Author(s)

In a paper forthcoming in The Energy Journal (Hartley, 2015), I examine motivations for entering long-term contracts to trade LNG. Consistent with the industry focus on the “bankability” of long-term contracts, the model posits that the key motivation for long-term contracts is that they reduce cash flow variability and thereby increasing the debt capacity of large, long-lived, capital investments for both the exporter and the importer. Increased leverage in turn reduces the cost of financing. These considerations imply, and the formal model shows, that additional debt under a long-term contract, and the benefits of a long-term contract relative to spot market trade, increase substantially with increasing spot price variability.

In this paper,1 I examine the recent evolution of markets for LNG and interpret those developments using insights from the model. I focus especially on the increasing amount of LNG being traded spot or under short-term contracts of less than four years duration. I argue that explanations for this, and other recent changes in LNG trading, imply that the proportion of LNG being traded under long-term contracts is likely to continue to decline and that the flexibility of long term contracts for trading LNG is likely to continue to increase.

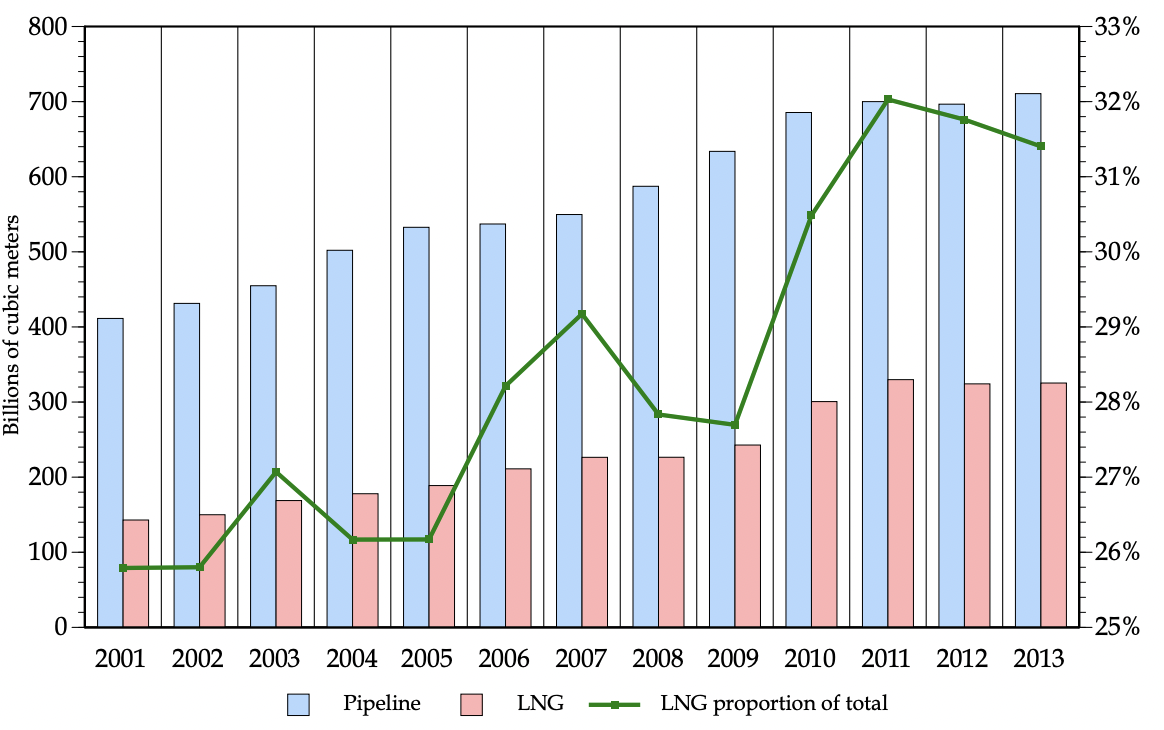

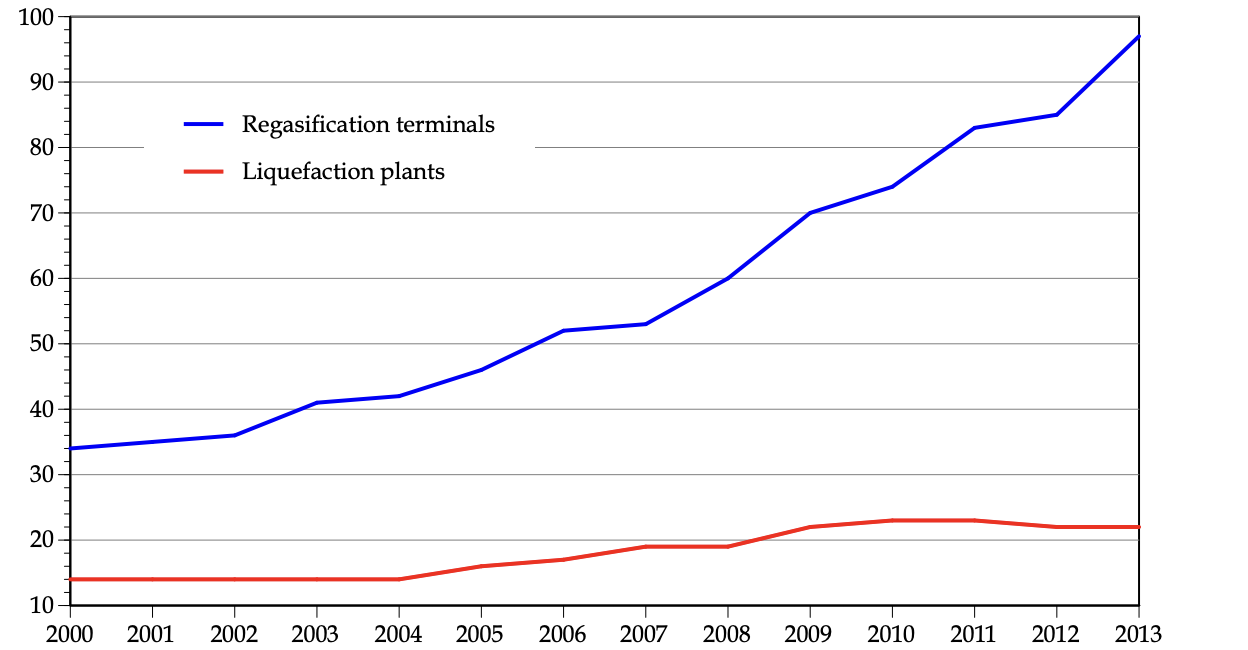

While international trade of natural gas via both pipeline and in the form of LNG has grown over the last decade or so, Figure 1, based on data from the BP Statistical Review of World Energy,2 shows that the amount traded as LNG has tended to grow somewhat more rapidly. Figure 2, based on data from the International Group of Liquefied Natural Gas Importers (GIIGNL), shows that the growth in LNG trade has been accompanied by growth in the numbers of liquefaction and regasification terminals, but that the latter has grown more rapidly than the former. This likely reflects the increasing economies of scale in liquefaction plants relative to regasification plants. Hence, a larger number of regasification plants can be served by a given liquefaction plant.

