Executive Summary

The decade 2003-2013 was an exceptional one for Latin America in social terms, but less clearly so in economic terms. Growth slowed down significantly after the exceptional factors that fed the 2003-2007 boom came to an end. The possible unwinding of the super-cycle in commodity prices and, to a lesser extent, of the expansionary monetary policy of the United States, has added new challenges. But the major issue is the need to overcome the poor long-term economic performance that has characterized the region in the post-market reforms period, particularly by adopting active production sector development strategies.

The decade 2003-2013 was, in many ways, an exceptional one for Latin America. No wonder some have referred to it as the “decade of Latin America,” a term that was coined to contrast it to the “lost decade” of the 1980s. The recent period was indeed outstanding in many ways, particularly in social terms. But in economic terms it is harder to argue that it was, as a whole, exceptional. Furthermore, economic conditions are rapidly shifting in the negative direction as part of a process that is global in nature but has, in particular, hit emerging economies in recent years. 2014 will mark the third consecutive year of slow regional economic growth in Latin America.

Significant Social Improvements

In social terms, improvements in human development are the result of a longer-term trend associated with the rapid expansion of social spending since the 1990s. To some extent, these improvements can be characterized as a “democratic dividend,” as they followed the broad-based return to democracy in most Latin American countries. But what was unique in 2003-2013 was the coincidence of this now long-term improvement in human development with one of the most significant advances in poverty reduction in history. The latter was, in turn, associated with the reversal of adverse trends that had been experienced in labor markets and income distribution during the previous two decades.

