Influential voices have been urging the world to move full speed ahead on the energy transition. UN Secretary General Antonio Guterres has warned that without progress on climate, “people in all countries will pay a tragic price.”1 And U.S. President Joe Biden has explicitly made potential influence on climate from modern emissions a central principle of his domestic and foreign policy plans with ambitious binding pledges, such as a net-zero carbon electricity grid by 2035. Pledges like these imply rapid but impractical displacement of fossil fuels with alternative energy technologies, which, in themselves, bear numerous consequences—including emissions associated with supply chains and the need to ensure reliable energy delivery.

With “climate” now a central agenda item, an influential constellation of policymakers, financiers, and NGOs based primarily in OECD countries is increasingly promoting a two-pronged strategy. Part one entails accelerated investment in renewable energy sources, especially wind and solar, which are assumed to have lower emissions and are considered more environmentally acceptable. Part two seeks to simultaneously constrict access to capital for suppliers of “traditional” (i.e., fossil) energy. The green investment side of this strategy has made real progress. According to data from Bloomberg and the International Energy Agency, alternative energy developers invested nearly $3 trillion between 2010 and 2020, about half of what was invested in upstream oil and gas.2 And energy production from wind and solar assets globally rose six-fold during the past decade.

Yet in spite of these advances, alternative energy technologies supply a fraction of usable energy. Ancient carbon stocks pulled from the earth still power modern civilization. Oil and gas combined still supplied nearly 60% of global primary energy in 2020—roughly their proportional share in 1965, but for an energy system that is now more than 3.5 times larger. Coal supplied an additional 27% of global primary energy. Wind and solar only supplied about 4% of global primary energy in 2020, their banner year to date and one in which fossil fuel production and consumption were disproportionately depressed. Electric vehicles (EVs) in use presently comprise less than 1% of the global light-duty fleet, and in most places, the electricity to charge their batteries still predominantly comes from carbon-based fuels.

Our review is not a call for inaction. Far from it. Instead, the core purpose of our report is to emphasize in realistic terms the complexity of the energy challenge and the scale necessary to effect meaningful change. These are critical—and thus far, largely overlooked—steps on the pathway to building a sustainable and energy-abundant future that fulfills the interconnected imperatives of human well-being and biosphere health alike.

Pushing to defund fossil fuels—before lower-carbon resources can credibly “fill the gap”—risks destabilizing a global energy- food-water-human well-being nexus that, sufficiently perturbed, would likely delay energy transition efforts for decades. The consequences of a delay would likely entail more cumulative carbon emitted than would be the case for a more orderly phasedown of fossil resources. The Biden administration’s “Long-Term Strategy” on climate itself points out that a delayed transition would entail a “higher likelihood of reaching catastrophic damages or ‘tipping points’ and potentially irreversible economic impacts.”3 In short, thermochemical and financial realities cannot be ignored—or we risk stranding the energy transition in the “valley of death,” upon whose rocky floor it now treads.

The past 10 years marked stage 1 of the global energy system’s mega-transect through the energy transition valley of death—initial scale up and fast progress downhill to the valley floor. Stage 2, the “valley floor”—which includes system disruptions and more complete public understanding of (and potential backlash to) the economic costs of the energy transition— is unfolding now and will intensify during the next several years. Stage 3, ascending the valley’s far wall, begins beyond 2025 and will feature an uncertain confluence of new technologies (such as small modular nuclear reactors) reaching commerciality, policy resets such as carbon taxes, and economic and supply chain burdens that, by that point, will have already imprinted their tangible and psychological impacts firmly into energy consumers and producers alike. Accordingly, what happens between now and the late 2020s, in all likelihood, will fundamentally determine the failure or success of an accelerated energy transition.

The Energy Transition Valley Of Death

The “valley of death” concept has long been used to describe the struggle by entrepreneurs to keep new ideas and products alive during the initial research and development cash-burn phase until proof of concept and commercial scaling are achieved. In software, scaling can happen at very low marginal cost.

The energy transition valley of death is very different. The prevailing view is that existing core low-emissions energy production technologies—wind, solar, grid-scale batteries for energy storage, and small modular nuclear reactors—are already either commercialized or have a clear path to commercial deployment. These views ignore the full and largely opaque costs of using wind, solar, and battery storage and the regulatory expense of licensing nuclear energy, biased by large-scale designs. Uncertainty about the energy transition valley of death curve means that underinvestment in incumbent energy sources can create—and prolong—an energy crisis. In one sense, there can be challenges in bringing a new energy system up to scale while it effectively competes with the massive—and generally lower-cost—installed base of legacy fossil fuel production and conversion systems.4 In truth, much of the legacy production base will be repurposed, at an expense that must be accounted for. And much of the legacy petrochemicals conversion base will continue to be required until materials science yields scalable alternatives.

Prematurely constraining access to fossil fuels could raise energy and materials costs to a level at which alternatives become more competitive, potentially even without subsidies. But the massive economic costs immediately imposed on consumers (voters) worldwide to close gaps in competitiveness5 would almost certainly trigger political backlash that could entrench extended fossil fuel dependence significantly beyond what present, path-dependent trends would imply. Indeed, backlash already is unfolding.

The existing reality of what Vaclav Smil6 calls “infrastructural inertia” would pave

the way for such an energy reversion. The world’s billion-odd cars still mostly use gasoline or diesel, and virtually all aircraft, heavy trucks, farm equipment, earthmovers, and ships are still oil burners. They will likely remain in service for decades to come, absent forced retirements that could collectively cost trillions of dollars. A car owner who spent $30,000 two years ago for a gasoline vehicle is unlikely to part with that machine even if a great electric vehicle comes to market next year—more so for a trucker who spent $150,000 or more for their tractor and trailer, or the shipowner or airline that spent $20-$30 million or more per unit on their new equipment. These heavy transport systems collectively drive close to 40% of total global oil use. The lion’s share of global electricity generators still combusts coal or natural gas, and many of these frequently have 30-40 years of service life remaining.

