The introduction of Mexico’s energy reforms in 2013–2014 unleashed a profound transformation in the natural gas industry that boosted an already growing trend in the country’s gas market. Due to the new institutional scaffolding put in place by the reforms and the Mexican government’s ongoing strategy to encourage the generation of power from cleaner sources, Mexico’s demand for natural gas has increased sharply over the past few years. As a result, natural gas is now regarded as the most important fuel in Mexico’s energy blend.1 According to the country’s Secretariat of Energy (SENER), this shift is only expected to accelerate. In fact, domestic natural gas demand is set to continue its upward trajectory through 2031.2

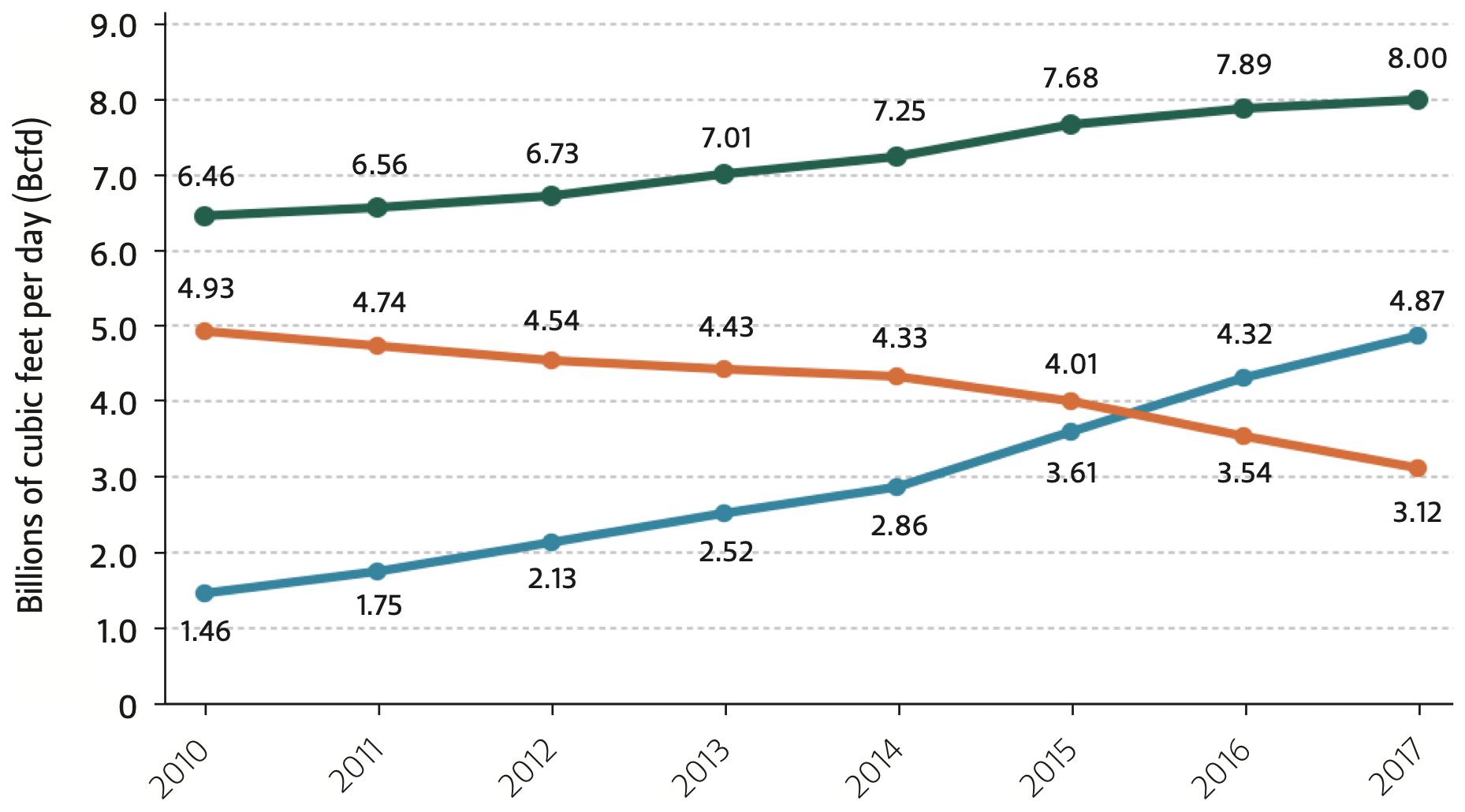

Amid this transition, one issue stands out: Since 2010, Mexico’s demand for gas has been accompanied by a persistent decline in domestic production, making imports increasingly vital in filling the gap between production and consumption (Figure 1). The National Hydrocarbons Commission (CNH)3 estimates that from January to October 2017, imports of natural gas averaged 61 percent of the country’s overall consumption—including for power generation, industry, transport, and household and commercial uses—representing a large jump from 32 percent in 2012. Of course, the natural gas produced and used by Petróleos Mexicanos (PEMEX) is included in this figure; but when PEMEX’s consumption is excluded, the import dependency of the rest of the economy is greater. This highlights the growing importance of natural gas for the overall economy. PEMEX consumes part of its own fuel to feed its industrial processes, so as domestic production declines, other sectors see an even greater need to import natural gas from abroad. For January through October 2017, 84 percent of the demand from all sectors excluding PEMEX was met via imports.4

Mexico’s dependency on imports can be worrisome, particularly if a truly integrated North American gas market develops in the future. Nevertheless, policymakers must bear in mind that implementing mechanisms to guarantee the supply of natural gas to domestic users such as power and manufacturing plants is, in fact, more important. And if demand must be met by imports for the time being, then so be it. Put simply, it is a matter of securing access to natural gas within the context of the widening gap between domestic demand and production. That is why if softening dependency on imports down the road is an overt policy goal, greater participation of firms in Mexico’s emerging natural gas market is an important avenue to pursue. For that to happen, investment in upstream activities and transport infrastructure, as well as the adoption of market-based practices, must be part of any policy that seeks to reduce import dependency. Importantly, even if the North American market continues to become more integrated, such a path will benefit Mexico and its natural gas consumers by deepening the market and providing adequate access to multiple sources of supply.5

Though it is certain that increasing Mexico’s production is important, easing import dependency will certainly be more complicated in the absence of a more efficient and competitive market.

Growing Demand Meets Falling Production

