Author(s)

Overview

The Gulf Cooperation Council (GCC) countries — Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) — have changed significantly in the 15 years since a regional nuclear energy program was first considered. Their developmental needs, as well as their infrastructure and governance capabilities, have grown considerably. Additionally, their environmental pledges to achieve net-zero carbon emissions require reliable clean energy systems to maintain their nations’ socioeconomic well-being. This brief calls on the GCC states to reassess the viability of establishing a joint regional nuclear power plant to align with their sustainable development goals as well as to advance the region’s long-term prosperity.

Background

Conducting Joint Studies on Nuclear Energy Programs

In 2006, at the 27th session of the GCC Supreme Council, the GCC countries decided to conduct a joint study on utilizing nuclear technology for peaceful applications including electricity generation and water desalination. GCC member states agreed that the International Atomic Energy Agency (IAEA) should carry out a preliminary feasibility study on nuclear energy applications for these purposes, followed by a detailed study and implementation program.

The next year, the IAEA completed the feasibility study, which demonstrated the cost-effectiveness of nuclear applications for power generation and water desalination to meet GCC member states’ increasing energy demand. The study also emphasized the need to strengthen and develop related infrastructure and institutional frameworks. Additionally, it recommended that the GCC countries conduct further detailed studies.

In 2010, the GCC countries commissioned a consultant company to identify and assess potential collaboration programs among their states in nuclear energy areas. The study’s main objectives were:

- Identify and evaluate potential collaboration areas within civil nuclear energy.

- Examine the feasibility of developing a joint regional nuclear power plant.

The study’s findings on the second objective indicated that a joint power plant was both technically and commercially feasible, due to the availability of potential sites across the GCC region and international precedent for similar collaborative projects.

However, it noted several critical prerequisites for establishing a joint nuclear plant, including:

- Upgrading the electrical grid.

- Developing commercial infrastructure for electricity trade and establishing agreements on electricity pricing and/or ownership structure.

- Securing a commitment from a member state to host the joint regional nuclear power plant.

- Ensuring the willingness of participating member states to rely on the host state for power supply.

Abandoning the Joint Regional Nuclear Plant Initiative

Despite these studies on joint nuclear energy programs, each GCC state was pursuing its own independent nuclear program by late 2010. The lack of coordination and delays in the GCC’s unified nuclear initiative prompted individual states to advance their nuclear energy goals separately, as a region-wide approach did not seem viable at the time.

The GCC states’ individual efforts resulted in the following:

- UAE demonstrated the strongest commitment to its nuclear goal, selecting a Korean-led consortium to build four APR-1400 reactors.

- Saudi Arabia announced a 20-year plan to build 16 nuclear reactors.

- Kuwait contemplated building up to six reactors, with the first two expected by 2021–22.

- Qatar, despite its gas reserves, also explored nuclear power options, aiming to add 5,400 megawatt (MW) by 2036, and signed agreements with Russia, EDF Energy, and Areva.

As of December 2024, the UAE has four operational reactors with a total capacity of 5,348 MW and is proposing to build two additional reactors with a total capacity of 2,800 MW. Saudi Arabia is planning for two reactors with a total capacity of 2,900 MW. The remaining GCC countries are still considering nuclear energy capabilities. Though Kuwait canceled its nuclear program in 2011 and is not officially pursuing a nuclear power application program, it is exploring the feasibility of new advanced nuclear technologies — particularly the use of small modular reactors (SMRs).[1] Bahrain recently expressed its interest in SMRs if they become financially viable and commercially available. Qatar announced that it is currently investing in a project to develop SMRs with Rolls-Royce SMR Ltd; however, there are no immediate plans to build local capacity. Oman’s situation is similar, as no plans for local capacity construction have been announced.

Given the advances in the GCC states’ infrastructure, interests, and nuclear power technologies, is a joint nuclear power plant now technically and commercially feasible in the region?

Revisiting the Case for a Joint Regional Nuclear Power Plant: What Has Changed in 15 Years?

The idea of a joint regional nuclear power plant was last considered about 15 years ago. Since then, the region has experienced significant transformations: demographic, socioeconomic, political, and infrastructural. This section highlights the key changes.

Socioeconomic Changes

Recent statistics show (Figure 1) the evolving dynamics in the GCC states:

