Author(s)

Download the full written testimony here.

This testimony was delivered before the U.S. House of Representatives Committee on Foreign Affairs Subcommittee of Terrorism, Nonproliferation and Trade on April 2, 2014.

During the past decade, innovative new techniques involving the use of horizontal drilling with hydraulic fracturing have resulted in the rapid growth in production of natural gas, crude oil and natural gas liquids from shale formations in the United States. This has already transformed the North American gas market, generating ripple effects around the world and setting the stage for a period of global gas market transition. For the purposes of this exposition, it has also significantly impacted the US domestic crude oil market, and contributed to the benchmark US domestic crude oil price – West Texas Intermediate (WTI) – becoming substantially discounted to global benchmark crudes. While this discount arose largely due to constraints on the ability to move crude oil away from Cushing, OK, it has triggered a concern that broader discounts of US crude oil prices relative to global market prices are on the horizon. Specifically, a constraint on the ability to arbitrage a price differential drove the discount of WTI, so it stands to reason that a constraint on the ability to arbitrage US crude at the coasts will more broadly emerge as the existing constraint banning US oil exports becomes binding.

Due to existing regulatory and market institutions, the US will remain a preferred area for upstream development, as long as the balance between price and cost remains favorable relative to other regions of the world; so, the US stands to contribute greatly to global supply growth over the foreseeable future. Indeed, the type of well-documented transformational change that has been set in motion in global gas markets is becoming more and more visible in the global oil market. Rapid growth in US light tight oil (LTO) production has contributed to a decline in US oil imports and to the US becoming a net exporter of petroleum products. Nevertheless, the impact on global crude oil market may be muted by current regulation in the US. Suffice it to say, there is substantial interest in changing the long-standing laws banning crude oil exports.

In January 2014, the Center for Energy Studies (CES) at Rice University’s Baker Institute launched a study, jointly with Columbia University’s Center for Global Energy Policy, into the consequences of allowing crude oil exports from the US. The first phase of the study involves applying established economic principles to understand how existing laws that prohibit the export of crude oil from the US impact gasoline prices (and petroleum product prices more generally) and US energy security. The second phase of the study takes a more in depth view of the downstream and upstream oil and gas sectors in order to understand how existing laws will impact opportunities in each. The comments herein focus on phase one.

