When enough start-up firms are formed, active, and headed toward success in an urban area, they can support a community of other entrepreneurship ecosystem organizations around them. These other ecosystem organizations can, in turn, support the creation of yet more new start-ups. When this happens an entrepreneurship ecosystem has reached “critical mass” and achieved a “virtuous cycle.”

Venture capitalists are a prominent and important component of an entrepreneurship ecosystem. Venture capitalists invest in high-growth, high- technology start-up firms at a critical stage of their development. The quantity of venture capital invested is therefore an important measure of the health of an entrepreneurship ecosystem. In this issue brief, we use the total venture capital investment in start-up companies that received a round of financing within the past 10 years1 to ask the question: What is the state of entrepreneurship in Texas and what will it look like in the future?

Texas Compared With Other States

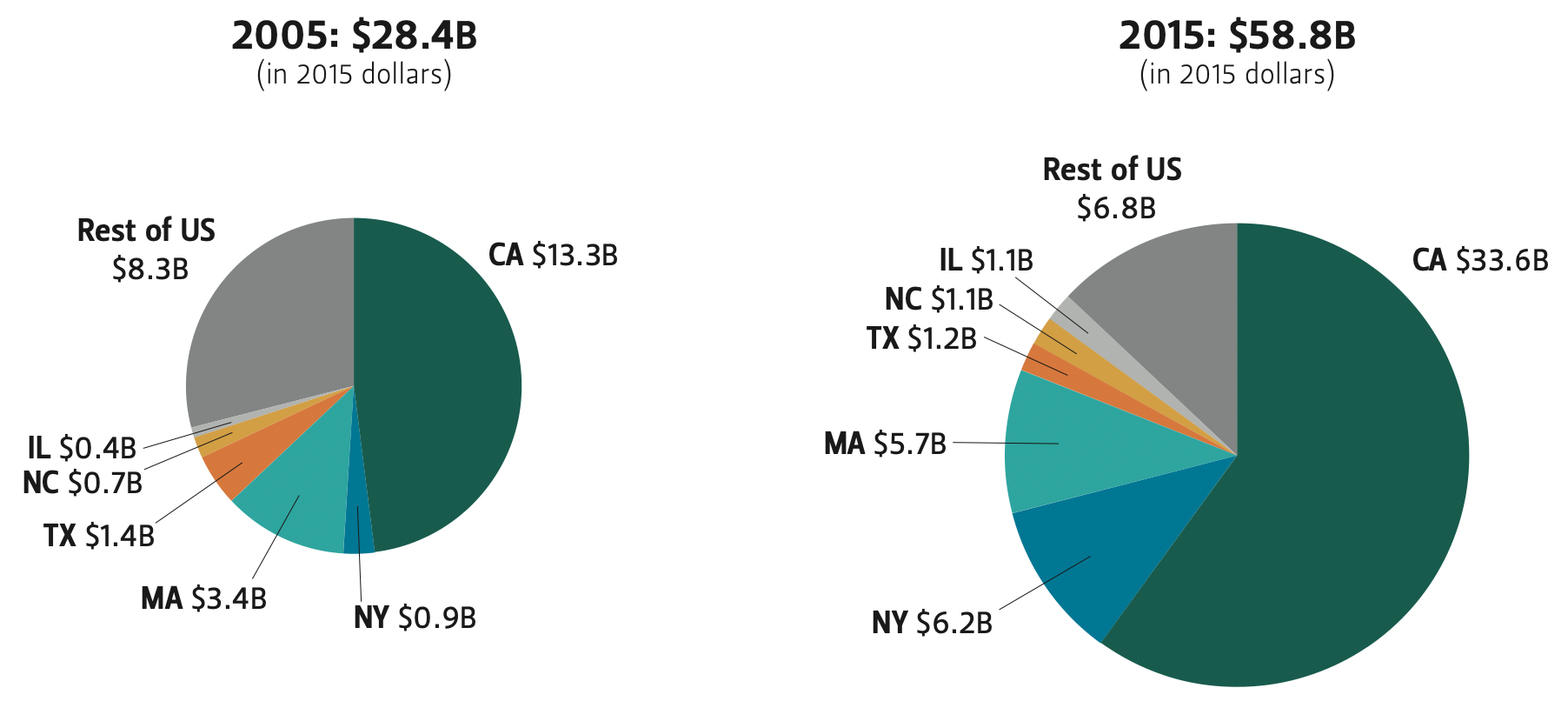

Just a decade ago, Texas’ venture capital investment was the third largest in the United States.2 Today, it has fallen to fourth and is set to slide to sixth, likely even before 2016 is out. If current trends continue, Texas, the second-largest state in the U.S. in terms of gross domestic product (GDP), will be struggling to remain in the top 10 for venture capital investment within the next decade.

