Author(s)

Will OPEC+ begin to reverse large production cuts at its June 1 meeting? In large part, it will depend on whose oil market outlook is closest to the mark.

At its most recent meeting, on April 3, the OPEC+ Joint Ministerial Monitoring Committee endorsed the ongoing extension of voluntary production cuts through the second quarter of this year. These cuts were discussed when they were first agreed to at the end of November 2023. These voluntary cuts — over 2 million barrels per day (Mb/d) by a subset of the group’s membership, led by Saudi Arabia and Russia — are in addition to previous reductions that are slated to remain in place throughout 2024.

As recently explained, OPEC+ has been forced to extend its “temporary” production cuts repeatedly. Will the June 1 meeting result in yet another instance of what must be a disappointingly familiar ritual for the OPEC+ group?

In the oil market, June 1 is a long way off! However, rising tensions in the Middle East have left the market on edge and worried about heightened geopolitical risks to supply. Given the importance of oil price movements to producers and consumers, a closer look at the factors likely to drive OPEC+ decisions is always relevant.

Crucially, the outlook for global supply and demand growth this year is unusually uncertain. Significantly, the outlook for demand growth among the three main public forecasters — OPEC, the International Energy Agency (IEA), and the U.S. Energy Department (DOE) — varies widely. The question of demand — and also supply outside the OPEC+ group — will play a critical part in driving the OPEC+ course of action, and for oil prices, over the rest of this year.