A Demand-Supply Motivation: Global and in the US

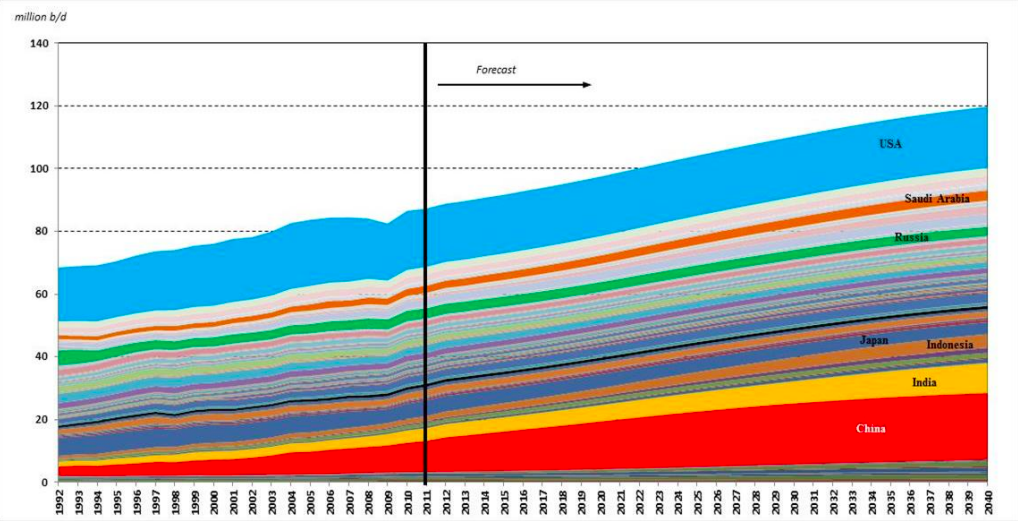

As seen in Figure 1, global crude oil demand is projected to increase to just short of 120 million barrels per day by 2040. The majority of the projected growth will come from developing Asian economies, particularly China and India, but also several other Asia-Pacific countries. Importantly, demand in the countries of the Middle East is projected to grow among the fastest in the world, attributed to economic growth as well as heavily subsidized domestic energy prices. Of course, a lifting of subsidies would abate the projected growth, but absent a significant shift in domestic energy pricing policy, these countries will be challenged to maintain, much less grow, exports. This, in turn, signals a need for new sources of supply, and could move the geopolitical compass toward new supply growth areas, particularly those with abundant, accessible unconventional resources such as Canada and the US.

Figure 1 — Baker Institute CES Global Oil Demand Outlook by Country, 1992–2040

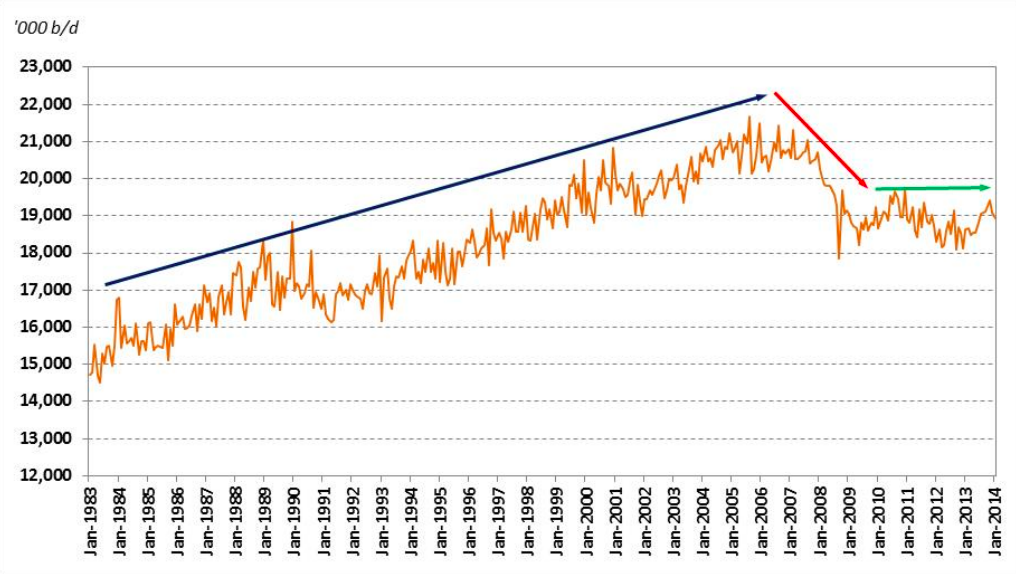

The US is poised to become a significant supplier to the global oil market. This is the result of both the aforementioned domestic supply developments and the recent trends seen on the demand side of the equation. Figure 2 indicates US demand for crude and petroleum products. Notably, we see a significant decline in demand post 2006. This was driven largely by the economic malaise of the period, but advances in end-user efficiency have also played a significant part. However, the immediate decline in demand seen from 2006 through 2009 has not been offset by a “rebound”, with demand remaining relatively flat for the past five years. This has, in turn, set the stage for what has transpired on the supply side of the market.

