Author(s)

Executive Summary

With the recent approval of Mexico’s energy reform and the current enthusiasm of South American governments to attract foreign investment in oil, one might be tempted to conclude that the tide of resource nationalism is receding in the region. Nevertheless, the cycles of investment and expropriation that have characterized the oil sector in Latin America are unlikely to go away.

Recent History

The first decade of this century witnessed one of the largest resource windfalls for commodity exporters in history. Countries in Latin America benefited tremendously from the large and persistent increase in commodity prices. The price of oil in particular increased from a low of $10 per barrel in 1998 to above $100 per barrel 10 years later, generating a revenue boom for the region’s net exporters of hydrocarbons: Venezuela, Mexico, Ecuador, Colombia, and Bolivia. It also significantly benefited Brazil, a large producer but net importer, and even Argentina, a rapidly declining exporter.

As in the 1970s, the oil boom was accompanied by a wave of resource nationalism, that is, a government encroachment on the property rights of foreign investors. In the period from 2002 to 2012, taxes were significantly increased, contracts were forcefully renegotiated, and foreign investors were nationalized outright. This happened in four out of the five hydrocarbon exporters with foreign investment in oil and gas: Venezuela, Bolivia, Ecuador, and Argentina. In Mexico, the largest oil producer in the region, the oil industry remained a state monopoly until 2014.

As recently as 2012, the Argentinean government nationalized YPF, the formerly privatized national oil company, crowning a decade of eroding conditions for oil investors in the region. Some countries, such as Brazil and Colombia, did not follow the expropriation trend. Still, Latin America was the leading example of a global phenomenon of increased state intervention and nationalization. All around the world, the government “take” increased in most oil-exporting countries. Russia is the most notable example, but others in the Caspian region, Africa, and the Middle East followed this trend as well. In fact, even in Brazil—one of the countries that attracted the most oil investments during the previous decade—some symptoms of resource nationalism have been apparent.

In contrast, during the last five years we have witnessed a strong countercurrent of government efforts to attract foreign oil investment to the region. This has happened despite the fact that one of the triggers of the nationalist tide, the oil price boom, has not faded away. Venezuela, the leader of the resource nationalist movement, announced in 2009 that it would auction new areas for joint ventures with foreign companies in extra-heavy oil projects in the Orinoco Belt. This occurred just a couple of years after the nationalization process that started in 2005 was finalized in 2007. During the last five years, PDVSA, the Venezuelan national oil company, has signed seven major extra-heavy joint venture projects with foreign partners, including Chevron, CNPC, ENI, Repsol, and Rosneft. These projects would require more than USD 100 billion in investment and, when completed, would yield more than 1.5 million barrels a day in production. PDVSA has also pursued smaller partnerships with foreign companies in conventional oil production, and a major offshore non-associated natural gas project in a joint venture with Repsol and ENI. In fact, despite the radical leftist discourse of the Venezuelan government, it has been actively courting foreign investors since 2013.

Undoubtedly, the most important new development in the region’s oil industry is the opening of Mexico’s hydrocarbon sector to foreign investment. After more than seven decades of state monopoly, the administration of President Enrique Peña Nieto—leader of the PRI, the party that nationalized the sector in 1938—promoted a pathbreaking constitutional reform to make this opening possible. Thus, the last stronghold of resource nationalism in the region moved toward granting a significant role to the private sector in the exploitation of oil and gas resources. This event will very likely reconfigure the Latin American oil industry in the decades to come.

Even Argentina, after it renationalized in 2012, quickly announced that it wanted to attract foreign investors to develop its massive unconventional shale resources in the Vaca Muerta basin of the province of Neuquén. Recently, it signed a joint venture with Chevron to develop these resources and announced a settlement with Repsol, the expropriated shareholder of YPF. Similarly, after the expropriation of oil contracts, Ecuador signed significant deals with CNPC, the Chinese national oil company, which has become a key player in the production and especially the marketing of Ecuadorian oil. Lastly, in the past few years, Bolivia has also announced new investment projects with foreign partners in natural gas. Meanwhile, Brazil, Colombia, and Peru keep regularly auctioning oil blocks for exploration.

