Author(s)

Ask any economist about the gross receipts tax (GRT) and you are likely to get a frown of disapproval. However, in 2017, four states—Oregon, Oklahoma, Louisiana, and West Virginia—sought to enact a statewide GRT. Although none of the proposals was implemented, Oregon has indicated that it might propose creating a GRT again in the next legislative session,1 and West Virginia’s proposal was approved by the legislature but ultimately not enacted.2

In Texas, the franchise tax, a hybrid form of the GRT, has been the subject of several lawsuits. For example, the Texas Supreme Court in September heard oral arguments for a case in which the petitioner claimed that the 10-year-old franchise tax is actually an income tax. The unpopularity of the tax is widespread, leading policymakers to propose repealing it; however, such efforts were unsuccessful in the 2017 legislative session. How can we explain that four states that do not have the GRT are seeking to enact it, while Texas is trying to repeal the GRT? What led to these seemingly conflicting trends?

What Is a GRT and What Has Caused the Recent Surge of State GRT Proposals?

Five states (Ohio, Texas, Delaware, Washington, and Nevada) currently have a statewide GRT. Besides Delaware, these states do not explicitly refer to the tax as a GRT—Ohio refers to the GRT as the commercial activity tax (CAT), Texas calls the state GRT a franchise tax or margin tax, Washington named its GRT as the business and occupation (B&O) tax, and Nevada’s GRT is the commerce tax. New Mexico has a GRT, but its characteristics are more similar to a broad-based sales tax.3

Typically, states impose a GRT as a privilege of doing business in the state. In its most general form, the base of the GRT comprises the receipts from all sales of goods and services, and applies to all businesses within a state. A GRT does not provide allowances for costs incurred by sellers or offer exemptions to particular types of sales. Business entities simply apply a single tax rate to the sales receipts to calculate the taxes owed.4 None of the current state GRTs fit squarely into this description—they either exclude certain types of sales or entities, tax different businesses at different rates, or allow various deductions.

The recent proliferation of GRT proposals is not new. Several states went through similar exercises in the early 2000s; New Jersey, Michigan, and Kentucky even passed state laws adopting a GRT, but they were later repealed.5 In the first decade of this century, states considered GRTs to generate revenue, enhance business competitiveness, or implement alternatives to the administratively burdensome state corporate income tax (CIT). Similar objectives drove the 2017 wave of GRT proposals—all four states have budget deficits, and additional revenue is crucial. They also need to reform their states’ outdated tax systems to match current economic realities. In some ways, states may find it easier to tax services by enacting a GRT than by expanding the existing sales or income tax base. The GRT also seems easier to understand and explain than other taxes. Additionally, the GRT’s misleadingly low statutory tax rates are more acceptable at first glance, despite the hidden pyramiding effects that lead to higher effective tax rates (ETRs), as discussed in the next section.

Several states originally based their GRT proposals on Ohio’s CAT. What makes the Ohio CAT an attractive version of the GRT is that it replaced more unpopular taxes and has a broad-base, low-rate structure. Specifically, the CAT replaced the state’s franchise and personal property taxes in 2005. Many residents believed that the franchise tax was subject to excessive tax avoidance planning and did not generate sufficient revenue, while the personal property tax on businesses was viewed as detrimental to the state’s extensive but fragile manufacturing base. In contrast, the CAT has a broad base that approximates a standard GRT in that it does not allow deductions for the costs of goods sold (COGS) or other expenses.6 The tax base also includes the rapidly growing service sector, which was not covered under the previous tax system. The CAT rate is 0.26 percent, which is relatively low, for businesses with gross receipts of over $1 million.

Economists’ Views of the GRT

Economists generally agree that business taxes are imposed to reflect the true costs of a business’ activities. Certain costs generated by businesses (such as air and water pollution) and costs of government services that businesses benefit from (such as education, transportation, infrastructure, public safety, fire, the judicial system, etc.) are not fully or voluntarily reflected in their financial statements.7 Business taxes therefore incorporate these costs into business operations.

This principle implies that as long as the entities benefit from governmental services, they should pay for them. From this perspective, paying business taxes is viewed as similar to paying for other production inputs; in this case, the payment is for public services instead of land or labor. Unless a certain industry or type of entity benefits from such services differently than other types of industries or entities, all businesses should be taxed uniformly regardless of profitability, nonprofit status, or charitable functions. However, although theoretically true, this generalization is not widely applied by legislators and businesses in practice. People tend to react negatively toward taxing businesses that operate at a loss or serve as nonprofit or charitable organizations, even if they do use government services.

