Author(s)

The following paper was distributed by Energy Futures Initiative (EFI) in April 2023 as part of a working group study. The full workshop report can be found on the EFI website.

Abstract

This paper seeks to elevate some important points regarding the future of US natural gas. Broad goals for economic development, environment, and energy security will define the global future of natural gas, and some regions will inevitably chart different courses than others. US natural gas can play an important role if it is accessible, its environmental performance is verifiable, and the market continues to operate with the transparency that has driven it to become the largest and most liquid regional gas market in the world.

Changes in production, consumption, and trade over the last 20 years have motivated a radical shift in the US natural gas landscape, with LNG exports taking center-stage in the last 5 years. The interest in US LNG exports is market-motivated, and recent geopolitical events have prodded new global gas market realities that favor US exports. The rapid growth in LNG exports over the last 5 years alongside the currently high utilization rates of US LNG export terminals indicate the desirability of US-sourced LNG supplies.

Domestically, the geographic distribution of production growth – in particular the Marcellus and Utica shales in the Mid-Atlantic and the Permian basin in New Mexico and Texas – has created challenges to develop new infrastructure to serve domestic demand and support LNG exports. This has highlighted the importance of a deeply interconnected North American market to ensure regional price dislocations are minimized and regional gains from trade are accessible across North America.

Several different analyses have been commissioned by the US DOE to make a public interest determination regarding US LNG exports. Every study has identified a net gain from trade across a wide range of different scenarios considered, and the net benefits increase with resource availability. While often framed in context of a larger resource base with more elastic cost-of-supply, this also indicates that anything that impedes the development of connective infrastructure will reduce net gains from trade.

As global energy markets continue their inexorable transition to a lower GHG future, sources of energy supply that are competitive, accessible, and environmentally favorable will thrive. This is exactly where US natural gas can find its comparative advantage.

1. Introduction

The global energy industry is undergoing dramatic change. Technological change, environmental preference, the ever-present role of geopolitics in energy trade and energy access, and energy security all dominate current discourse. Uncertainty abounds.

Over the last two decades, technological and process innovations unlocked unconventional oil and natural gas resources in the US, radically shifting the global energy paradigm by making the United States the fastest growing oil and gas producer in the world. At the same time, strong economic growth in China, India and other developing nations have brought significant growth in energy demand, with profound implications for energy trade. Together, these two developments – which are, at their core, innovation and growth – have been the largest sources of structural transition in the global energy system over the last 30 years. So, it stands to reason that innovation and growth should be at the center of understanding what will drive change over the next 30 years.

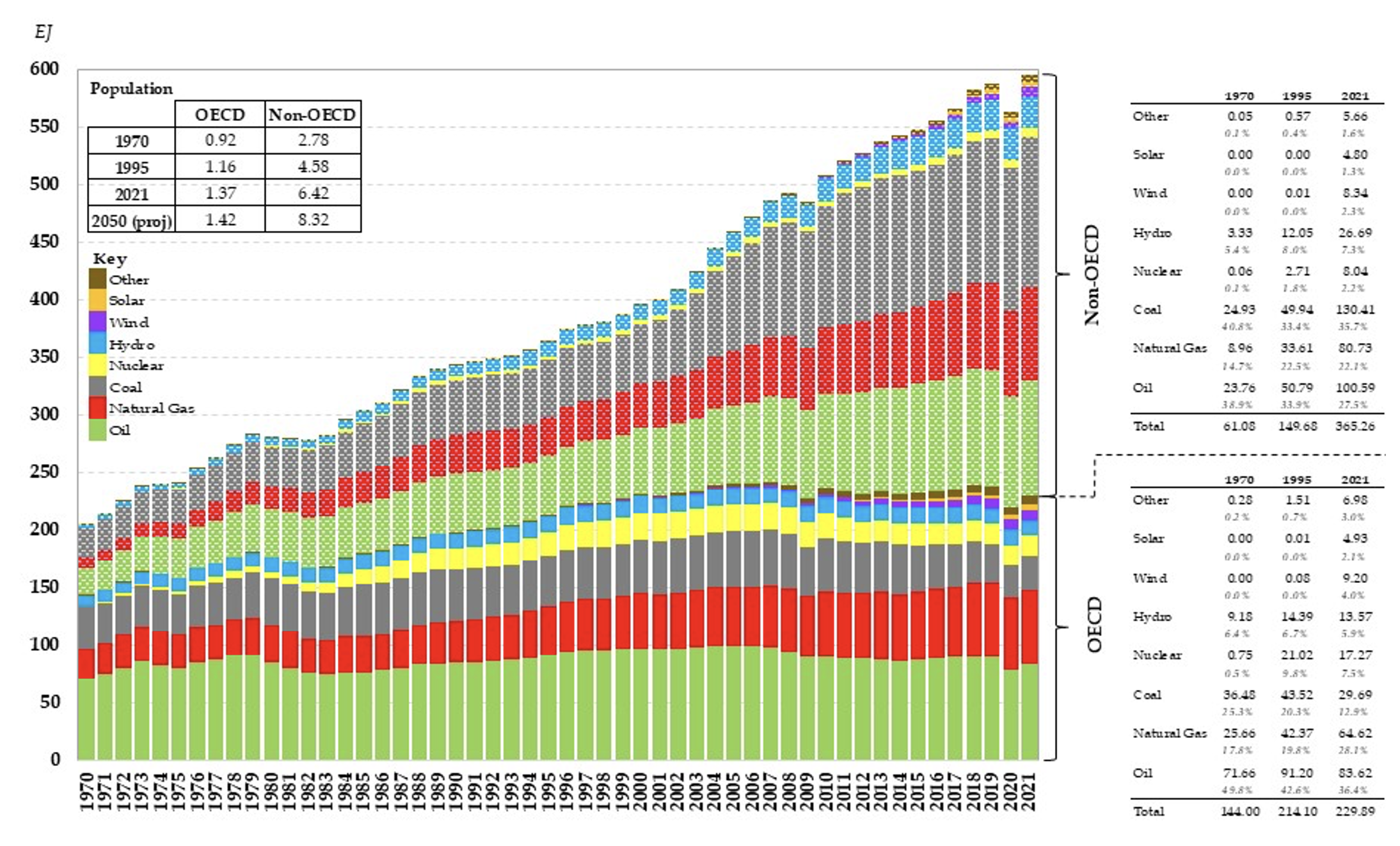

On a global scale the share of crude oil, natural gas and coal collectively accounted for 82.3% of global energy demand in 2021 versus 85.6% in 1995 and 93.3% in 1970. Despite the decline in share, demand for the fuels increased by 62.6% from 1970 to 1995 and another 57.2% to 2021 (see Figure 1). Natural gas demand has increased more than 4-fold since 1970, with demand in the developing world (non-OECD) increasing almost 10-fold.

Over the last several years environmental policy and technological innovation has propelled wind and solar energy growth in the US and Europe. Coupled with a significant increase in natural gas use, the consumption of coal in those regions has fallen, driving a decline in CO2 emissions. Thus, natural gas has already played a role in reducing CO2 emissions, but the work is not yet done. Indeed, pledges to achieve net-zero CO2 emissions have multiplied rapidly. In the US, policy has evolved to support a portfolio of different solutions.[1] Some of these provisions favor natural gas, others do not. There are a number of different low-carbon strategies that reflect the aspirations of investors, policy support, and comparative advantages. Natural gas is an integral part of many of these strategies.

