Executive Summary

Our analysis of 10 years of data on the Affordable Care Act (ACA) in Texas reveals that the ACA marketplace has helped significantly reduce the number of uninsured Texans. Key highlights drawn from our research include:

- Texans want and will buy affordable health insurance.

- We have an opportunity to enroll more Texans in ACA marketplace plans.

- Texas policymakers should recognize the value of the ACA and work to maximize its impact.

Introduction

One of the primary goals of the Affordable Care Act (ACA) was to increase access to affordable health insurance for Americans. When the ACA was enacted in 2010, Texas had the highest uninsured rate (23.7%) in the country — 5.6 million people. The Texas Health and Human Services Commission estimated that full implementation of the ACA could cut the uninsured rate in half, with 36% or 2 million people gaining subsidized coverage through the ACA marketplace and 24% or 1.3 million people gaining coverage through Medicaid expansion.

However, Texas did not embrace the ACA as a pathway to provide coverage for its citizens. In fact, the state fought the law at every turn in the early years, filing numerous lawsuits challenging its legality, refusing to support access to ACA marketplace plans through available channels, and declining to expand Medicaid.

Notwithstanding these obstacles, the ACA has benefited Texans, particularly the marketplace, which has enabled over 2 million people to obtain affordable coverage not otherwise available in the state. Our review of 10 years of data shows how the ACA marketplace helped reduce the rate of uninsured Texans by one-quarter, from 23.7% in 2010 to 18% in 2021.

In this brief, we offer key insights on the effectiveness of the ACA in Texas, as well as policy recommendations to help all Texans gain access to affordable health coverage.

