Introduction

Saudi Arabia’s launch of an oil price war in March 2020 left many observers wondering about the wisdom of exacerbating stress on the global oil market from an enormous demand shock due to the Covid-19 pandemic. But there are several factors that suggest—even if retroactively rationalizing the Saudi move—logical reasons for the Saudi action.

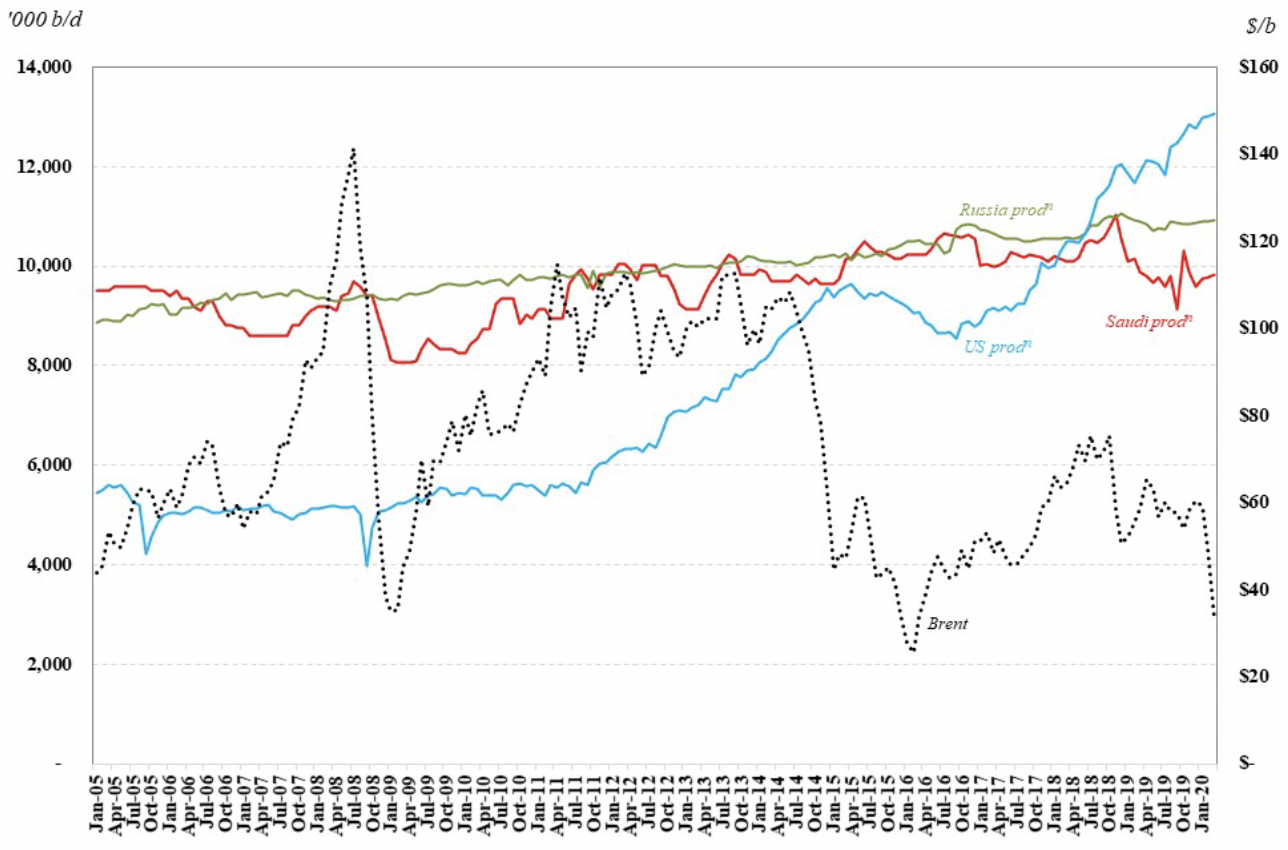

As depicted in Figure 1, Saudi production since July 2016 has been declining, except for a short-lived increase in late 2018. The Saudi decline has been accompanied by a dramatic increase in US shale production over the same period, to the tune of 4.4 million barrels per day (Mb/d). This occurred even as oil prices generally declined since mid-2018, which contributed to thinking within the kingdom that its influential role as the world’s strategic supplier of oil was being undermined by the relentless rise of US shale. One way of reestablishing Saudi primacy is to seek a larger share of the global market by cutting prices and chasing out higher cost production, despite the short-term pain of a price war.

