Author(s)

Media outlets from coast to coast have reported a significant increase of start-up companies over the past two years.1 Whatever the reasons behind the surge of new businesses—pursuing one’s long-term passion, realigning one’s skills, wanting to be one’s own boss, or following the Great Resignation2—the growing number of entrepreneurs is a welcoming development in the aftermath of the pandemic. Entrepreneurship is a documented contributor of job growth, innovation, and economic resiliency, and COVID has been a catalyst for galvanizing these new entrepreneurs.

According to the U.S. Census Bureau, about 3.5 million and 4.4 million new business applications were filed in 2019 and 2020, respectively. This represents a 25% increase between 2019 and 2020. The growth continued into 2021, when new business applications jumped to 5.4 million, a 23% increase over 2020.3

In light of the great interest in entrepreneurship, this brief reviews five tax benefits commonly used, and sometimes overlooked, by entrepreneurs. It also discusses recent changes and policy proposals relevant to these provisions.

R&D Tax Credits

Technological innovation has long been identified as a primary driver of economic growth. As such, it is not surprising that tax codes have provisions to incentivize research and development (R&D) activities. One of the most well-known is the research and experiment tax credit (commonly known as the R&D tax credit) under Section 41 of the Internal Revenue Code (IRC). What is intriguing is that although this tax incentive has existed since the 1980s, it has been temporarily extended 16 times and was only made permanent in 2015.4 The most recent Joint Committee on Taxation (JCT) estimate shows that R&D tax credits cost the federal government $13.2 billion in 2021, and the cost will increase to $17.3 billion in 2024.5

Overall, the tax credit intends to increase business investment in R&D spending by reducing the cost of conducting qualified research activities. These activities must be experimental and seek to discover information that is technological in nature. In addition, the applications of research outcomes must help to develop new or improved business components, defined as products, processes, computer software techniques, formulas, or inventions to be sold, leased licensed, or used by the firm performing the research.6

Therefore, research activities conducted after commercial production has commenced do not qualify. Research that duplicates existing business components or activities that adapt existing business components to a specific customer’s needs are also disqualified. In addition, activities that develop internally used software, surveys, and market research are not considered qualified activities. Finally, the activities need to be conducted in the U.S. to qualify for an R&D tax credit.7

Expenses associated with performing qualified research activities, known as qualified research expenditures (QREs), form the basis of an R&D tax credit calculation. Generally, the credit amounts are 20% of a firm’s QREs above a certain threshold. After 2006, an alternative simplified credit (ASC) also became an option. The ASC is equal to 14% of a taxpayer’s QREs in the current tax year over a certain threshold, calculated differently from that under the regular method.8

Both in-house and contract research expenses from qualified research activities can be QREs. For in-house activities, salaries, costs of supplies and materials are common components. For third party expenses, 65% to 100% of the expenses can be qualified expenses depending on the entity performing the activity. However, certain expenses are not QREs. For instance, building an equipment expenses, overhead (water, electricity, insurance, property taxes), and fringe benefits of researchers are excluded.

The long history of the credit and the numerous guidelines issued over time do not necessarily mean the applications are unambiguous. In fact, taxpayers and the IRS often argue in court as to whether certain activities are qualified research activities—which result in different QRE amounts and associated R&D credits depending on the nature of the activity.

The Biden administration’s FY 2022 proposed budget recognizes the importance of R&D activities. It proposes to repeal the foreign-derived intangible income (FDII) deduction, a provision that taxes at a reduced rate export revenue generated by U.S.-based intellectual property (IP), and deploys the revenue to directly incentivize R&D activities.9 Although the budget proposal does not specify how the revenue will be used, directionally it recognizes that domestic R&D deserves further investment. The associated revenue is not trivial: JCT estimates the FDII costs the government $127 billion between 2020 and 2024, which is roughly double the cost of R&D tax credits taken per year.10