The Valley Floor: Rocky and Slow Energy Transition Process

Many parts of the world—including key portions of the United States, such as California and Texas—have completed stage 1 of a three-part journey. During the green boom between 2010 and 2020, wind and solar grew explosively due to (1) a combination of subsidies and favorable policies singularly focused on emissions restraint and (2) the ability of intermittent sources to piggyback on a multitrillion- dollar existing set of coal, gas, hydro, and nuclear power stations that could generally act as de facto “batteries” by throttling output up to compensate for calm winds and cloudy skies—or down during bright, windy times.

Herein lies the less sexy but more important side of a green energy transition: marshalling capital and political will for a process that will take decades to achieve full effect and will have bumps along the way. The global energy system has been in constant transition for the past two centuries as a continuing series of industrial and technical revolutions enables our access to the BTUs, joules, and kilowatts needed to run modern civilization.

A confluence of thermochemical, logistical, and economic factors drove prior energy transitions. Each was “salad to steak” in that coal was 50% more energy dense than wood, and oil was about 50% more energy dense than coal (and better suited to power cars, ships, planes, trains, and trucks).7 Each evolution took decades and typically saw energy abundance increase. Indeed, in 1965 during the “oil age,” the United States consumed about three times as much energy per capita as the country did at the tail end of the “wood age” a century earlier.

Even as the thermodynamic and logistical upsides of these new energy sources became apparent—for instance, coal beating wood as an industrial fuel, oil surpassing coal as a transport fuel, steam power replacing sails, and direct heating vanquishing passive solar—the new source often took decades to meaningfully displace the old. Change took a long time because the installed infrastructure for producing, moving, and consuming the old fuel source was capital-intensive, designed to run for many years, and was expensive and difficult to replace. Serendipity often played a role as well.

For instance, gas displaced a massive chunk of U.S. coal demand over the past 15 years, because supplies surged right as the numerous coal-fired plants built during the energy crises of the 1970s and 1980s were nearing the end of their operational lives and could be retired without stranding invested capital. In turn, natural gas facilitated renewables’ ascent, because gas plants can rapidly throttle up or down to compensate for intermittency in wind and solar power generation in a way that coal plants could not have.

Energy abundance from carbon sources has also helped compensate for the fact that, in tandem with energy transition efforts, global demand has continued to expand. For the 20 years prior to the coronavirus pandemic, global primary energy use expanded at an average rate of 2% per year. As the world recovers from the pandemic, the trend will likely continue. Keeping up with rising energy needs, while also trying to reduce carbon intensity with sources that have low energy density, will pose unprecedented challenges.

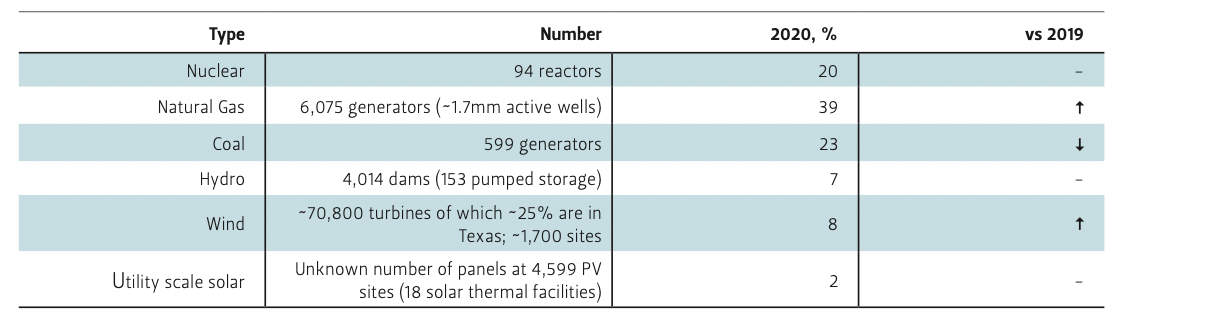

Consider the United States, which itself accounts for about 16% of global primary energy use. Based on current operating experience and technology, upwards of about 460,000 onshore wind turbines, seven times the current installed base, could be required to produce 50% of the American electricity supply.8 Assuming so large an expansion could even gain public acceptance, it would require massively augmenting transmission capacity and storage and/or backup generation. Funding such an effort—which addresses the electricity sector only—could still realistically cost an order of magnitude more than the American Recovery and Reinvestment Act of 2009, deployed after the 2008 financial crisis.

Developing countries face even greater relative challenges. Ambitious leaders seek to not only address the “kilowatt-scale” problem of alleviating individual citizens’ energy poverty, but also to power industrialization programs that require tens of gigawatts (or more) of power per country. In pursuit of their goals, they will use the resources most available to them. For Nigeria, Mozambique, and Tanzania, that will be gas, as Nigerian Vice President Yemi Osinbajo explained in an August 2021 Foreign Affairs essay.9 Ethiopia will rely on hydropower, even though the Grand Ethiopian Renaissance Dam stokes conflict with Egypt and Sudan. China, India, Indonesia, South Africa, Botswana, and others will likely lean most heavily on abundant and secure domestic coal. And with OECD countries deciding at the 2021 United Nations Climate Change Conference (commonly referred to as COP26) to end fossil fuel project finance, non-OECD countries will find other sources to fund existential energy development. Most of these options would substantially reduce the United States and the European Union’s (EU) leverage to encourage sustainable development.

Emissions impacts of differential development would be momentous. Non- OECD economies, led by China and India, now emit twice as much carbon dioxide each year as their OECD (i.e., high-income) counterparts. To understand what that means in policy terms, if the OECD achieved “net-zero” today, non-OECD emissions would equal what the entire world emitted in the late 1990s—when climate alarm bells were already beginning to ring.

“Green” Energy Sources Can’t Scale Without Energy—and Carbon—Abundance

Oil and gas are themselves energy transition minerals. First, they facilitate incorporation of renewables into existing power systems. In the United States especially, the 2010-2020 green boom succeeded in large part because the shale boom delivered nearly four units of natural gas energy to market for every unit of wind and solar power supplied during that time.10 Natural gas powering throttleable turbines effectively serves as a grid-scale “chemical battery” to compensate for weather-driven variation in wind and solar generation.

