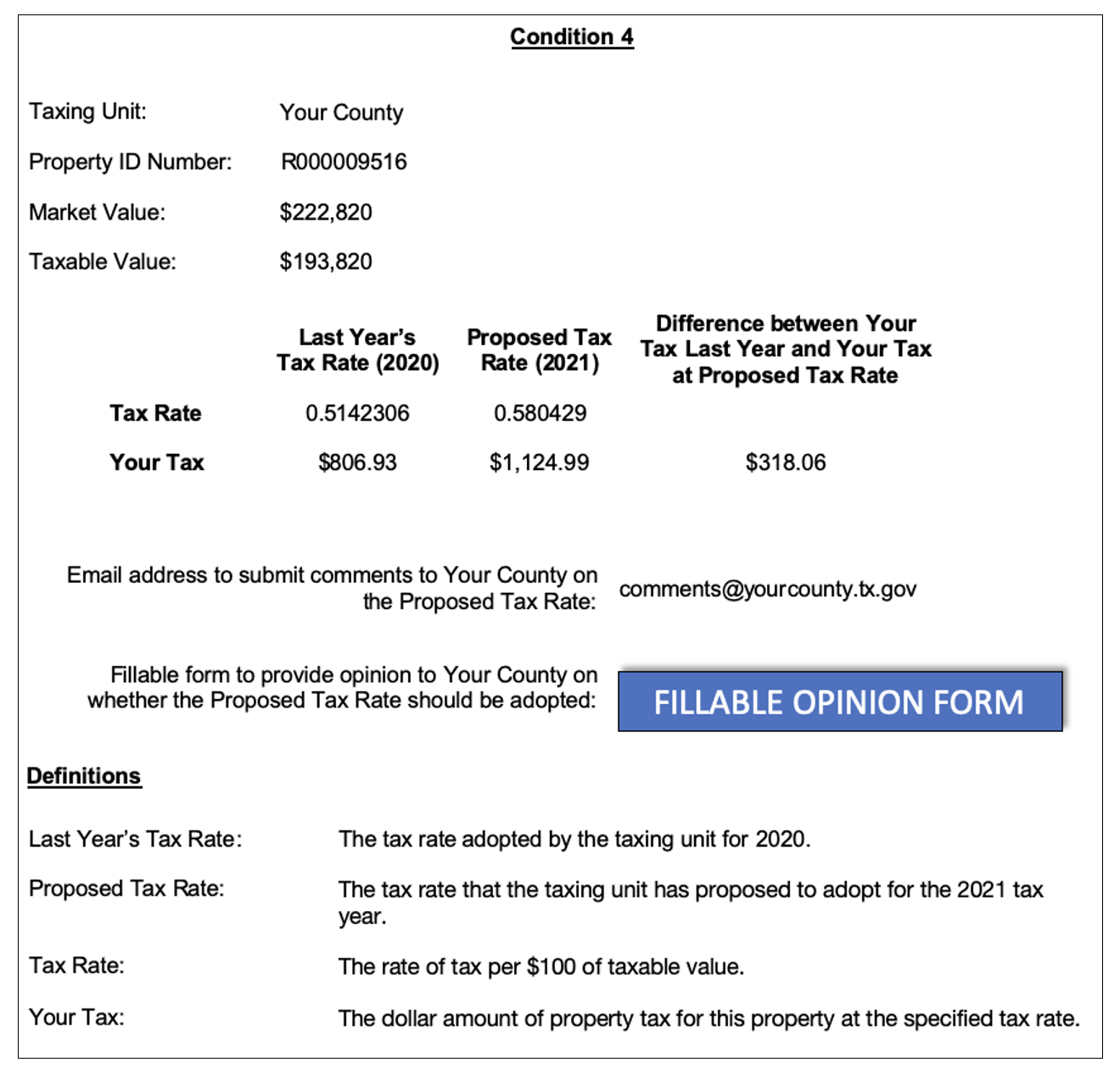

The hypothetical tax rate notice in each condition followed the form of the new Texas law, except for the variables that were manipulated. In order to ensure that the tax rates in the study were of realistic scale and relationship to one another, the conditions showed the actual tax rates, taxable value and tax amounts of the 2020 digital tax rate notice for one property in Van Zandt County, Texas.[2] Every possible comparison of a tax rate for 2021 to the tax rate for 2020, and the associated tax amount, represented a tax increase. The four conditions used in the study are shown in Appendix A: Study 1 Conditions. Condition 3 adhered to the form of tax rate notice required by the Texas law.[3] The other three conditions were variations on this form that manipulated the independent variables.

Sample

The final analyses were conducted on 527 participants. Two participants were deleted because they responded “no” to both survey items that asked whether they were homeowners or business owners (the selection criteria required participants to be a homeowner and/or a business owner). An additional 17 records were deleted because the participants completed less than 50% of the survey.

A majority of the sample was comprised of business owners (52.56%). The sample was predominantly male (63%). The average age of the sample was 58.22 years, and participant ages ranged from 21 to 95 years. The ethnic composition of the sample was as follows: White (67.5%), Hispanic (14.23%), Black (2.85%), Asian (6.6%), American Indian or Alaska Native (0.57%). Only 6.83% of the sample preferred not to reveal their ethnicity, and 1.33% did not respond to the question. A majority of the participants identified themselves as being extremely proficient in reading the English language. The educational attainment of the sample was as follows: bachelor’s degree (33%), master’s degree (≈23%), high school diploma (20%), associate’s degree (≈10%), professional degree (e.g., JD) (≈9%), doctoral degrees (4%), less than high school diploma (≈1%).

Independent Variables

Explicit language in the tax rate notice: The purpose of this variable was to determine whether providing language in the tax rate notice that explicitly states a tax increase enhances a participant’s understanding of the notice. Each of the four conditions showed the dollar amount of the tax increase, which was either $48.09 or $318.06. This variable was manipulated by adding the word “increase” after the dollar amount of the tax increase for the explicit conditions and by omitting the word “increase” after the dollar amount of the tax increase for non-explicit conditions.

