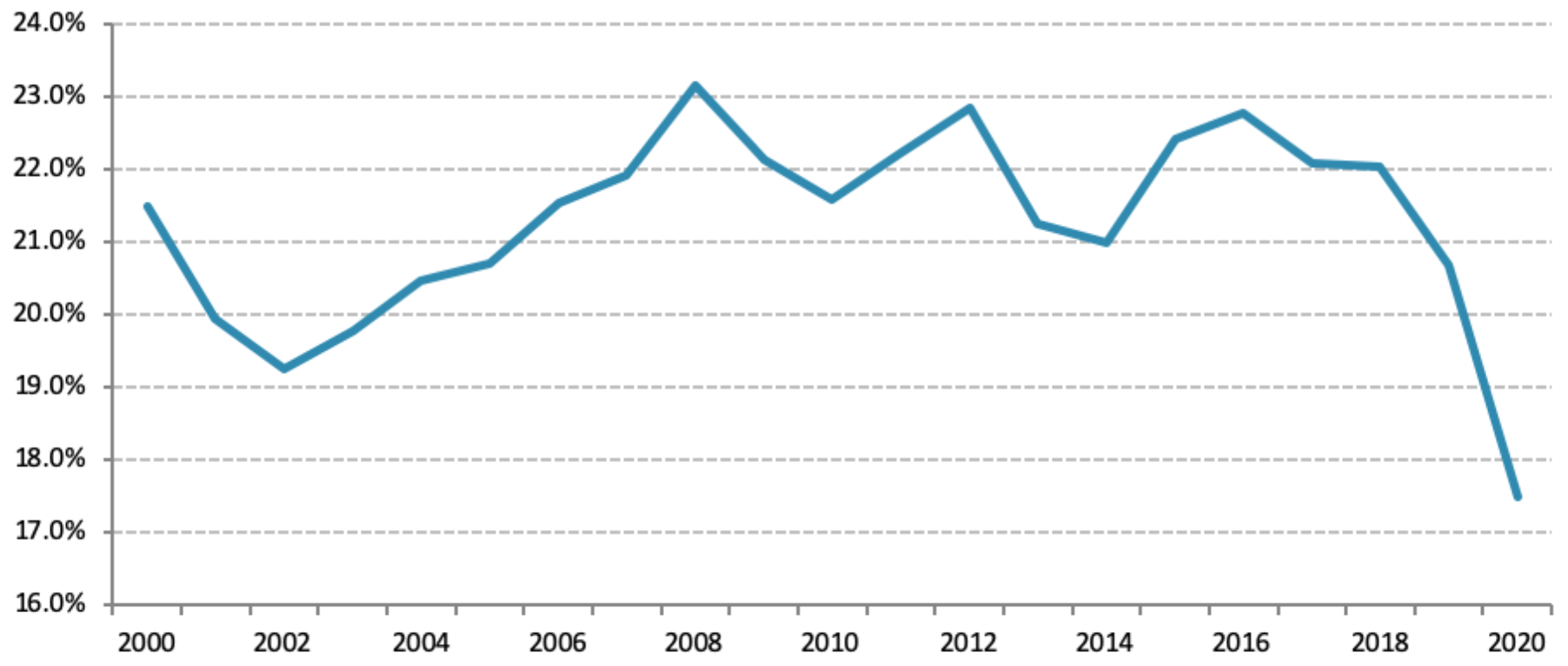

Since Mexican President Andrés Manuel López Obrador began his term in December 2018, the Mexican economy has contracted by approximately 9%,1 the largest economic decline since 1932 (Figure 1). This collapse is primarily due to the government’s inadequate public health strategy in dealing with COVID19 and the absence of an economic stimulus response to address the effects of the pandemic on the country’s gross domestic product (GDP). There is also a persistent public insecurity problem and a growing climate of uncertainty for investors and businesses due to the federal government’s hostile rhetoric and policies toward the private sector. Finally, the political landscape is not encouraging. López Obrador has opted for a strategy of confrontation with the media, opposition parties, several sectors of civil society, and organizations that handle regulatory issues, transparency, and fiscal policy. This political strategy undermines democracy, weakens the rule of law in Mexico, and diminishes the possibility of a stable environment that could lead to economic recovery.

Figure 1 — Mexican GDP Growth Rate, 2000–2020

In 2021, predictions indicate that economic performance will not be enough to recover the ground lost in 2019 and 2020.2 Growth projections are estimated at barely 3.7%.3 At this rate, the recovery could take until 2024 just to reach 2019 economic levels.4

The government is creating massive uncertainty—through both its actions, such as questioning the motives of private actors and changing market norms from one day to the next, and its conspicuous inaction, such as the absence of a strategy to deal with public insecurity and its failure to develop an economic stimulus policy in the face of the pandemic. This uncertainty is almost guaranteed to continue. Consequently, investors, who had little confidence in the government before the pandemic, are even more hesitant to invest in Mexico now. Private investment has been declining since 2018,5 and recovery efforts are also likely to be hindered by the lack of public investment, which has been waning due to the federal government’s austerity policy,6 underspending in the federal budget,7 and low government tax collection.8 Total investment in Mexico has dramatically decreased since 2018 (Figure 2), and this landscape will almost certainly prolong recovery.

