Abstract

The United Arab Emirates has exhibited increasing discomfort with the OPEC cartel’s actions in recent years, particularly since 2016 brought Russia into a leadership role alongside Saudi Arabia in the enlarged OPEC+ group. Since late 2022, aggressive oil production cuts have left the UAE with a disproportionately large quantity of unused oil output capacity, prompting questions about the costs of its OPEC membership.

This paper examines arguments for and against a departure by the UAE from the cartel, which would be the most high-profile departure from the group to date, overshadowing Qatar’s 2019 exit. Overall, the UAE’s status as an ultra-wealthy and diversified economy with sophisticated diplomatic ambitions leaves it increasingly isolated within a producers’ club that, since the 2016 expansion, has become dominated by petrostates with stronger preferences for high oil prices.

We find that the UAE’s departure from OPEC would lead to clear short-term gains and the unfettering of the country’s oil production. Such a move could bring upward of $50 billion in additional yearly revenues based on current spare capacity and the completion of ongoing capital investment. Further benefits include prospects for improved relations with the United States. Such gains would have to be weighed against the likelihood of fractured relations with neighboring Saudi Arabia and the potential for a damaging price war.

Introduction

Abu Dhabi’s membership in the Organization of the Petroleum Exporting Countries (OPEC) has long been part of the emirate’s identity as a wealthy oil state with significant influence in the global economy. Abu Dhabi joined during OPEC’s formative years, even before the founding of the United Arab Emirates (UAE) in 1971. Early entry allowed Abu Dhabi to participate in the 1973 Arab oil embargo and join the spate of oil sector nationalizations that followed. The emirate’s enormous resource base, sophisticated production, and diplomatic skills have rendered it a central player within the cartel ever since. In turn, Abu Dhabi’s influence within OPEC has raised the country’s profile on the international stage.

Over the years, the UAE’s national interests have occasionally been at odds with those of other members of the cartel, including those of OPEC’s dominant player, Saudi Arabia. Abu Dhabi has previously managed to overcome those difficulties and remain supportive of Saudi leadership, even when it meant shouldering a disproportionately large share of the cartel’s collective production cuts.

But since the alliance expanded into OPEC+, bringing Russia (and other participating non-OPEC producers) into the fold in 2016, the UAE’s interests and those of the new Saudi-Russian leadership axis have diverged more sharply. The OPEC+ cartel has embarked on a markedly nonaligned path, with the Saudi leadership balancing its long-running partnership with Washington against an increasingly important working relationship with Russia and strategic ties with China.

The result within OPEC is a more “price-hawkish” oil market strategy that has favored preemptive production cuts aimed at heading off any potential decline in oil prices. The price-hawkishness has come alongside increasing support by Riyadh for Russia’s interests and a deterioration of Saudi-U.S. relations that has sharpened under the administration of U.S. President Joe Biden.

For the UAE, which in terms of oil policy is dominated by Abu Dhabi, the shift in OPEC’s approach appears increasingly at odds with its own resource monetization strategy. These differences are becoming apparent in the fraying of ties between the UAE and OPEC and between Abu Dhabi and Riyadh.

A key source of strain is Abu Dhabi’s inability to bring onstream the oil production capacity becoming available after a multiyear investment program overseen by the Abu Dhabi National Oil Company (ADNOC). ADNOC had already raised production capacity to about 4 million barrels per day (Mb/d)[1] in 2023 with plans to reach 5 Mb/d by 2027.[2] In March 2023, however, the UAE’s output was limited to roughly 3 Mb/d.[3] Following additional voluntary cuts that took effect in May 2023, the UAE’s production target fell below 2.9 Mb/d.[4] This leaves the UAE with more than 1 Mb/d of spare production capacity. In absolute terms, only Saudi Arabia holds greater spare capacity. As a share of total capacity, the UAE’s unused excess is by far the largest within OPEC — a lopsided burden that is likely to grow as ADNOC’s continued investment brings further capacity increases.

Another source of discomfort in Abu Dhabi is a newfound willingness of OPEC+ leadership — Saudi Arabia and Russia in particular — to disregard U.S. preferences for increased oil supply and reduced market prices. Saudi-OPEC clashes with Washington also appear to be causing Emirati officials to distance themselves from cartel decisions. In short, a series of disputes have ensued over what Emirati officials view as disproportionately large constraints on production capacity, over-aggressive Saudi-authored cuts, and a leadership structure that has both weakened prior relations with Washington and diluted Abu Dhabi’s once-influential role within the group.

Since 2020, various press reports have emerged suggesting that the UAE has considered a departure from OPEC.[5] The country’s frustrations spilled into public view in 2021, when Emirati negotiators walked away from talks to raise OPEC+ output as the world moved out of pandemic-era lockdowns. The walkout caused a temporary breakdown in cartel decision-making. The Financial Times reported “growing unanimity among Emirati officials surrounding de facto leader Sheikh Mohammed bin Zayed al-Nahyan that it could be in the UAE’s best interests to go it alone.”[6]

This paper examines the UAE’s struggles with the cartel and its dominant player, Saudi Arabia. We investigate changes in cartel dynamics since the OPEC+ expansion and appraise the costs and benefits of membership in seeking to determine whether the UAE would be better off outside the OPEC cartel. In analyzing these questions, we also examine whether pressure within OPEC is broad-based, or rather a product of increasingly fraught relations between leadership in Abu Dhabi and Riyadh. How much have the OPEC+ expansion and the increasing role of Russia weighed on the UAE’s membership? And how might Abu Dhabi’s relations with the United States and Saudi Arabia be altered by an OPEC departure?

The paper begins with historical background on OPEC and the UAE’s relations with the United States and Saudi Arabia. It then examines the precedent set by Qatar’s decision to quit the cartel in 2019 before exploring the rationales for Abu Dhabi’s potential departure from OPEC as well as for its remaining within the cartel. We conclude that any decision by the UAE to depart OPEC should hinge on its long-term view of relations with Saudi Arabia and the benefits of coordinating oil policy within the cartel. Leaving OPEC would certainly provide Abu Dhabi with improved freedom of action and a significant income boost based on its current quota, but these benefits come at the expense of damaged ties and lost influence with Riyadh, as well as a potential oil price war.

Historical Background

The emirate of Abu Dhabi joined OPEC in 1967, seven years after the cartel was launched in Baghdad by its five founding members: Saudi Arabia, Iraq, Iran, Kuwait, and Venezuela. The UAE formally assumed Abu Dhabi’s membership of OPEC (and OAPEC, the Organization of Arab Petroleum Exporting Countries) in 1974.[7] However, Abu Dhabi, with an estimated 96% of the UAE’s proven oil reserves, continues to govern national resource decisions, since the Emirati constitution assigns control over natural resources to the federation’s individual emirates.[8]

The Arab-led oil embargo of 1973-74 saw OPEC become a transformative force. The cartel oversaw the quadrupling of oil prices and the collectivized nationalization of member governments’ oil sectors.[9] At that time, Abu Dhabi acquired controlling stakes in companies operating its own oil and gas sector. But the UAE never pursued 100% ownership, preferring to maintain partnerships with international energy companies despite many other OPEC states opting for full nationalization.[10]