Although all policymakers agree innovation is important, not everyone shares the administration’s view about eliminating the FDII deduction. Some lawmakers believe domestic R&D incentives are not sufficient to keep American-developed IP in the U.S.11 They argue that R&D incentives are different from those encouraged under the FDII; the former serves as “input” measures that reduce R&D costs on the front-end regardless of whether the outcomes are successful or not, whereas the latter is an output measure that complements R&D incentives by rewarding successful research. They also point out that 19 out of 37 OECD countries have the IP box (or patent box) mechanism, which provides a similar tax incentive.12 In addition, the FDII deduction provides an important counterbalance to another international tax provision, the Global Intangible Low-Tax Income (GILTI) tax, which is a 10.5% minimum tax on

return generated from valuable intangibles.13 This provision intends to discourage tax-motivated IP offshoring and keep the IP in the U.S. or even encourage reshoring.

The 83(b) Election

Equity compensation is important for businesses in various stages of development. It is particularly important for start-up companies when only limited cash funds are available to reward employees. Restrictions are often attached to equity compensation. For instance, the stock is subject to vesting over multiple years, and the employee must remain with the company during this period.

The 83(b) election, named after Section 83(b) of the IRC, essentially provides an employee or start-up business owner the option to pay taxes on the fair market value (FMV) of the restricted stock at the time of grant. The FMV is typically much lower than that at the time of vesting if the start-up company is successful and its stock value continues to rise.

The election essentially allows the recipient of equity compensation to prepay his or her tax liability on a low valuation in anticipation of future appreciation, before the vesting period even starts. Any subsequent appreciation in value is not included in the recipient’s compensation when the restricted stock is vested. It is worth noting that the election only offers tax benefits when the stock or equity is provided as compensation. When the shares are sold, capital gains tax will need to be applied on the proceeds of the transaction. The tax basis is the amount the recipient paid to get the stock plus the amount he or she included in income as compensation.14

The 83(b) election is often overlooked because the election documents must be sent to the IRS and the employer within 30 days after the issuance of restricted shares.15 In addition, these elections are generally not revocable. As such, there are potential risks: it could be a powerful tool that saves the recipient a large amount of tax if the company is successful. However, if the stock value goes down or the company files for bankruptcy, the irrevocable nature of the election means that the recipient overpaid taxes at a higher equity value.

A similar disadvantage could be that if a recipient leaves the firm before the vesting period is over, the recipient would have prepaid taxes for shares he or she never received. Another drawback is more pertinent to established companies. For these companies, stock value at the time of grant could be high and the associated tax due is substantial. Under these circumstances, taxpayers may need to raise funds by selling other investments to pay taxes in advance. As such, this election generates a lesser cash burden for recipients when the stock value and the associated tax due is low at the time of issuance.

Qualified Small Business Stock (QSBS)

Section 1202 of the IRC provides up to 100% exclusion of taxable gains on the sale of qualified small business stock (QSBS). Although this incentive has been in place for almost three decades, it drew considerable attention over the last few months because of the Biden administration’s plan to increase the federal long-term capital gains tax rate.

This benefit allows tax-free capital gains for up to $10 million or 10 times the cost basis of QSBS held longer than five years.16 To qualify for QSBS benefit, the entity needs to be a C-corporation and meet the active business requirement, meaning that at least 80% of its assets are used for actively conducting qualified trade or business.17 In addition, because it is a small business benefit, the entity cannot have over $50 million in gross assets at the time of stock issuance.

The shares must be issued directly from the qualified small business in exchange for either cash or services provided by the recipients. In other words, both shares sold to early investors in exchange for cash and stock given to employees in exchange for services qualify, but the shares cannot be obtained through secondary markets. The underlying equity instruments can be common or preferred stocks; however, instruments that promise future equity, such as a convertible note or simple agreement for future equity (SAFE), do not immediately qualify.18 These instruments will begin to qualify when they convert to stock, and the five-year holding period begins at the date of conversion.