Business tax instruments generally include the CIT, GRT, and value-added tax (VAT),8 which are discussed below.

VAT

Many economists agree that a VAT is more efficient than other business taxes. From a benefits-received perspective, external costs generated and government services used by businesses are roughly proportional to the incremental value created by business entities at each stage of operations, which is precisely the VAT’s measure of economic activity.9

There are several alternative structures for a VAT. The income-based VAT taxes the sum of different forms of income, including labor compensation, rental payments, interest payments, and profits. The base of a consumption-based VAT is the difference between a firm’s sales and its purchases from other firms. The tax bases under these two methods can be constructed to be similar to each other, while the major difference is the treatment of capital assets. A consumption-based VAT allows businesses to expense capital purchases, whereas an income-based VAT replaces expensing with deductions for depreciation, similar to a standard income tax.10 Finally, tax filing is reasonably straightforward, especially for an income-based VAT, because many components can be pulled from federal tax returns.11

Similar to the GRT, a VAT is levied at each stage of operation, but it differs from the GRT in that it allows deductions of all inter-firm purchases at each stage. The net effect is the same as taxing the full value of goods and services at the time of final sale, and there are no repetitive taxes for inputs used in earlier stages of production.

GRT

The GRT is viewed as a bad tax primarily because of “tax pyramiding.” Pyramiding occurs when products and services are taxed each time they are purchased and sold by subsequent firms during the production process.12 The tax thus becomes part of the base in each subsequent sale, and final purchasers pay a higher tax because of the repeated taxation of the same inputs.13 Because of the lack of deductions for business-to-business (B2B) sales and the repetitive tax levy at each stage of production, the effective tax rate (ETR) on final sales under the GRT is not only higher than the statutory rate, it could also be different for similar goods, depending on the number of taxable intermediate transactions in the production/distribution process. The more times the products change hands across entities, the higher the ETR. In addition, ETRs also increase if value adds happens earlier in the production process because there are more stages for the tax to cascade.

One consequence of pyramiding is that it provides an incentive for vertical integration, which creates a bias against small firms that might otherwise provide services to larger entities. Over the last decade, U.S. firms have become increasingly specialized and hence vertically disintegrated. If this trend enhances productivity, some observers argue that a tax system that goes against it would tend to depress growth.14 As such, based on the benefits-received principle, the phenomenon of pyramiding may alter gross receipts to the extent that it is not a good proxy for the external costs generated by businesses.

What is the impact of GRT pyramiding? The limited studies available on pyramiding most commonly cite research referencing Washington’s B&O tax. Its estimated effective tax rate ranges from 0.8 percent (1.6 times pyramiding) for the retail trade industry to 3.2 percent (1.5 times pyramiding) for electric, gas, and other utility industries, with wide variation in ETRs and pyramiding across industries. Certain industries such as food manufacturing have an ETR of 2 percent but pyramid 6.7 times. The average statewide ETR for all industries is 1.5 percent, which translates to 2.5 times pyramiding.15 Some economists view these results as large distortions, while others interpret the results from a tax rate differential perspective and indicate that the pyramiding is modest.16

In principle, tax pyramiding can be fixed by exempting the sale of intermediate goods and services from the GRT base, with the trade-off being reduced revenues, increased complexity in taxation, and conversion of the GRT to a tax that bears characteristics of other tax instruments. This begs the question of why the alternatives are not implemented in the first place. For example, taxing only the value-added portion at each production stage instead of the full value of the good or service makes the GRT resemble a VAT. Lawmakers who propose a GRT are well aware of the issue of pyramiding and generally try to fix it either by offering tax credits or exemptions to industries with high levels of pyramiding, or by implementing differential tax rates for different economic sectors.17

One thing to note is that although pyramiding is the GRT’s major flaw, it is not unique to the GRT. Certain states that impose retail sales taxes on B2B transactions also face the risk of pyramiding. For example, about 35 percent of Connecticut’s 2014 retail sales taxes came from B2B transactions, which are taxed at 6.35 percent, totaling $1.4 billion.18 New Mexico’s “GRT” taxes B2B transactions but provides “chain of commerce” deductions similar to those under a VAT. A study estimated that about 32 percent of GRT revenue collected by the state, which was about $748 million in 2005, came from pyramiding. The state’s pyramiding relief solved 36 percent of the issue, but also gave up $427 million in revenue.19