At $3 per million BTU—approximating U.S. Henry Hub prices over much of the

past decade—electricity generated from natural gas can be supplied at about $20 per megawatt hour (MWh). A megawatt- hour is enough electricity to power 200 homes for an hour on a hot Texas summer day. That MWh price for gas includes the cost of finding and producing the gas, pipeline transportation, crucial energy storage (including storage of energy content inherent in the fuel source), delivery to the powerplant, and conversion.

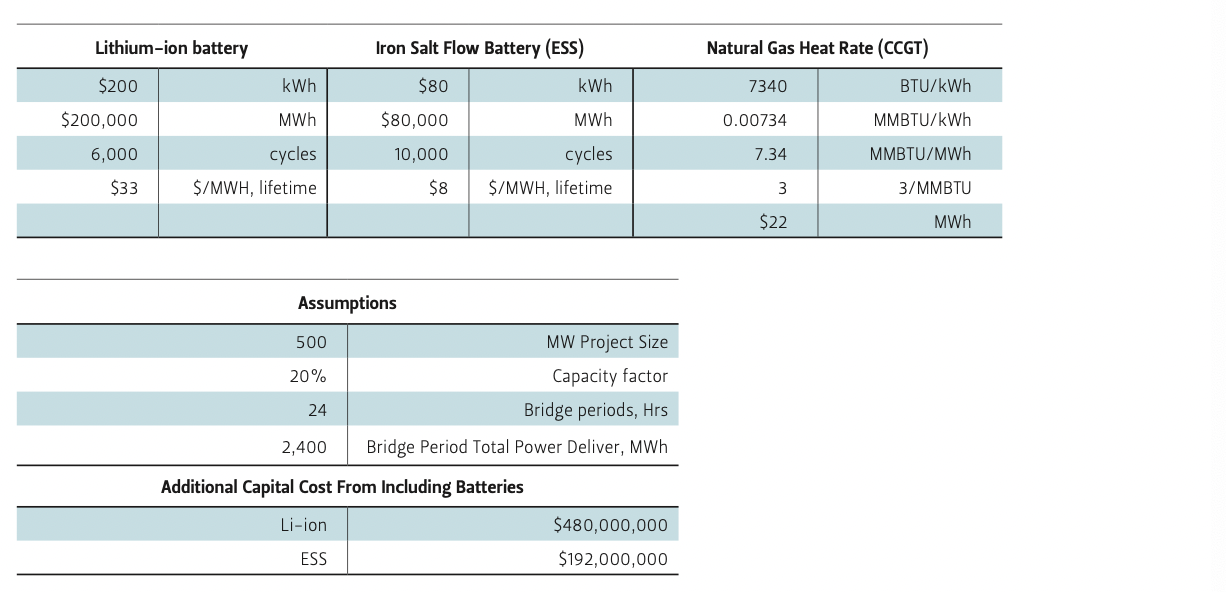

Lithium-ion batteries can provide energy storage for slightly more than $30 per MWh, amortized over their full-service life (assuming 6,000 discharge/recharge cycles). At present, most grid-based lithium-ion adder batteries can only provide about four hours of warrantied discharge. Iron salt flow batteries now being deployed at utility scale by the Bill Gates-backed firm ESS can likely do so for less than $10/MWh (assuming a 10,000-cycle life), but must be paid for upfront when a project is built and can add $200 to $500 million in capital cost to a world-scale solar or wind power project (Appendix Table 1).

Second, oil and gas literally form the physical building blocks of the wind turbines and solar panels the world now craves. Wind turbines would not exist without fiberglass and thermoset plastics. Solar photovoltaics would not be possible without plexiglass. Electric vehicles, meanwhile, embed large amounts of energy (and carbon) in their batteries and many kilograms (kg) of plastic and other petroleum-derived materials.11

A Tesla Model 3, the world’s bestselling full-size EV to date, contains approximately 200 kg of plastics, rubber, and textiles— virtually all of which are petroleum- derived.12 The plastics content of battery electric vehicles (BEVs) will likely increase as automakers use advanced polymers to reduce weight and accommodate heavy batteries to push the performance envelope. And battery packs themselves will likely incorporate more plastics for weight and safety.13

As such, demand for plastics is projected to grow at least as fast, if not faster, than metals—including those like lithium that are integral to BEVs and “green” power production and grids. And if accelerated transition efforts succeed, plastics and petrochemicals would have to effectively carry the full burden of oil and gas resource development costs, but spread across a number of barrels and cubic feet much smaller than today’s number. Neither the economic “stress test” of the most extreme energy transition assumptions on the global oil and gas businesses nor the cost of very expensive downstream investments have been explored.

Materials intensity associated with energy transition technologies like wind, solar, battery storage for grids, and battery EVs exceeds that of conventional technologies because of lower energy density. In fact, the pronounced tradeoff between energy density and materials intensity represents an enormous gap in energy transition thinking, analysis,

and policymaking. For instance, Argonne National Laboratory modeling suggests that BEVs still have a very long way to go to reach the same level of performance as gasoline and diesel engines.14 To have BEVs and gasoline-fueled vehicles on equal footing by 2045-2050 will require continued improvements in weight reduction, aerodynamics, engine efficiency, battery energy density, and motor power density.

Raw materials needs will also likely increase the amount of capital invested per unit of capacity installed. For instance, adding enough wind capacity to supply 1% of the primary energy used by the world today could require 100,000 or more tonnes of various rare earth metals—a substantial portion of global supply and most sourced from China—as well as more than 4.5 million tonnes of copper, another critical input metal poised for a supply crunch as the energy transition unfolds. While the 1% example is hypothetical and real-world energy demand will be met by a variety of suppliers, it nonetheless illustrates the sheer scale of materials (and capital) required to continue and perhaps even deepen the energy transition, should policymakers in key countries decide to do so (Appendix Table 2).

