One of the most important and counter-intuitive ideas in financial regulation is that more regulation is not always better. While some degree of regulation can help improve financial stability, complex and overlapping regulations can actually cause banks to increase their risk-taking activities.

U.S. bank regulators have recently proposed two reforms related to the issue of complexity. First, the Board of Governors of the Federal Reserve System (the Fed) has introduced a proposal that would simplify bank capital regulations.1 Second, the Fed and the Office of the Comptroller of the Currency (OCC) have proposed reducing the capital requirement for large banks known as the Enhanced Supplementary Leverage Ratio (eSLR), which would push the financial regulatory system toward greater complexity.2

This issue brief summarizes the debate over regulatory complexity, outlines the current proposals from the Fed and the OCC, and recommends reforms to help improve financial stability.

Regulatory Complexity

Banks in the United States are subject to a wide variety of regulations, the scope and scale of which have drastically increased since the 2008 financial crisis.3 While some regulations may be effective at reducing bank risk, complex regulations can actually increase risk in several ways. For instance, overlapping rules can push banks to take risks that were not expected by the regulators. Complexity also creates loopholes that allow banks to take even greater risks. Finally, if regulators do not properly understand the riskiness of different assets, they can unintentionally encourage risky investments.

The dozens of capital and liquidity standards required of U.S. banks are often overlapping, or even contradictory.4 For example, suppose a bank holds mostly moderately risky assets such as real estate loans, but it can earn the same rate of return by holding some combination of very safe (e.g., U.S. Treasury bonds) and very risky assets, like mortgage-backed securities (MBSs). U.S. capital regulations encourage banks to hold fewer risky assets—like MBSs—and more moderate-risk real estate loans. Liquidity ratios, on the other hand, require banks to hold safe, liquid assets like Treasury bonds, which means that banks must also hold risky MBSs in order to earn the same overall rate of return. It is unclear whether these conflicting regulations will cause banks to increase or decrease their holdings of risky assets.5

Complex regulations are also easier to manipulate for bankers looking to avoid such restrictions. As an analogy, consider the complexity of the tax code. Most people agree a simple tax code would be better for everyone. We might allow small deductions to benefit certain groups, such as charities or new home owners, but too many deductions could allow people with high incomes to avoid large portions of their tax burdens. Similarly, a complex regulatory system allows banks to avoid the rules that might restrict their risk-taking activities. Reducing regulatory complexity can help eliminate loopholes and stabilize the financial system.

One example of regulatory complexity is the system of risk-based capital (RBC) regulations used by U.S. banking regulators. In the RBC system, regulators assign a rating to each class of bank assets based on its perceived level of risk. For example, cash and U.S. Treasury bonds are considered completely safe, while high-yield junk bonds are considered very risky, with residential real estate loans falling in the middle range. The RBC formula determines the bank’s required level of equity capital based on the riskiness of its asset holdings, with more capital required for high-risk assets and less capital for safer assets.

The RBC ratio is described by regulators as an improvement over the simple leverage capital ratio, calculated as the bank’s equity divided by its total assets. Regulators argue that the RBC ratio is more effective because it accounts for the riskiness of different bank assets. This can be problematic, however, when regulators misjudge the risk of particular assets. In the 1990s and early 2000s, for example, MBSs were thought to be very low-risk assets and were therefore assigned the lowest risk ratings in the RBC formula. This encouraged banks to buy MBSs and promoted the massive buildup of MBS holdings in the banking system, which played a major contributing role in the financial crisis.6

Flaws in the RBC formula encourage banks to invest in assets that are rated incorrectly by the regulators, which can simultaneously decrease their required levels of capital while increasing their levels of risk.7 It is therefore unclear from theory alone whether complex regulations will increase or decrease risk.8 We must turn to studies of the U.S. banking system to see if RBC regulations are, in practice, more effective than simple capital rules.