Figure 2 — Gross Fixed Investment (as a Percentage of GDP)

The Four Pillars of the Mexican Economy

Faced with this outlook, it is important to examine the four economic pillars that are often credited with bolstering Mexico’s economy in 2019 and 2020. These pillars include the manufacturing sector (especially the automobile sector); remittances, or the money Mexican migrants sent to their families from abroad; the tourism industry, which, despite a notable decrease, continued to be a significant source of income for Mexican citizens; and oil exports from Petróleos Mexicanos (Pemex), Mexico’s state-owned petroleum company. These pillars likely prevented a greater economic contraction during the pandemic and could contribute to recovery efforts in the near-term (from 2022 to 2024). This issue brief looks at each of these pillars, based on the conviction that recovery depends on them.

Manufacturing Sector

Mexico’s economic recovery will depend considerably on the behavior of the manufacturing sector, mainly exports. In recent years, exports from Mexico's manufacturing industry accounted for more than 88% of the nations' total exports.9 Moreover, in the last five years, this sector has contributed on average more than 17% of the GDP each year.10

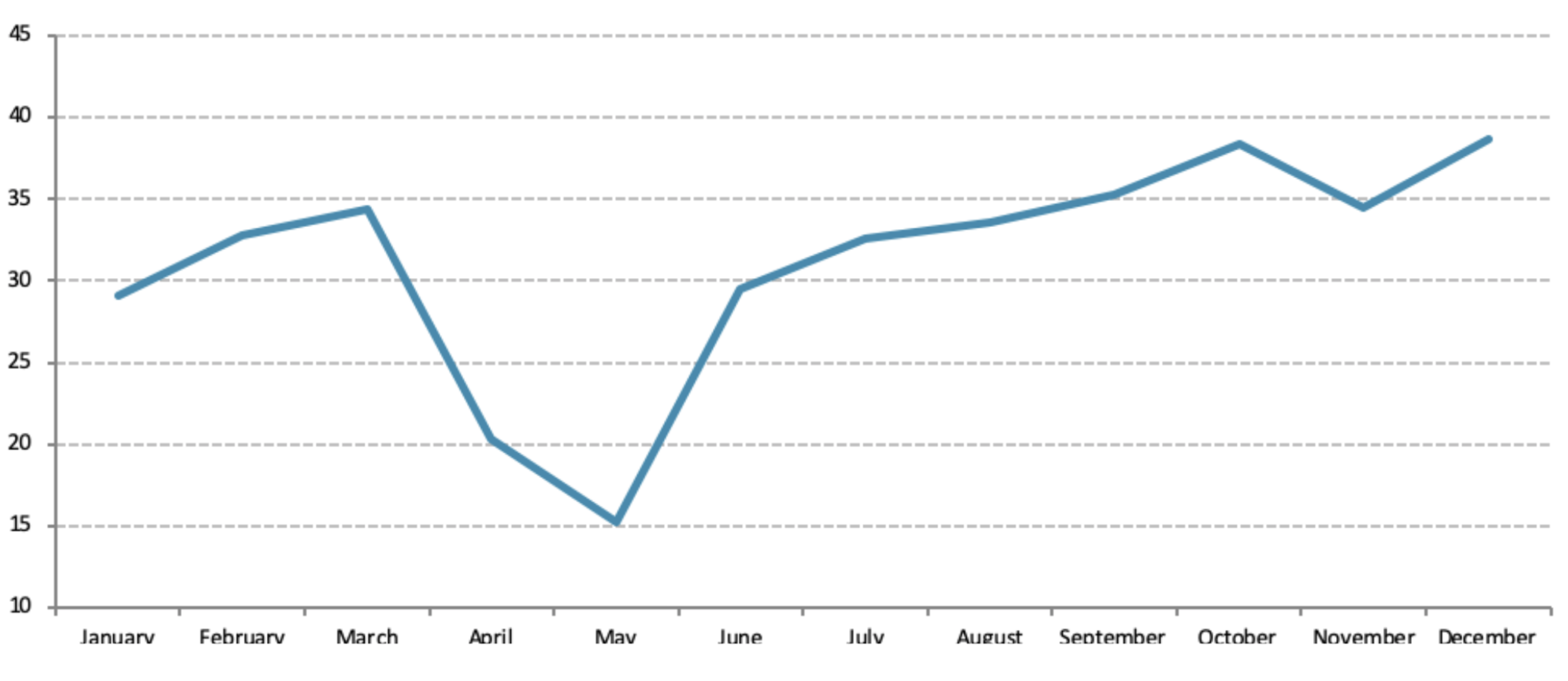

Despite the pandemic and the slump in the U.S. economy (the main market for Mexican exports), the manufacturing sector lost strength only in March and April of 2020, recovering in the following months (Figure 3). Those two months led to a decrease in exports of 8.9% in 2020 compared to 2019 (Figure 4). As the U.S. economy recovers this year, it is expected that Mexican exports will trend upward again, to levels greater than those seen in 2019. This will positively impact the economy. Since exports from this sector are mostly to the United States (more than 80%) and since U.S. manufacturing has recently been recovering, the effects on the Mexican manufacturing sector should be favorable, strengthening Mexico’s economy in the months and years to come.

Figure 3 — Manufacturing Exports in 2020 (Billions of Dollars)

Figure 4 — Manufacturing Exports, 2010–2020 (Billions of Dollars)

Remittances

Remittances have become one of the most important sources of currency and income in Mexico—the second largest behind the manufacturing sector. They support the domestic consumption of many households that receive them—most of them low-income households.