China dominates supply, processing, and refining of strategic metals such as rare earth elements, copper, aluminum, nickel, vanadium, and many more. Such control is consequential and could encumber energy transition plans, especially as geostrategic competition heats up between China, the United States, and key regional players like Japan. Beijing has weaponized its resources before, throttling rare earth exports to Japanese firms in the wake of a 2010 maritime dispute.15 Memories of that event likely help explain why China’s recent decision in October 2021 to consolidate its three largest producers of rare earth elements into a sovereign-owned behemoth rattled both the metals industries and customers. This move also raised a host of international supply chain security questions.16

China’s centerpiece role goes beyond raw materials into manufacturing by seeking to occupy top rungs of emerging global value chains, as articulated in the nation’s “Made in China 2025” plan. PRC-based firms control about 60% of wind turbine production, 70% of solar photovoltaic panel output, and 70% to 100% of electric vehicle battery production (depending upon chemistry).17 Along with manufacturing dominance comes control of intellectual property (IP), including IP obtained through partnerships in China with multinational companies. This means that even for investments outside of China, few choices presently exist that are not China-based partners or suppliers.

Wind, solar, and batteries are widely perceived to be “cheap” relative to legacy fuels. But the cost reductions and declining cost curves broadly used to justify their accelerated deployment reflect the distortionary impacts of industrial policy measures Beijing deployed over the past two decades to gain control and influence over energy transition-related raw materials supply chains and manufacturing. Repatriating supply chains and relocating manufacturing in the United States, Europe, and elsewhere almost certainly will make the essential components of green energy dreams much more expensive. These adjustments will come on top of price appreciation for essential minerals and metals, as post-pandemic economic recovery spreads and consumer demand for goods and services rebounds.

And, as we note above, costs typically associated with green energy reflect only installed equipment—not the full costs associated with integration into power grids. For wind and solar, the full cost must include system reliability with all that entails. For BEVs, the full cost must include power system revamping and expansion with recharging and more. In fact, we don’t know the sum total of costs for these technologies—and will learn as we go.

Accelerated energy transition’s public finance component—the subsidies and other support deemed vital to ensuring the scale-up of alternative energy technologies, not least by ensuring attractive returns to investors—is bundled into taxpayer obligations, further exacerbating cost opacity. Critics point to subsidies that have underpinned fossil fuel use around the world. This is fair criticism given the inefficiencies in energy consumption that are engendered and how they discourage private investment. However, public fiscal commitments for “green new deals” could realistically swamp what governments have spent thus far on legacy fossil fuels and would likely do so in a compressed timeframe that magnifies the apparent pocketbook impacts—and resultant political repercussions.

Carbon Newtonian Physics

Oil price volatility since the 2004-2008 price supercycle, and the major price crashes in 2014 and again during the 2020 coronavirus lockdowns, sequentially tarnished oil and gas’s reputation with investors, who could achieve far better returns from buying tech stocks and other assets. The sector’s poor financial performance was a wound largely inflicted by commodity price crashes, driven in significant part by its own productivity.

This in turn sowed the seeds for anti-carbon investment frameworks to spread across tens of trillions of dollars’ worth of institutional capital. Fund managers found signing onto politically fashionable carbon restriction measures easy, because they had often already sold down their holdings. Indeed, for most of the 2014 to early 2021 period, investors saw little need to delve into the oil and gas business’s animating forces when they could instead buy stock in Facebook, Amazon, Netflix, and other names that delivered outsized portfolio returns as oil languished.

Now that oil hovers near $75 per barrel, the broader world grapples with a massively impactful contradiction. On one side is the move, largely driven by a narrow slice of wealthy elites in the United States and Western Europe, to accelerate the energy transition by constraining investment in carbon fuel supplies. These actors seek to simultaneously (1) extract capital from enterprises that could have otherwise funded investments needed to meet present and future demand, (2) support post-carbon narratives disconnected from present global energy realities, and (3) operationalize these narratives through ideological restrictions on investments in companies that produce many carbon-based fuels. As 350.org puts it, “cut off the social license and financing for fossil fuel companies—divest, de-sponsor, and defund.”18 On the other side, billions of global consumers are caught in a pincers movement between anti-carbon politics that impede the capital deployments necessary to offset oil and gas wells’ relentless natural decline rate—a distortion that, if left unaddressed, will create further inflationary pressures.

In the most extreme cases, such as coal or oil sands, a growing group of institutional capital pools actively encourage divesting such assets, even though doing so does not remove their products and emissions from the energy system. In the lesser cases that apply to many publicly traded oil and gas producers at present, carbon restrictors impose substantial “indirect carbon taxes” through tough environmental, social, and governance (ESG) requirements and also discourage the deployment of capital to fund net growth in future production—including in “bridge fuels” that the global energy system will need to reduce coal use in a timely, large-scale fashion. ExxonMobil offers a contemporary example. Following a bruising battle, activist hedge fund Engine No.1 managed to place three new directors on Exxon’s board in mid-2021, and these individuals now reportedly question major future growth investments, including the massive Rovuma gas field development in Mozambique.19

Collectively, the dynamics discussed above look increasingly likely to usher in an era of “carbon Newtonian physics,” where a reaction to emissions concerns will likely, over time, precipitate an equal and opposite reaction. Pushback appears poised to coalesce around three primary vectors, discussed in order of their likely manifestation.

First, an alternative ecosystem of capital providers around the world will increasingly break with the carbon restriction herd if commodity prices remain high enough to tempt them with returns attainable by buying hydrocarbon producer stocks, facilitating debt sales, and lending to them. Globally, ESG-driven funds held about $40 trillion in assets under management at year-end 2020—a massive sum.20 But the corollary is that about $70 trillion worth of investable assets remain outside such strictures and could invest at greater scale in “traditional” energy producers.21 Crackdowns on tech companies in key jurisdictions, including China, the EU, and perhaps also the United States, could accelerate this trend by amplifying the relative attractiveness of hydrocarbon assets.

Second, high energy prices will very likely catalyze consumer rebellions at the ballot box, in the streets, and also among large commercial parties that anchor customers in many energy grids. Recent history is replete with examples of energy price spikes and supply shortages that have triggered violent unrest: in the Ivory Coast in 2016, the Yellow Vest Movement in France since 2018, in Iran in 2019, Kazakhstan in 2022, and so forth.

