Introduction

As the global economy was struck by shortages and higher prices of ammonia, urea, and other nitrogen fertilizers1 in 2021 (Figure 1), concerns quickly arose regarding crop yields, inflation, and food security. While the impact on food production in 2022 remains to be seen, something that may occur as the harvest season progresses, prices have certainly taken a blow in every corner of the world. The Food Price Index (FFPI) of the Food and Agriculture Organization of the United Nations (FAO), which monitors monthly changes in the international prices of a set basket of food commodities, reached a 10-year high in 2021, indicating that food prices were 28.1% higher than in 2020.2

For many reasons, Mexico is particularly exposed and vulnerable to these events.

The country was once known for its robust ammonia and urea production capabilities, but policy decisions over the past two decades have shattered its ability to manufacture these fertilizers. Instead, current domestic demand for ammonia and urea is for the most part met by imports. For President Andrés Manuel López Obrador, who has declared that Mexico must produce a greater share of the energy and agricultural commodities it consumes, the growing cost of ammonia and urea imports (Figures 2 and 3) may be upsetting. And for now, the reality that the Mexican government should bear in mind as it deploys any new policy is this: local farmers, including those from Mexico’s most marginalized regions, are at the mercy of a complex global context in which high prices of crop nutrients are likely to persist through 2022. In sum, spiking fertilizer prices—if sustained—could mean higher costs to produce crops and/or compel farmers to cut back on fertilizer use, which could have an effect on crop yields and even planted acreage, principally among Mexico’s most vulnerable farmers. And down the line, it could also lead to higher food prices for consumers.

An Uncertain International Context

The production and prices of urea and ammonia, as global commodities, can be affected by numerous factors, including disruptive weather conditions, energy and transportation costs, and supply chain issues. The nexus among these factors has been more than evident over the past year in different parts of the world.3

In the United States, while ammonia plants maintained full operations in 2020, the winter storm that caught Texas by surprise in February 2021 and Hurricane Ida, which struck the coasts of the Gulf of Mexico later in August of that year, negatively impacted the production of ammonia, as half of the U.S. supply is manufactured in the region.4