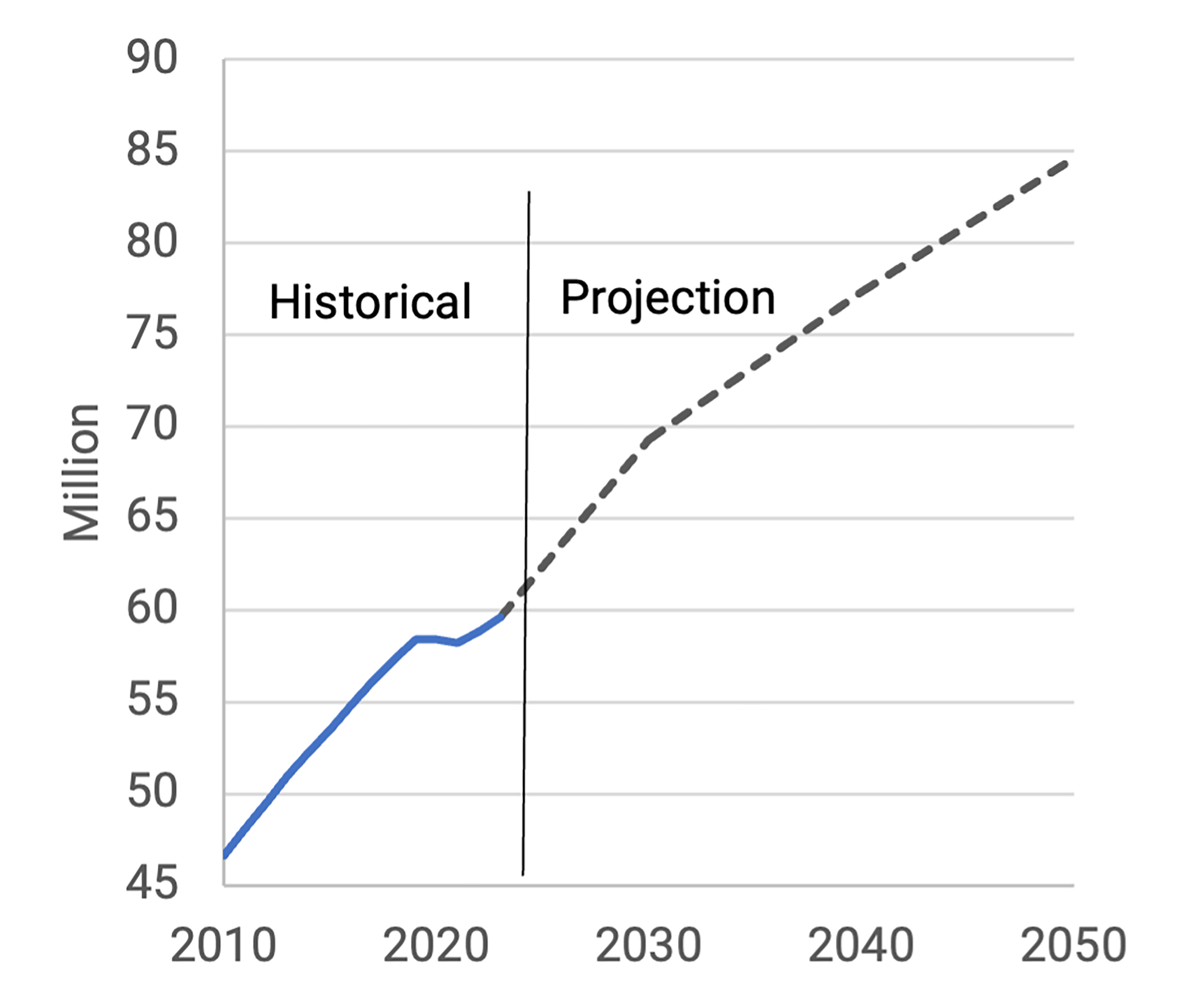

- Population increased from approximately 47 million in 2010 to 60 million in 2023.