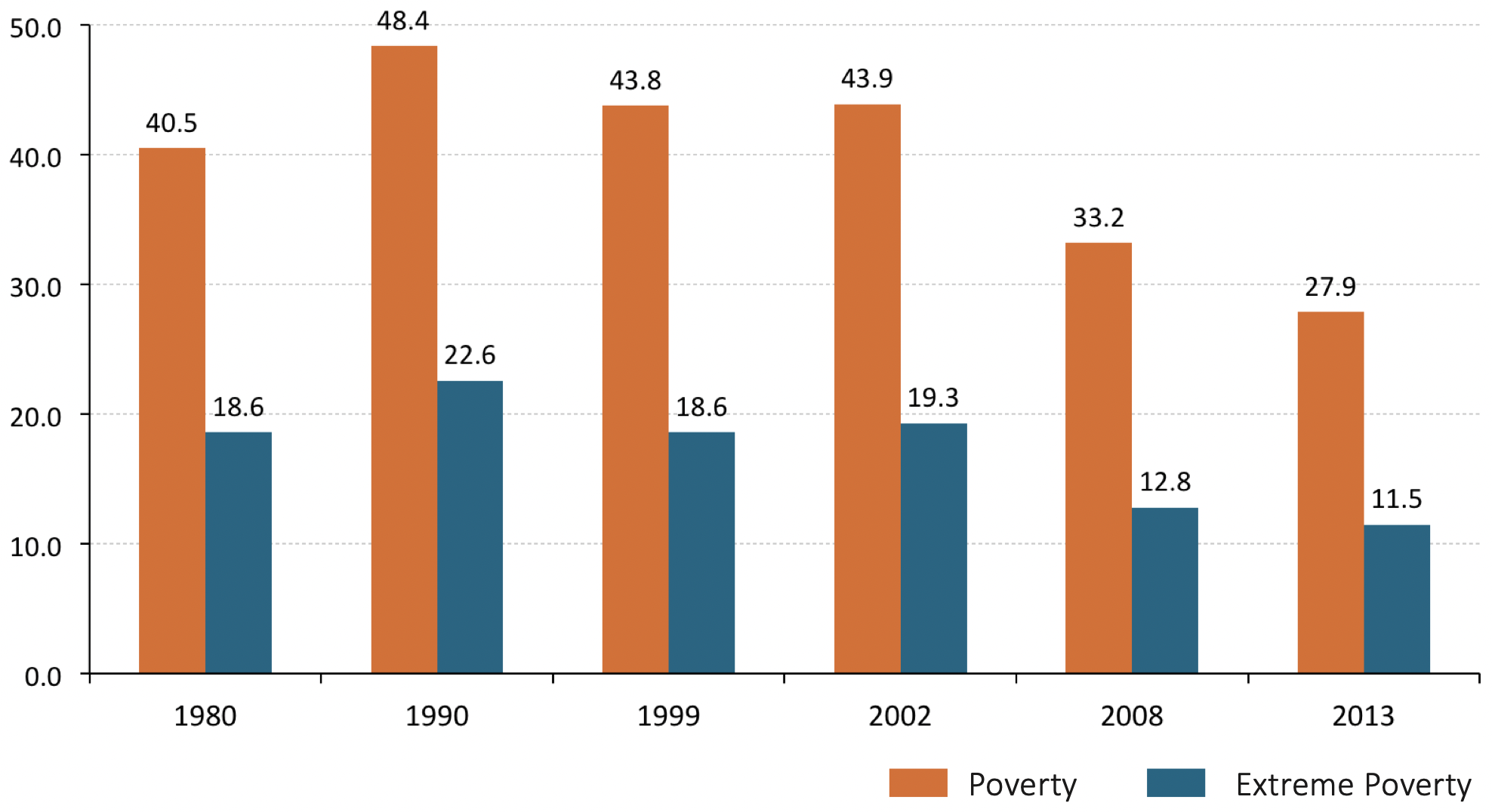

Regional unemployment fell from 11.3 percent in 2003 to 6.2 percent in 2013, according to data from the Economic Commission for Latin America and the Caribbean (ECLAC) and the International Labor Organization (2014). An additional 4.6 percent of the population of working age found jobs, with a growing proportion of them in formal employment. Even more remarkable, given the region’s history, was the reversal of the deterioration in income inequality that had been experienced by most countries in the region during the previous two decades, and that had been the result of the macroeconomic adjustment that took place during the lost decade, the effects of market liberalization, and/or the emerging countries’ crisis that broke out in East Asia in 1997. Indeed, in contrast with the relatively entrenched adverse global pattern, income distribution improved in most Latin American countries in 2003-2013, giving rise to a burgeoning middle class.1 The result of falling inequality with more rapid economic growth was a spectacular reduction in poverty levels. As Figure 1 indicates, 2002 poverty headcount ratios were still above 1980 levels, but then experienced a reduction of 16 percentage points over the next decade. This is unique in Latin American history, and in fact is only matched by the reduction that took place in the 1970s.

Figure 1 — Poverty and Extreme Poverty in Latin America

These improvements must be taken, in any case, with a grain of salt. The significant increase in the coverage of education and health has not been matched by improvements in quality, as the recent discussion of how the region has scored in the OECD’s Programme for International Student Assessment (PISA) tests indicates. Informality still predominates in most countries’ labor markets and income inequality continues to be the highest in the world, together with that of some sub-Saharan African countries. Furthermore, improvements in income inequality and poverty seem to have stagnated in recent years as a result of the slowdown in economic growth.