Clarity: The purpose of this variable was to examine whether the use of jargon impairs a participant’s understanding of the notice. This variable was manipulated by the presence and absence of last year’s tax rate, no-new-revenue tax rate and voter-approval tax rate. Specifically:

(i) In the low-clarity conditions, last year’s tax rate and related tax amount were absent, and the no-new-revenue tax rate with related tax amount and voter-approval tax rate were present. The tax increase was presented as the difference between the tax amount at the proposed tax rate and the tax amount at the no-new-revenue tax rate, which was $48.09; and

(ii) In the high-clarity conditions, last year’s tax rate with the related tax amount was present, and the no-new-revenue tax rate with related tax amount and voter-approval tax rate were absent. The tax increase was presented as the difference between the tax amount at the proposed tax rate and the tax amount at last year’s tax rate, which was $318.06.

Dependent Variables

Comprehension of tax rate notice: This variable is operationalized as the participant’s understanding of the notice and was measured in two different ways. First, we measured how easy it was for participants in various conditions to identify a change in the tax amount using a Likert-type survey item (“The notice presented above helped me easily identify the change in the amount of property tax I would be required to pay.”). The response options ranged from 1=Strongly disagree to 5=Strongly agree. Second, we measured participants’ understanding of the notice with two multiple choice items. The first item (“The notice presented above proposes a tax increase.”) had response options true or false. The response option “true” received a score of 1 and “false” received a 0. The second item (“Compared to 2020, which of the following is true for 2021?”) had response options: (a) The county has proposed a property tax increase. (b) The county has proposed a property tax decrease. (c) The county has proposed to keep property taxes the same. This item was recoded to be a binary item such that those who chose a response option (a) received a score of 1 and those who chose either of the other two response options were given a score of 0. We created a composite average score of these two items.

Feedback: Participants’ likelihood of sending feedback was measured using a single item: “The sample notice provides an opportunity to send feedback to the county on the proposed tax rate and how it affects you. If this were a real notice, would you send feedback to the county?” (Response options: yes/no).

Results

Between-subjects 2x2 ANOVA models were conducted to test the first two hypotheses. A logistic regression model was conducted to test the third hypothesis.

Hypothesis 1 stated that tax rate notices including language that explicitly makes participants aware of an increase in tax rate will enhance participants’ understanding of the notice. This hypothesis was not supported. As mentioned above, we operationalized comprehension of the tax rate notice, first, in relation to ease of identifying a change in tax amount due on the notice and, second, by requesting participants to identify whether the notice represents a tax increase or decrease. The ANOVA model revealed that participants who were assigned to the explicit condition (with the word “increase” next to the change in the tax amount) (M= 4.07) were as likely as participants who were assigned to the non-explicit condition (without the word “increase” next to the change in the tax amount) (M = 4.14; (F (3,523) = 0.7, p = 0.4)) to agree that the notice made it easy for them to identify a change in the tax amount due to the county. In other words, both sets of participants reported that the notices they received were equally helpful in identifying the change in the property tax amount they are required to pay to the county. A following between-subjects 2x2 ANOVA model revealed that participants in the explicit (M = .95) and non-explicit (M =.94; (F (3,523) =.12, p = 0.7)) conditions exhibited a similar understanding of the tax rate notice. Specifically, both sets of participants responded to a similar number of questions correctly by identifying a tax increase.

Hypothesis 2 predicted that tax rate notices with higher clarity would enhance participants’ comprehension of the notice. This hypothesis was supported. The ANOVA model revealed that participants who received a tax rate notice without jargon (M = 4.41) were more likely to agree that the notice made it easy for them to identify a change in tax amount due to the county compared to the participants who received a tax rate notice with jargon (M= 3.81) (F (3,523) = 49.15, p <.001). A subsequent between subjects 2x2 ANOVA model was conducted to examine if participants who received the tax rate notice with no jargon were able to demonstrate a higher level of notice comprehension than those who received a tax rate with jargon. Results revealed that indeed clarity does matter. On average, participants who received the notice with no jargon (M =.98) answered more questions correctly by identifying a tax increase than those who received a notice with jargon (M = .90) (F (3,523) =24.02, p <.001). However, with respect to Hypothesis 2, the study contained a confounding variable. All participants who were shown a notice without jargon were also shown a tax increase of $318.06, while all participants who were shown a notice with jargon were shown a tax increase of only $48.09. (This confounding variable resulted from using the actual tax rates of Van Zandt County for all conditions.) Consequently, it is unclear whether the better performance and ease of participants who received a notice without jargon was attributable to the absence of jargon or to the greater magnitude of the tax increase. We addressed this question in Study 2, discussed below.

Hypotheses 3(a) and 3(b) predicted that participants who read tax rate notices with explicit language stating an increase in tax amount or with no jargon, respectively, would be more inclined to provide feedback to the county than those who read notices with no explicit language or with jargon. The logistic regression results revealed that there was no association between explicit language (i.e., the addition of the word “increase”) and the participant’s likelihood of providing feedback, OR (Odds Ratio) = 0.79, p = 0.4. The odds of providing feedback were 21% lower for participants who received notices with explicit language than those who received notices without the explicit language, but this difference was not statistically significant. Hence, Hypothesis 3(a) was not supported. However, the odds of providing feedback was two times greater among participants who received notices with no jargon than participants who received notices with jargon, OR = 2.24, p = .002. The odds of providing feedback were 124% more for participants who received a notice without jargon than those who received notices with jargon, and this difference was statistically significant. The results suggest that clarity of the notice plays a role in encouraging property owners to provide feedback to county officials. Like our findings for Hypothesis 2, it was unclear whether the greater likelihood of giving feedback resulted from the absence of jargon or from the greater magnitude of the tax increase in notices without jargon. We also teased out the answer to this question in Study 2.