Figure 1 — International Pipeline and LNG Imports

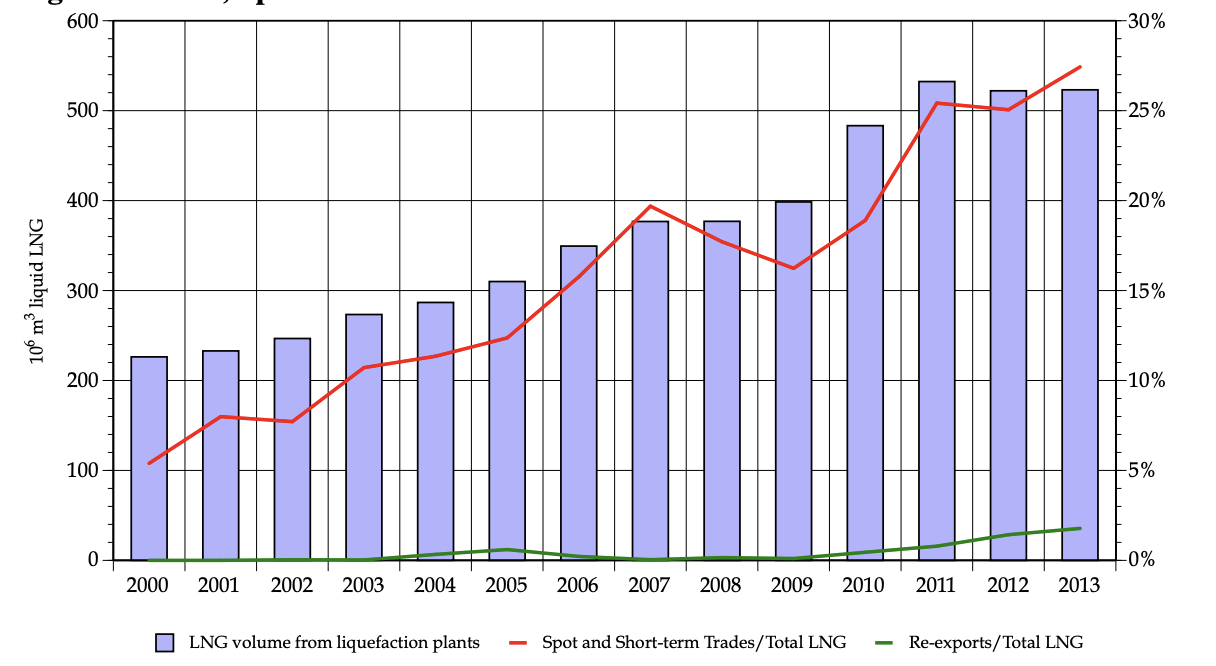

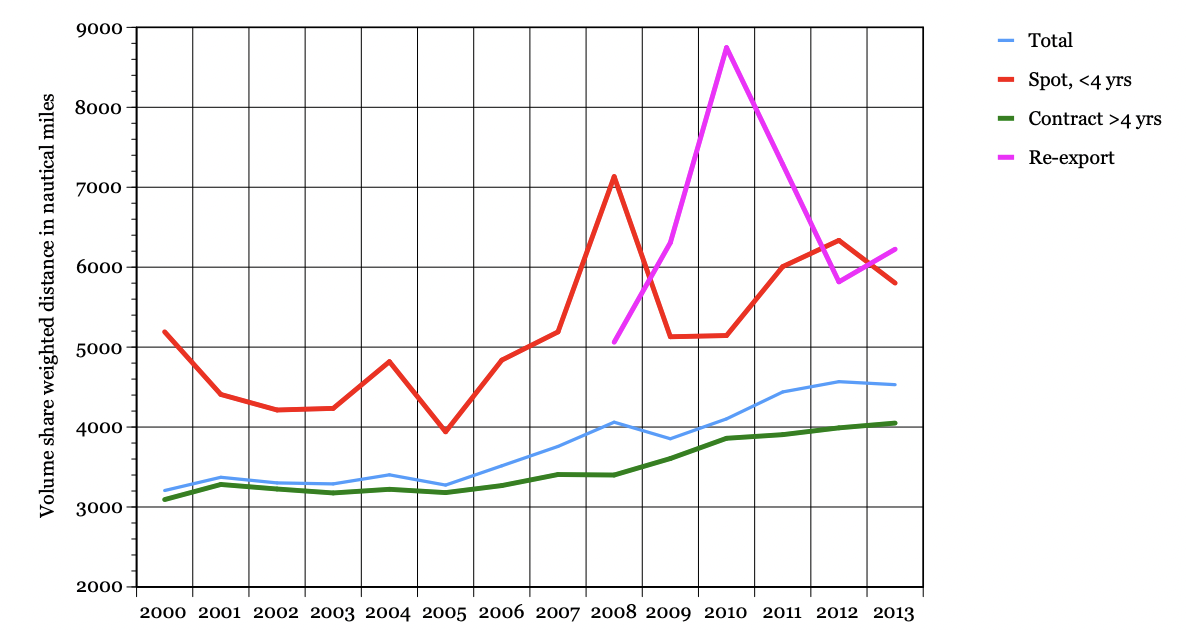

The structure of the LNG market also has changed substantially over the last decade or so. In particular, while long-term contracts between exporters and importers have long dominated the international market for LNG, this has been changing over the last decade or so. Figure 3, also based on data from GIIGNL, shows that spot and short-term (less than four-year duration) contract trades generally increased from 2000 to become more than 25% of total trade after 2011. Figure 3 also graphs re-exports of LNG as a proportion of total LNG traded from liquefaction plants.