A More Mixed Economic Panorama

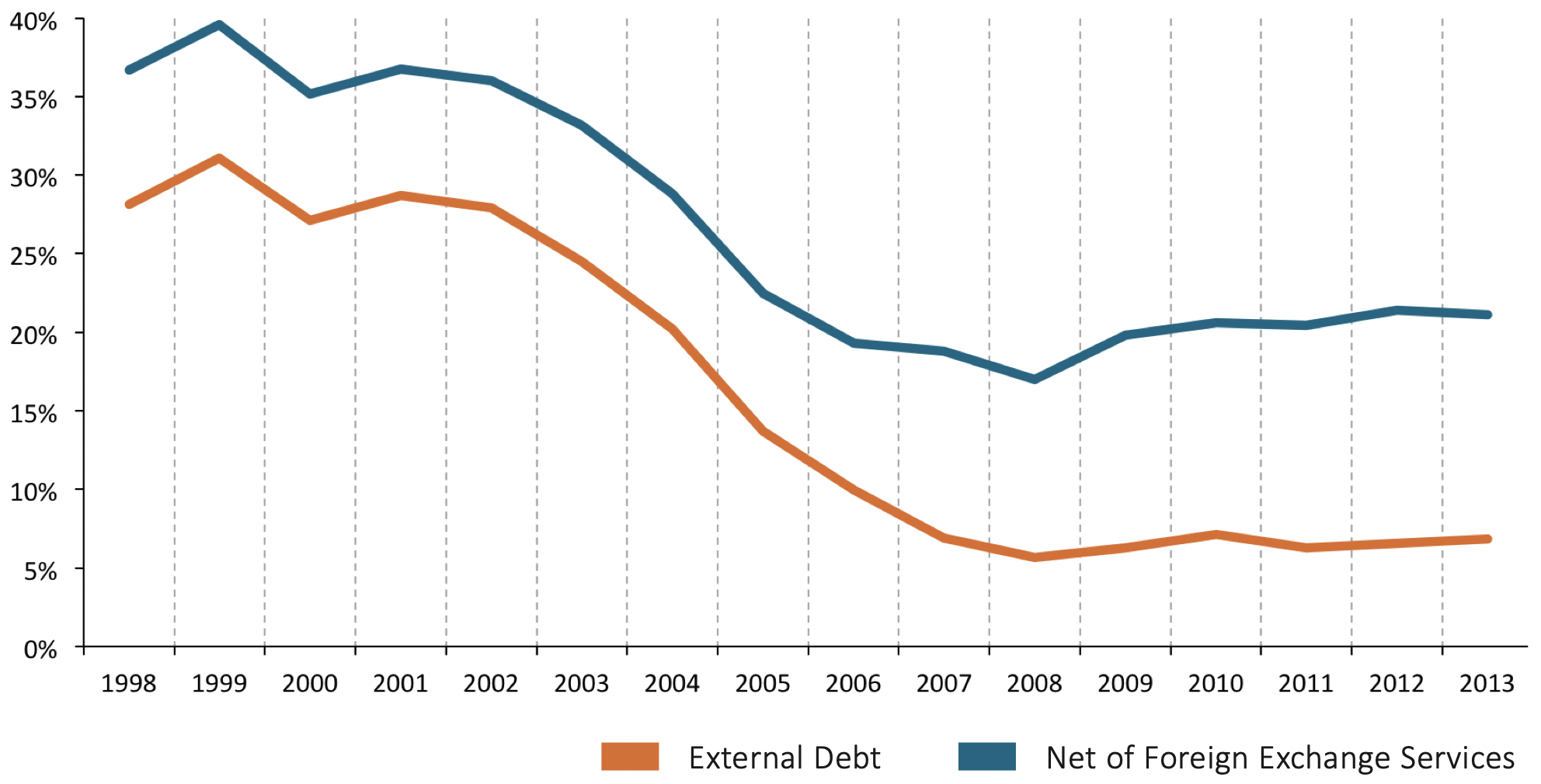

Figure 2 — External Debt as % of GDP at 2000 Parity Exchange Rates

In economic terms, there have also been improvements in many areas. Most countries have now experienced over two decades of low fiscal deficits and over one decade of one-digit inflation rates. The 2003-2007 boom led to a sharp reduction in debt ratios and a massive accumulation of foreign exchange reserves. The result was a reduction in the external debt, net of foreign exchange reserves, from an average of 28.6 percent of GDP in 1998-2002 to 5.7 percent in 2008, a level that has only moderately increased since then (Figure 2). The result has been an extraordinary access to external financing at moderate interest rates since the mid-2000s, only briefly interrupted by the collapse of Lehman Brothers in September 2008 (see below). This allowed the region to manage the 2008-2009 North Atlantic financial crisis2 with an unprecedented room of maneuver to adopt counter-cyclical monetary and credit policies, which were complemented in a few countries by counter-cyclical fiscal policies (Ocampo 2012).

