Introduction

Donald Trump returns to the Oval Office in 2025 to confront a very different set of dynamics in the Middle East and Persian Gulf from those his first administration left behind in 2020. Nominations to his second administration indicate that officials seek to renew the policy of “maximum pressure” on Iran imposed in 2018 after the U.S. withdrawal from the Joint Comprehensive Plan of Action (JCPOA), known as the Iran nuclear deal, a move that Joe Biden did not reverse during his single term in office.

Over the intervening four years, regional rapprochement between Iran and U.S. partners in the Gulf region and the growth of Iranian oil flows to China have created new “facts on the ground” for the incoming White House and foreign policy teams. Iran has grown more sophisticated and successful in cloaking oil exports, while its trade partners have collaborated more deeply in the subterfuge in the interest of maintaining important fuel shipments put at risk by U.S. sanctions. However, Iran’s weakened position after the December 2024 fall of Syria’s Bashar Assad adds a new twist to this dynamic, following the degrading of Hezbollah in Lebanon.

A Trump-led reenforcing of U.S. sanctions on Iranian oil exports is likely to find acquiescence in Europe but be less welcome in the Gulf region, where fears of an Iranian response — up to and including attacks on shipping and other targets linked to energy pricing — are driving rapprochement.

On the other side of the ledger, the large overhang in global oil supply suggests that oil markets are in a good position to absorb any loss of Iranian supply. Several OPEC members have signaled increasing impatience with long-standing quota restrictions and would relish the opportunity to bring idled capacity to market. Considerations should be made for Iran’s responses to the bottling up of its export economy.

Iran’s ability to counter sanctions has also grown. The shadow networks of intermediaries and front organizations around the world have enabled Iran’s “dark fleet” to operate, bypassing restrictions and significantly increasing the sale and transfer of oil, primarily to buyers in China. The size of these networks also means that there is scope for enhancing compliance and enforcement of existing sanctions and working more assertively with authorities worldwide to identify breaches and close loopholes. That said, it is precisely the international nature of these networks that makes them points of vulnerability that can be targeted with greater allocation of resources and policy intent.

Iran has indicated that it will respond to U.S. pressure with maximum resistance, asserting that it is better prepared now than during the first Trump administration to counter sanctions. While Tehran has expressed willingness to engage in new negotiations with Washington, it is also exploring various options to raise the costs of what it views as the U.S.’ pursuit of regime change and economic strangulation of a nation of 90 million. Reciprocal actions by Iran could drive an escalatory cycle, including nuclear weaponization activity, that diverts costly U.S. time and attention. Few players beyond Israel appear interested in a U.S. war with Iran, which could upend regional stability and set back the ongoing economic diversification investments prioritized in the Gulf Cooperation Council (GCC). The Trump administration must weigh the costs of greater involvement and expense in an intensified conflict with Iran with the potential gains of doing so, as well as the opportunity costs of attention diverted from other U.S. national interests.

Alternatively, the U.S. could pursue a grand bargain with Iran, addressing not only the nuclear issue but also other areas of contention in exchange for sanctions relief. Such an approach would require significant political capital and bold leadership, as past U.S.-Iran negotiations — and previous attempts at a comprehensive agreement — demonstrate that such efforts face considerable obstacles in both Washington and Tehran.

To assess the issues highlighted above, this brief will deliver the following:

- An overview of the sanctions regime that has developed over more than four decades.

- An examination of Iran’s patterns of oil exports and dark fleet movements.

- OPEC+ and oil market considerations.

- The Iraq connection.

- Potential Iranian responses to U.S. pressure and engagement.

A Brief History of Sanctions on Iran

U.S. sanctions and other measures on Iran go back 45 years and have evolved and expanded considerably in their scope and scale. Taken together, they encompass primary and secondary sanctions that prohibit nearly all trade between the U.S. and Iran. These restrictions cover the energy and financial sectors as well as others, such as shipping and the arms trade, in addition to proliferation activities. The measures are based on multiple legal authorities and have been introduced by both the executive and legislative branches of the U.S. government, with the International Emergency Economic Powers Act (IEEPA) of 1977 invoked for the first time in 1979 to impose economic sanctions on Iran, giving the president sweeping powers to declare national emergencies in respect of specific issues.

Sanctions were initially introduced in the wake of the storming of the U.S. Embassy and seizure of American diplomats in Tehran in November 1979, when President Jimmy Carter issued Executive Order 12170. This declared a national emergency vis-à-vis the situation in Iran (which remains in force) and froze Iranian government assets in the United States. In January 1984, the State Department designated Iran a state sponsor of terrorism after the deadly Beirut terrorist bombings of the U.S. Embassy in April 1983 and U.S. Marine barracks in October 1983 that killed 241 Marines and other U.S. military personnel.

In 1992, the Iran-Iraq Arms Non-Proliferation Act targeted Iran’s proliferation activities, as did Executive Order 12957, issued in 1995 to renew the national emergency declaration. The 1996 Iran Sanctions Act introduced secondary sanctions aimed at foreign companies investing in the Iranian energy sector. The 1996 act met with resistance from European Union (EU) states at the extraterritorial application of U.S. domestic law.