While a few early studies favored RBC ratios,9 more recent studies find that complex RBC regulations are not effective predictors of risk. In 2012, Andrew Haldane, now chief economist at the Bank of England, gave a controversial presentation at the Federal Reserve Bank of Kansas City’s annual conference in Jackson Hole, Wyoming, in which he provided evidence that simple capital ratios were better than RBC ratios at predicting the failures of major international banks during the financial crisis.10 These results were corroborated for U.S. banks by researchers from the World Bank and the International Monetary Fund,11 as well as by economists from New York University, including Nobel Laureate Robert Engle.12 My own (co-authored) research similarly finds that simple capital ratios are better than RBC ratios as predictors of a variety of indicators of bank risk and performance.13

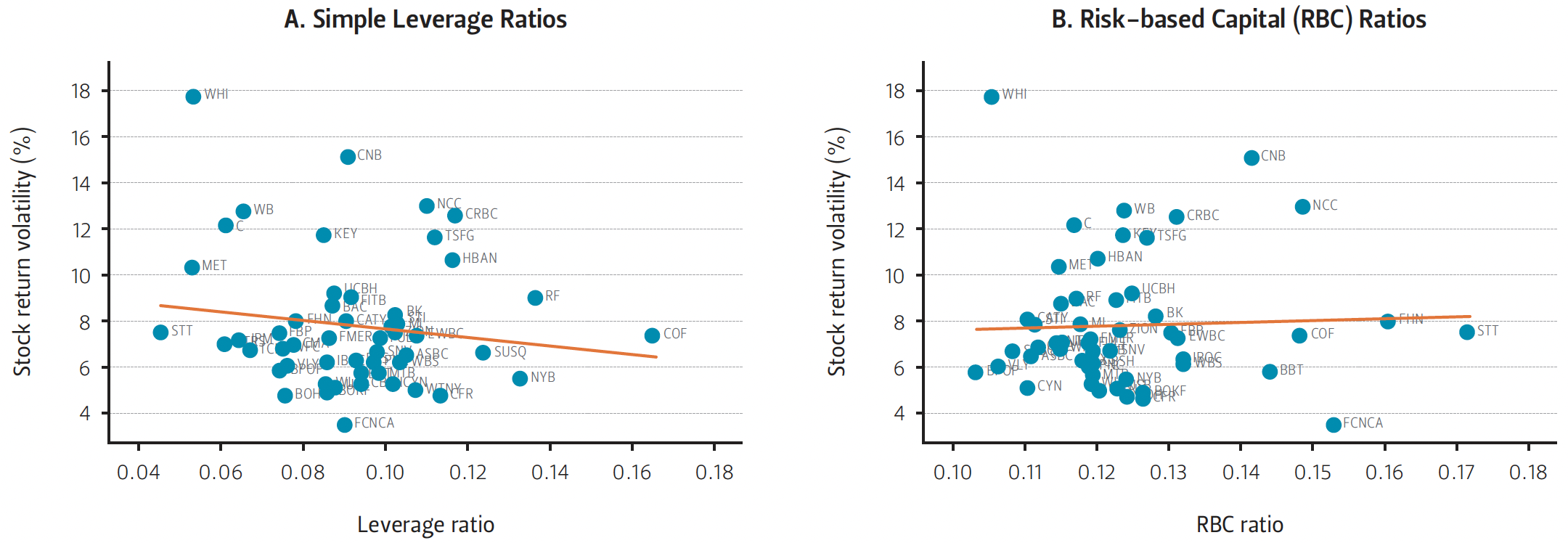

As an example, Figures 1A and 1B compare the risk level and capital ratios of U.S. bank holding companies with total assets of $10 billion or more as of September 30, 2008, the peak of the financial crisis.14 On the x-axes, Figure 1A shows each bank’s leverage capital ratio, and Figure 1B shows each bank’s RBC ratio. The y-axes show the standard deviation of each bank’s stock returns—a common indicator of risk—over the following quarter.

The solid orange lines in each figure estimate the average change in risk as capital increases. We see in Figure 1A that the line slopes downward, indicating (as expected) that higher-leverage capital ratios are associated with lower bank risk. In Figure 1B, however, the solid orange line slopes slightly upward, indicating that banks with higher RBC ratios tended to have higher risk as measured by the volatility of their stock returns. Figure 1 illustrates the general finding of the academic literature, that simple capital ratios are effective indicators of bank risk, while regulators’ complex RBC ratios are not.

