Entrepreneurs face a myriad of managerial decisions and tasks as they set out to start a new business. One early decision is whether to operate as a sole proprietorship or as a business entity such as a limited liability company (LLC), a decision for which seeking legal advice is often recommended. Research demonstrates that small and medium enterprises benefit substantially from legal advice, with improvements to employment, profitability, and reinvestment.1 The risk associated with an entrepreneur’s particular line of business is a primary consideration for lawyers when advising whether to form a business entity,2 but that consideration is misplaced given the uninsurable risks that threaten the personal assets of sole proprietors regardless of the line of business.3 Nonetheless, the IRS recently reported that of the 25.5 million individual tax returns filed for 2016 that included business income, only 7.3% of those businesses (1.9 million) were formed as LLCs.4 While the use of LLCs by single-owner businesses has steadily increased since 2001,5 the IRS data suggest that the vast majority of single-owner businesses in the U.S. today operate as sole proprietorships.6 Given the advantages of an LLC and frequent advice to form one, we explore the reasons for the low adoption of the LLC form of business by entrepreneurs and ways to increase its use.7

The Complexity of the Sole Proprietorship-LLC Decision

The decision to operate as a sole proprietorship or a business entity is a complex one. A sole proprietorship is a business in which one person owns all the assets, owes all of the liabilities, and operates in their personal capacity.8 In other words, Joe’s Body Shop and its owner Joe are the same “person” from a legal perspective. Joe is responsible for everything related to Joe’s Body Shop just as he is responsible for all other areas of his life. In contrast, a business entity is a distinct legal “person” from its owners. Joe’s Plumbing LLC and its owner Joe are two separate people from a legal perspective. Although Joe owns Joe’s Plumbing LLC, Joe does not own the property of the company and cannot be forced to pay its debts,9 just as he does not own his neighbor’s property and cannot be forced to pay his neighbor’s debts.

The formation of an LLC requires work and financial resources in addition to the work and resources of running the business itself (e.g., the development, marketing, and delivery of a product), while the establishment of a sole proprietorship requires no additional effort or cash.10 An LLC is created by filing formation documents with a government office, usually the secretary of state. In contrast, a sole proprietorship is created by default, in the absence of filing formation documents with a government office. Even a child’s lemonade stand is a sole proprietorship. The decision to form an LLC is followed by the work and expense of formation, namely filing a certificate of formation with the secretary of state and paying the associated fee.11 A new LLC also must begin keeping records of its accounts and owners.12 The paperwork requirements of an LLC and the cost of formation are the price an entrepreneur must pay for the liability protection afforded by the LLC. Those costs are perhaps analogous to paying the premium for an insurance policy that protects the entrepreneur’s personal assets from every potential financial liability that could arise from the business. The trade-off seems largely worth it since such comprehensive insurance does not exist for a sole proprietor.

Why Do So Few Entrepreneurs Form LLCs?

Entrepreneurs tend to make most of the decisions associated with establishing their businesses (i.e., decisions not directly associated with product development) in a haste, and they often base these decisions on a few primary factors that are inappropriate over the long term,13 such as legal fees.14 In their initial consultations, lawyers and accountants tend to provide entrepreneurs with sound advice to protect their assets from future liability risks,15 and a reliable way for entrepreneurs to protect their personal assets is to conduct business in an entity such as an LLC.16 A few factors that entrepreneurs ought to consider while deciding on whether to form an LLC include the extent to which their personal assets are vulnerable to business liabilities; tax implications; and the degree to which potential lenders and investors are likely to be attracted to the venture.17 One would expect that such advice would result in an overwhelming number of LLC formations. However, IRS data on the number of single-owner businesses formed as LLCs strongly suggest otherwise.18

Research on small business formation offers several possible explanations for the willingness of entrepreneurs to risk their personal assets in a sole proprietorship. We make an implicit assumption that entrepreneurs make rational decisions, but research shows that individuals tend to weigh probabilities in a nonlinear manner; specifically, people tend to overweight low probabilities and underweight high probabilities.19 Entrepreneurs may underweight the probability of personal liability arising from their businesses over the long term. The limited number of LLCs formed also could be attributed to entrepreneurs’ inability to make sound decisions due to cognitive overload or limited cognitive resources,20 as they are required to make many business decisions related to setting up a new business within a limited time. Additionally, entrepreneurs are likely to be better idea creators than strategic planners, and they often lack the esoteric knowledge required to make legal or financial decisions.21 Therefore, the novel set of decisions entrepreneurs are required to make is likely to overwhelm them, prompting relatively quick decision-making. These decisions are often based on factors they can comprehend and compare easily such as costs.22