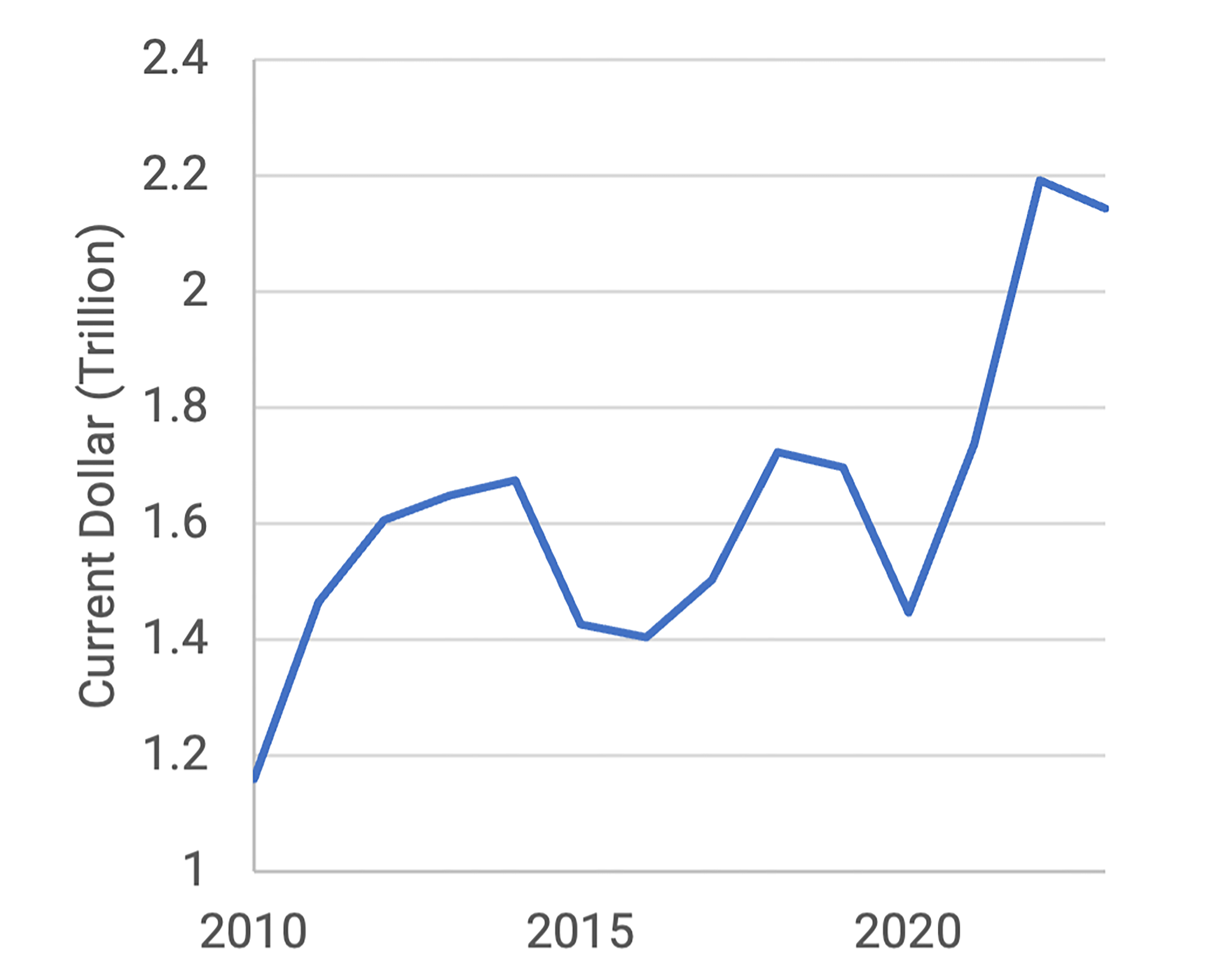

- Combined GDP grew from around $1.16 trillion in 2010 to $2.1 trillion in 2023.

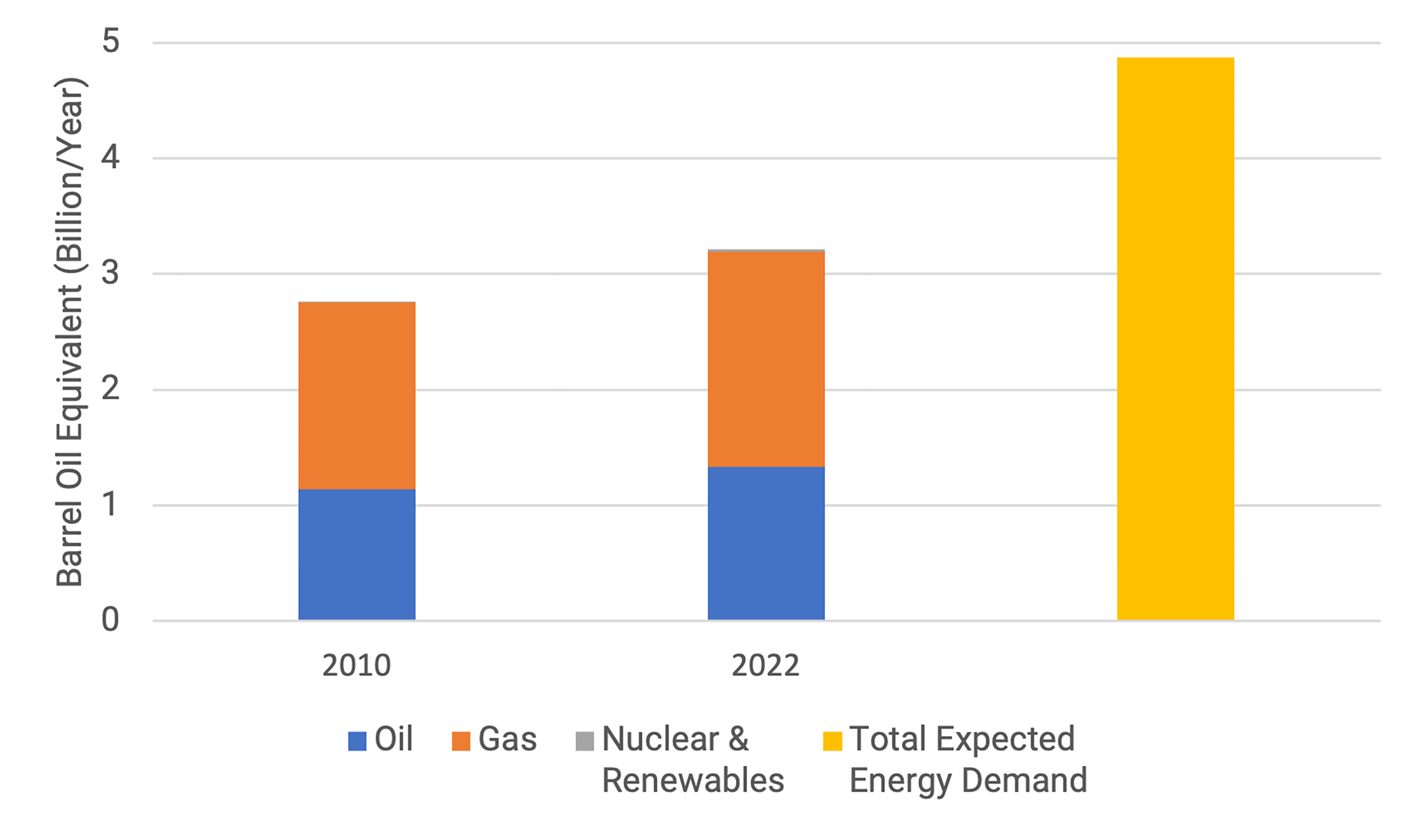

- Energy demand in 2022 was 1.2 times higher than in 2010.

