The U.S. has entered a new economic era based on technological innovation, entrepreneurship, and free market capitalism: High-growth, high-technology firms accounted for more than two-thirds of all U.S. GDP growth over the last decade.1,2

A 2011 report estimated that high-growth, high-tech firms make up around 21% of the economy.3 From 2005 to 2014, the mature subset of these firms grew at an average real annual rate of between 5% and 7%.4 These figures imply that this sector has been contributing more than 1% of U.S. GDP growth, which has averaged just 1.5% over the last decade.

The high-growth, high-tech sector appears about to increase dramatically. With potential double-digit growth from this sector, combined with its ever-greater role in the economy, the U.S. could see 5% GDP growth from this new vanguard of free enterprise. Policy to support this sector could enhance and hasten its rise, or could destroy this new American dream.

The Unmeasured Powerhouse

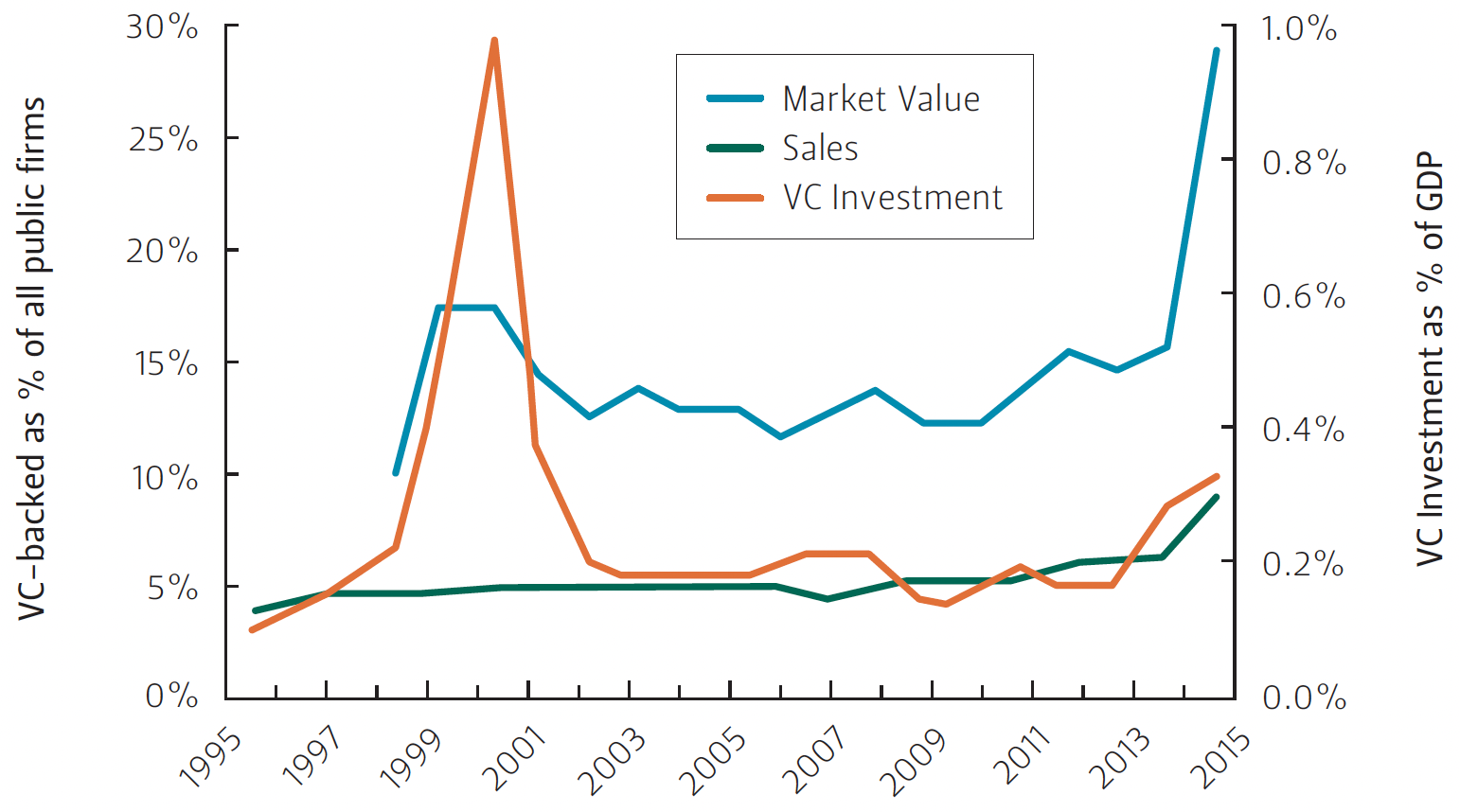

Figure 1 — VC Investment, Sales, and Market Value

The U.S. has the largest and most sophisticated venture capital (VC) industry in the world. In real terms, VC investment doubled from under $30 billion across 3,237 companies in 2002 to over $60 billion across 4,561 companies in 2015.5 It now accounts for around one-third of a percent of U.S. GDP.

But most of the GDP contribution of high-growth, high-tech firms comes after VC investment has ended. There is little public data on this crucial sector. Estimates suggest that it now makes up between 10% and 30% of the economy, and is expanding rapidly.

Explosive Growth

In the last 10 years, high-growth, high-tech firms have dominated U.S. markets for initial public offerings (IPOs) and for acquisitions of private companies; they now account for an average of more than 90% of each market’s value each year.6 This incredible flow of new firms changed the composition of big business. In 2014, 15% of all public market capitalization came from high-growth, high-tech firms; in 2015, it was over 28%. In October 2016, the five largest U. S. firms were Apple, Alphabet (Google), Microsoft, Amazon.com, and Facebook. Every one of these firms was VC backed.7

Enhancing Competition

Large firms are less competitive than they used to be. On average across 13 recorded sectors of the U.S. economy, more than 26% of revenue came from the 50 largest firms in 2012.8 This worrying 4% increase from 1997 prompted calls for anti-trust intervention. But high-growth, high-tech firms are intensely competitive. They disrupt conventional markets, create new products and services, or add new dimensions of competition through platforms. In recent years, platforms have enabled competitive new markets for everything from accommodation to labor, and transport to retail.