The Lilliputian web of anti-carbon constraints spreading through major global financial centers does not just bind multibillion-dollar Gullivers on Wall Street and Canary Wharf. It also hinders efforts to address energy poverty that denies cooking, lighting, sanitation, clean water, and economic opportunity to billions worldwide.

Energy price spikes also affect food security. The prices of multiple critical global commodities—including staple food grains— often move in close synchronization with oil prices due to the prevalence of petroleum- based agricultural inputs and the use of grains to produce biofuels that compete with and are blended with oil-derived fuels. Lester Brown, president of the Earth Institute, noted in 2014 that “[i]f I were to pick a single indicator—economic, political, social—that I think will tell us more than any other, it would be the price of grain.”22 When that price spikes along with oil, unrest indeed follows. During the last oil price upswing in 2004-2008, grain price shocks catalyzed unrest in multiple developing countries, including Bangladesh, Egypt, and Haiti. Periods of prolonged upward oil price movement have coincided with increases in corn prices over the past 30 years. In turn, corn price updrafts often presage price increases for other staple grains, as consumers substitute them for each other.

While the mid-2000s food riots occurred in the developing world, food insecurity now stalks parts of the OECD as well. The COVID-19 pandemic has revealed that many Americans also live on an economic knife’s edge with respect to food security. Scholars from the University of California, Davis and Northwestern University found that in 2020 during the pandemic, approximately 25% of U.S. families surveyed said that food supplies “just didn’t last” and that they could not afford to buy more—a proportion roughly triple the pre-pandemic level.23

Large industrial and corporate actors will also vote with their feet if energy price pressures and/or supply issues interfere with operations. In March 2021, Global Foundries, one of the world’s largest semiconductor manufacturers, filed to become an independent, self-managed utility.24 It seeks to leave Green Mountain Power’s Vermont service area and instead directly procure wholesale power from the regional grid, because its Vermont facility pays electricity prices almost twice what Global Foundries plants pay in upstate New York.

“Islanding” by large industrial and commercial customers can take a number of forms, including leaving retail providers that are bound by renewables mandates and, in some instances, even generating their own power. In any event, Global Foundries’ ongoing quest for cheaper electricity may be a harbinger of more such moves to come, especially for energy price-sensitive businesses. Power grid reliability may also promote more vertical integration by industrial power users given that the costs of power outages can be significant. For instance, Samsung and NXP lost at least $450 million from a month-long production disruption at their three Austin area chip fabs caused by the “Great Texas Blackout” of February 2021.25

Third, root capital providers such as pension funds will increasingly be forced to reckon with the reality that restrictions on investing in hydrocarbon producers may impede their ability to deliver the minimum returns thresholds necessary to meet obligations to hundreds of millions of current and future retirees across the OECD and non-OECD worlds. Key capital stewards already question the wisdom of divestment. For instance, the CEO of CalPERS (California Public Employees’ Retirement System), which now manages close to $500 billion in assets, noted in 2018 that “[d]ivestment limits our investment options. With a targeted return of 7%, we need access to all potential investments across all asset classes. Divesting does the exact opposite—it shrinks the investment universe.”

Shrinking the investment universe does a few things, none of them beneficial to the world’s population. Capital constraints hinder the energy system’s ability to meet a demand call that is poised to increase and that requires all sources to both meet immediate demand and also ensure the energy abundance necessary for a successful transition to lower-emissions resources moving forward. Restraining many large capital pools from flowing toward opportunities underpinned by demand also deprives common citizens— hundreds of millions of them—of the returns that could otherwise accrue to their 401Ks or other retirement accounts.

Carbon politics co-existed uneasily with pension investment policies during the golden decade between 2010 and 2020 when shale abundance cushioned renewables’ entry into the market and effectively allowed both camps to claim progress. But as renewables prove unable to scale at the level necessary to meet multi- exajoule demands on short timeframes, the turn away from carbon may demand a correction. To quantify the emerging quandary, oil and gas alone could require nearly $12 trillion of investment during the next 20 years to meet global demand, according to OPEC.26

Finally, in all, a great unknown exists: Will queasiness with ESG challenges associated with the enormous expansion of raw materials supply chains undermine apparent investor eagerness to defund carbon-based fuels and materials? Potentially vast and consequential sustainability challenges are associated with alternative energy technologies and components. The tradeoff between lower energy density and higher materials intensity is acute. Already the mining, minerals processing, and manufacturing industries are under increasing pressure to lower energy use, reduce emissions, report and verify ESG metrics, and manage and mitigate life-cycle risks and uncertainties.

Raw materials operations, in particular, encompass large-scale extractive operations mainly in fragile states. Over the past few decades, difficulty finding and developing new resources, especially high-quality resources, has meant bringing to market lower-grade deposits in larger tonnages to attain the same volumes of useful metals and chemicals. Having lower-grade resources means more complex, energy-intensive, and emissions-yielding processing. These realities are informing a growing push for recycling, but recovery of metals and materials from plastics is itself an industrial enterprise with substantial requirements for energy and hazardous materials management. A good example is the growing concern around battery metals and materials for EVs. To ensure their own ESG branding, automakers are forced to take larger footprints in materials sourcing and supply chains with commensurate transparency for both automakers and their vendors and suppliers across the board. It will take decades more to build the “net- zero” platforms to support “net-zero” emissions targets—if it is even possible.27

A New 2020s Climate Insurgency?

Capital starvation, consumer backlash, and fiduciary imperatives to deliver returns increasingly appear poised to deliver a carbon resurgence. Unlike the green insurgency turned green tsunami, a “keep carbon longer” resurgence will not require aggressive education, indoctrination, or subsidies. Instead, economic forces will mediate based on affordability, reliability, and scale.

