This brief describes key takeaways from the German Natural Gas Market Balance Dashboard, an interactive dashboard developed by Miaomiao Rimmer and Luke (Leelook) Min that assesses the potential outcomes for natural gas market balances in Germany. Visit the dashboard to assess other potential outcomes.

Abstract

Russia’s invasion of Ukraine on February 24, 2022, compromised the security of natural gas supply in Europe. The balance of 2022 was aimed at bracing for a potentially difficult winter marked by high prices and considerable uncertainty. While the winter has not been as bad as it could have been, the situation is far from settled. Future natural gas supply faces tremendous precarity due to the substantial reduction in Russian gas imports. Germany, the European Union’s largest economy, is a microcosm of the European natural gas market and of the current and future issues facing Europe. Natural gas is important for manufacturing, so compromised imports will continue to have an outsized effect on both gas availability and economic performance for the EU as a whole. In order to assess the potential outcomes for natural gas market balances this winter and next in Germany, we constructed three demand-oriented scenarios: 1) cold winter 2022-23, 2) mild winter 2022-23, and 3) an extreme case. Herein, we describe the key takeaways from these scenarios and highlight some critical points.

Framing the Issue

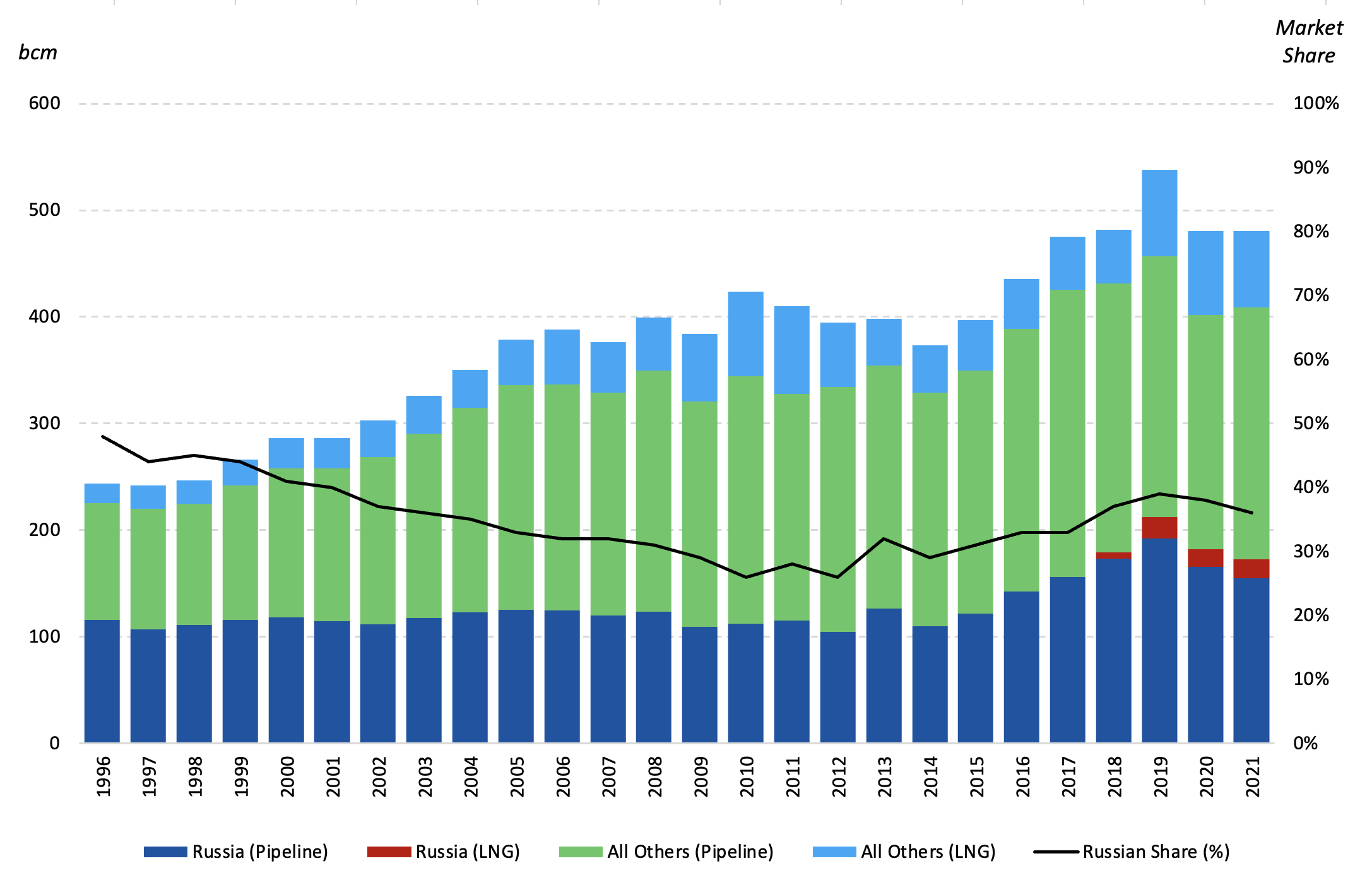

Europe spent the balance of 2022 bracing for a potentially difficult winter. Natural gas supply in particular, faced, and continues to face, tremendous precarity due to the substantial reduction in Russian gas imports. A combination of new liquefied natural gas (LNG) imports and additional pipeline supplies from other producing regions together are not sufficient to make up for the nearly 40% market share that Russian gas volumes recently occupied (see Figure 1). As such, Europe will need to employ a combination of fuel-switching and demand-rationing to weather the storms of this winter and the balance of 2023 into next winter.

Figure 1 — Natural Gas Imports to the European Union and Russian Market Share of Total Supply

Note bcm: billion cubic meters.

The difficulties do not end with winter 2022-23. The risk of natural gas shortages and high price burdens on European consumers will likely persist, as all signs point to even greater difficulties the following winter. The lingering impacts of reduced Russian gas supplies to Europe will have spillover effects for the world. Already, European demand for LNG imports has forced LNG prices to unprecedented highs, driving a redirection of marketed volumes away from Asia to Europe. This stands in stark contrast to the status quo that generally persisted previously, where Europe was viewed as a “market of last resort” for global LNG volumes.[1] Indeed, European LNG terminals operated at their maximum capacity in an effort to fill storage for this winter.[2]