So, is the resource nationalism wave fading in the region? It is important to understand the structural causes of the phenomenon to properly answer this question.

The Origin of the Investment, Expropriation, and Reopening Cycles

One might be tempted to attribute the recent wave of resource nationalism largely to the more general phenomenon of the resurgence of left-wing politics in Latin America. After all, the nationalizers—Hugo Chavez of Venezuela, Evo Morales of Bolivia, Rafael Correa of Ecuador, and Cristina Kirchner of Argentina—are leaders of the more radical version of the leftwing movement in the region. In contrast, countries that have not expropriated or moved in the opposite direction—such as Brazil, Colombia, and Peru, or more recently Mexico—have had either moderate-left or center-right parties in power. However, to understand the dynamics of resource nationalism, it is important to focus on the deeper determinants of the historical cycles of private opening and resource nationalism. These are the incentives faced by political leaders under different scenarios of international prices, production and reserve tendencies, and net exports (imports).

Expropriation tends to occur when prices rise substantially, because its benefits increase significantly. This has been shown to be the tendency around the developing world. Nationalization is also more likely in an environment of high and increasing reserves and production and when the country is a large net exporter. Thus, after a cycle of significant and successful private investment, the probability of expropriation paradoxically increases. Due to the size of the oil rents, which can be as high as 90 percent of revenues, the magnitude of the fiscal benefits can be politically irresistible. Most relevant petroleum exporters are fiscally reliant on oil, that is, oil revenues represent more than 30 percent of total government revenue. Moreover, because it is a high sunk-cost sector in which investments have long-term maturity, the effects of a decline in investment can take years to lead to the consequent decline in production. Therefore, government leaders with a short-term horizon can be tempted to obtain high immediate benefits while deferring costs, leaving future leaders to bear the political consequences of declining production and revenues. To illustrate the dynamic of incentives, this issue brief will focus on the three leading producers and reserve holders in the region: Venezuela, Mexico, and Brazil.

Venezuela: A Successful Opening Breeds Nationalization, While Stagnation Breed Pragmatism

In the 1990s, facing low oil prices, fiscal crises, and significant investment needs, Venezuela opened the oil sector to private investment in riskier and less profitable projects. This was a major departure from the nationalization in 1976, which had made state-owned PDVSA the monopoly producer. The opening brought in significant investments by major international players, including Exxon, Shell, BP, Chevron, and Total. This allowed for a significant increase in production of more than 1 million barrels per day (equivalent to more than one-third of current production levels).

President Chavez was elected in 1998 when oil prices bottomed out, but he did not change these oil deals until 2005, after all major investments had been made and prices had increased significantly. The protracted and confrontational expropriation process that ensued significantly increased the government’s share of revenues. It also had significant reputational effects, delaying all major new investments and creating very high opportunity costs in terms of foregone future production. Lately, as production faltered and the high-spending regime became desperate for more revenues, pragmatism has led the government to offer investors better terms and guarantees. Even though investors are still very cautious, the change in the Venezuelan government’s attitude is palpable. If prices weaken, the government’s fiscal desperation will rise and it will offer more concessions to investors.