Figure 2 — Growth in Liquefaction and Regasification Terminals

Figure 3 — Total, Spot and Short-term LNG Trade

Writing in the IGU 2006-2009 Triennium Work Report (International Gas Union (2009), hereafter referenced as IGU (2009)), Bezanis and Ahmad discussed the evolution of destination clauses in long-term LNG contracts. Such clauses prevent the importer from re-exporting LNG to another buyer if the price they can get exceeds the value of the LNG to them at the moment. Bezanis and Ahmad note that while increases in the number of buyers and sellers of LNG have made destination clauses more difficult to enforce, the finding by the EU Commission in 2001 that destination clauses are anti-competitive also played a role. Suppliers of natural gas to Europe subsequently gradually eliminated such clauses. Also writing in IGU (2009), Nakamura remarked that spot market trades had been stimulated by re-export of cargoes from buyer’s LNG storage tanks and increased destination flexibility in long-term contracts.

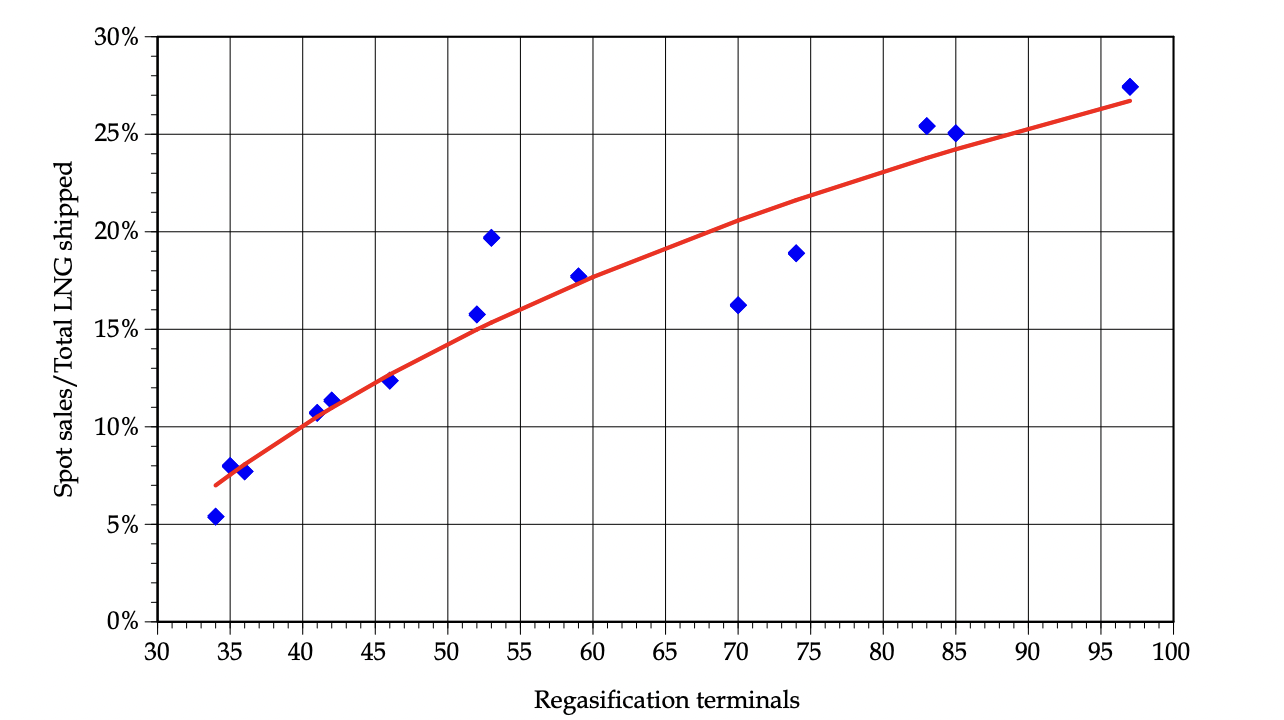

Figure 4 — Proportion of Spot LNG Trade and Number of Regasification Terminals

The period of substantial re-export of LNG is too short to make definitive statements about what it may be most closely related to. There is some evidence, however, that the growth of spot and short-term trading may be closely related to the increase in the number of buyers of LNG. This is illustrated in Figure 4, which is also based on GIIGNL data. The curve also graphed in the figure suggests a simple log-linear relationship.3

