Decentralized finance (DeFi) — the application of blockchain technology to financial services — has the potential to increase efficiency in financial markets, promote competition, improve access to capital for small businesses and contribute to economic growth. For all its prospective benefits, however, the technology also presents substantial challenges for user accessibility, fair competition and law enforcement. The expansion of the emerging DeFi market depends on whether the concerns of investors, consumers and governing authorities can be successfully addressed — without regulating the technology into inefficiency and disuse in the process. In this report, we discuss a few of the challenges and concerns surrounding DeFi and leading sources of thought and action on those topics. We also explore the applicability of embedded regulation, which holds promise as a bridge between regulation and innovation.

What Is DeFi?

DeFi postulates that financial services need not rely on centralized intermediaries (such as banks, brokers or governments) but can instead be provided directly by end users to other end users. This can be achieved through peer-to-peer software based on blockchain technology (Schär 2021). DeFi needs blockchain technology — a digital decentralized ledger that is transparent, immutable and public in nature — to function securely and effectively (IBM 2022). Blockchain’s decentralized ledger technology (DLT) records transactions and tracks assets, allowing users to see the origin and end of each transaction without using intermediaries. The digital ledgers are held on the computers, or nodes, supplied by users on the blockchain.

DeFi provides an alternative to traditional financial services, which necessitate the costs of intermediaries (Roose 2022). It offers a distributed innovation process that lets information flow in a managed way between users (Chesbrough, Vanhaverbeke and West 2014); instead of using third parties, DeFi seeks to enable individual users to lend, borrow, manage assets or obtain insurance directly from one another (Chohan 2021).