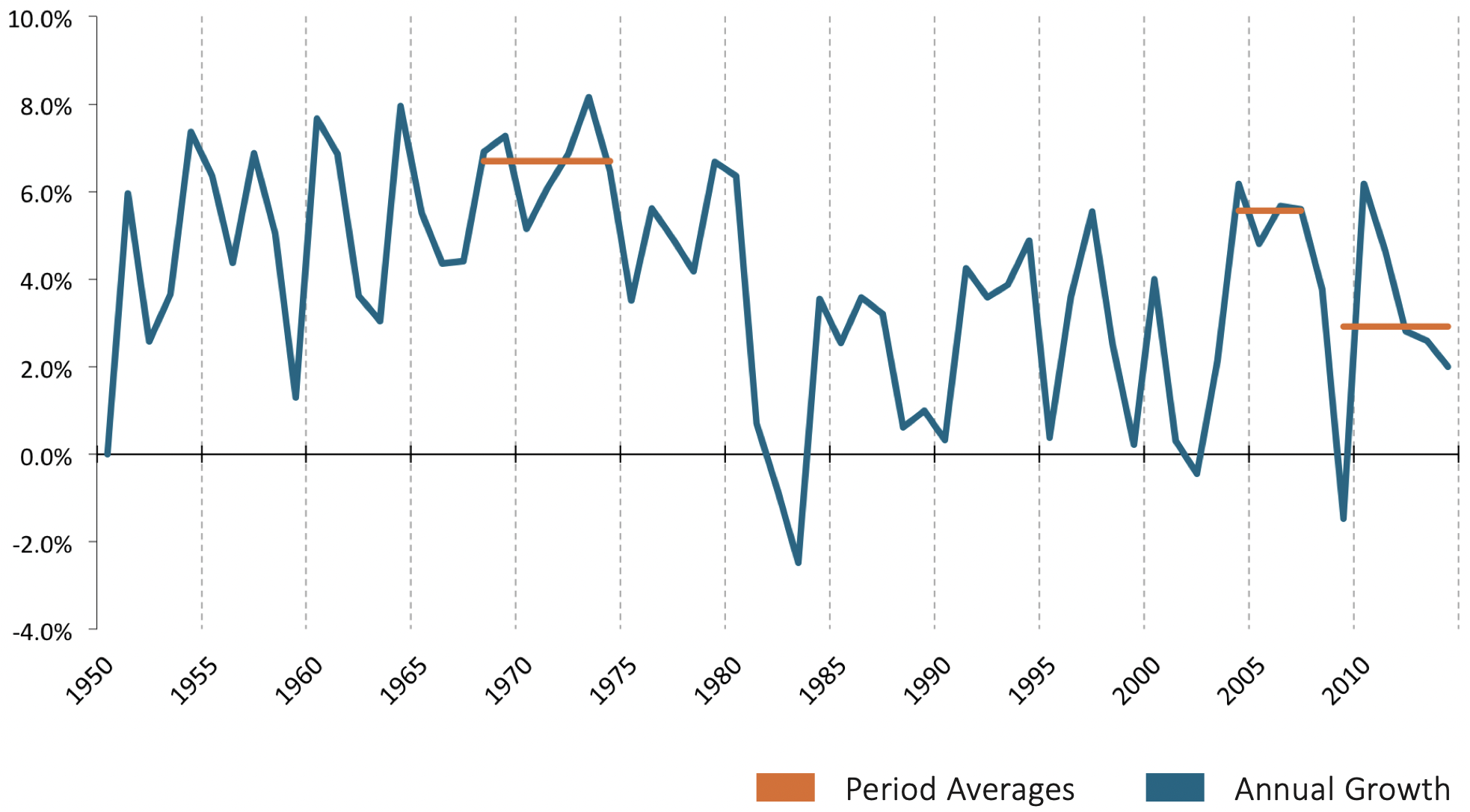

The period 2003-2007 was also, in terms of economic growth, the best experienced by the region since 1967-1974 (Figure 3). Furthermore, in contrast to the 1990-1997 expansion, investment ratios also increased substantially. These have remained high since 2007, at levels that are only slightly below the peak reached in the second half of the 1970s. Indeed, investment ratios are similar to the late 1970s peak if we exclude Brazil and Venezuela, two countries that continue to invest less than was typical at that time. However, the North Atlantic crisis generated a broad-based slowdown and a recession in several countries, notably in Mexico. This was reflected in an overall regional recession in 2009, the worst experienced by the region since 1983. Recovery was very strong in 2010 but followed by a slowdown that has been reflected now in three years consecutive years of slow economic growth. Overall, growth slowed down from an average of 5.6 percent a year in 2003-2007 to 2.9 percent in 2007-2014, slightly below the mediocre 3.3 percent annual growth rate achieved since 1990. So, in a significant sense, we can talk of a “quinquennium of Latin America” (i.e., 2003-2007) rather than of a “Latin American decade.” It should be said, nonetheless, that a few economies did experience an exceptional decade, notably Panama, Peru, and Uruguay, which grew at average annual rates of over 6 percent a year in 2003-2013.

Figure 3 — Latin American GDP Growth, 1950–2014

To take an even more nuanced approach, even in 2003-2007, Latin America grew at a slower rate than the average for the developing world, with the latter reaching 7.4 percent a year according to United Nations data.3 Indeed, the region grew at slower rates than all of the Asian sub-regions, sub-Saharan Africa and the transition economies of Eastern Europe and Central Asia. Latin America only surpassed North Africa by a narrow margin.

An Interpretation of Recent Economic Trends

How can we interpret economic trends over the past decade? Beyond the advances in macroeconomic policies and outcomes, what characterized the period 2003-2007 was the extraordinary coincidence of four positive external factors: (i) migration opportunities (regular and irregular), particularly to the United States and Spain; (ii) booming international trade; (iii) the upward phase of a “super-cycle” of commodity prices; and (iv) broad access to external financing at terms that were the best since the second half of the 1970s. Of these positive conditions, the first two disappeared with the North Atlantic financial crisis, the third is weakening and may soon be over, and the fourth has also weakened but has remained, so far, favorable.

Migration opportunities are, indeed, largely gone. There is now net migration out of Spain and, according to the Pew Hispanic Institute, the number of unauthorized migrants in the United States fell during 2008-2009 and has leveled off since then (Passel et al. 2014). A major effect was the reduction in remittances during the worst years of the crisis, which has been followed by a recovery without yet reaching pre-crisis levels (IDB-MIF 2014).