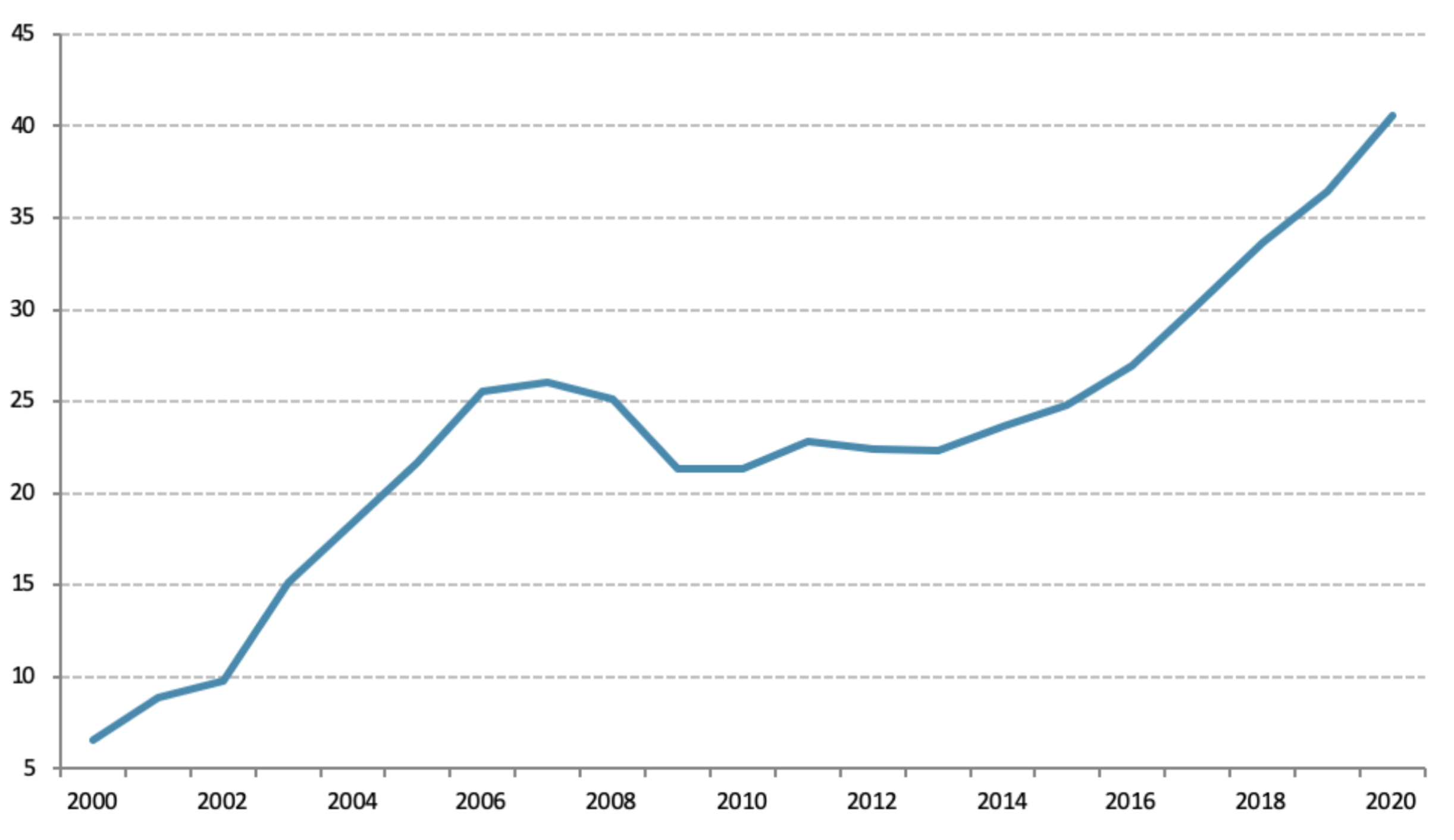

Remittances sent to Mexico have grown exponentially since 2013 (Figure 5), reaching a historic high in 2020, when they were worth $40.6 billion. That meant an increase of 11.4% over 2019 and 82.1% over 2013. This historic high was significantly driven by the fiscal assistance the United States gave its workers, including many Mexican migrants.

Figure 5 — Remittances (Billions of Dollars)

