After a brief delay, the OPEC+ group met on Nov. 30 and agreed to extend production cuts through the first quarter of 2024.

The prospect for additional cuts was widely anticipated, but the market has not been impressed by the meeting’s outcome: Oil prices on Dec. 4, when this commentary was written, were below pre-meeting levels with Brent crude — the international benchmark — near $78 per barrel.

Why are markets unimpressed? My read is that both the process and volumes are contributing to the disappointment. But that doesn’t mean the OPEC+ cuts are unimportant.

First, the process.

The group was originally slated to meet on Nov. 26 before the start of the UN Climate Change Conference (COP 28) in Dubai. Markets were widely anticipating that Saudi Arabia and Russia would extend the voluntary cuts they have had in place most of the year through the first quarter. This would have been in addition to new production quotas for the entire group that were announced in June — seeking to better align with individual members’ production capacity. These new quotas were slated to take effect Jan. 1 for the entirety of 2024.

But on Nov. 26, it was suddenly announced that the group was postponing its meeting until Nov. 30. Initial press reports indicated that some African producers wanted to revisit the lower quotas they had been assigned for 2024.

However, something else was afoot. Amid growing fears of an over-supplied market and deteriorating commodity investor sentiment, word began to circulate that the group felt the need for additional action.

The official OPEC press release simply stated that, based on an independent review process laid out in June, new quotas had been agreed for Angola, Congo, and Nigeria. In addition, it was announced that Brazil had joined the OPEC+ group.

But separately, individual members then began to announce coordinated, additional cuts for the first quarter — a similar dynamic to the voluntary cuts announced in April. Saudi Arabia and Russia would extend their existing voluntary cuts, as the market had expected. Additionally, OPEC members (Iraq, the United Arab Emirates, Kuwait, and Algeria) and non-OPEC members (Kazakhstan and Oman) announced cuts, as they had done in April — Gabon participated in the April voluntary cuts but not last week’s. As was the case previously, countries already falling short of their production quotas did not participate in voluntary cuts.

The nature of these cuts is complicated. Most notably, in extending its voluntary cuts, Russia announced it would reduce exports, not production, and split its 500,000 b/d reduction between crude oil (300,000 b/d) and refined products (200,000 b/d). Moreover, the cuts are not relative to the country’s official baseline production figure, but rather relative to export levels for May/June 2023.

In addition, the new cuts (excepting Saudi Arabia and Russia) are relative to the quotas that will take effect in January, rather than cuts from current production.

Another source of confusion is Brazil’s membership. The group’s interest in adding Brazil is understandable — after the United States, Brazil has been one of the world’s largest sources of supply growth. But what exactly is the nature of Brazil’s participation? After the meeting, the chief executive of national company Petrobras said the country would not accept any production restrictions. This would be similar to Mexico, which is an original OPEC+ member but does not accept production targets. Then, President Lula da Silva said at COP28 that Brazil joined OPEC+ as an observer “because we need to convince the countries that produce oil that they need to prepare for the end of fossil fuels.”

The other action item on the meeting agenda was to revisit quotas assigned to African countries that were chronic under-producers before the realignment of quotas took place in the Fall: Nigeria, Angola, and Congo. Nigeria has been able to boost output over the past few months and therefore had its January quota boosted, though the new quota remains well below the current one; Angola could not boost output and was given an even lower quota which it is protesting. Since both countries already produce well below their target, these quota assignments will not matter in terms of barrels to the market.

And then, questions about barrels.

The continuation of Saudi cuts is relatively straightforward — and, again, unsurprising. But Russia’s plan to continue basing its cuts on exports, and to split the cuts between crude oil and refined products, will make tracking and verification more challenging at a time when the G7 countries and oil analysts are already struggling to track Russian exports given the growing use of a “dark fleet.”

On paper, the other countries’ voluntary cuts are also straightforward: While each country announced its voluntary cut in barrels, I calculate that they are all 5% below the new Jan. 2024 targets.