Where Do We Stand? Strong OPEC+ Discipline, yet Rising Inventories

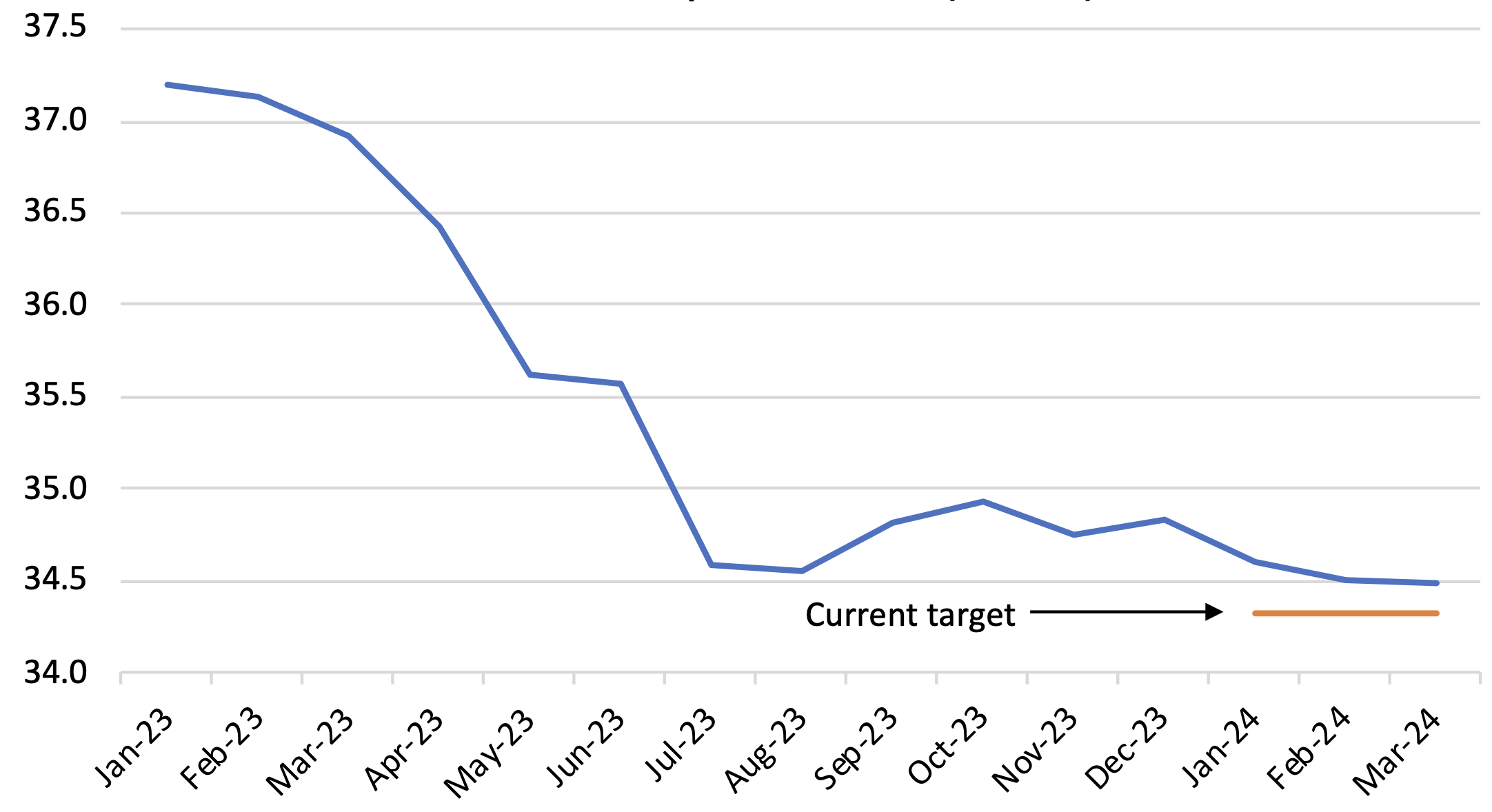

Compliance with the ongoing OPEC+ production cuts remains solid. A monthly production survey by SPGlobal puts the group’s current production at less than 0.2 Mb/d above the collective production target (Figure 1).

Figure 1 — OPEC+ Crude Production (Mb/d)

Note: Excludes Angola (which left OPEC January 2024) and Mexico (which does not accept OPEC+ production targets). Also excludes OPEC members not assigned production targets

Despite the high level of compliance, the IEA’s monthly Oil Market Report shows that global oil inventories have increased in the first quarter. To be fair, the IEA also states that commercial inventories among its member countries remain below average, after falling slightly in 2023. Recent weekly U.S. data show that inventories are continuing to build so far in April.[1]

With strong OPEC+ compliance and below-average inventories, oil prices have drifted higher this year, with an added push from the increased Middle East tensions. The international benchmark Dated Brent rose from $78 per barrel at the beginning of the year to a peak of $93 on April 12 as markets anticipated an Iranian-led attack on Israel, which took place April 13. Prices since then have dipped as regional actors appear — for now — to be trying to avoid further escalation; as of this writing (April 22) Brent stands near $87, which is close to its level before Israel’s attack on Iranian Revolutionary Guard officers in Syria in early April.

As a result of large, ongoing production cuts, global spare capacity has risen significantly. The IEA reports that OPEC+ countries now hold roughly 5.5 Mb/d of spare production capacity, an increase of around 3 Mb/d over the past year or so. OPEC Middle East countries, led by Saudi Arabia and the UAE, account for virtually all of that figure (90%). The large buffer of spare production capacity has helped to mute concerns about risks to supply even as Middle East tensions have ratcheted up and G7 sanctions on Russian oil exports remain in place.

Short-Term Outlooks: OPEC Stands Out as a Demand Bull

What is the outlook for oil markets over the remainder of 2024? There is an unusually wide range of forecasts among the most widely-followed and publicly-available sources: The U.S. DOE, the IEA, and OPEC each produce a monthly oil market outlook.[2]

The three outlooks are broadly similar in their view of non-OPEC production growth this year, which is widely expected to slow from the very strong growth seen in 2023. In particular, all three groups expect U.S. growth to slow significantly. Projected non-OPEC growth for 2024 among the three groups is tightly bunched around 1 Mb/d, with the U.S. DOE at the low end of the range at 0.8 Mb/d and the IEA the high end at 1.2 Mb/d. OPEC sits exactly in the center of the trio, with projected non-OPEC supply growth of 1 Mb/d.