Marcum and Blair astutely note that cost (e.g., filing fees or fees to consult a lawyer or an accountant) plays a significant role in entrepreneurs’ decision-making processes because cost is a factor that is concrete in nature (i.e., involves numbers) and lends itself to easy comparison.23 For instance, an entrepreneur is able to compare two numbers—in Texas it costs $300 to form an LLC24 and $0 to start a sole proprietorship—more easily than they can understand the taxation and legal attributes of an LLC and a sole proprietorship. Marcum and Blair further assert that when entrepreneurs decide to go for the cheaper option (i.e., sole proprietorship), they are not basing this decision on whether or not they can afford the filing fees; instead they are choosing an option that is effortless to adopt. The alternative requires time and money, and these costs are amplified when professional advice is sought from lawyers or accountants. Some empirical research provides further evidence for cost being a deterrent to the formation of LLCs across different states in the United States. A study examined the popularity of LLCs across states, which were categorized into three groups: states where LLC filing fees were the same as corporation filing fees; states where LLC filing fees were less than corporation filing fees; and states where LLC filing fees were more than corporation filing fees. The study findings indicate that states where it cost the same or less to form an LLC compared to forming a corporation had more businesses registered as LLCs.25

Potential Intervention to Promote LLC Formation

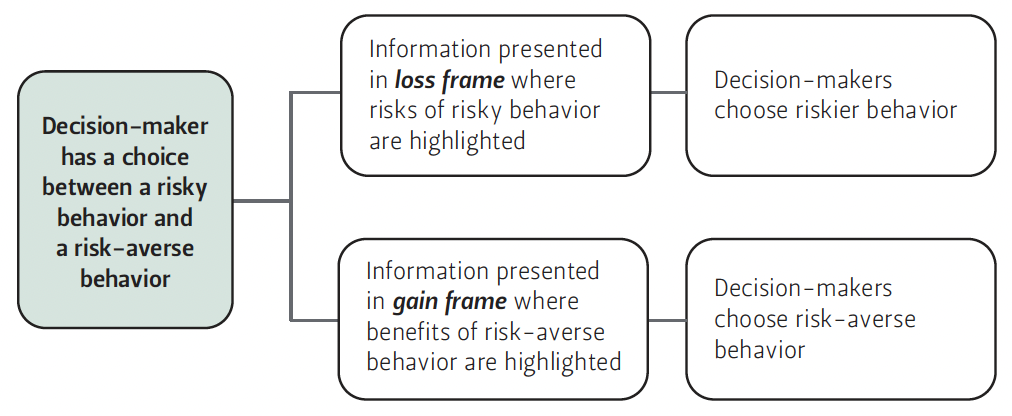

Figure 1 — Prospect Theory

The field of message framing offers an intervention that may encourage entrepreneurs to establish their businesses as LLCs. Message framing simply refers to emphasizing either the positive or negative outcomes of executing or failing to execute a behavior.26 According to prospect theory, individuals making decisions encode the information associated with their options either in the form of potential gains or losses (see Figure 1).27 When information about risky and risk-averse options is presented in a loss frame (i.e., costs of the risky behavior are highlighted), individuals are more likely to opt for the riskier option. In contrast, when information is presented in a gain frame (i.e., the benefits/advantages of risk-averse behavior are highlighted), decision-makers are likely to opt for the risk-averse option. Thus, the theory posits that risky behaviors are more likely to be adopted when losses/ costs are made prominent to decision-makers. Alternatively, decision-makers are likely to adopt risk-averse behavior when gains/benefits are made salient.

Message framing has been extensively used in the promotion of various detection behaviors—such as using mammograms for early breast cancer detection28 and conducting tests for HIV29—as well as prevention behaviors, such as using condoms during sexual intercourse30 and applying sunscreen.31 In the case of detection behaviors, uncertainty and psychological risk are always present because individuals assume they are healthy before the test, and they have to accept the risk that the screening may reveal otherwise. In such instances, research shows that individuals are motivated to adopt the psychologically risky behavior (i.e., getting a mammogram or a HIV screening test) when the disadvantages of not adopting this behavior are made salient to them.32 On the other hand, prevention behaviors come with little uncertainty or psychological risk. For instance, the act of applying sunscreen is not perceived as risky by the decision-maker. Prospect theory and other empirical research suggest that gain-framed messages are more persuasive in promulgating these risk-aversive behaviors.33

Policy Recommendations

Prospect theory and the success of utilizing message framing in promoting desired health behaviors can be extended to promote a desired “economic health behavior” among entrepreneurs—the formation of an LLC. We argue that when entrepreneurs choose to operate their business as an LLC they are executing a risk-averse behavior similar to the preventative behaviors discussed above; hence the Small Business Administration (SBA), the state government offices charged with the formation of business entities, and advisors at business incubators or accelerators should recommend that entrepreneurs form their businesses as LLCs. According to prospect theory, those communications are likely to be more persuasive when they are structured in a gain frame rather than a loss frame.