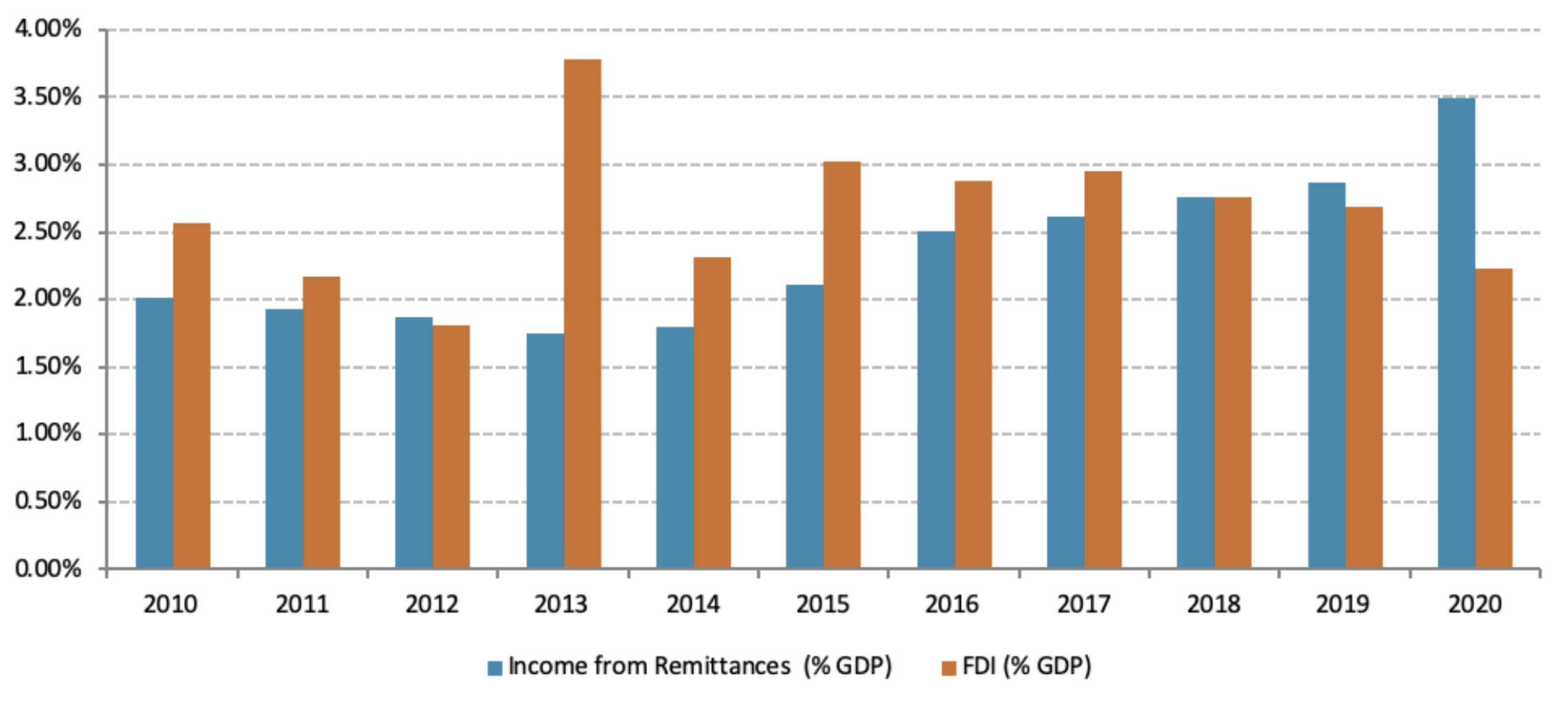

Remittance income as a percentage of GDP in Mexico has also grown considerably since 2013. In 2020, it made up 3.5% of the country’s GDP, a 1.75 percentage point increase over 2013 (Figure 6). The numbers show how important remittances have been to the Mexican economy and why they will be a key factor in boosting Mexico’s economic recovery in 2021.

In fact, remittances have become so important to Mexico that they are as large as the foreign direct investment (FDI) flows the country receives (Figure 6). Whereas remittances have grown in recent years, FDIs have decreased considerably since 2018. In 2020, remittances became the second source of income in the country, only behind the auto industry. FDIs are in third place.

Figure 6 — Income From Remittances and FDIs as a Percentage of Mexico’s GDP, 2010–2020