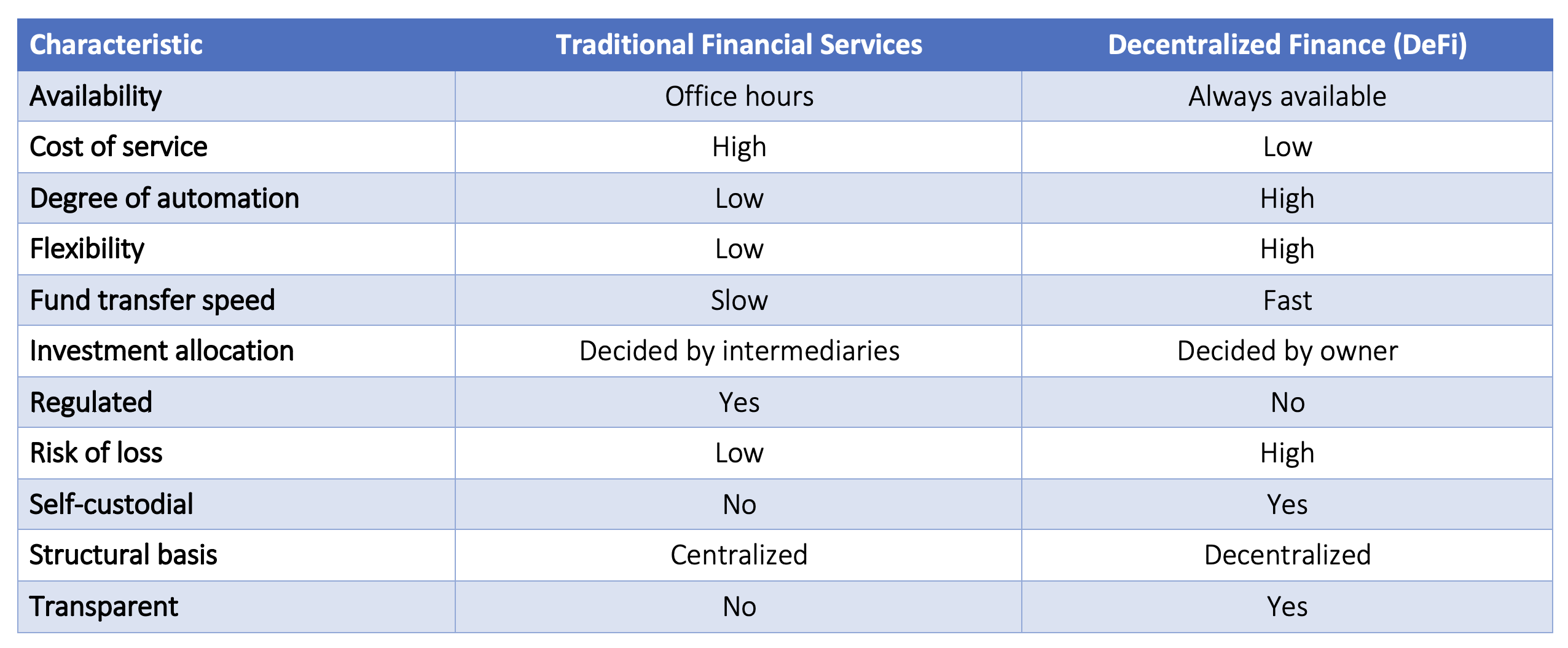

The main differences between DeFi and traditional finance lie in DeFi’s automation and decentralization. DeFi runs on blockchain technology, which replicates its encrypted records on numerous nodes all over the world (Pilkington 2016). For the most part, this technology remains unregulated; system participation is anonymous in some blockchain models, and no central party can decide who can and cannot participate. It is possible, however, to create a permissioned blockchain to which only one or a few participants can grant access to others (IBM 2022). Table 1 provides a comparison of the main characteristics of traditional and decentralized financial services.

Table 1 — Brief Comparison of Traditional and Decentralized Finance Services

As of July 2022, $42.98 billion had been locked into DeFi contracts (DeFi Pulse, n.d.). Figure 1 shows the evolution of the total value locked (TVL) in DeFi contracts in U.S. dollars. Between mid-2020 and October 2022, a tremendous amount of attention and money flowed into DeFi systems. At its highest point, in November 2021, TVL in DeFi contracts reached $107.5 billion. The graph in Figure 1 reflects both the steep growth of DeFi and the volatility of crypto markets over the past two years.

Figure 1 — Total Value Locked (TVL) in DeFi Contracts (in U.S. Dollars)

Both risks and opportunities for real world applications have arisen from these digital markets. As we write, new companies are creating innovative ecosystems in which entrepreneurs and small companies can access capital by connecting their real-world assets to DeFi platforms and using those assets as collateral. One example is Centrifuge, a DeFi-based lending protocol that focuses on making alternative credit more accessible for small businesses and entrepreneurs by offering investors access to liquidity pools with stable yields (Kraken, n.d.). Centrifuge’s idea of “unlocking liquidity for real world assets” is a new concept in which individuals with traditional assets like invoices, mortgages or streaming royalties can convert those assets into non-fungible tokens (NFTs), and then use those NFTs as collateral for loans at competitive interest rates. Investor-users purchase Centrifuge tokens with stablecoins to create a liquidity pool for loans to other individuals.[1]

Implications of DeFi for Competition and Antitrust Policies

According to economic theory, when firms compete for customers, it leads to lower prices, higher quality goods and services, greater variety and more innovation (The White House 2021). When there is insufficient competition, dominant firms can use their market power to block potential competitors from entering the market. This prevents entrepreneurs and small businesses from participating on a level playing field and turning their ideas into new goods and services. Cetorelli et al. (2007) show that the share of total bank assets held by the top four U.S. commercial banks increased steadily from 1990 to 2004, signaling a concentration risk in American financial markets.

“Antitrust” refers to the laws and policies that regulate the concentration of economic power to avoid monopolies and anticompetitive practices (Cornell Law School, n.d.). These laws and regulations enable market stability, social welfare and fair competition. Below, we discuss three competition and antitrust considerations in relation to DeFi: barriers to entry to financial markets, open finance and decentralized autonomous organization (DAO) design.

Barriers to Entry

The introduction of DeFi to financial markets is not expected to be smooth, and in the beginning traditional financial institutions may have an advantage. As in any other market, new competitors or services must overcome certain challenges in order to gain market share. And as Jin and Vinella (2022) recognize, a significant response from current financial service providers is likely, since they will not simply give up their market share. DeFi also faces specific barriers to entry such as high initial investment costs.

Moreover, DeFi entrants lack the trove of historical data held by incumbent financial institutions. Consumers may likewise be reluctant to use DeFi services because of the inconvenience and cost of migrating information from, or sharing information with, a traditional financial institution. As such, a rapid adoption of DeFi services by consumers is not expected. Users normally take some time to learn, trust and adapt to new technologies. When it relates to financial services and consumers’ financial security, we expect technology to be adopted at an even slower pace.

Traditional financial system actors are powerful and, obviously, financially capable. The traditional financial system is big enough and complex enough to deter any new competitor. According to the Boston Consulting Group (2021), financial assets account for roughly 60% of net wealth globally, representing around $250 trillion. In the U.S. alone, the Federal Deposit Insurance Corporation (FDIC) insures 4,787 bank institutions, which together encompass 82,184 branch offices and manage $24.066 billion in financial assets (2022). JPMorgan Chase has more than 51 million digital customers in the U.S., the highest of any bank in the country (Green 2019); by contrast, the largest DeFi network, Bitcoin, has fewer than 15,000 active nodes all over the world (Jin and Vinella 2022).