Germany in Focus

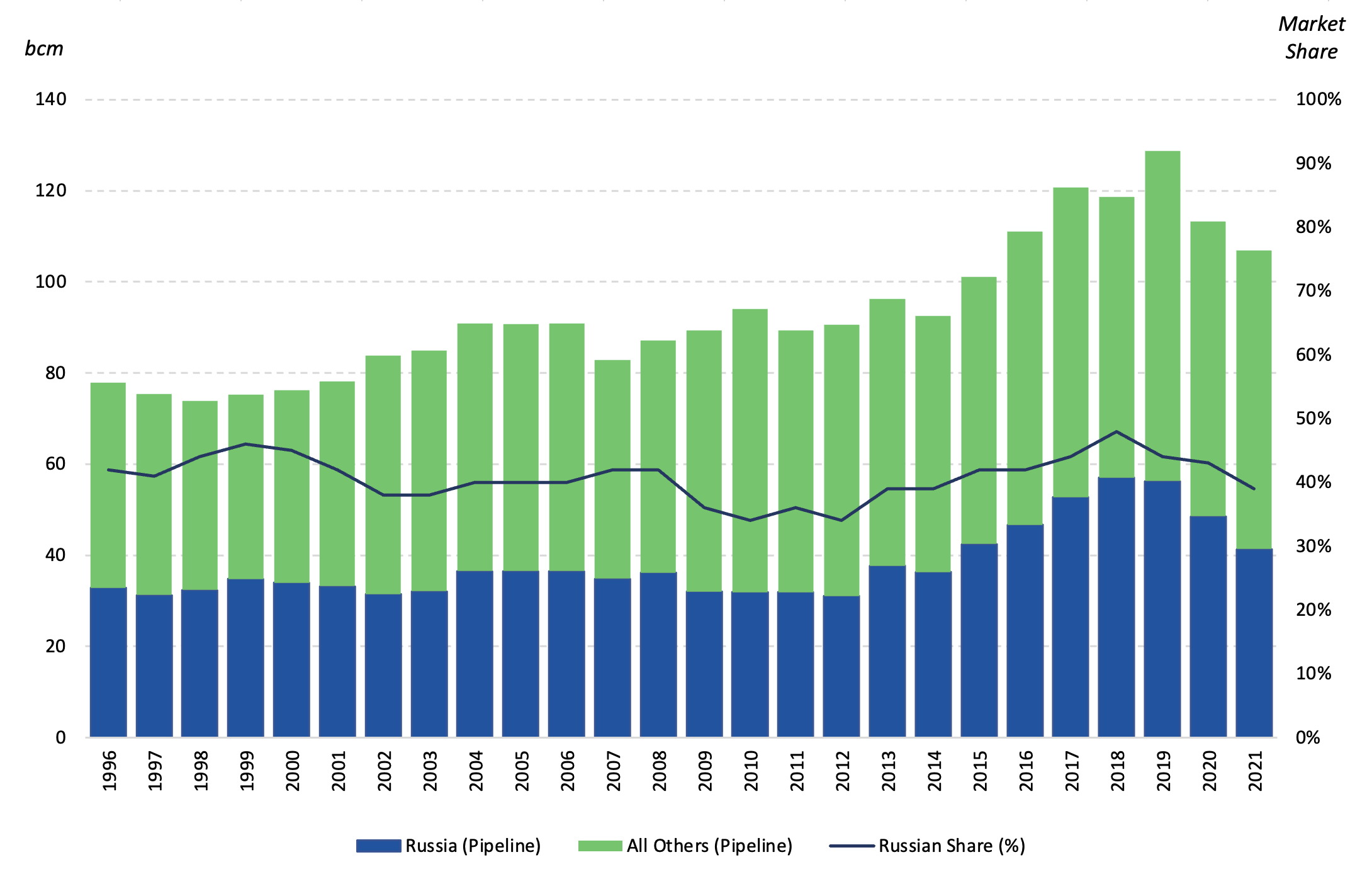

Germany is a microcosm of the European natural gas market and of the current and future issues facing the EU. Figure 2 shows Russian gas supply to Germany. As the EU’s largest economy, much of which relies on natural gas for manufacturing, Germany has an outsized effect on both gas availability and economic performance for the EU as a whole. Over the past decade, Germany has accounted for as much as one-quarter of all natural gas imports to the EU in any given year, and for one-third of all imports to the EU from Russia. As such, anything that affects the natural gas market in Germany is likely to have ramifications for the EU as a whole.

Figure 2 — Natural Gas Imports to Germany and Russian Market Share of Total Supply

Note Germany reexports some of its imports to neighboring countries, so not all of the imported volumes are consumed domestically.

Regarding the German gas market, Russian natural gas imports have accounted for at least 40% of supply since the 1990s. This reliance has been fortified in recent years by two pipeline projects for direct delivery of Russian gas into Germany:

- Nord Stream 1, a pipeline that began operations in 2011 with 55 billion cubic meters per year (bcm/y) capacity.

- Nord Stream 2, a pipeline completed in 2022 but never commissioned, which would have added another 55 bcm/y of capacity to the Russian-sourced imports.