Figure 1 — Stock Return Volatility Among Bank Holding Companies With Over $10 Billion in Total Assets (Q4 of 2008)

Some financial regulators have come to understand the dangers of regulatory complexity. Thomas Hoenig, former vice chairman of the Federal Deposit Insurance Corporation (FDIC), has long been a critic of regulatory complexity, and of RBC regulation in particular.15 More recently, two former chairs of the FDIC have also spoken out on the advantages of simple capital ratios. As Sheila Bair described, “Because their judgments about risk had been so wrong, regulators after the financial crisis have made greater use of capital standards that don’t rely on government risk assumptions.”16 Martin Gruenberg concurred that “Strengthening leverage capital requirements … was among the most important post-crisis reforms.”17

Recent legislative proposals have also favored simple capital ratios over complex RBC regulations. Bills that passed the House18 and Senate19—sponsored by Representative Jeb Hensarling (R-TX) and Senator Mike Crapo (R-ID) respectively—would allow banks with less than $10 billion in total assets to be exempted from many restrictions and reporting requirements, so long as they maintain sufficiently high levels of capital. The intent of these bills is to provide regulatory relief for well-capitalized community banks, but the emphasis on leverage ratios rather than RBC ratios has the added benefit of avoiding the negative incentives created by regulatory complexity, which—as detailed above—can encourage banks to increase their risk-taking activities.

Proposed Rule Changes

The Fed and the OCC have recently proposed two changes to the capital rules that apply to large banking institutions. Although the reforms affect only small portions of the vast framework of banking regulations, both address banks’ capital requirements, which are the most fundamental form of banking regulation. In addition, they provide perspective regarding regulators’ understanding of regulations and potential future plans.

First, the Fed has proposed to simplify capital regulations by combining two existing standards. Banks currently are assigned a minimum level of capital that must be maintained on a year-round basis, but once per year they also face a stress test known as the Comprehensive Capital Analysis and Review (CCAR), which estimates their required levels of capital during an economic downturn. The new proposal would combine these capital requirements into a single year-round standard based on each bank’s performance in the annual stress test. The new “stress buffer” would replace a portion of the current requirements known as the “capital conservation buffer.” The stress buffer would modestly increase required levels of capital since it would be set at greater than or equal to the capital conservation buffer, which is 2.5 percent of risk-weighted assets. This change would decrease regulatory complexity by reducing the number of capital requirements applied to banks from 24 to 14.

Second, the Fed and the OCC have proposed tailoring the eSLR to banks of different risk profiles. The eSLR is equal to the supplementary leverage ratio (SLR), currently set at 3 percent of “total leverage exposure” (total assets plus off-balance-sheet exposures) for banks with assets of $700 billion or more, plus an “enhancement” of 2 percent for global systemically important banks (GSIBs). Rather than apply the standard enhancement of 2 percent to all GSIBs, the Fed and the OCC have proposed the rate be set at half of each GSIB’s RBC capital surcharge as set by the Office of Financial Stability, which ranges from 1 percent to 3.5 percent based on a five-factor risk analysis. Similar changes are to be applied to the requirements for total loss-absorbing capital (TLAC).

This proposal is worrisome for two reasons. The main criticism of the eSLR modification proposal is that it will increase bank risk by reducing required levels of capital. The Fed and the OCC estimate a modest reduction of $400 million in GSIBs’ total capital requirements that, they argue, could spur bank lending. The FDIC, on the other hand, estimates a capital decrease of $121 billion, which could have substantial effects on bank risk.

Contrary to the Fed and the OCC’s claims, most academic research on optimal capital ratios finds that higher capital requirements would help stabilize the financial system with few adverse effects on lending. Some studies find that higher capital requirements since the financial crisis are associated with lower bank lending, but it is difficult to know if such effects were caused specifically by capital requirements or by other regulations, such as restrictions on mortgage lending. Studies that compare the costs of lower lending to the benefits of increased stability often find that capital should optimally be much higher than the current levels, possibly in the range of 15 to 20 percent of total assets, rather than the current average of about 11 percent.20

Second—but equally as important—the intent of lowering the eSLR is that the RBC ratio rather than a leverage ratio would become main determinant of bank behavior.21 For example, Randal Quarles, vice chairman for supervision at the Fed, recently testified before the U.S. Senate Committee on Banking, Housing, and Urban Affairs that simple leverage requirements can encourage banks to take excessive risks.22 As a banker constrained by a leverage ratio, he argued, “You will bear the same capital cost if you take on a very risky asset versus if you take on a less risky asset.” While Quarles is correct that simple leverage ratios assign equal weights to assets of different risk levels, he overlooks the fact that an incorrectly specified RBC rule can actually put less weight on risky assets, as was the case with MBSs prior to the financial crisis.