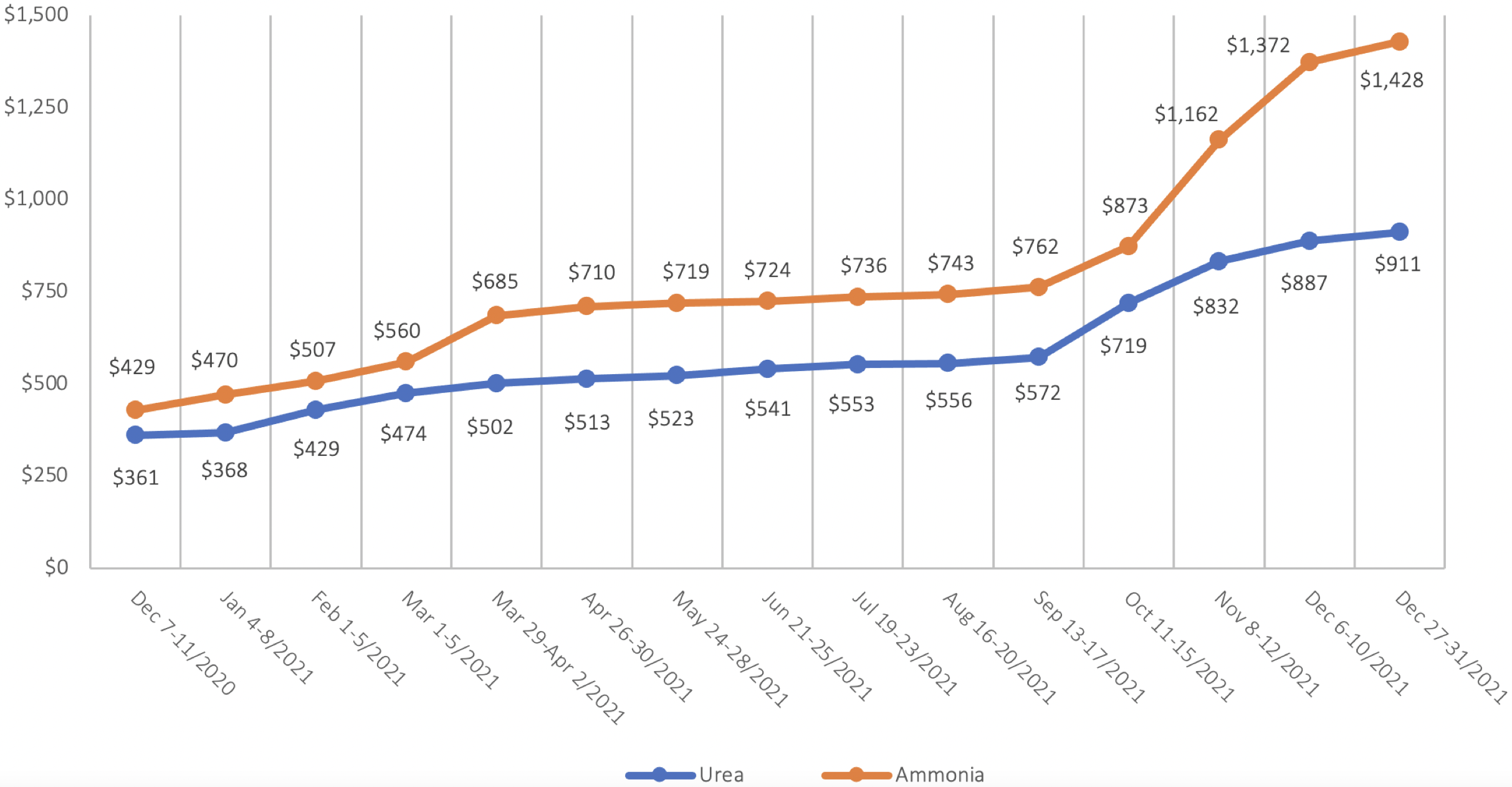

Figure 1 — Prices of Urea and Ammonia in the U.S. Corn Belt, in U.S.$5

In addition to ammonia plants having to shut down operations due to these weather-related factors, the prices of nitrogen fertilizers were also under pressure as the cost of natural gas, which is their primary input, also increased. According to the U.S. Energy Information Administration, the Henry Hub spot price of natural gas (the U.S. benchmark) averaged $3.89 per million British thermal units (MMBtu) in 2021, up from $2.03 per MMBtu in 2020. And on a monthly scale, the price of natural gas stood at $3.79 per MMBtu in December 2021, an increase of 46% from the same month in 2020.6

Largely driven by all of these factors, prices per ton of ammonia in the U.S. Corn Belt escalated sharply, from $429 in December 7–11, 2020, to $1,428 (an all-time high) in the last week of December 2021—a leap of 232.8% in a span of 12 months. Likewise, retail prices of urea skyrocketed through the same period to a record peak: from $361 per ton to $911 per ton (Figure 1).7

In Europe, a slightly more complex phenomenon was observed throughout the urea chain. Natural gas prices—which soared by around 600% in 20218 amid looser COVID-related restrictions and a tight supply from Russia, among other factors that pushed up demand—had reached an all-time-high price of US$42.91 per MMBtu as of December 15.9 This price, which was 11 times higher than in the United States during that month, made the cost of ammonia, the most important raw material in the making of nitrogen fertilizers, climb sharply from US$110 per ton in the summer of 2020 to US$1,000 per ton in November 2021.10 The prohibitive prices of natural gas caused several ammonia and nitrogen fertilizer plants across Europe to curtail production or even cease operations temporarily, further exacerbating supply concerns.

This market uncertainty is likely to linger for most of 2022 because Russia, the world's leading exporter of urea, has imposed export restrictions effective December 2021 through May 2022, with the goal of keeping food and fertilizer prices under control and tackling domestic supply concerns, and China, the world’s second-largest exporter, has suspended shipments of urea abroad until June 2022.11

As such, the prices of urea, ammonia, and other fertilizers12 are projected to remain relatively high during at least the first six months of 2022.13 But, if in addition to Russia’s and China’s export restrictions, global supply continues to be distressed by rising natural gas prices, adverse weather conditions, trade disputes, and rising shipping costs, among other factors, the high cost of nutrients may linger for longer or worsen.