Figure 1 — Crude and Lease Condensate Production in the US, Saudi Arabia, and Russia, and Brent Crude Price (January 2005–March 2020)

However, the Saudi price war strategy appears to have underestimated the devastating effect of the Covid-19 pandemic on oil consumption. The International Energy Agency and other observers have estimated that 20 Mb/d or more of global consumption could be temporarily lost, due to dramatic reductions of transportation and other sources of oil use.

Against the backdrop of such a massive collapse, Saudi Arabia may not need a price war to achieve its aims. The virus-induced demand shock has already pushed prices below levels at which high-cost production is economically viable. Moreover, the massive oversupply to the market is creating doubts about the ability of inventory capacity to absorb the excess production.1 If, as seems likely, global storage capacity is exhausted, there will be continued downward pressure on price. In short, market effects alone ought to achieve Saudi objectives.

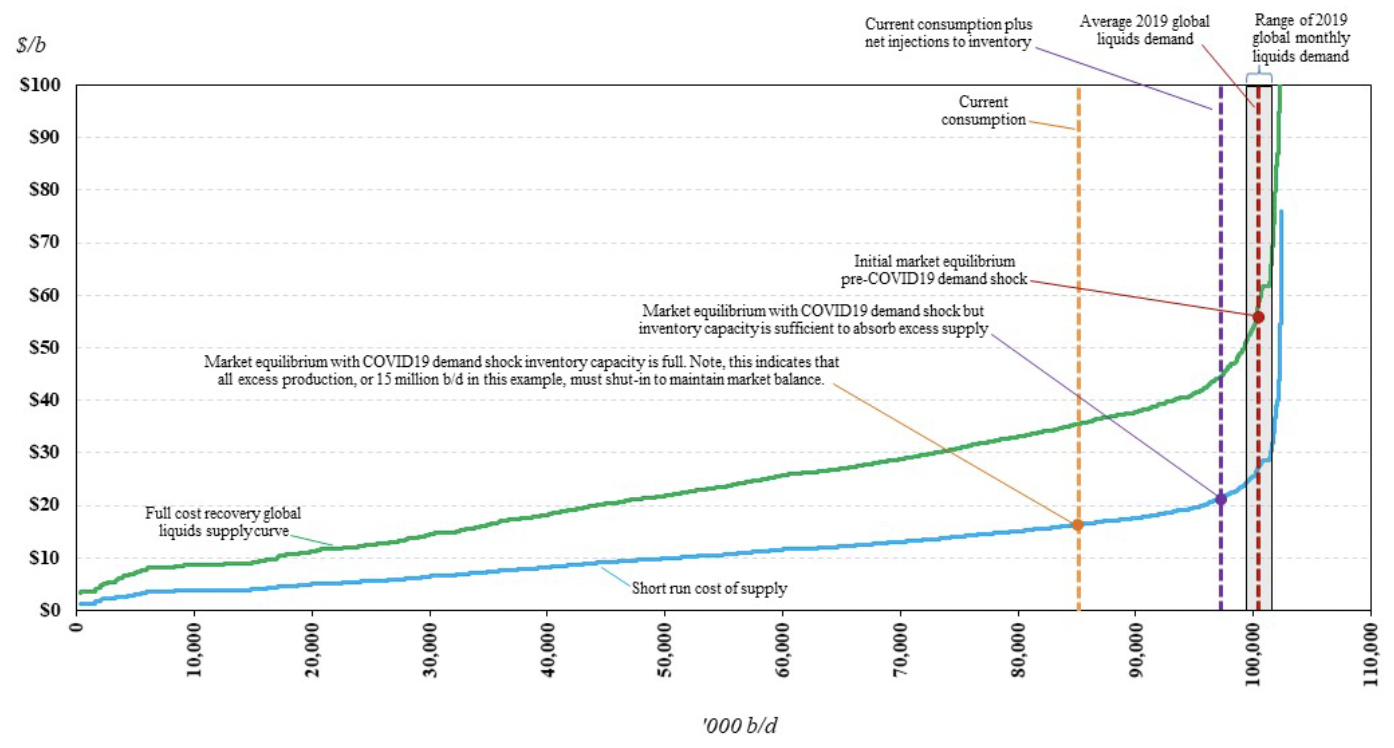

The global liquids supply curve below (Figure 2) illustrates the depth and severity of the Covid-19 demand shock. Before the Covid-19 virus struck, the global liquids supply curve indicated full cost recovery market equilibrium in the range of $50-$65/b, depending on the level of consumption, which fluctuated monthly around the annual average (as indicated) throughout the year. If Saudi Arabia and Russia boost output as promised (an additional 3 million to 3.5 million b/d), that supply would reflect levels in line with a competitive, inframarginal producer. From Figure 2, we can infer that such an increase in supply from low-cost producers would drive a new long-run market equilibrium in the $40-$45/b window, although prices would likely dip lower in the short term as higher-cost supply is chased out.

But that’s not the whole story. The dramatic, unexpected collapse in oil consumption has placed the market in a very different short-run situation. The extreme oversupply to the market will drive price down to a point that still indicates market clearing, but under very different circumstances. Specifically, the demand level at which the market clears reflects consumption plus net injections to inventories. In a “normal” year, net injections roughly balance to meet seasonal demand fluctuations. However, with so much surplus oil being produced, it’s going into inventories. If storage fills, prices would need to fall even more to shut-in production.