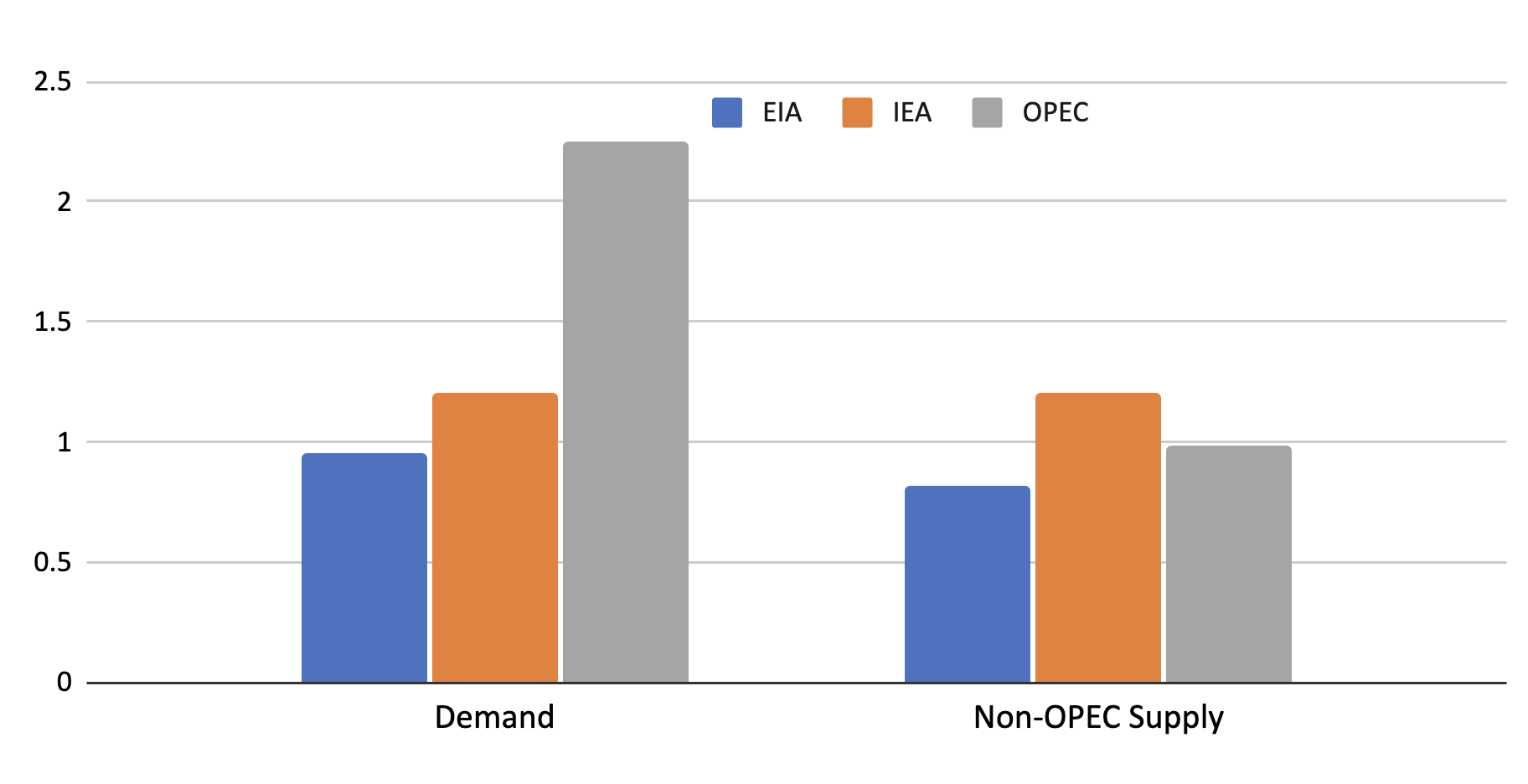

By far the largest differences among the three forecasters for 2024 are in their global oil demand growth projections. After seeing strong global growth of at least 2 Mb/d in 2023 (the tail end of the global recovery from COVID-19), the U.S. DOE and IEA both project a significant slowdown this year, with 2024 demand growth projected at 1 and 1.2 Mb/d, respectively. OPEC, in contrast, forecasts continued strong demand growth of 2.3 Mb/d (Figure 2).