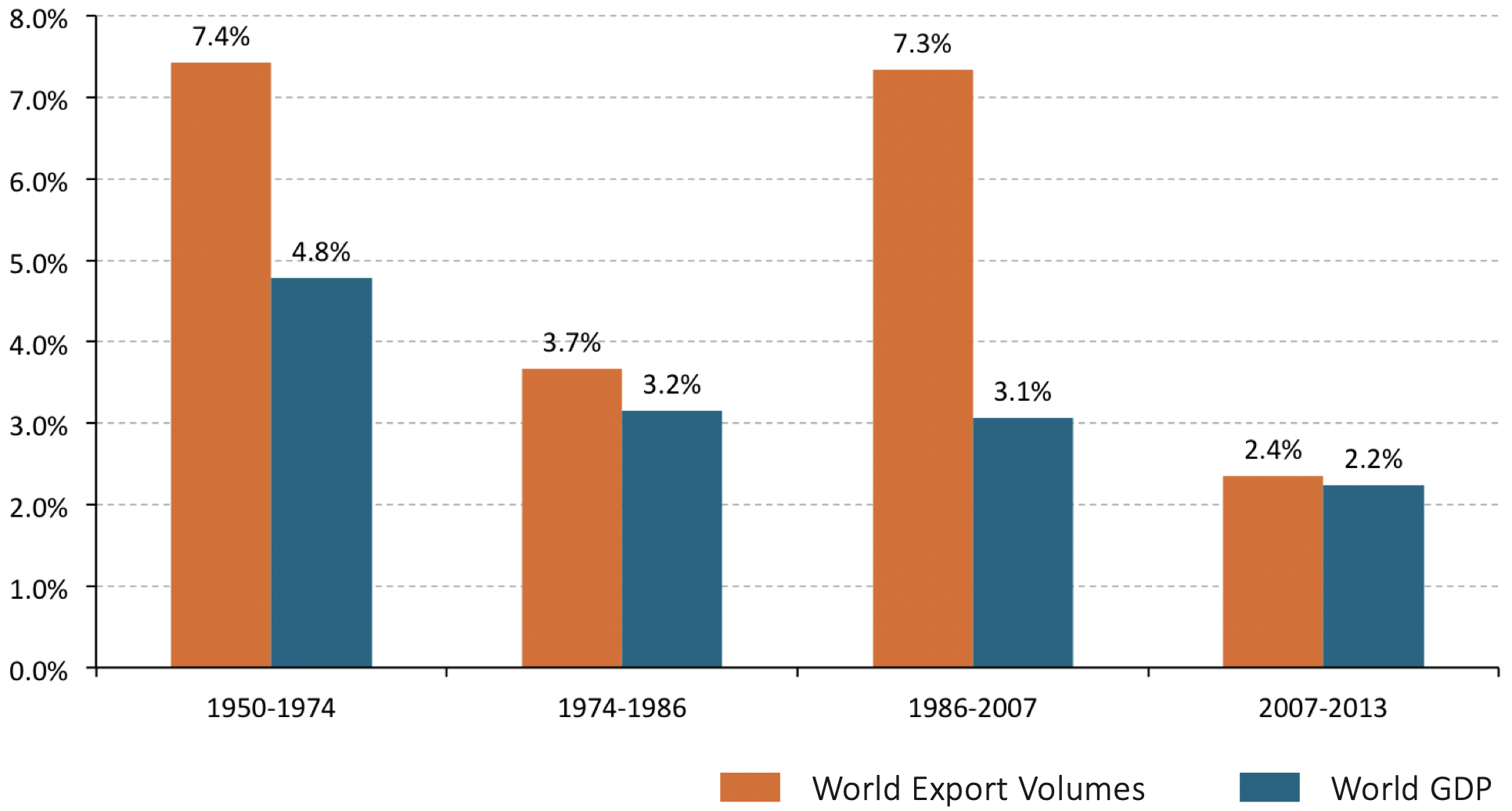

Figure 4 — Growth of World GDP and World Trade Volumes

In turn, international trade experienced a dramatic initial contraction (in fact, the worst peacetime contraction in world history) after the collapse of Lehman Brothers in 2008. Although it recovered fast, international trade has settled since 2011 at a relatively slow rate of growth. The net effect, as Figure 4 shows, is that the world economy has experienced in recent years the slowest rate of growth in world trade since the Second World War. This is not only due to the slower growth of the world economy but also of the lowest elasticity of world trade volumes to GDP (the ratio of the growth rate of trade to that of GDP) of the post-war period.