While Nord Stream 2 was not commissioned, its mere existence promised additional volumes, abating investments in other sources of supply into Germany. If Nord Stream 2 had been commissioned and become fully operational, the pipeline together with Nord Stream 1 could have satisfied Germany’s entire annual gas demand and provided some gas for reexports. Both pipelines were portrayed by Germany as a part of the EU’s gas market diversification efforts away from transit country risk, i.e., the diversification of gas transit away from Ukraine that both Russia and Germany had considered to be unreliable. At the same time, the need for diversification of suppliers — in particular via LNG imports — was dismissed on the basis of high costs compared to Russian supply.

The notion that Europe would move away from fossil fuels, including natural gas, had also dampened interest from policymakers and corporations in developing long-lived import infrastructures underpinned by long-term supply contracts. Indeed, this perspective was actively reinforced by energy transition policies advanced by most countries in Western Europe. In Germany, the policy of Energiewende (energy transformation) was aimed at facilitating the goal of economy-wide decarbonization. Low-cost natural gas from Russia was considered a bridge fuel that would help reach its goal, particularly since the German plans for the energy transition also required phasing out the country’s nuclear fleet by the end of 2022. Importantly, while Germany has been the most aggressive of European countries in its effort to eliminate nuclear power, the attitudes of other European countries have been largely ambivalent. Even France, which is very dependent on nuclear power for its energy needs, had not been proactive in maintaining or rebuilding its aging nuclear power fleet until the current energy crisis.