Of course, there are regional constraints that will exert pressures on local prices and production, but Figure 2 is meant to reference the global benchmark equilibrium rather than regional prices. In any case, the market clearing equilibrium will reflect short-run production costs and the ability of storage to soak up excess supply. If consumption remains very low, storage will fill. Lack of storage generates a different source of pressure, leading to further price collapses until firms shut-in production so that the market balances.

Figure 2 — Global Liquids Market Equilibrium in the Presence of an Extreme Demand Shock

The magnitude of production shut-ins depends on how far consumption falls relative to contemporaneous production and how rapidly storage fills. Regardless, the combined effects of these simultaneous stresses—Covid-19 demand destruction and increased output from Saudi Arabia and Russia—place immense pressure on storage capacity and the global oil market.

Punishment Strategy: The Price War

Why launch a price war? A price war does not appear to have been the agreed-upon strategy of Riyadh and Moscow going into the March OPEC+ meeting. At the time, the full extent of demand destruction from Covid-19 had not been realized. Regardless, energy ministers from Saudi Arabia and Russia said that the two countries would stop abiding by OPEC+ production quotas when they expired April 1. Both promised additional increases in production, with Saudi Arabia vowing to bring all its spare production capacity online to reach a production record of 12.3 million b/d. If followed through as announced, the Saudi and Russian increases would add over 3 million b/d of low-cost oil to global supply.

Normally, Saudi Arabia, the world’s dominant oil exporter and de facto leader of the OPEC cartel, uses its spare capacity to reduce volatility in oil markets and protect the global economy from a volatile, cyclical industry.2 Maintaining spare capacity also allows Riyadh to achieve the more self-serving goal of protecting long-run demand for oil and maintaining oil’s price advantage over alternate fuels and technologies. In March, however, Saudi officials vowed to deploy spare capacity not to ease volatility but to exacerbate it. In other words, to launch a price war.