What the Data Reveal: ACA Enrollment is on the Rise in Texas

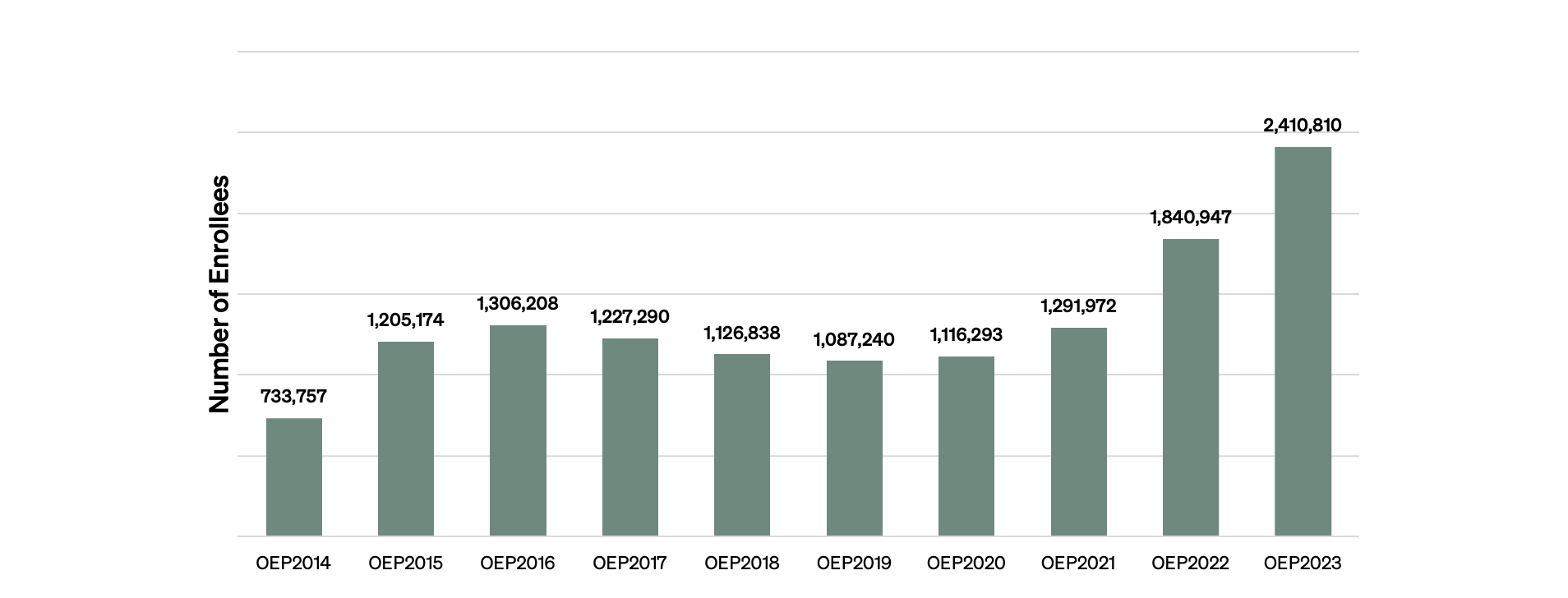

The marketplace holds an annual open enrollment period (OEP) in the latter part of each year to enable Americans — typically those who do not have health insurance through their job, Medicare, Medicaid, or another source — to select and purchase health plans. Figure 1 shows a noticeable increase in ACA enrollment in Texas over the past 10 OEPs with a record enrollment of 2.4 million people in 2023.

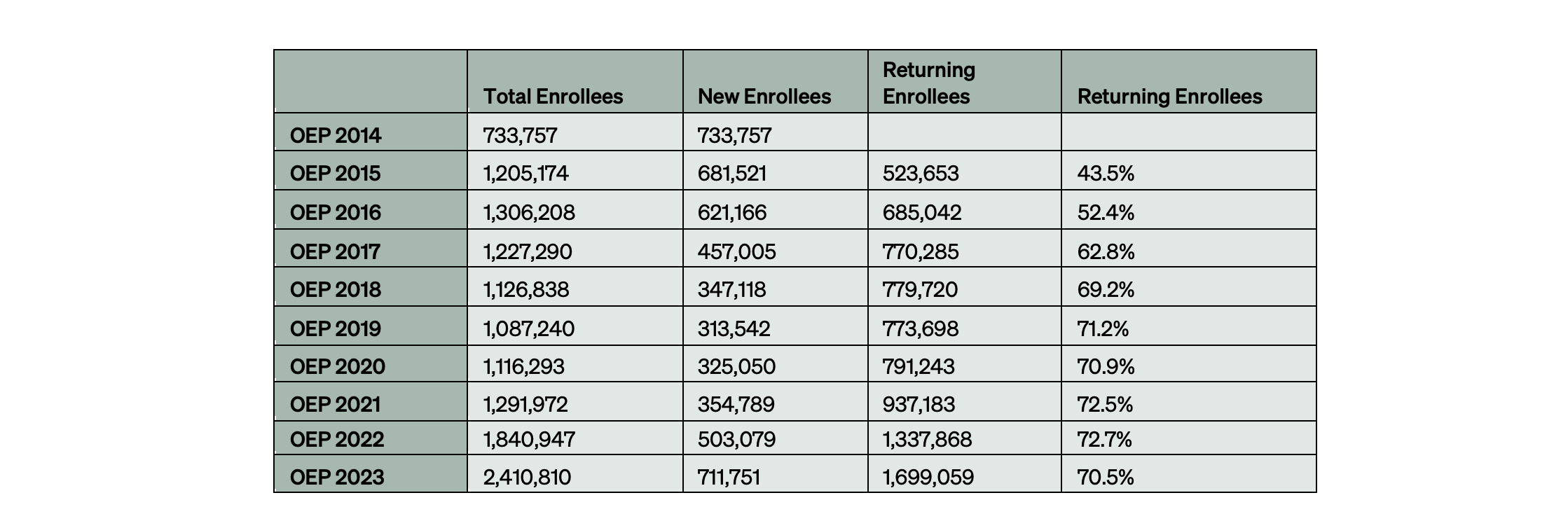

As Table 1 shows, the increase in the Texas ACA enrollee population during the 2023 OEP is largely driven by the growth of returning enrollees. The percentage of enrollees returning to the marketplace year over year has grown steadily from 43% in OEP 2015 to 70% in OEP 2023, even as the total number of enrollees climbed from just over 700,000 in OEP 2014 to over 2 million in OEP 2023, indicating the program’s staying power. Similarly, there is a spike in the number of new consumers in the 2023 OEP compared to previous years.