The “wind drought” in the fall of 2021 stoked fears about a lack of sufficient redundancy in the European energy mix.[3] Then, with Russia’s invasion of Ukraine, Russian President Vladimir Putin threw a boulder into the proverbial pond of European energy policy. Energy security became top of mind for most European policymakers and the general public. In March 2022, merely two weeks after the invasion, natural gas and nuclear energy were both somewhat back in favor and declared “in line with EU climate and environmental objectives” by the European Commission Directorate‑General for Financial Stability, Financial Services and Capital Markets Union.[4] In turn, an accelerated emphasis on bringing more LNG import capacity online emerged.[5]

While floating storage and regasification units (FSRU) have been mobilized as near-term opportunities to bring more LNG into Germany, there is limited capacity along LNG supply chains to do more in the near term. A lack of spare LNG liquefaction and tanker capacity drove the LNG market into a very tight situation, so much so that large Asian buyers redirected cargoes to Europe and rationed their own demands. Hence, Germany (and Europe more generally) has been faced with the unavoidable outcome of having to use other fuels to sate its energy needs and/or ration its own gas demand, particularly industrial demand.[6] According to Bundesnetzagentur, industrial demand in October 2022 was 27.4% lower than the average from 2018 to 2021, a time period that included the COVID-19 pandemic.[7] High energy prices have many companies, like Germany-based BASF, considering relocation to countries like the U.S. and China. This does not bode well for the future of the German economy, nor, by extension, for Europe as a whole.

Scenario Analysis: Revelations about this Winter and Next

In order to assess the potential outcomes for natural gas market balance this winter and next in Germany, we constructed three demand-oriented scenarios: 1) cold winter 2022-23, 2) mild winter 2022-23 and 3) an extreme case in which this winter and the next are colder than normal, with a warmer than normal summer. We then evaluated the implications of LNG imports and storage policies in each scenario. The tool for analysis can be accessed here.[8]

Herein, we describe the key takeaways from these scenarios and highlight some critical points. Across the three scenarios, imbalance is inevitable — even in a mild winter — and the imbalance can only be rectified through fuel-switching and demand-rationing. In this regard, LNG imports are critical for market balance in every case considered, as two German FSRU terminals in Wilhelmshaven and Brunsbüttel will bring an additional import capacity of 16 bcm/y.

Storage targets that bring inventories to near-full capacity are helpful. They provide a form of insurance that can alleviate shortages during winter periods, but they are not enough by themselves.[9] In fact, the analysis indicates that the combination of new LNG imports and full storage will still require other active margins of response — fuel-switching and/or demand-rationing — even with a mild winter.[10] If the winter is colder than average, the situation tightens significantly.[11] To date, the mild winter scenario has been playing out.

One margin that Germany can consider is its exports to neighboring countries. Specifically, Germany can flex these down to minimum historical levels, which is the assumption in the scenarios we constructed. However, depending on realized demand across all of Europe, this could put pressure on gas market balances in Germany’s neighboring regions as well. The political and social fallout that could result might weaken European resolve to completely wean itself from Russian natural gas.[12]

In all of the scenarios we considered, the demand outlook is critical for assessing costs. The 2023 demand forecast is 73.5 bcm for the mild winter 2022-23 scenario, 90.0 bcm for the cold winter 2022-23 scenario, and 95.7 bcm for the extreme scenario. For comparison, demand in Germany was 93.6 bcm in 2021, 89.3 bcm in 2020, 91.8 bcm in 2019 and 85.5 bcm in 2018. Notably, while the mild scenario represents an extremely low-demand case relative to recent history, our analysis indicates that the market will only balance with proactive demand-rationing and/or fuel-switching.

Importantly, our analysis indicates that the gas market balance issues in Germany and throughout Europe will persist. It is likely that the balance of 2023 will be focused on refilling storage for winter 2023-24. In fact, refilling storage will become more difficult if this winter is colder than normal, as inventories will be drawn down more than is typical, and Russian gas will not be available to prepare for next winter. Replenishing depleted inventories in a supply-constrained environment will carry implications for demand-rationing and fuel-switching through the balance of 2023.