Another entry barrier for DeFi is that not every customer in the financial system trusts or uses digital technology. People who are older, have a lower socioeconomic status and/or live in rural areas, among other vulnerable groups, may have limited access to or understanding of electronic devices capable of engaging in DeFi. Moreover, even if people have access to this kind of technology, they may not have the necessary skills to use it. Internet access may also be a barrier for some. For this reason, DeFi could potentially widen the financial inclusion gap.

Additionally, many people may prefer human contact over automated services. When it comes to finance, an in-person experience might feel more trustworthy than an experience with software doing what it is programmed to do (Mims 2021). Software can also be inflexible compared to human interaction. Take, for example, a phone call; many people prefer to speak directly with a company’s representative, rather than work through a computerized voice menu. People are generally change-resistant, and DeFi platforms will need to build trust in order for consumers to accept their services. This entry barrier puts DeFi at a disadvantage compared to traditional financial services, which typically offer physical locations and human interaction.

Finally, incumbent financial service providers have the capability to build blockchain or DeFi applications themselves. They also could acquire DeFi start-ups, instead of competing against them. Big banks in the U.S. are already investing heavily in this area (Yang 2022; JPMorgan, n.d.). JPMorgan Chase invests $12 billion each year on emerging technology, funding a team of 50,000 technologists (JPMorgan Chase, n.d.). In short, new DeFi service providers will have to overcome both financial and pragmatic challenges in order to succeed in the financial market against existing participants.

Open Finance

The term “open finance” refers to a movement toward greater transparency, accessibility and shareability of users’ financial data with the goal of fostering competition in the financial services sector. In short, open finance platforms are data-portability systems that allow consumers to share their financial data across providers, reducing data-driven barriers of entry to financial markets and enabling competition. The concept can be facilitated through DeFi. With open finance systems, new companies can use historical financial data to create and offer new services that target customers’ specific needs. As Awrey and Macey (2022) note, it can level the informational playing field and foster competition among incumbent financial institutions and a new generation of companies, many of whom are trying to satisfy consumers seeking to make faster payments, borrow money, invest their savings, exchange currencies, manage budgets and so on.

Zetzsche, Arner and Buckley (2020) argue that as a policy objective, open finance is justified on pro-competition grounds, as it addresses market efficiency, economies of scale and situations in which data determines competitive strength. American and Chinese information technology (IT) markets have tended toward oligopoly or monopoly over the past decade; open finance systems can counteract this by hampering industry concentration. Arguably, the main assets of tech giants Google, Facebook, Amazon and Alibaba are their pools of consumer and supplier data (Ramos and Villar 2018). With this data, they can better advertise, determine prices, offer new tailored services and reach more clients. The concentration of information and data promotes monopolistic behavior and market collusion (Patterson 2017), leading to higher prices at the expense of consumers. Open finance presents an opportunity to counter the trend of data accumulation in just one or a few entities and to instead benefit consumers through increased competition in financial markets.

If strategically applied by a jurisdiction, open finance systems can enable consumers to quickly, simply and securely move their financial data between financial service providers like banks, investment management firms and insurance companies (Nicholls 2019). This should make the entrance of new DeFi service suppliers more feasible; open finance can lessen major barriers to entry such as lack of historical financial data for users, and reduce the costs and inconvenience to users of switching from traditional financial services to DeFi services.

DAO Design

The concept of a decentralized autonomous organization (DAO) was introduced by Ethereum co-founder Vitalik Buterin in 2014. A DAO is a collectively-owned, blockchain-governed organization working toward a shared mission. Smart contracts define how the organization works and how funds are spent. DAOs are constructed by a series of interrelated smart contracts — codes that automatically execute transactions on a blockchain network when previously established requirements are fulfilled — to achieve members' objectives. Buterin (2014) writes, “The ideal of a decentralized autonomous organization is easy to describe: it is an entity that lives on the internet and exists autonomously but also heavily relies on hiring individuals to perform certain tasks that the automaton itself cannot do.”

While DAOs can promote competition by increasing efficiencies and lowering costs for both DAO members and end users, they may also present antitrust challenges. Through automated decision-making, DAOs have the capacity to fix prices, divide markets, exchange sensitive information or restrain trade. A DAO could also enable competitors to collude when deciding what products to sell or what pricing strategies to implement. Further, a DAO designed with a profit orientation could engage in automated monopolistic behaviors if it gained a dominant position, especially in a particularly small market. While these behaviors are equally possible in traditional organizations run by humans, they may be harder to detect on a digital, autonomous, decentralized and potentially anonymous platform. As such, with regard to identifying antitrust violations and enforcing laws, DAOs present potential new challenges for authorities charged with protecting consumers.