Tourism

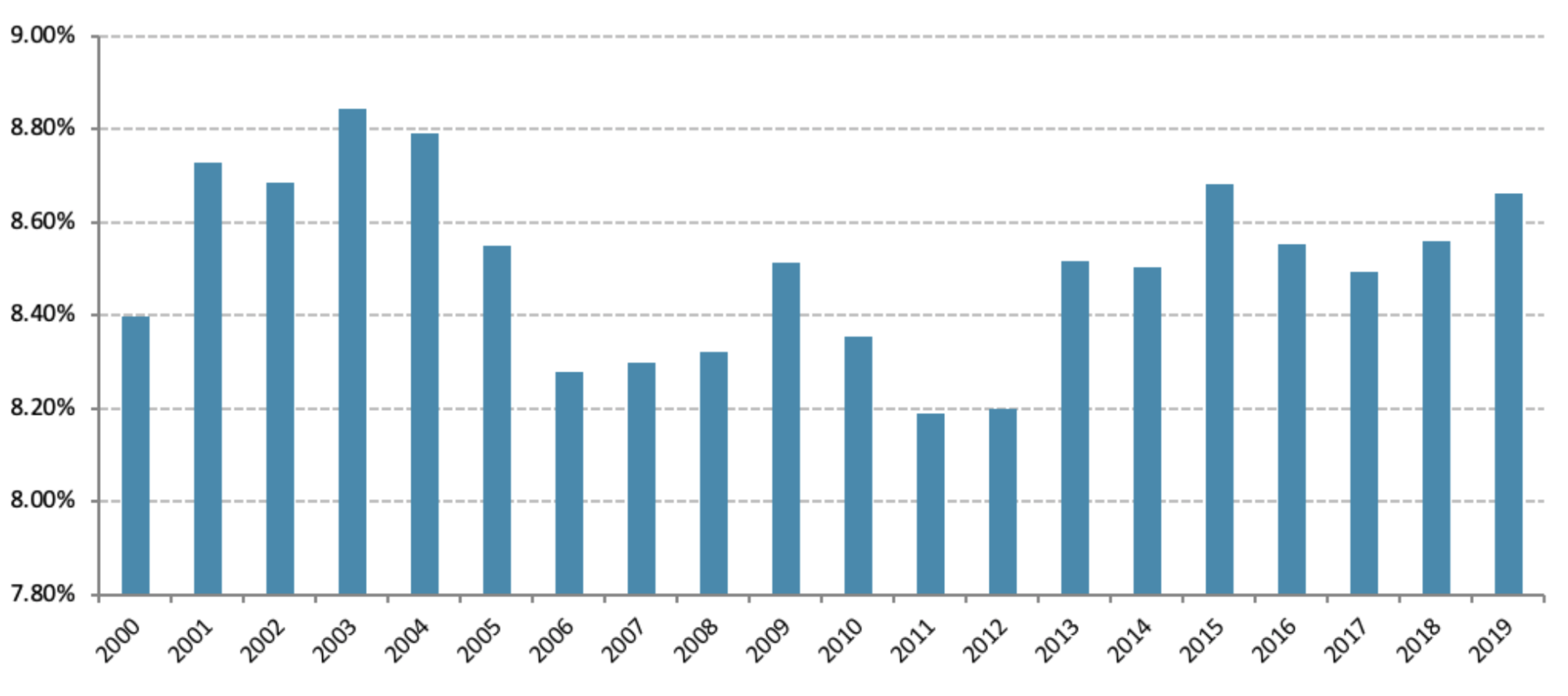

The restrictions placed on non-essential activities to stop the spread of COVID19 have had adverse effects on Mexico’s tourism sector, one of the most important industries for the national economy. In fact, tourism contributed approximately 8.5% to Mexico’s GDP from 2010 to 2019 (Figure 7). Many of Mexico’s tourism services were forced to close down during the pandemic, resulting in the tourism sector contributing less than 5% to the nation’s GDP in 2020.11 For 2021, predictions indicate that the reactivation of this sector will be very slow, and its contribution to GDP will continue to look similar to that of 2020. In the first half of the year, tourism will continue to be limited by national and international travel restrictions. Still, in the second half, this sector might see some improvement, especially as vaccination rates pick up in countries with people who like to vacation in Mexico, such as the United States and Canada. This might lead to restrictions being lifted on travel to Mexico.

Figure 7 — Contribution of Tourism to Total GDP

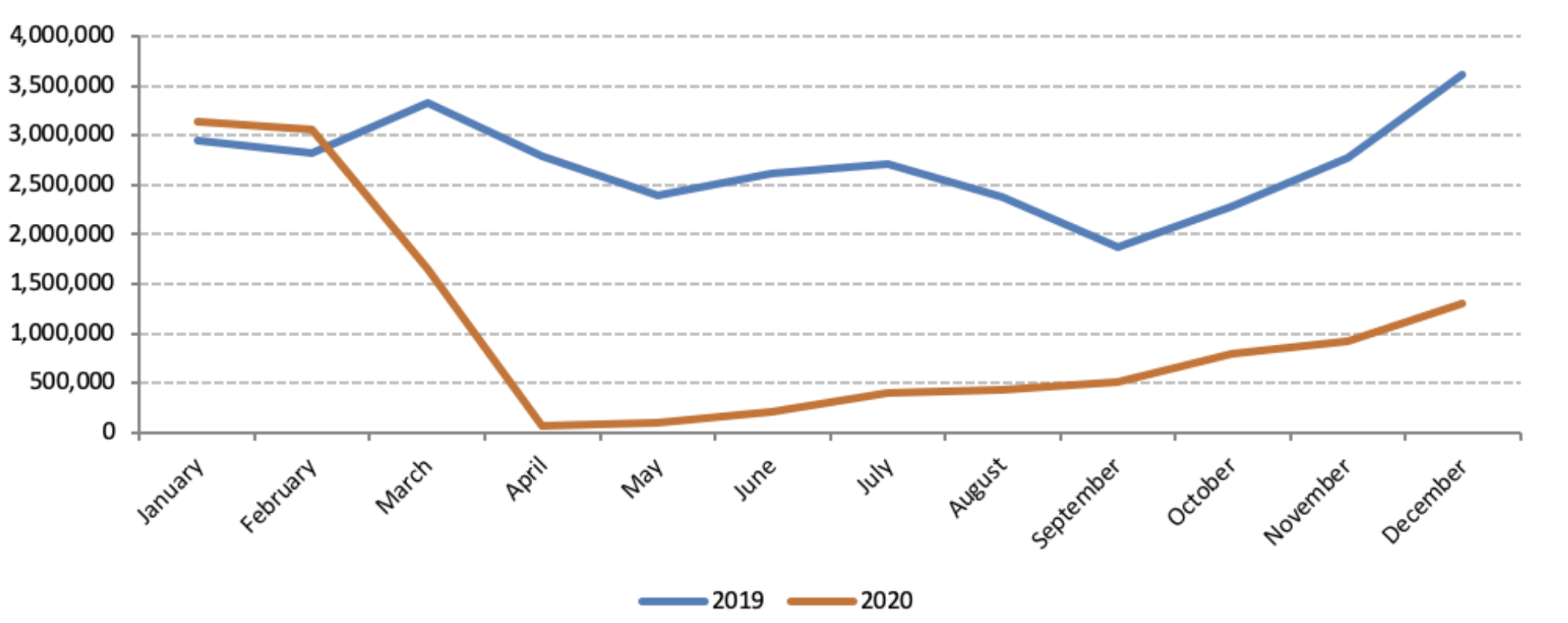

The reduction in tourism has also affected the labor market, since tourism generated 2.3 million jobs (5.5% of the country’s total) in 2019.12 In 2020, no new jobs were created in this sector, and many that already existed were lost. Meanwhile, the decline in tourism has had a negative effect on currency intake from foreign tourists. Before the pandemic, Mexico was the country with the most economic revenue from foreign travelers out of all countries in Latin America and the Caribbean region. In 2020, Mexico lost 19.8 million international travelers, a 61.2% decrease from 2019 figures (Figure 8).13 Last year, the economic revenue from foreign visitors was $9.3 billion, a 56.9% reduction compared to the revenue from 2019. This means that Mexico lost approximately $12.3 billion in revenue in 2020, which will have had an enormous impact on the nation’s economy.14 Since it does not appear that the situation will improve to pre-pandemic levels this year, this sector will continue to have a negative effect on the economy, and recovery will be very slow, taking as many as two to three years.