Figure 1 — Number of Texas ACA Enrollees, OEP 2014–23

Table 1 — New Versus Returning Enrollees, OEP 2014–23

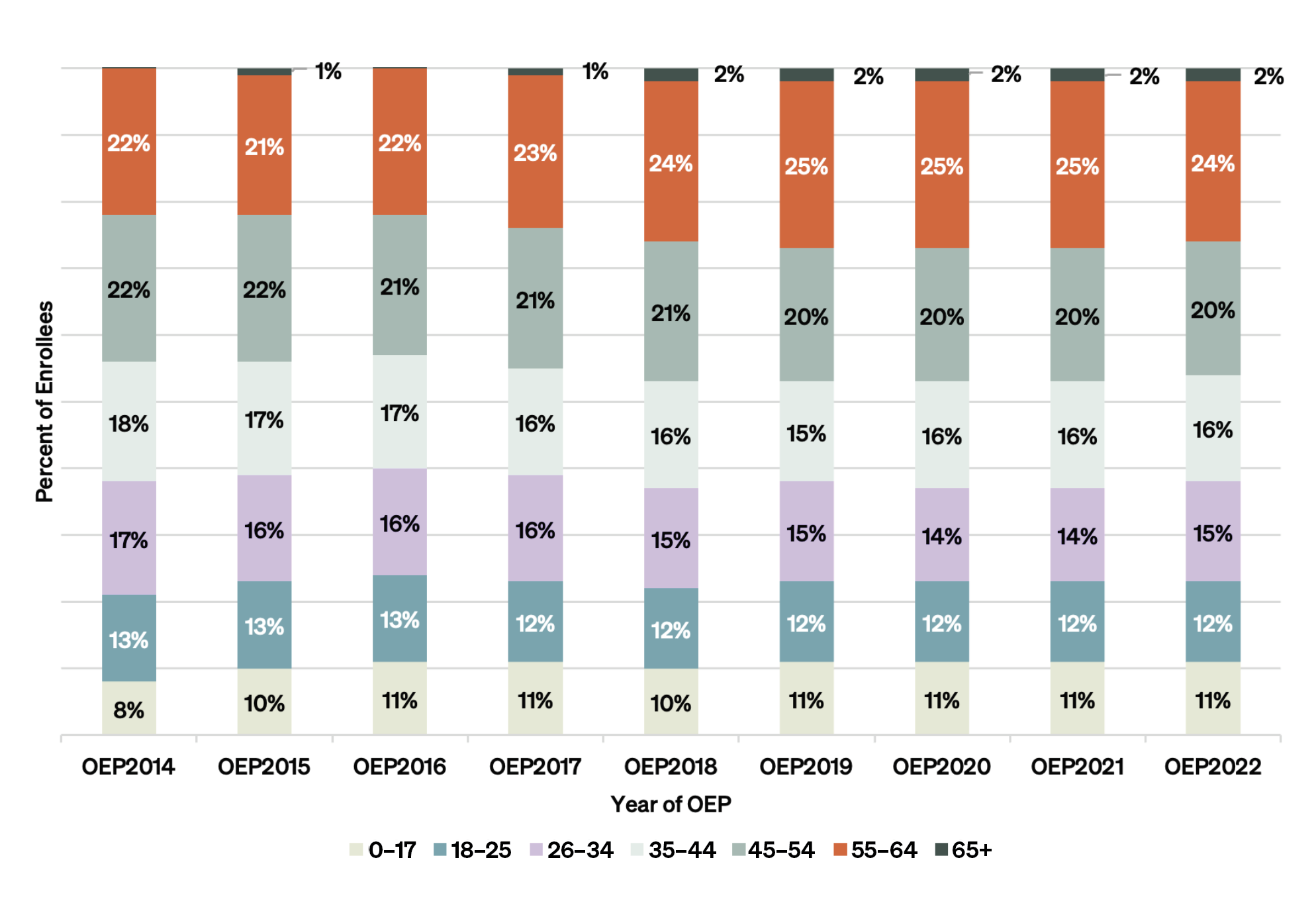

The data also show that adults of all ages have enrolled in marketplace plans. Pre-ACA questions about whether “young invincibles” (i.e., young people who think they are invincible and do not need health insurance) would enroll have been answered — yes.

Additionally, adults 45 and older have consistently comprised nearly half of all enrollees. This likely reflects the ACA’s goal of making health insurance more affordable for middle-aged adults who are often priced out of private markets due to high premiums for older individuals.