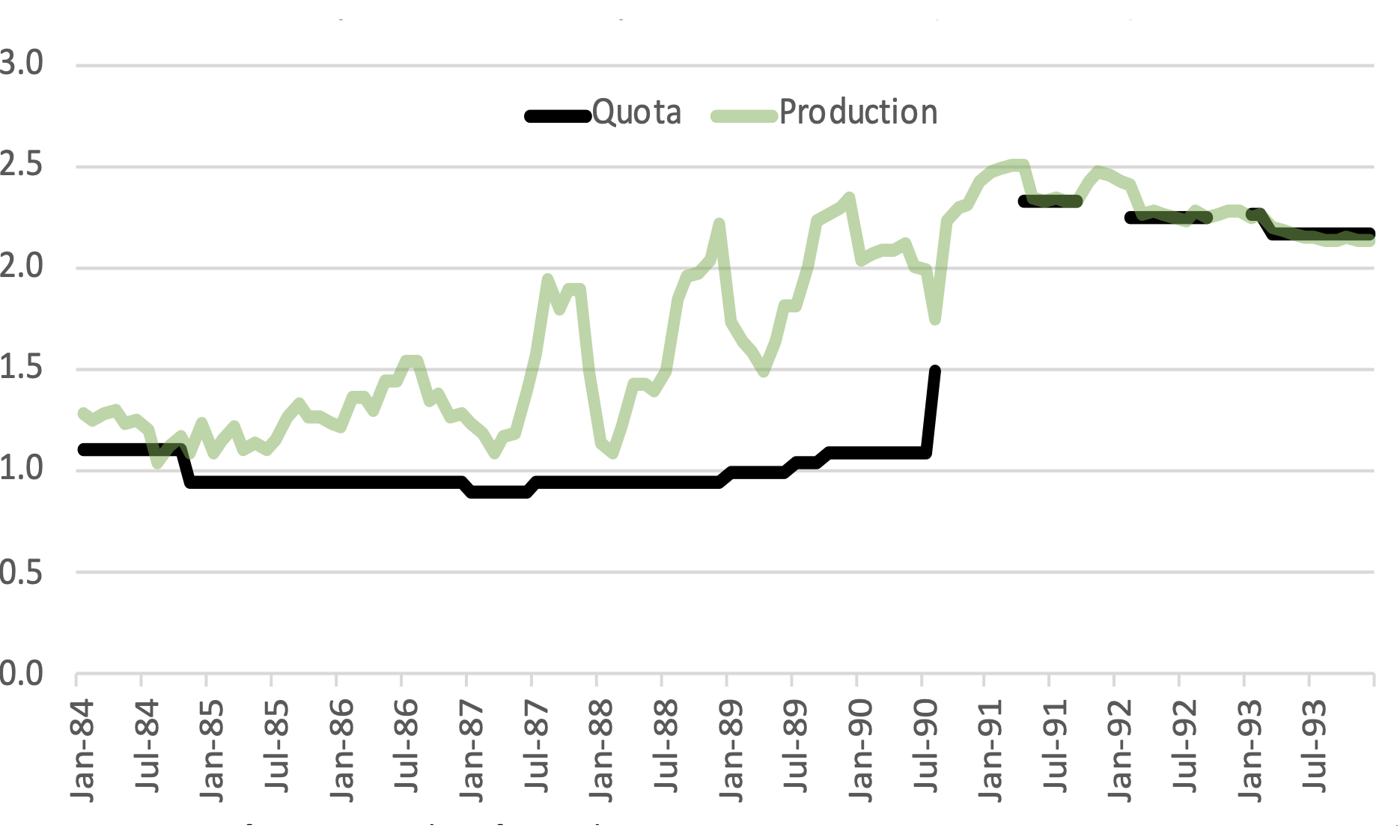

OPEC’s turn toward the “politicization of petroleum” brought long-term damage to the organization. Demand for oil fell during the 1980s, and new production came online in regions beyond OPEC’s reach. The cartel lost market share, and quota cheating further diluted its effectiveness. The UAE frequently exceeded its quota due to a dispute over whether OPEC quotas applied to the entire UAE or just Abu Dhabi;[11] this problem was resolved when Dubai’s production declined and production targets increased after the Iraqi invasion of Kuwait in 1990 (Figure 1).

Figure 1 — The UAE’s Production Consistently Exceeding Its OPEC Quota in the Mid-1980s

Note Gaps in quota history represent periods in which individual country quotas were suspended.

OPEC and its leadership in the Gulf’s oil capitals later disavowed resource-nationalist tactics in favor of pragmatic longer-term strategies aimed at price stability. Among these were the OPEC production increases in the early 2000s that served to moderate high prices.[12] Saudi Arabia’s actions — coordinating cuts in output with the rest of OPEC and increasing production to replace losses in capacity elsewhere — suggested a practice of placing greater value on oil market stability than on maximizing price.[13] The kingdom and the Emirates appeared to prize stability to a greater extent than their OPEC peers, which exhibited a shorter-term price focus and competed within the group.[14] In fact, OPEC spare capacity was deployed frequently between September 2005 and October 2014 and was demonstrated to reduce the volatility of global prices by as much as half.[15]

In recent years, however, OPEC decisions began to reflect a return to a more nationalist footing. The cartel has exhibited a reduced commitment to price stability — or perhaps a higher price target around which it seeks stability — and an intensified focus on maximizing revenue for member states. The working relationship with Russia, institutionalized via the 2016 OPEC+ expansion in response to the U.S. shale oil boom, helped create a more openly antagonistic stance toward U.S. interests. Among those facing OPEC’s ire were U.S. shale producers, whose dramatic growth in production since 2007 forced OPEC to curtail output during an expansion of Chinese oil demand.[16] U.S.-OPEC disputes intensified in 2022 when the Biden administration protested a large output cut, discussed below.[17]

UAE-U.S. Relations

For Washington, the UAE has evolved over the past five decades from an underdeveloped quasi-dependency to a major strategic partner. In the 1970s, the tribal confederation was considered so unprepared for independence that many observers expected it to be overrun by a larger neighbor or disintegrate due to internal tensions.[18] The UAE’s transformation in the time since has cast aside such fears. The country has become a regional power and major trade partner with sophisticated security services that have participated alongside U.S. forces in Afghanistan, Bosnia, Libya, Iraq, Syria, and elsewhere. This track record earned it the label “Little Sparta” in a 2014 comment attributed to U.S. Gen. James Mattis, who later became the secretary of defense in the Donald Trump administration.[19]

For most of the three decades after the UAE’s formation in 1971, its relations with Washington were low-key, with the young federation focused on nation-building. Sheikh Zayed bin Sultan Al Nahyan, ruler of Abu Dhabi from 1966 to 2004 and the “founding father” and first president of the UAE, maintained close relationships with states in the Arab and Islamic worlds, as well as a lifelong commitment to the Palestinian cause.[20] Zayed embraced the UAE’s participation in the Arab oil embargo between October 1973 and March 1974, stating, “If Arab land continues to be occupied and subject to aggression, we will use every weapon we possess, and first of all oil, to liberate our land.”[21] In Dubai, Sheikh Rashid bin Saeed Al Maktoum laid the non-oil foundations of the emirate’s economy.

Shaping today’s UAE-U.S. relationship was the devolution of ruling duties to the founders’ younger sons, Sheikh Mohammed bin Rashid Al Maktoum of Dubai and Sheikh Mohammed bin Zayed Al Nahyan of Abu Dhabi.[22] As Dubai’s oil production declined, Mohammed bin Rashid developed Dubai as a hub for trade, tourism, logistics, and financial services.[23] In Abu Dhabi, Mohammed bin Zayed led the response to the September 11, 2001, terrorist attacks in ways that exceeded his role as Army chief of staff and presaged his 2004 elevation to crown prince.[24]

In 2006, a political firestorm over the acquisition of a U.S. port management contract by a Dubai firm led Emirati policymakers to spend heavily on strengthening Beltway relationships.[25] Shared political and security interests became evident when the George W. Bush administration and Congress supported a landmark nuclear cooperation agreement with the UAE in 2009.[26] The 2020 signing of the Abraham Accords with Israel further established the UAE as a pacesetter and key partner of Washington in the shaping of the Middle East.[27]

Emirati-Saudi Relations Outside OPEC and the Oil Market

Relations between Saudi Arabia and the five other member states of the Gulf Cooperation Council (GCC) are inescapably bound up with imbalances in their size and conventional power. Saudi Arabia is seven times larger than Oman, which itself is bigger than the other four Gulf states put together.[28] Almost all the smaller Gulf states had territorial or political disputes with Saudi Arabia at various points in the 20th century.[29] For example, a 1970s border dispute with Saudi Arabia delayed the kingdom’s recognition of the UAE until 1974, three years after its formation.[30]

Several flash points indicated that bilateral ties between the UAE and Saudi Arabia remained tense even after the passing of Zayed in 2004 and of Saudi Arabia’s King Fahd bin Abdulaziz Al Saud in 2005. In the mid-2000s, Saudi officials protested against the construction of the Dolphin gas pipeline in an unsuccessful attempt to stop the project from supplying Qatari natural gas to the UAE and Oman.[31] Further, the Emirati-Saudi border dispute — seemingly settled in 1974 — flared up again in 2006, when the UAE published a map depicting a disputed territory as Emirati, and again in 2009, when Saudi officials temporarily restricted the entry of Emirati citizens holding identification cards emblazoned with the map in question.[32]

Further acrimony arose in 2009 when Riyadh was chosen as the site for the GCC Central Bank, an institution that Abu Dhabi had lobbied vigorously to host. The UAE then withdrew from the planned monetary union, scuttling the long-awaited project.[33] The following year saw a naval clash between Saudi and Emirati vessels, which drew international attention.[34]

When the Arab uprisings kicked off in 2010, however, the UAE and Saudi Arabia put aside these differences and began making common cause. Abu Dhabi and Riyadh perceived Qatari sympathies for Islamist-led political transitions as a threat, and moved to thwart such change by providing support to Egypt’s military-led government after the overthrow of then-President Mohamed Morsi’s Qatari-backed Islamist government. The UAE and Saudi Arabia also joined forces in 2015 against the Houthi movement in Yemen. In addition, the pair coordinated to place pressure on Qatar, first in 2013-14 and then in the wide-ranging effort to isolate Doha from 2017-20.[35]

Emirati-Saudi regional cooperation was bolstered by a perceived, albeit temporary, affinity between Mohammed bin Zayed (MbZ), the former crown prince and present ruler of Abu Dhabi, and Mohammed bin Salman Al Saud (MbS), the ambitious young son of King Salman who became crown prince of Saudi Arabia in 2017. MbZ may certainly have seen himself as a mentor to MbS, particularly in the early years of MbS’s rise from relative obscurity.[36]

Bilateral tensions reemerged, however, during the UAE’s 2019 redeployment of most of its forces away from the front line in Yemen. Abu Dhabi’s leadership also disagreed with Saudi Arabia’s willingness to resolve its dispute with Qatar. The two monarchies clashed further over trade tariffs in 2021 around the time of one of their OPEC+ disagreements.[37]

Further souring ties with the UAE — and especially Dubai — were revelations that the Saudi government was preparing to compel international companies to situate their regional headquarters in the kingdom as a prerequisite for doing business there. Still further challenges to the UAE’s economic interests arose in the announcement of plans to construct a massive new airport in Riyadh and launch a new Saudi airline.[38]

Gulf Regional Relations and the OPEC Factor

The Persian Gulf region has always been the heartland of OPEC. With the exception of Venezuela, all of the founders have a coastline on the Gulf. Qatar, which joined the cartel in 1961, was a member until 2019. The UAE’s 1967 entry was the last by a Gulf country. Oman and Bahrain never joined, although in 2016 both began cooperating with the expanded OPEC+ cartel.