In short, DAOs may foster competition and enable businesses to operate more efficiently. They also have an appealing internal governance structure that utilizes electronic voting. However, DAOs could raise a number of antitrust issues that authorities may struggle to address.

Implications of DeFi for Economic Growth

Potential Benefits

The Organisation for Economic Co-operation and Development (OECD) posits that DeFi applications have the potential to deliver significant economic efficiencies through the transfer of value without the need for trusted centralized intermediaries, bringing faster and cheaper automation of transactions (2022). With DeFi, it is possible to reduce transaction costs and promote transparency because all transactions are publicly available. No human involvement is needed, since transactions are triggered by data that is provided by the protocol or by external nodes known as “oracles.”[2]

Furthermore, DeFi has a money-multiplier effect. Applications for lending can canalize short-term savings and provide loans on demand, without the solvency and liquidity restrictions of traditional banks. As such, startup funding and short-term lending would be more widely available in the market, increasing economic opportunities. This could be translated into new businesses, greater investment, and, ultimately, expansion of GDP. DeFi could even create new jobs as participants in financial services and other industries enter the market.

The Financial Stability Board (FSB), an international organization that monitors and makes recommendations about the global financial system, notes that the application of DeFi technology may reduce the financial instability risks associated with traditional financial institutions (2019). The expected dispersion of financial service providers could diversify the financial system and reduce the concentration of suppliers. It could moderate the too-big-to-fail problem, in that the bankruptcy of a few institutions would no longer be a potentially catastrophic event for the economy as a whole.

With no central or single attack point, DeFi also offers security. A decentralized setting theoretically offers a stronger defense against cyber risks in terms of the integrity of financial records and service availability (FSB 2019). Furthermore, DeFi’s promise of interoperability could help promote innovation and build a vibrant financial ecosystem (Carter and Jeng 2021).

Most of the benefits mentioned above relate to efficiency, economic expansion, transparency and security. Next, we assess whether these benefits can outweigh potential risks and challenges.

Risks and Challenges

DeFi has a number of shortcomings. First, DeFi could promote financial exclusion; those poised to benefit from lower-cost, nontraditional financial services, like owners and managers of small and medium-sized businesses, may not have a sufficient understanding of DeFi systems to engage with them successfully or at all. Second, crypto-asset volatility can have a significant, negative impact on a user’s finances if it is not fully understood, and an unwitting user may place their trust in a risky platform. Third, while proponents of DeFi maintain that the system fosters trust through disintermediation and decentralization, another consideration is that users must put their trust in the creators of DeFi platforms’ underlying code and in the smart contracts that execute transactions. Few users would have enough technical skill to evaluate the code of a DeFi platform or a smart contract. As such, the adoption of DeFi will require users to trust software developers, in place of the regulated financial institutions that act as intermediaries in the traditional financial system.

DeFi networks are not currently regulated by any government, although the activity conducted on a DeFi network may very well be subject to law (such as securities or antitrust law) and fall within the jurisdiction of a regulating body (in the U.S., the Securities and Exchange Commission or the Federal Trade Commission). However, since decentralized networks are automated and community-governed, and may exist in multiple jurisdictions simultaneously, it is hard to identify decision-making actors that can be held responsible for network outcomes in any particular locality. This makes supervision, accountability and even legal notice difficult. The current legal system’s procedures are designed for centralized decision-making organizations with physical venues, like the incumbent financial institutions. DeFi systems are worldwide structures with no defined physical location or jurisdiction, and those qualities generate uncertainty and challenges for law enforcement (OECD 2022).

Consumer protection may also be a concern. Even if no minority group can manipulate DeFi networks with governance structures that require more than 50% of community votes, all participants, including consumers, can be affected if most nodes on a network decide to act in an illegal or unfair way. In a worst-case scenario, this could mean fraud and misappropriation of assets, since DeFi does not depend on a custodial system. Further, it is possible that changes to existing smart contracts within DeFi projects can be decided on and executed by the community despite the opposition of some participants. If so, consumers could be exposed to changes to the initial terms of the contract they had agreed upon.

DeFi may also present security and reliability issues. Contrary to what DeFi advocates have maintained, it is not impossible to manipulate a blockchain. The most vulnerable part of the chain appears to be the oracles, or the nodes that feed external data into the blockchain. If erroneous or fraudulent information is introduced, it can lead to massive consequences. For example, if manipulated price data is introduced into the blockchain, it can trigger massive buys or sales that otherwise wouldn’t happen under the governing smart contract parameters. This could result in considerable losses to some users and windfalls to others. Moreover, the permanent nature of the blockchain renders these frauds irreversible, even when they involve manipulated information or scams.