CIT

Despite its flaws, the GRT is viewed as superior to the CIT by certain state lawmakers for several reasons. First, the GRT includes more types of businesses—C-corp, S-corp, limited liability companies (LLCs), partnerships, etc.—in the tax base, as opposed to only C-corp in the CIT. The CIT tax base also has been shrinking because of the increasingly popular LLCs, which has reduced the number of C-corp formations. In addition, a GRT would tax service sector businesses that are often organized in non-corporate forms and therefore are exempted from the CIT.

From a tax rate and revenue perspective, a broader tax base allows the GRT to have lower tax rates than the CIT. Because the taxable entities are not limited to profitable corporations, the GRT tends to generate larger and more stable revenue.

The GRT also leaves fewer opportunities for tax planning because it applies to all businesses and all receipts. Accounting to determine taxable receipts is less complicated and costly than accounting to measure taxable income. As such, administrative costs are generally lower under the GRT.

Texas Perspective

In 2005, the Texas Supreme Court declared the Texas school finance system unconstitutional and indicated that the state-imposed cap on local property taxes for school maintenance and operations essentially converted it into a statewide property tax, which the Texas Constitution explicitly bans.20 In response, Texas lawmakers attempted to reduce the extent to which property taxes are used to finance public education. They did this by substantially modifying the state’s franchise tax to bring in more revenue, with the additional revenues used to fund schools. The modified franchise tax, also known as the margin tax, restructured the state business tax by replacing the taxable capital and earned surplus components with a new taxable margin component. There are four ways to calculate the taxable margin: total revenue times 70 percent, total revenue minus COGS, total revenue minus compensation, or total revenue minus $1 million.21 Texas has its own COGS definition, which generally includes all direct costs related to the acquisition and production of tangible personal property and real property.

The modified franchise tax has been subject to much criticism since it was signed into law.22 Its two major shortcomings are that it is complicated and has generated less revenue than projected.

From a structural perspective, the franchise tax has hybrid characteristics of the GRT and CIT, but retains the compliance and administrative complications of the CIT. Because of its marginal tax component, there has been debate about whether it is an income tax or a GRT. In 2006, Financial Accounting Standard Board (FASB) members indicated that the franchise tax was an income tax because it is based on a measure of income,23 a view the Texas Comptroller’s Office opposed.

From a revenue perspective, the franchise tax was projected to collect an estimated $6 billion before its enactment. The actual amount of revenue collected was $4.45 billion in 2008 and less than $4 billion in 2009;24 the annual revenue has been between $3 billion and $4 billion.25 The initial consensus was that the Great Recession led to revenues being $1.5 billion short of projections. Moreover, the state’s revenue estimates were based on federal tax data even though its COGS definition is not necessarily consistent with the federal definition. This imperfect match led to the overly optimistic initial revenue projection.

There have been numerous proposals in recent legislative sessions to challenge, modify, or repeal the tax. In the 2017 regular legislative session, H.B. 28 proposed a franchise tax rate reduction that would be based on the cash balance of surplus revenue available at the end of each fiscal biennium, with the tax cut the lesser of the ending surplus or $3.5 billion per biennium. The franchise tax rate would ideally decrease on a biannual basis, and once the adjusted rate reaches less than 15 percent of the current rate, the tax would automatically be repealed. Another proposal, S.B. 17, would have reduced the franchise tax rate each biennium, contingent upon state revenue growth of 5 percent.

Despite the lower than anticipated revenue collection, the franchise tax ranks as Texas’ third- or fourth-largest source of state tax revenue. Some Texas lawmakers voted against the repeal or sunset of the franchise tax in the most recent legislative session due to the lack of replacement revenue. As undesirable as the tax is, given that the franchise tax was intended to finance the state’s share of public education costs, eliminating it before finding alternative revenue sources is more unacceptable.26 If the state contributes less franchise tax revenue to fund public education, the share of local property taxes is likely to increase. If property values in Texas continue to increase, as they have been recently, then eventually homeowners will become dissatisfied with the rising share of property taxes in funding public education.27