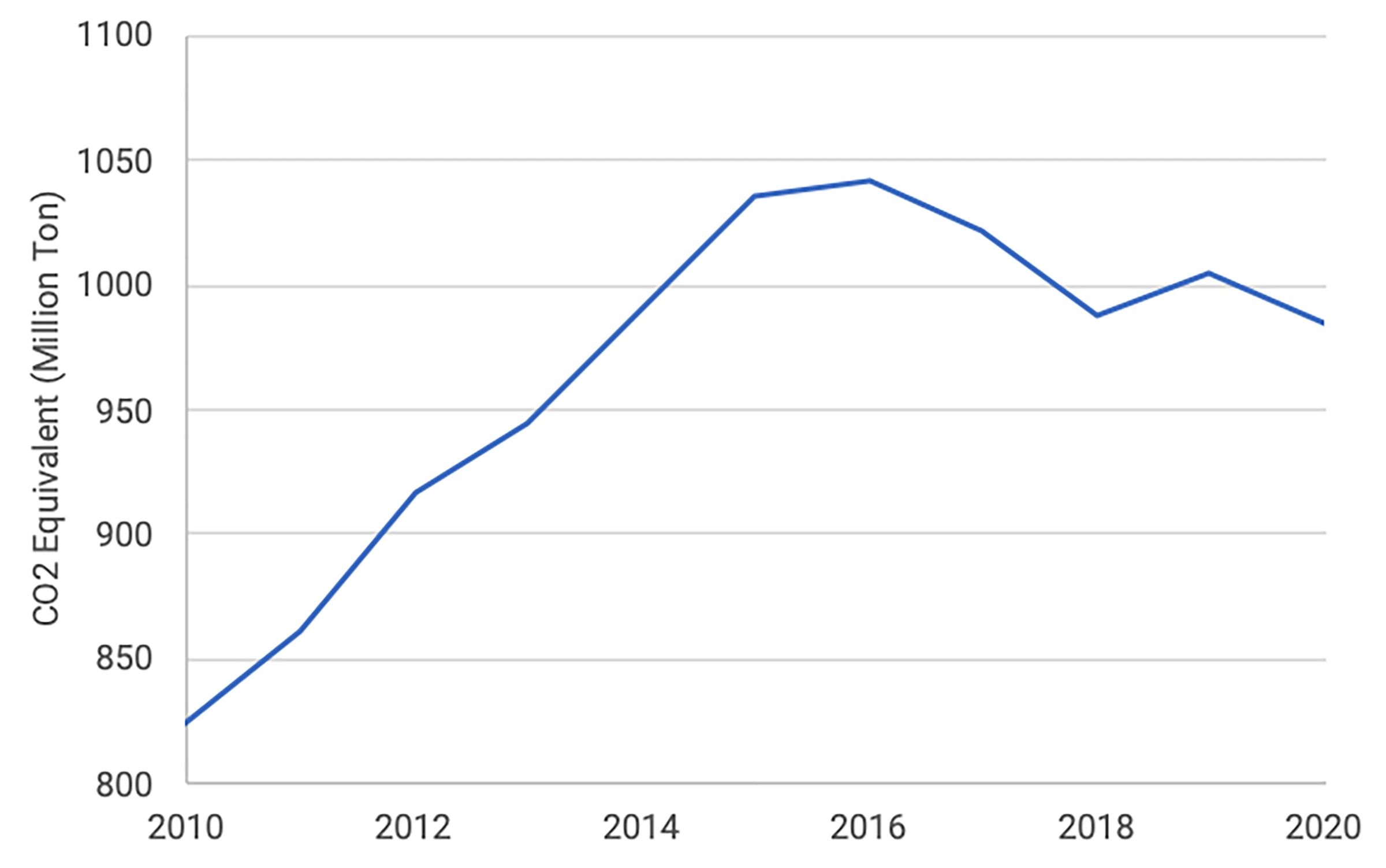

The GCC’s energy mix is still dominated by fossil fuels, with oil and oil products comprising 40% and natural gas 59% of energy consumption in 2022, while renewables, nuclear, and other sources accounted for less than 1% (Figure 1). Due to population and economic growth, the region’s carbon emissions increased from 824 million tons in 2010 to 985 million tons in 2020.

Most of the GCC states have pledged to achieve net-zero carbon emissions by either 2050 or 2060. In 2022, the total energy consumed in the GCC states was 3.2 billion barrels of oil equivalent (BOE), of which more than 99% was oil and gas, and consumption is expected to reach 4.8 billion BOE by 2050 (Figure 1). To reach the net-zero goal by then, the GCC states will need to use more clean energy sources and less fossil fuels. Given its intermittent nature and non-dispatchability, renewable energy cannot serve as the primary source to meet current base demand. In addition to clean energy technologies — blue/green hydrogen, energy storage, as well as carbon capture, utilization, and storage (CCUS), etc. — nuclear energy could be a valuable option to provide baseload power as well as load-following capabilities and ensuring stability. It would also reduce carbon emissions when replacing fossil-fired technologies.

Figure 1A — Population

Figure 1B — GDP

Figure 1C — Energy Demand

Figure 1D — Carbon Emissions

Regional Interconnection Power Grid

As mentioned above, the 2011 consultancy study noting the feasibility of a joint regional GCC power plant provided four key conditions — while insufficiently developed or unmet at the time — that were now addressed. One of these conditions is the availability and capacity level of the interconnected power grid in the region.

In 2001, the GCC states established the GCC Interconnection Authority (GCCIA) — a joint stock company comprised of the six GCC nations — with the mission of constructing and operating an interconnected power grid among the GCC states and expanding to other regions. Presently, GCCIA facilitates electricity exchange and trade among the six GCC members: Bahrain, Kuwait, Qatar, Saudi Arabia, Oman, and the UAE. GCCIA has a plan to connect with Egypt and Jordan, and linking with Iraq is underway.

The GCCIA continues enhancing its network’s capacity to accommodate member states’ increasing generation capacity. It conducted a techno-economic study to enhance the capacity and resiliency of its network by adding 400 kilovolt (kV) double-circuit lines for the Alfadhili-Ghunnan line — serving Bahrain, Kuwait, and Saudi Arabia — and the Ghunnan-Salwa line — serving Qatar, Saudi Arabia, and the UAE. The Wafra 400-kV transmission substation currently under construction in southern Kuwait near the Saudi Arabian border will increase the connection capacity with Kuwait to 3,500 MW.