Concluding Remarks

The 2022-23 winter heating season is not over. The natural gas market balance remains precarious, particularly if the winter turns colder. Management will require fuel-switching, demand-rationing and concerted effort to bring new gas supplies to Europe, all while policymakers must thread the needle of keeping energy supplies affordable to the general public. This will generally mean that large industrial consumers will be the first to face interruption.

As we move beyond this winter, we already see issues arising for the balance of 2023 and into the next winter heating season. The historical reliance on Russian natural gas for energy balances has set the stage for difficulties to persist, and possibly worsen. This outcome follows from several factors. To begin, global LNG supply cannot be increased quickly enough to offset lost imports of Russian pipeline volumes. It takes years to permit, build and commission new LNG export infrastructure and the associated supply chains to deliver LNG to regasification locations. While FSRUs can serve as a near-term bridge for LNG imports, a casual reliance on FSRUs does not address the lack of sufficient global liquefaction capacity, the time to build new capacity or constraints on the current availability of FSRU capacity. We already know that only about 6.6 million metric tons per year (mtpa), or 9.1 bcm/y, of baseload LNG capacity will enter global markets in 2023 (with 5.2 mtpa coming from Golden Pass in the U.S. and 1.4 mtpa coming from Congo-Brazzaville).[13] This, however, is nowhere close to the amount of Russian pipeline gas that has been removed from the European market since the invasion of Ukraine. So, the global market will remain stressed, carrying implications for Europe and beyond.

In general, infrastructure and logistical constraints prevent the global market from adjusting rapidly to lost Russian gas volume into Europe. In particular, Russian gas cannot simply be redirected to other markets (e.g., China) due to the lack of alternative infrastructure. As such, there is no displacement opportunity whereby greater Russian pipeline volumes move into Asia and allow more LNG to be redirected from Asia to Europe. Hence, logistics and a lack of excess pipeline capacity prevent rapid, full adjustment.

In addition, by law the EU’s natural gas storage must be filled to at least 90% by Nov. 1, 2023. Some countries have set even more aggressive requirements. In Germany, for instance, storage must be filled to 95% by Nov. 1. Such a legal imperative will result in the removal of supplies available to consumers during the non-heating season, since they are instead being injected into storage. This is likely to tighten markets throughout the entire year.

Finally, significant volumes were still flowing to Europe from Russia for most of 2022, which helped countries to fill storage in anticipation of the coming winter heating season. In 2023, these volumes are very likely to remain unavailable. As such, while the near-term emphasis should be on meeting heating demands for the remainder of winter 2022-23, winter 2023-24 may pose an even more difficult challenge.

Technical Note

Analysis of Germany’s natural gas market offers important insights for European markets and European policymaking, given the country’s unique role in the European Union. Although Germany is but one country in the heterogeneous EU, the relative size of its natural gas market means that what happens in Germany, with respect to its natural gas market balance, typically has ramifications for all of Europe.

To analyze the implications of recent events — particularly the Russian invasion of Ukraine — for the German gas market through winter 2023-24, we estimate a model of historical natural gas demand that is conditional on key determinants such as weather, price, renewable generation and the macroeconomy.

We then model supply into Germany as a function of domestic production, net imports of natural gas via pipeline, and the potential for liquefied natural gas (LNG) imports via floating storage and regasification units (FSRUs) that are being built to begin operations in late 2022 and early 2023. Notably, there are no historical data for LNG imports into Germany, as the country has been reliant on pipeline flows. But energy security concerns have altered this status quo, and new LNG imports set to commence. This turns out to be an important factor for balancing the German gas market going forward.

Storage is the balancing item on a seasonal basis between demand and supply, with storage injections occurring when supply exceeds demand and withdrawals occurring when demand exceeds supply. In our analysis, we include Germany’s law requiring natural gas storage to be filled to at least 95% by Nov. 1 of each year.

For the market to be in balance at any given time, natural gas demand must be met by a combination of domestic production, net imports and natural gas from storage. The results from our analysis indicate that there is likely to be insufficient supply to meet demand during some periods. As such, since markets always balance, the shortfall will need to be met by fuel-switching and/or demand-rationing, which is shown as a market “imbalance” in the scenarios.