Spot / Total = 0.1881ln(Regas) − 0.5932; R2 = 0.9167

The model presented in Hartley (2015) provides a possible explanation of the relationship graphed in Figure 4. The major disadvantage of long-term contracts is that they limit the ability of the contracting parties to take advantage of profitable short-term trading opportunities. The model presented in the paper shows how take-or-pay provisions4 and supplemental spot market trades limit the inefficiencies arising from contract limitations on trading outside of the longterm contract. Supplementary spot trading by parties to the contract can be thought of as exercising embedded options. As a result, it is not surprising that I find that increased variability of spot prices raises the value of these options and hence tends to increase the volume of spot market transactions undertaken by contracted parties.5

In the paper, I also argue that the variability of LNG demand shocks is likely to be much greater than the variability of LNG supply shocks. For example, demand will be affected by weather shocks, changes in the prices of competing fuels (especially for generating electricity), changes in business cycles that affect the demand for electricity and changes in the industrial demand for natural gas. Hence, an increase in the number of importers of LNG will greatly increase the opportunities to take advantage of short-term fluctuations in demand and prices.

Supplementary spot market trades by parties to long-term contracts can also be interpreted as greater use of swap agreements, increased destination flexibility in long-term contracts, and an increase in “branded LNG” whereby sellers of LNG source their supply from multiple locations instead of entering into contracts that tie imports by one customer to a small number of liquefaction plants.

Several other authors have noted that long-term contracts associated with LNG projects developed since 2000 have featured increased flexibility in these dimensions. For example, Nakamura (IGU (2009)) noted that some then recent LNG export projects had made final investment decisions without 100% off-take commitments by buyers. This left uncommitted quantities available for spot market trades. Nakamura also discussed growth in “branded LNG.” Similarly, Thompson (2009) notes that BG has signed contracts with several suppliers that allow it divert LNG to higher-value markets as the opportunity arises. To support this activity, BG has its own ships and considerable storage capacity at Lake Charles, Louisiana and the Dragon terminal in Wales. In fact, many major liquefaction and regasification terminals have substantial on-site LNG storage. National Grid sells available capacity in a dedicated LNG storage facility at Avonmouth in the UK. Singapore has also recently built a regasification terminal that will have throughput capacity surplus to domestic needs. This is apparently meant to facilitate pursuit of arbitrage opportunities in the LNG market.

Thompson (2009) also notes that, as the LNG market has matured, some early long-term contracts have expired leaving suppliers with spare capacity and without a need to finance large investments. Many of these suppliers have entered the short-term and spot market rather than sign new long-term contracts.

Finally, as emphasized by Weems (2006), long-term LNG contracts have become more flexible. For example, recent contracts allow quantity adjustments to cope with a multitude of circumstances, much greater destination flexibility, a much wider range of pricing options (including linking LNG prices to spot market natural gas prices) and price review provisions. Such contract provisions allow parties not only to cope with temporary operational disruptions but also to exploit profitable short-term trading opportunities.

An implicit assumption of the model developed in Hartley (2015) is that the contracting partners tend on average to be better suited to trading with each other than with outside parties. The model developed in that paper also shows that the advantages of a long-term contract decline as the average surplus in the trading relationship declines relative to the outside options. Specifically, let pX(t) denote the netback spot price available to the exporter if it has to sell to its next best alternative customer at t, pM(t) the next best import price available to the importer if it has to buy from its next best alternative supplier at t, p the long-term contract price to the importer and S the shipping cost from the liquefaction plant to the regasification plant (so p–S is the export netback price). The prices pX(t) and pM(t) will tend to be positively correlated if LNG markets are reasonably well-arbitraged, but since the locations of the next best customer for the exporter and next best supplier for the importer can differ from one period to the next, the relationship between pX(t) and pM(t) will generally vary over time. The parties to the long-term contract will be better suited to trading with each other than with outside parties if S is smaller than the average gap between pM(t) and pX(t). I then show that a smaller gap between and the average spot prices available to the importer reduces the advantages of a long-term contract. I also show that a smaller gap between average netback spot prices available to the exporter and the average spot prices available to the importer encourages substantially more spot market trading by parties to the contract.