Figure 8 — Foreign Visitors to Mexico, 2019–2020

Oil and Pemex

In recent years, Pemex has had a detrimental impact on Mexico’s economy. For decades, the state-owned oil company financed the federal government instead of reinvesting the resources it generated, but those days are over. Even so, President López Obrador has counted on the company to generate economic growth through the supposition that oil production could increase. That has not been the case. If we add in the fact that the federal government has heavily subsidized Pemex so that it could continue working as it has been, with no plans for investment or the development of new technology, the results are catastrophic. For one thing, oil production has gone down in recent years, and despite promises from the government, it has not increased at all in the last two years. The government also does not have a strategic business plan to avoid more losses or to refinance the company.

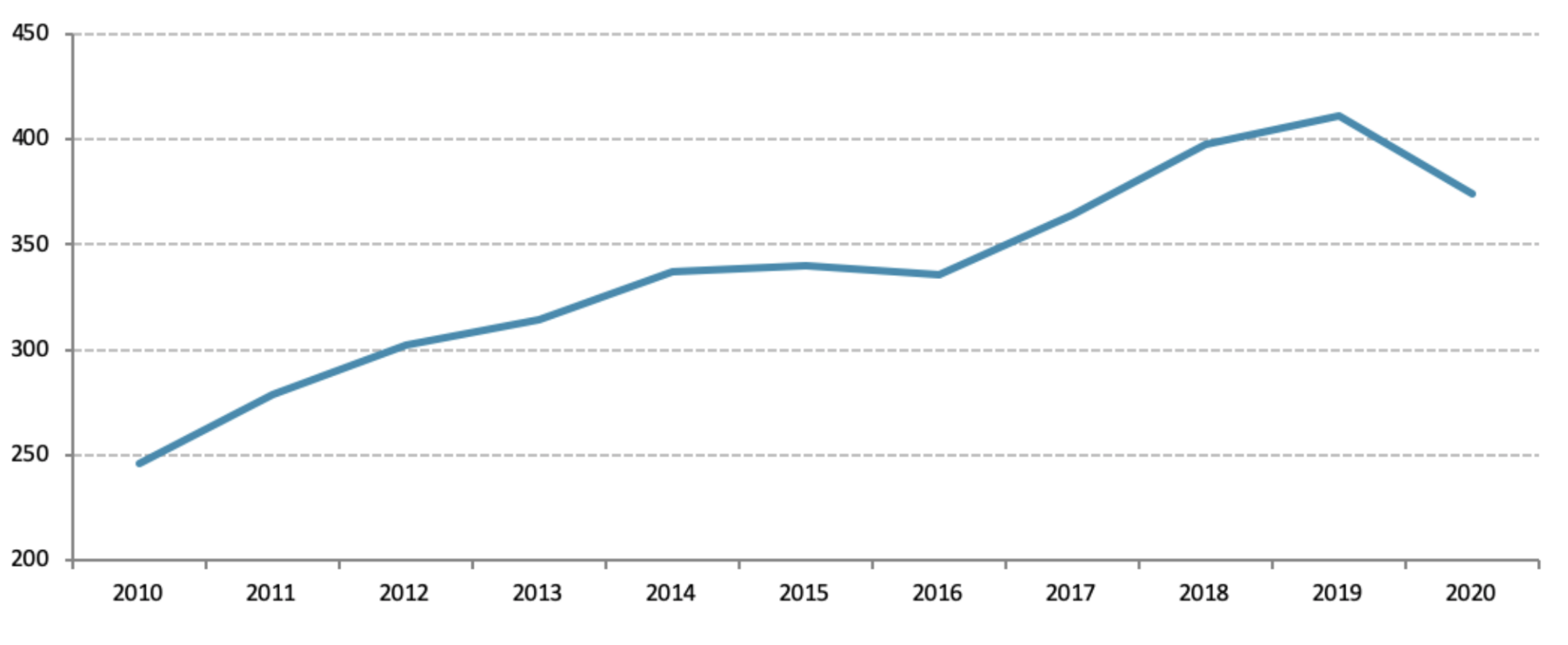

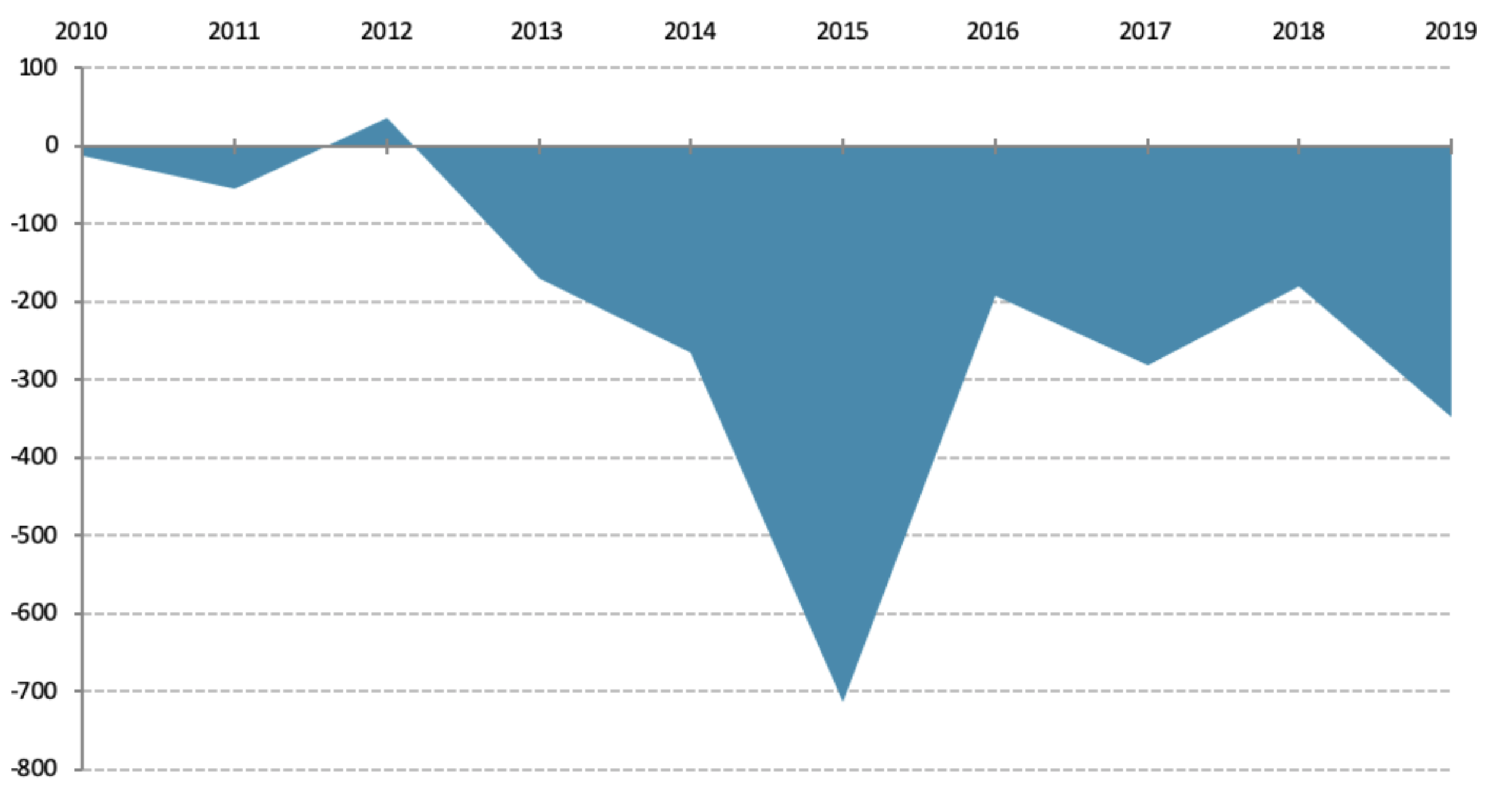

In 2019, Pemex had a net loss of more than 357 billion pesos ($17.4 billion)—more than double the losses from previous years (Figure 9). In 2020, the price war between the world’s main oil producers and the decrease in demand for oil due to the COVID19 crisis led Pemex to face even higher losses. In fact, Pemex generated an accumulated negative net profit of 605 billion pesos ($30.2 billion) for the third quarter last year.15 The net annual loss for 2020 is expected to be the highest in the last decade.

Figure 9 — Net Profits for Pemex (Billions of Pesos)

Thus, the recovery of Mexico’s economy in 2021 depends in large part on the fate of this company. If the federal government continues to financially support Pemex, it will seriously affect both the national economy and its fiscal soundness. Putting resources into Pemex is an inefficient use of money with no positive effects on the economy, since there is no plan to restructure it financially. If these resources were used to support businesses and people affected by the pandemic, the positive impact on the economy would be greater. Still, the economic rescue package for the pandemic has been one of the smallest in Latin America, at 1.1% of GDP.16 It is estimated that support for Pemex in 2021 could cost close to 1.4% of Mexico’s GDP.17 However, supporting Pemex through a profound restructuring would have a cost of between 10 and 12 GDP points.18