Demand

To forecast the short-run natural gas demand for Germany, we first estimate the following equation describing the demand for natural gas:

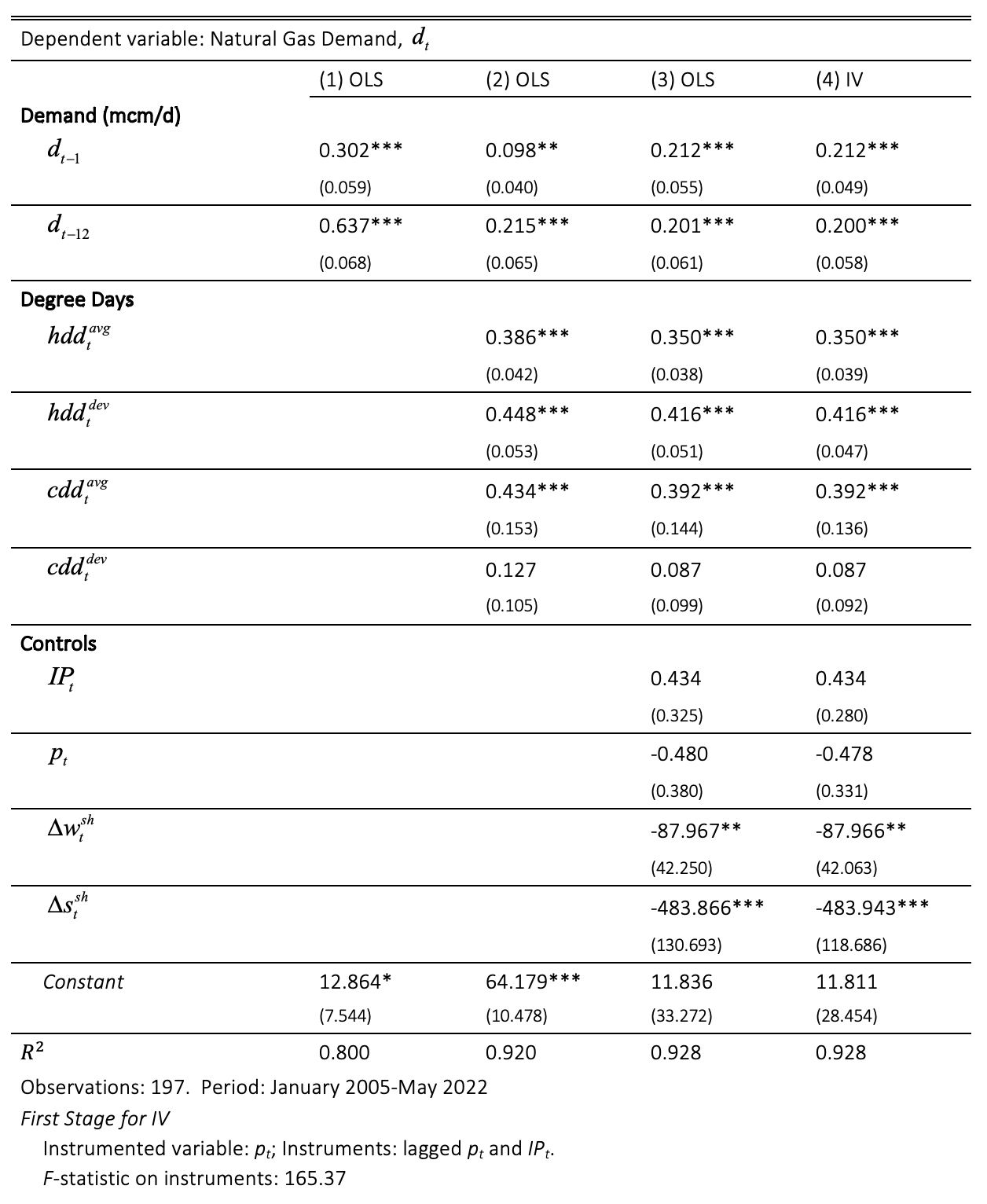

where dt denotes natural gas demand in month t in million cubic meters per day (mcm/d); hddtavg and cddtavg are the monthly long-run average heating and cooling degree days, respectively, and are included to capture normal seasonal movements in demand; hddtdev and cddtdevare the deviations in heating and cooling degree days from the long-run average in each month, respectively, and are included to capture the impact of deviations from normal seasonal weather patterns, i.e, hddtdev = hddt – hddtavg; IPt is the industrial production index in each month, and is included as a measure of macroeconomic performance; pt is the natural gas price at the Dutch Title Transfer Facility (TTF) in real U.S. dollars per million British thermal units (US$/mmbtu), and is included to capture the impacts of changes in market balance on demand; and Δwtsh and Δstsh are the changes in the shares of wind and solar generation, respectively, in total power generation, and are included to capture the effects over time of growth and variation in renewable generation sources on the use of natural gas.