Figure 2 — US Petroleum Demand, Jan1983–Jan2014

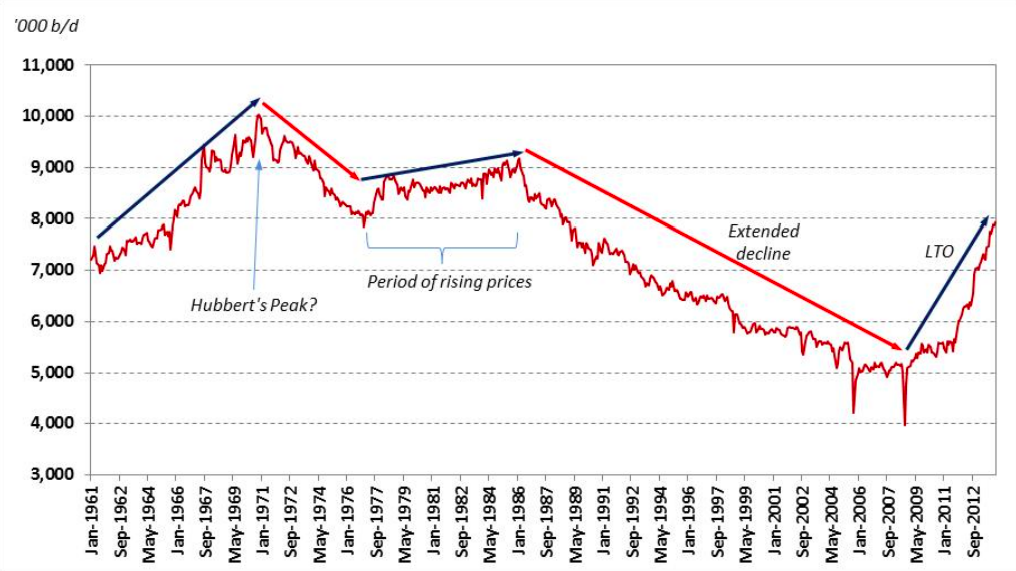

Already, we have seen crude oil production in the US rise dramatically year-over-year since 2008, primarily due to shale oil prospects. This represents a reversal of over three decades of production declines, and has turned the US from an ever-expanding sink for global crude oil into a viable global supply province in less than a decade. Of course, the global crude oil production anthology is still being written, but we have seen real supply-side responses to high prices in the last decade in the form of deep water and unconventional sources of oil. In fact, US production growth in the last five years, due in large part to new production from unconventional resources, has been the highest seen in many decades (see Figure 3).

Figure 3 — US Crude Oil Production, Jan1961–Jan2014

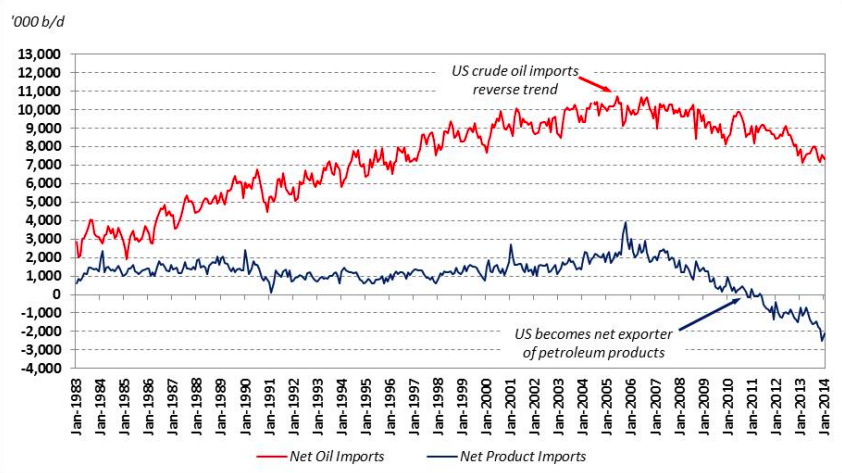

Analysis of Figure 3 stimulates interest to gain a better understanding of the long term prospects for US oil production growth along the lines of what has been witnessed since 2008. To date, growth in domestic production has been driven by LTO developments in the Bakken and Eagleford shale plays. With other opportunities – such as in the Permian basin – receiving increasing attention, the prospects for continued growth look promising. Already, we have seen declining US crude oil imports (see Figure 4).

Figure 4 — Shifts in US Crude Oil and Petroleum Product Trade, Jan1983–Jan2014

As noted above, declining demand since 2006 has played a major part as well. This is particularly salient for petroleum product markets, as the US now exports (net) upwards of 2.5 million barrels per day of petroleum products (see Figure 4). In fact, the combination of discounted crude oil, low cost natural gas, lower demand, and no policy-directed constraint on exporting refined products has allowed the U.S to effectively become a refining hub over the past few years, providing petroleum products to the global market place.