Today, it is significantly riskier for investors and financial consumers to hold assets on DeFi platforms than in regulated, centralized financial institutions. As far as we can ascertain, users have no recourse after the failure of a DeFi protocol, since it would be very difficult to identify the responsible actor. There are neither dispute resolution mechanisms nor recovery methods, exposing participants to a potential total loss of their investment. This risk is accentuated by the fact that DeFi projects can be launched by any programmer, with no testing or due diligence mandated by law in any known jurisdiction.

Another vulnerability for users on DeFi platforms is the possible existence of an “admin key” to the platform’s code. Developers sometimes keep an admin key that enables them to enter and repair the code of a DeFi protocol if it performs in an erratic manner. The existence of an admin key presents significant risks for users, since the keys can be used at any time to access user information or change a protocol’s operation from its roots. Application founders or developers could also use the admin key to seize an investor’s assets without justification. In short, despite the fundamentally decentralized nature of DeFi, its governance may still involve human intervention by way of admin keys and concentrated holdings of voting tokens.

Finally, DeFi protocols do not necessarily contribute to improved user awareness of financial risks. Although the platform’s code may be transparent, the average user would not have the sophisticated technical and financial knowledge required to understand the implicit risks of the system. Users would need both coding skills and deep financial literacy to understand the risks of the protocol for themselves (OECD 2022). Even users at the top of the game could have a difficult time assessing financial risks in DeFi protocols.

Looking Forward

The issues presently surrounding DeFi are complex, and it is impossible to predict whether its benefits will ultimately outweigh the risks for individual users and the challenges for traditional legal and economic systems. Free market innovation or government regulation — or some combination of the two — will be key to successfully overcoming those risks and challenges.

The accountability and law enforcement challenges presented by blockchain implementation are fundamental to the technology; they include the difficulty of identifying persons liable for faults in the automated outputs of a DeFi network and the complexity of determining the applicable law and jurisdiction. As Zetzsche, Arner and Buckley (2020) argue, DeFi could be subject to law either anywhere or everywhere, the latter being so problematic that it could deter participants from engaging in decentralized finance protocols. Regulatory technology (RegTech) could be a solution that enables DeFi’s economic benefits and addresses the concerns of users and financial regulators, as well as the major challenge that the rule of law in financial services poses for all actors, including developers, consumers and governments.

RegTech refers to the use of technology (both hardware and software) for regulatory compliance and supervision. One form of RegTech called “embedded supervision” could provide a regulatory window into DeFi networks. Embedded supervision is a “regulatory framework that provides compliance in decentralized markets to be automatically monitored by reading the market’s ledger ... reduc[ing] the need for firms to actively collect, verify and deliver data” (Auer 2022). Legal parameters could be embedded into DeFi code to meet regulatory screening objectives as part of the authorization requirements to enter financial markets. Embedded supervision is, essentially, an automated form of compliance.

Zetzsche, Arner and Buckley go one step further from the embedded supervision concept and advocate for “embedded regulation” (2020). Under this approach, the key regulatory objectives of market behavior, integrity and stability would be required to be part of the design of a DeFi system. Every protocol would implement regulatory features as part of its own automated structures, requiring input of specific data, quality conditions and other forms of traditional financial regulatory standards. Embedded regulation could also address the jurisdiction uncertainty of DeFi, if international consensus can be reached. In an example scenario, nations would agree that a DeFi network would be subject to the jurisdiction in which the supervisor of the network is located and that the embedded regulation system would have to comply only with the laws of that jurisdiction. Zetzsche, Arner and Buckley offer insight into how difficult it would be to achieve this broad consensus in the world’s nation-state form of governance.

DeFi has the potential to build more efficient financial markets and promote economic growth. Given antitrust and other legal considerations, the adaptation of DeFi systems to governance through RegTech’s embedded rules seems to be essential for proper market functioning. However, excessive regulation may also discourage entrepreneurial pursuits related to DeFi projects and restrict the very aspects that make DeFi unique among financial processes. In order for DeFi to maintain its status as an efficient alternative to traditional finance systems, it should remain as free as possible of intermediaries and unrestricted in its ability to stimulate innovation. Embedded regulation should only be enforced to the extent that it provides clarity and security to users of DeFi protocols. Ultimately, a balance will need to be established between the necessary regulation structure and the freedom to innovate.