OPEC is famously resilient to disputes between its member states. The unbroken membership of Iran and Iraq during their war of 1980-88 is the best-known example. Saudi Arabia and Iran also maintained a working relationship within OPEC even as bilateral diplomatic relations were cut in periods of tension, such as between 1988 and 1991 and again between 2016 and 2023. Governments have tended to value the strategic benefits of collaboration on oil market strategy and the added geopolitical stature of cartel membership, which outweigh the reduced freedom of oil output decisions. A few countries have departed — most notably Qatar, but also Indonesia and Ecuador (both of which quit, rejoined, and quit again). Gabon has also quit and rejoined.[39]

The Most Recent OPEC Exit: The Case of Qatar

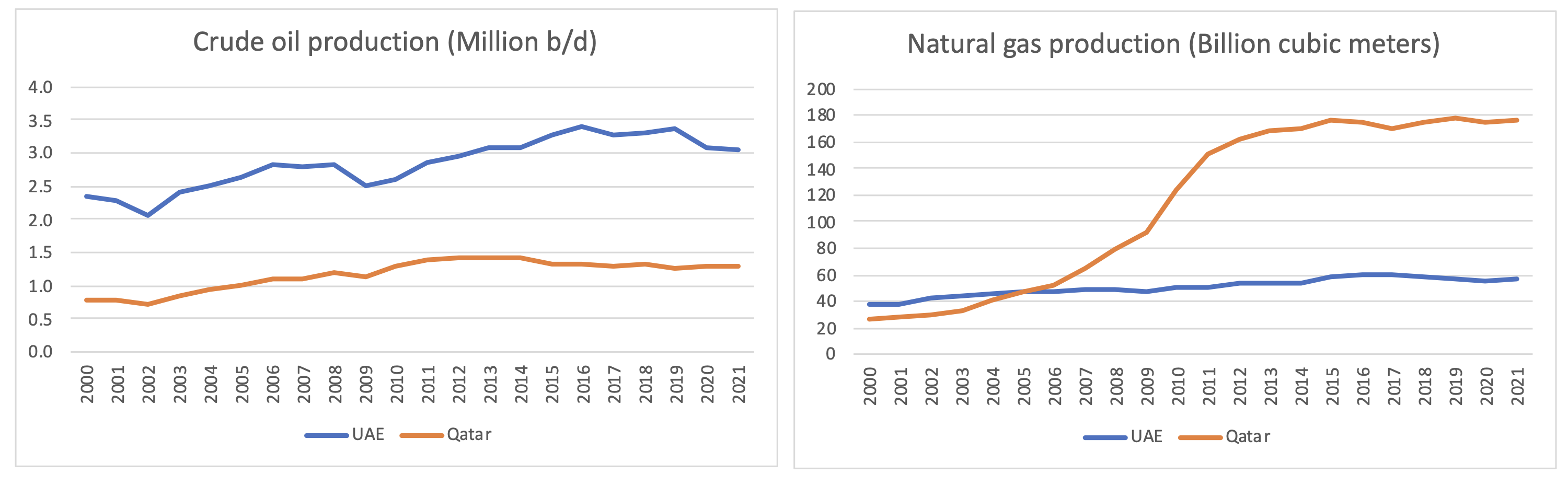

Perhaps the closest analogy to a potential departure by the UAE is Qatar’s 2019 OPEC withdrawal. The UAE and Qatar share numerous similarities, including their governance type, high per capita wealth, and paths toward economic diversification. But their resource bases are very different. Qatar’s hydrocarbon economy is dominated by the world’s largest nonassociated (i.e., not associated with oil) natural gas field, with a legacy crude oil sector far smaller than the UAE’s. In 2021, Qatar exported nearly 130 billion cubic meters (bcm) of natural gas (mainly as liquefied natural gas — making it at that time the world’s largest LNG exporter) while the UAE, a net gas importer, exported less than 10 bcm and imported nearly 20 bcm.[40] Doha’s OPEC departure was underwritten by huge growth in natural gas exports — which are not regulated by OPEC quotas — which had already increased its autonomy from the cartel.

Further, the Qatari decision to quit OPEC was not driven by production restraints imposed by the cartel, but rather arose from disputes with neighboring member states (Saudi Arabia and the UAE in particular) and by a recognition that Qatar’s energy future lay in gas. Qatari misgivings emerged in December 2018, when the country’s energy minister announced the departure in the midst of the blockade led by Abu Dhabi and Riyadh.[41] Soon thereafter, Qatar’s former prime minister described membership as a constraint on Qatari autonomy, saying OPEC was “useless” and “being used for purposes that harm our national interest.”[42] Saad Sherida al-Kaabi, Qatar’s minister of state for energy and the president and CEO of Qatar Petroleum (now QatarEnergy), added bluntly that OPEC had become “an organization managed by a country,” in clear reference to Saudi Arabia. Al-Kaabi noted that Qatar was unwilling “to put efforts and resources and time in an organization [it was] a very small player in,” and that he didn’t have a say in what was to happen.[43] Possible legal liabilities under the No Oil Producing and Exporting Cartels (NOPEC) legislation being debated in the U.S. Congress at the time may have further undermined the appeal of an already questionable membership.[44]

Qatar’s exit triggered no obvious backlash from the oil market or from other OPEC members beyond the ongoing Saudi- and Emirati-led blockade. A departure by a major OPEC producer like the UAE would be more disruptive, damaging the cartel’s market power and creating friction with the remaining members. The UAE produced 3.7 Mb/d of oil (total liquids production) in 2021 — nearly 2 Mb/d more than Qatar — on reserves nearly four times as large.[45]

Figure 2 — Dramatic Increase in Qatar’s Natural Gas Production

Emirati-Saudi Disputes in the Context of the Oil Market

Emirati misgivings about OPEC membership appear centered around production quotas and declining influence within the cartel’s post-2016 decision-making procedures. Ultimately, these grievances boil down to Abu Dhabi’s relationship with cartel leader Saudi Arabia. As we have seen, that relationship has been a mercurial one. Since the 1950s, Abu Dhabi-Riyadh relations have ranged from periods of open conflict to close friendship. But in past decades, oil market strategy has been one area of long-running agreement, with few outward signs of strain.

That pragmatic partnership appears to be waning. With increasing frequency, Abu Dhabi has found itself at odds with Riyadh and within OPEC+ over what it perceives as overweening constraints on its production ambitions and a lack of influence over the cartel’s decisions. Emirati requests for an updated production target reflecting its expanded capacity provoked a brief crisis within OPEC in 2021 (as mentioned above). That standoff was resolved when the UAE was granted a 10% increase in its “reference” production figure — upon which changes to quotas are based — to 3.5 Mb/d. This was accompanied by smaller reference increases (in percentage terms) for Saudi Arabia, Russia, Iraq, and Kuwait.[46]

More recent disputes have revolved around Riyadh’s increasing adherence to the so-called Saudi First doctrine. Under MbS’s de facto leadership, the kingdom has demonstrated newfound willingness to disregard U.S. preferences in favor of domestic priorities and in support of Saudi common interests with Beijing and Moscow.[47] The shift in Saudi behavior appears to be causing Abu Dhabi to distance itself from — or even disavow — some cartel decisions.

For instance, while Abu Dhabi issued a public statement in support of OPEC’s controversial October cut of 2 Mb/d, Emirati officials repudiated that statement in press leaks. Under condition of anonymity, sources from the UAE made it known that National Security Adviser Sheikh Tahnoun bin Zayed — brother of the Emirati president — traveled to Riyadh in a failed attempt to dissuade MbS from imposing what Abu Dhabi viewed as reckless cuts with obvious political implications for the U.S. midterm elections, then just two weeks away.[48] The leak served to differentiate Abu Dhabi from Saudi Arabia in Washington, where anti-Saudi sentiment was running high.[49]

Worth caveating is that the Saudi-Emirati disputes also coincided with the acute oil market stress of the COVID-19 pandemic and its sharp effects on oil demand. Global prices plummeted alongside oil consumption when government-ordered lockdowns shuttered entire economies in 2020, causing the OPEC+ group to implement the most dramatic voluntary oil production cuts on record. The plunge was followed by swift oil demand recovery in 2021 and 2022. The pandemic triggered widespread disagreement around OPEC’s oil market strategy.

OPEC+’s post-pandemic approach appears to favor the maximization of short-run revenue by restraining production, while the UAE’s preference (for reasons discussed elsewhere) is more weighted toward stepped-up output and shorter depletion horizons, with oil rents leveraged to diversify its economy beyond oil.

Unfortunately for Abu Dhabi, its preferences are outweighed by the Saudi-Russian axis, as well as the inclusion of a greater number of poorer petrostates like Nigeria, Azerbaijan, and Angola, which (unlike the wealthy UAE and Kuwait) lack the wherewithal and/or resources to invest in expanded production and diversify their economies. As a result, there appears to be greater consensus on group-wide production restrictions to support prices.[50]

Exacerbating the Saudi-Emirati strains are the kingdom’s travails in attracting foreign direct investment (FDI) to fund its spate of state-driven “gigaprojects,” such as Neom, the futuristic city being constructed in northwest Saudi Arabia. Such multibillion-dollar projects form the crux of MbS’s Vision 2030 goals, upon which the crown prince has invested considerable prestige. The large spending requirements and dearth of FDI are further drivers of Saudi preferences for higher oil prices.