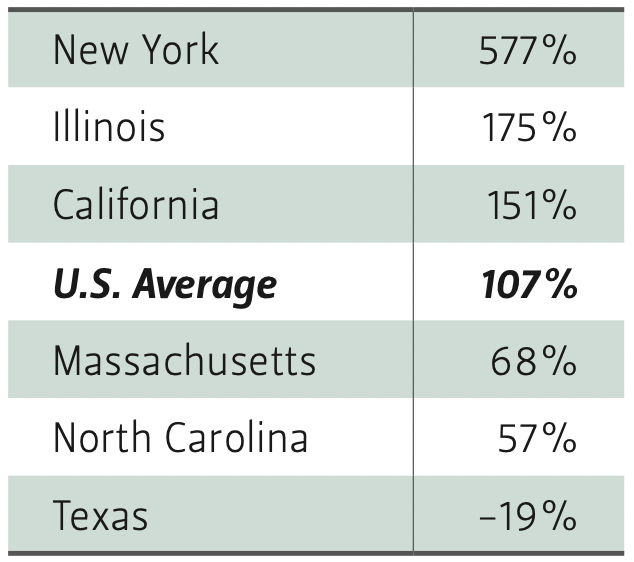

The reason for Texas’ relative decline is simple: while other high-ranking states are growing their venture capital investment at extremely fast rates, Texas’ venture capital investment has decreased 19% over the past 10 years in real terms.3 Of the top 10 states by venture capital investment, only Texas and New Jersey have shrunk. New Jersey has seen its money, talent, and returns flow across the border to its powerhouse neighbor; New York has grown its venture capital investment by 577% since 2005, and is now the second-largest jurisdiction for venture capital.

Figure 1 — Venture Capital Investments in the U.S. Grew by More Than 100% From 2005 to 2015

Across the United States, the average real growth rate of venture investment is 107% over the last decade. California has posted a growth rate of above 150% for the 10-year period, and has also increased its total share of venture capital investment to more than the rest of the country combined. Most of California’s venture capital is invested in Palo Alto, generally known as Silicon Valley. Massachusetts’ 68% growth in a decade is strong, and would likely have been enough to hold its world-class second-place title were it not for New York’s ability to bring its enormous financial resources to bear on its entrepreneurial economy. Historically, Massachusetts’ entrepreneurship was found along the western side of Route 128, the “Technology Highway” that circles Boston. However, the last decade saw the Technology Highway supplanted by a Boston/Cambridge ecosystem. Kendall Square, Cambridge, which abuts the MIT campus, is one focal point of this newer entrepreneurship community.

Texas also faces pressure from below. North Carolina, while officially fifth, is now neck-and-neck with Texas. North Carolina has had a virtuous entrepreneurship cycle in its Research Triangle since the turn of the century, and shows no sign of slowing down. Illinois, currently sixth, is a different kind of success story. As recently as seven years ago, Illinois’ entrepreneurship ecosystem wasn’t thriving. Then Chicago found a catalyst and now has a vibrant technology community that is churning out digital start-ups.4 As a consequence, Illinois’ venture capital industry has grown nearly 200% in the last 10 years. Today, just $51 million in investment (which doesn’t buy a decent biotech venture) separates Texas from sixth place. And Texas posted a meager $186 million of investment in the fourth quarter of 2015—a three-year low.