The GCCIA conducted a study assessing its capability to integrate with high-generation capacity renewable energy power plants — more than 5 GW — in the region. The study showed that the GCCIA can safely accommodate 1 GW of renewable energy system fluctuations. In addition, the authority has approved and applied a cybersecurity code of practice for its control and operation procedures.

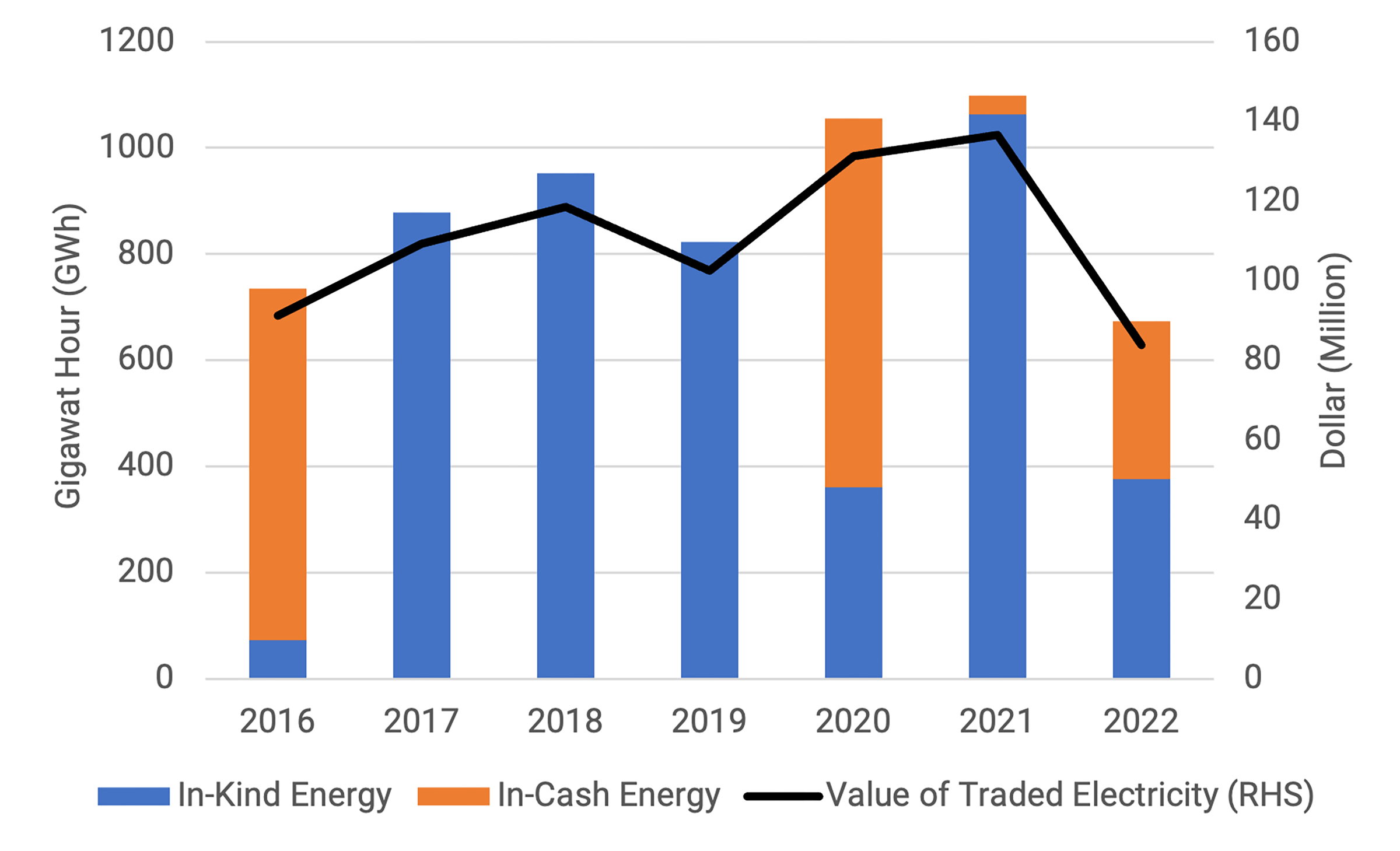

Given its current capacity, the GCCIA network can support increased electric flow between the GCC states, beyond just emergency response needs. The average annual energy flow between 2016 and 2022 was about 890 gigawatt-hours (GWh) with a total 6217 GWh (Figure 2). The network capacity continues to grow with the GCC countries’ increasing generation capacity.

Electricity Trade Framework

The second condition specified in the consultancy study is an electricity trade agreement among the GCC states, which did not exist in 2011. The electricity trade framework has noticeably matured in the GCC region. The total traded electric energy — both in-kind and in-cash — between 2016 and 2022 was 6,217 GWh, amounting to a value of $773.2 million (Figure 2). The number of offers and bids increased from five in 2016 to 45 and 40 in 2021 and 2022, respectively. In 2022, the GCCIA issued two tenders for Kuwait and Iraq’s long- and medium-term power purchase.

The electricity trade market in the GCC region is functional and has proven effective in accommodating transactions between all supply and demand nodes in the region. Importantly, electricity trade transactions have demonstrated a good-faith relationship between the GCC states that can be capitalized on for nuclear power collaborations.