Additionally, cartel governance has shifted to less transparent mechanisms. Russia and Saudi Arabia have made strategic decisions outside normal discussion fora, and then presented those as faits accomplis during broader OPEC+ meetings. For example, the voluntary OPEC+ cut in April 2023 was decided on informally, outside of the group’s established meeting process. Transparency within the cartel appears to be waning, with smaller producers increasingly sidelined. The UAE’s stature as OPEC+’s No. 4 producer (behind Saudi Arabia, Russia, and Iraq) and second-largest holder of spare capacity seems insufficient to assure it a correspondingly robust role in decision-making.

Reasons to Leave OPEC: What's to Be Gained?

Why might the UAE want to depart the cartel? The largest motivating factor is freedom of action in oil production and export. The UAE seeks short-term leeway around production and price decision-making as well as long-term positioning around the energy transition. But the deterioration of Emirati-Saudi ties also looms large.

Greater Freedom of Oil Production and Managing Through an Energy Transition

The UAE is carrying a disproportionate compliance burden in terms of the percentage of its production capacity sacrificed to the OPEC quota, and that burden is likely to grow over time as oil production capacity increases. This implies deepening losses in potential revenue and the UAE’s share of the oil market. On a more strategic, long-term level, diverging Emirati-OPEC+ strategies toward climate action pose even greater potential for friction and a stronger rationale for enhanced national control over oil output.

Tightened OPEC+ quotas have cost Abu Dhabi serious money in 2023. As mentioned, the UAE’s May 2023 quota — including both voluntary and mandatory cuts — is estimated at just under 2.9 Mb/d, which is less than 75% of the UAE’s total production capacity.

The UAE’s near-term economic interests would be better served by suspending its OPEC membership and maximizing production. At April 2023 prices, the UAE’s spare capacity represented foregone income of nearly $3 billion per month. With ADNOC’s expansion program intending to add another 1 Mb/d of new production by 2027 — with the aim of reaching the 5 Mb/d level — foregone revenues could nearly double. By 2028, therefore, departing OPEC could result in $50 billion to $70 billion per year in additional revenue.[51] That is roughly equivalent to 20% of Abu Dhabi’s 2022 GDP of $300 billion.

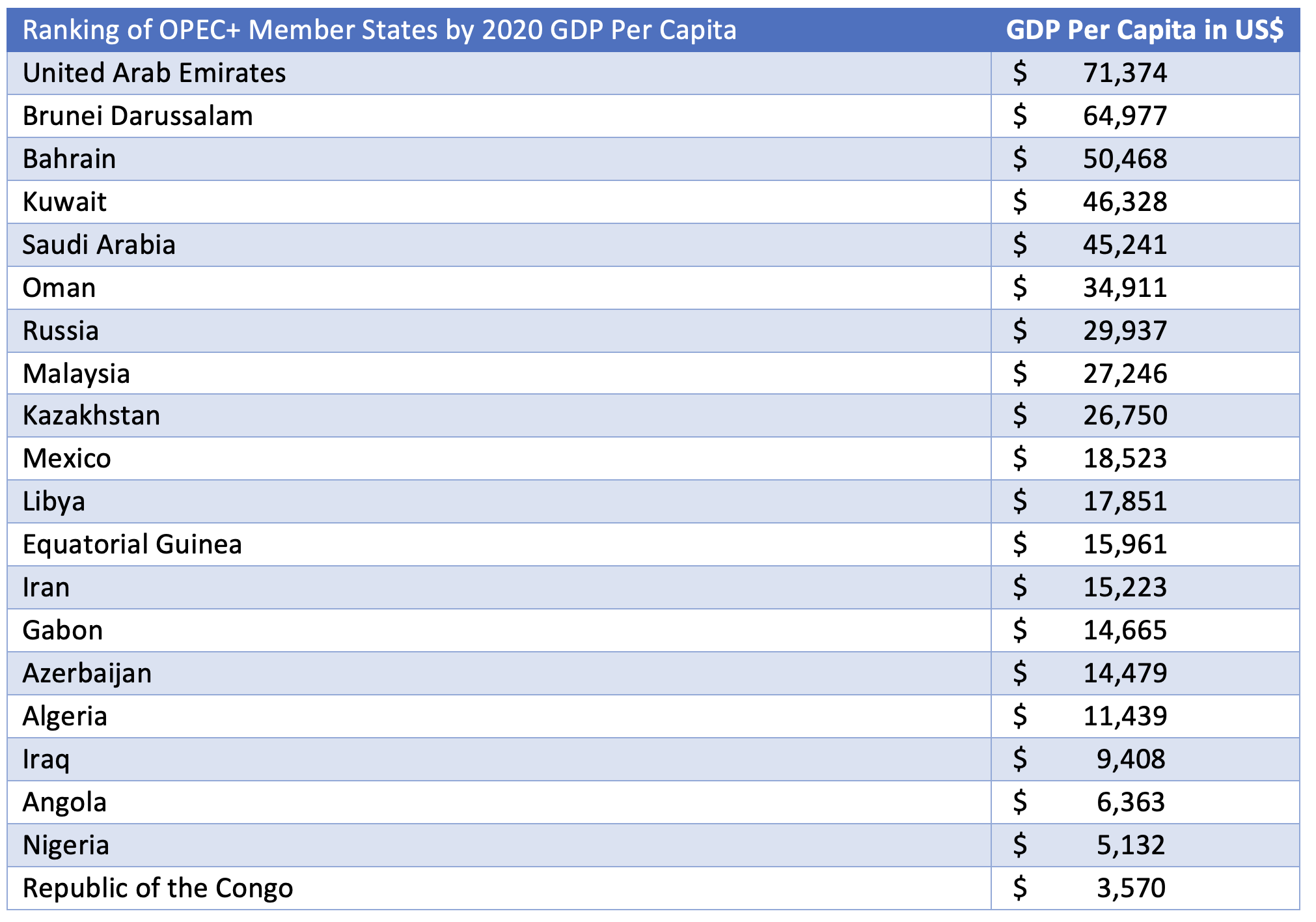

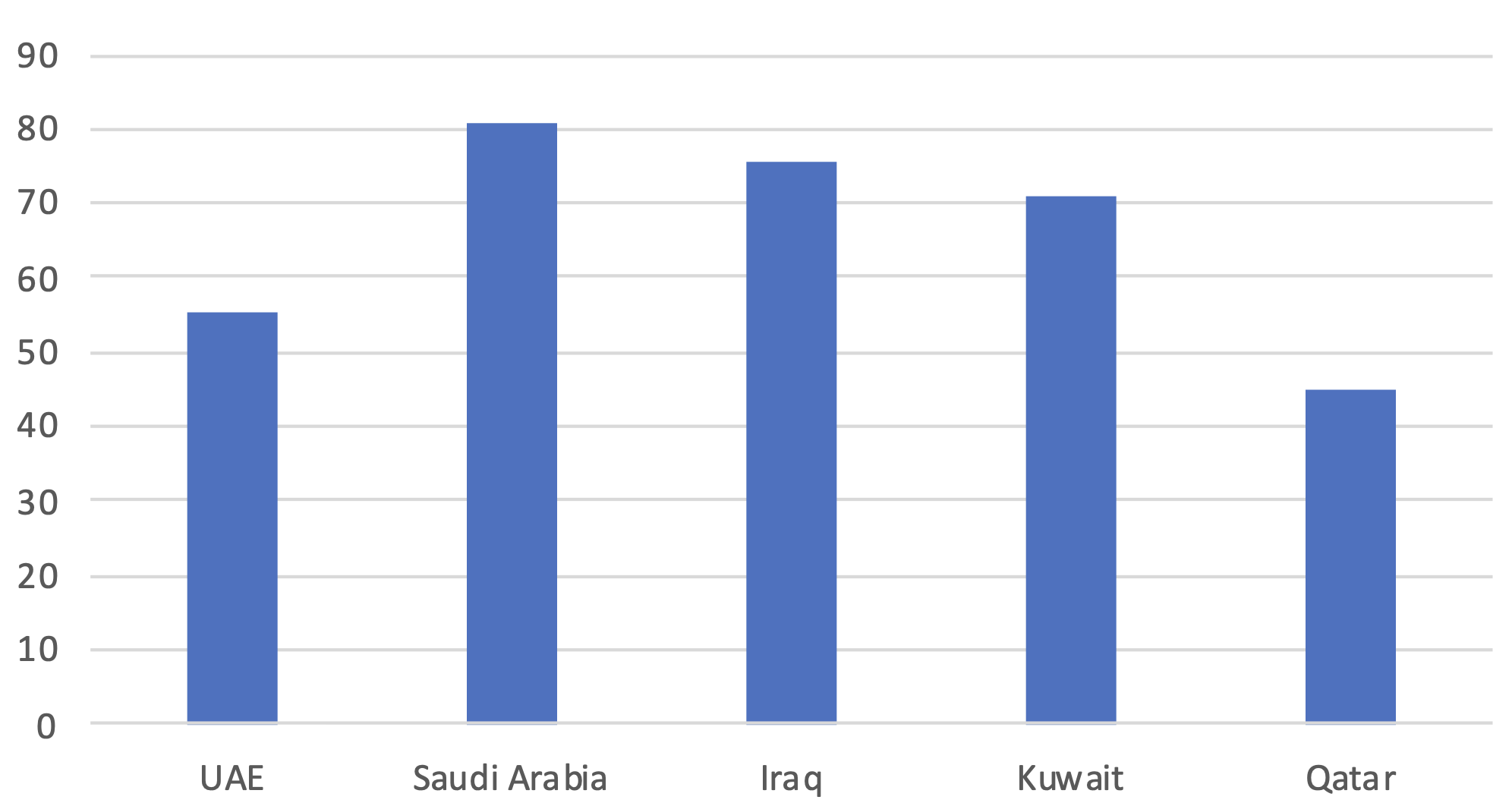

Further, OPEC would be hard-pressed to rein in a wayward UAE. Abu Dhabi is better suited to cope with lower prices or survive a price war than most of the OPEC member states. The UAE is by far the wealthiest member relative to population, with a GDP per capita nearly double that of Saudi Arabia, more than double that of Russia, and more than triple that of any of the 10 poorest producers (Table 1). In addition, the UAE holds one of the world’s largest sovereign wealth funds, and its diversified economy is better suited than many OPEC+ members to weather lower oil prices. The World Bank estimates that oil rents as a share of GDP in the UAE are half that of Saudi Arabia, and the break-even oil price for the UAE’s federal budget is much lower than Saudi Arabia’s (Figure 3).[52]

Table 1 — OPEC+ Countries Ranked by 2020 GDP Per Capita at PPP (current international $)

Note Recent data for Venezuela and South Sudan were unavailable.