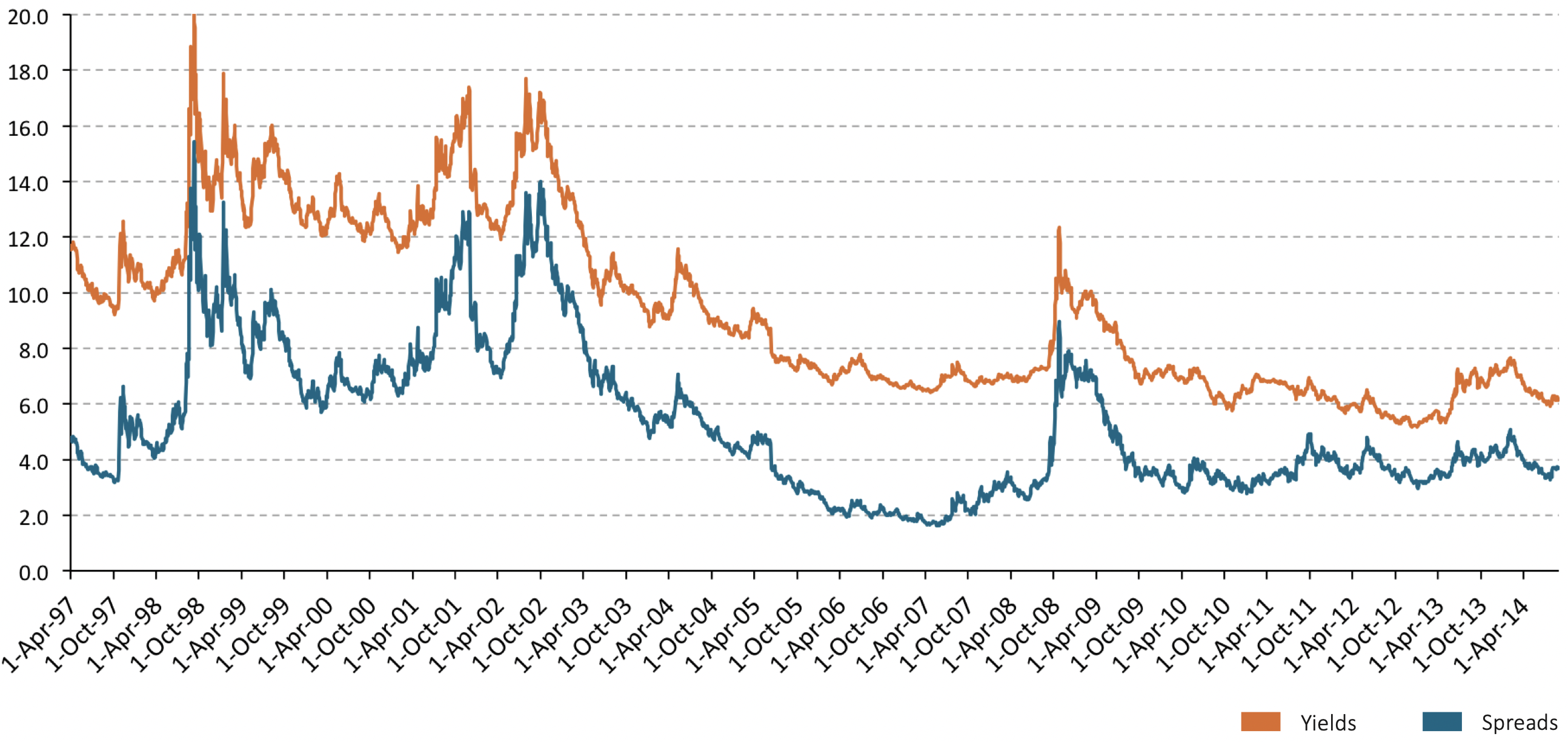

Commodity prices fell rapidly after the Lehman shock but recovered relatively fast. However, after a decade of high prices, commodity prices are likely to fall, following the long-term “super-cycles” (i.e., long-term real price cycles of around 30 years) that they have exhibited in the past (Erten and Ocampo 2013). There are, indeed, signs that this is starting to happen. Commodity prices peaked in 2011 and have fallen moderately since then. This is reflected in the terms of trade of Latin American countries, which are experiencing in 2014 their third consecutive year of deterioration (ECLAC 2014). However, the decline has so far been modest and stronger for minerals and tropical agriculture than for oil and temperate zone agriculture. As we will see below, the risks associated with the winding down of the positive phase of the commodity super-cycle are substantial. This means that, out of the four conditions that fed the 2003-2007 boom, the only one that remains in place is access to external financing. As in the past, external financing continues to be pro-cyclical but the associated cycles have moderated substantially. As Figure 5 shows, the Lehman shock generated a reversal of the very favorable external financing that prevailed prior to the crisis, as reflected in the evolution of risk spreads and total yields of Latin American bonds. But the shock was much more moderate than the one the region experienced after the sequence of the emerging countries’ crisis of the late 1990s.

Figure 5 — Risk Spreads and Yields of Latin American Bonds, April 1997–August 2014

The region was shut out of private capital markets only about a year,4 compared to six years in the late 1990s/early 2000s and eight years during the Latin American debt crisis of the 1980s. Furthermore, the shocks generated by the Euro crisis in 2011-2012 had only minor effects on Latin American risk spreads. In addition, the region was only weakly affected by the Federal Reserve’s gradual tapering of bond purchases, as the stronger initial shock when tapering was announced in May 2013 was partly reversed in 2014.

The strong resilience of Latin American external financing to recent shocks have two interlinked explanations: (i) the relatively low debt ratios that the region has exhibited since the mid-2000s (Figure 2), which make it look like a lower risk relative to the past as well as to other potential destinations of capital flows, and (ii) the high liquidity that characterizes global financial markets due to the expansionary monetary policies of all major developed countries. The latter is likely to continue in the next few years, with only a moderate reversal in the case of the United States.

Going Forward: Short- and Long-term Issues

Overall, this means that the exceptional conditions that facilitated the 2003-2007 Latin America boom have been followed by more mixed external conditions since the North Atlantic financial crisis. Two of the favorable factors—migration opportunities and rapid growth of international trade—are over, and will continue to be so in the foreseeable future. A third, the favorable phase of a super-cycle of commodity prices, has started to weaken. Thus, only a fourth, good access to capital markets, continues firmly in place, although it is also likely to moderate as U.S. monetary policy becomes less expansionary in the next few years.