For the most part, demand for natural gas in Mexico has expanded rapidly because of the Mexican government’s strategy to diversify the configuration of the national energy mix. This has entailed reducing consumption of more polluting and more expensive energy sources such as fuel oil6 and pledging to generate cleaner electricity to meet the country’s commitments to the environment.7 To be sure, this policy was crafted well before the approval of the 2013 energy reforms. For example, during the decade leading up to 2013, the generation of electricity from natural gas grew at an annual rate of 8.3 percent, while electricity generation from fuel oil declined at around 4.5 percent per annum.8

Figure 1 — Mexico’s Imports and Production of Dry Natural Gas (2010–2017)

Source Mexico’s National Hydrocarbons Commission, https://portal.cnih.cnh.gob.mx/downloads/es_MX/ estadisticas/Balance-Gas-Natural.pdf.

Currently, due to the power sector’s promotion of an aggressive policy strategy—one that includes the construction of transport infrastructure and combined cycle power plants across the country—natural gas has become this sector’s most important energy source. Among all fossil fuels used to generate power in 2016, official estimates put the share of natural gas at 68.7 percent, well ahead of coal, fuel oil, diesel, and petroleum coke.9 These numbers are met with a certain degree of concern in Mexico, since even greater natural gas imports are required to meet the growing domestic demand in the manufacturing and power generation sectors in particular (Figure 2). From 2010 to 2017, for example, Mexico’s gas imports almost tripled, even as domestic production declined by 36.7 percent (Figure 1). The need to sustain power plant operations is the main driver behind Mexico’s dependency on imported natural gas, which made up 63 percent of domestic supply in October 2017 (the most recent figure reported by the CNH).10

Going forward, the conditions are ripe for natural gas to become the mainstay of all energy sources in Mexico. In its most recent analyses of market conditions, SENER projects that the use of natural gas will further increase by 2031, primarily due to a large number of combined cycle power plants coming online over the next decade. The country’s demand is anticipated to reach 9.66 billions of cubic feet per day (Bcfd), an increase of almost 27 percent from 2016. The power sector is predicted to remain the leading consumer of natural gas and capture 61.6 percent of gas supply. In other words, demand for natural gas in electricity generation is expected to expand from 3.97 Bcfd in 2016 to 5.95 Bcfd in 2031, a trajectory that likely makes natural gas the most important energy source for the next few decades.11

Not Without Pipelines

It is understood within SENER that the strategy to supply natural gas to domestic users over the next 15 years mostly depends on (a) having access to production coming out of shale formations in the United States and (b) a positive change in investment conditions for PEMEX and private firms potentially interested in entering the Mexican upstream sector, largely incentivized by the energy reforms. However, it must be noted that this strategy cannot be effective without expanding the country’s capability to distribute natural gas. In other words, additional infrastructure to distribute gas will have to be built, which will require further investment. The administration of President Enrique Peña Nieto is conscious of this and, since the approval of reforms, has bolstered efforts to build more pipelines.12 Based on the national infrastructure program published in 2013, which stated that investment in natural gas transport capacity would be nine times larger than during the preceding administration, SENER designed a five-year plan to expand the length and capacity of the country’s pipeline network by 2019.13

