This brief is part of a series of policy recommendations for the administration of President Joe Biden. Focusing on a range of important issues facing the country, the briefs are intended to provide decision-makers with relevant and effective ideas for addressing domestic and foreign policy priorities. View the entire series at www.bakerinstitute.org/recommendations-2021.

The year 2020 was momentous and historic for many reasons. The world has faced and is still working to emerge from the global COVID-19 pandemic. The United States has transitioned to a new administration at a point when public opinion is more polarized than ever. The U.S. Congress and the new administration will have difficult economic policy decisions to make, which will necessarily require tradeoffs. This CPF transition policy brief focuses on U.S. deficits and debt. We highlight the unsustainability of the current debt trajectory and key policy levers that both Democrats and Republicans might use to stabilize the U.S. fiscal situation. Finally, we propose three main dimensions on which fiscal policy proposals should be evaluated to ensure transparency, fairness, and sustainability.

Unsustainable U.S. Deficits and Debt

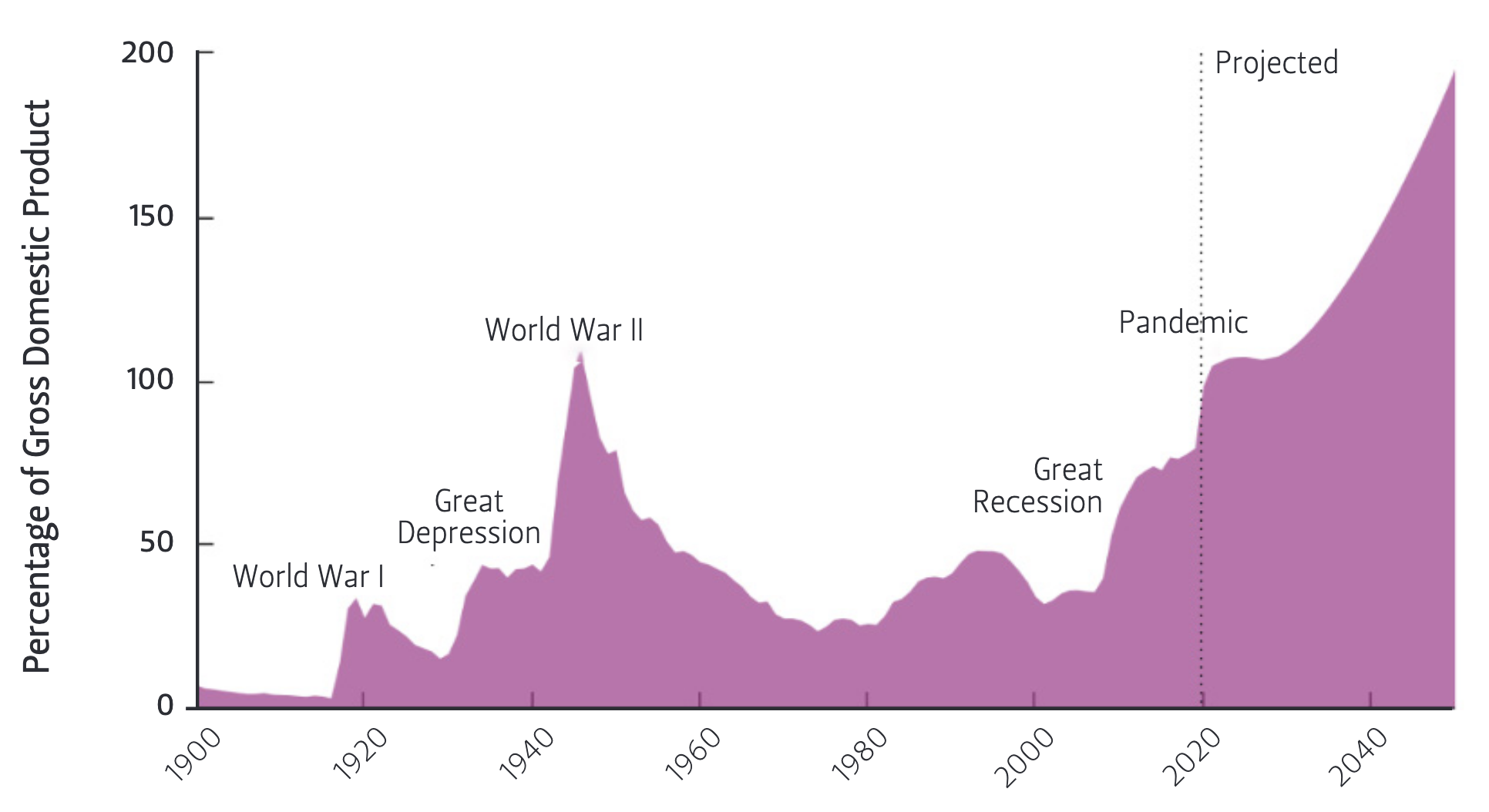

As the economy recovered from the 2008 mortgage security crisis and the resulting Great Recession, U.S. debt held by the public rose from 47% of GDP in 2009 to 80% of GDP in the first quarter of 2020.

The U.S. debt at the beginning of 2020 was still less than the maximum levels of more than 106% of GDP at the end of World War II. However, at the beginning of 2020, the U.S. publicly held debt was projected by the Congressional Budget Office (CBO) to increase to 144% of GDP by 2049. By September 2020, the revised CBO forecast for U.S. publicly held debt rose to 195% of GDP by 2050.