The efficacy of extending prospect theory to the promotion of business entity formation has not been empirically studied, but the formation of an LLC is analogous to insurance. Limited research on the promotion of long-term care insurance notes that policymakers have been framing the need for this type of insurance using a loss frame by highlighting the high costs of long-term care and emphasizing the increasing proportion of the elderly population that needs it. The findings of this study demonstrate that people are more willing to pay for long-term care insurance when its benefits are highlighted (e.g., buying this insurance ensures that you receive $5000 per month toward your home care) rather than when exposed to the costs of not buying this insurance.34 We assert that these findings can be extended to the domain of business entity formation, as forming an LLC is analogous to securing an insurance policy to limit personal liability in the future. As the very act of establishing an LLC is not perceived as risky, communication that is aimed at encouraging entrepreneurs to form an LLC should highlight the benefits. Advice should not focus on the drawbacks of a sole proprietorship. Specifically, government and private sector advisors should recommend that entrepreneurs form LLCs to keep their personal assets safe from claims against the business and to create a business that is ready to receive investors, instead of providing advice dwelling on the personal financial risk and other pitfalls associated with a sole proprietorship.

Finally, research in the message framing domain finds that certain individual differences have an impact on the extent to which a gain or a loss frame is perceived as persuasive. Some individuals are sensitive toward and respond to cues involving rewards and positive outcomes. These individuals are commonly referred to as approach-oriented individuals. Other individuals are sensitive to cues of threat and strive to avoid negative consequences. Such people are referred to as avoidance-oriented individuals.35 Past research notes that approach-oriented individuals are more receptive to gain-framed messages and avoidance-oriented individuals are more persuaded by loss-framed messages.36 These findings have implications for LLC formation. Advisors to entrepreneurs (e.g., the SBA and business incubators/accelerators) can administer a validated, free-to-use scale developed by Carver and White37 to gauge whether the entrepreneurs seeking help are approach-oriented or avoidance-oriented. This quick assessment will enable these practitioners to frame their pitch on LLC formation in a manner that is consistent with the entrepreneurs’ motivational disposition. The match between the message frame and motivation orientation is likely to persuade entrepreneurs more than dissuade them.

Endnotes

1. Paul J.A. Robso and Robert J. Bennett, “SME growth: The relationship with business advice and external collaboration,” Small Business Economics 15, no. 3 (2000): 193-208.

2. Tanya M. Marcum and Eden S. Blair, “Entrepreneurial decisions and legal issues in early venture stages: Advice that shouldn’t be ignored,” Business Horizons 54, no. 2 (2011): 143-152, https://doi.org/10.1016/j.bushor.2010.11.001.

3. Eden S. Blair, Tanya Marcum, and Fred Fry, “The disproportionate costs of forming LLCs Vs. Corporations: The impact on small firm liability protection,” Journal of Small Business Strategy 20, no. 2 (2009): 23-41.

4. Internal Revenue Service, “Sole Proprietorship Returns, Tax Year 2016,” Statistics of Income Bulletin, Spring 2019, https://www.irs.gov/pub/irs-soi/soi-a-inpr-id1905.pdf.

5. By single owner, we mean one natural person and some married couples. In the tax classification of LLCs, the IRS considers a married couple that owns a business as community property to be one person. INTERNAL REVENUE SERVICE, PUB. 3402, TAXATION OF LIMITED LIABILITY COMPANIES (2016), https://www.irs.gov/publications/p3402#en_US_201606_publink1000205890.

6. A corporation can also have one owner, but the IRS report cited does not include income from corporations (neither S nor C corporations).

7. Other types of business entities, such as corporations and partnerships, may also be considered by entrepreneurs. We discuss only LLCs in this brief because an LLC is the form of business entity most analogous to a sole proprietorship. An LLC that has only one owner (see note 1) is disregarded for federal income tax purposes, which means the income of the LLC is included in the income of the owner and is not separately taxed to the LLC.

8. Sole Proprietorship, BLACK’S LAW DICTIONARY (7th ed. 1999).

9. The owner of a business entity sometimes gives a personal guaranty for the repayment of a loan obtained by the business entity in order to induce the lender to make the loan. In such cases, the owner is responsible for repayment of the entity’s debt if the entity fails to do so, but that obligation arises by contract and would not exist in the absence of the personal guaranty.

10. If a sole proprietor intends to operate a business in Texas under a business name that does not include the proprietor’s surname, an assumed name certificate must be filed with the county clerk of each county in which the business will operate. Tex. Bus. & Com. Code §§ 71.051, 71.054.

11. Tex. Bus. Org. Code §§ 3.001, 4.154.

12. Tex. Bus. Org. Code § 3.151.

13. The potential financial liabilities entrepreneurs have to bear in the absence of forming a business entity are likely to outweigh a one-time finite cost they need to pay to form a business entity.