Figure 2 — Flow and Trade of Electric Energy Between the GCC States

Governance Capacity and Competency

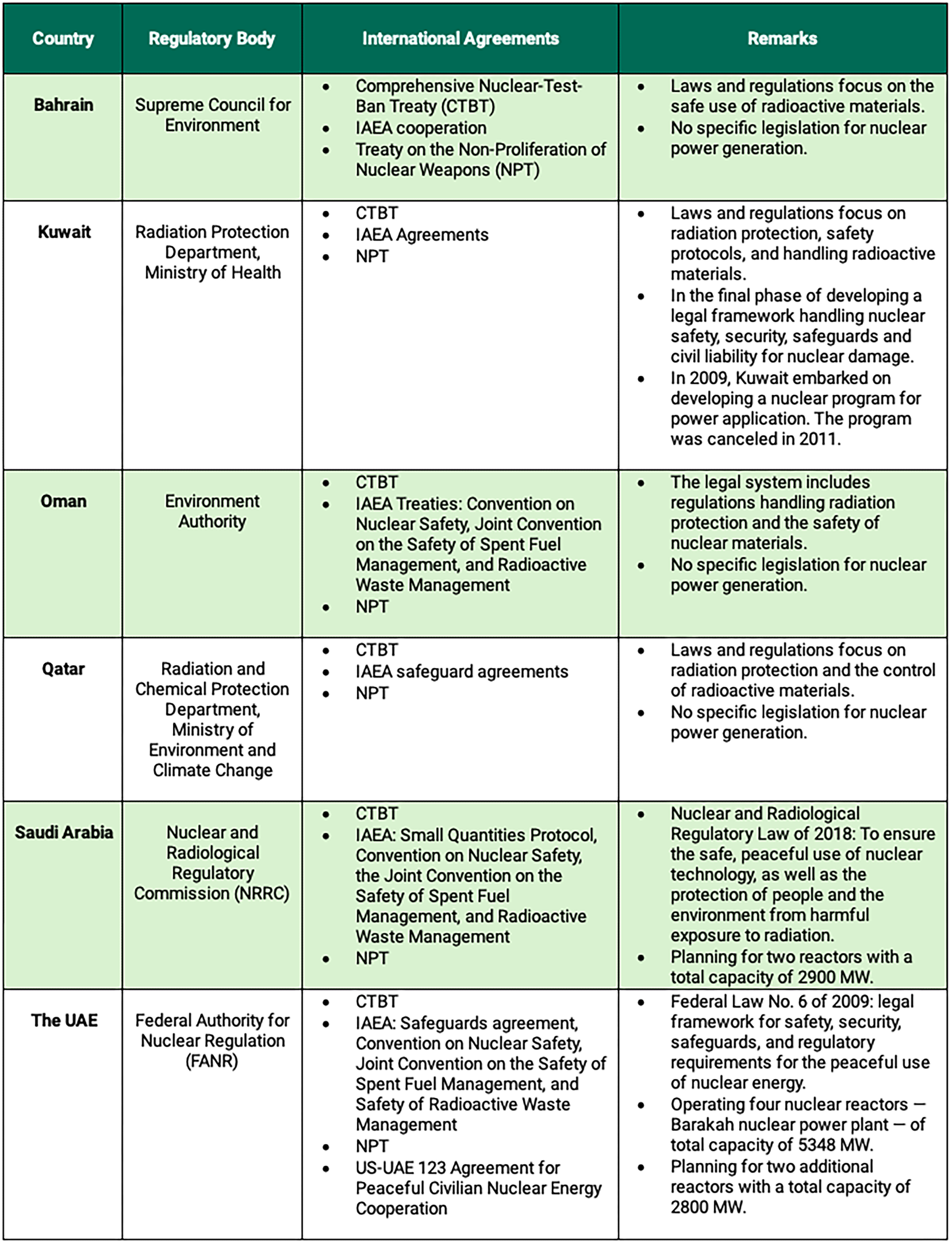

Since 2011, most GCC states made considerable progress in developing their nuclear legal and regulatory systems, with the UAE and Saudi Arabia leading the way.

The UAE — The UAE has the highest nuclear power capacity in the GCC, with over 5,300 MW from operating reactors, and followed the highest safety, security, and nonproliferation standards in developing its nuclear legal framework and regulation. It adopted six pillars including: operational transparency; nonproliferation; safety and security; cooperation with the IAEA and conformance to its standards; establishment of a peaceful domestic nuclear power capability in collaboration with the governments and firms of responsible nations, as well as with the assistance of appropriate expert organizations; and assurance of long-term sustainability of the UAE’s peaceful domestic nuclear power program.

Saudi Arabia — The Saudi Nuclear and Radiological Regulatory Commission (NRRC) was established in 2019 to regulate the peaceful use of nuclear energy and ionizing radiation. The NRRC’s responsibilities include: setting policies and regulations for monitoring activities and facilities; setting regulations for safety, security, and nuclear safeguards; monitoring the import, export, and circulation of nuclear materials; and setting requirements for nuclear and radiological emergency preparedness.

Each GCC state has its own goals and is continuously strengthening its national nuclear legal framework and regulations.

Table 1 summarizes the progress of the GCC states in key nuclear governance.

Table 1 — GCC States’ Nuclear Legal Frameworks and Regulations Profiles

In 2021, Saudi’s NRRC and the UAE’s Federal Authority for Nuclear Regulation (FANR) signed a collaboration agreement on nuclear and radiation regulatory affairs. In 2023, NRRC and Oman’s Environment Authority (EA) signed a memorandum of understanding that aims to develop cooperation in the use of nuclear technologies for peaceful purposes. The existing collaboration between the region’s regulatory authorities can serve as the foundation for regional nuclear programs. Having established their legal and regulatory frameworks, the UAE and Saudi Arabia could lead the development a common governance framework for GCC states.