The exclusion of capital gains could be highly beneficial for recipients, especially in coordination with the 83(b) election. Specifically, if a recipient makes the 83(b) election, the QSBS five-year holding period starts at election regardless of the vesting status of the restricted stock.19

If a taxpayer holds the QSBS for more than six months but less than five years, the taxpayer may be able to roll over gains into another QSBS within 60 days and defer paying taxes on these gains upon meeting certain requirements.20 Then, if the combined holding period exceeds five years, the taxpayer will still be able to utilize the tax benefits under Section 1202.

If, unfortunately, the investment in the QSBS is unsuccessful, the tax code allows write-offs of qualifying losses as ordinary income for up to $50,000 per individual (and $100,000 for joint filers) if certain conditions are met.21 The benefit lies in allowing these losses to offset ordinary income at a higher amount, instead of only allowing $3,000 against ordinary income if investors do not have capital gains to offset these losses.

Section 1202 was enacted in 1993 to encourage investment in small businesses. The rules specified that if the QSBS was acquired between 1993 and 2009, 50% of the capital gains were excluded. This percentage was increased to 75% in 2009, and again increased to the current 100% in 2010. The Biden administration, in its Build Back Better Act, proposes to reduce the exclusion to 50% for any taxpayer with an adjusted gross income over $400,000, or if the taxpayer is a trust or estate.22

Supporters of the reduction claim that because most beneficiaries are wealthy investors or early-stage employees of highly successful companies, the provision is not effective in stimulating investment in small businesses.23 The most recent JCT tax expenditure estimate shows that this provision cost the government $1.8 billion in 2021, and it is expected to cost $8 billion over a five-year period from 2020 to 2024.24 In addition, research on the economic benefits of QSBS is limited and inconclusive: some studies do show the provision reduced the cost of capital, and the issuing corporations captured benefits in the form of higher stock prices. Others believe such incentives distort the allocation of capital by encouraging equity investment in very small firms, and only certain, but not all, investors benefit.25

Others disagree. They believe that this tax benefit exists to facilitate access to equity capital for qualifie start-up companies, which often require medium- to long-term capital commitments. The QSBS enhances the attractiveness of these investments by increasing the potential after-tax returns compared to the more established alternatives. The legislative history of establishing QSBS in 1993 and the subsequent expansions show there is both support and need for these incentives.26 In addition, there are also concerns about how to bridge the transition period—taxpayers who made investments under the current law but have not realized their capital gains may suddenly be subject to a 50% reduction in benefits if this provision becomes law.

Incentive Stock Options (ISOs) and Non-qualified Stock Options (NSOs)