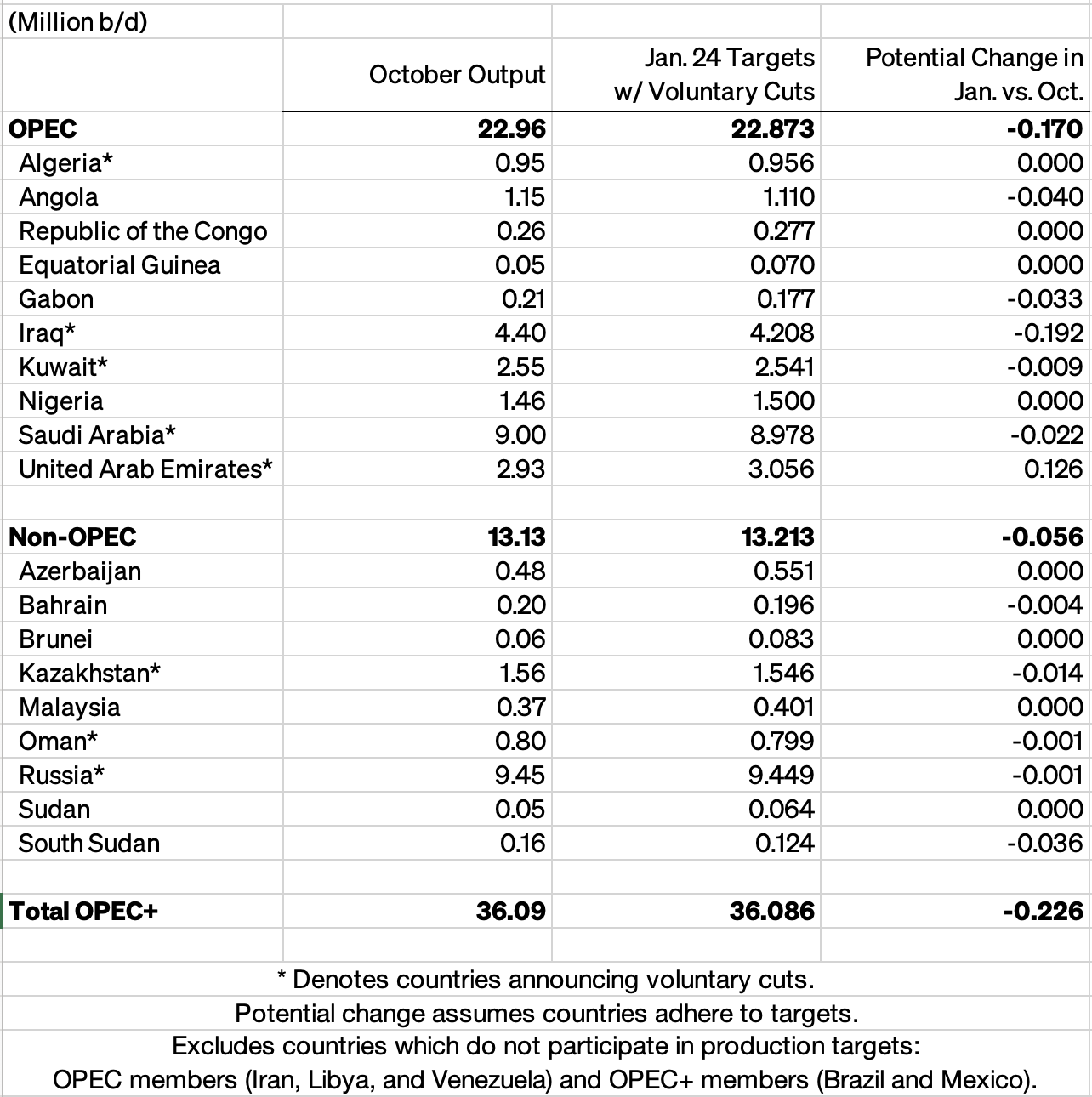

Note that each of the countries participating in voluntary cuts was slated to receive a higher quota in January. Since the voluntary cuts are based on those new quotas, we are unlikely to see material reductions relative to current production in most cases (Table 1). Indeed, for the UAE, its January quota will increase significantly (+340,000 b/d, 12%) as part of the realignment of quotas brokered earlier this year. A 5% cut from that new figure (-163,000 b/d) will still leave room for production to increase in January.

Additionally, Iraq — which agreed to a voluntary cut of 223,000 b/d — has been significantly over-producing recently. Its compliance with production cuts remains to be seen.

Netting out these dynamics, January OPEC+ production is unlikely to be significantly different from current levels, as shown in the accompanying table.

Still, the meeting’s outcome is significant.

The OPEC+ press release notes that the announced cuts for 1Q24 total 2.2 million barrels per day, relative to the new 2024 targets and taking into account voluntary Saudi/Russian cuts previously announced. It’s just that the market had already anticipated the roll-over of the Saudi and Russian cuts. Combined with the observation that the additional voluntary cuts are likely to result in a minimal reduction relative to current (October) levels, this helps to explain the market’s blasé reaction.

This is still a very different situation than would have been the case if the Saudi/Russian voluntary cuts had been allowed to expire and other quota increases went through as planned. The U.S. Department of Energy and the International Energy Agency both assess that the oil market in 2024 will require continued OPEC+ production discipline to keep the oil market from becoming over-supplied.

In that sense, while the OPEC+ meeting may not have boosted prices, it is will reduce the risk of additional price declines. But the difficulty in reaching an agreement last week could augur a year of difficult meetings ahead for the group if supply/demand developments play out as many analysts expect. While Saudi Energy Minister Prince Abdulaziz bin Salman has opened the door for the cuts to be extended beyond 1Q24, the group — at this point — does not plan to meet again until June 1.

Table 1 — OPEC Targets and Production

Note: “Jan. 24 Targets w/ Voluntary Cuts” is calculated based on the cuts detailed in OPEC’s press release and the original Jan. 2024 targets as amended for Russia, Angola, Congo, and Nigeria — with the exception of Saudi Arabia. For the latter, the original voluntary reduction of 500,000 b/d offered in April is included, as well as the 1 million b/d cut offered in June because its current production reflects both.

Members of the Baker Institute Center for Energy Studies receive advance access to expert analysis and commentaries. Learn more about becoming a member of the Energy Forum.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.