Technology Advancement Competitiveness

Advanced nuclear power generation technologies are revolutionizing the energy sector by offering safer, more efficient, and environmentally friendly alternatives to traditional nuclear reactors. Among these innovations, SMRs are notable for their ability to provide scalable, flexible power generation. SMRs have compact designs, allowing them to be deployed in remote areas or integrated into existing grids with ease. Their advanced safety features include passive cooling systems that reduce the risk of meltdowns. In addition to SMRs, Generation IV reactors — which operate at higher temperatures, enhancing efficiency and fuel utilization — have the potential to reduce nuclear waste by recycling spent fuel.

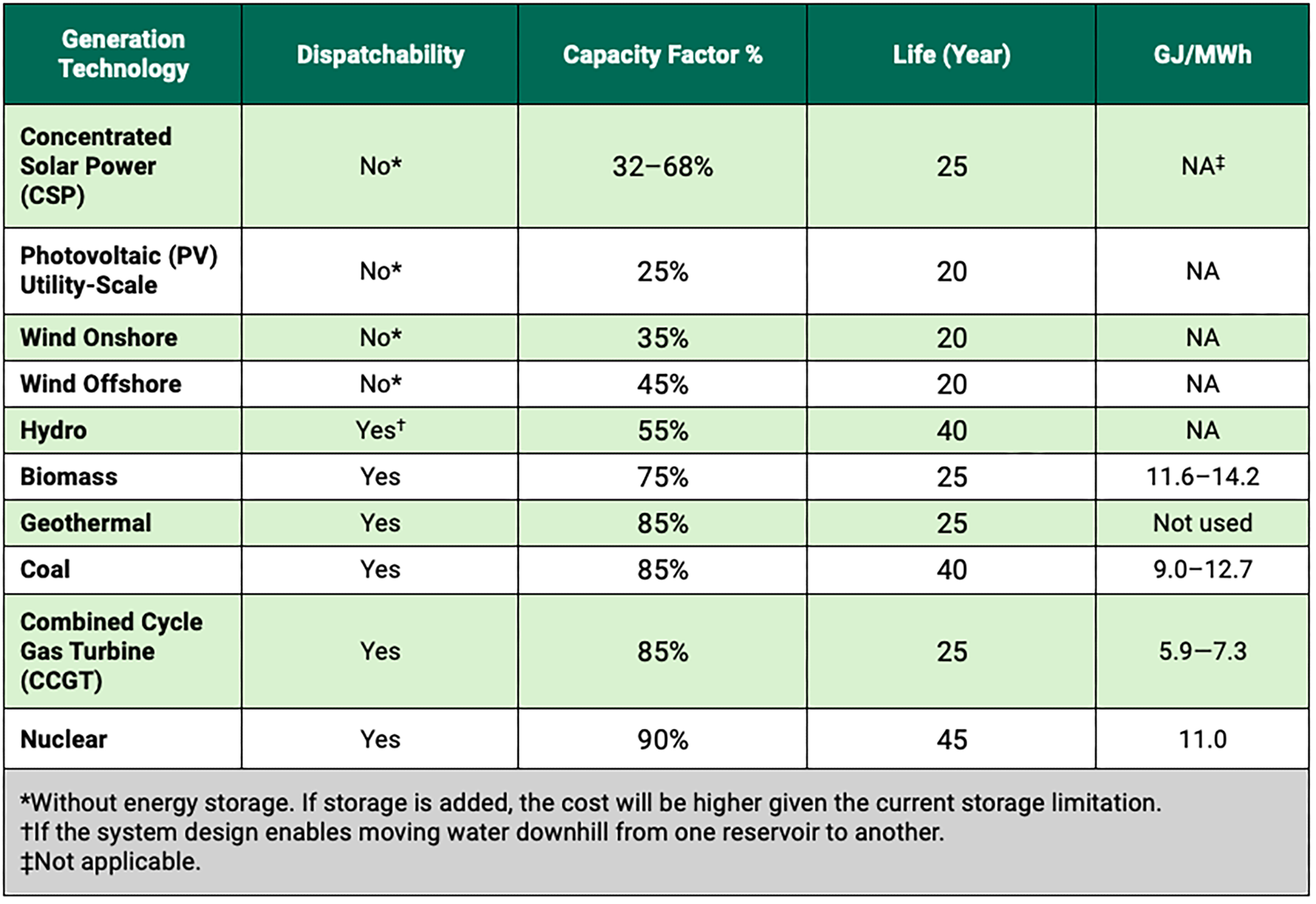

Advanced nuclear energy is increasingly becoming competitive with conventional power generation technologies. SMRs and Generation IV reactors offer cost advantages through modular construction, which reduces upfront capital investment and shortens construction times. Nuclear technology may be even more cost-effective than renewables in term of reliable long-term power generation. It is worth noting that economic evaluations of alternative electric generating technologies should not rely on the levelized cost of electricity (LCOE) — a measure of the lifetime costs of a technology divided by generated electricity. It has been demonstrated that LCOE is inappropriate for comparing intermittent generating technologies — such as solar and wind — with dispatchable generating technologies, such as fossil fuel power and nuclear technologies.

Table 2 lists and compares electricity generation technologies in terms of their dispatchability, availability, lifespan, and heat generation capability, and this last feature is significant for seawater desalination and petrochemical applications. Nuclear technology is distinguished by its available lifespan in addition to its dispatchability and load following when using SMRs.