How does a price war work, in theory? In a simple game theory construct, a dominant producer like Saudi Arabia has the ability to extract monopoly rents from residual demand (or demand not met at a particular price by all other producers) due to it being a low-cost producer. This strategy implies that withholding production (i.e., maintaining “spare capacity”) is optimal for the dominant producer. Withholding production results in a higher price than would be realized if the dominant firm were acting as a competitive, inframarginal player.

In the case of Saudi Arabia, if the kingdom’s oil strategists feel that a production cut would yield excessive rewards to competitors, they can order an increase in production as a deterrent. The increase is meant to demonstrate the kingdom has a credible tool of punishment for either low-cost producers who do not join the kingdom in making proportionate sacrifices, or high-cost producers who take advantage by ramping up output.

As mentioned above, US shale production, with costs triple or quadruple those of Saudi Arabia or Russia, has benefitted greatly from the kingdom’s constraints on oil production. The same punishment strategy might be used to discipline countries that cooperate inconsistently in the cartel’s production management. In today’s context, think Russia.

The Saudis have previously launched price wars many times, most recently in 2014, when OPEC members refused to cut production amid declining prices and rising US shale output. The most devastating price war took place in 1986, as punishment for rampant OPEC quota cheating and a realization that Saudi cuts were encouraging high-cost production in the US and North Sea.

A price war is a periodic and necessary part of dominant producer strategy as it re-exerts the promise of a credible threat to other low-cost producers as well as to higher cost competitive (or “fringe”) producers. The end goal is that the sacrifice in short-term revenues for the dominant player eventually begets a long-term advantage through an increase in market share without undermining prices because alternative supplies are discouraged by the threat—and occasional reality—of price wars.

However, as “fringe” supply becomes more elastic—as shale has done—it becomes more responsive to changes in market price. This pushes the dominant firm to increase production in a bid to capture increased market share, albeit at a lower price and higher sustained level of production. Hence, if the low-cost producers of the world begin to behave more competitively, the short-run punishment strategy leads to a lower long-term price.

Opportunism and Overreach

Launching a price war typically entails some level of strategic advance planning along with a triggering mechanism. Evidence around the current price war, however, suggests it is based on an opportunistic Saudi reaction to OPEC’s inability to secure sufficient production cuts in the OPEC+ meeting in Vienna in early March.

Heading into last month’s OPEC+ meetings, the market context was not generally understood to be as bleak as we now see it. Although analysts factored in some impact on global demand from Covid-19, a rough consensus found only a modest loss of the roughly 1 Mb/d of worldwide oil demand growth in 2020 that had been forecast before the onset of the virus.3 Based on that consensus, Saudi Arabia had been advocating for a collective production cut of 1.5 Mb/d, on top of the existing cuts of about 1.7 Mb/d that had already been put in place over the previous two years.

Had that scenario been accurate, the Saudis’ suggested cuts would have been sufficient to maintain the oil market balance in 2020, even with expected strong growth in production outside of OPEC. In an effort to promote the cuts, press reports indicated that the Saudis were willing to accept a disproportionately large reduction in their own production.4