The 2020-2021 time period may retrospectively turn out to mark the apogee of decree-based carbon restrictions driven by a tiny, well-placed, and wealthy segment from just a few of the world’s 200 countries—only one of which, the United States, is by itself a global energy system prime mover. To recap: (1) activist hedge fund Engine No.1 placed directors on the board of ExxonMobil, (2) a group of Dutch NGOs persuaded The Hague District Court to order Royal Dutch Shell to reduce the worldwide CO2 emissions attributable to its operations and products sold by 45% by 2030 relative to 2019 levels, (3) New York’s state pension fund announced plans to achieve “net-zero” portfolio carbon emissions by 204028 (which likely requires divestment of most fossil fuel holdings), and (4) BlackRock, the world’s largest asset manager, warned portfolio companies that “[n]o issue ranks higher than climate change on our clients’ lists of priorities.”29

Yet the unfolding energy crisis of winter 2021-2022 raises an unsettling question: What happens if the climate advocates’ newfound prominence in fact marks the inflection point at which they start being blamed for high gas bills, power outages, and flagging pension returns, rather than being protected and welcomed? From 2004 to 2008, consumers squarely blamed oil companies for high energy prices, with CEOs hauled to testify before the U.S. Congress and broad anger spreading across many countries at the notion of “outsized profits”— notwithstanding the conflation of gross revenue and actual profit margins.

In a 2021 and beyond energy price spike scenario, oil companies may find themselves taking a backseat to climate and carbon activists as targets for public anger. In the United States and other higher-income industrial societies—Poland, for instance— carbon energy has been intermingled with conservative and nationalist political identities. But the anger will be from a much broader societal base if energy price pain persists, especially if it bleeds into the prices of food and other basic necessities.

Salience and attribution matter. The drought-storm-flood nexus of climate change is a probability that unleashes havoc episodically and generally upon specific areas. It is also fundamentally a collective action problem, since we do not know whose greenhouse gas molecules are most responsible for a given disaster. In contrast, the energy-food-inflation nexus is a certainty that lightens wallets each day— and one for which consumers can and will attribute specific blame, if the effort is seen as politically-imposed.

In some countries, a revised green/renewables push that forces fuller accounting of systemic costs and demands a more incremental approach to decarbonization will likely only come after significant economic turmoil and political backlash that will require at least several years to fully play out. The United States fits squarely in this category. At the other end of the governance spectrum, China is already quietly reverting back to carbon energy resources—albeit alongside vocal leadership support for renewables. Vice Premier Li Keqiang noted at a National Energy Commission meeting on October 9, 2021 that China must maintain stable and secure energy supply chains and that this effort will include greater development of domestic coal, oil, and gas resources.30 Two weeks later, Premier Xi Jinping emphasized the importance of energy security, telling workers at the Shengli Oilfield that China must “ensure that its energy livelihood remains in its own hands” (能源的饭碗 必须端在自己手里).31 Translated into plain market signals, calls for redoubled hydrocarbon and coal supplies in the world’s single largest energy consumer (accounting for nearly 25% of global primary energy use) signal that carbon fuels of all stripes likely have a long runway ahead.

Corners of the financial markets more insulated from the climate lobby already recognize the opportunity in assets disfavored by contemporary consensus. Consider an October 2021 remark to the Financial Times by a hedge fund manager who noted that “[m]any of these [oil] companies are trading at very low cash flow multiples and at very big discounts to the replacement value of their assets. ... More people are driving gas- powered cars and scooters than ever.”32 Likewise, data from the Private Equity Stakeholder Project and the New York Times suggest that over the past decade, private equity firms have invested more than $800 billion in the fossil energy space.33

While capital will flow to the oil and gas sector so long as consumers demand those molecules, the source of capital matters for several reasons. First, hedge funds and private equity firms are typically the financiers of last resort and are much higher-cost capital providers than banks, equity markets, pension funds, and other sources. Second, while alternative investors’ assets under management are collectively huge, they likely cannot sustain the $500 billion-plus annual investment rates needed to meet the likely call for oil and gas globally. Third, in many cases, alternative investors must ultimately answer to root capital providers, like pension funds, that are increasingly subject to anti- fossil investment constraints that could percolate down and restrict the actions of managers the fund has allocated capital to. In simplest terms, higher capital costs and likely insufficient capital deployment capability ultimately mean slower resource development—and if demand persists, higher oil and gas bills paid by consumers.

These “side effects” may actually be intended by some green advocates as a way to increase green power. But they might want to pause and consider that as long as consumers demand oil, producers will supply it—but perhaps under a tripartite market structure very different from today’s. Private producers such as Mewbourne Oil (which by early October 2021 was running more rigs in the United States than Chevron and ExxonMobil combined) will constitute a growing slice of global production, as they acquire assets divested by traditional Big Oil companies struggling to remake themselves according to climate mandates.34 The second group will be private commodity traders such as Koch Industries, Vitol, Trafigura, and others, which already collectively handle more than one third of global oil flows and would be well positioned to acquire and integrate large upstream oil and gas producing assets.35 The third group consists of national and quasi-national oil companies.

Oil and gas are existential interests in Kuwait, Iran, Iraq, Qatar, Russia, Saudi Arabia, other key oil-exporting nations. Even as their diplomatic rhetoric increasingly accepts climate change and emissions concerns deeply held in Western Europe and the United States, they see themselves as the “last suppliers standing” in a carbon-pressured world and will continue investing to ensure their firms maintain the ability to supply global oil and gas demands. In short, more of the world’s oil and gas supply portfolio may shift to less transparent actors (to the potential detriment of the environment) and lower-scale and higher costs (to consumers’ detriment), empowering national oil companies located in often challenging regions that the U.S. has sought to strategically extricate itself from.

Can We Climb Out of the Valley?

Unlike the multi-decade lock-in imposed by large capital investments, the persuasions of emotive and fallible human beings can dynamically evolve. The same fervor that over the past decade drove increasing acceptance of restrictions on investments in carbon fuel production could turn the other way far more rapidly if anti-carbon efforts trigger global energy disruptions and consumer hardship before delivering tangible climate gains. On a less overtly political but equally consequential level, carbon investment strictures that leave fund managers unable to meet minimum returns thresholds could also prompt an about face as legal and market pressures reinforce each other.