Figure 3 — 2023 Fiscal Break-even Oil Prices ($ per barrel)

Having already begun to see the fruits of its capacity expansion, the UAE has been an early mover relative to other producers working to increase output. Meanwhile, Saudi national oil company Saudi Aramco in 2022 hastened its own plans to raise production capacity by 1 Mb/d to 13 Mb/d, matching the UAE’s target date.[53]

Another reason that oil producers might prefer to unburden themselves from OPEC’s production constraints has to do with the global transition toward clean energy. Countries that hold large oil reserves harbor concerns over the long-term viability of those resources, and one potential response is to reduce the risk of “stranded” reserves by increasing near-term oil output.[54] Ironically, officials in the UAE, Saudi Arabia, and other producer states have blamed energy transition policies for reducing investment in oil production more sharply than the corresponding decline in oil demand, a factor contributing to higher oil prices.[55] By this logic, ramping up production capacity can be touted as an effort to ensure a more “orderly” transition.

Moreover, freeing itself from OPEC would allow Abu Dhabi to more quickly diversify its economy. Revenues from stepped up oil production could be reinvested in insulating the Emirati economy from more aggressive global climate policies and any long-term decline in oil prices or demand, while investing in decarbonizing the national economy in line with the UAE’s pledge to reach net-zero carbon dioxide emissions by 2050.[56]

And finally, any departure from OPEC would signal a realignment of the UAE away from oil producers and toward a proactive position on climate more aligned with Washington and the European Union. Departing OPEC would also dovetail with the UAE’s role as host and leader of the 2023 United Nations Climate Change Conference (commonly referred to as COP28), which will take place in Dubai in December 2023. However, any cartel departure ahead of the COP28 talks risks a diplomatic backlash from oil-producing states that could undermine the success of the conference. This would augur for a delay in any withdrawal from OPEC until after the proceedings.

Greater Freedom of Diplomatic Maneuver

Emirati leaders view their country as a peer to developed economies, such as the members of the Organization for Economic Cooperation and Development (OECD), which pursue global, rather than regional, roles in international affairs. Leaving OPEC would demonstrate an expansion of Emirati statecraft and ambition, repositioning the country to face challenges associated with the energy transition and climate action.

A UAE outside OPEC would have greater flexibility to rethink “traditional” positions and adopt a forward-looking approach that fits an evolving global landscape, much as the 2020 Abraham Accords with Israel did at a regional level. While the UAE has sought to stay out of great power competition and strategic rivalries involving the U.S., Russia, and China, the rise of a genuinely multipolar order with many nodes of economic and political power has altered the horizons for Emirati engagement. Through Vision 2030, Saudi Arabia is seeking to insert itself into a rebalancing international order, but the UAE already possesses the logistical, infrastructural, and diplomatic heft to project itself on the world stage.

Improved Ties with Washington

An OPEC withdrawal might also bring an improvement in the UAE’s relations with Washington. Over the years, American politicians and pundits have labeled the cartel an “enemy of the free market” and a “club of adversaries” that colluded to undermine the economies of the developed world.[57] Exhibit A in this argument is OPEC’s role in the quadrupling of oil prices in 1974 and the nationalizations of member-state oil sectors. These events instigated an enormous transfer of wealth and geopolitical power from importing countries to oil-exporting states.[58]

This risk has reappeared now that OPEC+ has reoriented its emphasis toward a more activist quest for enhanced profits. The October 2022 specter of Saudi leadership pushing a production cut with the oil price at nearly $90 per barrel — while central banks worldwide grappled with inflation — triggered expressions of dismay from the governments of oil-consuming countries. (OPEC+ leaders note that subsequent oil price weakness in the face of a slowing world economy validated the decision to cut production.)

In the United States, the uproar was joined by President Biden and his staff. “We are re-evaluating our relationship with Saudi Arabia in light of these actions, and will continue to look for signs about where they stand in combating Russian aggression,” said John Kirby, a White House staffer with the National Security Council.[59] U.S. Senate Majority Leader Chuck Schumer declared, “What Saudi Arabia did to help Putin to continue to wage his despicable, vicious war against Ukraine will long be remembered by Americans.”[60]

The UAE’s stature in Washington may have been damaged by the country’s association with Saudi-led OPEC, given the dismay with the cartel’s willingness to undercut U.S. preferences in unfamiliar ways. In fact, the UAE’s ability to distance itself from the fallout was constrained by its OPEC membership, which implied support for the Saudi-authored cuts. Abu Dhabi was only able to make its opposition known via anonymous press briefings.[61] Those briefings suggested that the UAE remains attentive to policy and political discourse in the United States and is uncomfortable being portrayed as a disruptive actor.

Departing OPEC would put an end to the UAE’s double game, allowing it to maintain and strengthen ties with the United States without exposure to fallout from OPEC decisions. As an oil exporter, its interests in petroleum markets would remain congruent with those of OPEC, but departing the cartel would provide freedom of action on production and insulation from blame from Washington for OPEC market manipulation.[62] Other areas of strained relations with the U.S., such as the inflows of Russian capital into the UAE and concerns over a Chinese military facility reportedly under construction in Abu Dhabi, would remain, but these are unrelated to the UAE’s membership (or otherwise) in OPEC.

NOPEC Immunity

A subsidiary benefit could materialize in the event that the U.S. revives its longstanding threats of potential sanctions for cartel members based on U.S. antitrust laws. The passage of any so-called NOPEC bill would likely permit antitrust lawsuits to move ahead in U.S. courts. Plaintiffs might seek billions of dollars in damages for OPEC’s well-documented actions to constrain production and increase global oil prices, which guide pricing levels on petroleum products inside the United States. While successful judgments might not be uniformly enforced — and could perhaps be waived by the executive branch on grounds of national security — at minimum, the law’s passage would expose all OPEC member states to the possibility of future sanctions.

Immunity from NOPEC could represent one of a sheaf of diplomatic benefits for the UAE in any future U.S. campaign to convince Abu Dhabi to terminate its membership. Under the Trump administration in 2019, the risk of passage was sufficient to convince OPEC members and collaborators to alter the language used to describe their activities. OPEC officials began to describe the cartel as a “mechanism” rather than an organization. A document outlining the new OPEC+ alliance was carefully worded to emphasize “market stability” functions while avoiding antitrust trigger terminology such as “price preferences,” “quotas,” or “coordinated cuts” in production.[63]

It bears noting that the NOPEC bill has been introduced in Congress numerous times since 2000 and has never achieved passage into law. While sanctions on OPEC would play well among segments of the American public, such measures would also have drawbacks. These include deterring foreign investors from owning assets in the United States, angering allied countries over U.S. “interference” in sovereign trade relations that take place outside American jurisdiction, creating pressure for the oil trade to shift away from the dollar to reduce sanctions exposure, and harming the interests of U.S. oil producers that benefit from OPEC actions.

A Hybrid Approach?

Finally, the UAE can always reconsider any OPEC departure, as other members have done. If policymakers felt the gains from quitting were outweighed by benefits foregone, Abu Dhabi could follow the path of Indonesia, Ecuador, and Gabon and rejoin the cartel.[64] This possibility reduces the risk of a “brinkmanship” strategy, through which the UAE might threaten to quit without a relaxed quota forthcoming. If such demands went unmet, Abu Dhabi could demonstrate the credibility of its threat and actually depart the cartel. Later, if circumstances made OPEC membership more attractive, it could rejoin. A further hybrid option might be to quit and join the looser OPEC+ group of outsiders that caucus with the core cartel. Hybrid membership might allow the UAE to pump more oil and join cartel actions when convenient to national interests.