Figure 1 — Global Energy Use by Primary Source, OECD and non-OECD, 1970-2021

Natural gas has potential to reduce the CO2 footprint of energy systems in developing nations in Asia who are heavily dependent on coal, much as it already has in developed nations in the US and Europe. Whether or not natural gas fulfills this potential depends on (1) access to resources and (2) the demonstrated environmental performance of supply chains. Each of these is tightly linked with the availability and performance of infrastructure. Thus, sufficient investment and proper maintenance and operation are critical.[2]

As energy systems evolve to include new technologies – such as hydrogen and greater renewables – natural gas has a role to play as a feedstock and as a balancing resource. Its longevity in these roles will depend on its commercial value proposition. For instance, is natural gas with CO2 capture a more cost-effective feedstock for hydrogen or ammonia production? Is natural gas a more cost-effective option for balancing services on electricity grids than long-duration electricity storage options? The answer will ultimately depend on price, as a higher natural gas price reduces commercial viability relative to alternatives.

Regardless of what transpires, natural gas will likely persist in the energy system for decades. Even as new technologies offer competitive options to the services natural gas provides, time is required to develop the supply chains and infrastructure needed to displace natural gas from its current uses. Moreover, if natural gas demand is reduced, its price will decline, thus discouraging rapid demand destruction, all else equal.

The geographic distribution of natural gas resources relative to existing and emerging demands raises some very interesting questions about how global LNG markets will continue to evolve. Without doubt, the depth of LNG trade has increased substantially over the last 20 years, with the emergence of the US as a large LNG exporter since 2015 representing a game-changing shift.[3] How the global natural gas market evolves in the face of geopolitical strife, trade disputes, regional conflict, sanctions, energy security concerns, and net-zero targets is an open set of questions. But, to be sure, the answers will carry significant bearing for US LNG exports.

This paper is meant to elevate a conversation about the future of natural gas, from a US market perspective. There is diversity in regional and international perspectives rooted in goals for economic development, environment, and energy security, with some goals taking higher priority in some regions than others. US LNG exports stand to have an impact on regional energy transitions, but the extent is unclear. As such, this paper is organized as follows. We begin with a discussion of natural gas and the complexities of energy transitions. This is important context for understanding the potential role of natural gas, and provides motivation for a look at the US natural gas market and a multi-faceted discussion of US LNG exports – past, present and possible future. We then raise environmental concerns that must be addressed prior to closing. At different points in the text, we also shed light on the process and timeline for constructing LNG export sites and obtaining permits, identify issues that have arisen in this process, discuss the linkage between domestic supply and exports (today and in the future), expand on the market implications of constraints, and present thoughts on the path forward.

2. Natural Gas and Complexities of the Energy Transitions

The global energy challenge is, in short, the task of meeting energy demands in an environmentally sustainable manner while not compromising energy security and economic growth. The geopolitical tumult that accompanies this challenge is potentially profound, and will shape, and be shaped by, the evolution of energy markets. Demand, supply, trade, policy, and geopolitics are all are interconnected and critical to the future of global energy.

As energy markets transition, the roles of legacy, scale and technology are critical to defining what the future will bring. First, legacy is defined by existing infrastructures, energy delivery systems, and market designs, and it is the foundation on which change will be built. Moreover, legacy is different everywhere, having been influenced by regional comparative advantages. Second, scale matters because energy systems are large and must accommodate energy affordability and reliability, and be able to support continued economic growth. Finally, technology along the entire supply chain constantly evolves, and ultimately determines how energy sources will compete.

Capital investment is the vehicle for developing new legacies at scale and for the deployment of new technologies. Capital chases returns, and long-term returns are dictated by the principle of comparative advantage. As such, future investments and efforts to decarbonize energy systems will look different everywhere, dictated by a broad set of “resource” endowments – nature, minerals, energy, human capital, etc. Accordingly, lowering the carbon footprint of energy systems will require multiple solutions, including net decarbonization of incumbent supply chains, especially given the scale of existing energy systems. In the end, economics matter, and the principle of comparative advantage is key to any cost-benefit calculus.

The significant role of natural gas in the current US energy system is directly tied to expansive infrastructures to produce, move and use it in multiple end-use sectors. In general, the massive fixed costs associated with delivering energy services make displacing incumbent energy sources a very capital-intensive endeavor. Thus, natural gas is likely to remain a part of the national (and global) energy mix for decades to come. However, the extent to which natural gas remains in play will hinge on the environmental sustainability of the supply chain, so incumbent natural gas market participants will need to reduce their net environmental footprints.

Events over the last two years have served as an acute reminder that energy prices matter to policymakers, industrial consumers, and the general public. Since the re-opening of the world’s economies in the wake of the COVID-induced shutdowns in 2020, rising energy prices have led to calls from policy-makers for more investment in new production, in many cases from the same policy-makers that previously sought to phase out hydrocarbons. Since the beginning of 2022, with heightened geopolitical tensions spurred by the war in Ukraine, energy security has risen to the top of national concerns, thus highlighting the continued prominence of crude oil and natural gas in economic, security, and environmental policy considerations. The schizophrenic nature of discussions about the future role of hydrocarbons creates uncertainty for investors across the entire supply chain – from production to transport to delivery for end-use. Uncertainty is negatively correlated with investment, which is deleterious to long-term market stability.

One of the oldest lessons for enhancing energy security is diversity of supply – both in terms of the diversity of fuels to provide energy services and the diversity of suppliers for any single energy source. Placing too much of a region’s energy fortune on either one energy source or one supplier exposes the region to higher risk of disruption, and history has taught that energy disruptions are highly correlated with macroeconomic dislocations. As such, energy security has historically been a central consideration to policy-making, with different regional approaches prioritizing domestic energy sources whose supply chains are less exposed to being influenced by international events.[4] The energy crisis in Europe has provided the world with a stark reminder of the importance of affordable and reliable energy.

Financial sustainability is also critical for long-term energy solutions. Delivering energy services involves a supply chain that connects raw material inputs to conversion processes to end-uses. All costs along a supply chain matter. If an energy resource requires development of new supply chains, then the resource may face burdensome fixed costs, effectively stranding it.[5] Thus, an ability to leverage legacy infrastructures, or develop new infrastructures at low-cost, reduces development hurdles. So, a full supply chain approach is required for successful integration of energy sources and technologies.

Market structure also matters. Market liquidity creates support for investments along supply chains. When there are many market participants (i.e., market depth and liquidity), investments along the supply chain face lower transaction risk, which, in turn, facilitates greater levels of investment.[6] In this context, the US natural gas market is in a favorable position[7] – it is competitive, the majority of resources are privately owned, and investments are dictated by market conditions. The competitive nature of the US market is attractive to international investors who wish to diversify their sources of supply while minimizing the risk of disruption from State interference.

Given the attractiveness of US-sourced natural gas to international buyers, its role in assisting energy security, its impact to-date on CO2 emissions from US power generation, and accelerating efforts to reduce GHG emissions everywhere, an important question to ponder is, “How will US and global decarbonization efforts impact domestic and foreign investment in US natural gas and LNG supply chains?”

3. The Evolving U.S. Natural Gas Market

The evolution of the US natural gas industry over the last five decades is a story of policy and regulatory shifts that have unleashed market forces. The Natural Gas Policy Act (NGPA) of 1978[8] set in motion a series of changes that resulted in the US natural gas market becoming the most liquid, efficient natural gas market in the world. This, in turn, unlocked pathways for production growth, pipeline capacity investment, and demand growth, largely because price is now formed in a transparent, competitive market.

Prior to the NGPA, natural gas sales prices on interstate pipelines were controlled. Thus, producers often chose to sell to intrastate buyers first, thus contributing to shortages in states that did not have robust natural gas production. Price controls were ultimately eliminated so that prices could adjust to reflect a market-clearing supply-demand balance.[9] The NGPA also assigned authority to the Federal Energy Regulatory Commission (FERC) to regulate interstate natural gas movement. Over the next two decades, a series of FERC orders, culminating with Order 636,[10] completed the process of market restructuring.[11] Capacity rights were unbundled from pipeline ownership, and pipeline information was mandated to be openly published to establish transparency to support open market function.