Texas Court Cases

The Texas Supreme Court recently heard oral arguments in a case filed by Graphic Packaging Corp., which contends that the franchise tax is an income tax.28 The issue is that, under the Multistate Tax Compact,29 business taxpayers could elect to apportion income using an equally weighted three-factor apportionment formula based on a business’ sales, property, and payroll. However, the franchise tax essentially compels businesses to use gross receipts as the single factor to apportion its income under this tax. In 2015, a ruling from the Texas Third Court of Appeals found that the compact’s income-apportionment provision does not apply because the franchise tax is not an income tax. If the Texas Supreme Court decides that the franchise tax is an income tax, in favor of Graphic Packaging, the company’s 2008-2010 taxes paid would be reduced by millions. Other states, most notably Michigan, experienced similar challenges to state laws that resulted in amendments to the business tax, essentially repealing the Multistate Tax Compact. In addition to mandating a single factor of sales, Michigan’s 2014 amendment also imposed a controversial clause to retroactively apply the amendment, with an effective date of Jan. 1, 2008.30

Other recent lower court cases in Texas involving the franchise tax are mostly related to the calculation of COGS. Many businesses, other than those in the service industry, believe COGS offer more tax-saving opportunities than other deductions, and many cases center not only on whether a taxpayer is entitled to claim COGS but also what constitutes COGS. Because the definition of COGS under the franchise tax is not identical to the federal definition, the state must defend its definition. Generally, the comptroller’s view of what constitutes COGS is more limited than taxpayers’ interpretations. The courts are therefore often brought in to decide how the definition should be applied.

Autohaus LP filed a petition for review with the Texas Supreme Court and requested a repeal of a Court of Appeals ruling that repair labor costs were not involved in the production of goods and as such did not qualify as a COGS deduction. The Court of Appeals pointed out that the company bought the parts from third parties and simply resold and installed these parts on customers’ vehicles. The company, on the other hand, indicated that the legislature defined “production” to include “installation.”31 The petition is currently pending.

In May 2017, the Texas Third Court of Appeals rejected the state’s argument that movie theater chain AMC cannot deduct film exhibition costs from its franchise tax base because the company is not selling tangible goods. The Comptroller’s Office claimed that showing films involves the provision of a service or intangibles, but not the sale of tangible goods.32 The court indicated that AMC’s exhibition of movies to paying customers is properly considered tangible personal property. The Comptroller’s Office filed a petition for review in the Texas Supreme Court in August 2017.33

Conclusion

An increasing number of states are facing issues related to obsolete tax systems and revenue shortages. Many states began tax overhauls by repairing the CIT and several are exploring more fundamental tax reforms.