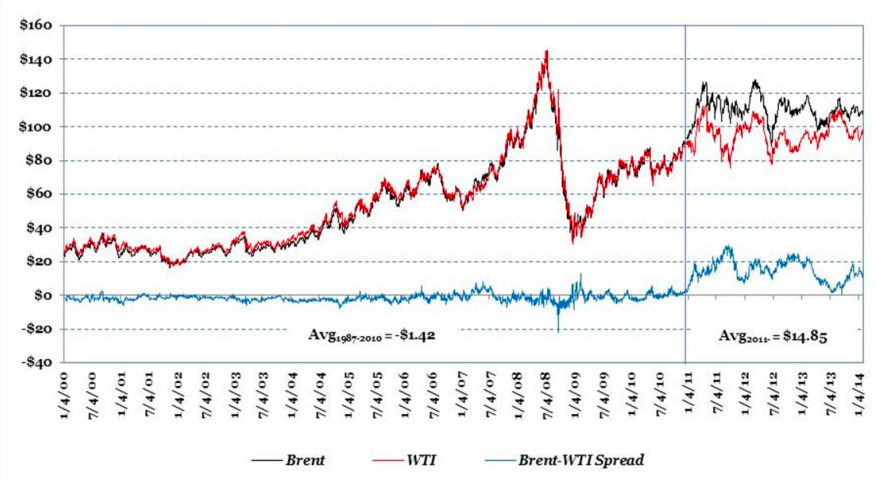

Strong domestic production growth coupled with a physical constraint on moving crude oil away from Cushing has resulted in a discount in the WTI price relative to the price at Brent (see Figure 5). In fact, the discount has average almost $15 per barrel since the end of 2010, which is especially remarkable given WTI priced at a premium of almost $1.50 (on average) the decade prior. There is mounting concern that the observed discount at WTI will spread to be more broadly representative of all US crude oil prices. This concern owes to the fact that current US policy explicitly prohibits exports of crude oil, thereby limiting arbitrage of growing domestic supply into the global market. The commercial implications are that lower domestic crude oil prices could trigger stronger profit opportunity for refineries in the near term, and may even encourage investment in the downstream in the longer term, should the discount persist. But, a persistent discount may also negatively impact US production, which has implications for the economic activity associated with upstream production and, of course, the impact that US shale will ultimately have on the global oil market. So, there are trade-offs that must be evaluated in the context of current law versus lifting the ban on crude oil exports.

Figure 5 — US Crude Price Discounts

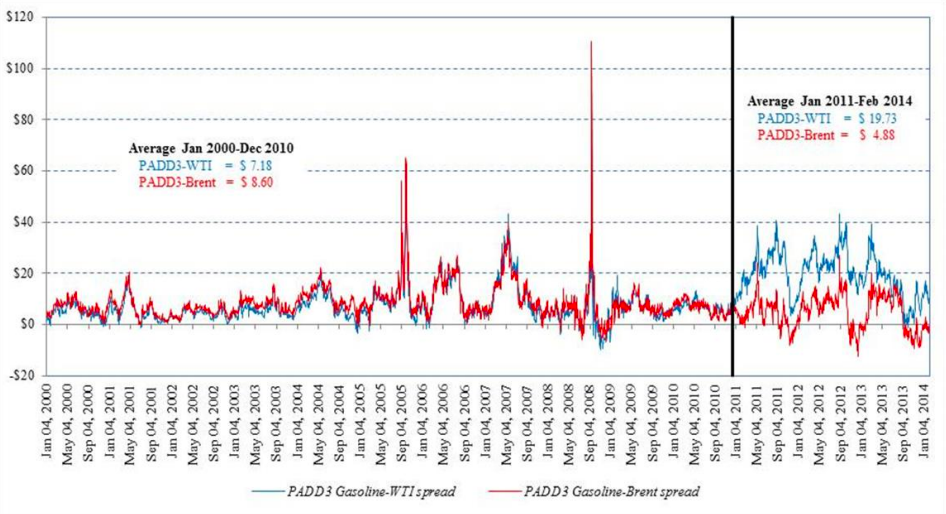

In order to understand what current law means relative to the alternative of lifting the ban on crude oil exports, we must first understand how current law is affecting the arbitrage opportunity. Consider the case where we have two markets – for example, a crude oil market and a petroleum product market – where one provides the feedstock for the other. If we place a constraint on the physical ability to trade in the feedstock market, but there are no such constraints on the final product market, then the global arbitrage opportunity moves into the final product market. In other words, since there is no constraint on trade in the final product market, it can fully adjust to capture any arbitrage opportunity that opens due to regional price differentials that may emerge in the feedstock market. Indeed, in Figure 6 we see the relative price of PADD 3 gasoline to Brent crude – an international benchmark crude – remained reasonably stable when compared to the relative price of PADD 3 gasoline to WTI. This indicates that although WTI became discounted relative to Brent due to physical constraints on trade away from Cushing, that discount did not matriculate into the price of domestic gasoline.