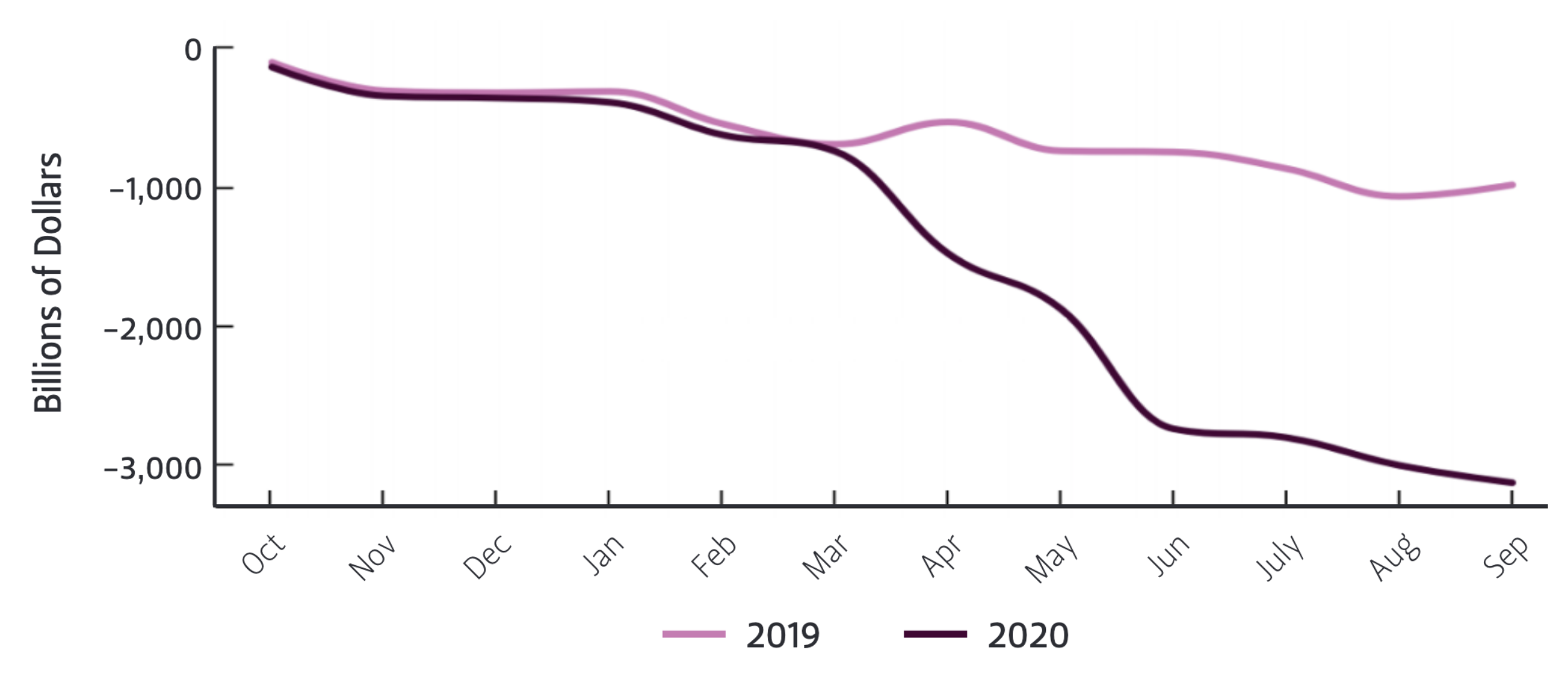

The coronavirus began hitting the United States in late February and early March 2020. Not only has the pandemic reduced output and employment in the United States, but it has also induced stimulus policies such as the $2.2 trillion CARES Act, an extensive lending program for a broad range of nonfinancial institutions, a $900 billion pandemic relief bill in late 2020, and a proposed $1.9 trillion Biden stimulus plan for early 2021. U.S. deficits ballooned beginning in March 2020. By September 2020, the cumulative deficit was $3.1 trillion—more than triple the cumulative deficit of $984 billion from September 2019—causing the increased debt projection of 195% of GDP by 2050.