Moreover, while supply chain bottlenecks triggered by the pandemic are driving inflation increases globally, in 2022 high prices of fertilizers are also anticipated to add pressure to the overall inflation outlook, and more specifically to food prices.14

PEMEX and Import Substitution

Given the international context around the production of fertilizers, global food prices have already hit a 10-year high in 2021, and the odds for the said trend to ease in the short term are thin.15 In fact, along with COVID-19 and its impact on growth rates, inflation is viewed as the largest threat to the world economy, including in developing countries such as Mexico, which registered an inflation rate of 7.36% in 2021—the highest since 2000.16

In effect, for Mexico, in this intricate environment in which numerous factors intertwine, the current prices of ammonia and urea (and other fertilizers) may not only feed into worries concerning food inflation and security and dependency on imports, but also impact vulnerable small local farmers in the country’s poorer regions, whose livelihoods could be shaken by rising fertilizer costs and shortages.

Policymakers have taken notice. Consistent with the president’s intention to hand Petróleos Mexicanos (PEMEX) the mandate to manage all hydrocarbon byproducts to meet domestic demand, the government of López Obrador announced on December 28, 2021, a US$300 million investment aimed at rehabilitating the ammonia and urea plants owned by the company.17 While the specifics of the investment are yet to be disclosed, some skepticism surrounds these plans, as the facilities involved—the Cosoleacaque petrochemical complex (ammonia) and the Pro-Agroindustria plant (urea) in the state of Veracruz—have often dealt with technical and operational complications over the past several years, with an evident impact on production and imports.