A. The Role of Liquidity

Transparency spawned the emergence of regional spot and futures (both “over-the-counter” and on financial exchanges) markets and stimulated efficiency improvements. It also encouraged competition and opened new investment opportunities.[12] As a result, new market hubs formed as a nexus for market liquidity and price discovery, and became the locus for physical and financial transactions. Hub services developed – including services such as parking, loaning, peaking, and balancing – and new physical and financial risk management capabilities evolved.

A hallmark of flexibility, hubs across the country have evolved in producing areas, in demand regions, in storage regions, and at points of significant pipeline interconnectivity. A critical lesson borne out by the evolution of the US natural gas market is that competition increases efficiency, encourages investment, and drives market development.

The liquidity of the US market has allowed buyers of natural gas to access supplies directly from pipelines while indexing purchases to regional market hubs. Thus, buyers do not need to negotiate all the way back to the wellhead. As such, feed gas supplies for US LNG liquefaction terminals can be accessed from existing pipeline capacity. To be clear, there are interconnect agreements and infrastructures required, and these vary by facility, but the need to access supplies directly from the wellhead is abated. This stands in stark contrast to LNG supplies from almost everywhere else in the world, and it owes directly to the natural gas market structure in the US, which is a distinct advantage for project development.

Going forward, “How will evolving market structure and regulation impact foreign interest in US-sourced LNG exports?”