The emissions math of a carbon resurgence would be brutal; a 1% increase in carbon fuels’ share of primary energy supplies could overwhelm the emissions offset of prior wind and solar progress by multiple years. Political challenges will be commensurately large, because while consumers in higher-income countries consider it important to address climate change, enthusiasm often fades in direct proportion to the costs consumers must personally bear. An “energy deprivation” approach, à la President Carter conspicuously wearing a sweater while signing emergency energy legislation in 1977, will likely fail with American voters (and those in many other polities as well).36

Ample energy supplies are the bedrock of modern civilization. As such, climate progress will require simultaneously seeking to maximize energy abundance, affordability, efficiency, and reliability. Successful approaches will emphasize “all sources on deck”—with a prominent role for wind, solar, and better grid batteries, but also major roles for vital but less popular characters: nuclear energy and carbon taxation. An “e pluribus unum” energy mindset that unites multiple resources based on the principles of (1) delivering energy abundance and security and (2) doing so in ways congruent with climate progress offers the most productive path to a much lower-emissions and prosperous 2050.

Endnotes

1. “Paris climate deal could go up in smoke without action: Guterres,” UN News, September 17, 2021, https://news.un.org/en/story/2021/09/1100242.

2. “Renewable Investment,” Bloomberg Green, accessed December 13, 2021, https://www.bloomberg.com/graphics/climate-change-data-green/investment.html.

3. The Long-Term Strategy of the United States: Pathways to Net-Zero Greenhouse Gas Emissions by 2050, United States Department of State, United States Executive Office of the President, Washington D.C., November 2021, https://unfccc.int/sites/default/files/resource/US_accessibleLTS2021.pdf.

4. Peter Hartley, Kenneth B. Medlock, Ted Temzelides, and Xinya Zhang, “Energy Sector Innovation and Growth: An Optimal Energy Crisis,” The Energy Journal 37, no. 1 (January 2016): 233–58, http://www.jstor.org/stable/24696708; Peter Hartley and Kenneth B. Medlock, “The Valley of Death for New Energy Technologies,” The Energy Journal 38, no. 3 (2017): 33–61. http://www.jstor.org/stable/44203642.

5. Gürcan Gülen, Chen-Hao Tsai, Deniese Palmer-Huggins, and Michelle Michot Foss, “Competitiveness of Renewable-Generation Resources,” The University of Texas at Austin’s Bureau of Economic Geology report, April 2018, https://www.beg.utexas.edu/files/energyecon/CEE_Research_Note_Competitiveness_ Generation_Apr18.pdf.

6. Vaclav Smil, Energy: A Beginner’s Guide (Oxford: Oneworld Publications, 2012).

7. “Typical calorific values of fuels,” Forest Research, accessed December 14, 2021, https://www.forestresearch.gov.uk/tools-and-resources/fthr/biomass-energy-resources/reference-biomass/facts-figures/typical-calorific-values-of-fuels/.

8. Michelle Michot Foss, Minerals and Materials for Energy: We Need to Change Thinking, Policy brief: Recommendations for the New Administration, 01.24.21. Rice University’s Baker Institute for Public Policy, Houston, Texas, https://www.bakerinstitute.org/media/files/files/380e0ff7/bi-brief-012421-ces-minerals.pdf.

9. Yemi Osinbajo, “The Divestment Delusion: Why Banning Fossil Fuel Investments Would Crush Africa,” Foreign Affairs, August 31, 2021, https://www.foreignaffairs.com/articles/africa/2021-08-31/divestment-delusion.

10. Authors’ calculation using data from U.S. Energy Information Administration, “Primary energy production by source,” accessed December 2021, https://www.eia.gov/totalenergy/data/annual/index.php.

11. Michelle Michot Foss, “The ‘Criticality’ of Minerals for Energy Transitions. Hydrocarbons? Yes, Hydrocarbons.,” Baker Institute Blog, February 8, 2021, https://www.bakerinstitute.org/research/the-criticality-of-minerals-for-energy-transitions-hydrocarbons-yes- hydrocarbons/.

12. Gensheng Gui, “Carbon Footprint Study of Tesla Model 3,” E3S Web of Conferences, 2019, https://www.e3s-conferences.org/articles/e3sconf/pdf/2019/62/e3sconf_icbte2019_01009.pdf.

13. Michelle Michot Foss, “Minerals & Materials Supply Chains—Considerations for Decarbonizing Transportation,” testimony before the U.S. House of Representatives Committee on Energy & Commerce Subcommittee on Energy, Hearing on “The CLEAN Future Act: Driving Decarbonization of the Transportation Sector” May 5, 2021, https://www.bakerinstitute.org/research/minerals-materials-supply-chains-considerations-for-decarbonizing-transportation/.

14. Vehicle performance requirements are: 0-60 mph acceleration in less than 9 seconds, sustainable speed of 65 mph on a 6% grade, driving range of 100 miles for the BEV 100, driving range of 300 miles for conventional vehicle and BEV 300. Ram Vijayagopal, “Comparing the Powertrain Energy and Power Densities of Electric and Gasoline Vehicles,” Presentation at Powertrain Strategies for the 21st Century, University of Michigan Transportation Research Institute, July 20, 2016. For the full report, see Ram Vijayagopal, Kevin Gallagher, Daeheung Lee, and Aymeric Rousseau, “Comparing the Powertrain Energy Densities of Electric and Gasoline Vehicles,” SAE Technical Paper 2016-01-0903, 2016, https://doi.org/10.4271/2016-01-0903.

15. Keith Bradsher, “Amid Tension, China Blocks Vital Exports to Japan,” New York Times, September 22, 2010, https://www.nytimes.com/2010/09/23/business/global/23rare.html.

16. Shunsuke Tabeta, “China to create rare-earths giant by joining three state companies,” Nikkei Asia, October 24, 2021, https://asia.nikkei.com/Economy/China-to-create-rare-earths-giant-by-joining-three-state-companies.

17. Based on Bloomberg New Energy Finance (licensed) and other sources. See endnote 12.

18. 350.org, accessed January 13, 2022, https://350.org/about/.