Study 2

The purpose of the follow-up study was to address the confounding variable in our initial study — the conditions containing the high-clarity (without jargon) tax rate notices also showed a greater tax increase. Hence, the design of Study 1 did not allow us to isolate the influence of clarity from the influence of the size of the tax increase on the dependent variables of interest, i.e., comprehension of tax rate notice and likelihood of giving feedback. In Study 2, the conditions were redesigned so that the effect of clarity on comprehension and feedback could be determined separately from the effect of the size of the tax increase on comprehension and feedback.

Procedure

For the follow-up study we contracted with Qualtrics for data collection. We provided the required distribution of demographic characteristics for the sample to Qualtrics such that the demographic distribution of Study 2 would be similar to the distribution in Study 1. This ensured similarity among sample characteristics between the two studies. In order to exclude participants in our previous study from the follow-up study, we used the following screening question: “Have you taken a survey related to property tax for the McNair Center for Entrepreneurship and Economic Growth with the Baker Institute?” Any person who responded “yes” to this survey item was required to exit the survey.

Participation in the survey was entirely voluntary, and participants were compensated for survey completion by the Qualtrics research services team. Data was collected in a confidential manner, and the research team sought approval from Rice University’s Institutional Review Board (IRB) before beginning data collection.

As the variable “explicit language in tax rate notice” did not have an impact on comprehension or likelihood of giving feedback in Study 1, we omitted this variable from Study 2. The two variables manipulated in Study 2 were (i) the magnitude of the tax increase presented in the notice and (ii) clarity, meaning the presence or absence of jargon. The study utilized the following four conditions: high tax increase/high clarity; high tax increase/low clarity; low tax increase/high clarity; low tax increase/low clarity. Each participant was randomly assigned to one of the four conditions. Similar to the previous study, in each condition, participants read a hypothetical tax rate notice that presented both a higher tax rate and a higher tax levy compared to the prior year.

Like Study 1, the hypothetical tax rate notice in each condition followed the form of the new Texas law, except for the variables that were manipulated, and each of the four conditions presented a tax increase. The tax rates and tax amounts differed from those in Study 1 in order to test the size of the tax increase as an independent variable. The four conditions used in the study are shown in Appendix B: Study 2 Conditions. Conditions 1 and 2 adhered to the form of tax rate notice required by the Texas law.[4] The other two conditions were variations on this form that manipulated the independent variables.

Sample

Power analysis using the estimates from Study 1 yielded a required sample size of 240 participants for Study 2 to replicate the findings from Study 1. The final analyses in Study 2 were conducted on 240 participants. The selection criteria required participants to be Texas residents and to own a home and/or a business in Texas. Additionally, participants had to have paid property tax in Texas within the last three years.

A majority of the sample was comprised of homeowners (52.92%). The sample was almost evenly split in terms of gender with female participation slightly higher (50.8%). The average participant age was 52.7 years, and participant ages ranged from 22 to 85 years. The ethnic composition of the sample was as follows: White (72.08%), Hispanic (10%), Black (7.50%), Asian (6.67%), American Indian or Alaska Native (0.83%). Only 2.92% of the sample did not respond to the question. A majority of the participants identified themselves as being extremely proficient in reading the English language. The educational attainment of the sample was as follows: bachelor’s degree (35%), master’s degree (≈22%), high school diploma (21%), associate’s degree (≈11%), professional degree (e.g., JD) (≈6%), doctoral degrees (≈3%), less than high school diploma (≈1%).

Independent Variables

Size of tax increase displayed on the tax rate notice. The purpose of this variable was to determine whether the size of the tax increase influenced a participant’s understanding of the notice or the likelihood of providing feedback. The low tax-increase conditions showed a tax increase of $48.09, and the high tax-increase conditions showed a tax increase of $318.06.

Clarity. This variable was manipulated and used in the same way as in Study 1.

Dependent Variables

Comprehension of the tax rate notice. This variable was operationalized and scored in the same manner as in Study 1.

Feedback. This variable was operationalized and scored in the same manner as in Study 1.

Exploratory research question to test the presence of a confound in Study 1: Will the size of the tax increase influence participants’ comprehension of the tax rate notice or the likelihood of providing feedback to the taxing authority?

Results

To test whether clarity of the tax rate notice or size of the tax increase was associated with notice comprehension, we carried out a 2x2 ANOVA model with clarity, tax increase and the interaction between these variables as the independent variables. To isolate the influence of each factor on the decision to give feedback, we carried out a binary logistic regression with clarity and the amount of tax increase as the independent variables and the likelihood of giving feedback as the dependent variable.

Hypothesis 2 predicted that tax rate notices with higher clarity would enhance participants’ comprehension of the notice. This hypothesis was supported. The ANOVA model revealed that participants who received a tax rate notice without jargon (M = 4.38) were more likely to agree that the notice made it easy for them to identify a change in tax amount due to the county compared to the participants who received a tax rate notice with jargon (M = 4.08) (F (3,236) = 9.60, p =.002). A subsequent between-subjects 2x2 ANOVA model was conducted to examine if participants who received the tax rate notice with no jargon were able to demonstrate a higher level of notice comprehension than those who received a tax rate notice with jargon. Results revealed that indeed clarity does matter. On average, participants who received the notice with no jargon answered more questions (88%) correctly by identifying a tax increase than those who received a notice with jargon (answered ≈81% questions correctly) (F (3,236) = 5.63, p =.018). The results so far are consistent with our findings from the previous research.

To determine the impact of the size of tax increase on the comprehension of the tax rate notice, the amount of the tax increase was included as one of the three variables in the 2x2 ANOVA described above. The results of this analysis showed that in terms of ease of identifying a change in the amount of tax due to the county, participants who received a tax rate notice that showed a high tax increase (M=4.18) did not differ from the participants who received a tax rate notice that showed a lower tax increase (M = 4.28) (F (3,236) = 0.72, p = .39). Similarly, participants who received the tax rate notice with a high tax increase answered a similar proportion of questions (84%) correctly as those who received a tax rate notice with a lower tax increase (F (3,236) = 0.01, p = .91). These results suggest that the size of tax increase did not confound the results on Hypothesis 2 in Study 1.