Through DeFi, blockchain technology is creating a path toward reduced costs and improved security and transparency in the financial system, but the industry is still disordered and mostly unregulated. A balanced, embedded system of regulation could achieve both objectives: providing certainty to the financial system and promoting freedom to innovate. It could meet the public policy objectives of consumer protection and financial market competition, and meanwhile unlock the potential that decentralized finance has to offer in terms of cost-efficiency and funding availability for entrepreneurs and businesses.

Organizing the Public Debate

Governments and the private sector together face numerous challenges to harnessing the potential of DeFi for the benefit of consumers, investors and the economy as a whole. With a substantial amount of capital already locked into DeFi contracts ($42.98 billion as of July 2022), the DeFi market is far more developed than the public policy framework to deal with it. However, the public debate about whether and how DeFi should be regulated is beginning to take shape. The White House, the Securities and Exchange Commission (SEC) and academics have already published organizing principles and next steps for assessing and meeting the challenges of DeFi.

On March 9, 2022, the White House published an Executive Order (EO) on “Ensuring Responsible Development of Digital Assets.” The order is intended to chart a course to reduce the risks that DeFi could pose to consumers, investors and businesses, while also promoting financial inclusion and stability, preventing criminal activities and addressing climate change. Recognizing that the United States derives substantial economic and national security benefits from the predominant role that the U.S. dollar and American financial institutions play in the global financial system, the EO is an effort to maintain the United States’ strategic financial leadership.

According to the EO, the increased use of digital assets and DeFi exchanges may increase the prevalence of crimes such as fraud and theft, privacy and data breaches, abusive practices and other cyber risks faced by consumers, investors and businesses. To tackle these concerns, the order requires federal agencies with jurisdiction over economic, legal, environmental, technological and national security issues to coordinate with one another to produce reports to the White House within 180 to 210 days of the date of the order. Then, President Joe Biden’s office will review reports and propose specific changes to legislation and policy within one year.

In their reports, the agencies are required to outline the specific risks and regulatory gaps posed by digital assets and provide recommendations to address both the risks and potential benefits of DeFi. At the time of this writing, the agencies are in the process of producing their reports and recommendations. The reports are expected to promote high standards of transparency, privacy and security for DeFi systems that align with the national security and economic interests of the United States and can help equip it to maintain its role as a world leader in financial markets. Legal and policy changes are expected in late 2023.

Another important aspect of the EO is that it encourages the chairman of the Federal Reserve to research the extent to which a central bank digital currency (CBDC) could improve the efficiency of payment systems and reduce their costs using DeFi structures. Specifically, the Federal Reserve is required to assess whether a U.S. CBDC would enhance or impede the ability of monetary policy to function effectively as a critical macroeconomic stabilization tool for the American economy. The Federal Reserve is also ordered to research the extent to which foreign CBDCs could displace existing national currencies and alter the payment system in ways that could undermine the United States’ financial centrality on the global stage.

Similarly, the SEC recently delivered a Statement on DeFi Risks, Regulations, and Opportunities, issued by Commissioner Caroline Crenshaw (2021). It warns that DeFi participants’ current “buyer beware” approach — disclosing that DeFi is risky without providing the details investors need to assess risk likelihood — is not an adequate foundation on which to build the next generation of financial markets. Without a common set of standards and a functional system to enforce them, markets can tend toward corruption, fraud, information asymmetries and cartel-like activity. Over time, this may reduce investor confidence and participation.

On the other hand, well-regulated markets tend to flourish, and the U.S. capital market is a great example. The U.S. has less than 5% of the world’s population, yet over half of global investment capital is generated in American markets (Clayton 2022). Because of its reliability, U.S. financial markets are the destination of choice for most investors seeking to raise capital abroad. American securities laws do not just impose burdens; they provide market certainty. But, in the new “Wild West” that DeFi poses, a robust regulatory framework that delivers significant protection for market participants has not yet been adopted.

In the United States, several federal authorities have prospective jurisdiction over different aspects of DeFi, including the Department of Justice (DOJ), the Financial Crimes Enforcement Network, the Internal Revenue Service and the SEC. Currently, however, DeFi investors do not get the same level of protection and disclosure that are customary in other regulated markets. As Crenshaw notes in her statement: “a variety of DeFi participants, activities, and assets fall within the SEC’s jurisdiction as they involve securities and securities-related conduct. But no DeFi participants within the SEC’s jurisdiction have registered with us” (2021).

Some DeFi projects fit precisely within the SEC’s jurisdiction, while others may struggle to comply with SEC regulations as currently applied. Nonetheless, DeFi should be regulated to reduce the potential for manipulative or fraudulent conduct. As Crenshaw (2021) states, the DeFi system should let capital flow efficiently to the best projects, rather than being hindered by hype or false claims. In decentralized networks with diffuse control and different interests, regulations serve to create shared incentives aligned to benefit the entire system and ensure fair opportunities for the least powerful participants.