B. The Physical U.S. Natural Gas Landscape

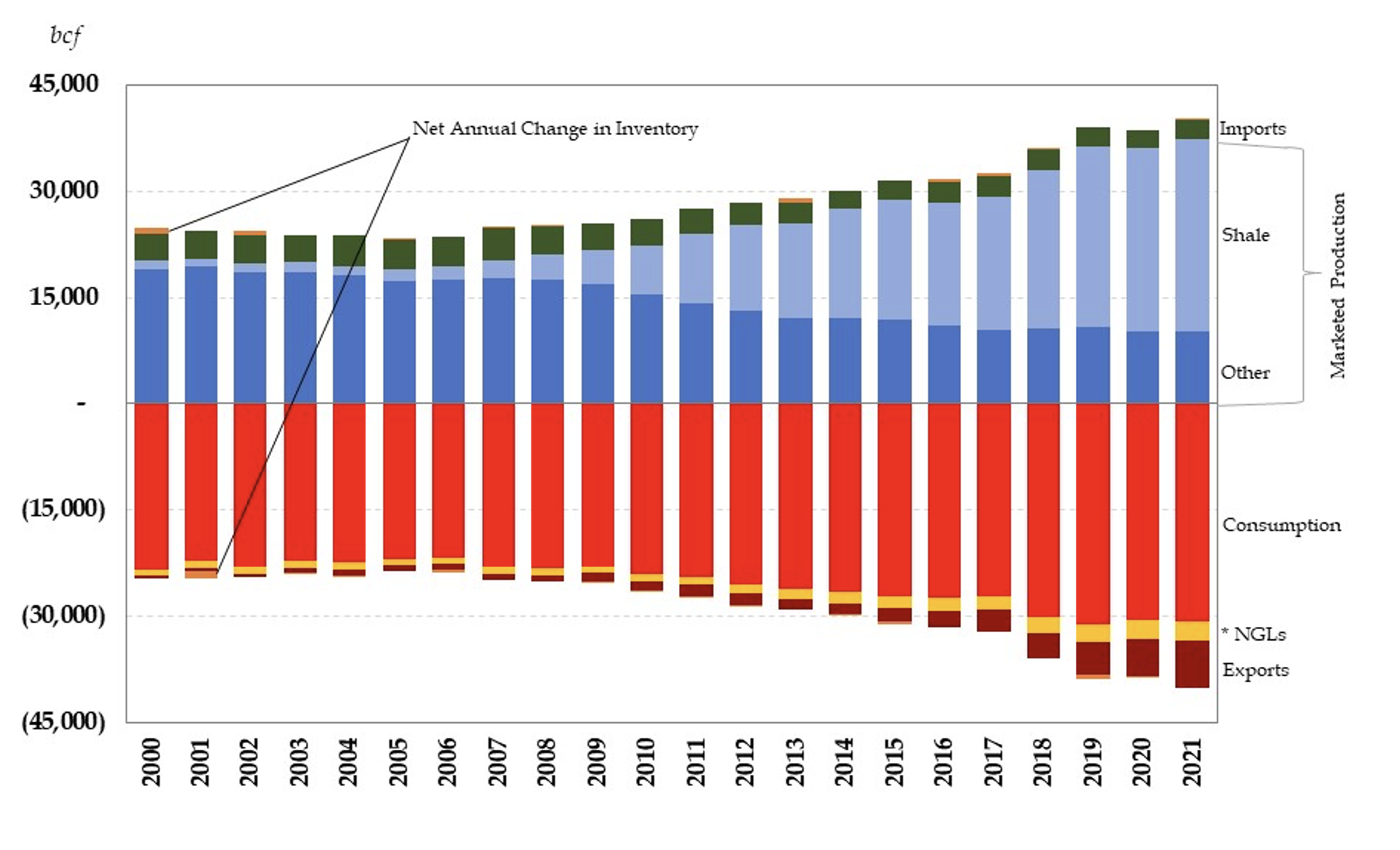

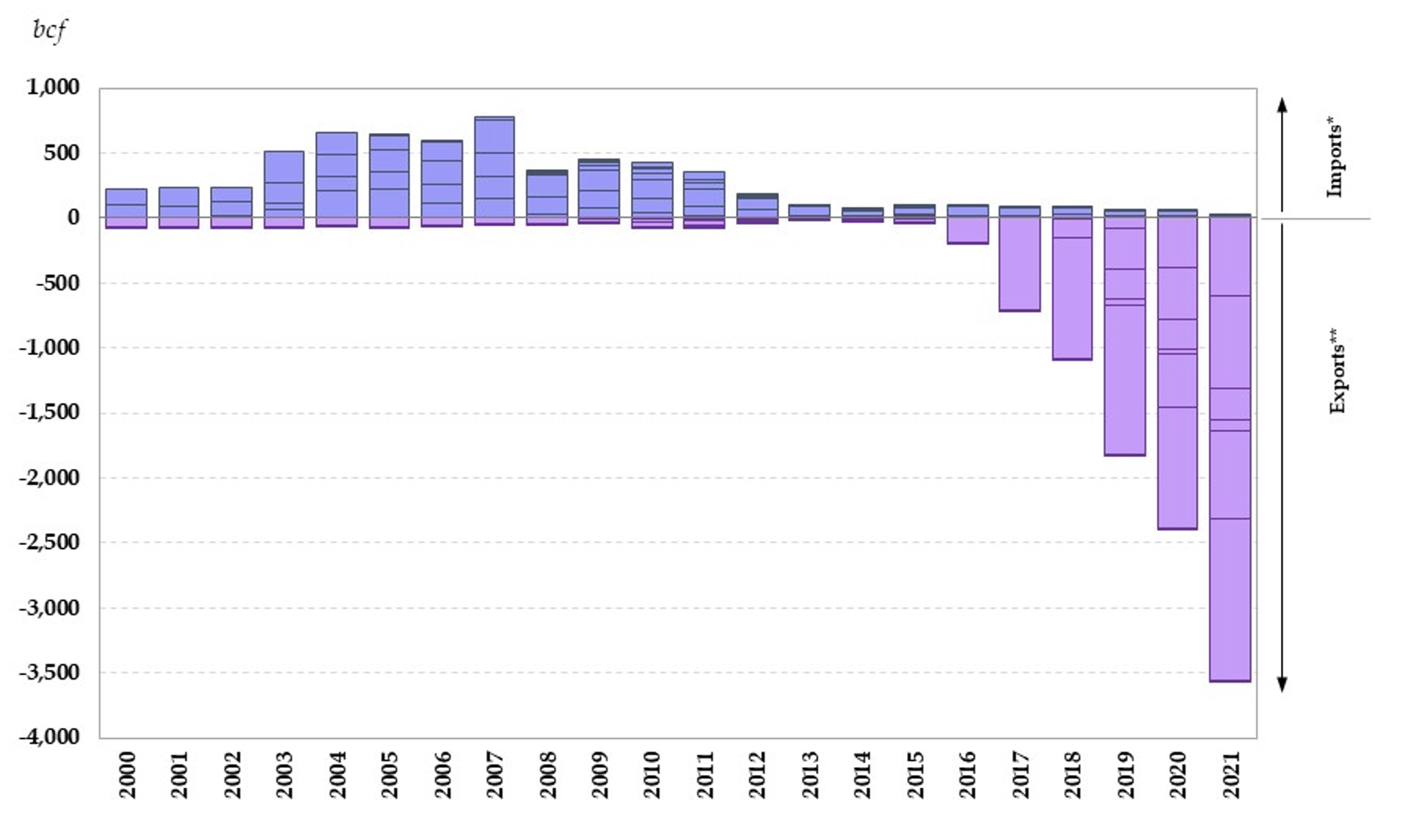

The US natural gas market is very large, accounting for 24% of global production and 21% of global consumption, in 2021. The majority of US natural gas production serves the domestic market, with growing exports (see Figure 2), about half of which is pipeline trade between the US and its neighbors (see Figure 4). In fact, the US market is deeply interconnected with Canada and Mexico, which is why it is often characterized as a “North American” market.

Figure 2 — US Natural Gas Market Balance, 2000-2021

Natural gas is also imported and exported as LNG (see Figures 4 and 7). LNG imports are primarily to the New England area, and are due to regional bottlenecks during peak demand periods resulting from insufficient pipeline capacity and a lack of local storage.[13] LNG exports have risen rapidly in recent years, primarily from export facilities in the US Gulf Coast, driven by the dramatic increase in domestic production from shale.

Given the tremendous increase in natural gas production from shale, as indicated in Figure 2, the US natural gas market has evolved rapidly. Domestically, since 2000, demand for natural gas has grown in every sector, except the residential sector where demand has remained fairly flat with year-on-year fluctuations largely due to differences in winter weather-driven heating demands. Industrial demand fell by about 25% from 2000 to 2009, but has since recovered to levels not seen since the late 1990s. Commercial sector natural gas use has grown modestly, at an average annual rate of 0.2%. The most notable shift in demand has occurred in the power generation sector, where demand has more than doubled since 2000, rising at an average annual rate of 3.7%.[14]

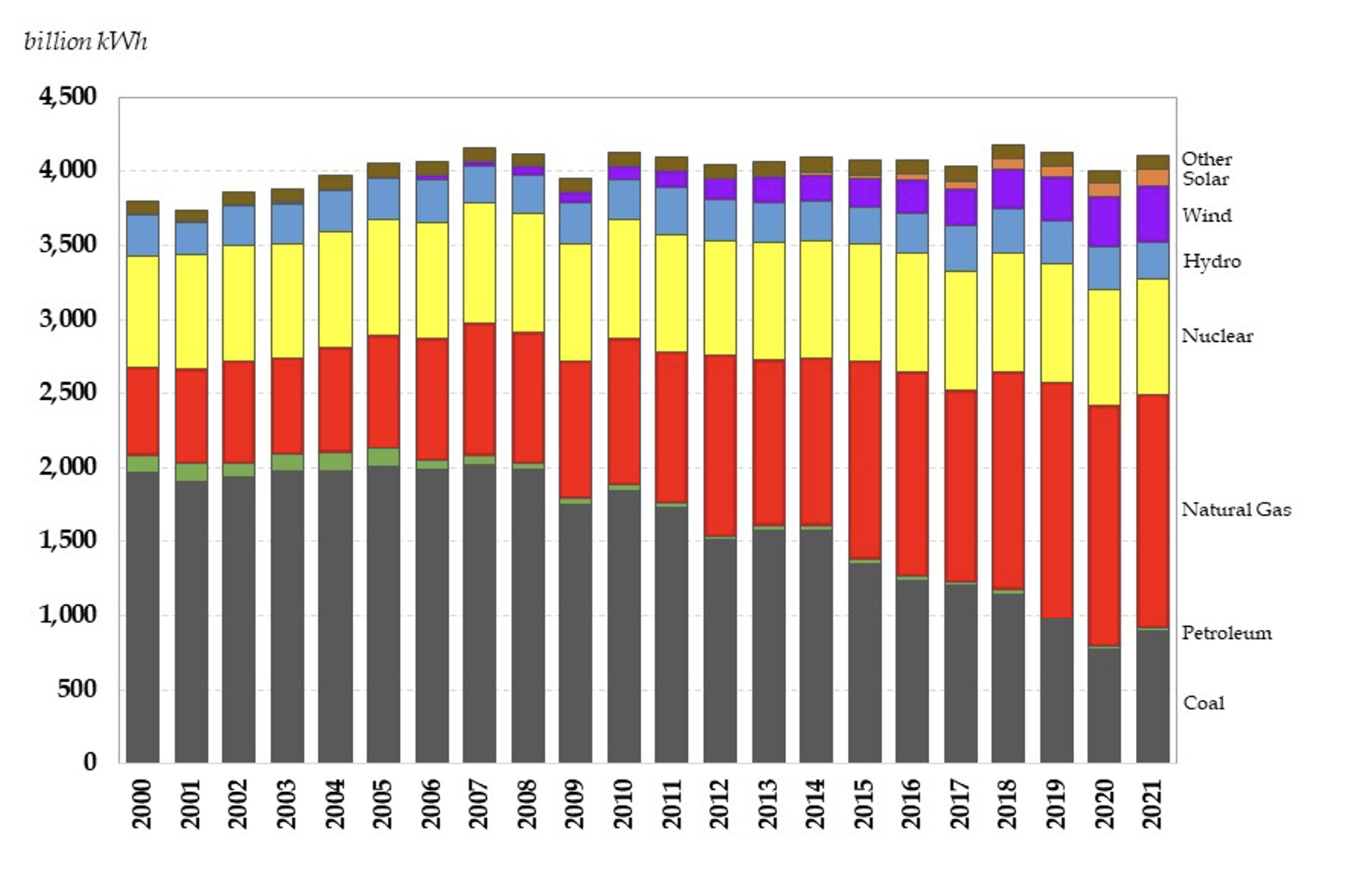

The growth in natural gas demand for power generation, most of which has occurred since 2009 (see Figure 3) concomitant with low natural gas prices, has facilitated significant retirement of coal generation since 2007 while accommodating the intermittency inherent to rapidly growing renewable generation sources.

Figure 3 — Net Power Generation by Source in the US, 2000-2021

To be clear, there remains substantial differences in the power generation mix by state,[15] which is not indicated in Figure 3, but natural gas has played a pivotal role in the transition of the US power generation sector over the last 15 years. The future role of natural gas in US power generation remains to be seen, particularly as policy continues to support renewable generation. But demands for reliability may dictate a long-term role for the balancing services natural gas can provide to grids. Nevertheless, in some regions of the US, there is an emerging conflict between regional public utility commission efforts to compensate reliability as a service and state government aspirations to move away from all fossil fuels, including natural gas.