Hypothesis 3(b) predicted that clarity of a tax rate notice would be positively associated with the likelihood of giving feedback to the county. The results of Study 1 supported this hypothesis, but we were unable to determine whether the higher tax increase or the clarity of the tax rate notice prompted participants to provide feedback. The results of a binary logistic regression in Study 2 revealed that the odds of giving feedback about the notice was two times greater among participants who received a notice with a higher tax increase than participants who received a notice with a lower tax increase, OR = 2.3, p = .002. The odds of giving feedback were 130% higher for participants who received the notice with a higher tax increase than those who received notices with a lower tax increase. This difference was statistically significant. Participants who received high-clarity (without jargon) notices had greater odds of giving feedback than those who received low-clarity (with jargon) notices, but the difference was not statistically significant, OR = 1.25, p = .393. The odds of giving feedback were 25.4% higher for participants who received high-clarity notices than for participants who received low-clarity notices, but this difference was not statistically significant. Therefore, the clarity of notices did not make a difference in giving feedback, and Hypothesis 3(b) was not supported. Nonetheless, the results trended in the direction of the hypothesis. Among participants who did provide feedback about the notice (n = 113), 53% received a notice with high clarity (without jargon) and approximately 46% received a notice with low clarity (with jargon).

Opinion and Preference Survey

Both Study 1 and Study 2 included survey items intended to gauge the general perceptions of participants about tax rate notices and the property tax burden. In each study, the hypothetical tax rate notice was followed by a series of survey questions. These items were not formulated in relation to a priori hypotheses and were exploratory in nature. One set of questions gauged participants’ perception of the clarity and helpfulness of the tax rate notice they were presented, such as “The notice helps me understand how much property tax I would have to pay.” A second set of questions sought to learn what information participants want in a tax rate notice, such as “It is important to me for the notice to show the dollar amount of property tax I would have to pay this year.” A third set of questions asked for the participants’ views on the property tax burden, such as “I am willing to pay more property tax if my county government provides more to county residents in exchange.” The response options for all questions in this section ranged from 1 = Strongly disagree to 5 = Strongly agree.

The results of the survey for Study 1 and Study 2 participants are summarized in Figures 1-3. Results did not vary according to the type of property owned by the participants; responses of homeowners and business owners were not remarkably different.