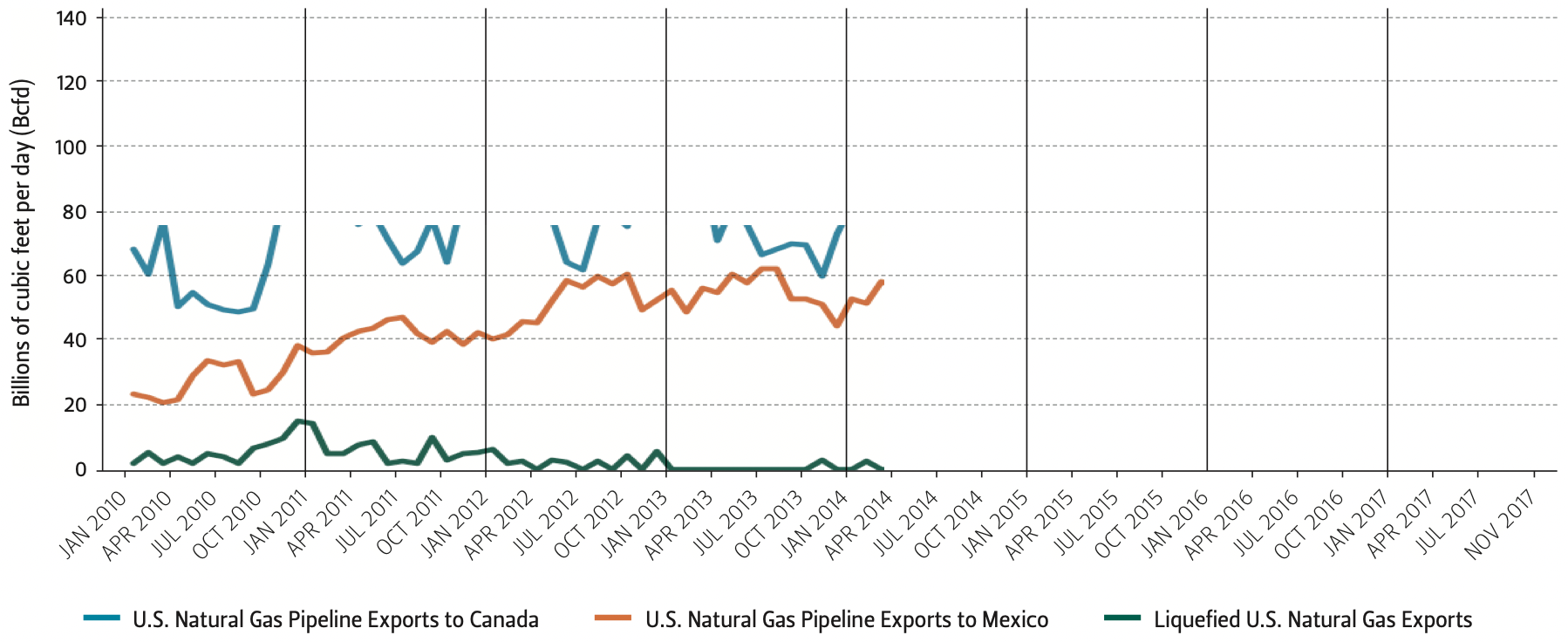

Mexico, which is currently the largest export market for U.S. natural gas, also needs to broaden its capacity to carry natural gas across the border. If proposed infrastructure projects become operational as planned, the U.S. Energy Information Administration estimates that cross-border natural gas transport capacity will reach 14 Bcfd by the end of 2018, almost twice the volume reported in 2016.14

The increasing gas transportation connectivity between the United States and Mexico can be interpreted in several ways. First, the abundant supply of natural gas in the United States and the prevailing affordable prices, particularly in the state of Texas, are strong enough factors to shape policymaking south of the border. Therefore, while ongoing energy reforms have played a key role in the transformation of the Mexican gas market, recent developments in Mexico cannot be delinked from the explosive upsurge in U.S. gas production. The growth in gas transportation capacity in Mexico is also partly in response to existing production dynamics north of the border. It is designed to favor the supply of natural gas from shale plays such as Eagle Ford and the Permian Basin to users in northern and central Mexico—including manufacturers, who have incentivized production integration under the North American Free Trade Agreement.