The discovery of two undeclared nuclear sites led to international sanctions via United Nations Security Council resolutions from 2006–10, which expanded and tightened nuclear-related sanctions. The latter was based on the International Atomic Energy Agency (IAEA) finding in 2005 that Iran was not complying with its obligations under the Nuclear Non-Proliferation Treaty, signed in 1968. The EU, Japan, South Korea, India, Canada, and Norway announced their own sanctions in 2010, the same year that Congress passed the Comprehensive Iran Sanctions, Accountability, and Divestment Act (CISADA). Further U.S. pressure arose from the National Defense Authorization Act for 2012, which authorized financial sanctions on third-country banks engaged in Iranian oil transactions and led the EU to halt imports.

The coordination of international and U.S. sanctions targeting nearly all aspects of the Iranian economy contributed to the 2012 back-channel dialogue between Iranian and U.S. officials, facilitated by Oman. Talks resulted in a Joint Plan of Action in 2013, setting the framework for the negotiations that produced the JCPOA in 2015.

Most UN and EU sanctions were lifted when the JCPOA was implemented in January 2016. The U.S. provided relief from secondary and nuclear-related sanctions, although other U.S. sanctions — targeting Iran’s ballistic missile development, support for terrorism, human rights abuses, and destabilizing regional activities — remained in place. In 2018, the Trump administration withdrew the U.S. from the JCPOA, despite Iran’s compliance with the agreement, reimposed all U.S. sanctions that had been eased, and later introduced a “maximum pressure” campaign designed to intensify sanctions enforcement. The U.S. efforts failed to force Iran to renegotiate the nuclear agreement. In fact, Tehran incrementally expanded its nuclear program, signaling readiness to reversal only if the U.S. returned to the JCPOA or if Europeans honored their commitments under the agreement. Since 2022, the EU has responded to renewed crackdowns on demonstrations in Iran, as well as Iranian military support for Russia’s war in Ukraine, with 10 new packages of sanctions on the Islamic Republic.

Should Trump wish to waive or lift economic sanctions, perhaps as part of a “grand bargain” with Iran, he would need to determine and certify that the Iranian government is no longer a state supporter of terrorism. This is required to lift the majority of sanctions imposed by CISADA in 2010. The president also has the authority to renew, alter, or revoke executive orders pursuant to the National Emergencies Act and the IEEPA, but Congress has in certain cases required a determination that specific conditions be met before an order can be revoked and the economic restrictions lifted. For instance, in 2016, the lifting of nuclear-related sanctions was provided through a new executive order, statutory waivers, and issuance of licenses by the Office of Foreign Assets Control at the Treasury Department.