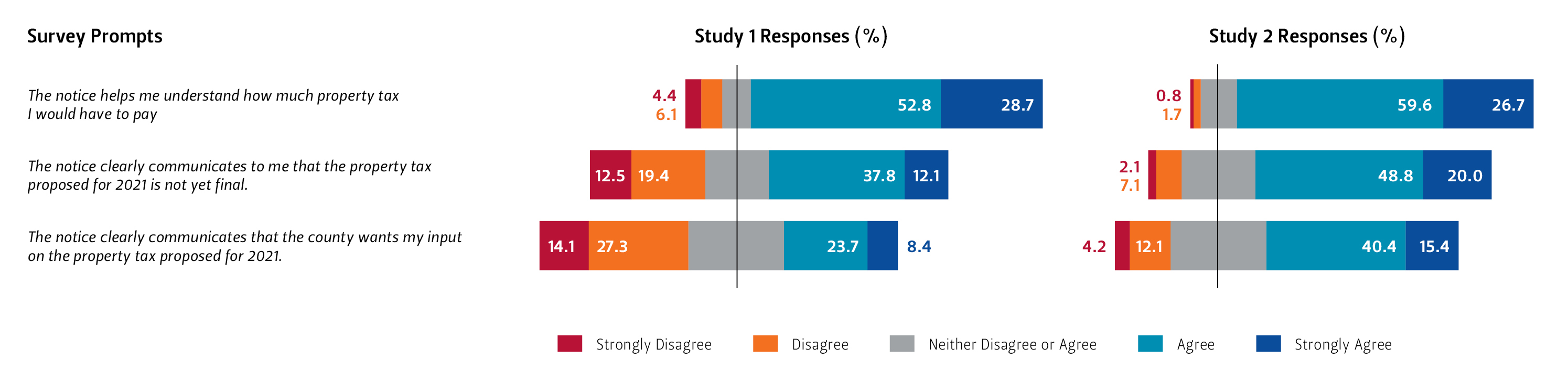

Figure 1 — Perception of Transparency

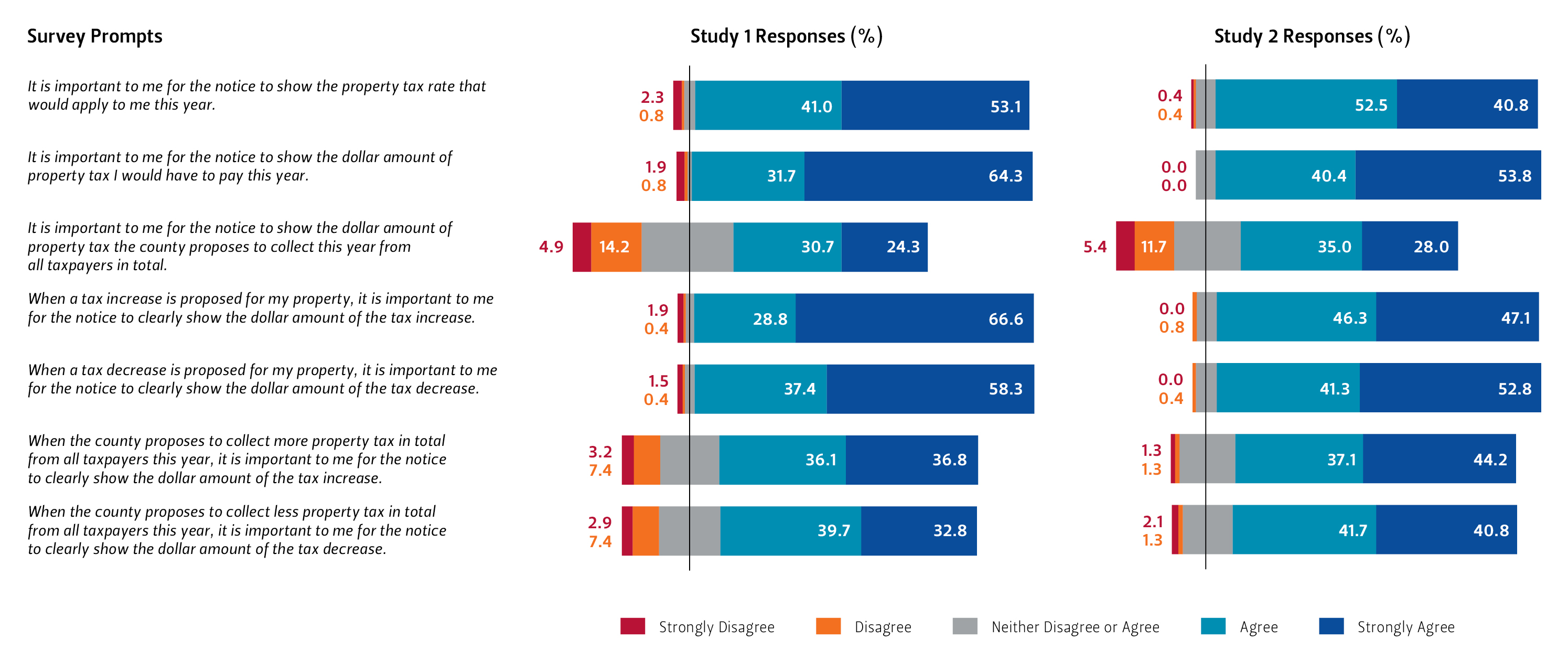

Figure 2 — Preference for Tax Information

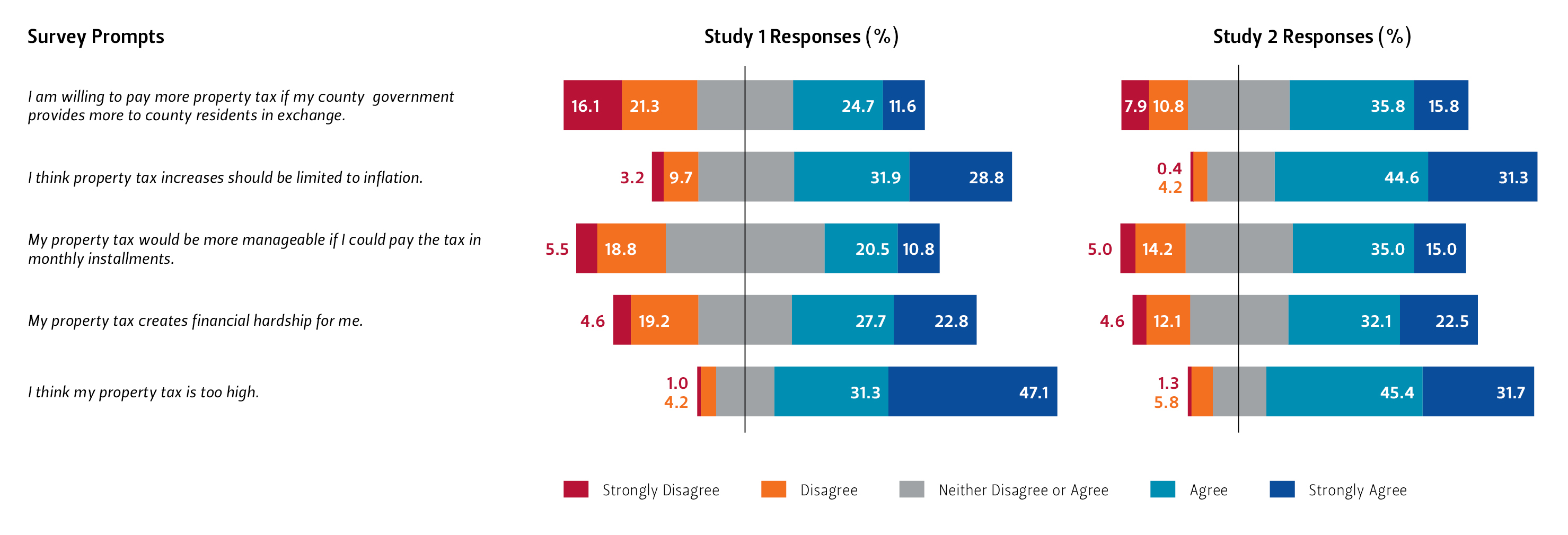

Figure 3 — View on Tax Burden

Discussion

The objective of our research was to find ways to enhance the efficacy of truth-in-taxation in Texas. The design of our study was informed by other research that suggests delivering a simplified, more salient tax rate notice to taxpayers will increase civic participation. We investigated what kind of information in the new digital tax rate notice enhances understanding of the notice and prompts taxpayers to give feedback to tax officials on a digital platform.

Our research revealed that a tax rate notice without jargon — i.e., comparing this year’s proposed tax to last year’s tax — performed slightly better than the form of notice required by the Texas law. The Texas law requires the tax rate notice for a county to contain the following elements:

- No-new-revenue tax rate;

- Taxes that would be imposed at the no-new-revenue tax rate;

- Voter-approval tax rate;

- Proposed tax rate;

- Taxes that would be imposed at the proposed tax rate; and

- The difference between the taxes that would be imposed at the no-new-revenue tax rate and the taxes that would be imposed at the proposed tax rate.