Drawbacks of an OPEC Exit

Despite the membership drawbacks outlined above, the fact remains that OPEC has persevered since 1960 due to the effectiveness of its actions and the value it provides its members, fiscally and diplomatically. The cartel is, as mentioned, exceptionally durable, able to carry out its duties amid global crises. In addition to the active management of production targets to support oil prices and national revenues, the foundation of its appeal to oil-producing states — and the aspects that have thus far protected it from antitrust actions — are found in two widely held principles of national self-determination: First, nation-states hold undisputed sovereignty over national resources. Second, sovereign governments are free to confer with each other over decisions that affect their individual and collective well-being.[65]

OPEC’s Benefits

Beyond these bedrock principles, OPEC provides valuable services for oil producers in terms of increased revenues and by moderating fluctuations in prices. Collective economic gains for oil producers from coordinated output appear too great to toss aside. For instance, OPEC cut its production by 5% in 2016, contributing to higher prices in 2017 and consequently resulting in revenues jumping by 29%.[66]

In the past, the OPEC cartel’s meetings provided a useful setting for discussion among exporters, and a forum where oil states interfaced with the global public — a forum that expanded its reach with the creation of the larger OPEC+ group. However, the recent move to more-cloistered and less-transparent OPEC+ meetings have changed the character of the organization. Whether or not those changes are permanent is unclear at the time of writing in May 2023, although the group has once again begun to hold at least some of its meetings in person. Regardless, OPEC (and OPEC+) leverages the economic magnitude of its activities to enhance the geopolitical profile and reputation of its members, including many small and weak states which otherwise lack comparable opportunities. The group also provides a forum for convening experts and engaging consuming countries and other stakeholders in dialogue.[67]

In addition, OPEC’s output manipulations might arguably be portrayed as marginally beneficial to the climate in the sense that, in a counterfactual world with no cartel, oil prices would likely be lower and oil demand — and therefore CO2 emissions — higher.

For the UAE: Increased Production, But No Guarantees on Other Goals

A departure from OPEC by the UAE could weaken the cohesiveness and effectiveness of the cartel. Since the UAE has long demonstrated adherence to quotas and alignment with Saudi leadership, the loss would be a significant blow to the cartel’s reputation, could encourage other members to quit, and could erode production discipline among the remaining members.

Leaving OPEC would imply that Abu Dhabi was no longer subject to the group’s production restraint and, as discussed above, would be free to produce at full capacity. (Other cartel members would decry such a move as “free-riding” on OPEC’s cuts to gain market share at the expense of the remaining cartel members, as they have argued in the past regarding the United States and Russia, before the latter joined OPEC+.)

Besides damaging a crucial institution of the global oil market, there are no guarantees that all the UAE’s grievances with the cartel would be assuaged by quitting. While an increase in Abu Dhabi’s oil export revenues could arise from unfettered production, quitting would not remedy the UAE’s concerns about a loss of influence within OPEC. Its influence on cartel decisions would go from insufficient to nonexistent. Withdrawing from OPEC would also reduce the UAE’s geopolitical stature outside the cartel. OPEC membership confers on the UAE not just influence on oil markets but the opportunity to be an interlocutor with Saudi Arabia and Russia. Of course, the loss of interlocutor status could be offset by an improvement in ties with the United States.

Moreover, a decision by the UAE to quit OPEC could trigger a response by the group — and by Saudi Arabia in particular — to engage in a price war. That is, members with spare production capacity could maximize output — as Saudi Arabia did in the early days of the COVID-19 pandemic — to force a price collapse and create incentives to bring other producers back to the negotiating table. While the UAE is well positioned to weather a price war because of its diversified, wealthy economy and small population, it would still see a significant reduction in oil revenues.

In the (unlikely) event of a complete breakdown of the organization, unmanaged production policies would drive a return of the extreme oil price volatility that has long been a feature of unmanaged oil markets.[68] Price shocks and wide swings in revenues impose costs on the national economies of producers and importers, as well as on businesses and individuals. Damages from oil shocks have been great enough that the United States, the world’s largest oil producer and consumer, played a leading role in the drastic OPEC+ cuts of 2020, when the COVID-19 pandemic led to an oil price collapse.[69] Volatility risks are a chief rationale for members’ maintaining surplus output capacity, which allows them to increase production during times of shortage.[70]

Risks of Further Retaliation

A total exit by the UAE from OPEC could also bring retaliation from remaining members in ways that extend beyond the oil market. Since Saudi Arabia and the UAE share long borders and airspace, a major dispute between the two that affected travel and trade would have capacity to cause serious economic hardship in the UAE. The Saudi- and Emirati-led embargo of Qatar between June 2017 and January 2021 involved the closure of borders and airspace as well as restrictions on the movement of people and trade. The Saudi leadership might conceivably ramp up efforts to isolate the UAE, analogous to ongoing Saudi moves to pressure international companies to relocate their regional headquarters to Riyadh by 2024. These could be augmented or enforced in more detrimental ways that take aim at the UAE’s stature as a hub for business, travel, tourism, entertainment, and trade.

Further, most of the surrounding countries in the region — including Iraq, Iran, and Kuwait — are OPEC member states, while Oman and Bahrain are OPEC+ members. Were these countries to band together to close borders or restrict airspace access or trade, the UAE could face even more critical hardships. Much of its imported food is transported across or grown in the surrounding OPEC member states, and its airlines’ competitiveness is based on access to regional airspace. The UAE’s position as a regional hub for goods shipped into the GCC’s common market could also be threatened. While such a harsh response is unlikely, the possibility bears investigation.

Conclusion

Abu Dhabi has been a stalwart of OPEC since 1967. As such, it has been a prime beneficiary of the cartel’s efforts over the years to increase oil revenues, nationalize foreign oil concessions, and manipulate oil markets to favor producers. One of the drivers of the UAE’s stunning wealth and national development arises from its willingness to devolve some national sovereignty over oil production to the collective interests of the cartel.

However, the UAE is now a highly developed nation-state with complex economic and diplomatic interests that extend beyond its exports of crude oil. Its economy has diversified more thoroughly than those of its fellow petrostates. For Abu Dhabi, oil is becoming a means to an end — the achievement of diversification and decarbonization necessary to meet its 2050 goals — rather than an end unto itself, as oil exports remain for most petrostates.

As such, further divergence is likely between the interests of the UAE and those of Saudi Arabia, Russia, and the large number of underdeveloped oil-dominated economies represented by OPEC. Abu Dhabi’s discomfort with OPEC’s quota management over the past few years appears as a symptom of a larger reality: In many ways, the UAE’s peers are the big diplomatic players within the OECD rather than the “nonaligned” developing states once represented by the Group of 77. The 2016 expansion of OPEC into OPEC+ has shifted cartel membership further toward the interests of the underdeveloped, for which price maximization remains paramount.

Add to this evolution the increasingly anti-U.S. cast that OPEC+ has adopted since the admission of Russia — and particularly since the start of the Biden administration — and the UAE’s status as an outlier becomes more pronounced. Abu Dhabi sees more merit in influencing Washington through pursuits of common cause than in incremental increases in earnings that antagonize its American friends.

The UAE’s near-term economic interests would be served by suspending its OPEC membership and bringing onstream its idled crude oil production. By 2028, when ADNOC’s expansion is complete, a strategy of maximum output could result in additional revenue of $50 billion to $70 billion per year at current prices. That is roughly equivalent to 20% of Abu Dhabi’s 2022 GDP.

Over the longer term, however, the case for departure looks murkier. The UAE’s small population, diverse economy, and enormous sovereign wealth fund suggest the country can attain its economic goals without the rash step of quitting OPEC and free-riding on the sacrifices of the cartel’s poorer member states. Such a self-serving move could cast Emirati-Saudi relations onto the rocks more permanently. The kingdom has demonstrated its willingness and ability to create discomfort within its region, with interventions in Yemen and Qatar, to name a few. Meanwhile, any improved Emirati partnership with the United States would be tempered by Washington’s bipartisan priority to reduce long-term exposure to the Middle East in favor of East Asia.

While the discussion presented here is neither fully informed nor exhaustive, our consideration of the potential risks and benefits of a departure by the UAE from OPEC highlights the short- and long-term dimensions of the decision and the critical importance placed by Emirati leadership upon the country’s long-term relations with Saudi Arabia.

Endnotes

[1] “UAE plans to increase its oil production capacity to 5mbd by 2025,” Gulf News, September 20, 2022, https://gulfnews.com/business/energy/uae-plans-to-increase-its-oil-production-capacity-to-5mbd-by-2025-1.90710432.

[2] Maha El Daha and Alaa Swilam, “UAE brings forward oil production capacity expansion to 2027,” Reuters, November 28, 2022, https://www.reuters.com/business/energy/uae-brings-forward-oil-production-capacity-expansion-2027-2022-11-28/.

[3] See Rosemary Griffin, Herman Wang, and Haripriya Banerjee, “OPEC+ crude oil production drops in March as sanctions hit Russian output: Platts survey,” S&PGlobal, April 11, 2023, https://bit.ly/3OIkaPg.

[4] OPEC Secretariat press release of April 3, 2023, and author calculations, https://www.opec.org/opec_web/en/press_room/7120.htm.

[5] Frank Kane, “UAE Leaving OPEC? A Storm in an Oil Barrel,” Arab News, November 23, 2020, https://www.arabnews.com/node/1766951; Natasha Turak, “Oil Prices Turn Positive After Falling by $2 a Barrel On a Report UAE is Considering Leaving OPEC,” CNBC, March 3, 2023, https://www.cnbc.com/2023/03/03/oil-prices-volatile-on-report-uae-is-considering-leaving-opec.html; Summer Said and Stephen Kalin, “Saudi Arabia and U.A.E. Clash Over Oil, Yemen as Rift Grows,” Wall Street Journal, March 3, 2023, https://www.wsj.com/articles/saudi-arabia-and-u-a-e-clash-over-oil-yemen-as-rift-grows-ff286ff9; Ruxandra Lordache, “No Current Plan for the UAE to Leave OPEC Oil Alliance, Sources Say,” CNBC, March 6, 2023, https://www.cnbc.com/2023/03/06/no-current-plan-for-the-uae-to-leave-opec-oil-alliance-sources-say.html; Nikolay Kozhanov and Karen E. Young, The Saudi-Emirati OPEC Rift Might Be Local, but the Core Dispute Is Global, Policy brief (Washington: Middle East Institute, July 13, 2021), https://www.mei.edu/publications/saudi-emirati-opec-rift-might-be-local-core-dispute-global; Anthony Di Paola and Javier Blas, “UAE Escalates OPEC Dispute as Tensions on Output Quotas Grow,” Bloomberg News, November 18, 2020, https://www.bloomberg.com/news/articles/2020-11-18/uae-escalates-opec-dispute-as-tensions-on-output-quotas-mount; Dania Saadi, Herman Wang, and Claudia Carpenter, “Seeds of OPEC+ Discord Planted by the UAE’s Oil Expansion Ambitions,” S&P Global Market Intelligence, July 4, 2021, https://www.spglobal.com/platts/en/market-insights/latest-news/oil/070421-seeds-of-opec-discord-planted-by-the-uaes-oil-expansion-ambitions.