Patterns in Iranian Oil Exports

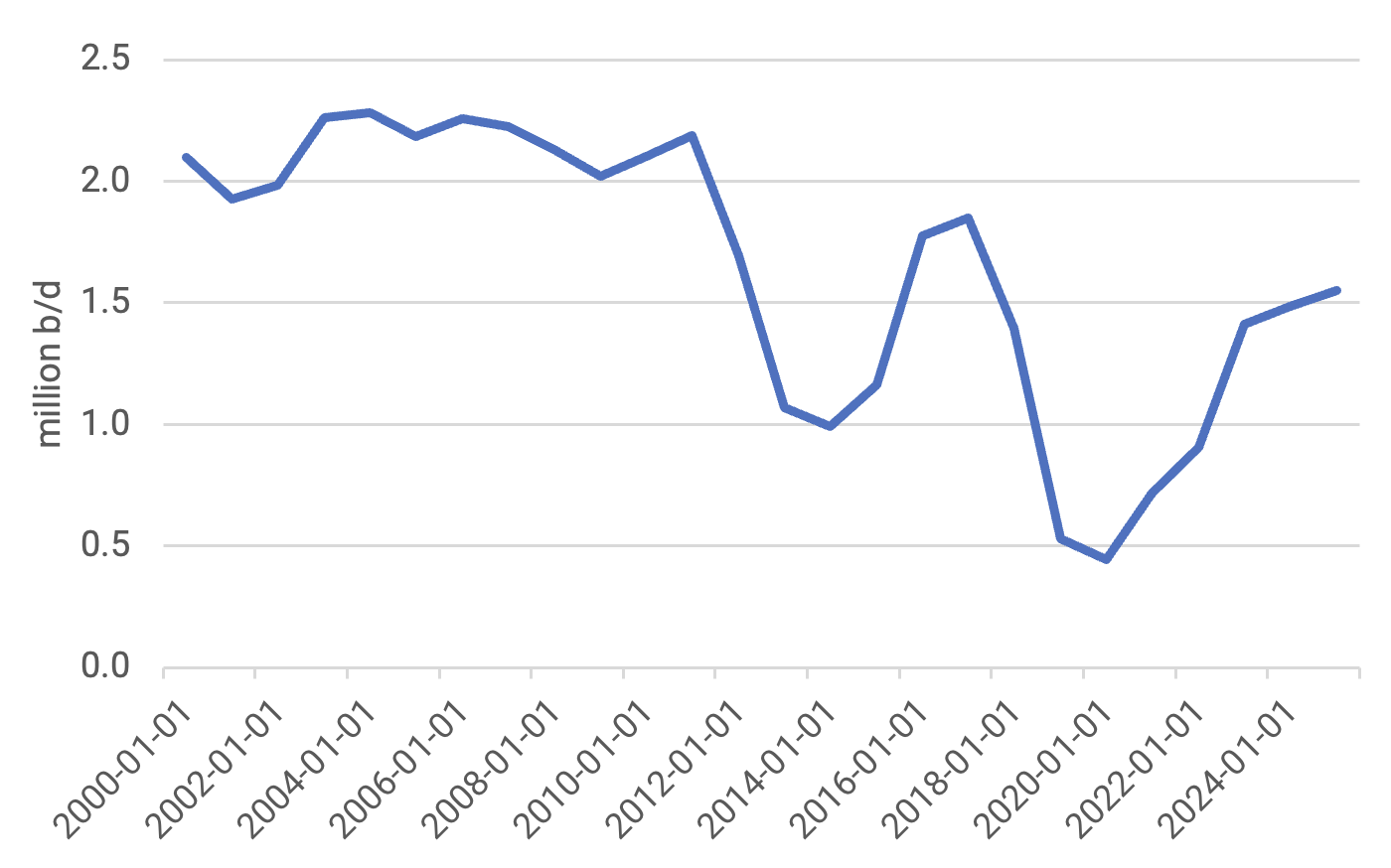

Iran has optimized sanctions evasion through sophisticated techniques developed through decades of practice. Despite sanctions, Iran exported an average of 1.3 million barrels of oil per day (mbd) in 2024, with shipments breaching 1.8 mbd in September, according to Kpler. Other estimates, such as one from the tracking firm TankerTrackers, are slightly higher, with monthly highs over 2 mbd. Figure 1 depicts Iranian exports seesawing since 2010 due to changes in sanctions and enforcement intensity.

Figure 1 — Iranian Crude Oil Exports Since 2000

About 90% of Iranian crude exports are landed in China, where Iranian oil forms some 10% of total Chinese imports, with the remainder going in far smaller amounts to Syria, Venezuela, and the United Arab Emirates (UAE). The U.S. Energy Information Administration (EIA) cites two estimates that Iran exported just over 1.2 mbd to China in 2023. Those flows rose in 2024 (Table 1).

Table 1 — Estimates of Iranian Oil Exports, 2018–23

Note: Thousand barrels per day.