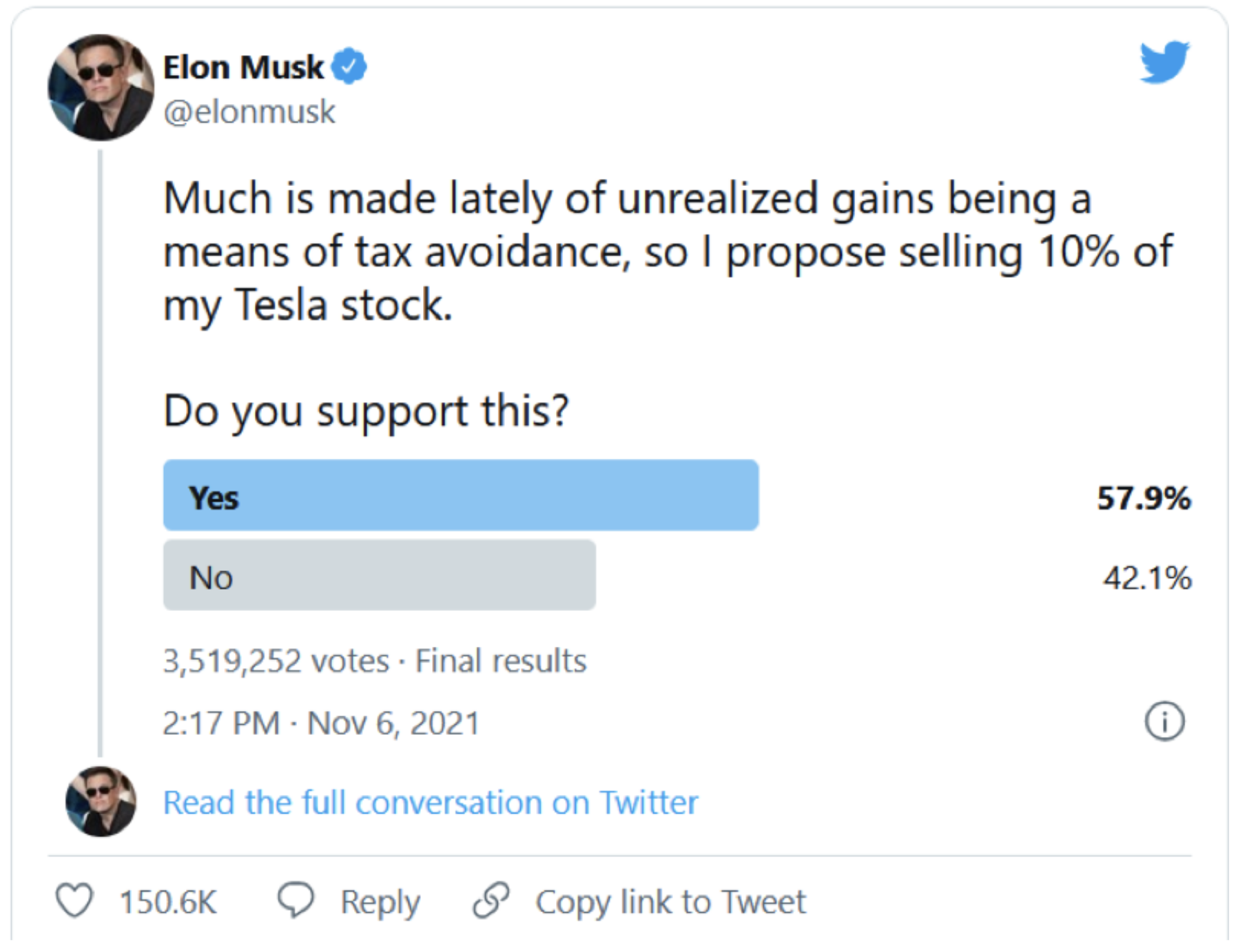

Elon Musk, an entrepreneur and one of the world’s wealthiest people, asked Twitter users last November if he should sell 10% of his Tesla holdings in the form of stock options. Although some were quick to point

out that Musk’s stock options are set to expire in August 2022—so he needs to act before these options become worthless—others believed this was a response to Democratic congressional members’ proposal to tax unrealized capital gains.27 In a follow-up tweet on December 19, 2021, Musk clarified that he would be paying over $11 billion in taxes, mostly from this sale.

Image — Musk Polls Twitter on Stock Sale

A stock option, a popular form of equity compensation, is the right to buy stock at an agreed-upon price (grant price) within a pre-specified timeframe (option term).28 Typically, the grant price is fixed and roughly equal to the equity’s FMV at the time of grant. The recipient can exercise the right to buy stock at the grant price during the option term. However, because options are not obligations to purchase, they expire after the pre-specified date and the recipient forfeits the right to purchase stock at the grant price.

For more established companies, stock options can be offered as part of a standard compensation package. For start-up companies, this type of equity compensation can be critical because it limits cash outlays while simultaneously providing incentives to recipients. The terms of stock options can include restrictions based on length of time, milestones, achievements, or vesting schedules to specify the date when the shares are eligible for purchase. These structures are designed to motivate loyalty and performance of the recipients—when the stock price continues to rise, the grant price remains set and option recipients stand to benefit.