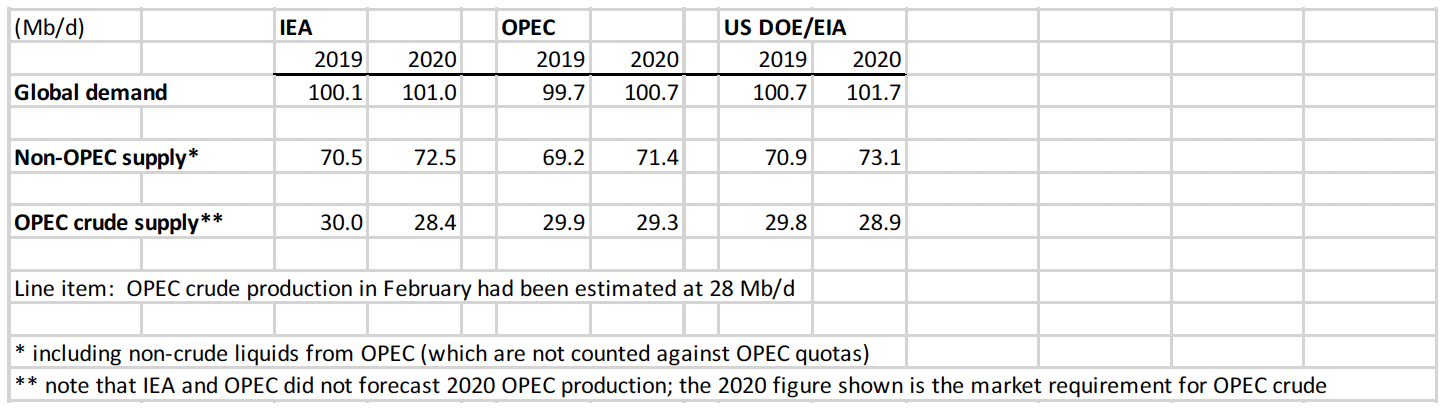

Figure 3 — Global Oil Market Analysis Available for the March OPEC+ Meetings

However, Russia had long signaled its reluctance to cut further. As the Covid-19 impact on global demand began to emerge, Russia used the emerging uncertainty to advocate for maintaining the existing production cuts until the OPEC+ countries had more clarity on the 2020 oil market. (Russian officials pointed to concerns about growing US oil market share and the fact that Russian individuals and firms were being targeted by US sanctions.)

When Saudi efforts to coordinate a joint position with Russia failed, the kingdom pushed through an agreement among OPEC members to cut production along the lines of their original proposal, leaving Russia with a “take it or leave it” option. Russia walked away, with its energy minister, Alexander Novak, saying that the existing production cutting agreement would not be renewed, but rather allowed to expire April 1.

It was then that Saudi Arabia responded with an abrupt about-face, announcing the record production levels of 12.3 million b/d that began in April. Riyadh said it would maintain that level in the coming months. Further, the Saudi oil minister ordered Saudi Aramco to raise its maximum sustainable production capacity from 12 million to 13 million barrels a day, earmarking $30 billion in capital investment to do so.5 At the same time, other OPEC+ producers began adding supply to the market as well, most notably Russia and the UAE.6

However, alarm over Covid-19’s spread began to ignite ever more drastic action in afflicted countries, including the United States, the world’s largest oil consumer. As country after country ordered its citizens to shelter in place, an unprecedentedly large swath of global transportation was idled. The virus’ effect on oil demand was thus dramatically stronger than that forecast in early projections.

Estimates of the impact are continuing to move rapidly, with the head of one of the major oil trading houses saying in early April that global oil demand may have been reduced by one-third, or 35 million b/d.7 Average yearly losses for the world as a whole depend on the severity and duration of the crisis. Most analysts now believe that global demand is likely to see the biggest annual decline ever, surpassing the decline of 2.6 Mb/d seen in 1980.8

From this perspective, Riyadh’s launching of a price war looks like a major overstep. Adding large volumes of supply amid a collapse in demand pushed down the oil price to $20 by March 30, the lowest level since 2002. Both the US and global benchmarks (WTI and Brent) have fallen by two-thirds since the beginning of the year. While prices later rebounded on speculation that OPEC+ members and other producers including the US may intervene to reduce supply, the discussion above makes clear that prices could fall further as storage fills, leaving oil with no place to go and forcing producers to shut-in wells.

The U.S. Response

As oil prices collapsed, President Donald Trump’s initial reaction was to applaud the prospect of lower prices at the pump. But as the impact on the domestic oil sector became apparent, the tone in Washington shifted, spurring an array of policy proposals that demonstrate the desperation in the US industry and among political representatives of oil-producing states. The proposals also pointed up the policymaking confusion in the United States around its simultaneous positions as the world’s No. 1 oil consumer and producer. Should policy favor consumer interests by encouraging low prices? Or should it cater to producer interests by fighting low prices?