[6] Simeon Kerr, Anjli Raval, and Derek Brower, “UAE-Saudi Brinkmanship Threatens Opec Unity as Oil Prices Soar,” Financial Times, July 6, 2021, https://www.ft.com/content/d0b77371-fdd3-4650-81e7-9b5e51f27bb9.

[7] Atef Suleiman, The Petroleum Experience of Abu Dhabi (Abu Dhabi: The Emirates Center for Strategic Studies and Research, 2007), 1.

[8] U.S. Energy Information Administration, Country Analysis Executive Summary: United Arab Emirates (Washington: May 6, 2020, 2). By contrast to Abu Dhabi’s plans to significantly increase production capacity from 4 million to 5 million barrels per day this decade, Dubai’s oil production peaked in 1991 at 410,000 barrels per day and had already more than halved by the end of the 1990s. It now stands at a trivial level. See Gerald Butt, “Oil and Gas in the UAE,” in Ibrahim al Abed and Peter Hellyer (eds.), United Arab Emirates: A New Perspective (London: Trident Press, 2001), 237. See also SPGlobal Platts Periodic Table of Oil: 5th edition, accessed April 17, 2023, https://www.spglobal.com/commodityinsights/plattscontent/_assets/_files/downloads/crude_grades_periodic_table/crude_grades_periodic_table.html.

[9] This is covered in detail in Jim Krane, Energy Kingdoms: Oil and Political Survival in the Persian Gulf (New York: Columbia University Press, 2019), 44-45.

[10] Butt, “Oil and Gas in the UAE,” 233.

[11] For an academic discussion, see A. F. Alhajji, “Why Do Some OPEC Members Cheat? The Case Of the United Arab Emirates,” Journal of Energy and Development 23, no. 1 (Autumn 1997): 59–69. https://www.jstor.org/stable/24808896.

[12] Reza Sanati, “OPEC and the International System: A Political History of Decisions and Behavior” (dissertation, Florida International University, 2014), 140, 295–299, https://digitalcommons.fiu.edu/etd/1149/.

[13] Khalid Alkhathlan, Dermot Gately, and Muhammad Javid, “Analysis of Saudi Arabia’s Behavior within OPEC and the World Oil Market,” Energy Policy 64 (2014): 209–25.

[14] Philipp Galkin, Tarek N Atalla, and Zhongyuan Ren, An Estimation of the Drivers Behind OPEC’s Quota Decisions (Riyadh: KAPSARC, July 2018).

[15] Depending on the price elasticity of global demand, Pierru, Smith, and Zamrik calculate that a 500,000 b/d increase in oil production (from OPEC spare capacity) provides oil importers with a collective reduction in oil prices of some $13 billion at a mid-range estimate of price elasticity of -0.3. Axel Pierru, James L. Smith, and Tamim Zamrik, “OPEC’s Impact on Oil Price Volatility: The Role of Spare Capacity,” Energy Journal 39, no. 2 (2018).

[16] Peter Volkmar, “Is OPEC Dead without Russia? Shedding Light on the Question Using Game Theory” (Houston, Rice University, 2019), https://bit.ly/3OBKWIW.

[17] Kristian Coates Ulrichsen, Mark Finley, and Jim Krane, The OPEC+ Phenomenon of Saudi-Russian Cooperation and Implications for US-Saudi Relations, research paper no. 10.18.22, Rice University’s Baker Institute for Public Policy, Houston, Texas, https://www.bakerinstitute.org/research/opec-phenomenon-saudi-russian-cooperation-and-implications-us-saudi-relations.

[18] Tensions between Dubai and Abu Dhabi over the sharing of power between emirate-level and federal authorities formed a near-constant backdrop to domestic politics in the UAE in its first decade and culminated in a threat in 1978 by the rulers of Dubai and Ras al-Khaimah to secede from the federation. See Tancred Bradshaw, The End of Empire in the Gulf: From Trucial States to United Arab Emirates (London: I.B. Tauris, 2020), 172.

[19] Rajiv Chandrasekaran, “In the UAE, the United States Has a Quiet, Potent Ally Nicknamed ‘Little Sparta’,” Washington Post, November 9, 2014.

[20] Vania Carvalho Pinto, “From ‘Follower’ to ‘Role Model:’ the Transformation to the UAE’s International Self-Image,” Journal of Arabian Studies 4, no. 2 (2014), 234.

[21] Hassan Hamdan Al-Alkim, The Foreign Policy of the United Arab Emirates (London: Saqi Books, 1989), 184.

[22] Neither Mohammed bin Rashid (in Dubai) nor Mohammed bin Zayed (in Abu Dhabi) was the immediate successor to his father; Mohammed bin Rashid served as crown prince of Dubai between 1990 and 2006, while Mohammed bin Zayed was crown prince of Abu Dhabi from 2004 to 2022. In practice, each came to direct and control most aspects of decision-making in their emirate for years before they formally became ruler.

[23] Jim Krane, Dubai: The Story of the World’s Fastest City (London: Atlantic Books, 2009), 181-82.

[24] Two of the 19 hijackers were UAE citizens. See: Robert Worth, “Mohammed bin Zayed’s Dark Vision of the Middle East’s Future,” New York Times, January 9, 2020.

[25] Ben Simpfendorfer, The New Silk Road: How a Rising Arab World is Turning Away from the West and Rediscovering China (New York: Palgrave Macmillan, 2009), 58.

[26] Ian Jackson, “Nuclear Energy and Proliferation Risks: Myths and Realities in the Persian Gulf,” International Affairs 85, no. 6 (2009): 1157; Kristian Coates Ulrichsen, The United Arab Emirates: Power, Politics and Policymaking (Abingdon: Routledge, 2016), 148.

[27] Quint Forgey, “‘The Dawn of a New Middle East’: Trump Celebrates Abraham Accords with White House Signing Ceremony,” Politico, September 15, 2020, https://www.politico.com/news/2020/09/15/trump-abraham-accords-palestinians-peace-deal-415083.

[28] Rory Miller, Desert Kingdoms to Global Powers: The Rise of the Arab Gulf (New Haven: Yale University Press, 2016), 8. Established in 1981, the GCC consists of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE.

[29] UAE-Saudi disputes include a standoff over the Buraimi oasis and its villages in the 1950s (before independence) that was a factor behind the creation of the Abu Dhabi Defense Force in the 1960s. Abu Dhabi’s then-ruler, Sheikh Shakhbhut bin Sultan Al Nahyan, “was adamant that he required an armed force of his own, predicating this need on the threat from Saudi Arabia.” Ash Rossiter, Security in the Gulf: Local Militaries before British Withdrawal (Cambridge: Cambridge University Press, 2020), 192. See also Michael Quentin Morton, Buraimi: The Struggle for Power, Influence and Oil in Arabia (London: I.B. Tauris, 2013), 95–109.

[30] Noura Saber Al-Mazrouei, The UAE and Saudi Arabia: Border Disputes and International Relations in the Gulf (London: I.B. Tauris, 2016), 147.

[31] “Saudi Arabia May Block Qatar-UAE Gas Pipeline,” Energy Intelligence, July 10, 2006. Saudi officials did prevent the northward extension of the Dolphin pipeline from Qatar to Kuwait on the grounds that it transited Saudi territorial waters.

[32] Simon Henderson, Map Wars: The UAE Reclaims Lost Territory from Saudi Arabia, The Washington Institute, January 19, 2006, https://www.washingtoninstitute.org/policy-analysis/map-wars-uae-reclaims-lost-territory-saudi-arabia; “Saudi and UAE Border in Dispute over ID Cards,” Reuters, August 23, 2009, https://www.reuters.com/article/idINIndia-41923020090823.

[33] Abdel Hai Mohamed, “Withdrawal from Single Currency ‘Final’,” Emirates 24/7, May 22, 2009, https://www.emirates247.com/eb247/economy/uae-economy/withdrawal-from-gcc-single-currency-final-2009-05-22-1.32862.

[34] Richard Spencer, “Naval Battle between UAE and Saudi Arabia Raises Fears for Gulf Security,” Daily Telegraph, March 26, 2010, https://www.telegraph.co.uk/news/worldnews/middleeast/unitedarabemirates/7521219/Naval-battle-between-UAE-and-Saudi-Arabia-raises-fears-for-Gulf-security.html.

[35] Kristian Coates Ulrichsen, Qatar and the Gulf Crisis (Oxford: Oxford University Press, 2020).

[36] Simon Henderson, “Meet the Two Princes Reshaping the Middle East,” Politico, June 13, 2017, https://www.politico.com/magazine/story/2017/06/13/saudi-arabia-middle-east-donald-trump-215254/; David Kirkpatrick, “The Most Powerful Arab Ruler Isn’t M.B.S. It’s M.B.Z.,” New York Times, June 2, 2019, https://www.nytimes.com/2019/06/02/world/middleeast/crown-prince-mohammed-bin-zayed.html.