Figure 2 — Enrollees by Age, OEP 2014–23

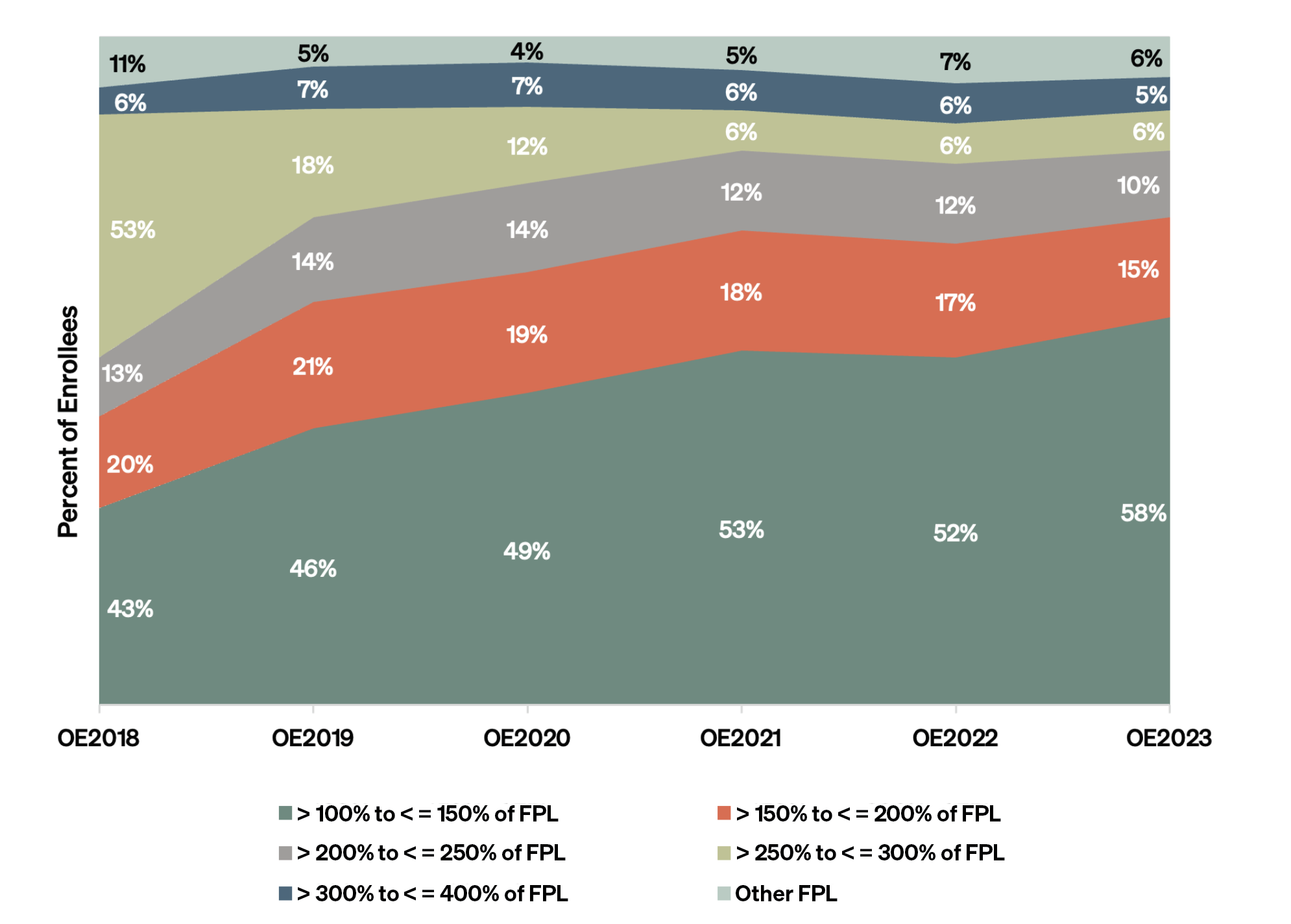

As Figure 3 shows, most enrollees were ranked as having low or moderately low income during OEP 2023. This is consistent with prior years and was anticipated by the ACA, which was specifically intended to help low-income populations afford health insurance. Pandemic-related premium subsidies, as well as the additional cost-sharing reductions for the lowest-income enrollees, likely increased their enrollment in the last two years.