Figure 2 — Oil Market 2024: Global Growth Projections (Mb/d)

It is important to point out that the IEA and OPEC do not make projections on OPEC production — instead both groups calculate a market requirement for OPEC output (essentially the difference between demand and non-OPEC supply), but they take the position that decisions on future OPEC production are made by OPEC itself. In a similar vein, neither group forecasts prices, which of course would depend on OPEC’s production decisions. Only the U.S. DOE projects OPEC production — predicting no change in 2024 versus 2023 output —as well as prices: DOE projects them to rise from an average of $82 per barrel last year to $89 this year.

While the IEA and OPEC do not forecast OPEC production, there are indications in each group’s reports of what they are thinking.

The IEA notes that additional supply “volumes from the United States, Brazil, Guyana and Canada alone could come close to meeting world oil demand growth for this year and next,” and that the market requirement for OPEC crude oil will be essentially unchanged this year. It adds that “OPEC+ supply is projected to fall by 820 kb/d, provided cuts are maintained through the second half of the year” (emphasis added).

In contrast, OPEC (with a much stronger forecast for global demand growth) reports that the market requirement for OPEC+ supply will grow by 0.9 Mb/d this year. While the group does not forecast OPEC production, it does project non-OPEC output, including for members of the OPEC+ Declaration of Cooperation. And here there is a big hint: OPEC projects that Russian supply will rise by about 0.4 Mb/d in the third quarter — that is, once the current voluntary production restraint is scheduled to expire at the end of the second quarter.

Additionally, OPEC flags the need to keep an eye on oil demand: “The robust oil demand outlook for the summer months warrants careful market monitoring.” Many observers have interpreted this as setting the table for the group to begin relaxing voluntary cuts when they meet on June 1. A different interpretation, however, is also possible: With the OPEC demand growth forecast so much larger than the consensus, they may be preparing to reduce their demand forecast, closer to the consensus figure. A downward revision for demand growth would call into question the need for increased supply in the second half of this year.

Will OPEC+ Voluntary Cuts Be Extended?

As mentioned above, June 1 is a long way off. Tensions in the Middle East could once again flare, and in a worst-case scenario, threaten regional production or exports. Additional G7 sanctions, or Ukrainian attacks, could impact Russian exports. Views of global fundamentals will continue to evolve: The U.S. DOE, IEA and OPEC will all publish one more market outlook before the OPEC+ meeting on June 1, and the DOE will continue to publish weekly data on domestic supply, demand, and inventories. Crude oil price movements will be critical as key OPEC+ members struggle to manage their budgets.

Another date to mark on your calendar — May 14: This is the date of the next OPEC Monthly Oil Market Report. If the OPEC group maintains its forecast for strong oil demand growth, it could portend a relaxation of voluntary production cuts. If it reduces its oil demand forecast to be more closely aligned with the other forecasters, the long hoped-for return of OPEC+ production may be further delayed.

Notes

[1] While all three forecasters’ supply/demand balances imply that global inventories should have fallen in the first quarter, here I am citing estimates of actual inventory changes. A discrepancy between implied and observed inventory changes may be an indicator that underlying supply and demand levels may be subject to future revision. For better or worse, forecasting is both an art and a science.

[2] The following discussion is based on the groups’ April oil market outlooks. Note that the International Energy Agency (IEA)’s monthly report and its related data require a subscription, but a summary is freely available at the link provided.

Members of the Baker Institute Center for Energy Studies receive advance access to expert analysis and commentaries. Learn more about becoming a member of the Energy Forum.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.