Trump announced on March 13 a plan to support domestic producers by purchasing 77 million barrels of US crude oil to fill the nation’s Strategic Petroleum Reserve. However, the Energy Department’s solicitation of offers for an initial purchase of 30 million barrels was withdrawn because it was not funded in Congress’ stimulus legislation. The administration also said it was considering policies such as low-interest loans and additional tax incentives to support domestic producers, but these measures were also left out of the stimulus.

On March 20, Texas Railroad Commissioner Ryan Sitton announced he had discussed constraints on Texas oil production with OPEC’s Secretary General Mohammed Barkindo, and said that the RRC retained legal authority to enforce production cuts in Texas. Such an action would essentially render Texas a de facto member of OPEC+, and could run contrary to the Sherman Antitrust Act, at least in spirit.9 Sitton’s comments divided the industry, attracting support from firms such as Pioneer Natural Resources and Parsley Energy, along with opposition from a group of major US producers, along with RRC chairman Wayne Christian and the American Petroleum Institute, the main industry lobby.10

On March 23, US Secretary of Energy Dan Brouillette acknowledged that his agency was in talks with Saudi Arabia, and was considering, among many other options, whether it might join the kingdom in a US-Saudi oil alliance.11 A similar alliance was mentioned in a letter to the administration from US senators of oil-producing states, who argued that Saudi Arabia should leave OPEC, a proposal that would probably cause the cartel to fail.12 It is unclear whether the envisioned alliance would encourage collusion between Washington and Riyadh over production levels or prices; again, such practices would be hard to square with the Sherman Act. Other suggestions being proffered around Washington include using US sanctions or tariffs to punish Saudi Arabia (and Russia) for “dumping” crude oil onto the global market.13 On March 26, US Secretary of State Mike Pompeo appealed to Saudi Arabia—the current president of the G20—to “rise to the occasion” and call off its price war. Pompeo, a key proponent of the Trump administration’s “America First” strategy—which rejects magnanimous policy actions not explicitly in the national interest—was essentially pleading with Saudi Arabia to make the sort of sacrifice that would run contrary to Trump administration doctrine.14 The subsequent G20 statement made no mention of the oil market.15

Finally, Trump tweeted on April 2 that he had spoken with Saudi Crown Prince Mohammed bin Salman, and that the Saudi leader had spoken with Russian President Vladimir Putin and agreed to cut oil production. Although both Saudi and Russian officials denied an agreement had been reached, OPEC did announce its intention to hold a virtual meeting with OPEC+ partners and other interested countries in early April.

What’s Next?

The collapse in oil prices is forcing the world’s producers to slash spending, halt drilling, and shed workers. The US administration and the G7 countries as a group have criticized the OPEC+ price war as adding unnecessary volatility when the global economy is already reeling under the Covid-19 pandemic.

The pain extends even to Saudi Arabia, where higher production will not offset the revenue lost by the price collapse. The kingdom has begun to cut government spending and has raised its debt ceiling significantly. Funds needed to drive the ambitious reforms contained in the Vision 2030 and National Transformation Plan were being pinched. If the Saudi leadership is focused on maintaining sufficient revenues in the next year or two to fund its reforms, a return to a managed market would seem to be the revenue-maximizing approach.

The future path of the oil market will depend in great deal on both the strategic calculus of the Saudi leadership and the practical matters of funding government budgets as well as long-term national transformation.

Conclusion

Amid one of the sharpest oil price declines ever seen, the United States finds itself in a new position and unsure how to react. In the past, it was easy: as a large importer, lower prices were good for the US economy. With the US now the world’s largest producer and consumer, the country’s political leaders have struggled to devise policies that balance the needs of both producers as well as consumers. The raft of contradictory and unfamiliar proposals emerging in the wake of the price crash demonstrates that policymaking consensus about the American role in oil markets and, indeed, what constitutes appropriate governance and guidance of the US oil industry, were yet to be decided. But understanding both the strategic and tactical considerations of its long-time ally Saudi Arabia will be a key factor for the success of US policy.