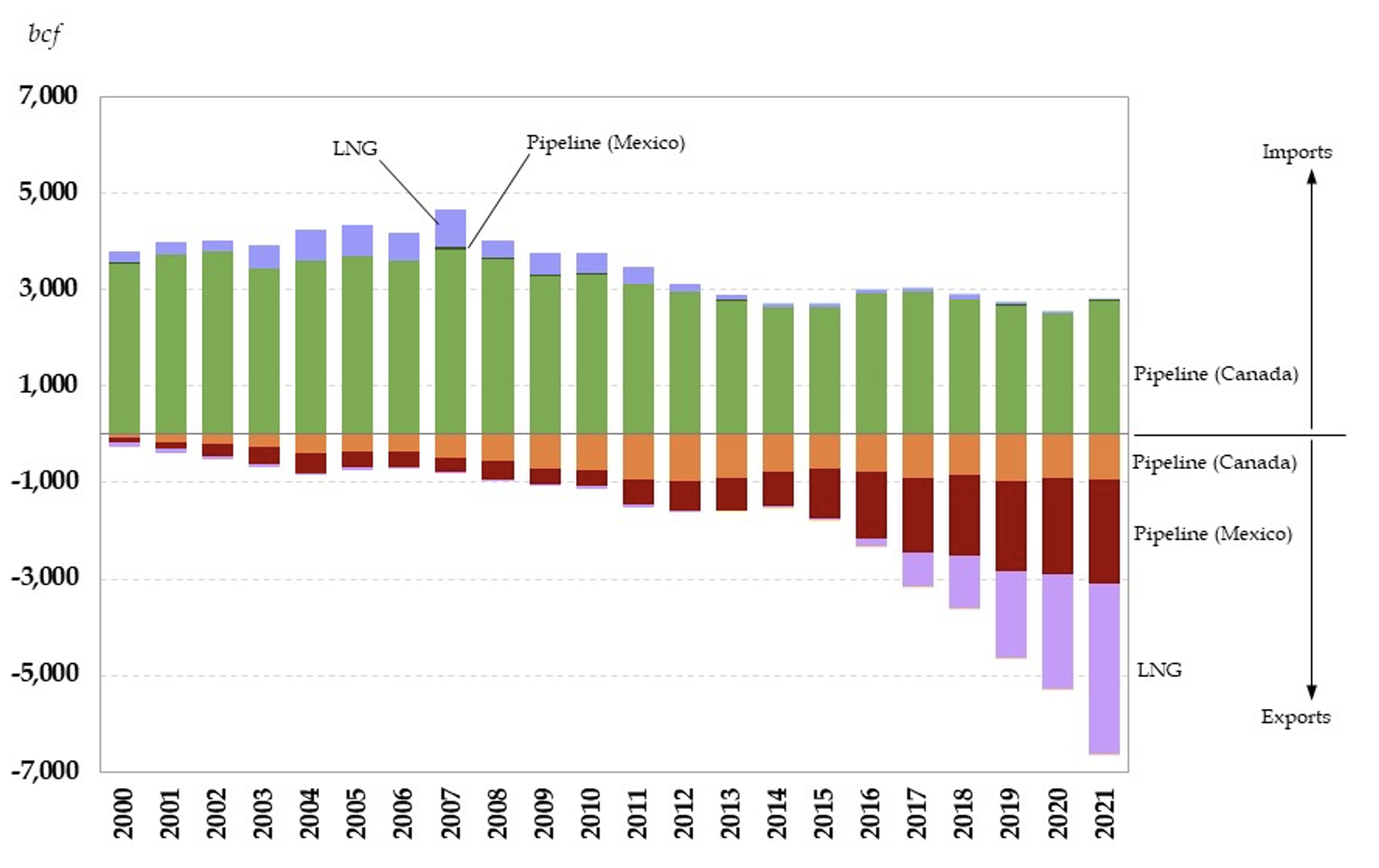

Natural gas trade has also changed significantly (see Figure 4). In the early 2000s, the US was the highest priced market in the world. This led to tremendous interest in importing LNG to the US through vertically integrated supply chains from distant locations, such as Australia and Qatar. Developers applied for, and received, licenses to import LNG to the US in concert with sinking billions of dollars overseas to develop new upstream production and liquefaction facilities. They also completed development of new LNG import capacity, which resulted in an increase in annual LNG imports through 2007.

Figure 4 — US Natural Gas Trade, 2000-2021

Source Data sourced from the US Energy Information Administration

At the same time, however, competition in the US upstream saw a large number of small producers push along a different margin of response to the high price environment – domestic shale resources. LNG imports required large upfront investments, which is why firms with large balance sheets and an international presence were well-suited to push in that direction. Domestic shale opportunities required a much lower upfront commitment, which is why smaller players capitalized along that margin. Industrial consumers shuttered some activities, choosing to offshore them thereby driving a reduction in industrial gas use, thus exercising yet another margin of response to high prices. The uncertainty regarding which path would win drove diversity across various investment paths, and history has since been written with regard to what ultimately transpired – the shale revolution was born.

While shale resources were already identified as having enormous potential, thus representing a necessary condition for increase domestic production, their technical and commercial viability was historically questioned. Technology improvements coupled with the market and regulatory structure in the US proved to be the sufficient conditions for the shale revolution.[16] As a result, the US natural gas market turned from deficiency to abundance.

In 2021, the US was a net exporter of just over 3.8 bcf/d, which is notable because as recently as 2007 the US was a net importer of about the same volume. Until 2019, the US was still a net importer by pipeline, with almost all imports coming from Canada. The US still imports gas from Canada (and remains a net importer from Canada), but pipeline exports to Mexico have grown significantly over the last decade. Since 2000, US pipeline exports to Mexico have increased over 20-fold, with the vast majority of the growth since 2010.

The radical shift in the US natural gas market over the last decade has seen exports grow from 0.1% of total available supply in 2015 to 8.9% in 2021. LNG exports totaled 3,560 bcf in 2021, representing just over half of all exports, which stood at 6,653 bcf. Moreover, LNG exports overtook pipeline exports in 2021 for the first time ever. Given the interest in US-sourced LNG from Europe and Asia and the capacity of operating plus approved LNG export terminals, it is likely that 2021 marks a new reality for US gas, one that is more focused on accessing international, waterborne markets. What remains to be seen is how Canadian natural gas will complement or compete with US natural gas. A complementary role would see greater Canadian pipeline exports to the US Lower 48 thereby backfilling the continental market to offset greater loading at LNG export terminals. If, however, pipeline constraints are present, then Canadian natural gas producers will seek other market outlets, such as LNG, and be forced to compete with US LNG in the global market.

This begs an important question, “How will development (or lack thereof) of pipelines in the North American natural gas market shape the future of US and North American market integration and exports?”