Figure 3 — Enrollees by Income Level, OEP 2018–23

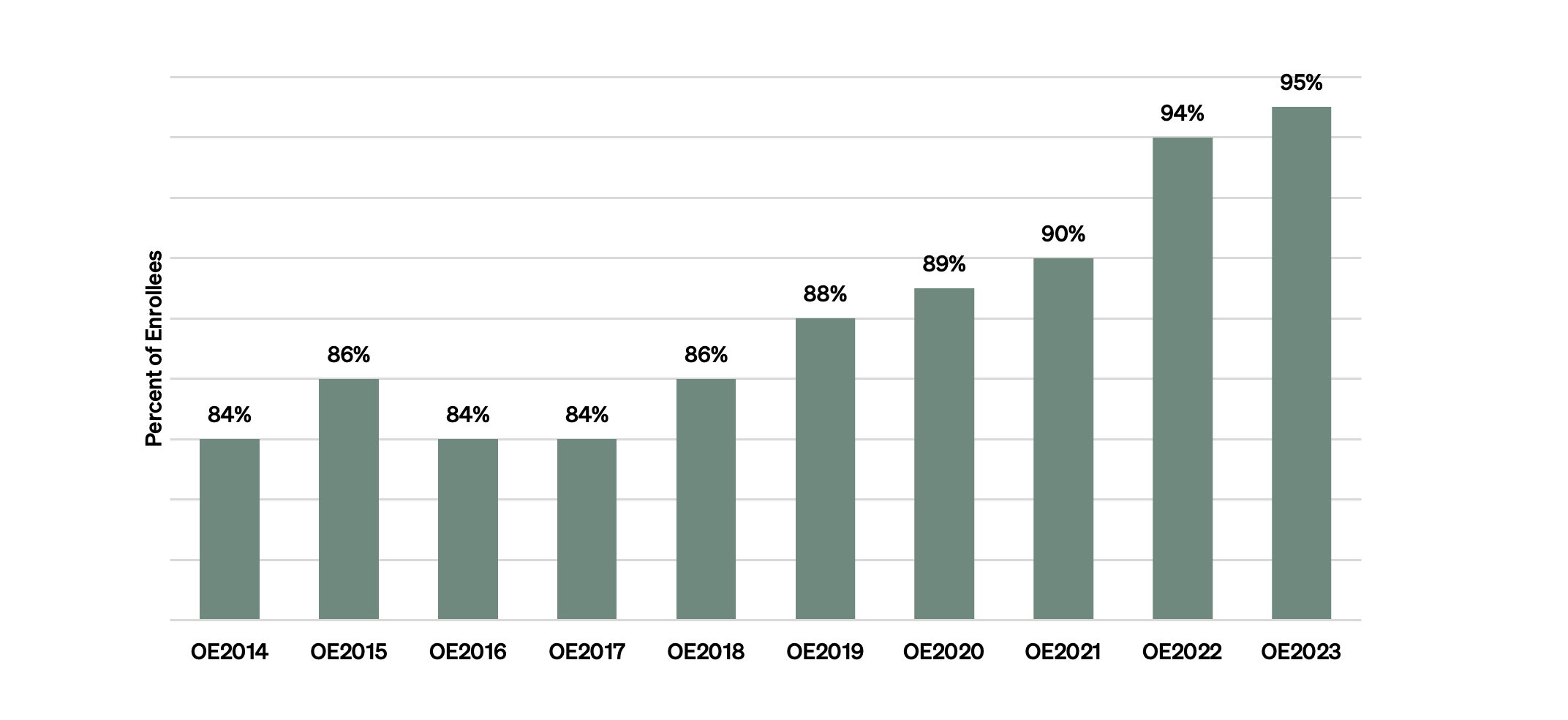

As expected, the vast majority of enrollees received premium subsidies, rising from 83% in 2014 to 95% in 2023, as shown in Figure 4.