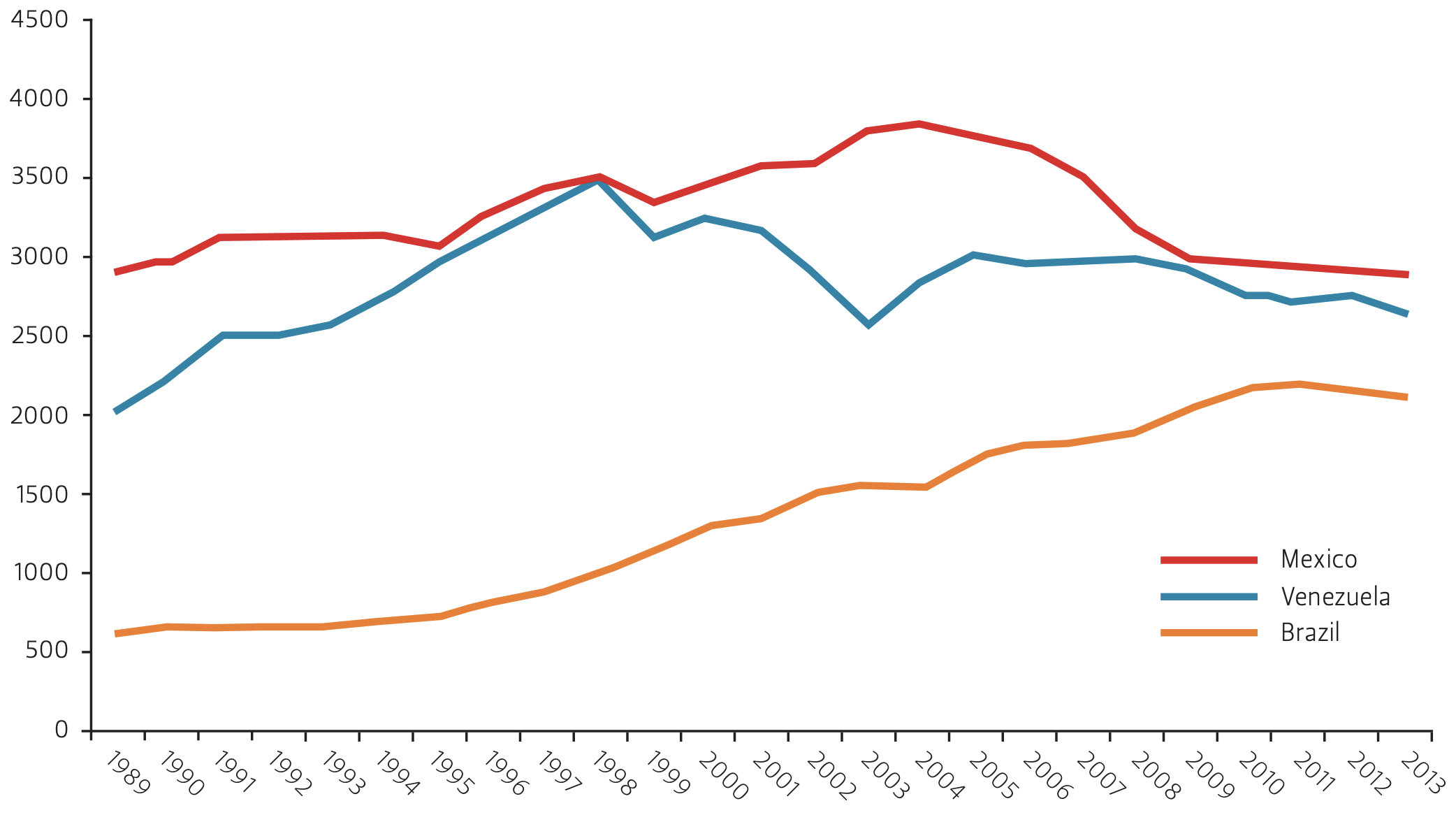

Figure 1 — Oil Production: The Big Three in Latin America (Thousand Barrels per Day)

In sum, foreign investors were victims of the price boom and their own success in increasing production and reserves. The cycle of investment and expropriation in Venezuela had significant similarities to what happened in Argentina, Bolivia, and Ecuador. In all four countries, an oil opening produced an increase in privately operated production, followed by expropriation when conditions were ripe.