At a high level, a company commonly issues two types of stock options: the Incentive Stock Option (ISO) and Non-qualified Stock Option (NSO). Generally, only employees can receive ISOs and this instrument enjoys favorable tax treatments. The NSOs, on the other hand can be offered to employees, consultants, and other service providers.29

NSOs are generally taxed at an amount equal to the difference between the grant price and the FMV of the shares (often called as tax spread) on the date of exercise. This amount is taxable as ordinary income even if the recipient has not sold any shares. Later, when the recipient sells the stocks, the sale price minus the FMV at exercise is taxed at the capital gains rate.

On the other hand, ISOs are not taxed at exercise. Instead, the gains will be taxed when the recipient sells or otherwise disposes of his or her shares. Assuming the recipient sells the shares several years later, he or she will be taxed at the long-term capital gains rate on the difference between the grant price and stock price at the date of sale.

The preferential tax treatments of ISOs come with certain restrictions. First, ISOs can only be granted by a C-corporation. The holding period requirement specifies that ISOs must be held for more than two years after the grant and the sharesobtained upon exercising ISOs must be held for more than one year after exercise. In addition, the FMV of ISOs that are exercisable for the first time in any calendar year ma not exceed $100,000 based on the FMV a the time of grant. The excess portion, if any, will be treated as NSOs that do not qualify for any preferential tax treatment.30

Often, the holding period requirement and acquisition are the two major reasons that ISO holders fail to benefit from favorable tax treatments. For instance, when a start-up company is acquired, the ISOs are cancelled in exchange for cash payments, which are taxed as ordinary income instead of capital gains.

Profits Interests and Carried Interests

Many tax benefits discussed so far are applicable to corporations, which makes profits interests an attractive tax incentive for non-corporations, such as Limited Liability Companies (LLCs) or partnerships.31 Similar to ISOs, profits interests are not taxable for the recipient on the date of the grant. It will be taxable when the profits interests are disposed, at the capital gains tax rate. Conceptually, profits interests represent rights to share future value increases of the LLCs.32

A special feature about this instrument is that upon receiving profits interests, the recipient becomes a partner of the entity and is no longer treated as an employee for tax purposes. As such, the recipient will be responsible for filing his or her own estimated tax payments and will start receiving Form K-1 (a statement typically issued to a partner regarding a partner’s investment in partnership interests) instead of Form W-2 (a statement typically issued to an employee regarding his or her taxable wage and withholding).

Similar to stock options, profits interests can be granted subject to vesting based on time or performance.33 Because of the restrictive nature of vesting requirements, a recipient is allowed to make an 83(b) election at the time of issuance. This protects the recipient’s opportunity to be taxed on the value of profits interests on the date of grant. When the businesses that issue profits interests are applicable partnership interests (APIs), the interests are known as carried interests. APIs are typically associated with entities that conduct investment activities—for example, hedge fund, private equity, and ventur capital firms. The carried interests have been perceived as a loophole for tax avoidance, essentially allowing these firms to compensate highly paid workers by converting wage income to capital gains that are subject to lower tax rates. As such, the Tax Cuts and Jobs Act (TCJA) added Section 1061 to limit certain tax benefits to prevent abuse.34 Most notably, taxpayers who receive carried interests are required to use a three-year holding period to benefit from the long-term capital gains tax treatment.

Conclusion

A great number of new businesses were created in the past two years. Some are highly encouraged by this development. Small businesses have been the cornerstone

of the U.S. economy, and entrepreneurs often generate ideas that are critical to innovation. However, others provide a more cautious perspective. They believe workers may return to the traditional

form of employee relationship once the business sector recovers from the havoc created by the pandemic.35 Besides, it is uncertain whether these new start-ups represent innovative business models that will disrupt current operations and generate job opportunities, or whether they are simply sole proprietors replacing shut-down businesses during the pandemic. It may take years to fully uncover the long-term trend, i.e., when statistics such as business survival rates, tax records, and employment data become available. Regardless of the long-term outcomes, it is certain that workers devote their time and resources to be productive forces of the economy.

Entrepreneurs and small business owners who pursue their passion, decide to change their lifestyle, or have great ideas to fill voids in the current system have many things to consider— business ideas,

funds, ownership arrangement, operations, and entity structure, to name a few. Tax provisions, including the ones discussed in this brief, can provide powerful incentives for entrepreneurs and attract investments that enable innovative ideas.