Thinking optimistically, Pemex could become an important input for the economy if oil prices went up dramatically, but this would also depend on worldwide recovery. For now, however, it is a drag on the country’s GDP.

Conclusion

The recovery of Mexico’s economy will depend in large part on the four key factors analyzed here. The manufacturing sector and remittances are predicted to have a positive effect in bolstering economic recovery. Mexico’s manufacturing sector will likely improve greatly due to the greater dynamism of the U.S. market and the reestablishment of exports from this sector. Remittances will also be a key factor in the economic recovery. Since their expansion has been consistent since 2013, this year it is expected that they will reach a new historic high, continuing to drive the country’s growth. Already in January and February 2021, they showed strong growth.19

The reactivation of tourism will depend on how efficiently the COVID-19 vaccine is distributed in Mexico and internationally. If it is handled relatively well, tourists will be able to travel without fear of contagion, and restrictions on certain international travelers will likely be lifted. By the second half of the year, it is therefore expected that this sector will start to be reactivated with greater force.

However, Pemex’s financial situation is predicted to continue to deteriorate,20 especially if it does not undergo a restructuring or take on partnerships with the private sector. Because of this, the company will likely contribute to Mexico’s weakening finances in 2021. Pemex is the factor that could have the greatest negative repercussions on the economy—although it will depend in part on the ups and downs of the international market.

At the same time, economic recovery must not rest on these four pillars alone. It should begin with a radical shift in the way the López Obrador administration makes decisions. Yet, changes are unlikely to come any time soon, given López Obrador’s overriding ideological orientation. Unfortunately, this means Mexico’s president will probably continue to make political decisions that will lead to market uncertainty and a much more sluggish and difficult recovery.