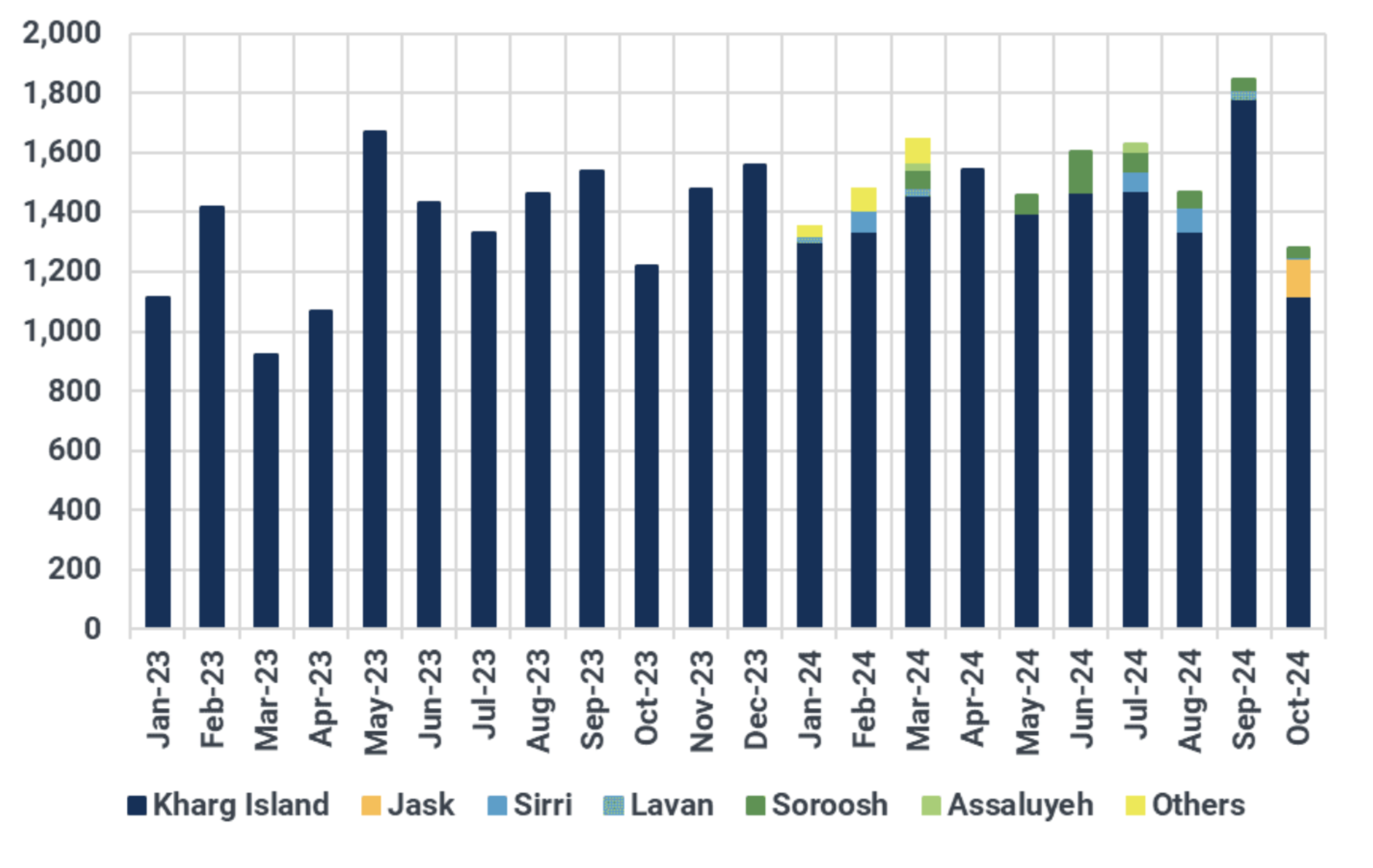

Iran’s exports originate mainly from Persian Gulf terminals at Kharg Island, Iran's primary oil export terminal located 16 miles off the coast, and smaller facilities inside the Gulf. A new export terminal outside the Strait of Hormuz at Jask on the Gulf of Oman began shipping small cargoes in 2024, as shown in Figure 2. Jask’s opening was facilitated by the 2021 completion of the first phase of a 1,000-kilometer onshore pipeline from the Goureh oilfield, with an initial capacity of 300,000 barrels/day that is set to increase to 1 mbd.

The risks to the global economy from the blockage of oil exports via Hormuz had already led to the construction of export capacity outside the strait by Saudi Arabia and the UAE. Iran has threatened to close the strait in response to an attack by Israel or the United States. The new Jask terminal could prevent such a closure from bottling up Iran’s entire export capacity. Kuwait and Qatar, major exporters of oil and liquefied natural gas (LNG), respectively, lack any alternative to the Strait of Hormuz. Their exports would be blocked in the event of a Hormuz closure.

Figure 2 — Iranian Oil Exports by Port of Origin

Smuggled Iranian crude oil sells at a discount to unsanctioned oil, one of the factors attracting willing buyers. Sources cited by the EIA suggest Iran is accepting discounts from the Brent index of as much as $13 per barrel (bbl) for its light crude and $20/bbl for its heavy crude (Table 2). Bloomberg estimated that transporters of Iranian crude used ship-to-ship transfers to evade U.S. sanctions and export some 350 million barrels of Iranian oil in the first nine months of 2024. On an annual basis, that is equivalent to 1.3 mbd and worth approximately $28 billion before any discounts. After discounting, Iran’s gross receipts would be in the range of $20 billion to $24 billion. Some Iranian oil exports — mainly to Venezuela and Assad-controlled Syria prior to December 2024 — are remunerated by using lines of credit or barter agreements rather than cash payments.

Table 2 — Estimated Annual Prices of Oil Exports, 2018–23

Note: Nominal dollars per barrel.

Iran’s ‘Dark Fleet’

According to a list released by the EIA, Iranian oil is moved around the globe via an informal and secretive network of nearly 400 vessels and receiving or transshipment ports and offshore locations that have been handling Iranian crude oil and condensate exports since 2021, with China being the primary destination. Moreover, the Islamic Revolutionary Guard Corps (IRGC) appears to be playing a more prominent and direct role in all aspects of Iran’s oil export, logistics, and shipping infrastructure.

Moving a single shipment of sanctioned oil from Iran to China using the “dark fleet” typically involves three vessels and two ship-to-ship transfers, as described by Bloomberg and others. A first tanker vessel brings crude from the Iranian export terminal to a second vessel, making a ship-to-ship transfer in a holding area just outside the Strait of Hormuz in the Gulf of Oman. The second vessel brings the crude to another transshipment point in the South China Sea off the east coast of Malaysia, where oil is transferred to a third vessel, a China-bound tanker. These ships tend to bring Iranian oil to one of several ports in China’s Shandong province, where many privately held so-called “teapot” refineries operate.

A Bloomberg analysis of satellite imagery found a large increase in ship-to-ship transfers in the South China Sea over the past few years. More than 10% of tanker ships idling off Malaysia’s east coast in 2024 were parked side-by-side with another tanker vessel. In 2020, the imagery found just 5% of ships idling in the area were involved in such suspicious pairings. The oil delivered is often reported to Chinese customs authorities as Malaysian crude rather than Iranian, even though customs reporting of Chinese oil imports from Malaysia in 2023 totaled 1.1 mbd, double Malaysia’s reported 2023 crude oil production of 508,000 b/d. In some cases, “North Dubai” has been used as a code for Iran in documents related to such shipments.