Endnotes

1. See Joseph Melhuish, “It’s All Just Wild”: Tech Start-Ups Reach a New Peak of Froth,” New York Times, January 24, 2022, https://www.nytimes.com/2022/01/19/technology/tech-startup-funding.html; and

Samantha Masunaga, “Dream of Becoming Your Own Boss? These Women Made It Happen During COVID,” Los Angeles Times, September 16, 2021, https://www.latimes.com/business/story/2021-09-16/women-entrepreneurs-covid-pandemic-first-time-business-owners.

2. Michelle Fox, “Start-ups Boomed During the Pandemic. Here is How Some Entrepreneurs Found a Niche,” CNBC, May 27, 2021, https://www.cnbc.com/2021/05/27/how-entrepreneurs-found-their-start-up-niche-during-covid-19.html.

3. U.S. Census Bureau, “Business and Industry, Business Formation Statistics,” last visited April 4, 2022, https://www.census.gov/econ/currentdata/.

4. Gary Guenther, “Research Tax Credit: Current Law and Policy Issues for the 114th Congress,” CRS Report, June 18, 2016, https://crsreports.congress.gov/product/details?prodcode=RL31181.

5. Joint Committee on Taxation, "Estimates of Federal Tax Expenditures for Fiscal Years 2020-2024,” JCX-23-20, November 5, 2020, https://www.jct.gov/publications/2020/jcx-23-20/.

6. Internal Revenue Service, Section 41–Credit for Increasing Research Activities, last visited: April 4, 2022, https://www.irs.gov/pub/irs-regs/research_credit_basic_sec41.pdf.

7. For detailed discussion, see Section 41(d)(4) of the Internal Revenue Code (IRC).

8. Because of the different thresholds under the regular credit and the ASC, a taxpayer is unlikely to benefit equally under both calculations. Typically, start-up companies benefit more under the ASC

9. U.S. Department of Treasury, General Explanations of the Administration’s Fiscal Year 2022 Revenue Proposals: Repeal the deduction for foreign-derived intangible income (FDII), page 11, May 2021, https://home.treasury.gov/system/files/131/General-Explanations-FY2022.pdf.

10. Joint Committee on Taxation, Estimates of Federal Tax Expenditures for

Fiscal Years 2020-2024.

11. Kevin Hern et. al, Letter to Secretary Yellen Regarding the Elimination of FDII

Deduction, July 28, 2021, https://hern.house.gov/uploadedfiles/7.28.2021_kevin_hern_fdii_letter.pdf.

12. A patent box (or IP box) taxes revenue generated by intellectual property at a rate that is lower than the typical corporate income tax rate. The goal is to encourage research and development.

13. GILTI is calculated as the total active income earned by a U.S. firm’s foreign affiliates that exceeds 10% of the firm’s depreciable tangible property. The return that exceeds 10% is presumed to come from income that is attributable to intangibles. The Biden administration’s Build Back Better Act proposes to expand the GILTI.

14. IRS, Publication 525, Taxable and Nontaxable Income: Restricted Property, page 14, January 13, 2022, https://www.irs.gov/pub/irs-pdf/p525.pdf. This publication also explains the difference between restricted stock and restricted stock unit (commonly known as RSU). An 83(b) election is not allowed for the latter.

15. Certain remedies may be available for taxpayers missed the 30-day window. See https://www.aicpa.org/news/article/what-to-do-for-a-missed-sec-83-b-election.

16. Specifically, the exclusion is the greater of $10 million cumulatively or 10 times of the cost basis per year. See https://www.law.cornell.edu/uscode/text/26/1202 for details.

17. Certain industries are excluded from the benefit: hotels, farms, mining concerns, restaurants, financial institutions, or certain services such as health, architecture, law, accounting, or engineering. This is known as the qualified trade or businesses requirements.