[37] Elana DeLozier, UAE Drawdown May Isolate Saudi Arabia in Yemen, The Washington Institute, July 2, 2019, https://www.washingtoninstitute.org/policy-analysis/uae-drawdown-may-isolate-saudi-arabia-yemen; Eric Shawn, “UAE Said to be Holding Up Gulf Deal That Could End Qatar Blockade and Protect US Interests in Middle East,” Fox News, July 9, 2020, https://www.foxnews.com/world/uae-holding-up-gulf-deal-end-qatar-blockade-protect-us-interests; Simeon Kerr, “Trade Emerges as Latest Flashpoint in Deepening Saudi-UAE Rivalry,” Financial Times, July 13, 2021, https://www.ft.com/content/0cb64e0b-fcad-4992-beed-191261caa406.

[38] Andrew England, “Foreign Companies Pushed to Site Regional HQs in Saudi Arabia,” Financial Times, February 15, 2021, https://www.ft.com/content/b24df75c-b7ef-46ec-aad7-e3ed7b753328; Samer Al-Atrush, Simeon Kerr, and Andrew England, “Saudi Arabia Looks at Tax Relief for Multinationals Relocating HQs,” Financial Times, March 4, 2023, https://www.ft.com/content/e956333d-ea10-4b14-8c48-185570b0d057; Sean Mathews, “Saudi Arabia’s New Airline Will Shake up Gulf Competition,” Middle East Eye, April 6, 2023, https://www.middleeasteye.net/news/saudi-arabia-new-disruptive-airline-shakes-up-gulf.

[39] See OPEC, “Member Countries,” accessed April 17, 2023, https://www.opec.org/opec_web/en/about_us/25.htm.

[40] bp Statistical Review of World Energy, 2022.

[41] Kristian Coates Ulrichsen, “Why is Qatar Leaving OPEC?,” New York Times, December 10, 2018, https://www.nytimes.com/2018/12/10/opinion/qatar-leaving-opec-saudi-arabia-blockade-failure.html.

[42] Jim Krane, “Qatar to Saudi Arabia: We'd Rather Quit OPEC than Cut Ties with Iran or Close Al Jazeera,” Forbes, December 4, 2018, https://www.forbes.com/sites/thebakersinstitute/2018/12/04/qatar-to-saudi-arabia-we-would-rather-quit-opec-than-cut-relations-with-iran-or-shutter-al-jazeera.

[43] Ben Hubbard and Stanley Reed, “Qatar Says It Will Leave OPEC and Focus on Natural Gas,” New York Times, December 3, 2018, https://www.nytimes.com/2018/12/03/world/middleeast/qatar-withdraw-opec.html.

[44] Steven Wright, “Why Qatar Left OPEC,” Al Jazeera, December 6, 2018, https://www.aljazeera.com/opinions/2018/12/6/why-qatar-left-opec.

[45] bp Statistical Review of World Energy, 2022.

[46] Stanley Reed, “Oil Nations Again Fail to Reach Deal as U.A.E. Demands Higher Quota,” New York Times, July 5, 2021, https://www.nytimes.com/2021/07/05/business/opec-plus-oil-production-uae.html. For discussion of the agreement resolving the standoff, see OPEC press release “19th OPEC and non-OPEC Ministerial Meeting concludes” and accompanying “Table – Reference production,” July 18, 2021, https://www.opec.org/opec_web/en/press_room/6512.htm

[47] Coates Ulrichsen, Finley, and Krane, The OPEC+ Phenomenon of Saudi-Russian Cooperation.

[48] Summer Said and Dion Nissenbaum, “Before OPEC+ Production Cut, Saudis Heard Objections From a Top Ally, the U.A.E.,” Wall Street Journal, November 1, 2022, https://www.wsj.com/articles/before-opec-production-cut-saudis-heard-objections-from-a-top-ally-the-u-a-e-11667335415.

[49] Briefing in Houston attended by Krane and Ulrichsen on October 24, 2022, with a former State Department official, held under condition of anonymity.

[50] Kozhanov and Young, The Saudi-Emirati OPEC Rift Might Be Local, but the Core Dispute Is Global, https://www.mei.edu/publications/saudi-emirati-opec-rift-might-be-local-core-dispute-global.

[51] This is without considering changes in oil price that might occur from the additional oil supplied to the market; see the discussion in the following section.

[52] See World Bank, “Oil rents (% of GDP) - United Arab Emirates,” https://data.worldbank.org/indicator/NY.GDP.PETR.RT.ZS?locations=AE and World Bank, “Oil rents (% of GDP) – Saudi Arabia,” https://data.worldbank.org/indicator/NY.GDP.PETR.RT.ZS?locations=SA.

[53] Javier Blas, “Saudi Arabia Reveals Oil Output Is Near Its Ceiling,” Bloomberg, July 21, 2022, https://www.washingtonpost.com/business/energy/saudi-arabia-reveals-oil-output-is-near-its-ceiling/2022/07/20/eff7aff6-081b-11ed-80b6-43f2bfcc6662_story.html.

[54] Note however that energy sector officials in many of the Gulf states have expressed doubts about any near-term peak in global demand, and OPEC’s own long-term oil market outlook expects global demand to continue rising in the coming decades. See Alex Lawler, “OPEC raises long-term oil demand view, calls for investment,” Reuters, October 31, 2022, https://www.reuters.com/business/energy/opec-raises-long-term-oil-demand-view-calls-investment-2022-10-31/.

[55] One potential outcome of an increase in Saudi production capacity is a closer alignment of Saudi oil market strategy with preferences in the UAE. Also see the April 27 statement by OPEC Secretary General Haitham al Ghais as reported by Javier Blas, https://bit.ly/3MZRnnZ.

[56] Jim Krane, “The ‘Carbon Neutral Petro-State:’ An Oxymoron? The UAE Thinks Not,” Forbes, October 11, 2021, https://www.forbes.com/sites/thebakersinstitute/2021/10/11/the-carbon-neutral-petro-state-an-oxymoron-the-uae-thinks-not/.

[57] For more on the origins of the villainous portrayal of OPEC in the United States, see: Joshua A. Merritt, “Using OPEC as a Villain in Narratives,” Working Paper (Corvallis: Oregon State University, 2016), https://ir.library.oregonstate.edu/concern/graduate_projects/nc580p048.

[58] This is covered in detail in Krane, Energy Kingdoms, 40–51.

[59] Ben Hubbard, “Saudi Arabia and U.S. Trade Accusations over Oil Cuts,” New York Times, October 13, 2022, https://www.nytimes.com/2022/10/13/world/middleeast/us-saudi-oil-production.html.

[60] Quoted in Emile Hokayem, “Fraught Relations: Saudi Ambitions and American Anger,” Survival 64, no. 6 (2023): 7-8.

[61] Said and Nissenbaum, “Before OPEC+ Production Cut, Saudis Heard Objections From a Top Ally, the U.A.E.”.; Said and Kalin, “Saudi Arabia and U.A.E. Clash Over Oil, Yemen as Rift Grows.”

[62] Sam Fleming et al., “West Presses UAE to Clamp Down on Suspected Russia Sanctions Busting,” Financial Times, March 1, 2023, https://www.ft.com/content/fca1878e-9198-4500-b888-24b17043c507; John Hudson, Ellen Nakashima, and Liz Sly, “Buildup Resumed at Suspected Chinese Military Site in UAE, Leak Says,” Washington Post, April 26, 2023, https://www.washingtonpost.com/national-security/2023/04/26/chinese-military-base-uae/.

[63] “OPEC, Russia draft cooperation charter offers no formal body: document,” Reuters, February 11, 2019, https://www.reuters.com/article/us-oil-opec-russia/opec-russia-draft-cooperation-charter-offers-no-formal-body-document-idUSKCN1Q01I9.

[64] Indonesia was an OPEC member between 1962 and 2008, but rejoined and then re-quit in 2016. Ecuador held membership from 1973-1992 and rejoined in 2007, but left again in 2020. Gabon was a member from 1975-1995, rejoined in 2016, and is still a member at the time of writing.

[65] These issues were previously explored in Jim Krane, “Does Saudi Arabia Need OPEC?,” scholarly paper (Washington: The Arab Gulf States Institute in Washington, November 2019), https://agsiw.org/wp-content/uploads/2019/11/Jim-Krane_Saudi-OPEC_ONLINE-1.pdf.

[66] US Energy Information Administration, Short-Term Energy Outlook, Government report (Washington: U.S. Energy Information Administration, August 2018).

[67] See for example, the annual Symposium on Energy Outlooks, jointly hosted by OPEC, the IEA, and the International Energy Forum. https://bit.ly/3IEd7TS.

[68] See Bob McNally, Crude Volatility: The History and the Future of Boom-Bust Oil Prices (New York: Columbia University Press, 2017).

[69] See Clifford Krauss, “Oil Nations, Prodded by Trump, Reach Deal to Slash Production,” New York Times, April 12, 2020, https://www.nytimes.com/2020/04/12/business/energy-environment/opec-russia-saudi-arabia-oil-coronavirus.html.

[70] While spare capacity is frequently a result of production restraint, in Saudi Arabia there is also a more strategic component: The kingdom has long maintained a buffer of spare production capacity beyond its normal market/production aspirations as a security cushion, analogous to the strategic oil stockpiles held by the United States and other consuming countries.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.