Figure 6 — US Gasoline Price Discounts?

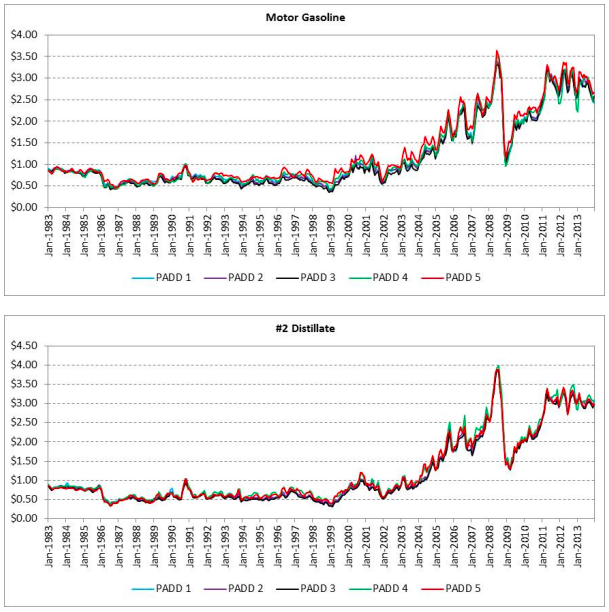

We expand on the above claim in a moment, but taking the thesis as given we should see the spread between WTI and petroleum product prices also widen. This follows because with no constraint on physical trade in the product market, its clearing price will be set by the cost of supply – or the crude barrel – at the margin. This barrel will distinctly not be the price of the discounted barrel of domestic crude oil. Such a pricing mechanism requires, of course, that there be no constraint on trade in the product market. As can generally be seen in Figure 7, wholesale US petroleum product prices continue to move very closely together, as they have since the early 1980s. This is indicative of a petroleum product market in which there is no binding physical constraint to arbitrage price movements across regions.