18. For discussions about convertible debt and SAFE, see Joyce Beebe, Tax Considerations of Crowdfunding, Issue Brief 03.05.20, Rice University’s Baker Institute for Public Policy, Houston, Texas, March 5, 2020.

19. The holding period begins just after the property is transferred. See https://www.law.cornell.edu/cfr/text/26/1.83-4.

20. See Section 1045 of the IRC (Qualified Rollovers).

21. See Section 1244 of the IRC (Ordinary Income Treatment of Losses on Sales of Small Business Stock).

22. U.S. House of Representatives, ‘Build Back Better Act,’ H.R. 5376, 117th Congress, Page 2213 of 2468, last visited April 4, 2022, https://www.congress.gov/bill/117th-congress/house-bill/5376/text.

23. Manoj Viswanathan, “The Qualified Small Business Stock Exclusion: How Startup Shareholders Get $10 Million (Or More) Tax Free,” Columbia Law Review Forum 120, no. 1 (January 13, 2020): 29-42, https://columbialawreview.org/content/the-qualified-small-business-stock-exclusion-how-startup-shareholders-get-10-million-or-more-tax-free/.

24. Joint Committee on Taxation, “Estimates of Federal Tax Expenditures for Fiscal Years 2020-2024.”

25. Gary Guenther, “Small Business Tax Benefits: Current Law, RL 32254,” Congressional Research Service, November 20, 2021, https://crsreports.congress.gov/product/pdf/RL/RL32254.

26. For a discussion about the legislative history of QSBS, see Benjamin Willis, “Building Back Biden’ American Start-Up Through Tax Incentives,” Forbes, November 29, 2021, https://www.forbes.com/sites/taxnotes/2021/11/29/building-back-bidens-american-start-up-through-tax-incentives/?sh=8dabd6854692.

27. “Behind Elon Musk’s Twitter Poll is a Tax Bill Come Due,” New York Times, November 8, 2021, https://www.nytimes.com/2021/11/08/business/elon-musk-twitter-poll.html.

28. Some plans call a grant price an exercise price or a strike price

29. See IRS, Topic No. 427–Stock Options, last updated: January 21, 2022, https://www.irs.gov/taxtopics/tc427.

30. Certain restrictions also apply to significant shareholders who own more than 10% of shares. In particular, the grant price for these shareholders must be at least 110% of the FMV and they must exercise within five years of the grant. If these conditions are not met, the options will automatically be treated as NSOs for federal income tax purposes.

31. An LLC with at least two members is treated as a partnership for federal income tax purposes unless the entity elects to be taxed as a corporation through Form 8832. See IRS, Limited Liability Companies,

February 24, 2022, https://www.irsgov/businesses/small-businesses-self- employed/limited-liability-company-llc.

32. In contrast to profits interests, capital interests are like shares of a corporation and give a holder the right to a share of the existing value of the entity. For instance, if an LLC dissolves immediately

after issuing profits interests and capital interests by selling its assets and distributing the proceeds, the capital interest recipients, but not the profits interest recipients, will be entitled to a portion of the proceeds.

33. The IRS has issued two guidance documents to clarify “safe harbor” tax treatments of profits interests: see Rev. Proc. 93-27 and Rev. Proc. 2001-43.

34. Pub. L. 115-97, Tax Cuts and Jobs Act, December 22, 2017, https://www.congress.gov/115/plaws/publ97/PLAW-115publ97.pdf. In addition, the Treasury released final regulations in 2021 to provide further guidance. See IRS publications (1) T.D. 9945, January 7, 2021, https://www.irs.gov/pub/irs-drop/td-9945.pdf and (2) Section 1061 Reporting Guidance FAQs, November 3, 2021, https://www.irs.gov/businesses/partnerships/section-1061-reporting-guidance-faqs.

35. Ben Casselman, “Start-Up Boom in the Pandemic is Growing Stronger,” New York Times, August 19, 2021, https://www.nytimes.com/2021/08/19/business/startup-business-creation-pandemic.html.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.