The estimation results for equation (1) are in presented in Table 1, and the results in Column 3 of Table 1 are used to generate the demand forecast in each scenario.

Supply

We define natural gas supply in Germany as the sum of domestic production, net imports via pipeline and LNG imports. Pipeline imports are separated into two categories: Russian and all other. The imports from Russia include both direct and indirect pipeline routes including Nord Stream 1 (Russia), Yamal-Europe (Poland), and MEGAL (Czech Republic). The main sources of other natural gas imports are countries such as Norway, the Netherlands and Belgium.

Natural gas that transits Germany for export to neighboring countries is also included. These exports act as a net reduction in supply available for use in Germany. There are historically no LNG import terminals in Germany, so LNG imports are prospective imports that would be derived from new import capacity, such as from FSRUs that are expected to begin operations in late 2022 and early 2023.

Storage

Any deficit or surplus in the natural gas market is balanced through storage withdrawals or injections. For instance, during winter months, when heating demands increase, natural gas is withdrawn from storage to provide volume to market when demand exceeds supply. In the spring, summer and fall months, storage is typically refilled as supply exceeds demand.

A major factor to consider is the availability of supply relative to demand, which is why storage has historically been the “balancing” feature of the market. If something decreases supply and/or increases demand, then storage levels will be lower than normal, which will increase the market price. Accordingly, if something increases supply and/or decreases demand, then storage levels will be higher than normal, decreasing the market price. In this way, storage is like insurance for market balance; the market is at a higher risk of imbalance when storage levels are low relative to demand, thus triggering a higher price (i.e., evidence of a risk premium) to stimulate supply and discourage demand. Alternatively, if the market is well-supplied, the risk of imbalance is low, the price is low, and the need for inventory to meet demand is reduced.

Germany has underground gas storage capacity of 25 billion cubic meters (bcm), which can typically provide more than 25% of annual consumption. The German government requires natural gas in storage to be at 95% of capacity by Nov. 1 of each year in order to abate the risk of insufficient supply to meet winter demand.

Policy

We consider two main policy measures that Germany is utilizing to manage the energy crisis. The first measure calls for a minimum storage level to ensure a sufficient buffer to meet the gap created by the exit of Russian volumes.[14] Notably, this requirement can indirectly raise prices while storage is being filled, since it pulls the required volumes out of the market. The justification, however, is the risk of insufficient supply available to the market in the case of a geopolitical disruption, and the hope is that the additional volume will abate price increases in the future.

To see how storage volumes mitigate deficits for each scenario, it is possible to choose the storage level to either (a) follow storage targets or (b) evolve unconstrained with a minimum volume of 25% of the historically observed minimum level. In case (a), it is assumed that the German government targets a minimum level of gas storage that mimics the targets set for 2022. In case (b), we do not restrict storage to follow a certain path, but we do assume that it does not fall below 25% of the historically observed minimum level at the end of winter heating season.[15] In both cases, the German gas market is forced to balance through other mechanisms when storage becomes insufficient. Balancing can occur through increased LNG imports, increased pipeline imports, fuel-switching or demand-rationing.

Regarding LNG imports, it is assumed that two FSRUs come online in Wilhelmshaven and Brunsbüttel, Germany, respectively, as expected at the end of 2022 and the beginning of 2023. These FSRUs will add additional capacity of 16 bcm per year (y), or 43.8 million cubic meter (mcm) per day (d). In order to illustrate the impact of LNG imports, users can choose in each scenario whether or not these LNG imports occur.

With these two measures implemented in the analysis, we measure the balance in the German natural gas market as demand net of supply and net-withdrawal (or, withdrawal minus injection) to illustrate the potential deficit (conversely, the surplus) in any given scenario.