As former SEC chairman Jay Clayton wrote in a commentary earlier this year (2022), the U.S. needs to embrace the efficiencies provided by DeFi, such as fast payments and custody of assets in digital form. The working group created by the EO on “Ensuring Responsible Development of Digital Assets” should move forward on rules for stablecoins as a means of payment, and not as a security or commodity. At the same time, the SEC should issue requirements for the custody of tokenized assets, and the DOJ should pursue lawbreakers in order to send a clear message. The worst-case scenario is that the U.S. fails to act, to the detriment of both the American economy and our global financial infrastructure.

Endnotes

[1] Stablecoins are a form of cryptocurrency whose value is tied to the value of a fiat currency or a commodity. TAXbit, “What Is DeFi and How Does It Work?,” accessed August 22, 2022, https://taxbit.com/blog/what-is-defi-and-how-does-it-work; Centrifuge Docs, accessed August 22, 2022, https://docs.centrifuge.io.

[2] Oracles are entities that connect blockchains to external systems, thereby enabling smart contracts to execute based upon inputs from the real world. “What Is a Blockchain Oracle?,” Chainlink, https://chain.link/education/blockchain-oracles.

References

Auer, R. 2022. “Embedded Supervision: How to Build Regulation into Decentralized Finance.” CESifo Working Paper No. 9771. https://dx.doi.org/10.2139/ssrn.4127658.

Awrey, D. and J. Macey. 2022. “The Promise and Perils of Open Finance.” European Corporate Governance Institute – Law Working Paper No. 632/2022, University of Chicago Institute for Law & Economics Research Paper No. 956. http://dx.doi.org/10.2139/ssrn.4045640.

Benedetti, H. and S. Labbé. Forthcoming. “A Closer Look Into Decentralized Finance.” In The Emerald Handbook on Cryptoassets. https://dx.doi.org/10.2139/ssrn.4069011.

Zakrzewski, Anna, Joseph Carrubba, Dean Frankle, Andrew Hardie, Michael Kahlich, Daniel Kessler, Hans Montgomery, Edoardo Palmisani, Olivia Shipton, AkinSoysal, Tjun Tang, and Andre Xavier. 2021. Global Wealth 2021: When Clients Take the Lead. Boston: Boston Consulting Group. https://web-assets.bcg.com/d4/47/64895c544486a7411b06ba4099f2/bcg-global-wealth-2021-jun-2021.pdf.

Buterin, V. 2014. “DAOs, DACs, Das and More: An Incomplete Terminology Guide.” Ethereum Foundation (blog). May 6, 2014. https://blog.ethereum.org/2014/05/06/daos-dacs-das-and-more-an-incomplete-terminology-guide/.

Carter, N. and L. Jeng. 2021. “DeFi Protocol Risks: The Paradox of DeFi.” RiskBooks. https://dx.doi.org/10.2139/ssrn.3866699.

Cetorelli, Nicola, Beverly Hirtle, Donald Morgan, Stavros Peristiani, and João Santos. 2007. Trends in Financial Market Concentration and Their Implications for Market Stability. The Federal Reserve Bank of New York Economic Policy Review.

Chesbrough, H., Vanhaverbeke, W. & West, J. 2014. New Frontiers in Open Innovation. Oxford University Press: New York City.

Chohan, U. 2021. “Decentralized Finance (DeFi): An Emergent Alternative Financial Architecture.” Critical Blockchain Research Initiative Working Papers SSRN. http://dx.doi.org/10.2139/ssrn.3791921.

Clayton, J. 2022. “The Peculiar Challenges of Crypto Regulation.” Wall Street Journal, August 25, 2022. http://bit.ly/3EdQdiP.

Cornell Law School. n.d. “Antitrust.” Accessed July 19, 2022. http://bit.ly/3O41dE9.

DeFi Pulse Network. n.d. Accessed July 19, 2022. https://www.defipulse.com/.

Federal Deposit Insurance Corporation. 2022. “BankFind Suite.” Accessed July 7, 2022. https://banks.data.fdic.gov/bankfind-suite/bankfind.

Financial Stability Board. 2019. “Crypto-assets: Work underway, regulatory approaches and potential gaps.” https://www.fsb.org/2019/05/crypto-assets-work-underway-regulatory-approaches-and-potential-gaps/.

Green, R. 2019. “JPMorgan Chase’s investment in digital is allowing it to maintain a healthy user engagement.” Business Insider, October 16, 2019. http://bit.ly/3hKbUQd.

IBM. 2022. “What Is Blockchain Technology?.” Accessed July 18, 2022. https://www.ibm.com/topics/what-is-blockchain.