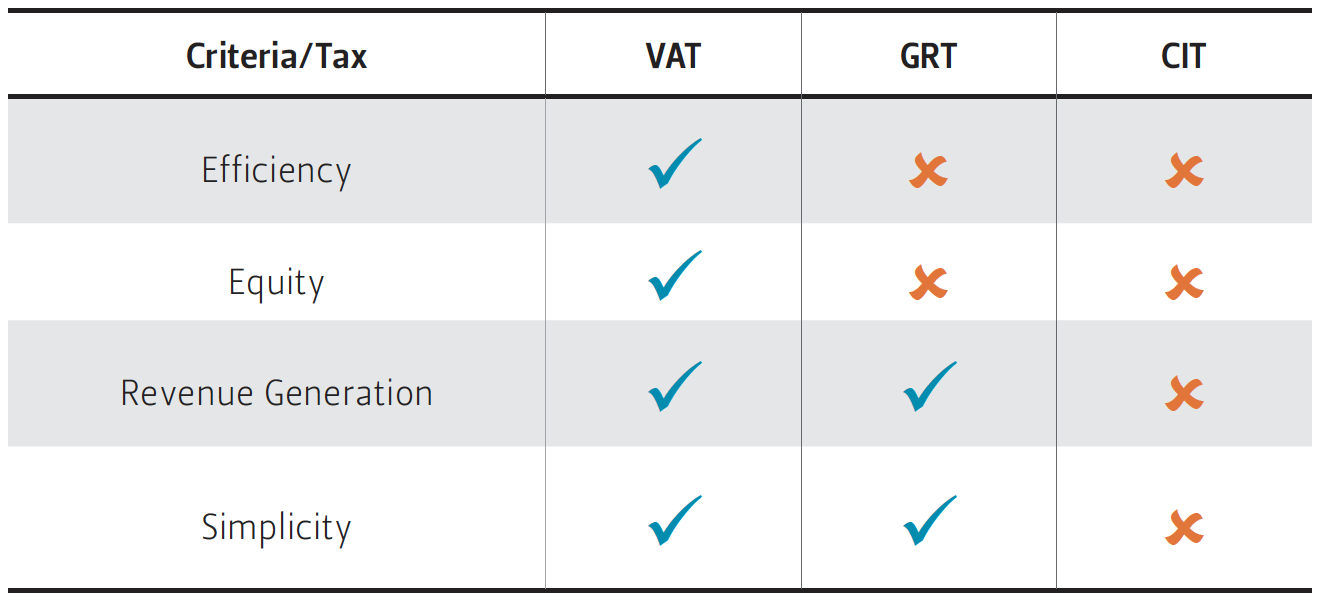

From a mechanism design perspective, a good business tax is 1) efficient, in that it distorts the private sector as little as possible and mostly likely uses a broad-based, low-rate tax structure; 2) fair, where similarly situated entities are taxed similarly; 3) generates sufficient revenue; and 4) simple.

Figure 1 — Comparison of Business Taxes Against Economic Criteria

Source Author’s own elaboration.

State business tax reform cannot happen in a vacuum. A state’s existing business tax structure, economic climate, industry concentration, and other state or local taxes all need to be considered. Although most economists support the VAT, its transition costs and unfamiliarity have been major obstacles to its successful adoption. A policy choice between the GRT and the CIT may reflect what is more tolerable to state and local constituents and policymakers—a distortionary tax that generates revenue, or the incumbent, more complicated tax. What Figure 1 does not show is the intensity of public opinion regarding each criteria.

Public opinion as to what is preferable may also change over time. Michigan adopted a business activities tax—a type of VAT—from 1953 to 1967, switched to a CIT between 1968 and 1975, then moved to a single business tax—an income-based VAT—from 1976 to 2007. From 2008 to 2011, it used the Michigan Business Tax, a type of GRT. Finally, Michigan switched back to the CIT in 2012, which it has used ever since.34 Thus, over the last 50 years, Michigan experimented with all three types of business taxes.

Regardless of which business tax a state decides to implement, the overarching characteristics that are desirable are clear: the tax should be a broad-based, low-rate tax that has limited pyramiding and does not create many tax avoidance opportunities. After such a tax is enacted, states also need to avoid the pressure to erode the tax base over time—either by offering concessions to specific industries, excluding particular groups, or providing incentives for certain activities. Without ongoing maintenance, the shrinking tax base will necessitate rate increases to bring in the same amount of revenue, and the modified tax may eventually look like the CIT today.

Endnotes

1. Maria Eberle and Nicole Ford, “Not Dead Yet: Oregon Voters Propose another Gross Receipts Tax in the Wake of Market-Based Sourcing,” July 31, 2017. https://www.lexology.com/library/detail.aspx?g=a851a212-6f97-4a37-887b-f3b1216287e7.

2. West Virginia’s S.B. 484 passed both the Senate and the House, but was not included in the revised proposal during the special session or in the final budget. See: http://www.legis.state.wv.us/Bill_Status/bills_history.cfm?INPUT=484&year=2017&sessiontype=RS.

3. New Mexico’s GRT or non-statewide GRTs (e.g., municipal level GRTs or GRTs that are applicable to limited types of expenditures) are not considered in this brief.

4. Thomas Pogue, “The Gross Receipts Tax: A New Approach to Business Taxation?” National Tax Journal Vol. LX, no. 4 (December 2007): 799-819.

5. Other states that proposed GRTs in the early 2000s include Illinois, Maine, and Montana.

6. It excludes nonprofit and government entities.

7. Pogue, “The Gross Receipts Tax: A New Approach to Business Taxation?”

8. Some economists excluded the general sales tax because it is only collected from businesses out of lower compliance/administrative costs considerations. Individuals bear the burdens of sales tax.

9. Pogue (2007) indicated that an income-based VAT is superior to the GRT, but the GRT may not be preferable to a consumption-based VAT.

10. For a detailed discussion of the VAT, see George Zodrow, Texas Tax Options, Rice University’s Baker Institute for Public Policy, Houston, TX, January 2006, https://www.bakerinstitute.org/research/texas-tax-options/.