Figure 7 — US Petroleum Product Prices Continue to Move Together

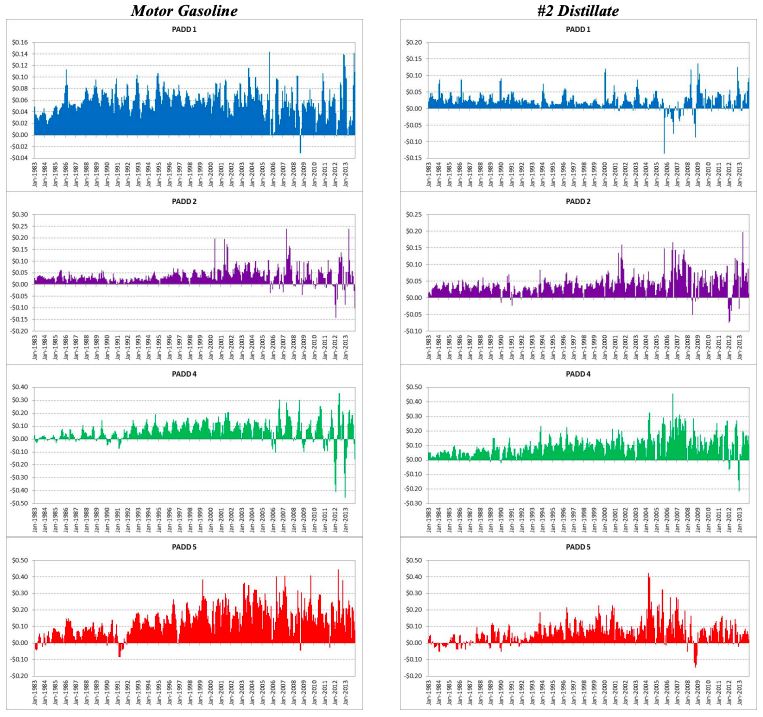

We also see that there is no apparent constraint on wholesale trade across regions in the U.S. As seen in Figure 8, the prices of motor gasoline and #2 distillate in PADDs 1, 2, 4, and 5 remain, for the most part, above the price in PADD 3. There are noticeable points of departure in the motor gasoline price spreads in PADDs 2 and 4, particularly later in the time horizon, but these should not be interpreted as the result of crude oil price discount in these regions yielding a lower gasoline price. Indeed, if that were true we would see the same effect arising in the market for #2 distillate. Hence, it points to other issues related to gasoline specifically – such as seasonal pressures and costs for other feedstock – that are not as prevalent in the distillate market.

Figure 8 — US Petroleum Product Prices – Evidence of Discounts Relative to PADD 3?

A Framework for Analysis

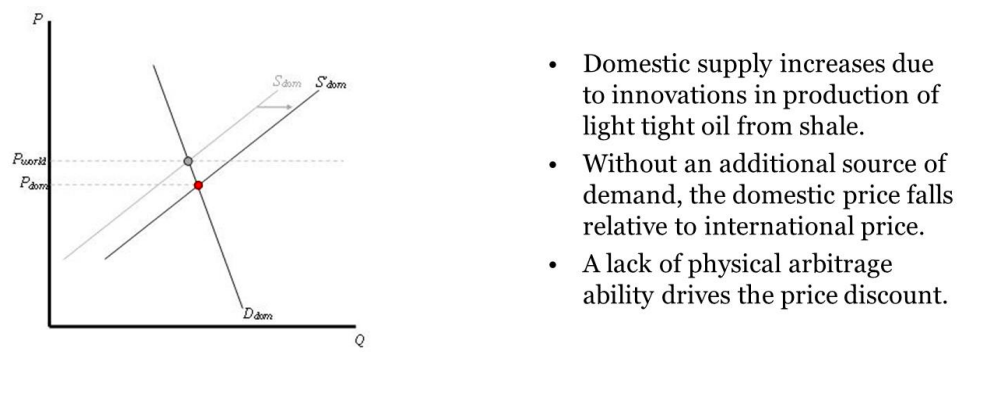

Is there a justification for the paradigm discussed above in economic theory? Yes. To begin, the US domestic crude oil supply curve shifts out, a result generated by technological advances in producing crude oil from shale. The ultimate outcome for price will be determined by the extent to which new sources of demand are allowed to be realized.

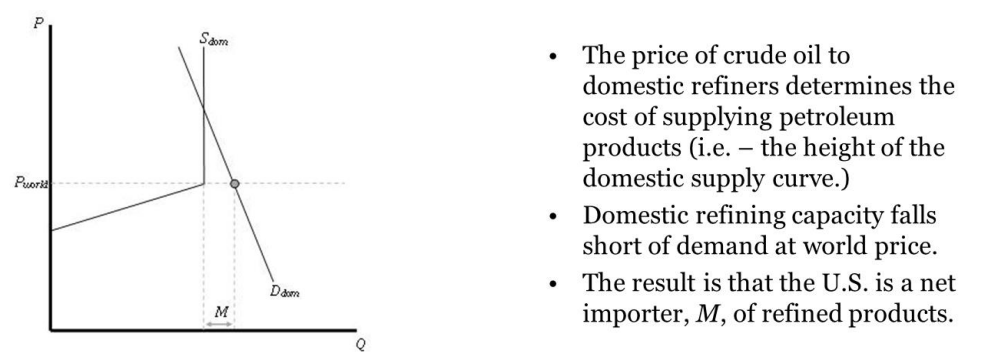

Figure 9 — The US as Net Petroleum Product Importer (Prior to 2011)

Figure 10 — The Domestic Crude Oil Market – Initial Impact of LTO Production Growth