Mexico: The Collapse of a Giant and Its Consequences

Mexico was an exception to the liberalizing trend in the 1990s. Historical and ideological reasons are relevant to explaining this exceptionalism, but the major factor behind the lack of reform is the fact that Mexico’s production kept increasing without significant new investments. The giant oil field Cantarell, which produced more than 2 million barrels a day at its peak (close to two-thirds of the country’s production), allowed the government to over-tax and conceal the significant inefficiencies of the national oil monopoly, Pemex. The future costs of the lack of investment were not perceived by the political leadership and even less by the general public, so there was no push for reform.

Once Cantarell’s production started to collapse in 2005, the need for reform became clearer, but high oil prices made it less urgent at first. However, as Pemex’s capital expenditures dramatically increased but only barely slowed declining output, the case for reform became much stronger. Cantarell’s production has declined by more than 75 percent from its peak. With the election of President Peña, institutional gridlock eased and reform was finally passed. Mexico, as Venezuela in the past, is opening the riskier, less profitable projects, which require large investments and complex technology. In contrast to Venezuela, it is building a robust institutional framework to support reform. This might provide a longer life to the investment cycle. However, if the incentives for expropriation appear in the future, one cannot discard the possibility of a partial reversion of reform, especially given the enduring strength of nationalistic ideology in Mexico.

Brazil: Resource Nationalist?

Even though Brazil is still a net importer of oil, it has increased its production more than fourfold over the last two decades to levels comparable to Mexico and Venezuela. That success is largely the result of the liberalization of the oil industry in the 1990s, when Petrobras, the national oil company, was partially privatized and the petroleum sector opened to foreign investment. As a net importer, the country was eager to maximize its production and, until recently, did not focus on extracting fiscal rents. However, the discovery of massive deep offshore reserves in the pre-salt area began to change the incentives of the government. In contrast to its South American counterparts, Brazil did not nationalize or force the renegotiation of the contracts. However, it did increase the government’s share for future pre-salt projects. It required Petrobras to be the operator, established an ambitious policy of local content, and increasingly subsidized the domestic gasoline market. Moreover, the private shareholders of Petrobras were diluted when the government exchanged oil reserves for equity in the company, in a move that some analysts considered a form of expropriation.

Thus, even though Brazil has been considered a model of oil regulatory policy, the effects of its success and the prospect of becoming a net oil exporter have also induced a milder form of resource nationalism. This has already had negative implications for investment and production, which have not reached their targets during the last three years; in fact, production has been declining. Still, in comparison to other countries in the region, Brazil has maintained a rational and pragmatic long-term policy.

The case of Colombia has some similarities. When facing a collapse in production, Colombia copied the Brazilian liberalization model and had significant success in increasing production, but not yet in incorporating new reserves. In contrast to Brazil, this situation keeps providing strong incentives for the government to focus on providing relatively attractive conditions for investment.

Implications for the Future of the Latin American Oil Industry

As argued here, the incentives provided by price cycles, investment cycles, endowments, and institutions are key to understanding the waves of resource nationalism and liberalization. The region has been more prone to this type of policy volatility than other regions in the world, possibly due to the combination of factional democracies, weak rule of law, and high inequality.

Given propitious circumstances, resource nationalistic ideologies could flourish again. After a cycle of significant investment that adds substantial production and reserves, the incentives for changing the rules may resurface. Institutions that encourage governments to take longer-term approaches and that limit their ability to opportunistically renege on deals could moderate the effects of these volatile incentives. Independent regulatory agencies, as well as progressive and effective tax regimes that properly tax the windfall profits, would be helpful.

Conversely, changing incentives, like those induced by a period of low oil prices, could further promote pragmatism and liberalization. In general, net importers or countries that have declining production or reserves would be pressed to be more open.

From the countries’ perspective, resource nationalism is only a problem if it hinders the development of the oil sector and has negative long-term welfare implications. A pragmatic version of nationalism, one that maximizes enduring benefits for the nation without volatile policy cycles, is highly desirable, if all too rare, in Latin America. Understanding the challenges explored here and creating institutions to mitigate them should be one of the main long-term goals of policy reform.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.