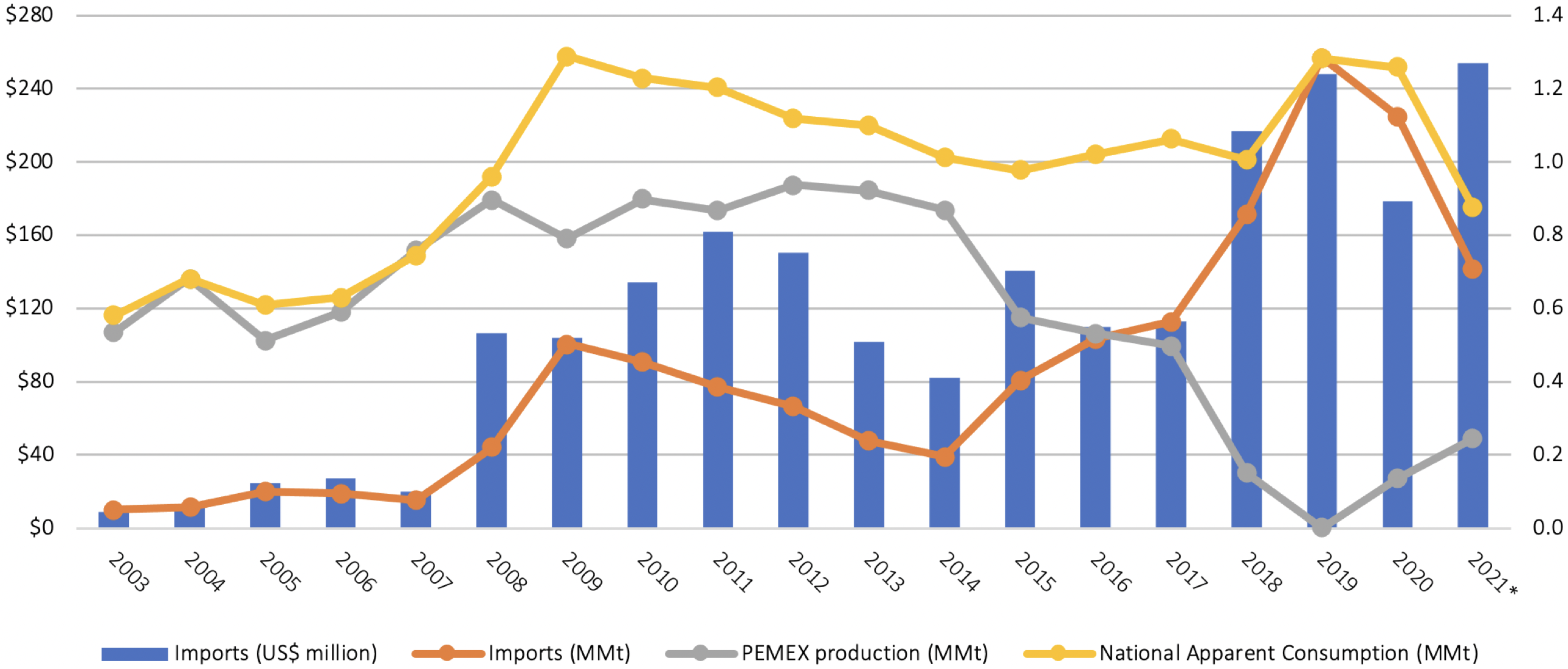

With regard to ammonia, although PEMEX reports an installed yield capacity of 1.44 million tons (MMt),18 the 2019–202119 utilization rate only averaged 8.75%, meaning that production over that period averaged 0.126 MMt per year. The Cosoleacaque petrochemical complex, the sole domestic ammonia producer, hit rock bottom in 2019 since it remained idle for the entire year, which prompted imports to reach an all-time high in terms of tonnage (1.285 MMt) and value (US$248 million) (Figure 2).

Moreover, Figure 2 shows an even more thought-provoking consequence regarding the high-price environment that prevailed in 2021 for ammonia. Even though imports declined from 1.037 MMt in January 2020–November 2020 to 0.709 MMt over the same span of months in 2021, or 31.6%, their value swelled by 57.3%, from $161.4 million to $253.9 million during the same period.20 In other words, price fluctuations in 2021 mean that Mexico paid substantially more dollars for each ton of ammonia sourced abroad. Another implication worth considering is related to apparent consumption, which in 2020 amounted to 1.258 MMt, while in January 2021–November 2021 it stood at 0.877 MMt. Although 2021 values refer to a period of just 11 months, it is evident that local ammonia demand is expected to be lower than during the previous year, suggesting that Mexico’s farmers and other industrial users are poorly supplied and that the cost is too high for farmers to keep up their past levels of fertilizer use. A similar statement is valid in the case of urea.

Urea is Mexico’s top nitrogen fertilizer in terms of consumption21 and its significance is in part attributed to the fact that it sits at the core of a thread of value-adding activities that involves the production of natural gas and ammonia as well as food staples. Despite this importance, urea is one of the blind spots of Mexico's policy concerning PEMEX, as its production continues to be an unresolved issue. Pro-Agroindustria, the urea plant that PEMEX acquired during the previous administration, began production intermittently in April 2020, but it ceased operations in April 2021 due to disruptions in the supply of ammonia.23 Later, in his appearance before the Chamber of Deputies on October 27, 2021, PEMEX CEO Octavio Romero Oropeza alluded to the resumption of urea production at Pro-Agroindustria, but no further details were provided at that time. On December 28, 2021, at the presentation of the $300 million plan mentioned above, Romero Oropeza reported that PEMEX’s monthly urea production was 28,000 tons.24

Figure 2 — Mexico's Consumption of Ammonia, Imports and Production, 2003–202122

However, it is worth noting that databases including those of the National Association of the Chemical Industry (ANIQ), Energy Information System (SIE), and even PEMEX fail to make urea production numbers available. So even though the extent to which domestic demand depends on PEMEX production is an unknown number, the fact that Pro-Agroindustria frequently shuts down operations indicates that the tonnage of urea sourced abroad still meets most domestic demand.