As previously discussed, academic research does not support Quarles’ argument for RBC ratios over simple capital ratios. The Fed’s proposal cites a study by researchers at the Federal Reserve Bank of New York arguing for the complementarity of RBC and simple capital ratios.23 That study, however, finds that “the risk-weighted ratio does not consistently outperform the simpler ratios, particularly with short horizons of less than two years”24 and that “in a short time horizon, risk weighting can overstate differences in asset return variances and hence reduce the accuracy of the risk-weighted ratio as a measure of capital adequacy.”25 This evidence is consistent with other recent studies finding that simple capital ratios are better than RBC ratios as predictors of bank risk.

Recommendations

Given the evidence on the negative consequences of regulatory complexity, the following actions by the Fed and the OCC could help improve U.S. financial regulations and reduce the probability of another financial crisis:

1. The Fed should adopt its proposal to simplify bank capital regulations by integrating its stress-testing program with its regulatory capital rules. It should consider further ways to reduce regulatory complexity in order to minimize risk in the banking system.

2. The Fed and the OCC should abandon their proposed modifications to the eSLR and instead make greater use of simple leverage ratios as binding constraints on bank capital.

3. Future proposals should consider raising—not lowering—bank capital requirements, since higher levels of capital are likely to improve financial stability with only minor effects on bank lending.

Endnotes

1. Federal Reserve System, “Amendments to the Regulatory Capital, Capital Plan, and Stress Test Rules,” Federal Register 83, no. 80 (April 25, 2018): 18160–88.

2. Department of the Treasury Office of the Comptroller of the Currency and Federal Reserve System, “Regulatory Capital Rules: Regulatory Capital, Enhanced Supplementary Leverage Ratio Standards for U.S. Global Systemically Important Bank Holding Companies and Certain of Their Subsidiary Insured Depository Institutions; Total Loss-Absorbing Capacity Requirements for U.S. Global Systemically Important Bank Holding Companies,” Federal Register 83, no. 76 (April 19, 2018): 17317–27.

3. A report from the U.S. Treasury describes the Dodd-Frank Act as “the most comprehensive set of reforms to our financial system since the Great Depression.” See The Dodd-Frank Act: Reforming Wall Street and Protecting Main Street (Washington, D.C.: U.S. Department of the Treasury, 2017).

4. For a mathematical example, see Andrew G. Haldane, “Multi-Polar Regulation,” International Journal of Central Banking 11, no. 3 (2015): 385–401.

5. As Haldane (2015) describes, “Since the crisis, regulation has become multi-polar. But the impact of this regime shift on analytical models and real-world behavior remains largely uncharted territory” (397).

6. As Senator Elizabeth Warren (D-MA) recently noted, “regulators treated dangerous mortgage-backed securities the same way they treated safe Treasury bonds... and the result was that taxpayers were left holding the bag when the big banks didn’t have enough capital to withstand losses.” See “The Semiannual Testimony on the Federal Reserve’s Supervision and Regulation of the Financial System,” U.S. Senate Committee on Banking, Housing, and Urban Affairs, Washington, D.C., April 19, 2018.

7. For numerical examples, see Thomas L. Hogan, Neil Meredith, and Xuhao Pan, “The Failure of Risk-based Capital Regulation,” Mercatus on Policy no. 120 (Mercatus Center at George Mason University, Arlington, Virginia, January 2013); Thomas L. Hogan and G.P. Manish, “Banking Regulation and Knowledge Problems,” Advances in Austrian Economics 20 (2016): 213–34.