Participants in our research (both Study 1 and Study 2) demonstrated better understanding of the tax rate notice when it contained the following information:

- Last year’s tax rate;

- Taxes imposed last year;

- Proposed tax rate;

- Taxes that would be imposed at the proposed tax rate; and

- The difference between the taxes that would be imposed at the proposed tax rate and the taxes imposed last year.

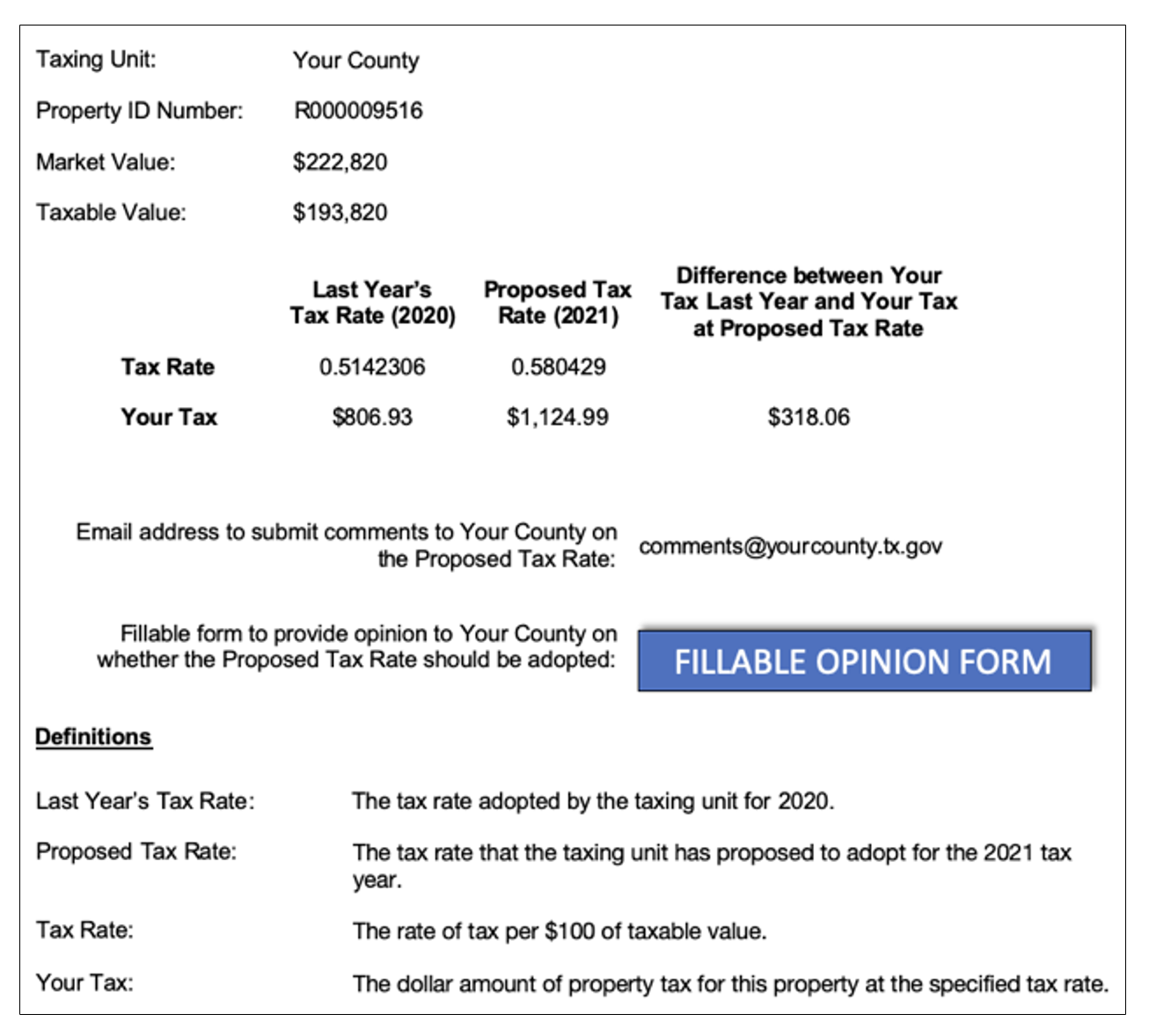

In other words, research participants better understood the tax rate notice when we substituted last year’s tax rate for the no-new-revenue tax rate and omitted the voter-approval tax rate, as shown in Figure 4.

Figure 4

Also, more participants thought the notice comparing this year’s tax to last year’s tax (like the notice pictured above) made it easy to identify a tax increase, compared to the notice required by the Texas law. The results were not affected by the size of the tax increase. In other words, an easy-to-understand and salient notice performs better than a jargon-filled notice regardless of the size of tax increase presented in the notice.

These results are consistent with cognitive load theory and research on salience. Comparing an individual property owner’s tax for this year to last year is both easier to understand and more relevant to the individual. The no-new-revenue tax rate and the voter-approval tax rate are extremely complex legal constructs that serve as, respectively, a benchmark and a limit at the level of the county or other taxing unit, not the individual level. The no-new-revenue tax rate and the voter-approval tax rate are not real tax rates that anyone, anywhere is required to pay.[5] Property owners have to assert more mental effort to understand the constructed tax rates and what the rates mean for them.

In our efforts to determine what prompts property owners to give feedback to taxing authorities, we found that the form of the notice did not matter in and of itself, but that the amount of the tax increase presented in the notice mattered a great deal. Participants who were shown a $318.06 tax increase were more than twice as likely to give feedback compared to those who were shown a $48.09 tax increase. One way to look at these results is straight-forward and, probably, intuitive: Taxpayers are more likely to give feedback to taxing authorities when expected to pay a larger amount of money compared to a smaller amount. Another implication of these results is also present but less obvious. Although the form of notice does not affect feedback in and of itself, the form of the notice presented does determine the amount of tax increase that will be presented,[6] and the amount of the tax increase does affect feedback.