11. Robert D. Ebel, LeAnn Luna, and Matthew N. Murray, “State General Business Taxation One More Time: CIT, GRT, or VAT?” National Tax Journal 69, no. 4 (December 2007): 739-762.

12. New Mexico Tax Research Institute, “Pyramiding Transactions Taxes in New Mexico: A Report on the Gross Receipts Tax,” Albuquerque, New Mexico, September 2015.

13. Ebel, Luna, and Murray, “State General Business Taxation One More Time.”

14. William A. Testa and Richard H. Mattoon, “Is There a Role for Gross Receipts Taxation?” National Tax Journal Vol. LX, no. 4 (December 2007): 821-840.

15. Andrew Chamberlain and Patrick Fleenor, “Tax Pyramiding: The Economic Consequences of Gross Receipt Taxes.” Tax Foundation Special Report No. 147 (December 2006); Washington State Tax Structure Committee, “Tax Alternatives for Washington State: A Report to the Legislature,” Volumes 1&2, (November 2002).

16. Pogue (2007) indicated: “The tax rate differentials lead to inefficiency by creating artificial differences in the costs. If tax rates due to pyramiding are the same in all sectors, then pyramiding causes no cost distortions among taxed sectors.”

17. Chamberlain and Fleenor, “Tax Pyramiding: The Economic Consequences of Gross Receipt Taxes.”

18. Ebel, Luna, and Murray, “State General Business Taxation One More Time.”

19. New Mexico Tax Research Institute, “Pyramiding Transactions Taxes in New Mexico.”

20. Neeley v. West Orange-Cove I.S.D. (Nov. 22, 2005).

21. This option was effective on Jan. 1, 2014. Certain qualifying entities can also choose to use EZ computation. See: https://comptroller.texas.gov/taxes/publications/98-806.php.

22. Scott Drenkard, “The Texas Margin Tax: A Failed Experiment,” Tax Foundation Special Report No. 226 (January 2015).

23. Financial Accounting Standards Board, Meeting Minutes, Texas Franchise Tax, http://www.fasb.org/board_meeting_minutes/08-02-06_texas_franchise_tax.pdf.

24. Billy Hamilton, “The Tax that Fell to Earth: Lessons from the Texas Margin Tax’s Launch,” State Tax Notes 57 (2010): 671–675.

25. Texas Comptroller of Public Accounts, Annual Financial Reports, FYE 2007-2016 https://comptroller.texas.gov/transparency/reports/annual-financial/.

26. Ashley Goudeau, “Texas House passes bill to eliminate the franchise tax,” KVUE.com, April 28, 2017, http://www.kvue.com/news/politics/texas-house-passes-bill-to-eliminate-the-franchise-tax/434996414.

27. Ross Ramsey, “Today’s hated business tax is tomorrow’s property tax relief,” The Texas Tribune, April 26, 2017, https://www.texastribune.org/2017/04/26/analysis-todays-hated-business-tax-tomorrows-property-tax-relief/.

28. Graphic Packaging Corp. v. Hegar, Tex., No. 15-0669. Oral arguments were held on Sept. 13, 2017. See http://data.scotxblog.com/scotx/no/15-0669.

29. Texas is a member of the Multistate Tax Commission and its Multistate Tax Compact. The purpose of the compact is to promote uniformity in state taxes. At the same time, the compact is also a binding interstate contract in which Texas is bound by the Compact Election and the Compact Formula.

30. The businesses that challenged the Michigan amendment include: IBM Corp., Gillette Commercial Operations North America, Goodyear Tire & Rubber Co., DirecTV Group Holdings, Sonoco Products Co., and R.J. Reynolds Co. The U.S. Supreme Court did not accept any petition to review these cases.

31. Autohaus LP v. Hegar, Tex., No. 17-0253. Petition for review was filed on May 24, 2017. The court requested response was filed on Sep 6, 2017. The petition remains pending. See http://data.scotxblog.com/scotx/no/17-0253.

32. Am. Multi-Cinema, Inc. v. Hegar, Tex. App., 3rd Dist., No. 03-14-00397-CV.

33. Hegar, Tex. v. Am. Multi-Cinema, Inc., No. 17-0464. See http://data.scotxblog.com/scotx/no/17-0464.

34. Citizens Research Council of Michigan, “Outline of the Michigan Tax System” (2016 Edition).

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.