Texas’ Three Urban Centers

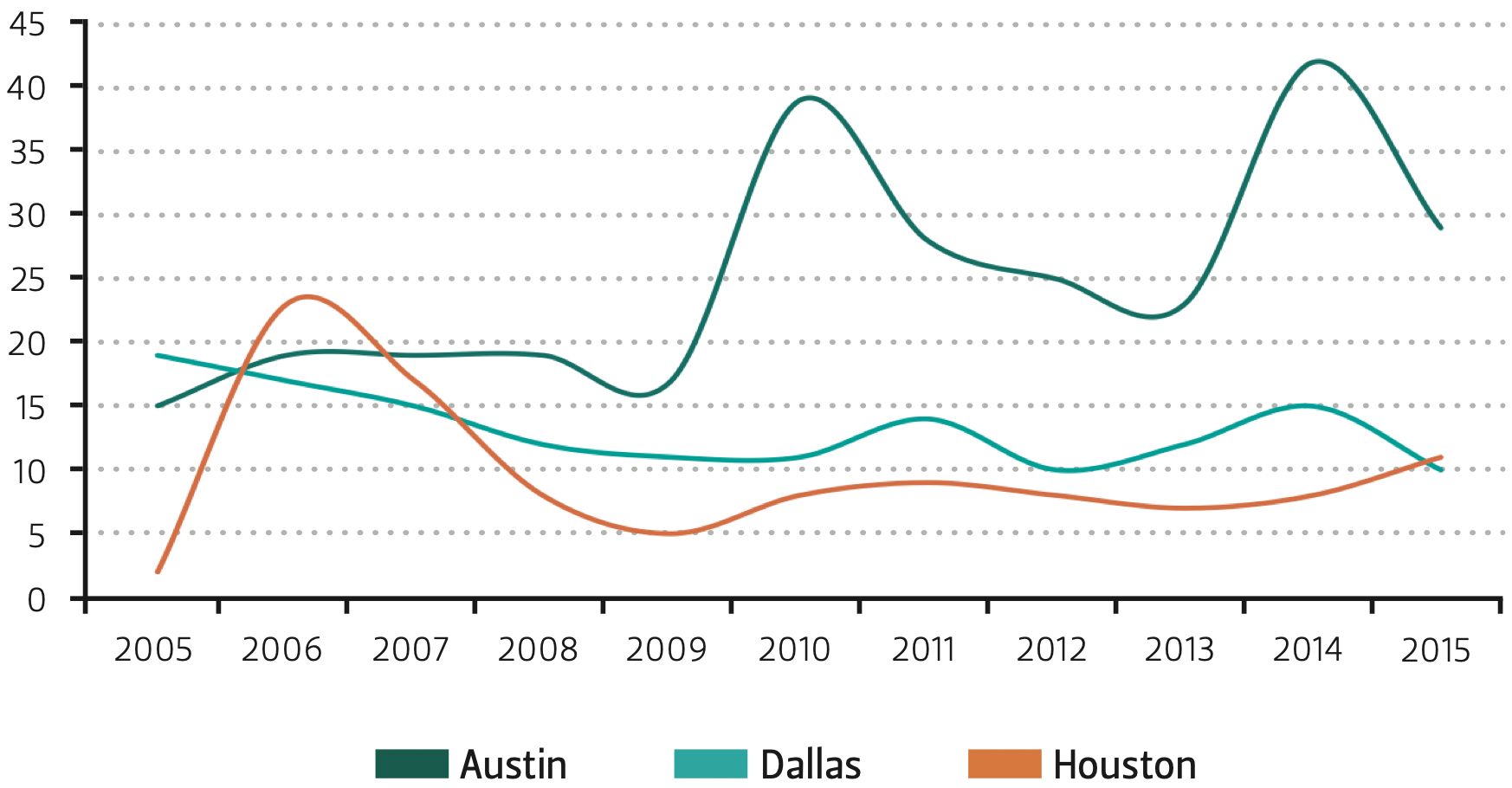

Figure 2 — Newly Financed Start-ups in Major Texas Cities

Entrepreneurship ecosystems are an urban phenomenon. An entrepreneurship ecosystem needs what economists call “agglomeration” to reach critical mass: start- ups and other ecosystem organizations all need to be in close proximity. It is therefore unsurprising that almost all of Texas’ venture capital investment occurs in the state’s three largest metropolitan areas: Houston, Dallas, and Austin. In the past decade, only one city—Austin—has probably achieved a virtuous cycle. Although it still has its swings from quarter to quarter, Austin now appears to be sustainably producing entrepreneurial investment and growth.