The GIIGNL data contains volumes of LNG shipped between different trading partners. It also provides a table of active sea transportation routes in each year and the distances traversed by those voyages. Unfortunately, the latter data do not appear to be completely accurate.6 We therefore consulted a separate source to derive a consistent set of shipping distances. The locations of the liquefaction and regasification terminals in each country were identified using Google maps (the relevant facilities are relatively easy to identify using the satellite images and Google maps then provides the corresponding latitudes and longitudes). These locations were then entered into the web site VesselDistance.com to obtain an estimate of the shipping distances between the liquefaction terminals in nautical miles. In most cases, these distances corresponded closely with the ones reported by GIIGNL. In many cases, when two countries are recorded to have traded LNG, there is more than one pair of liquefaction and regasification terminals in the list of active transportation routes for that year that could have been involved in the trade. We therefore averaged the shipping distances for the possible routes to obtain a shipping distance for the LNG traded between the country pair. Using these distances, we were then able to calculate the average distance LNG was transported when the trades were conducted under long-term contracts or spot or short-term contracts or were re-exports. The results are graphed in Figure 5.

Figure 5 — Average Transportation Distance for Different Types of LNG Trades

Focus first on the average distance that LNG is transported regardless of the type of trade (the light blue line in Figure 5). One might have thought that the large increase in numbers of potential trading partners revealed in Figure 2 would have reduced the average distance that LNG is traded. Since the global surface area is finite, an increase in the number of trading pairs eventually must have this effect. Over the period under consideration, however, the opposite has occurred. A possible explanation is that the falling cost of shipping LNG has facilitated longer distance trades, although different growth rates in regional demands no doubt has played a significant role. In particular, the last decade has witnessed a decline in US demand and simultaneous rapid growth in demand in East Asian markets, which are further form the major sources of supply. Such a longer-term structural explanation is consistent with the generally rising dark green line in Figure 5, which shows the average transport distance for the subset of trades conducted under long-term contracts.

The most striking result in Figure 5, however, is the large gap between the red and fuchsia lines on the one hand and the green line on the other. Consistent with the model discussed in Hartley (2015), this gap shows that long-term contract trades tend to occur between partners that are better suited to trading with each other because the costs of trade are lower.

What does this analysis suggest about future developments in the market for LNG? Prospective exports of LNG from the US should further stimulate the trends toward more spot and short-term trading and greater flexibility in long-term LNG contracts. These projects have featured sales on a tolling basis whereby the customers purchase the gas from the US market at a price related to the Henry Hub price and then pay the liquefaction plant operator a fee to liquefy the gas and load it onto ships for export. Many purchasers have also contracted for supply that would go into global portfolios rather being dedicated to any particular customer. Of relevance to the model of long-term contracting presented in Hartley (2015), many of these projects also plan to use modular liquefaction units with lower capacity, but also much lower capital costs per unit of capacity than current technology. Many of the projects also can utilize port and pipeline facilities previously constructed to support regasification terminals, further reducing up-front capital costs. Lower investment costs in turn reduce the need for long-term contracts to stabilize cash flows and underwrite debt financing. The reduced up-front capital costs and further development of “branded LNG” or portfolio trading should also reduce the benefits of vertical integration between LNG liquefaction capacity and LNG marketing.