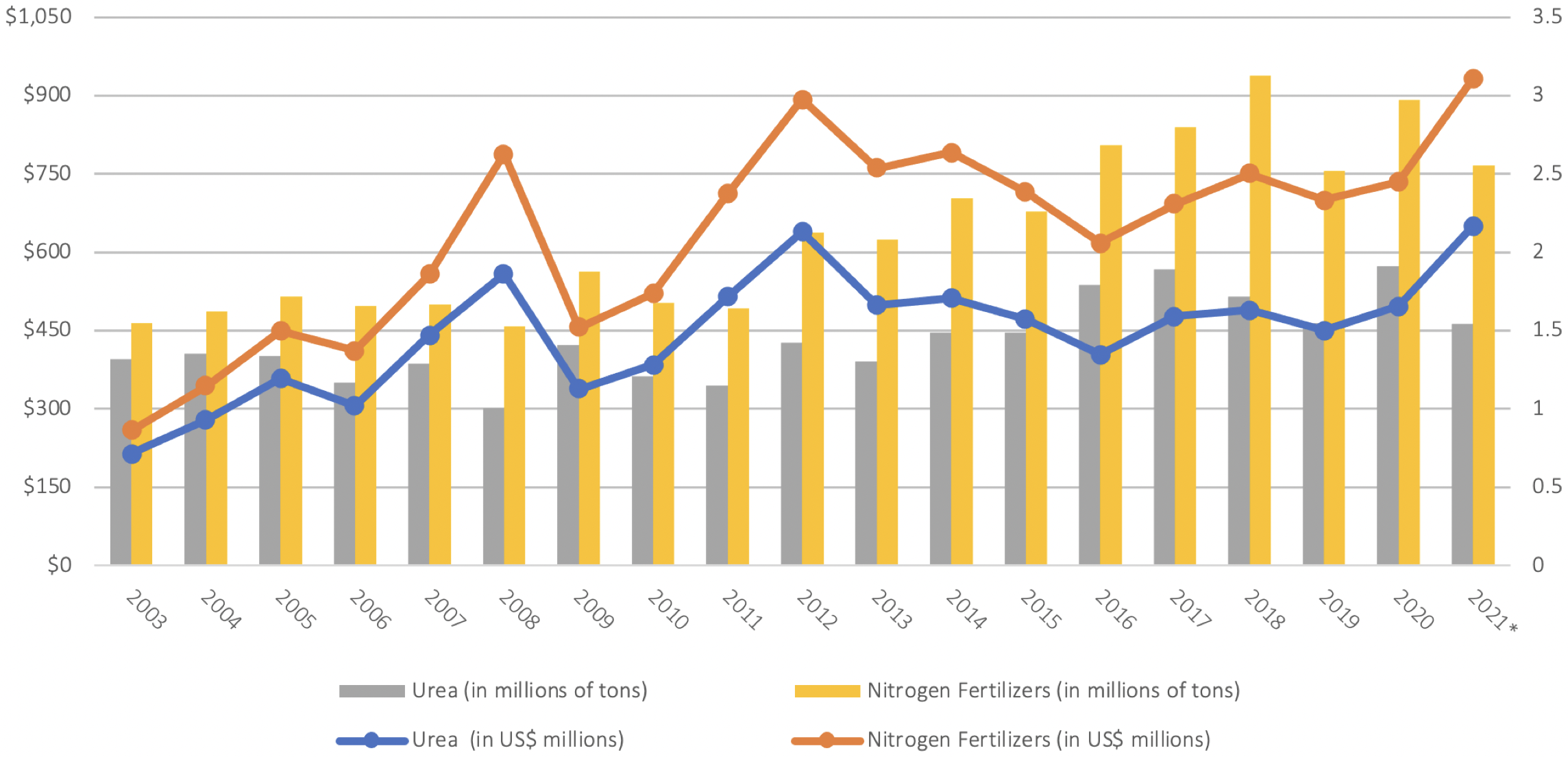

Hence it comes as no surprise that, as shown in Figure 3, urea imports have steadily increased since at least 2003, though more sharply in 2016–2020 with imports averaging 1.77 MMt annually, up from 1.303 MMt in 2003–2015. In January 2021–November 2021, imports vis-à-vis the same period in 2020 descended by 12.7% amid the price spike environment, and, similar to the case of ammonia, their total cost increased by 42.4%, from $456.8 million in 2020 to $650.7 million in 2021.25

It is evident in Figure 3 that there is an upward trend and, if urea production woes persist, the situation could lead to yearly imports reaching and even surpassing the 2 MMt threshold sooner than expected. That volume was nearly attained in 2017 and more recently in 2020, when imports amounted to 1.891 MMt and 1.911 MMt, respectively.

Figure 3 — Mexico's Imports of Urea and Nitrogen Fertilizers, 2003–202126

This certainly is the scenario that the plan announced on December 28, 2021, is aimed at preventing in the years to come. Accordingly, PEMEX is counting on upgrading Pro-Agroindustria, a plant that reportedly has a capacity to produce up to 0.99 MMt of urea,27 equivalent to approximately 52% of all 2020 imports. So, the fact that Mexico disburses hundreds of millions of dollars for crop nutrients while PEMEX plants remain either idle or partly utilized is unsettling for the current administration, whose narrative in the realm of energy and food production frequently highlights the notion of self-sufficiency. The Pro-Agroindustria and Cosoleacaque plants, which boast important features in terms of infrastructure, represent the only short- and medium-term option to rebuild the domestic ammonia-urea value chain; however, to achieve a longer-term solution, a much more robust policy strategy will be required.