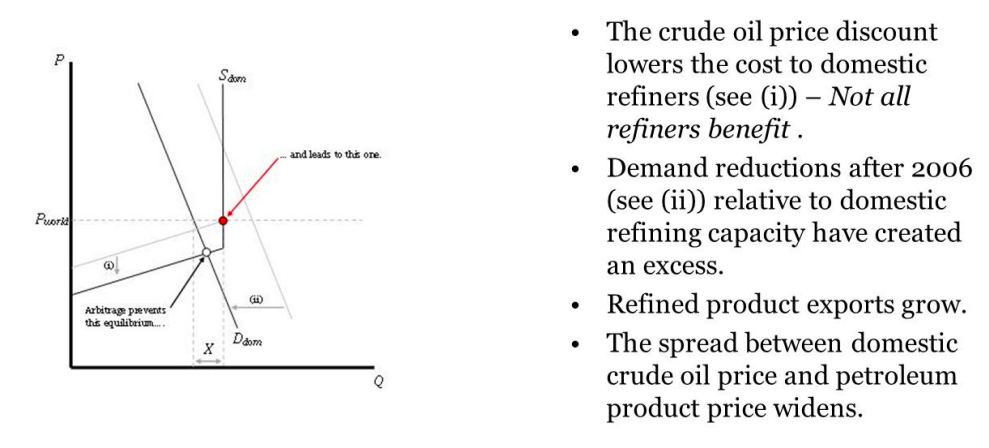

Figure 11 — Implications for Petroleum Product Price and Trade

Under the status quo of no US crude oil exports Figures 9 through 11 depict why the price of petroleum products will rise relative to the domestic crude oil price but not the international crude oil price. The constraint on crude oil exports pushes the arbitrage opportunity downstream into the product market where there is no constraint on trade.

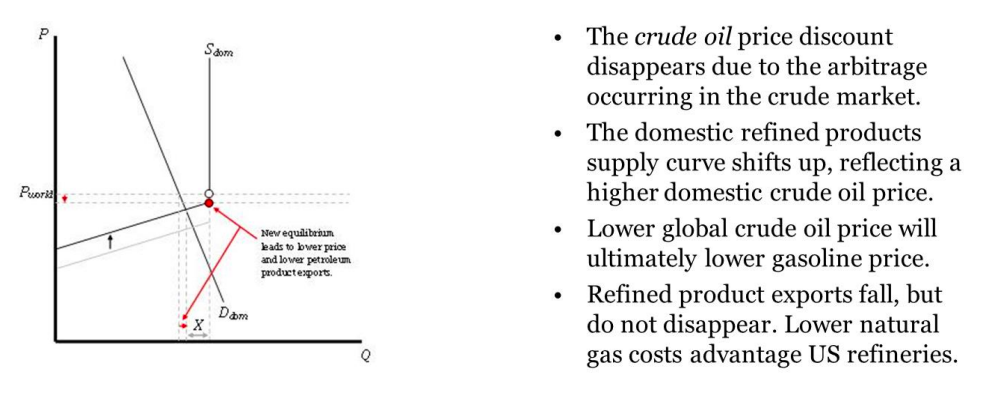

Figures 12 and 13 present the alternative to the status quo summarized in Figure 9 through 11. Specifically, we see in Figures 12 and 13 the effect of lifting the ban on crude oil exports. In this case, the arbitrage opportunity that exists in the crude oil market can be captured by domestic producers. This results in greater trade in the crude oil market, but less trade from the US in the product market. Relaxing the constraint allows the gains from trade in oil to be captured.

Figure 12 — Lifting the Crude Oil Export Ban – Impact on Crude Oil Price

Figure 13 — Lifting the Crude Oil Export Ban – Impact on Petroleum Product Price

It is important to recognize that lifting the ban on exports results in additional demand for US produced crude oil, effectively shifting the demand curve out (see Figure 12). This facilitates more production from the US, which is why such a policy will exert some downward pressure on the global price. The degree to which this occurs is highly dependent on a variety of factors – such as OPEC response and the relative elasticity of supply and demand both domestically and internationally – but, qualitatively, the pressure is for price to move down, not up. The bottom line is that the implications of US LTO production on the global oil market are highly dependent on US policy with regard to oil exports. Specifically, the impacts are larger in the case where the US market is more fully integrated via trade with the global market, meaning greater fungibility enhances the impacts of US LTO production.