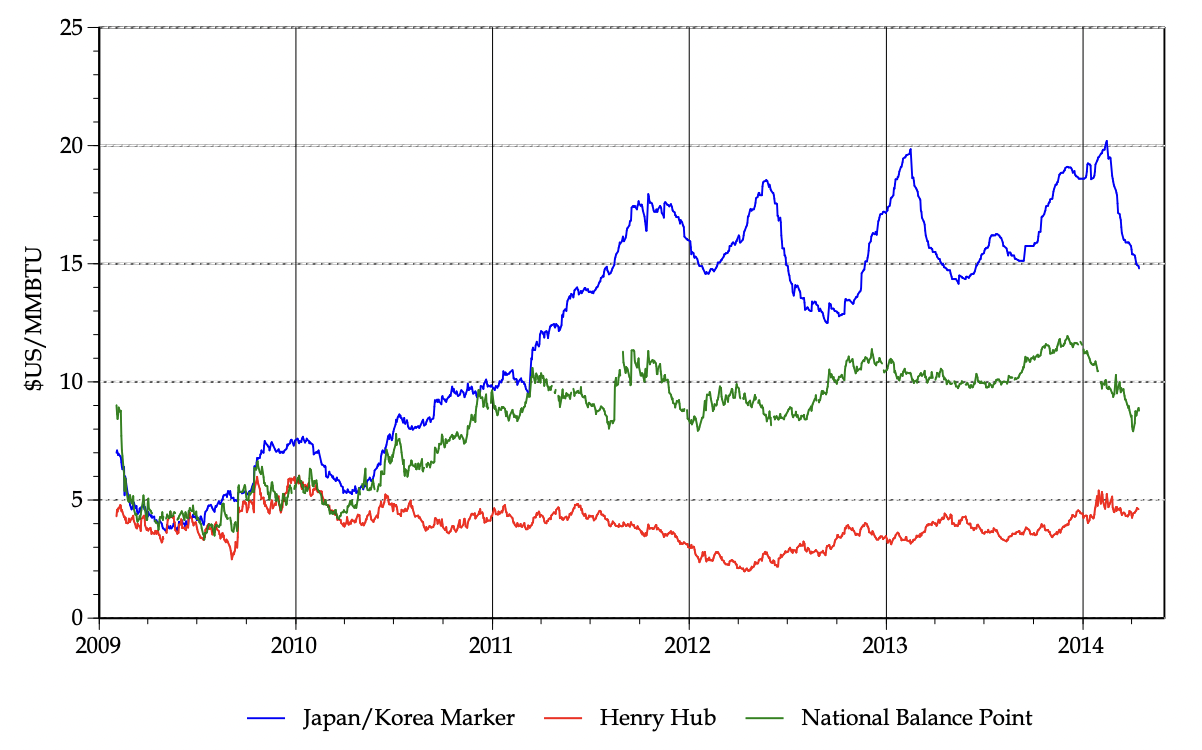

Increases in spot and short-term trading and greater flexibility in long-term LNG contracts could, in turn, reinforce the initial increase in spot market liquidity. In a previous paper (Brito and Hartley, 2007) co-authored with a colleague at Rice University, we explained how the LNG market could be characterized by multiple equilibriums, and shift between those equilibriums as expectations changed. Specifically, we showed that a small exogenous increase in spot market liquidity could stimulate additional spot market trading in market equilibrium. Simultaneously, the surplus from trading under a long-term contract would decline, thereby likely reducing the liquidity of the long-term bilateral contract market. These changes could make developers of new projects more content to leave more of their capacity exposed to spot market trading. While the focus of this article has been on the growth in spot and short-term trades and how they may facilitate price arbitrage in world natural gas markets, many other commentators have instead continued to speak about segmented markets. They have in mind the large gaps between natural gas prices in different parts of the world. This is illustrated in Figure 6 using spot market prices for the US, UK and NE Asian markets.

Figure 6 — Recent Evolution of Spot Natural Gas Prices

Figure 7 — US LNG Imports Relative to Marketed Natural Gas Production

Rather than focusing on the gaps between prices after mid-2010, however, I would instead point to the close relationship prior to that time. The divergence of the Henry Hub price from mid-2010 resulted from the expansion of unconventional production which effectively turned natural gas into a non-traded good for the US and Canada market as a whole.7 This is illustrated in Figure 7, which graphs US imports of LNG relative to marketed natural gas production. Once exports of LNG from the US begin, they should again link US prices to prices prevailing in trading partners, albeit with a discount to reflect the costs of liquefaction, transportation and regasification.

The other price divergence reflected in Figure 6 occurs in March 2011, when the Japan-Korea marker price deviates from the NBP price in the UK. This is evidently the result of the Fukushima nuclear disaster. Following the disaster, the Japanese government shut down all of Japan’s nuclear power plants, greatly increasing the demand for LNG to generate electricity.8 The large increase in prices is analogous to a basis blowout that occurs in the US market when, for example, a very cold episode in the northeast (as in the winter of 2014) increases demand beyond the capability of the current delivery infrastructure. The large differential between LNG prices in northeast Asia and elsewhere should largely disappear if either Japanese nuclear plants are re-started (greatly decreasing the temporary surge in demand) or new supply is bought on stream to satisfy the higher long run demand.