Our survey of participants’ perceptions about the tax rate notice and the property tax burden suggests areas for further research and possible improvements to the tax rate notice.

- Perception of Transparency. While the vast majority of participants agreed or strongly agreed that the tax rate notice helped them understand how much property tax they would have to pay (81.5% in Study 1; 86.3% in Study 2), fewer participants agreed or strongly agreed that the notice clearly communicated that the proposed tax was not yet final (49.9% in Study 1; 68.8% in Study 2) and that the county wanted their input (32.1% in Study 1; 55.9% in Study 2).

- Preference for Tax Information. With respect to the content of the tax rate notice, the vast majority of participants agreed or strongly agreed that the following elements of the notice that related to their individual property were important to them: the proposed tax rate (94.1% in Study 1; 93.3% in Study 2), the dollar amount of tax at the proposed tax rate (96.0% in Study 1; 94.2% in Study 2), the dollar amount of their tax increase (95.4% in Study 1; 93.3% in Study 2),and the dollar amount of their tax decrease (95.6% in Study 1; 94.1% in Study 2). A smaller majority agreed or strongly agreed that information for the county as a whole was important to them: the total dollar amount of tax to be collected from all taxpayers in the county (55% in Study 1; 63% in Study 2), the total dollar amount of an increase in that number (72.9% in Study 1; 81.3% in Study 2), and the total dollar amount of a decrease in that number (72.5% in Study 1; 82.5% in Study 2).

- View on Tax Burden. In response to questions about the property tax burden, the largest majority of participants agreed or strongly agreed that their property tax is too high (78.4% in Study 1; 77.1% in Study 2) and that increases should be limited to inflation (60.7% in Study 1; 75.8% in Study 2). Only a minority or small majority of participants agreed or strongly agreed that property tax created a financial hardship (50.5% in Study 1; 54.6% in Study 2), monthly installments would make property tax more manageable (31.3% in Study 1; 50.0% in Study 2), and they were willing to pay more property tax if the county provided more services (36.2% in Study 1; 51.7% in Study 2).

Recommendations

Our studies found that property owners better understand a notice that provides tax information about their own property rather than information about the county as a whole. Our survey also revealed that property owners want tax information about their own property more than they want tax information about the county as a whole. The form of the truth-in-taxation notice in Texas should be revised to give property owners the information they want and can best use. Specifically, Section 26.17(b)(1)-(11) of the Texas Tax Code should be amended to require the digital tax rate notice to include the following information for a property:

- Last year’s tax rate;

- Taxes imposed last year;

- Proposed tax rate;

- Taxes that would be imposed at the proposed tax rate; and

- The difference between the taxes that would be imposed at the proposed tax rate and the taxes imposed last year.

Our studies also found that property owners are more likely to provide feedback to taxing authorities when presented with a larger tax increase compared to a smaller tax increase. Throughout our research, it became apparent how the choice of information presented in the notice drives the amount of the tax increase that will be shown in the notice. (See endnote 7.) The format of notice that we recommend, which would compare the dollar amount of tax paid last year to the dollar amount of tax proposed for this year, would provide property owners with the most accurate and truthful statement possible of the amount of a tax increase (or decrease) proposed for their property. The suggested format would ensure transparency between the taxing unit and property owners.[7] In turn, since the scale of tax increase motivates feedback, the recommended form of notice would help to “right-size” the amount of feedback from property owners to taxing authorities, neither driving too much nor too little feedback.

Although property owners have greater interest in tax information related to their own properties, our survey revealed that a large majority of property owners are interested in tax information for the taxing unit as a whole, such as increases and decreases in total tax collections from all taxpayers. A large majority are also interested in a limitation on tax increases.[8] Identifying the clearest and most salient mechanism(s) to satisfy the preferences of taxpayers for tax information and tax limitations for a taxing unit as a whole is beyond the scope of this paper, but the question merits further research.

Since truth-in-taxation measures are intended to serve the taxpayers, not the government, it is incumbent upon the government to make tax rate notices clear, relevant, and, above all, truthful for taxpayers. Our recommendations, based on our research, would serve that objective.

References

Bland, Robert L. and Phanit Laosirirat. 1997. “Tax limitations to reduce municipal property taxes: Truth in taxation in Texas.” Journal of Urban Affairs 19, no. 1 (1997): 45-58. https://doi.org/10.1111/j.1467-9906.1997.tb00396.x.

Cornia, Gary C. and Lawrence C. Walters. 2006. “Full disclosure: Controlling property tax increases during periods of increasing housing values.” National Tax Journal 59 (2006): 735-749. https://www.journals.uchicago.edu/doi/10.17310/ntj.2006.3.22.

Eom, Tae Ho and Ross Rubenstein. 2006. “Do state-funded property tax exemptions increase local government inefficiency? An analysis of New York state's STAR program.” Public Budgeting and Finance 26, no. 1 (2006): 66-87. https://doi.org/10.1111/j.1540-5850.2006.00839.x.

Fischel, William A. 2001. “Homevoters, municipal corporate governance, and the benefit view of the property tax.” National Tax Journal 54, no. 1 (2001): 157-174. https://www.journals.uchicago.edu/doi/abs/10.17310/ntj.2001.1.08?journalCode=ntj.

Goodman, Christopher B. 2018. “House prices and property tax revenues during the boom and bust: Evidence from small‐area estimates.” Growth and Change 49 (2018): 636-656. https://doi.org/10.1111/grow.12261.

Lyman, Rick. 2006. “As property values rise, homeowners feel pinch.” New York Times, February 19, 2006. https://www.nytimes.com/2006/02/19/realestate/as-property-values-rise-homeowners-feel-pinch.html.