8. As VanHoose (2007, 3681) describes, “The theoretical banking literature is sharply divided about the effects of capital requirements on bank behavior and, hence, on the risks faced by individual institutions and the banking system as a whole.” See David VanHoose, “Theories of bank behavior under capital regulation,” Journal of Banking and Finance 31 (2007): 3680–97.

9. See Robert B. Avery and Allen N. Berger, “Risk-Based Capital and Deposit Insurance Reform,” Journal of Banking and Finance 15 (1991): 847–74; Ronald E. Shrieves and Drew Dahl, “The relationship between risk and capital in commercial banks,” Journal of Banking and Finance 16 (1992): 439–57.

10. Andrew G. Haldane and Vasileios Madouros, “The Dog and the Frisbee” (speech given at the Federal Reserve Bank of Kansas City's 36th economic policy symposium, Jackson Hole, Wyoming, August 31, 2012). Their results for GSIBs were shown to apply to U.S. banks by Thomas L. Hogan, Neil R. Meredith, and Xuhao (Harry) Pan, “Evaluating risk-based capital regulation,” Review of Financial Economics, forthcoming.

11. Asli Demirgüç-Kunt, Enrica Detragiache, and Ouarda Merrouche, “Bank Capital: Lessons from the Financial Crisis,” Journal of Money, Credit, and Banking 45, no. 6 (2013): 1147–64.

12. Viral V. Acharya, Robert Engle, and Diane Pierret, “Testing Macroprudential Stress Tests: The Risk of Regulatory Risk Weights,” Journal of Monetary Economics 65 (2014): 36–53.

13. See Thomas L. Hogan, “Capital and risk in commercial banking: A comparison of capital and risk-based capital ratios,” Quarterly Review of Economics and Finance 57 (2015): 32-45; Thomas L. Hogan and Neil R. Meredith, “Risk and Risk-Based Capital of US Bank Holding Companies,” Journal of Regulatory Economics 49 no. 1 (2016): 86–112.

14. Due to insufficient stock price data, some banks are not shown in this figure, which includes 53 of the 70 bank holding companies that reported total assets of $10 billion or more on their Q3 2008 Consolidated Financial Statements for Bank Holding Companies (Y-9C) reports.

15. Thomas Hoenig, “A Conversation about Regulatory Relief and the Community Bank” (remarks given at the 24th Annual Hyman P. Minsky Conference, National Press Club, Washington, D.C., April 15, 2015).

16. Sheila Bair, “Congress Flirts With Disaster on Bank Leverage Ratios,” The Wall Street Journal, February 12, 2018. See also Thomas M. Hoeing and Sheila C. Bair, “Relaxing Bank Capital Requirements Would Risk Another Crisis,” The Wall Street Journal, April 26, 2018.

17. “Notice of Proposed Rulemaking on Supplementary Leverage Ratio Issued by the Federal Reserve and OCC” (statement of Martin J. Gruenberg, Chairman, Federal Deposit Insurance Corporation, April 11, 2018).

18. Financial CHOICE Act of 2017, H.R. 10, 115th Cong. (2017).

19. Economic Growth, Regulatory Relief, and Consumer Protection Act, S. 2155, 115th Cong. (2017).

20. See, for example, James R. Barth and Stephen Matteo Miller, “Benefits and Costs of a Higher Bank Leverage Ratio” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, Virginia, February 2017); “The Minneapolis Plan to End Too Big to Fail” (Federal Reserve Bank of Minneapolis Special Studies, 23A, Minneapolis, Minnesota, 2016).

21. As the Fed’s proposal summary describes, “These changes would provide improved incentives and better ensure that the eSLR generally serves as a backstop to risk-based capital requirements rather than as generally a binding constraint on firms” (1). See Gibson et al., “Joint notice of proposed rulemaking to modify the enhanced supplementary leverage ratio standards applicable to U.S. global systemically important bank holding companies and certain of their insured depository institution subsidiaries” (memo to the Board of Governors of the Federal Reserve System, April 5, 2018).

22. “The Semiannual Testimony.”

23. Arturo Estrella, Sangkyun Park, and Stavros Peristiani, “Capital Ratios and Credit Ratings as Predictors of Bank Failures,” FRBNY Economic Policy Review (July 2000): 33–52.

24. Ibid., 33.

25. Ibid., 50.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.