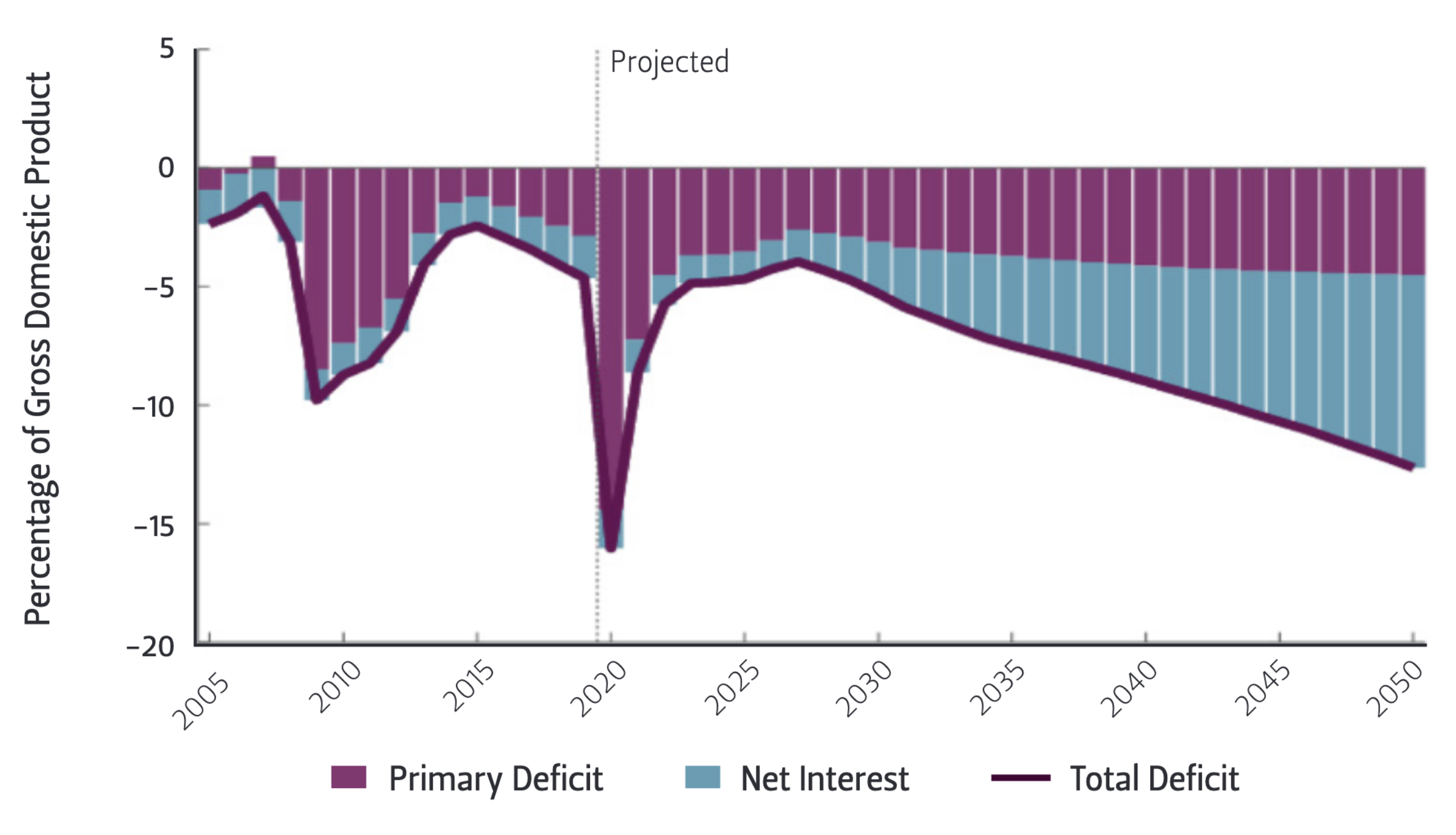

As shown in Figure 3, the primary deficit is projected to return to more moderate levels after 2020. However, the large increases in the deficit will be driven primarily by the increasing net interest payments on the debt between now and 2050. To stabilize U.S. deficits and debt, policymakers will face difficult tradeoffs that involve combinations of increased taxes, decreased spending, and efforts to foster economic growth.

Figure 1 — Federal Debt Held by the Public (1900 to 2050)

Figure 2 — Monthly Cumulative Deficits (FY 2019 to 2020)

Figure 3 — Total Deficits, Primary Deficits, and Net Interest

Note Primary deficits or surpluses exclude net spending for interest.

Policy Levers

Recent fiscal policy parameters proposed or changed in the last four years include the following. This is not an exhaustive list but rather a menu of the most likely options.

- Marginal tax rates on personal income tax brackets

- Welfare credits such as earned income tax credit (EITC) or child tax credit (CTC)

- Payroll tax limits, limitations on itemized deductions

- Estate tax, dividends tax, capital gains tax, value added tax, carbon tax

- Corporate income tax, capital expensing/ depreciation rules

- Defense spending, infrastructure spending

- Healthcare reform (Medicare, Medicaid), Social Security reform

Three Dimensions of Analysis

The political process tends to prioritize short-term benefits at the expense of long-term considerations. Any stabilizing fiscal policy changes mentioned above or otherwise should be accompanied by clear projections of the costs and benefits in the short-run, long-run, and across different parts of the distribution of households and businesses.

In other words, robust policy responses should include the following considerations:

- Short-run effects

- Long-run effects

- Distributional effects (households and businesses)

