To access the full paper, download the PDF on the left-hand sidebar.

I. Introduction

The past decade has yielded dramatic change in the natural gas industry. Specifically, there has been rapid development of technology allowing the recovering of natural gas from shale formations. This technology has been applied with much success in North America, and there is much interest in seeing similar developments in other countries around the world. Since 2000, production of natural gas from shale formations in North America has dramatically altered the global natural gas market landscape. In fact, the emergence of shale gas is perhaps the most significant development in global energy markets in the last decade.

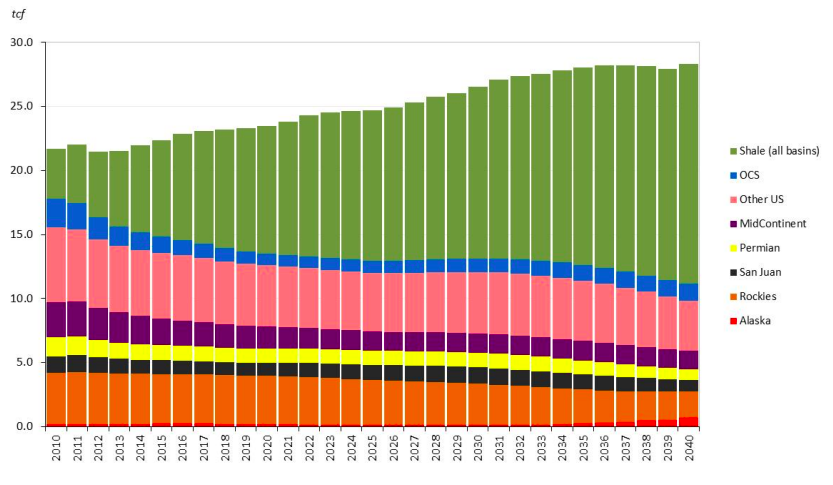

Knowledge of the shale gas resource is not new as geologists have long known about the existence of shale formations, and accessing those resources was long held in the geology community to be an issue of technology and cost. In the past decade, innovations involving the use of horizontal drilling with hydraulic fracturing have yielded substantial cost reductions, making shale gas production a commercial reality. In fact, shale gas production in the United States has increased from virtually nothing in 2000 to over 10 billion cubic feet per day (bcfd) in 2010, and it is expected to more than quadruple by 2040, reaching over 50 percent of total U.S. natural gas production by the 2030s (see Figure 1).

Figure 1 — U.S. Natural Gas Production Through 2040 (Reference Case)

To be sure, shale gas developments in North have had a ripple effect across the globe by displacement of supply in global trade and by fostering a growing interest in shale resource potential in other parts of the world. Thus, North American shale gas developments are having effects far beyond the North American market, and these impacts are likely to expand over time.

The state of knowledge regarding the portion of shale gas that is economically recoverable has changed rapidly over the last 10 years. A simple chronology of assessments for North America, where most development activity has occurred to date, is as follows:

- As recently as 2003, the National Petroleum Council estimated that about 38 tcf of technically recoverable resources was spread across multiple basins in the North America.

- In 2005, the Energy Information Administration (EIA) was using an estimate of 140 tcf in its Annual Energy Outlook as a mean for North American technically recoverable shale gas resource.

- In 2008, Navigant Counseling, Inc. estimated a mean of 280 tcf of technically recoverable resources from reviewable geologic literature, but a survey of producers indicated up to 840 tcf.

- In 2009, the Potential Gas Committee put its mean estimate at just over 680 tcf.

- In 2011, Advanced Resources International (ARI) reported an estimate of about 1,930 tcf of technically recoverable resource for North America, with over 860 tcf in U.S. gas shales alone.

Importantly, although each assessment is from an independent source, the estimates are increasing over time as more drilling occurs and technological advances are made. Moreover, the shift in the generally accepted assessment of recoverable shale resource has left producers, consumers, and governments all grappling with the implications for markets as well as the geopolitical repercussions.