Austin, Dallas, and Houston all had similar numbers of start-up companies receiving their first round investments in 2006. However, by 2009 Austin was building momentum, and now sees between 30 and 40 new companies financed each year, while both Houston and Dallas have flatlined.

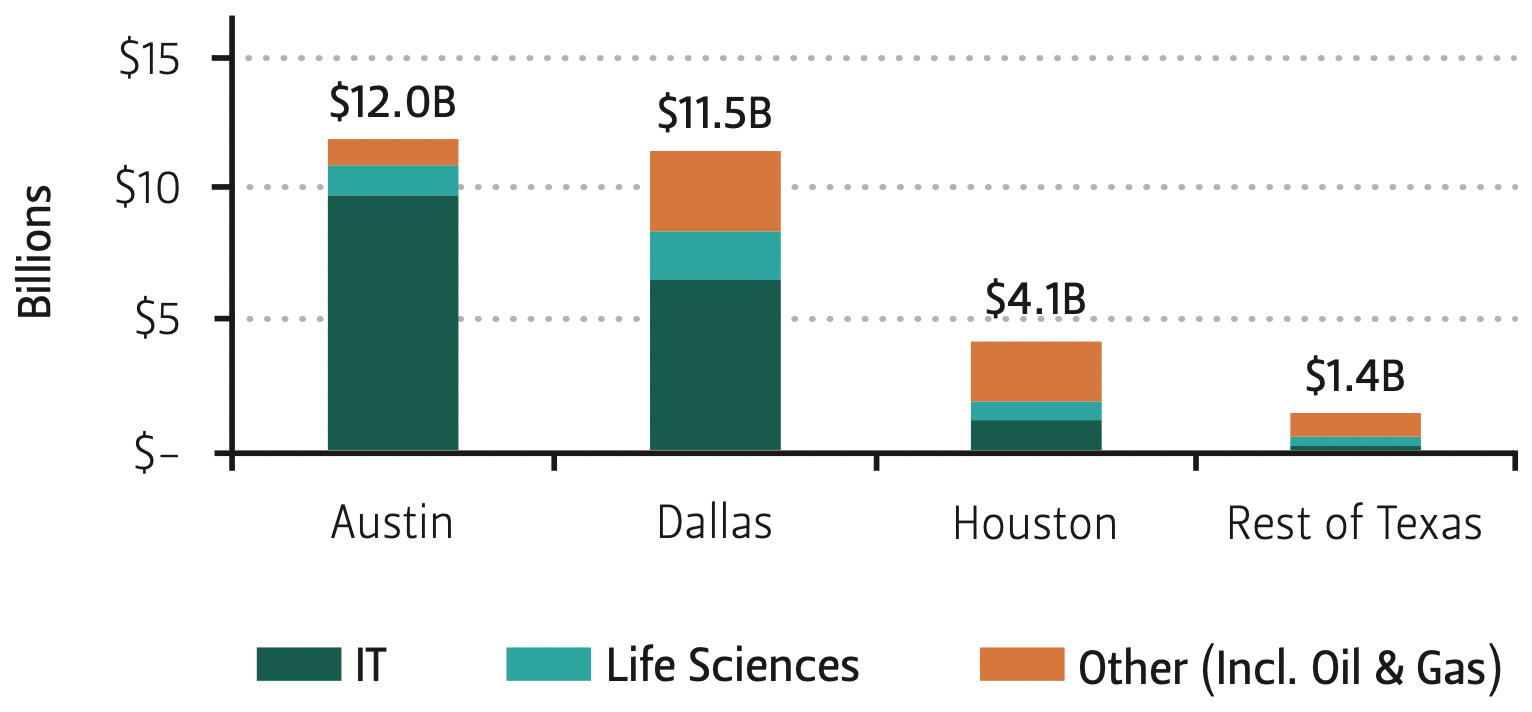

Figure 3 — Total Venture Capital Invested Into Texas Start-ups in the Last Decade

Outside of Houston, Dallas, and Austin, start-ups in Texas received just $1.4 billion in venture capital in the last 10 years. Nearly half of this came from San Antonio, which developed some life science companies next to its highly ranked medical center.5 The remainder came (almost exclusively) from investments in oil and gas companies scattered throughout the state.