Both the Joint Committee on Taxation (JCT) and CBO regularly provide short-term and long-term estimates of the revenue and macroeconomic effects of tax and spending policy changes. The JCT and CBO also often provide distributional analyses of the effect of policy on households by income group. Other organizations can provide distributional analyses that show the effects of policies on other household dimensions such as age or on business dimensions such as industry and firm size. For this reason, analyses by nongovernmental entities and think tanks, including CPF’s modeling initiatives, add important perspectives regarding the costs and benefits of fiscal policy reforms.

Conclusion

The current fiscal path of the U.S. economy is not sustainable. The new administration has an opportunity to work with Congress to enact bipartisan legislation that addresses the hard decisions and tradeoffs involved. If the policymakers are transparent about the costs and benefits of these policies in the short- term, long-term, and across the different types of U.S. households and businesses, then those policies are more likely to be representative of the preferences of their constituents. The Center for Public Finance at Rice University’s Baker Institute for Public Policy will continue to provide analyses that cover these three dimensions of evaluation.

References

Dahl, Molly. 2020. The 2020 Long-Term Budget Outlook. Congressional Budget Office, September 21. https://www.cbo.gov/publication/56516.

Topoleski, Julie. 2019. The 2019 Long-Term Budget Outlook. Congressional Budget Office, June 25. https://www.cbo.gov/publication/55331.

Sauter Regan, Dawn, Jon Sperl, and Jennifer Shand. 2020. Monthly Budget Review: Summary for Fiscal Year 2020. Congressional Budget Office, November 9. https://www.cbo.gov/system/files/2020-11/56746-MBR.pdf

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.