Scenario

In order to assess the potential outcomes for natural gas market balances this winter and next in Germany, we constructed three demand-oriented scenarios: (1) cold winter 2022-23, (2) mild winter 2022-23, and (3) and extreme case in which this winter and the next are colder than normal.[16]

Across all scenarios, we make the following common assumptions that:

- Germany receives no Russian pipeline natural gas;

- Germany maximizes net imports from non-Russian countries;

- Domestic production remains at recent historical levels;

- The industrial production growth rate is fixed at the historical minimum of -8% per year; and

- The shares of wind and solar generation in total power generation stay at recent historical average levels.

We also use the TTF futures price as a proxy for future gas prices.

Table 1 — Estimation Results

Endnotes

[1] See, for example, Howard Rogers, Does the Portfolio Business Model Spell the End of Long-Term Oil-Indexed LNG Contracts?, (Oxford: Oxford Institute for Energy Studies, 2017).

[2] Miles, Steven R., Gabriel Collins, and Anna Mikulska. 2022. US Needs LNG to Fight a Two-Front Gas War. Policy report no. 08.18.22. Rice University's Baker Institute for Public Policy, Houston, Texas. https://doi.org/10.25613/GDVP-QN45.

[3] Nora Buli and Stine Jacobsen, “Analysis: Weak winds worsened Europe's power crunch; utilities need better storage,” Reuters, December 22, 2021.

[4] Directorate-General for Financial Stability, Financial Services and Capital Markets Union, “EU taxonomy: Complementary Climate Delegated Act to accelerate decarbonization,” European Commission, February 2, 2022.

[5] See Gabriel Collins, Kenneth B. Medlock III, Anna Mikulska, and Steven R. Miles, Strategic Response Options if Russia Cuts Gas Supplies to Europe, Research paper 02.11.2022, Rice University's Baker Institute for Public Policy, Houston, Texas.

[6] Tom Käckenhoff, Vera Eckert, and Christoph Steitz, “As German gas rationing looms, industry begs exemptions,” Reuters, August 9, 2022.

[7] Bundesnetzagentur, “Current Gas Supply Situation,” accessed December 1, 2022.

[8] A technical note to explain the modeling effort is also available in the appendix. We provide the description of our modeling approach to analyze the German natural gas market and include demand, supply, storage, policy and scenario. Using historical data, we estimate a natural gas demand function by linear regression and forecast demand for different scenarios. Across the scenarios, we make common assumptions regarding natural gas imports via pipelines. Each scenario has different assumptions regarding weather. For policy analysis, we provide two storage paths to meet mandates and include LNG imports via new FSRUs.

[9] German gas storage is 98.2% full as of November 29, 2022, which on its own can provide about one-quarter of annual consumption. Aggregated Gas Storage Inventory.

[10] Demand-rationing for natural gas is already taking place among commercial and industrial users. We, however, define realized rationing as the difference between industrial consumption and its historical minimum. Then, we assume that such demand-rationing will continue throughout the prediction period by applying the share of the rationed volumes to total consumption in Oct. 2022 (18.8%) to quantify demand-rationing that would occur regardless of market balance if such demand-rationing behavior were to persist going forward. Note that this is a somewhat conservative assumption providing a minimum bound in that we ignore the commercial side.

[11] We note that net withdrawals relative to gas in storage in every scenario not only fall within the historical range of net withdrawals, but are also less than the withdrawal capacity limit.

[12] See Perdana et al., “European Economic impacts of cutting energy imports from Russia: A computable general equilibrium analysis,” Energy Strategy Reviews vol. 44, 2022.

[13] Miles, Steven R., Gabriel Collins, and Anna Mikulska, US Needs LNG to Fight a Two-Front Gas War.

[14] The German government has raised the mandatory natural gas storage targets as follows: 40% by Feb. 1, 75% by Sept. 1, 85% by Oct. 1 and 95% by Nov. 1. The storage reached 99.3%, full higher than the government’s new goal, on Nov. 2, 2022.

[15] By making such assumptions, we allow storage to be withdrawn down to a level that is realistically manageable to prepare for the next winter, in that we limit the storage from falling to zero.

[16] We assume an average summer for scenarios (1) and (2) and a hotter than normal summer for scenario (3).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.