The dark fleet tankers hauling Iranian oil are generally more than 20 years old, flying flags of convenience from countries with little or no connection to the trade, and are often uninsured or carrying coverage from non-Western firms. Ownership is cloaked by registry entries providing minimal and often false details or by using shell company registries to obscure financial ties, underpinned by a sophisticated “shadow-banking” system that has extended its reach over the years. When a tanker is sanctioned, it is either renamed or replaced by an alternate smuggling vessel, reports MEES.

Driving Iran and its customer base to cloak the extent of their trade are the risks that changing political winds in Washington could bring enhanced restrictions on Iran and its trading partners. Obfuscating measures appear to be based on the likelihood that Washington will impose — or enforce or enhance — secondary sanctions on firms or countries buying Iranian oil. Official Chinese government statements declare trade with Iran legitimate and beneficial, while Iranian officials have described China as a “friend for hard times.”

Despite such statements of support, the trade remains cloaked for reasons that go beyond protecting Iran. No single entity (either internationally or in the U.S.) exists to coordinate the tracking and monitoring of shadow vessels, which instead is performed by an array of private groups. This has led to gaps in oversight among U.S. government officials, shipping companies, and insurers. The use of clandestine transfers and untraceable owners and insurers and the relabeling of Iranian oil as Malaysian also serve to provide Chinese and other importing firms with “plausible deniability” that could prove helpful in maneuvering around future U.S. sanctions aimed at them, including retroactive targeting.

Imposition of Additional Sanctions

For any further tightening of sanctions or imposition of additional measures on Iran to succeed, the U.S. will need regional and international support. A similar coordinated effort between 2010 and 2012, coupled with then-President Barack Obama’s promise of sanctions relief and acknowledgment of Iran’s right to uranium enrichment, ultimately created internal pressure on the Islamic Republic in favor of an agreement and altered Tehran’s calculus ahead of the JCPOA. It may be difficult for the incoming Trump administration to isolate Iran in a more fragmented global order and with deeper Iranian connections to Russia and China, as well as Saudi Arabia and the UAE.

International support will be needed if action to avert the “snapback” deadline in October 2025 is to be taken, but dynamics within the UN Security Council do not suggest that either Russia or China will support or at least abstain from additional resolutions on Iran. Instead, the attacks on international shipping by Houthi rebels in Yemen since November 2023 have underscored the ability of Russian- and Chinese-linked tankers and dry cargo to transit the Red Sea and transport Russian oil from Black Sea ports to key markets in India and China, as well as for Chinese goods to reach destinations via the Bab al-Mandab and the Red Sea, which are critical elements of Beijing’s Maritime Silk Road initiative.

The U.S. may opt to engage bilaterally with partners, such as the UAE and Turkey, to enhance compliance with secondary sanctions with Iran and make it more difficult for Iran’s shadow-banking system to operate. It may also opt to work with Iraq to reduce its reliance on Iran for natural gas and electricity. Working closely with Panamanian authorities to restrict the permissive environment for front companies and tanker charters would engage with the “shadow fleet” in less provocative ways than maritime interdiction, which would undermine international norms and expose U.S. shipping to potential retaliation.

So much of Iran’s oil trading relies on a wide range of intermediaries and shell companies in third countries, including in states that are not U.S. adversaries, and would be vulnerable to closer monitoring and disruption if the political will to ensure compliance is matched by an increase in resources to do so.

Furthermore, the use, or overuse, of U.S. sanctions and secondary sanctions in particular is encouraging trade obfuscation. China, Iran, Russia, and other countries are incentivized to avoid commerce denominated in U.S. dollars and avoid contact with the U.S. banking system, through which sanctions could be applied and assets frozen or seized. China’s yuan-based interbank payment system (CIPS), which is increasing trade in currencies other than the U.S. dollar, is one option. Another potential option is Hong Kong, home to the only large-scale dollar-clearing system outside the U.S., which allows dollar transactions that do not involve institutions in the United States. Trump has, however, threatened to impose tariffs of 100% against BRICS (Brazil, Russia, India, China, and South Africa) member states, the economic organization that now also includes Iran, should they seek to create a new currency and challenge the dollar’s status as the world’s reserve currency.

Even U.S. allies in Europe have prepared an alternate trade-clearing architecture outside the dollar that avoids seizure of their assets in the event of U.S. sanctions and allows them discretion in choosing whether or not to support U.S. foreign policy goals.

Over time, these trends are pushing greater amounts of trade into less transparent avenues, making accounting, documentation, and analysis more difficult. The practice also reduces trade efficiency and increases greenhouse gas emissions due to the use of less efficient ships and indirect trade routes. Meanwhile, ship-to-ship transfers increase the likelihood of oil spills and contamination. Another increase in U.S. enforcement of U.S. sanctions on legitimate trade between sovereign states will exacerbate these negative trends.