In summary, based on our analysis, we foresee continuing evolution of world LNG markets toward a larger proportion of volumes being traded on short-term contracts or sold as spot cargoes, and increased use of swaps, re-exports and other short-term arrangements to take advantage of temporary arbitrage opportunities. Conversely, volumes moved under long-term contracts can be expected to decline in the years ahead. We should also expect the current dramatic divergence in natural gas prices around the world to diminish greatly as a result of price arbitrage.

References

Brito, Dagobert and Peter Hartley. 2007. “Expectations and the Evolving World Gas Market.” The Energy Journal 28, no. 1: 1–24.

Hartley, Peter R. 2015. “The Future of Long-term LNG Contracts.” The Energy Journal (forthcoming).

International Gas Union. 2009. “2006-2009 Triennium Work Report, Programme Committee D Study Group 2, LNG, Chapter 3: LNG Contracts.” Paper presented to the International Gas Union 24th World Gas Conference, Buenos Aires, Argentina, October 5–9.

Thompson, Stephen. 2009. “The New LNG Trading Model: Short-Term Market Developments and Prospects.” Poten & Partners, Inc. Paper presented to the International Gas Union 24th World Gas Conference, Buenos Aires, Argentina, October 5–9.

Weems, Philip R. 2006. “Evolution of Long-Term LNG Sales Contracts: Trends and Issues.” Oil, Gas and Energy Law 4, no. 1.

Endnotes

1. I thank Michael Maher for valuable comments.

2. The data graphed is imports. The US Energy Information Administration (EIA) also reports data on total imports of dry natural gas by country and region and imports of LNG. However, as of October 2014, the latter series terminated in 2009. The two series give similar values for LNG imports, but the EIA reports substantially higher volumes of pipeline imports with the difference generally declining over time. LNG grows as a proportion of total imports in both series. The LNG imports reported in both the BP and the EIA statistics also are reasonably close to the data reported in the other source for graphs in this article, namely the annual statistical reports produced by the International Group of Liquefied Natural Gas Importers (GIIGNL).

3. The fraction of spot and short-term trade was not as closely related to the number of liquefaction terminals (sellers). The coefficient on this variable was insignificant when included in the regression.

4. Weems (2006) notes that take-or-pay provisions were not present in all LNG contracts signed in the 1960s but became standard in LNG contracts signed in the 1970s. He also observes that take-or-pay provisions remain in recent contracts even though they have allowed more flexibility on other margins.

5. The model also shows that changes in the variability of spot prices (holding the average levels fixed) have complicated effects on the optimal contract price and volume. Increased variability of spot market prices also tends to increase the ex-post inefficiencies of contractual limits on trading, and on that account reduces the attractiveness of long-term contracts.

6. For example, voyages that should be very similar in length sometimes are not, while the same voyage is sometimes recorded as being of different length in different years. In addition, in many years, trade volumes between countries are reported without there being a corresponding pair of origin and destination ports in the two countries listed in the table of active shipping routes.

7. It also freed up LNG from Trinidad to go to Europe, thereby replacing a relatively short-distance trade by a longer distance one. On the other hand, LNG from Qatar that had previously been destined for the US market instead was shipped generally longer distances to northeast Asia. Further expansion of northeast Asian demand relative to European demand could further increase the average shipping distance for Qatari LNG.

8. According to data from the EIA, following a decline of more than 43.6% in Japanese nuclear output in 2011 relative to 2010, natural gas consumption (supplied almost entirely by LNG imports) jumped more than 13% from 2010 to 2011 and more than an additional 0.5% from 2011 to 2012. The further, almost 89% decline in nuclear generation in 2012 relative to 2011 was compensated largely by increased coal and oil use, with the consumption of both growing by more than 5.5% from 2011 to 2012. While electricity consumption fell by more than 7% from 2010 to 2011, it was virtually unchanged from 2011 to 2012.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.