Endnotes

1. See, for example, John Kemp, “Global oil storage to fill rapidly as consumption plunges,” Reuters, March 27, 2020, https://www.reuters.com/article/us-oil-prices-kemp-column/column-global-oil-storage-to-fill-rapidly-as-consumption-plunges-kemp-idUSKBN21E2BR.

2. Axel Pierru, James L. Smith, and Tamim Zamrik, “OPEC’s Impact on Oil Price Volatility: The Role of Spare Capacity,” The Energy Journal 39, no. 2 (2018).

3. At the time, most analysts were expecting a deep impact on Chinese oil demand in the first quarter of 2020, a modest impact elsewhere, and a relatively swift recovery during the second half of the year. For example, the IEA’s February Oil Market Report (the current edition at the time of the OPEC+ meeting) projected a small decline in global oil demand in the first quarter, but recovery thereafter.

4. The Saudi proposal was for total OPEC+ cuts of 1.5 Mb/d, of which OPEC would take 1 Mb/d, and within OPEC, the kingdom would accept a cut of 400,000 b/d. Heading into the meeting, Saudi Arabia already had been producing well below its target level in an apparent effort to support prices. Estimated production in February (based on a contemporaneous survey of industry analysts conducted by S&P Global) was 9.69 Mb/d vs. the kingdom’s allocation of 10.14 Mb/d.

5. Verity Ratcliffe, Anthony Di Paola, and Matthew Martin, “Saudi Arabia Pledges to Expand Oil Output Capacity,” Bloomberg News, March 11, 2020, https://www.bloomberg.com/news/articles/2020-03-11/aramco-will-boost-oil-output-capacity-to-13-million-barrels-day.

6. Russian officials initially said that they planned to add 300,000 b/d of production in a short period, but later backed away from that plan.

7. See Grant Smith, Javier Blas, and Olga Tanas, “Trump Meets U.S. Oil Leaders After OPEC+ Urges Cuts to Stem Rout,” Bloomberg, April 3, 2020, https://www.bloomberg.com/news/articles/2020-04-03/opec-to-hold-virtual-meeting-monday-as-trump-pushes-for-cut.

8. BP Statistical Review of World Energy, 2019 edition.

9. Corporate Finance Institute, “Sherman Antitrust Act,” https://corporatefinanceinstitute.com/resources/knowledge/finance/sherman-antitrust-act/.

10. The Railroad Commission was to discuss the proposal on April 14, 2020. See, for example, Amy Harder, “Texas oil regulators poised to debate historic production controls,” Axios, https://www.axios.com/texas-oil-regulators-production-controls-1e75b92c-71fa-435b-b9ae- 3569a7f4d80a.html.

11. Stephen Cunningham, “U.S.-Saudi Oil Accord One Idea Discussed, Energy Secretary Says,” Bloomberg, March 23, 2020, https://www.bloomberg.com/news/articles/2020-03-23/u-s-saudi-oil-accord-one-idea-discussed-energy-secretary-says.

12. US Senators Lisa Murkowski et al. to US Secretary of State Mike Pompeo, March 25, 2020, letter, Congress of the United States, https://www.energy.senate.gov/public/index.cfm?a=files.serve&File_id=36C4A67D-7C57-49B2-BEF2-4EB95E441B99.

13. “Domestic Energy Producers Alliance Asks Commerce Secretary to ‘step up’,” news release, March 19, 2020, https://depausa.org/domestic-energy-producers-alliance-asks-commerce-secretary-to-step-up/.

14. “Pompeo urges Riyadh to ‘stabilise energy markets’,” Middle East Eye, March 25, 2020, https://www.middleeasteye.net/news/pompeo-urges-riyadh-stabilise-energy-markets-call-mbs.

15. “Extraordinary G20 Leaders’ Summit: Statement on COVID-19,” via G20 Information Centre, University of Toronto, March 26, 2020, http://www.g20.utoronto.ca/2020/2020-g20-statement-0326.html.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.