It remains to be seen if this plan will materialize, considering that previous announcements and events failed to translate into tangible results. Would the success of the new policy mean that Mexico will be able to weather fertilizer price fluctuations (current and future) and ease off import dependency? A brief answer would be: to some degree. Even if PEMEX upgrades its ammonia and urea plants, current production and import levels (Figures 2 and 3) suggest that domestic demand is robust enough to accommodate other industry participants that, in the long run, could complement PEMEX in supplying local farmers and other users and help Mexico withstand volatility in international markets.

Final Remarks

The decision of the López Obrador administration to address current issues with the ammonia and urea markets through a reactivation of the plants owned by PEMEX takes place within a complex global context—circumstances the fertilizer industry experienced in 2021 and that are likely to linger in 2022, along with the tribulations both commodities face at home. Many of the factors that made the global nitrogen fertilizer environment complex in 2021 may persist through 2022. For example, urea shortages may continue as a result of the export restrictions imposed by Russia and China, both of which are Mexico’s top sources of imports. In addition, shipping costs may not go back to pre-pandemic levels and may instead remain relatively high. Supply chain complications may also continue. And in Europe, natural gas prices could even top 2021 levels because of geopolitical events involving Russia and other suppliers. The list could go on. Moreover, at home, the ammonia and urea value chain continues to be hindered by technical issues exacerbated by the aging state of the government-owned infrastructure as well as the financial woes of PEMEX—the national oil company. The tight availability of natural gas to feed the PEMEX ammonia complex is also an issue of great relevance that has yet to be addressed by the government.

In 2022, this multifaceted setting could hit local farmers in the form of higher prices for crop nutrients, and this in turn raises concerns about food production and food prices. Their connection clearly shows that this is essentially a chain whose influence could be borne all the way to dinner tables in the form of food inflation. Thus, for a market that sources abroad a large share of the nitrogen fertilizers (and even key food staples such as corn) it demands, the string of events described above exhibits, on the one hand, the need to craft and implement policies that address the tribulations surrounding the domestic production of ammonia and urea and, on the other, the value creation opportunities in petrochemicals that Mexico continues to miss.

Endnotes

1. According to the Harmonized System (HS) used by Mexico’s Tariff Information System Via Internet (SIAVI), nitrogen fertilizers are classified as follows: urea (310210), ammonium sulphate (310221), ammonium sulphate-nitrate mix (310229), ammonium nitrate (310230), ammonium nitrate limestone (310240), sodium nitrate (310250), calcium-ammonium nitrate mix (310260), calcium cyanamide (310270), urea-ammonium nitrate mix (310280), and nitrogenous fertilizer mixes (310290). The numbers in parentheses are the HS codes given to each commodity. This issue brief focuses on urea since it accounts for the largest share of imports and domestic consumption of nitrogen fertilizers in Mexico. Ammonia, which is the principal raw material in the production of urea, is also discussed.

2. The FFPI basket of food commodities comprises cereals, dairy, meat, vegetables, and sugar. For a more detailed description, see: Food and Agriculture Organization of the United Nations (FAO), “FAO Food Price Index,” January 6, 2021, https://bit.ly/3Ff1vlK.

3. Christopher Glen, “TFI to the House Agricultural Committee: Fertilizer is a Global Commodity Critical to Our Nation’s Food Supply Chain,” The Fertilizer Institute (TFI), November 2, 2021, https://bit.ly/33twehp.

4. United States Geological Survey, Nitrogen Statistics and Information, Ammonia 2021, https://on.doi.gov/3zRDZu0. 5. Russ Quinn, “Nitrogen fertilizer prices continue to push harder,” DTN/Progressive Farmer, December 15, 2021, https://bit.ly/3HWtLLv.

6. U.S. Energy Information Administration (EIA), “Henry Hub Natural Gas Spot Price (Annual and Monthly),” https://bit.ly/3zWOlsn.