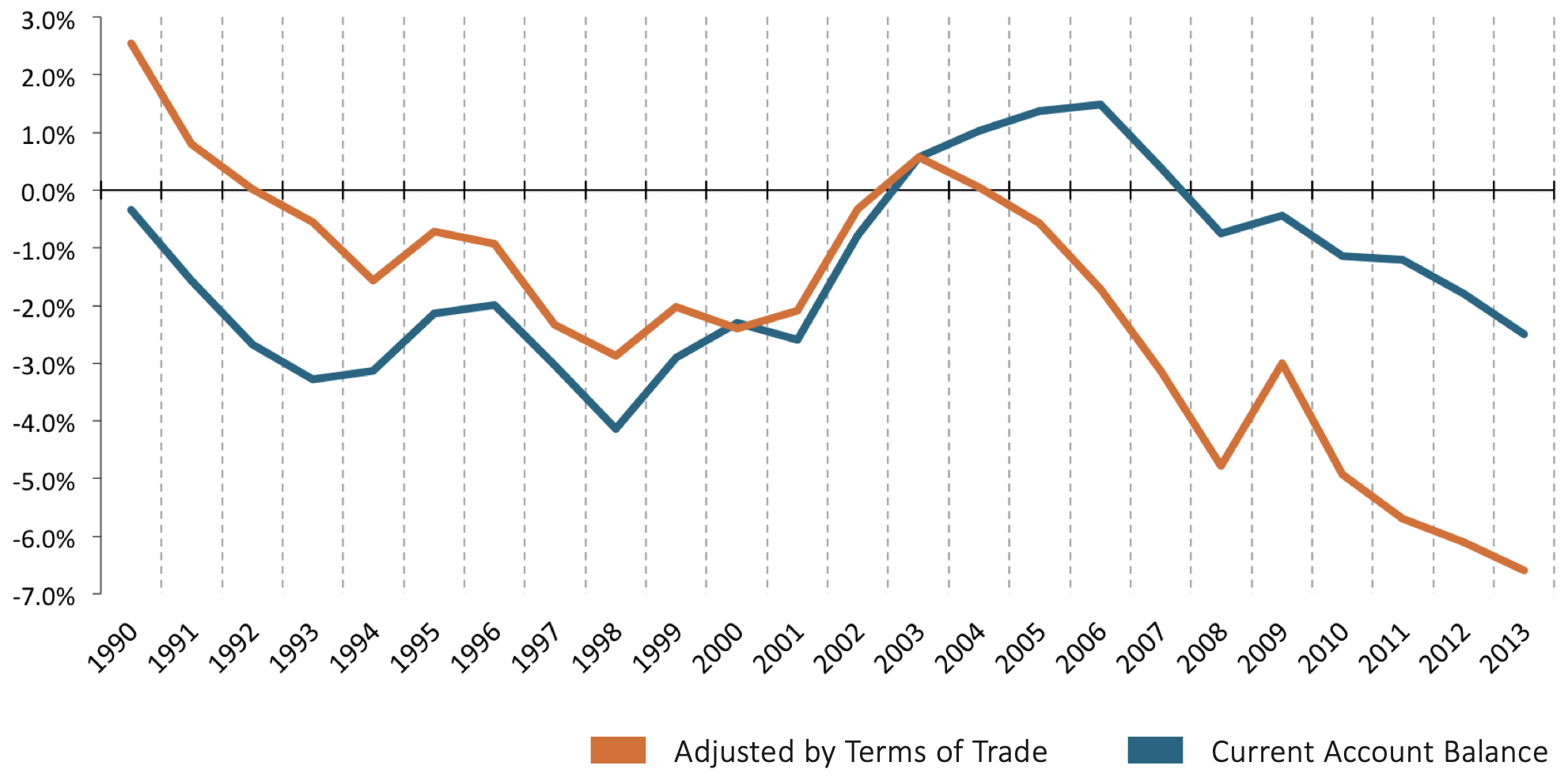

Figure 6 — Current Account Balance as a Proportion of GDP

In the face of changing external conditions, the greatest strength is low external indebtedness mixed with high foreign exchange reserves (strong external balance sheets—see Figure 2 again), as well as the broader perception (a few countries aside) of stronger macroeconomic management than in the past. The greatest risk is the potential current account deficit of the balance of payments associated with the fact that the region has spent and, in fact, overspent the commodity boom.5 Indeed, despite the very favorable terms of trade, the region has been running a current account deficit, which in macroeconomic terms indicates that aggregate spending has surpassed aggregate production. This is reflected in Figure 6, which shows a simple estimate of the current account adjusted by the evolution of the terms of trade (taking the start of the commodity boom, the year 2003, as a reference). One way to understand the estimates in this graph is that the “potential” current account deficit of Latin America (i.e., the current account deficit estimated at 2003 terms of trade) was about 7 percent of GDP in 2013, a situation that is much worse than the deficit estimated at current prices and, particularly, the deficit that prevailed prior to the crisis of the late 1990s according to either of the two estimates.

Beyond that, the basic problem is the slow long-term economic growth that has prevailed since market reforms were put in place two to two-and-a-half decades ago.6 There are several interpretations for this weak performance, but the most important one is that the orthodox export-led model that Latin America adopted during this period—i.e., a model that relied essentially on trade liberalization to generate the signal to specialize according to the comparative advantage of countries—has not proven to be a strong engine of economic growth. By the adjective “orthodox,” I mean that the export-led model followed by Latin America is different from the equally export-led model pursued by rapidly growing East Asian economies, but which exhibits a clear focus on the technological upgrading of the export basket. The Latin American variant was able to deliver, at best, mediocre rates of growth in the region even in the face of the spectacular expansion of world trade that characterized the two decades prior to the North Atlantic financial crisis (Figure 4). As we have seen, growth has only been 3.3 percent a year since 1990.

This is, of course, consistent with the views long espoused by the structuralist tradition that the technological upgrading of the production structure is the key to dynamic growth (see, for example, Ocampo, Rada and Taylor 2009). In export-led models, this means that the technological upgrading of the export basket is the key to success. This may not be confined to manufactures, as it should include the technological upgrading of natural-resource production and the development of modern services. This is why I prefer the term “production sector strategies” to the older concept of “industrial policies.”

The problems generated by Latin America’s patterns of specialization in inducing poor growth and productivity performance are now clear.7

The associated problems include a premature de-industrialization and abandonment of production sector policies. The region specialized according to its static comparative advantages in sectors that offered fewer opportunities for diversification and improvements in product quality (Hausmann 2011). The technological gap widened, not only in relation with the dynamic Asian economies, but also with the more developed natural-resource-intensive economies. This is reflected in a lower share of engineering-intensive industries, the meager resources used for research and development, and a near absence of patenting compared to those groups of economies (ECLAC 2012, Ch. II).

There is, therefore, a need to return to more active production sector strategies if the region wants to speed up long-term economic growth. It is true that these policies involve risks of failure and rent seeking—problems that, in any case, are not unique to them. Developing such new activities is a learning process in which “winners” are in a sense created rather than chosen ex ante. The new activities that should be promoted depend on domestic capacities, must be done in close partnership with the private sector, and should have technological upgrading as the central criteria. And they must be supported by competitive exchange rates.