Figure 2 — U.S. Natural Gas Exports (January 2010–November 2017)

This creates a virtuous cycle for energy integration in general—the competitiveness of gas prices in the U.S. incentivizes transportation capacity growth south of the border, which makes it easier for gas to flow to multiple locations in Mexico. In turn, this increases Mexico’s dependence on U.S. gas markets, but it also strengthens Mexico’s competitiveness in manufacturing, further fueling the need for U.S. gas. The downside is that many in Mexico see this dependence as a disadvantage but have no power to influence the structural pull of the production, transportation, and consumption markets, which now have a dynamic of their own.

Conclusion

Enormous inefficiencies in Mexico’s gas production and transportation sectors have accumulated over the past decades, resulting in the decline in Mexico’s natural gas production and a situation that will require considerable resources to be reversed. The way forward is to halt state-generated distortions of the market, realize the value of the participation of firms—both private and state-owned—and recognize the necessity of their participation to make Mexico more competitive. Firms—from producers to pipeline operators—and a solid governmental regulatory apparatus must now help guarantee the consistent supply of natural gas to users, as the country’s development becomes even more dependent on secure flows of natural gas. For such firms to be incentivized to invest in and obtain greater efficiencies from gas market integration, SENER must continue making progress in building a more efficient market.

Endnotes

1. Prospectiva de gas natural 2016-2030 (Ciudad de México: Secretaría de Energía, 2016), https://www.gob.mx/cms/uploads/attachment/file/177624/Prospectiva_de_Gas_Natural_ 2016-2030.pdf.

2. Prospectiva de gas natural 2017-2031 (Ciudad de México: Secretaría de Energía, 2017), https://www.gob.mx/cms/uploads/attachment/file/286233/Prospectiva_de_Gas_Natural_ 2017.pdf.

3. Comisión Nacional de Hidrocarburos, “Balance de gas natural,” October 2017, https://portal.cnih.cnh.gob.mx/downloads/es_MX/estadisticas/Balance%20Gas%20 Natural.pdf.

4. From January to October 2017, the import share of domestic demand (excluding PEMEX’s needs) remained above 80 percent for every month.

5. Kenneth B. Medlock III, The Land of Opportunity? Policy, Constraints, and Energy Security in North America (Houston, Texas: Rice University's Baker Institute for Public Policy, June 2, 2014), https://www.bakerinstitute.org/media/files/files/94020ec4/CES-Pub-EnergySecurity-060214.pdf.

6. Using diesel in gas turbines generates 1,408.3 kg of carbon dioxide per megawatt hour (Mwh), while burning natural gas in combined cycle plants produces 417.3 kg of carbon dioxide per Mwh. See Programa de desarrollo del sistema eléctrico nacional: PRODESEN 2017-2031 (Ciudad de México: Secretaría de Energía, 2017), http://base.energia.gob.mx/prodesen/PRODESEN2017/PRODESEN-2017-2031.pdf.

7. The projection is that Mexico’s power output from cleaner sources will grow from 22.7 percent in 2017 to 38.2 percent in 2031. See Prospectiva del sector eléctrico, 2017-2031 (Ciudad de México: Secretaría de Energía, 2017), https://www.gob.mx/cms/uploads/attachment/file/284345/Prospectiva_del_Sector_El_ ctrico_2017.pdf.

8. Prospectiva del sector eléctrico, 2013-2027 (Ciudad de México: Secretaría de Energía, 2012), https://www.gob.mx/cms/uploads/attachment/file/62958/Prospectiva_del_Sector_El_ ctrico_2012-2026.pdf.

9. Prospectiva de gas natural 2017-2031.

10. Comisión Nacional de Hidrocarburos, “Balance de gas natural.”

11. Prospectiva de gas natural 2017-2031.

12. Plan quinquenal de expansión del sistema de transporte y almacenamiento nacional integrado de gas natural, 2015- 2019 (Ciudad de México: Secretaría de Energía, 2014), https://www.gob.mx/cms/uploads/attachment/file/43397/Plan_Quinquenal_del_Sistema_ de_Transporte_y_Almacenamiento_Nacional_Integrado_de_Gas_Natural_2015-2019.pdf.

13. Programa nacional de infraestructura 2014–2018 (Ciudad de México: Presidencia de la República, 2013), http://cdn.presidencia.gob.mx/pni/programa-nacional-de-infraestructura-2014-2018.pdf?v=1.

14. U.S. Energy Information Administration, “New U.S. border-crossing pipelines bring shale gas to more regions in Mexico,” December 1, 2016, https://www.eia.gov/todayinenergy/detail.php?id=28972.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.