4. U.S. LNG Exports — Unleashing Market Forces

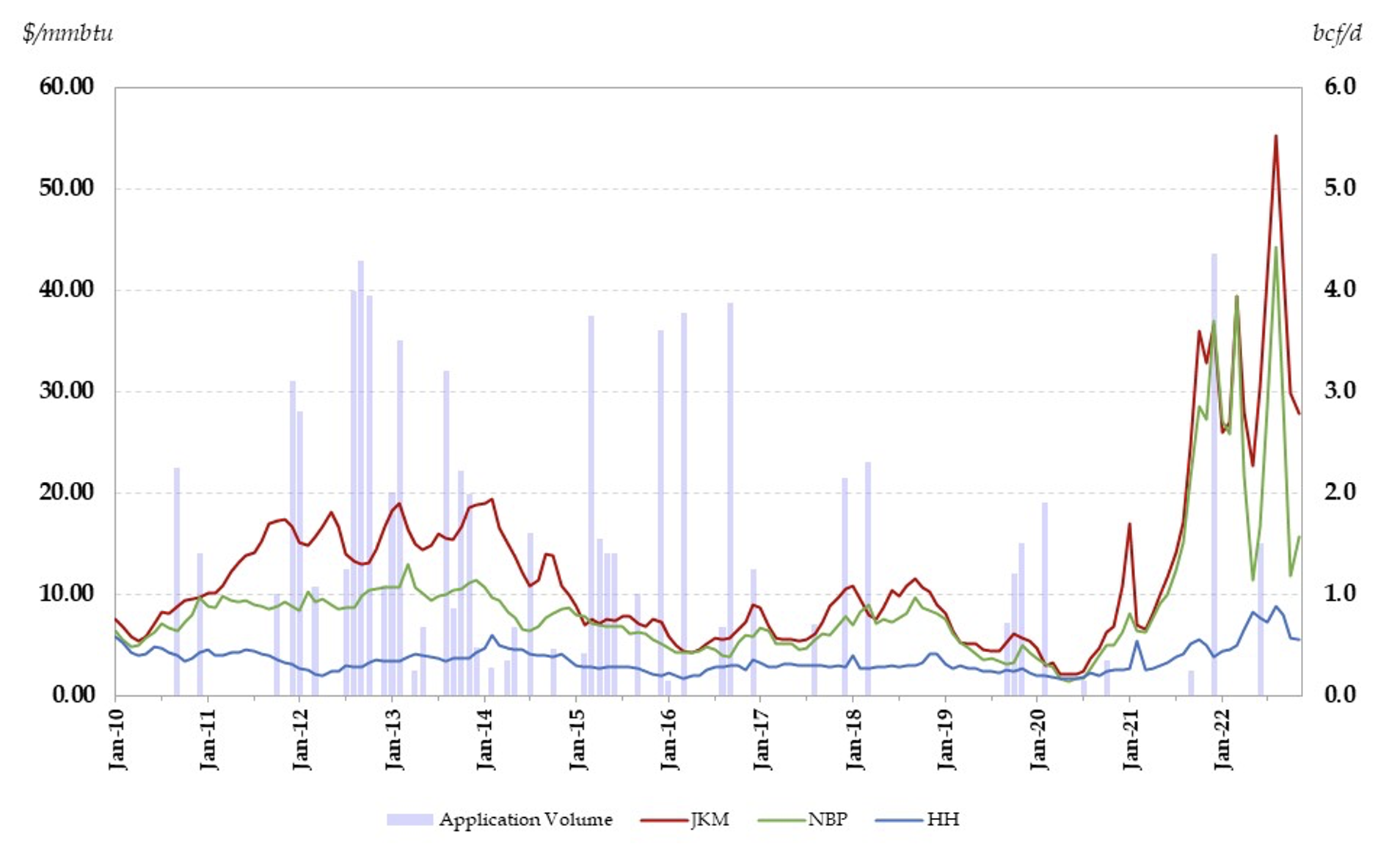

The US LNG industry has changed significantly over the last 20 years. As shale production increased, imports became less necessary. Then, international price dislocations (Fukushima in particular) triggered immense interest in exports. In fact, when the disaster at Fukushima occurred on March 11, 2011, all of Japan’s nuclear power generation capacity was shutdown, forcing the JKM price to levels not previously seen (see Figure 5).

Figure 5 — International Prices and Applications for LNG Exports, Feb09-Nov22

The price level at JKM resulted in significant demand to move available LNG supplies toward Japan. In turn, the natural gas price increased at NBP in Europe because the marginal source of supply (LNG) was now facing extreme competition. The resulting spreads between Henry Hub and the international market triggered a wave of LNG export applications in the US – a total of 51 applications for up to 54.2 bcf/d were filed between October 2011 and December 2015. This was in addition to 3 other applications totaling 3.6 bcf/d that had been filed in the last four months of 2010.

The intense interest in LNG exports that arose in 2011 should not have been surprising. The commercial prospects of selling into a much higher priced international market were very attractive for potential LNG suppliers, and access to lower priced gas from the US was attractive to LNG buyers in Asia and Europe. Hence, the shale revolution, coupled with the transitory shock of Fukushima in the midst of growing demand for LNG in Asia, set the stage for classic gains from trade.[17]

The average spreads between Henry Hub and JKM and NBP from March 2011 through December 2015 were $10.04/mmbtu and $5.32/mmbtu, respectively. Given the average price at Henry Hub over that period ($3.47/mmbtu), such spreads would cover a full value chain outlay – from liquefaction to shipping to regasification – of between $5 billion and $14 billion, depending on where the LNG is loaded and delivered.[18] The initial applications for licenses to export were largely focused on converting import terminals into export terminals, so some of the upfront fixed cost related to terminal development was already sunk.[19] This made those sites even more attractive from a commercial perspective.

Given the price spreads seen more recently between Henry Hub and the international market, “How will US LNG exports evolve, especially considering the volumes associated with export license applications already approved and terminals already under construction?”

A. Licensing LNG Exports — The State of Play

Before LNG can be exported, the DOE is required to make a “public interest determination” to determine if the export is in the best interest of the US and its citizens.[20] Exports to countries with whom the US has a free trade agreement (FTA) are deemed to be in the public interest, so applications for a license to export to FTA countries are generally approved very quickly. A non-FTA export license requires a more arduous test for approval.

If trade with a specific country is prohibited by law, an export license will not be granted. Otherwise, when determining if a license to export to non-FTA countries is in the public interest, the DOE examines the economic and environmental impact of the proposed export project. To do this, the DOE has commissioned multiple studies examining different export levels (we return to these below) and their impact on the US macroeconomy in order to ascertain if there are net gains from trade in a general equilibrium setting. The DOE also takes into consideration different studies of environmental impact.

The process for reviewing LNG export applications, which is published in the Federal Register,[21] has evolved. Some notable steps include:

- On May 29, 2014, DOE proposed to end its practice of issuing conditional approval for exports, thereby simplifying the process. It would no longer make final public interest determinations until after completion of the reviews under NEPA.[22]

- The study, “Life Cycle Greenhouse Gas Perspective on Exporting Liquefied Natural Gas from the United States” prepared by the National Energy Technology Laboratory (NETL) in June 2014 began to be considered by DOE in its review of LNG export licenses.[23]

- On August 15, 2014, the Office of Fossil Energy at DOE published the final Addendum to “Environmental Review Documents Concerning Exports of Natural Gas from The United States” to respond to numerous concerns raised in public comments regarding the environmental impacts of shale gas development.[24] The Addendum is taken into consideration in review of LNG export licenses.

- On October 28, 2020, DOE issued an order extending export authorizations to non-FTA countries through 2050.[25]

While DOE must determine if a license to export is in the public interest, it does not authorize facility siting and construction, nor does it have jurisdiction over operations. These matters fall to the Federal Energy Regulatory Commission (FERC) for onshore and near-shore facilities.[26] A major part of the approval process for facility siting, FERC leads the environmental impact assessments of proposed export projects according to the National Environmental Policy Act (NEPA). Once FERC approves a facility, the DOE will complete its review to determine if a license to export should be granted. The license is an important step in project development as it provides a bankable authorization to export LNG and obtain sufficient contractual interest for offtake and financing for development.