Empowering Start-ups

High-growth, high-tech firms rely on different markets for capital, training, partners, labor, and services to serve different parts of their life cycle. Policy to enhance these markets must be tailored appropriately.

At an early stage, start-ups participate in urban entrepreneurship ecosystems. These ecosystems include angel investors, VCs, accelerators, incubators, co-working spaces, and hubs. Firm equity is their currency. One U.S. policy goal should be to increase early-stage capital that competes on the basis of returns to investment.

Changes to the tax code to lower the cost of start-up equity should target only market-based investment; nonmarket investment can do an extraordinary amount of harm. The carried interest revenue procedure applies to partnership agreements used in alternative investments, including VC.9 Removing or ameliorating the carried interest revenue procedure from VC would reduce market-based investment in start-up firms.

Supporting Expansion

Supporting later-stage expansion may be even more important than enhancing early-stage growth. Mature high-growth, high-tech firms could flourish if they had more open access to domestic and global markets for capital, talent, and their products.

Acquisitions and initial public offerings provide crucial access to capital for the commercialization of high-growth, high-tech ideas. Exceptions to regulations for high-growth, high-tech firms should be considered as a part of broader regulatory reform in domestic capital markets.

Likewise, high-skill immigration reform, trade policy with strong intellectual property provisions, sector-specific regulation reform, and promotion of STEM education would all help America’s high-growth, high-tech firms achieve and sustain double-digit growth.

Endnotes

1. Research assistance provided by Ben Baldazo, Carlin Cherry, and Avesh Krishna.

2. U.S. GDP and GDP growth from the World Bank.

3. IHS Global Insight, “Venture Impact: The Economic Importance of Venture Capital-Backed Companies to the U.S. Economy,” NVCA, 2011.

4. Data from COMPUSTAT, VentureXpert, and Bureau of Labor Statistics. Sales growth was 5% and market capitalization growth was 7% for publicly traded VC-backed firms.

5. PWC Moneytree.

6. Data from Global New Issues, SDC Mergers & Acquisitions, and VentureXpert. The acquisition market shift came first in 2006; the IPO market followed four years later in 2010.

7. Microsoft received less VC investment than the others. David Marquardt and Technology Venture Investors held just 6.2% of Microsoft’s stock in 1985.

8. Economic Census (1997 and 2012), Census Bureau.

9. Revenue Procedure 93-27, 1993 C.B. 343, clarified by Rev. Proc. 2001-43, 2001-2 C.B. 191, Internal Revenue Service.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.