OPEC and Oil Market Considerations

Were Iran’s 1.5 mbd of oil exports somehow lost to the world market, the loss would — all else constant — serve to tighten supply and raise prices. Data from Kpler has suggested that the Trump administration could realistically target the removal of between 500,000 and 600,000 b/d of Iranian oil by mid-2025 and bring Iran’s export level down to about 1 mbd. It nevertheless remains unclear which U.S. measures would have the greatest trade-reducing effects.

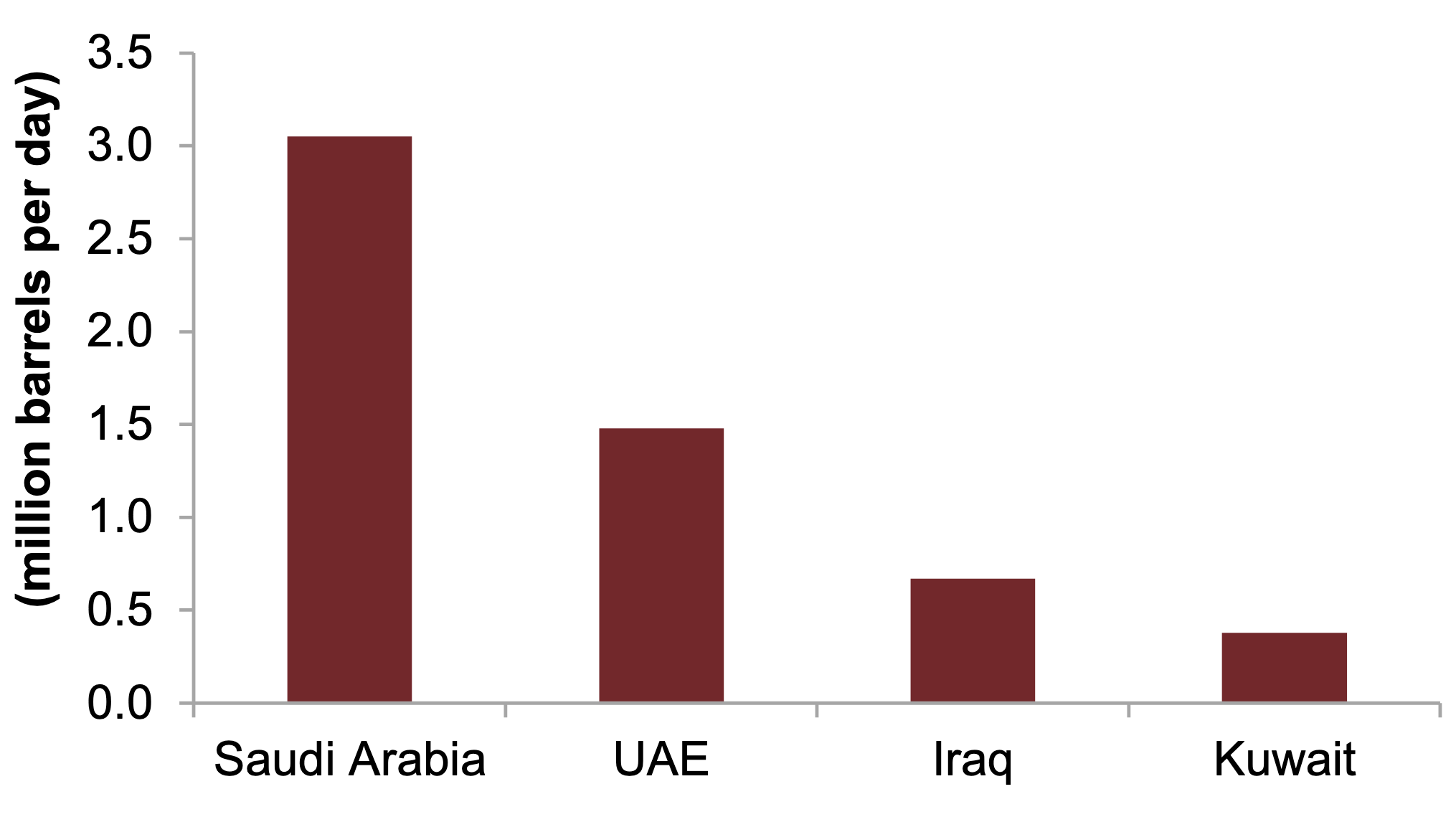

However, a few weeks before the start of Trump’s second term, the global oil market has appeared to be in a good position to absorb a potential loss of Iranian exports. The market has languished in a state of oversupply, despite the OPEC cartel holding more than 5 mbd of spare production capacity, as the EIA reported in November — more than enough to cover the loss of Iran’s 1.5 mbd of exports (Figure 3). Further, OPEC member states, including Iraq, Kuwait, and especially the UAE, have either increased production capacity or are in the midst of doing so. The UAE, with roughly one-third of its production capacity idled by OPEC quotas, has expressed a desire for a greater share of the market. Saudi Arabia is also producing far below levels it maintained in recent years.