Jin, J. and P. Vinella. 2022. “Some of the Challenges Facing DeFi for Mass Adoption.” Working Paper 1. http://bit.ly/3tvt9Y4.

JPMorgan. n.d. “Cutting-edge blockchain solutions to complex business challenges.” https://www.jpmorgan.com/onyx/blockchain-launch.htm.

JPMorgan Chase. n.d. “This $12 Billion Tech Investment Could Disrupt BankingAccessed July 19, 2022. https://www.jpmorganchase.com/news-stories/tech-investment-could-disrupt-banking.

Kraken. n.d. “What Is Centrifuge? (CFG).” Accessed August 22, 2022. https://www.kraken.com/learn/what-is-centrifuge-cfg.

Mims, C. 2021. “Why Artificial Intelligence Isn’t Intelligent.” Wall Street Journal, July 31, 2021. https://www.wsj.com/articles/why-artificial-intelligence-isnt-intelligent-11627704050.

Nicholls, C. 2019. “Open Banking and the Rise of FinTech: Innovative Finance and Functional Regulation.” Banking & Finance Law Review 35, no. 1: 121–151. http://bit.ly/3hJRWoP.

Organisation for Economic Co-operation and Development. 2022. Why Decentralised Finance (DeFi) Matters and the Policy Implications. Paris: OECD Paris. https://www.oecd.org/daf/fin/financial-markets/Why-Decentralised-Finance-DeFi-Matters-and-the-Policy-Implications.pdf.

Patterson, M. 2017. Antitrust Law in the New Economy: Google, Yelp, LIBOR and the Control of Information. Cambridge: Harvard University Press. https://doi.org/10.2307/j.ctvc2rkm6.

Pilkington, M. 2016. “Blockchain Technology: Principles and Applications.” In Research Handbook on Digital Transformations. Edward Elgar Publishing.

Ramos, D. and J.P. Villar. 2018. Competition Issues in the Area of Financial Technology (Fintech). European Parliament. Directorate General for Internal Policies. PE 631.061. www.europarl.europa.eu/RegData/etudes/IDAN/2019/631061/IPOL_IDA(2019)631061_EN.pdf.

Roose, K. 2022. “What Is DeFi?.” New York Times. Accessed July 18, 2022. https://www.nytimes.com/interactive/2022/03/18/technology/what-is-defi-cryptocurrency.html.

Schär, F. 2021. “Decentralized Finance: On Blockchain and Smart Contract Based Financial Markets.” Federal Reserve Bank of St. Louis Review 2: 153–74. https://doi.org/10.20955/r.103.153-74.

Schueffel, P. 2021. “DeFi: Decentralized Finance – An Introduction and Overview.” Journal of Innovation Management 9, no. 3: 1–11. https://doi.org/10.24840/2183-0606_009.003_0001.

Schueffel, P., N. Groeneweg, and R. Baldegger. 2019. The Crypto Encyclopedia: Coins, Tokens and Digital Assets from A to Z. Bern: Growth Publisher.

U.S. Securities and Exchange Commission. 2021. Statement on DeFi Risks, Regulations, and Opportunities. https://www.sec.gov/news/statement/crenshaw-defi-20211109.

The White House. 2021. “The Importance of Competition for the American Economy.” https://www.whitehouse.gov/cea/written-materials/2021/07/09/the-importance-of-competition-for-the-american-economy/#_ftn1.

The White House. 2022. Executive Order on Ensuring Responsible Development of Digital Assets. https://www.whitehouse.gov/briefing-room/presidential-actions/2022/03/09/executive-order-on-ensuring-responsible-development-of-digital-assets/.

World Economic Forum. 2021. Decentralized Finance (DeFi) Policy-Maker Toolkit. In collaboration with the Wharton Blockchain and Digital Asset Project. https://www3.weforum.org/docs/WEF_DeFi_Policy_Maker_Toolkit_2021.pdf.

Yang, Y. 2022. “JPMorgan Finds New Use for Blockchain in Trading and Lending.” Bloomberg, May 26, 2022. https://www.bloomberg.com/news/articles/2022-05-26/jpmorgan-finds-new-use-for-blockchain-in-collateral-settlement.

Zetzsche, D., D. Arner, and R. Buckley. 2020. “Decentralized Finance.” Journal of Financial Regulation 6: 172–203. https://academic.oup.com/jfr/article/6/2/172/5913239.

This publication was made possible by a grant from the Puentes Consortium. The authors would also like to acknowledge the invaluable contribution and support of Jennifer Rabb, director of the Baker Institute McNair Center for Entrepreneurship and Economic Growth.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.