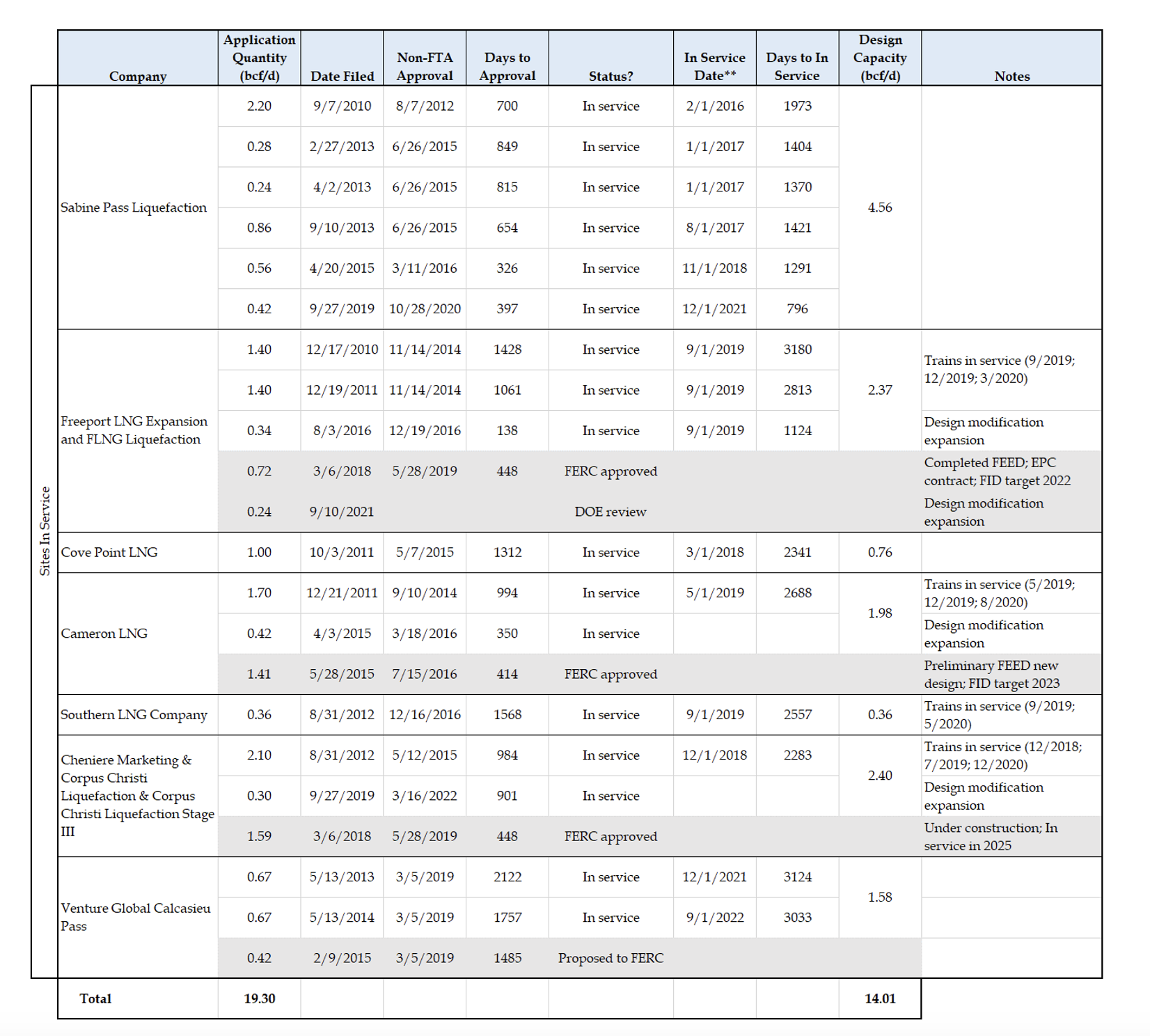

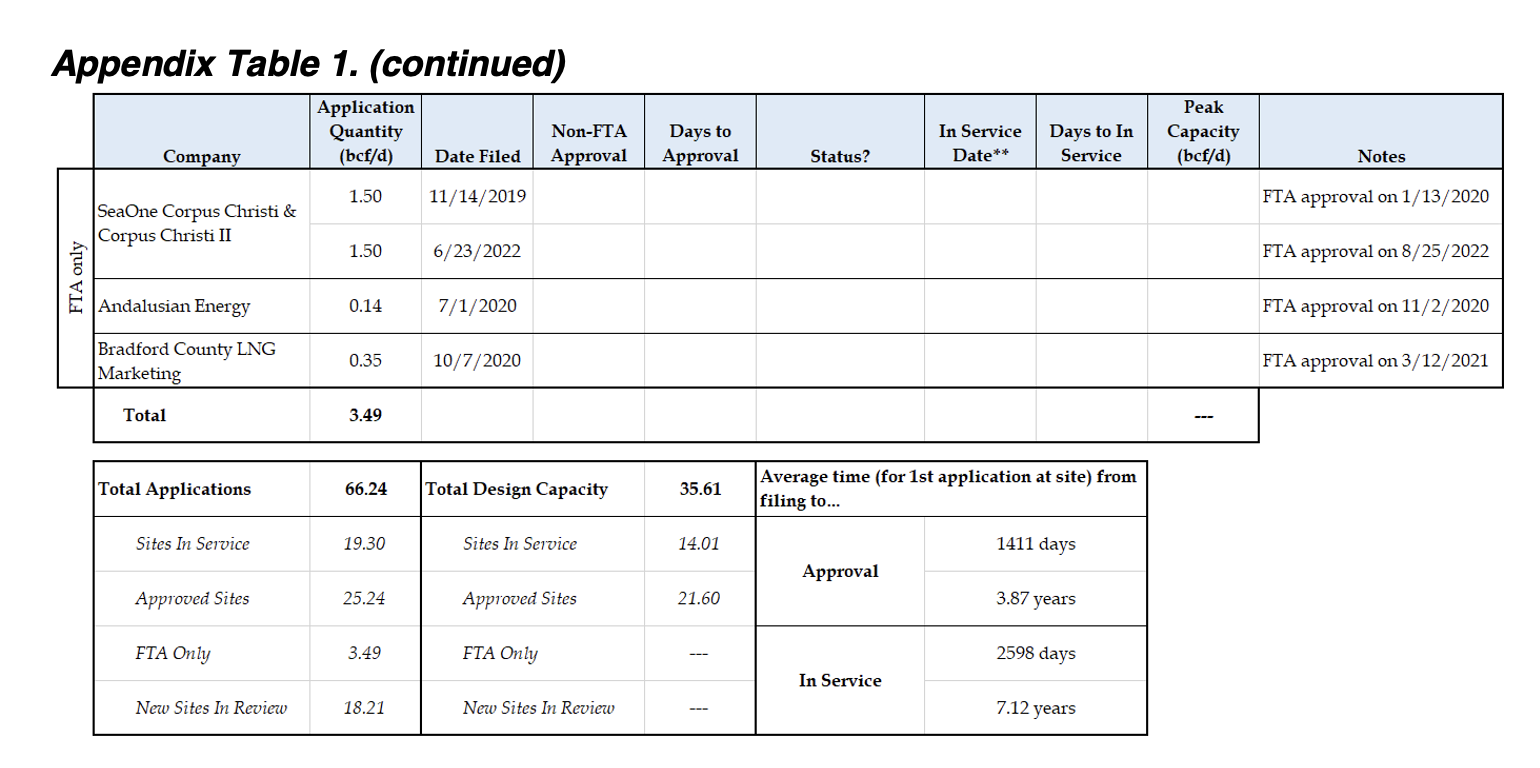

The length of time from the application for an export license to a terminal beginning commercial operation varies by location (see Appendix Table 1). Although not universal, export license approvals at brownfield sites, particularly smaller expansions, tend to take less time than the first application filed for a given site. For the first applications filed at a given site, the average time it has taken for applications to be approved for export to non-FTA countries is 1,411 days (3.87 years), with a range between 700 and 2,525 days (1.92 and 6.92 years, respectively). The average time it has taken from the date an application was filed to commercial operation is 2,598 days (7.12 years), with a range between 1,973 and 3,180 days (5.41 and 8.71 years, respectively).