Figure 4 — Percent of Enrollees with Premium Subsidies, OEP 2014–23

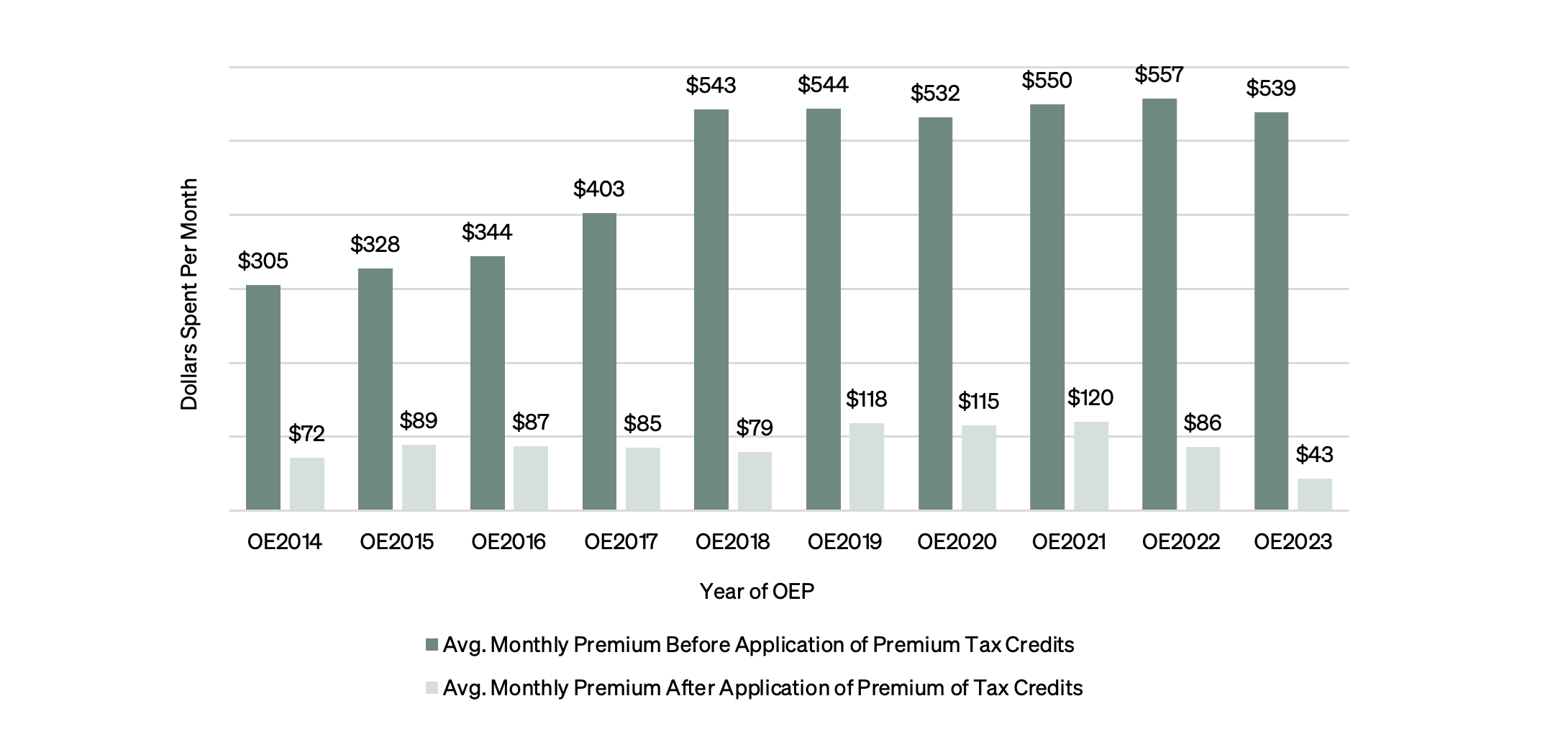

Average premiums rose after the first few years that the marketplace was in effect, as insurers began to understand the usage patterns of these newly insured Texans. Premiums have since stabilized over the last six years. The substantial increase in subsidies in 2022 and 2023 — and the accompanying reductions in premium costs after the subsidies — were due to the American Rescue Plan Act (2021) and the Inflation Reduction Act (2022). Without these pandemic-era laws, it is likely that the subsidized premiums for 2022 and 2023 would have been closer to $115, rather than $86 and $43, respectively.

Figure 5 — Premiums After Subsidies, OEP 2014–23

Conclusions and Policy Recommendations

Texans want and will buy affordable health insurance.

The latest Texas ACA enrollment data in 2023 offers some encouraging news as more than 2.4 million Texans signed up for health coverage in the ACA marketplace, an increase of 30% from the previous year. Our analysis shows that 95% of Texas ACA enrollees received federal tax credits to subsidize their premium costs. In fact, because of federal tax credits, the average cost of premiums for Texas enrollees was only $43 per month. This clearly demonstrates there is a great need for affordable health insurance coverage for low-income Texans. Additionally, nearly three-quarters of the ACA enrollee population were returning customers, year after year, which shows that Texans who enroll in ACA marketplace plans want to keep their affordable health coverage.

We have an opportunity to enroll more Texans in ACA marketplace plans.

As Texas has dropped coverage for nearly 1 million Medicaid enrollees as the federal response to the COVID-19 pandemic winds down, the ACA marketplace may offer affordable coverage for those Texans. As suggested in a recent analysis of Medicaid and marketplace caseload growth, researchers point out that marketplace take-up still has substantial room for growth, especially with the enhanced federal subsidies that will remain available through at least 2025. The state and its community partner agencies should ramp up efforts to help those Texans navigate and select marketplace plans.

Texas policymakers should recognize the value of the ACA and work to maximize its impact.

The noticeable increase in ACA enrollment in Texas has prompted state lawmakers to consider the creation of a state-based marketplace exchange in Texas. This reflects a marked shift among lawmakers in recognizing the ACA as a credible and effective policy tool to address health coverage needs for lower-income Texans. While the merits of this proposal have yet to be fully debated, this marks a change in attitude by lawmakers about the ability of the ACA to solve Texas’ persistently high uninsured rates. Texas continues to experience the highest uninsured rate in the country, and the coverage problem is compounded by the recent removal of 1 million enrollees from Medicaid as the pandemic winds down. The ACA has a lot to offer Texans, and we urge the Legislature to find ways to maximize its impact.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.