Figure 3 — OPEC Spare Production Capacity and WTI Crude Oil Prices

Figure 4 — OPEC Spare Capacity

Note: Four OPEC members in the Gulf had more than 5 mbd of spare oil production capacity in 2024.

Any capture of Iranian market share lost to U.S. sanctions would not be risk-free. Iranian leaders should be expected to respond against rivals seen as taking advantage of its losses. Responses might even be made by physical means, such as sabotage of trading vessels or direct attack on oil installations, as was seen during the first Trump administration’s maximum pressure campaign. Memories are still fresh in Riyadh and Abu Dhabi of the attacks against maritime and energy targets in Saudi Arabia and the UAE in 2019. The subsequent inaction by the White House caused shockwaves in regional capitals, ultimately encouraging reconciliation with Tehran.

As a precaution, OPEC should be expected to take pains to present any rollback of cuts leading to production increases as a decision made independently of U.S. sanctions on Iran, and not something being done to take advantage of Iran’s quarrels with the Trump administration. Indeed, OPEC officials have long said that quota reductions are inevitable. Production increases had been telegraphed in numerous official OPEC and member country statements prior to Trump’s victory in the 2024 election.

The Iraq Connection

Another potential avenue for pressure on Iran is over its exports of natural gas and electricity to neighboring Iraq, which imports as much as 70 million cubic meters/day of natural gas from Iran during the peak summer demand season. Under a deal between Baghdad and Washington, the U.S. government has agreed to temporarily waive U.S. sanctions. In 2023, Iraq and Iran agreed to allow payment in Iraqi crude oil to further distance the trade from U.S. sanctions on payments to Iran. The State Department has been helping the Iraqi government (including in sessions held at the Baker Institute) to attract foreign investment to capture flared Iraqi gas and divert it to its power sector in hopes of boosting Iraqi generation capacity and reducing dependence on Iranian gas.

Iraq’s prodigious gas resources suggest that reliance on Iranian supply should be temporary as long as investment terms are sufficient to attract capital. Further, Iranian exports have proven fickle, cut off at times when Iranian domestic needs prevailed.

Regardless, Iraq’s electricity sector imports a significant amount of its supplies from Iran. In 2022, about 25% of Iraq’s electricity was generated by a combination of natural gas produced in Iran and electricity imported from Iran. A five-year bilateral agreement signed in 2022 set a base volume of 1 gigawatts (GW) of power exports during the peak summer months. Despite the agreement, Iranian exports to Iraq have declined, driven by shortages inside Iran. Data from the Iranian Ministry of Energy’s statistics archive shows that Tehran’s net electricity exports have drastically decreased from 2012 to 2022 due to a reduced surplus of electricity available for export. Iran cut its electricity exports to Iraq after 2020 from 7.4 terawatt-hours (TWh) to 3.5 TWh in 2022 because of power shortages in Iran.

Given Iraq’s acute and ongoing shortages of power and dangerous peak summer temperatures, U.S. pressure to curtail Iraqi imports of Iranian power or gas would be ill-advised until alternate supply or replacement Iraqi capacity is available. Iraq’s forthcoming tie-in to the GCC Interconnection Authority’s power trading system, along with smaller tie-ins with Turkey and Jordan, could prove useful in this regard.

Finally, Iraq has also served as a smuggling transit country for Iranian crude oil. During the first Trump administration, Iraq served as an informal destination for Iranian crude oil that was blended with and reexported as Iraqi crude as a workaround to avoid U.S sanctions. That smuggling avenue still continues on a smaller scale — roughly $1 billion each year — and could be revived if U.S. sanctions enforcement is enhanced.

Potential Responses From Iran

From Iran’s perspective, the Biden administration has effectively continued the Trump-era maximum pressure policy by neither returning to the JCPOA nor lifting sanctions on Iranian oil exports. However, an informal understanding with Tehran has allowed the Biden administration to ease enforcement of these U.S. sanctions, enabling Iran to increase oil exports — primarily to China — in exchange for limited constraints on its nuclear activities, the release of U.S. hostages, and a reduction in attacks by its non-state allies on U.S. forces in the region. A reinstatement of the maximum pressure policy under the second Trump administration would likely attempt to eliminate Iran’s oil exports entirely, potentially dismantling what has remained of that understanding.

Additionally, Iran faces an impending domestic energy crisis marked by gasoline and natural gas shortages. Combined with the frequency of protests over economic, social, and political grievances, another pressure campaign might exacerbate internal unrest. This outcome was a key consideration behind the original Trump administration’s maximum pressure strategy, which aimed to leverage domestic turmoil to weaken the regime. In response to that strategy, Iran resorted to harsh crackdowns on dissent, expanded support for regional non-state allies, and targeted the Middle East interests of the U.S. and its allies.

The reintroduction of the maximum pressure strategy raises critical questions about Iran’s likely reactions. Its response will depend on two core assumptions:

- Trump’s unpredictability as a double-edged sword. Iranian leaders may perceive Trump’s second term not just as a challenge, but also as an opportunity. They could view his transactional approach and willingness to defy traditional norms as a chance to exploit divisions within U.S. domestic and international politics.