Endnotes

1. Jesus Cañas and Chloe Smith, “Mexico’s Economy Shows Signs of Improvement,” Federal Reserve Bank of Dallas, September 23, 2020, https://www.dallasfed.org/research/update/mex/2020/2009.aspx.

2. World Bank Group, Global Economic Perspectives: Latin America and the Caribbean, January 2021, https://pubdocs.worldbank.org/en/515911599838716981/Global-Economic-Prospects-January-2021-Regional-Overview-LAC.pdf.

3. Daniel Zaga, Alessandra Ortiz, and Jesus Leal Trujillo, “Mexico: Rocky road to recovery,” Deloitte Insights, December 21, 2020, https://www2.deloitte.com/us/en/insights/economy/americas/mexico-economic-outlook.html.

4. Arnulfo Rodríguez and Carlos Serrano, “Mexico: The economic recovery will be slow and square root shaped,” BBVA Research, June 19, 2020, https://www.bbvaresearch.com/en/publicaciones/mexico-the-economic-recovery-will-be-slow-and-square-root-shaped/.

5. “Mexico Foreign Direct Investment: 1960-2020 Data, 2021-2023 Forecast,” Trading Economics, https://tradingeconomics.com/mexico/foreign-direct-investment.

6. “Seguirán recortes a gasto de Gobierno en 2021: AMLO,” El Economista, January 4, 2021, https://www.eleconomista.com.mx/politica/Seguiran-recortes-a-gasto-de-Gobierno-en-2021-AMLO-2021-0104-0009.html.

7. Zenyazen Flores, “Subejercicio del Gobierno asciende a 364 mil mdp a octubre; ingresos presupuestarios caen 4.9%,” El Financiero, November 30, 2020, https://www.elfinanciero.com.mx/economia/subejercicio-del-gobierno-asciende-a-364-mil-mdp-a-octubre-ingresos-presupuestarios-caen-4-9/.

8. José Manuel Arteaga, “Tiene México baja recaudación: SAT,” Instituto Mexicano de Contadores Públicos, https://imcp.org.mx/mexico-registra-los-ingresos-tributarios-mas-bajos-de-america-latina-los-cuales-se-ubican-en-9-del-pib-reconocio-el-servicio-de-administracion-tributaria-sat/.

9. Banxico (Banco de México), “Indicators on Merchandise Trade Balance of Mexico,” https://www.banxico.org.mx/SieInternet/consultarDirectorioInternetAction.do?sector=1&idCuadro=CE160&accion=consultarCuadro&l ocale=en.

10. Banxico, “Gross Domestic Product,” https://www.banxico.org.mx/SieInternet/consultarDirectorioInternetAction.do?sector=2&idCuadro=CR201&accion=consultarCuadro &locale=en.

11. Ana M. Lopez, “Mexico: Impact of COVID-19 on the tourism sector 2020,” Statista, August 28, 2020, https://www.statista.com/statistics/1124221/coronavirus-impact-tourism-sector-mexico/.

12. “Resultados de la Cuenta Satélite del Turismo de México 2019 (CSTM),” Secretaria del Turismo y Dataur, 2019, https://www.datatur.sectur.gob.mx/SiteCollectionImages/SitePages/ProductoDestacado3/ CSTM_2019.jpg

13. Unidad de Política Migratoria de la Secretaría de Gobernación, “Boletines Estadísticos: Registro de Entradas, 2020,” http://www.politicamigratoria.gob.mx/es/PoliticaMigratoria/CuadrosBOLETIN?Anual=20 20&Secc=1.

14. INEGI (National Institute of Statistics and Geography), “Encuesta de Turismo de Internación (ETI),” https://www.inegi.org.mx/programas/eti/2018/#Tabulados.

15. Karol García, “Pemex acumula pérdida de 605,176 millones de pesos hasta septiembre,” October 28, 2020, El Economista, https://www.eleconomista.com.mx/empresas/Pemex-acumula-perdida-de-605176-millones-de-pesos-hasta-septiembre---20201028-0061.html.

16. CEPAL (The United Nations Economic Commission for Latin America and the Caribbean), “Enfrentar los efectos cada vez mayores del COVID-19 para una reactivación con igualdad: nuevas proyecciones,” July 15, 2020, https://repositorio.cepal.org/bitstream/handle/11362/45782/4/ S2000471_es.pdf.

17. Guillermo Castañares, “Recuperación de México está sujeta a medidas de apoyo a personas y empresas,” El Finaciero, January 13, 2021, https://www.elfinanciero.com.mx/economia/recuperacion-sujeta-a-medidas-de-apoyo.

18. Fundación de Estudios Financieros, “Análisis Financiero de la Evolución de Pemex, 2009-2019, Evaluación de la posibilidad de un Impacto Sistémico en México,” 2020, https://www.fundef.mx/wp-content/uploads/2021/02/Doc.AnalisisFinancieroPemexFUNDEF.pdf.

19. Juan José Li Ng, “México: Estimaciones del flujo de remesas por entidad federativa para 2021,” BBVA Research, March 1, 2021, https://www.bbvaresearch.com/publicaciones/mexico-estimaciones-del-flujo-de-remesas-por-entidad-federativa-para-2021/.

20. Fitch Ratings, “Petroleos Mexicanos (PEMEX),” Ratings Report, September 21, 2020, https://www.fitchratings.com/research/corporate-finance/petroleos-mexicanos-pemex-21-09-2020.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.