Bringing It All Together

First, the wholesale price of gasoline is set by the crude barrel at the margin. Since there are no restrictions on gasoline exports, this means the barrel at the margin is an internationally traded barrel. As such, the price of gasoline domestically will converge to a value reflecting a fully arbitraged international price, correcting for the cost of trade.

Effectively, the constraint on crude oil exports moves the arbitrage opportunity downstream. This is not a groundbreaking result. Rather, it is exactly what constraints do. They secure rents in certain parts of the value chain by limiting market responsiveness.

So, is there evidence of a binding constraint? Yes, the spread between WTI and Brent is on critical piece of evidence. While this was not driven by the export ban, it does indicate exactly what will happen in the event of a physical constraint on the ability to trade. As that constraint is relaxed, the export restriction will become binding, especially as domestic LTO production backs out all the imported light crude volumes it can. We will see evidence of this as spreads emerge between the Louisiana Light Sweet (LLS) crude oil price and international crude oil prices.

Another point of evidence of a binding constraint can be seen in the higher volatility of the spread between US gasoline price and WTI. This volatility emerges because once the binding constraint is realized then any movement in demand is revealed through an exacerbated price movement for oil but not for petroleum products.

If exports reduce the price of crude internationally, then domestic gasoline price should fall. The question then becomes, is the current ban on oil exports worth it?

A Comment on Energy Security

The concept of energy security really began to take hold as a matter of national interest following the oil price shocks of the 1970s. In fact, every recession since World War II, except one, has been preceded by a run up in the price of oil. This strong correlation has prompted many policies aimed at mitigating the impacts of rising oil prices. As such, “energy security” generally refers to policies that aim to ensure adequate supplies of energy at a reasonable price in order to avoid the macroeconomic dislocations associated with energy price spikes or supply disruptions.

So, how exactly do high oil prices negatively impact the economy? The literature on this matter is fairly deep, and there have been many proposed channels to convey the correlation, some of which carry a causal overtone. These channels can be summarized into

… inflationary effects

- Increases in the price of oil (energy) lead to inflation which lowers the quantity of real balances in an economy thereby reducing consumption of all goods and services.

- Counter-inflationary monetary policy responses to the inflationary pressures generated by oil (energy) price increases result in a decline in investment and net exports, and consumption to a lesser extent.

… trade balance effects

- Oil (energy) price increases result in income transfers from oil (energy) importing countries to oil (energy) exporting countries. This, in turn, causes rational agents in the oil (energy) importing countries to reduce consumption thereby depressing output.

… industrial influences

- If oil (energy) and capital are complements in the production process, then oil (energy) price increases will induce a reduction in the utilization of capital as energy use is reduced. This, in turn, suppresses output.

- If it is costly to shift specialized labor and capital between sectors, then oil (energy) price increases can decrease output by decreasing factor employment. If a recession is not unreasonably long, the high costs of training will cause specialized labor to wait until conditions improve rather than seek employment in another sector.

… and investment impacts

- In the face of high uncertainty about future price, which may arise when a price shift is unexpected, it is optimal for firms to postpone irreversible investment expenditures. Investments are irreversible when they are firm or industry specific.

While all of these channels of transmission matter to some extent, it is important to recognize that the oil prices – and, more importantly, oil product prices – are determined in the international market. So, regardless of policy on crude oil exports, as long as product markets remain fully fungible, the above proposed mechanisms for transmission of rising prices to negatively impact economic activity generally remain in play.

The one channel of transmission that is distinctly different with regard to US export policy is the “balance of trade” channel. Here, oil importers do worse when price rise, while exporters do better. It then follows that if the US becomes a larger exporter of light crude oil, while importing heavier crudes to match current refinery configurations, the net impact on the US trade balance is overall positive. Moreover, if prices rise, the export of light crudes provides an “exporter benefit”. In effect, it shields the economy from increases in prices in a way that is not otherwise present.

Importantly, the theoretical framework here is fairly well established, so qualitatively this can stated with a fair degree of certainty. However, the degree to which any energy security benefit would be conveyed has yet to be determined. That is a matter of ongoing research.