Mansbridge, Jane. 2009. “A ‘selection model’ of political representation.” Journal of Political Philosophy 17, no. 4 (2009): 369-398. https://doi.org/10.1111/j.1467-9760.2009.00337.x.

O'Neill, Onora. 2002. A Question of Trust: The BBC Reith Lectures 2002. Cambridge: Cambridge University Press.

Paas, Fred, Alexander Renkl, and John Sweller. 2003. “Cognitive load theory and instructional design: recent developments.” Educational Psychologist 38, no. 1 (2003): 1-4. https://doi.org/10.1207/S15326985EP3801_1.

Rabb, Jennifer. 2019. Increasing property tax accountability in the digital age. Rice University’s Baker Institute for Public Policy, Houston, Texas (2019): 1-10. https://www.bakerinstitute.org/sites/default/files/2019-10/import/mcnair-pub-propertytax-030819.pdf.

Ramsey, Ross. 2019. “Analysis: Property tax relief in Texas, perhaps — but not right away.” The Texas Tribune, September 27, 2019. https://www.texastribune.org/2019/09/27/property-tax-relief-texas-perhaps-not-right-away/

Shadbegian, Ronald J. 1999. “The effects of tax and expenditure limitations on the revenue structure of local government.” National Tax Journal 52, no. 2 (1999): 221-37. https://www.journals.uchicago.edu/doi/abs/10.1086/NTJ41789391?journalCode=ntj.

Texas Tax Code §26.06.

Texas Property Tax Reform and Transparency Act of 2019, S.B.2, eff. January 1, 2020. https://capitol.texas.gov/tlodocs/86R/billtext/html/SB00002F.HTM.

Thomsen, Mette K. and Morten Jakobsen, M. 2015. “Influencing citizen coproduction by sending encouragement and advice: A field experiment.” International Public Management Journal 18, no. 2 (2015): 286-303. https://doi.org/10.1080/10967494.2014.996628.

van Eijk, C. and T. P. S. Steen. 2014. “Why People Co-Produce: Analysing citizens’ perceptions on co-planning engagement in health care services.” Public Management Review 16, no. 3 (2014): 358-382. https://doi.org/10.1080/14719037.2013.841458.

Wallot, Sebastian, Beth O'Brien, Anna Haussmann, Heidi Kloos, and Marlene Lyby. 2014. “The role of reading time complexity and reading speed in text comprehension.” Journal of Experimental Psychology: Learning, Memory, And Cognition 40, no. 6 (2014): 1745-1765. https://doi.org/10.1037/xlm0000030.

Endnotes

[1] For example, Hidalgo County is the most populous county for both SD 20 and SD 27. Following the methodology, we selected Hidalgo for SD 20, and for SD 27, we selected its second-most populated county, Cameron. We departed from the methodology for five SDs in very populous counties where the SD covers only part of a single county. Specifically, we had no alternative but to select Harris County for SD 6, SD 7 and SD 15, as there were no other counties in those districts. For the same reason, we had to select Dallas County for SD 16 and SD 23, even though the methodology also yielded Dallas County for SD 9. We also departed from the methodology for SD 1 and selected its second-most populous county, Gregg, after we could not obtain a response from the appraisal district of its most populous county, Smith.

[2] We did, however, shift the tax information of Van Zandt County and the sample property forward by one year in our study. Specifically, the 2019 and 2020 information from Van Zandt County and the sample property was represented as 2020 and 2021 information in our study.

[3] See Tex. Tax Code §26.17(a)(5)(F).

[4] See Tex. Tax Code §26.17(a)(5)(F).

[5] See Tex. Tax Code § 26.04(c); Texas Comptroller of Public Accounts, Tax Rate Calculation, last visited December 8, 2022, https://comptroller.texas.gov/taxes/property-tax/truth-in-taxation/calculations.php.

[6] The conditions in Study 1 that adhered to the format required by the Texas law showed the difference between tax at the proposed tax rate and tax at the no-new-revenue tax rate, a difference of $48.09. (See Conditions 1 and 2 in Appendix A.) The other two conditions in Study 1, which were experimental, showed the difference between tax at the proposed tax rate and tax actually paid last year, a difference of $318.06. (See Conditions 3 and 4 in Appendix A.) The higher dollar figure was the actual tax increase experienced by the property owner whose tax information was utilized in our study, and the lower dollar figure was the tax increase required to be presented in the notice by the Texas law. In other words, the actual tax rate notice for the property utilized in our study, following the form of the Texas law, understated the proposed tax increase for the property by 82%. Further research is needed to determine how frequently the format of notice under the Texas law understates the amount of the tax increase that a property owner would experience at the proposed tax rate.

[7] In contrast, the tax rate notice required by the current Texas law will often misrepresent the amount of a tax increase. The notice required by current law represents the amount of a tax increase as (i) the amount of tax proposed for this year minus (ii) the amount of tax that would be due at the no-new-revenue tax rate, if it were a real tax rate. See Tex. Tax Code § 27.17(b)(11). If the tax at the no-new-revenue tax rate is greater than last year’s tax, the notice will understate the dollar amount of the tax increase proposed for the property. Conversely, if the tax at the no-new-revenue tax rate is less than last year’s tax, the notice will overstate the dollar amount of the tax increase proposed for the property. Further research is needed to determine how prevalent each of these scenarios is in Texas.

[8] A large majority of participants (60.7% in Study 1; 75.8% in Study 2) agreed or strongly agreed with the statement, “I think property tax increases should be limited to inflation.” However, inflation was the only type of limitation presented in the survey, and we do not know how participants would rate an inflation-based limit if they were also presented with other possible mechanisms for limiting tax increases.

Appendix A: Study 1 Conditions

Figure 1A — Condition 1

Figure 2A — Condition 2

Figure 3A — Condition 3

Figure 4A — Condition 4

Appendix B: Study 2 Conditions

Figure 1B — Condition 1

Figure 2B — Condition 2

Figure 3B — Condition 3

Figure 4B — Condition 4

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.