Austin

Austin’s venture industry composition is fairly typical of a balanced start-up community, although perhaps overly dominated by information communication technology (ICT) and underrepresented in the life sciences. With $12 billion invested and a GDP less than 25% of either Houston or Dallas,6 Austin’s vibrant start-up community attracts the most venture capital investment in the state. Adjusted for GDP, Austin has investment levels five times that of Dallas and 10 times that of Houston. Although nothing in entrepreneurship is certain, Austin certainly appears to be at critical mass.

Dallas

Table 1 — 10-Year Growth Rates for Six Top Venture Capital States

Dallas outperformed Houston in total venture capital investments by over $7 billion since 2005.7 Dallas has had the strongest communications and media presence of all the Texas metro areas,8 as well as more medical and biotechnology investment than both Houston and Austin combined. However, it has had only a small amount of semiconductor investment—approximately one-third that of Austin. This is surprising, as Dallas is home to Texas Instruments, one of the world’s largest semiconductor firms.9

Given its economic size, Dallas’ total venture capital investment is anemic. Over the last decade, Dallas has declined from about 20 start-up companies receiving venture capital investment per year to around 10. This is not evidence of a virtuous cycle.

Houston

With just $4.1 billion invested in start-up companies that have received a round of funding since 2006, Houston has seen less venture capital in 10 years than New York City now sees in one.

Despite having the Texas Medical Center (TMC)—the largest medical center in the world with over 100,000 employees and 7,000 patient beds—Houston has seen a meager 26 life science companies funded in the past decade. These 26 companies raised a combined total of less than $800 million. In comparison, the Boston/Cambridge life science sector has between 20 and 40 deals bringing in as much as $1 billion each quarter: What Houston and the TMC have taken 10 years to accomplish, a thriving entrepreneurship ecosystem can accomplish every couple of months. There is only a single mature mid-size venture capital fund, Mercury Fund, with a focus on the life sciences active in Houston today.10

Information communication technology firms are the heart of a good entrepreneurship ecosystem. In most cities, ICT start-ups account for between one-half and two-thirds of venture investment. Over the last decade, an average of six ICT start- up companies a year have received small to moderate amounts of venture financing in Houston, and this average masks an underlying declining trend.

Although this might seem bleak, the worst has likely already happened. In 2013 four ICT start-ups received venture capital for the first time, in 2014 this number rose to five, and in 2015 there were six receiving a total of around $20 million. Houston does also have a mid-size venture fund to anchor the sector.11 Nevertheless, Houston remains a far cry from Austin, which saw 22 new ICT start-ups receive $93 million in 2015.

Energy Ventures

Texas, and particularly Houston, is about oil. The energy sector accounts for approximately one-third of Houston’s GDP, 20% of salary income, and 10% of employment.12 It is therefore unsurprising that Houston and Dallas are the nation’s capitals for oil and gas ventures.13 However, traditional venture capitalists don’t invest in this sector.14 Although they do invest in adjacent sectors like green energy, new chemicals, and advanced materials, there seem to be little, if any, spillovers from oil and gas ventures into the rest of the entrepreneurial economy.

Texas can’t rely on energy entrepreneurship. Texas’ investment in oil and gas ventures simply isn’t a lot when compared to venture investment in other sectors elsewhere. And right now the prognosis not does look good for energy entrepreneurship: the price of oil has recently dipped below $30 per barrel (for West Texas Intermediate), and Houston’s energy-specific Surge Ventures’ accelerator15 shut down its fourth cohort in the last quarter of 2015.

Conclusion

The condition of the venture capital industry provides a good indication of the state of an entrepreneurship ecosystem. In Texas, entrepreneurship should be strengthening the economic power and stability of the state. An examination of Texas’ venture capital industry strongly suggests that this isn’t the case. Adjusting for inflation, the Texan venture capital industry is 19% smaller than a decade ago, while U.S. venture capital investment has grown by an average 107%.