Table 2 — Main Features of Electricity Generation Technologies

Notes: GJ — Gigajoule; MWh — megawatt-hour.

Expected Benefits of a Joint Regional Nuclear Power Plant

With the GCC region’s considerable progress in the past 15 years — in infrastructure, governance, and experience in managing nuclear facilities — the prospect of a joint regional nuclear power plant is now more realistic. The 2011 consultancy study noted several benefits that remain relevant today:

- For states wanting to use nuclear power to meet their energy demands, a joint nuclear plant would help to assure partners and the international community that a civil nuclear program is being operated in accordance with international obligations and with full transparency.

- Participating GCC states with no nuclear power plants on their territories would not need to develop the extensive national infrastructure typically required to support a nuclear program. The member states hosting nuclear plants could lessen the financial burden by sharing planning and implementation costs with the other GCC nations.

- Those countries with small land areas and limited geographic depth — such as Bahrain, Kuwait, and Qatar — would greatly benefit from such a collaboration, as the larger GCC states are able to build nuclear plants on their territory.

Several successful bilateral and multilateral projects exist where countries cooperate through financing, technology sharing, and energy distribution (Table 3). One example of such cooperation is the cross-border electricity sharing from nuclear power plants in France with other European nations. The UAE and Saudi Arabia could similarly export electricity generated from nuclear plants to neighboring GCC states through the GCCIA network. GCC members could choose to adopt one or more of the models presented in Table 3, perhaps entering into an equity partnership, collaborating to jointly invest in a nuclear power plant.

Table 3 — Examples of Joint Nuclear Power Plants and Organizations

Commercial Model Scenarios

The capital structure and commercial arrangements of commercial nuclear power plants can vary widely. They may be owned by multiple entities with different ownership shares, and these entities may engage in the project through joint ventures, limited recourse subsidiaries, or independently. Additionally, the operator of the plant could be a separate entity, such as a joint venture or a single-purpose company. New nuclear projects may be promoted and financed by governments, large utilities with strong financial backing, special-purpose vehicles, or a combination of these.

Two GCC member states — Saudia Arabia and the UAE — have the governance and infrastructure capabilities necessary to manage safeguards, security, and liability requirements for hosting nuclear facilities. They may be open to hosting additional nuclear power plants, exporting electricity to neighboring states, and sharing the financing responsibilities through various models, including:

- Joint Ventures — Collaboration among governments or national electricity companies, with financing via power purchase agreements (PPAs).

- Project Leadership — One member state leads the project, while others contribute financing or purchase equity stakes.

- Public-Private Partnership — Member states partner with a developer under a build-operate-transfer (BOT) contract.

- Third-Party Operation — Member states entering PPAs with a third party that develops and operates the plant, without taking equity stakes.

- Alternative Models — Other arrangement that best align with the shared interests of member states.

No matter which model is chosen, government involvement — whether directly, or indirectly through national electricity companies — is essential to a project’s commercial viability and risk mitigation.

Challenges Facing a Joint Regional Nuclear Cooperation

The main challenges to establishing a nuclear power program are not technical but stem from geopolitical tensions, sociopolitical factors, and public perceptions. For GCC member states, depending on the commercial model selected, the following issues may arise:

- Reliance on Others for Electricity — Some member states may be reluctant to rely on other member states for their electricity supply.

- Political Instability — Instability in a partner member state could disrupt commitments to the project and potentially impact the safety and operation of the joint plant.

- Imbalance of Power — A larger or more economically/politically dominant partner member state might exert undue influence over the project, creating tensions or perceptions of unequal benefits, particularly if one partner bears more financial risk or receives less energy output.

- Public Acceptance — Gaining public support for hosting a nuclear power plant and nuclear waste repository within a specific member state could be challenging.

These concerns can be addressed through dialogue at all levels — starting with national leaders and cascading to technical stakeholders — between countries considering a joint nuclear power plant. In such dialogues, it is worth noting the good faith demonstrated by GCC states in previous in-kind electricity trade transactions could provide a strong foundation for building a reliable and fair partnership.

Conclusions

The GCC states’ first attempt to develop a joint regional nuclear power plant was unsuccessful, due to the lack of relevant infrastructure, governance, and expertise. These issues resulted in delays and lack of coordination, leading to each member state pursuing individual nuclear programs.

Fifteen years later, conditions in the GCC region have significantly improved, marked by an expanded interconnection grid capacity, a functioning electricity trade system among member states, established nuclear legal frameworks and regulations, as well as experience in the construction and operation of nuclear facilities. These changes provide a more feasible entryway into a GCC joint nuclear power plant than previously thought. A quick overview highlights the region’s progress:

- The UAE has four nuclear units in operation and plans to build additional nuclear power reactors.

- Saudi Arabia is working toward constructing its own nuclear power plants.

- The remaining GCC states are exploring the nuclear option — in particular, new advanced nuclear reactor technologies including SMRs.

The growing potential for nuclear energy in the GCC region warrants serious consideration and strategic planning. GCC member states are strongly advised to revisit and reassess the opportunities for collaboration in harnessing nuclear energy to meet their developmental and environmental goals.

Note

[1] State of Kuwait, Amiri Decree no. 259: “Disbanding Kuwait National Nuclear Energy Committee,” July 24, 2011; Yousef Mohammad Al-Abdullah et al., “Assessment of the Feasibility of Nuclear Small Modular Reactors in the Power Generation Portfolio in Kuwait,” Kuwait Institute for Scientific Research, 2024.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.