19. Christopher M. Matthews and Emily Glazer, “Exxon Debates Abandoning Some of Its Biggest Oil and Gas Projects,” Wall Street Journal, October 20, 2021, https://www.wsj.com/articles/exxon-debates-abandoning-some-of-its-biggest-oil-and-gas-projects-11634739779?mod=hp_lead_pos1.

20. Sophie Baker, “Global ESG-data driven assets hit $40.5 trillion,” GreenWorks, accessed December 14, 2021, https://www.greenworksenvironmentalpartnership.com/global-esg-data-driven-assets-hit-40-5-trillion/.

21. “Asset and wealth management revolution: The power to shape the future,” PWC, accessed December 14, 2021, https://www.pwc.com/gx/en/industries/financial-services/asset-management/publications/asset-wealth-management-revolution-2020.html.

22. Joshua Keating, “A Revolution Marches on Its Stomach,” Slate, April 8, 2014, https://slate.com/technology/2014/04/food-riots-and-revolution-grain-prices-predict-political-instability.html.

23. Marianne P. Bitler, Hilary W. Hoynes, and Diane Whitmore Schanzenbach, “The social safety net in the wake of COVID-19,” Brookings Papers on Economic Activity, BPEA Conference Drafts, June 25, 2020, https://www.brookings.edu/wp-content/uploads/2020/06/Bitler-et-al-conference-draft.pdf.

24. Vermont Public Utility Commission, “GLOBALFOUNDRIES U.S. 2 LLC / request to operate a Self-Managed Utility,” 21-1107-PET, filed March 17, 2021, https://epuc.vermont.gov/?q=node/64/157291/FV-ALLOTDOX-PTL.

25. Kara Carlson, “Shutdown of Austin fab during freeze cost Samsung at least $268 million,” Austin American-Statesman, April 30, 2021, https://www.statesman.com/story/business/2021/04/30/austin-fab-shutdown-during-texas-freeze-cost-samsung-millions/4891405001/; Kara Carlson, “NXP could lose $100 million due to weather shutdown of Austin plants,” Austin American-Statesman, March 12, 2021, https://www.statesman.com/story/business/2021/03/12/nxp-could-lose-100-million-due-weather-shutdown-austin-plants/4664621001/.

26. OPEC (Organization of the Petroleum Exporting Countries), OPEC World Oil Outlook 2021, 2021, 139, https://woo.opec.org/pdf- download/index.php.

27. A forthcoming review of nickel demand growth for batteries and a case study of Chinese investment in Indonesia highlights these quandaries (Michelle Michot Foss and Jacob Koelsch, February 2022).

28. “New York State Pension Fund Sets 2040 Net Zero Carbon Emissions Target,” Office of the New York State Comptroller, December 9, 2020, https://www.osc.state.ny.us/press/releases/2020/12/new-york-state-pension-fund-sets-2040-net-zero-carbon-emissions-target.

29. “Letter to CEOs,” BlackRock, January 30, 2021, https://corpgov.law.harvard. edu/2021/01/30/letter-to-ceos/.

30. “Li Keqiang presided over a meeting of the National Energy Commission, emphasizing ensuring stable energy supply and safety, enhancing green development support capabilities Han Zheng attended,” Xinhua News Agency, October 11, 2021, http://www.gov.cn/xinwen/2021-10/11/content_5641907.htm.

31. “Xi Jinping encourages the majority of oil workers to achieve better results and new achievements,” Xinhua News Agency Weibo, October 22, 2021, http://www.news.cn/politics/leaders/2021-10/22/c_1127983430.htm.

32. Laurence Fletcher and Derek Brower, “Hedge funds cash in as green investors dump energy stocks,” Financial Times, October 6, 2021, https://www.ft.com/content/ed11c971-be02-47dc-875b-90762b35080e.

33. Hiroko Tabuchi, “Private Equity Funds, Sensing Profit in Tumult, Are Propping Up Oil,” New York Times, October 13, 2021, https://www.nytimes.com/2021/10/13/climate/private-equity-funds-oil-gas-fossil-fuels.html.

34. David Wethe, Kevin Crowley, and Sergio Chapa, “Shale Oil is Booming Again in the Permian,” Houston Chronicle, October 11, 2021, https://www.houstonchronicle.com/business/energy/article/Shale-Oil-Is-Booming-Again-in-the-Permian-16525317.php.

35. Andreas Goldthau and Llewelyn Hughes, “Saudi on the Rhine? Explaining the emergence of private governance in the global oil market,” Review of International Political Economy 28, no. 5 (2020): 1410-1432, https://doi.org/10.1080/09692290.2020.1748683.

36. Nina S. Hyde, “President Carter, the Sweater Man,” Washington Post, February 5, 1977, https://www.washingtonpost.com/archive/lifestyle/1977/02/05/president-carter-the-sweater-man/56e7a4cf-102a-4b09-8aa7-b19d9a06f50b/.

Table 1 — Estimated Upfront Capital Cost Impacts of Adding 24-Hr Duration Battery to Grid-Scale Wind/Solar Projects

Sources ESS Inc., “Long Duration Energy Storage Systems for a Cleaner Future,” Investor Relations Presentation, August 30, 2021, slide 25, https://s28.q4cdn. com/365128779/files/doc_presentations/2021/ESS_Analyst-Day-Presentation-8-30-21.pdf; U.S. Energy Information Administration, “Natural gas-fired electricity conversion efficiency grows as coal remains stable,” August 21, 2017, https://www.eia.gov/todayinenergy/detail.php?id=32572.

Table 2 — Comparison of Existing Utility Scale Power Generation Assets vs. What Would Be Needed to Reach 50% of U.S. Net Electricity Production

Sources See the U.S. Energy Information Administration https://www.eia.gov/electricity/data.php for plant capacities and counts and https://www.eia.gov/ tools/faqs/faq.php?id=207&t=3 for nuclear. See also the U.S. Wind Turbine Database from the U.S. Geological Survey (USGS) https://eerscmap.usgs.gov/uswtdb/ and the interactive map from the USGS ScienceBase Catalog for the U.S. solar footprint https://www.sciencebase.gov/catalog/item/imap/57a25271e4b006cb45 553efa.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.