Texas is a multi-centered state, but three of its four centers are drastically underperforming in entrepreneurship in comparison to other major cities. Austin has seen an impressive 170% growth16 in its entrepreneurship ecosystem over the past decade. It has outpaced even the quickly rising national tide. San Antonio may have the seed for future life science and IT clusters, but at present it is a micro- ecosystem at best. Houston and Dallas, two of the largest metropolitan economies in the nation, each have a figurative pint of entrepreneurship in their 10-gallon hats.

If current trends hold over the next decade, Austin’s entrepreneurship ecosystem will prosper, San Antonio’s may find traction, and both Dallas’ and Houston’s will fail. There is, however, a reason for hope: Both Houston and Dallas have the human and financial capital needed to build a great ecosystem. Texas urgently needs to find a catalyst for change if it is to remain at least a top 10 venture capital state.

Endnotes

1. The primary data used in this report comes from Thomson Reuters Corporation’s VentureXpert database. This data is drawn at the portfolio company level. In order to be included in the sample, a start-up company must have received at least one round of venture financing between 2006 and 2015. However, we record each start-up company’s total venture capital investment to date. As a consequence, venture capital investment made prior to 2006 is included provided that the recipient start-up received additional investment in the last decade.

2. State-level and national data in this report is taken from www.PWCMoneyTree.com. The PWCMoneyTree data is endorsed by the National Venture Capital Association and is an “official" aggregation of the Thomson Reuter Corporation’s VentureXpert data.

3. Inflation data from the U.S. Bureau of Labor Statistics: www.bls.gov/data/inflation_calculator.htm.

4. See Built in Chicago, www.builtinchicago.org/2016/01/19/2015-chicago-startup-report.

5. Six San Antonio universities and research institutions received a combined $95 million in NIH funding in 2015.

6. Gross Domestic Product (GDP) data is from the U.S. Bureau of Economic Analysis: http://www.bea.gov/newsreleases/regional/gdp_metro/gdp_metro_newsrelease.htm.

7. This is partly due to a number of older start-up companies still receiving late-stage funding in Dallas.

8. Communication and media companies in Dallas received approximately 23% of the city’s total investment, with over $2.6 billion in investment across 33 companies that received financing from 2005 to 2015. Comparatively, Austin’s communication and media sector saw only $550 million in investment in the same period.

9. IHS Technology, “Preliminary Worldwide Ranking of the Top 20 Suppliers of Semiconductors in 2014,” Dec. 22, 2014, http://press.ihs.com/press-release/technology/global-semiconductor-market-set-strongest-growth-four-years-2014.

10. Mercury Fund has a dual focus on life science and software. A new life science fund, Houston Health Ventures (HHV), made its first investment in December 2015. HHV’s capital under management is unknown. Another life sciences fund, Essex Woodlands Health Ventures, was established in Houston in 1985 and still has a presence in Houston, but has since relocated its headquarters to Palo Alto, California. Essex Woodlands has made over 150 investments and has raised more than $2.5 billion since its inception.

11. Mercury Fund invests as a lead investor in early stage software start-ups. Having a local lead investor is crucial. Without one, it can become impossible to attract outside capital. Venture capitalists syndicate their investments. Because venture capitalists need to resolve information problems, the “lead investor” is nearly always local and specializes in the portfolio company’s area.

12. Greater Houston Partnership, “The Economy at a Glance” 25, no. 1 (January 2016), http://www.houston.org/pdf/research/quickview/Economy_at_a_Glance.pdf.

13. Oil and gas venture capital investments recorded in VentureXpert were all made by specialist energy funds. There are six of these funds that remain active today, ranging from Chevron Technology Ventures, with more than $300 million under management, to Small Ventures USA, with just over $2m under management. Although these funds are small to mid-sized, their investments appear closer to private equity than true venture capital.

14. Venture capitalists invest in high-growth start-up firms that have comparatively few fixed assets and so are unable to raise debt financing. Oil and gas companies can be high-growth but they usually depend on large scale infrastructure that they can use as collateral.

15. An accelerator is a “fixed-term, cohort-based program, including mentorship and educational components, that culminates in a public pitch event, often referred to as ‘demo-day’.” See Daniel C. Fehder and Yael V. Hochberg, “Accelerators and the regional supply of venture capital investment,” 2014. Available at SSRN.org.

16. Austin’s growth over the 10-year period was calculated using a linear regression on the number of companies receiving first investment.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.