- Structural obstacles to sanctions relief. Iranian policymakers are skeptical that meaningful sanctions relief is achievable, regardless of their concessions. U.S. domestic politics make it politically costly for any administration to adopt policies that could be seen as benefiting Iran.

Based on these assumptions, Iran is likely to pursue a dual-track approach of “maximum interactions” and “maximum resistance.” On the one hand, it will seek to negotiate with various regional and international actors to manage tensions and explore limited agreements with the United States. Public statements by Iranian officials suggest an openness to dialogue with the Trump administration. On the other hand, Iran is preparing for a new wave of U.S. pressure by enhancing its resilience and readiness.

As stated earlier, several developments since 2016 could shape Iran’s strategy. Iran has strengthened ties with Russia and China and reduced tensions with regional neighbors like Saudi Arabia, improving its strategic position. However, Iran’s relations with Europe have declined. The European Union, previously hesitant to enforce Trump-era sanctions, is now more hawkish due to the Ukraine war and Iran’s supply of drones and missiles to Russia. Recent EU actions, including sanctions on Iranian airlines and shipping companies, reflect this shift. European leaders have also threatened to trigger the JCPOA’s snapback mechanism if Iran does not agree to a new nuclear deal. Tehran’s immediate goal is to maintain negotiations with Europe until October 2025, when the snapback mechanism is set to expire.

Iran can also further leverage its nuclear threshold status by threatening — and potentially taking — steps toward weaponization. In recent months, Iranian officials have explicitly stated that if Tehran is cornered, it may reconsider its deterrence strategy, which currently prohibits the acquisition of nuclear weapons. U.S. officials believe that Iran has not made a political decision to pursue a nuclear bomb, and many observers interpret these threats as a bargaining tactic.

Despite setbacks following the events of Oct. 7, 2023, Iran’s regional allies retain the capacity to disrupt global oil flows at key choke points, such as the Red Sea. Iraqi militant groups, in particular, play a dual role: exerting pressure on regional actors to maintain Iran’s oil exports and assisting in oil sales disguised as Iraqi-origin oil.

Domestically, the Islamic Republic faces widespread discontent across social strata that could deepen under external pressure. The regime, however, appears prepared to suppress protests should renewed sanctions intensify unrest. At the same time, external pressure could also generate a rally-around-the-flag effect, fostering greater elite cohesion and hardening the regime’s stance.

In parallel with its signals of flexibility in negotiations, the Islamic Republic also appears willing to adopt a risk-taking approach to resist U.S. pressure, as many regime elites fear that conceding to Trump’s demands would be worse than fighting back, akin to “committing suicide out of fear of death.”

Should the Trump administration pursue a grand bargain with Iran, Tehran may interpret this as a diversion from what it perceives as Washington’s true intention: regime change. Iranian officials have repeatedly asserted that U.S. calls for negotiations are a deceptive ploy to lower Iran’s defenses and maximize pressure. In a recent speech, Supreme Leader Ali Khamenei underscored this view, citing not only Iran’s historical experience but also Syria as the latest “victim” of the U.S.’ duplicitous diplomacy. Khamenei believes Assad faltered because he trusted promises and offers from the U.S. and its allies, weakening his ties with the Axis of Resistance.

Nevertheless, Iran is not unfamiliar with the concept of a grand bargain. In 2003, Tehran reportedly proposed a comprehensive deal to the United States that offered “full cooperation” and transparency on the nuclear issue, support for the Arab League’s 2002 “land for peace” initiative regarding Israel-Palestine, and a commitment to transition its non-state allies, such as Hezbollah and Hamas, into political entities. The U.S. refusal to engage with this proposal — dismissing it as not credible—deepened Iran’s skepticism regarding Washington’s commitment to lasting agreements, a doubt that was only reinforced by the U.S. withdrawal from the JCPOA.

For the Trump administration to overcome this deep mistrust and credibly signal its intentions, it may need to demonstrate bipartisan commitment. Involving the U.S. Congress, for example, could help assure Iran that any deal is durable and not merely a tactical effort to strip Tehran of its leverage before pursuing regime change. Otherwise, the initiative would likely be perceived as a nonstarter, designed so that Iran's rejection could enable the United States to build international consensus for its maximum pressure policy.

Conclusion

Officials around the world, including in Iran and the Gulf States, are prepared for the return to office of a president whose mercurial nature and transactional approach to the policy process is well known and, to the degree possible, has been “priced in” to decision-making. In the absence of a major change in U.S. strategy toward Iran — moving toward direct dialogue or outright war — it would appear that the Trump administration’s options are similar to those that faced President Joe Biden. Are the benefits to be gained from tightening sanctions and ratcheting up conflict with Iran worth the costs of Iranian retaliation? Is there confidence that an escalatory cycle with Iran can be contained and/or managed, and not result in an Iranian nuclear breakout and weaponization? If not, there may be more of a continuation of a U.S. policy that stays the Biden course under Trump with minor adjustments.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.© 2024 Rice University’s Baker Institute for Public Policy