Shale gas developments stand to exert enormous influence on the structure of the global gas market. Throughout the 1990s, natural gas producers in the Middle East and Africa, anticipating rising demand for LNG from the United States in particular, began investing heavily in expanding LNG export capability, concomitant with investments in regasification being made in the United States. But the rapid growth in shale gas production has turned such expectations upside down and rendered many of those investments obsolete. Import terminals for liquefied natural gas (LNG) are now scarcely utilized, and the prospects that the United States will become highly dependent on foreign imports in the coming years are receding.

Rising shale gas production in the United States is also having an impact on markets in Europe and Asia. In particular, LNG supplies whose development was anchored on the belief that the United States would be a premium market are now being diverted to European and Asian buyers. Not only has this immediately presented consumers in Europe with an alternative to Russian pipeline supplies, it is also exerting pressure on the status quo of indexing gas sales in both Europe and Asia to a premium marker determined by the price of petroleum products. In recent rounds of renegotiations, Russia has had to accept far lower prices from many of its traditional long-term customers and has accepted a partial link to gas on gas pricing.

Revelations about the potential for increased shale gas production are also occurring in other regions around the world, with shale gas discoveries being discussed in Europe, China, India, Australia, and elsewhere. To be sure, the enormity of global shale gas potential will have significant geopolitical ramifications and exert a powerful influence on U.S. energy and foreign policy.

In this study, we utilize scenario analysis to examine the role that China plays in the future of global gas market developments. In doing so, we consider two cases, which we compare to a reference case, where:

- China's technically recoverable shale resource base is dramatically larger; and

- China's economic growth falters, thus lowering natural gas demand growth

We also expand on the effect of shale gas developments more generally by highlighting a recent paper by Medlock and Jaffe (2011) in which no shale is developed anywhere in the world. This highlights the overall importance of the shale gas resource to international gas markets.

Among the geopolitical repercussions of expanding shale gas production are:

- It virtually eliminates U.S. requirements for imported LNG for at least two decades, reducing U.S. and Chinese dependence on Middle East natural gas supplies, lowering the incentives for geopolitical and commercial competition between the two largest consuming countries, and providing both countries with new opportunities to diversify their energy supply.

- It substantially reduces Russia's market share in both Europe and Asia, depending on the amount of shale resource that is ultimately available in both regions.

- It lowers prices and stimulates greater use of natural gas, thereby having significant implications for global environment objectives to the extent it displaces coal.

- It reduces overall dependence on Iranian natural gas, which limits Iran's ability to tap energy diplomacy as a means to strengthen its regional power or to buttress its nuclear aspirations.

It should be pointed out that the sustained rapid development of shale gas is not a certainty. In particular, environmental concerns regarding the use and potential contamination of water resources are major issues that will need to be addressed before governments will allow full realization of shale's growth potential. In China, in particular, water availability for hydraulic fracturing may considerably diminish the potential for domestic shale development.

According to a report by Gleick et al. (2008), China faces some of the most severe water challenges in the world due to overallocation, inefficient usage, and widespread pollution, as well as a fairly weak regulatory body. Moreover, the response to issues of scarcity from Beijing and central water agencies has typically been one involving proposals for massive new infrastructure to divert water from one region to another rather than new approaches to management. One such massive project is the South-to-North Water Transfer Project, which will funnel 45 billion cubic meters (bcm) of water to the northern part of the country through teh Yangtze River basin but will not be completed for several decades at the earliest. There are also plans for investment in water distribution systems and the construction of more than 1,000 water and wastewater treatment facilities. Plans for coastal water desalination are also in their early stages.

Regional conflicts over water allocation have emerged from a national water policy that seems centered around moving water from region to region via large infrastructure projects. This national policy stance is not new. The intensity of the problem in some regions can be witnessed by the fact that periodic clashes have occurred since the 1970s over water from the Zhang River. The North China Plains also face fierce competition over water, as Beijing's growing population has led to the city's exploitation of nearly all major rivers flowing through surrounding provinces.

Figure 2 highlights the potential water availability issues and their intersection with potential gas developments. Notice, with the exception of only a couple of basins, the coincidence of shale gas resources and water stress is very high. Due to potential water constraints, we have substantially reduced the technically recoverable shale gas resource base in China in our Reference Case. However, we do compare this outcome to one in which any potential water issues can be largely overcome, which results in a technically recoverable shale resource base that is substantially larger. We describe all scenarios in more detail below.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.