14. Marcum and Blair, “Entrepreneurial decisions.”

15. Eden S. Blair and Tanya M. Marcum, “Heed our advice: Exploring how professionals guide small business owners in start-up entity choice,” Journal of Small Business Management 53, no. 1 (2015): 249- 265, https://doi.org/10.1111/jsbm.12073.

16. Blair, Marcum, and Fry, “The disproportionate costs.”

17. R.P. Khandekar and J.E Young, “Selecting a legal structure: A strategic decision,” Journal of Small Business Management 23, no. 1 (1985): 47-55.

18. INTERNAL REVENUE SERVICE, supra.

19. Colin F. Camerer, “Neuroeconomics: Using neuroscience to make economic predictions,” The Economic Journal 117, no. 519 (2007): C26-C42, https://doi.org/10.1111/j.1468-0297.2007.02033.x.

20. Gerd Gigerenzer and Daniel G. Goldstein, “Reasoning the fast and frugal way: Models of bounded rationality,” Psychological Review 103, no. 4 (1996): 650-669. https://doi.org/10.1037/0033-295x.103.4.650.

21. Eugene Smith, Yve Hampson, Ian Chaston, and Beryl Badger, “Managerial behavior, entrepreneurial style, and small firm performance,” Journal of Small Business Management 41, no. 1 (2003): 47-67, https://doi.org/10.1111/1540-627x.00066.

22. Marcum and Blair, “Entrepreneurial decisions;” Blair, Marcum, and Fry, “The disproportionate costs.”

23. Marcum and Blair, “Entrepreneurial decisions.”

24. Tex. Bus. Org. Code §§ 4.152, 4.154.

25. Blair, Marcum, and Fry, “The disproportionate costs.”

26. Alexander J. Rothman and Peter Salovey, “Shaping perceptions to motivate healthy behavior: The role of message framing,” Psychological Bulletin 121, no. 1 (1997): 3-19, https://doi.org/10.1037/0033-2909.121.1.3.

27. Daniel Kahneman and Amos Tversky, “Prospect theory: An analysis of decision under risk,” Econometrica 47, no. 2 (1979): 263, https://doi.org/10.2307/1914185.

28. Sara M. Banks, Peter Salovey, Susan Greener, Alexander J. Rothman, Anne Moyer, John Beauvais, and Elissa Epel, “The effects of message framing on mammography utilization,” Health Psychology 14, no. 2 (1995): 178-184, https://doi.org/10.1037/0278-6133.14.2.178.

29. Seth C. Kalichman and Brenda Coley, “Context framing to enhance HIV-antibody-testing messages targeted to African American women,” Health Psychology 14, no. 3 (1995): 247-254, https://doi.org/10.1037/0278-6133.14.3.247.

30. Rocio Garcia-Retamero and Edward T. Cokely, “Effective communication of risks to young adults: Using message framing and visual aids to increase condom use and STD screening,” Journal of Experimental Psychology: Applied 17, no. 3 (2011): 270- 287, https://doi.org/10.1037/a0023677.

31. Alexander J. Rothman, Peter Salovey, Carol Antone, Kelli Keough, and Chloe Drake Martin, “The influence of message framing on intentions to perform health behaviors,” Journal of Experimental Social Psychology 29, no. 5 (1993): 408-433.

32. Peter Salovey and Pamela Williams- Piehota, “Field experiments in social psychology,” American Behavioral Scientist 47, no. 5 (2004): 488-505, https://doi.org/10.1177/0002764203259293.

33. Kahneman and Tversky, “Prospect theory.”

34. Jeremey Pincus, Katherine Hopewood, and Robert Mills, “Framing the decision to buy long-term care insurance: Losses and gains in the context of statistical and narrative evidence,” Journal of Financial Services Marketing 22, no. 1 (2017): 33-40, https://doi.org/10.1057/s41264-017-0019-4.

35. Charles S. Carver, Steven K. Sutton, and Michael F. Scheier, “Action, emotion, and personality: Emerging conceptual integration,” Personality and Social Psychology Bulletin 26, no. 6 (2000): 741-751, https://doi.org/10.1177/0146167200268008.

36. Traci Mann, David Sherman, and John Updegraff, “Dispositional motivations and message framing: A test of the congruency hypothesis in college students,” Health Psychology 23, no. 3 (2004): 330-334, https://doi.org/10.1037/0278-6133.23.3.330.

37. Charles S. Carver and Teri L. White, “Behavioral inhibition, behavioral activation, and affective responses to impending reward and punishment: The BIS/BAS scales,” Journal of Personality and Social Psychology 67, no. 2 (1994): 319-333, https://doi.org/10.1037/0022-3514.67.2.319.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.