7. All-time-high values for both ammonia and urea refer to the DTN data set. DTN is a data, analytics, and technology company that surveys retail fertilizer prices from about 300 retailers in the U.S. Corn Belt every week. Russ Quinn, “DTN Retail Fertilizer Trends: Anhydrous, 10-34-0 led fertilizer prices up,” DTN/Progressive Farmer, January 5, 2022, https://bit.ly/33bHyPB.

8. Tom Wilson and Nastassia Astrasheuskaya, “European natural gas prices rise further as freezing weather arrives,” Financial Times, December 20, 2021, https://on.ft.com/3fg0sHv.

9. Vipul Garg, “Global ammonia prices surge on European natural gas cost push,” S&P Global Platts, December 16, 2021, https://bit.ly/3tkSSU3.

10. Katherine Dunn, “Energy crisis is hitting fertilizer – and risking a food shortage,” Fortune, November 5, 2021, https://bit.ly/3nnlN6a.

11. John Baffes and Wee Chian Koh, “Soaring fertilizer prices add to inflationary pressures and food security concerns,” World Bank Blogs, November 15, 2021, https://bit.ly/33btENr. For data on urea exports, see UN Comtrade Database, “Exports of urea per country,” 2020, https://bit.ly/31StLgh.

12. This refers to potassium and phosphorus fertilizers, whose prices in 2021 also scored sharp increases. See The World Bank (WB), “Commodities Price Data 2019–2021 (The Pink Sheet), January 4, 2022, https://bit.ly/3nlMsQU. See also Russ Quinn, “Retail fertilizer prices continue to rise at start of 2022, but at slower pace,” DTN/Progressive Farmer, January 12, 2022, https://bit.ly/3zWWzAF.

13. Mike McGinnis, “An end date to higher fertilizer prices is unknown, AFBF economists say,” Successful Farming, January 8, 2022, https://bit.ly/3Guu4gq.

14. Chris Morris, “Fertilizer shortage means that food prices are about to get even higher,” Fortune, November 3, 2021, https://bit.ly/3fmRPuO.

15. Rabobank, Agri Commodity Markets Outlook 2022, https://bit.ly/3KkmaIO.

16. Mexico’s National Institute of Statistics and Geography (INEGI), “National consumer price index (INPC),” 2021, https://bit.ly/31UVxbQ.

17. The government hints that the announced resources will also help upgrade a PEMEX-owned plant of phosphate fertilizers in the state of Michoacán. See Petróleos Mexicanos (PEMEX), “Octavio Romero Oropeza presentó las 10 tareas para el fortalecimiento de Pemex,” press release no. 227, December 28, 2021, https://bit.ly/3JSfmlk.

18. PEMEX, 2020 Report submitted to the U.S. Security Exchange Commission, Form 20-F, https://bit.ly/3FwDNBv.

19. 2021 refers to January 2021– November 2021.

20. Total ammonia imports in 2020 stood at 1.124 MMt and their value at $178.4 million (Figure 2).

21. Mexico’s Center for Sustainable Rural Development and Food Sovereignty Studies (CEDRSSA), Fertilizers (blog), January 15, 2019, https://bit.ly/3G8wlh0.

22. Trade data compiled from: Mexico’s Tariff Information System Via Internet (SIAVI), Imports of ammonia (2814), 2003–2021, http://www.economia-snci.gob.mx/. Values of PEMEX ammonia production obtained from: Mexico’s Energy Information System (SIE), Production of ammonia, 2003–2021, https://sie.energia.gob.mx/. PEMEX, Petroleum statistics, December 2021, https://bit.ly/3gFqJj9.

23. PEMEX, 2020 Report submitted to the U.S. Security Exchange Commission, Form 20-F, https://bit.ly/3FwDNBv.

24. As reported in the stenographic version of President Lopez Obrador's morning press conference on December 28, 2021. See: https://bit.ly/3tzSUaZ.

25. Comparisons refer to January– November of each year. The value of imports is set to be higher once data for the entire year (2021) is released.

26. SIAVI, “Imports of nitrogen fertilizers (3102) and urea (310210),” http://www.economia-snci.gob.mx/.

27. PEMEX, “Pemex reactivará la producción de fertilizantes en México,” Press release no. 5, January 16, 2014, https://bit.ly/3Iju8Aa.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.