Needless to say, the need for a clear attention on technological upgrading is critical, given the prospects of lack of dynamism of world trade and the evidence that Latin America is ceasing to be a region of abundant low-skilled labor—a fact that is, no doubt, one of the factors contributing to a better income distribution. Given those prospects, three additional ingredients are essential. The first one is the need to link to China, but in a way that overcomes the 19th century pattern that characterizes Latin America’s trade with the Asian giant, under which the region exports a handful of commodities in exchange for an increasingly diversified array of manufactures—a specialization pattern that amply benefits China. The lack of dynamism of world trade and the premium it places on domestic markets create the need for a second ingredient: a new emphasis on the “expanded domestic market” fostered by the Latin America integration process. But this means stopping the political stalemate that currently characterizes integration processes in Latin America and particularly in South America. The third ingredient is overcoming the significant lag in physical infrastructure that the region has accumulated since the debt crisis, as public sector investment remained depressed and public-private partnerships did not deliver as much as expected.

The mix of technological upgrading, significantly diversifying its trade with China, betting on strong integration processes, and heavily investing in physical infrastructure are, therefore, the keys to dynamic long-term growth in Latin America. The region still has far to go.

Endnotes

1. See, for example, Gasparini and Lustig (2011), ECLAC (2013, Part I), World Bank (2013) and Cornia (2014).

2. I prefer this term to “global financial crisis” since, although the crisis had global effects, the financial meltdown concentrated in the United States and Western Europe.

3. This data is published regularly in the UN’s World Economic Situation and Prospects. See the latest data at United Nations (2014).

4. Of course, a few countries have been partly or totally shut from global private capital markets due to external default and debt restructuring (e.g., Argentina) and/or the perception of political risk (e.g., Venezuela). Ecuador belonged to these categories, but has joined in recent years the group of countries with access to private markets.

5. This was already true at the end of the 2003-2007 boom (see Ocampo, 2009) and worsened in later years (Ocampo, 2012). For a detailed analysis, see IMF (2013).

6. The paragraphs that follow borrow from a blog that I published in September 14, 2012, in VoxLacea (http://vox.lacea.org/?q=blog/latam_economic_growth).

7. See in this regard an analysis of productivity performance in Latin America since 1990 in ECLAC (2014), Part II, Ch. III.

References

Cornia, Giovanni Andrea. 2014. “Inequality trends and their determinants: Latin America over the period 1990-2010.” In Falling Inequality in Latin America: Policy Changes and Lessons, Chapter 2. Oxford: Oxford University Press.

Economic Commission for Latin America and the Caribbean (ECLAC). 2012. Cambio estructural para la igualdad: Una visión integrada del desarrollo. Santiago: ECLAC.

ECLAC. 2013. Panorama Social de América Latina 2012. Santiago: ECLAC.

ECLAC. 2014. Estudio económico de América Latina y el Caribe. Santiago: ECLAC. ECLAC and International Labor Organization (ILO). 2014. Coyuntura Laboral en América Latina y el Caribe no. 10, May.

Erten, Bilge and José Antonio Ocampo. 2013. “Super-cycles of commodity prices since the mid-nineteenth century.” World Development 44: 14-30.

Gasparini, Leonardo and Nora Lustig. 2011. “The Rise and Fall of Income Inequality in Latin America.” In The Oxford Handbook of Latin American Economics, edited by José Antonio Ocampo and Jaime Ros, Chapter 27. Oxford: Oxford University Press.

Hausmann, Ricardo. 2011. “Structural Transformation and Economic Growth in Latin America.” In The Oxford Handbook of Latin American Economics, edited by José Antonio Ocampo and Jaime Ros, Chapter 21. Oxford: Oxford University Press.

Interamerican Development Bank, Multilateral Investment Fund (IDB-MIF). 2014. Las remesas a América Latina y el Caribe en 2013: Aún sin alcanzar niveles de pre-crisis. Washington, D.C.: IDB.

International Monetary Fund (IMF). 2013. World Economic and Financial Surveys, Regional Economic Outlook, Western Hemisphere: Time to Rebuild Policy Space, May. Washington, D.C.: IMF.

Ocampo, José Antonio. 2009. “Latin America and the Global Financial Crisis.” Cambridge Journal of Economics 33, no. 4 (July): 703-724.

Ocampo, José Antonio. 2012. “How Well has Latin America Fared During the Global Financial Crisis?” In The Global Economic Crisis in Latin America: Impacts and Prospects, edited by Michael Cohen, Chapter 2. Milton Park: Routledge.

Ocampo, José Antonio, Codrina Rada, and Lance Taylor. 2009. Growth and Policy in Developing Countries: A Structuralist Approach. New York: Columbia University Press.

Passel, Jeffrey S., D’Vera Cohn, Jens Manuel Krogstad, and Ana Gonzalez-Barrera. 2014. “As Growth Stalls, Unauthorized Migrant Population becomes More Settled.” Pew Research Center, September. http://www.pewhispanic.org/files/2014/09/2014-09-03_Unauthorized-Final.pdf.

United Nations. 2014. World Economic Situation and Prospects 2014. New York:

United Nations. World Bank. 2013. Economic Mobility and the Rise of the Latin American Middle Class. Washington, D.C.: World Bank.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.