Notably, the fastest time to approval then operation was Sabine Pass, which was a conversion of an existing LNG import terminal and the first site to receive approval in the Lower 48. In the other extreme, there are a handful of applications that were filed in 2013 that are still in DOE review, but in each case, DOE is waiting for the relevant environmental review under NEPA, which is in FERC’s jurisdiction. If and when these projects are finally approved, the time from application to approval will certainly be longer than the historical average referenced above. In addition, once projects currently under construction begin operating, the time from application to commercial service will end up being greater than the historical average. For example, Golden Pass is slated to begin commercial operations in 2023, which will be more than 10 years after the application for export was filed.

Of course, the long lead times for commercial operation do not fall entirely on the shoulders of DOE and FERC. Shifting market conditions have also played a role, as softening global LNG prices after 2015 resulted in a market where buyers began to demand more flexible, shorter duration contract terms.[27] For an LNG supplier looking to secure offtake for 20 or more years to underpin project finance, this presented a dilemma for certain projects. Interestingly, recent market conditions have spawned a renewed interest in longer duration contracts, although inflation and higher interest rates present a different challenge for project finance. Where this leads for project development in the US remains to be seen, especially given the existing queue of projects.

Regardless of the reasons, the extensive amount of time it takes to receive approval for export then begin commercial operation is concerning for any project developer. Given the time to build a greenfield export facility, many of the newer projects still awaiting approval will not likely be operational until sometime in 2027/28, at the earliest. This tends to favor expansion at sites already in service, and conveys a distinct first-mover advantage.

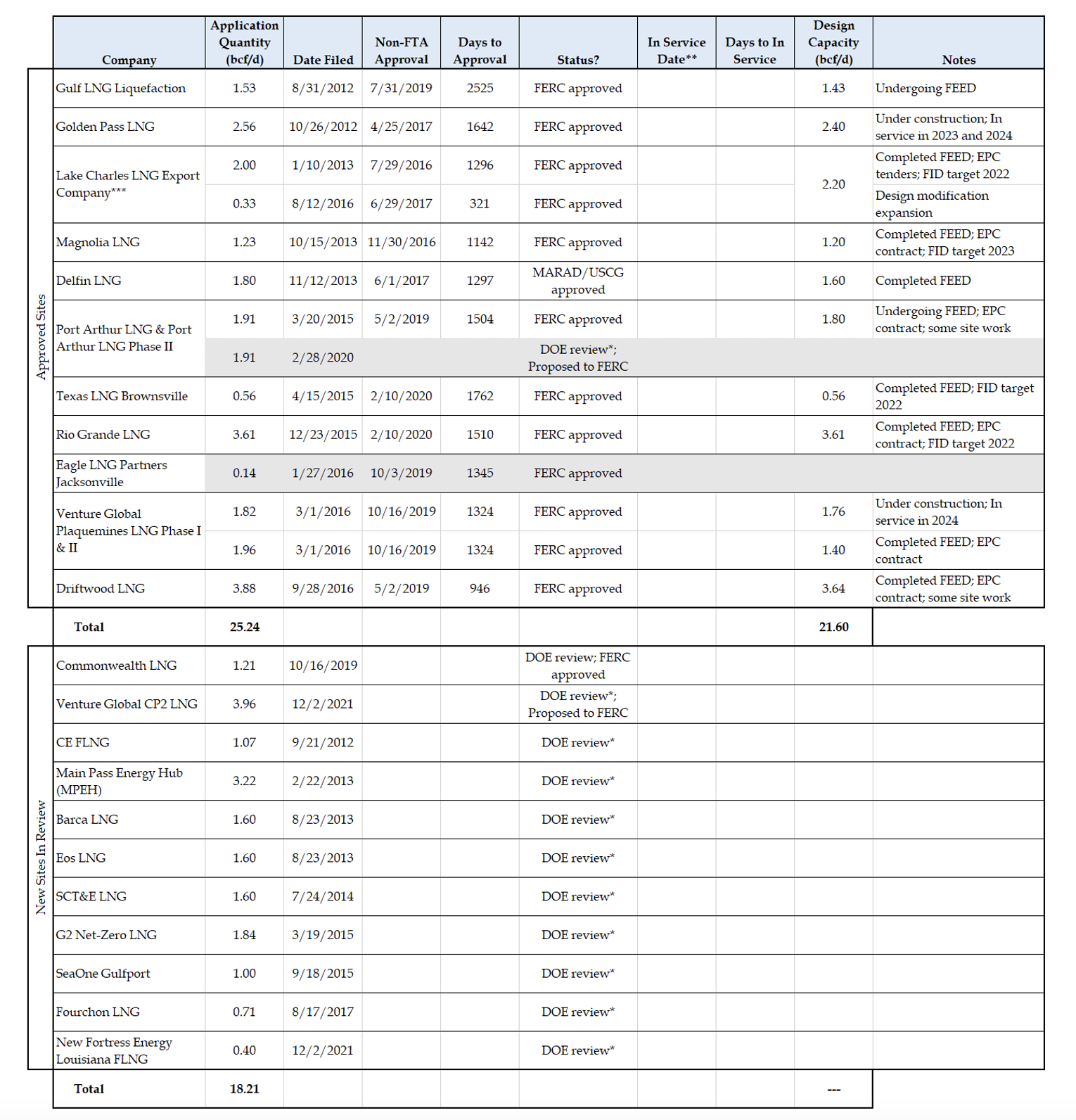

Since September 2010, there have been seventy-one applications filed with DOE to export LNG that total 84.6 bcf/d of capacity. Of that total, twenty-two applications (19.3 bcf/d) have been filed that are associated with sites already in service, resulting in the current design capacity for US LNG exports of just over 14 bcf/d.[28] Of the remaining forty-nine applications, fourteen (25.2 bcf/d) have been approved but are not yet in service, eleven (18.2 bcf/d) are in review with DOE, four (3.5 bcf/d) are for export to FTA countries (primarily to the Caribbean and Latin America), and eighteen applications (18.4 bcf/d) have been withdrawn, vacated or dismissed. Appendix Table 1 summarizes the applications with detail, but does not include those that have been withdrawn, vacated or dismissed. Note that these data do not include export terminals proposed in Canada or Mexico, some of which draw on natural gas produced in the US.

Altogether, if we only include the 5 approved applications at existing sites and applications that have already been approved, the total US LNG export capacity in the Lower 48 could expand from 14 bcf/d to over 42 bcf/d in the next few years. If we also consider applications that are in review at DOE plus the approved capacity for export to FTA countries only, the total capacity could expand up to 66.2 bcf/d. Of course, this would require all of these proposed sites actually be built.

Using history as a guide, some of the pending applications will not likely move forward, and some of the currently approved terminal capacity may not find sufficient market support to be constructed. A license to export does not imply exports. Ultimately, market conditions will dictate the terms of trade and whether or not LNG export capacity is built and how intensely it is utilized. But any increase in export capacity will likely need to be met by a combination of new domestic production and increased imports from Canada. In both cases, additional pipeline capacity would be needed to ensure regional supplies are accessible.

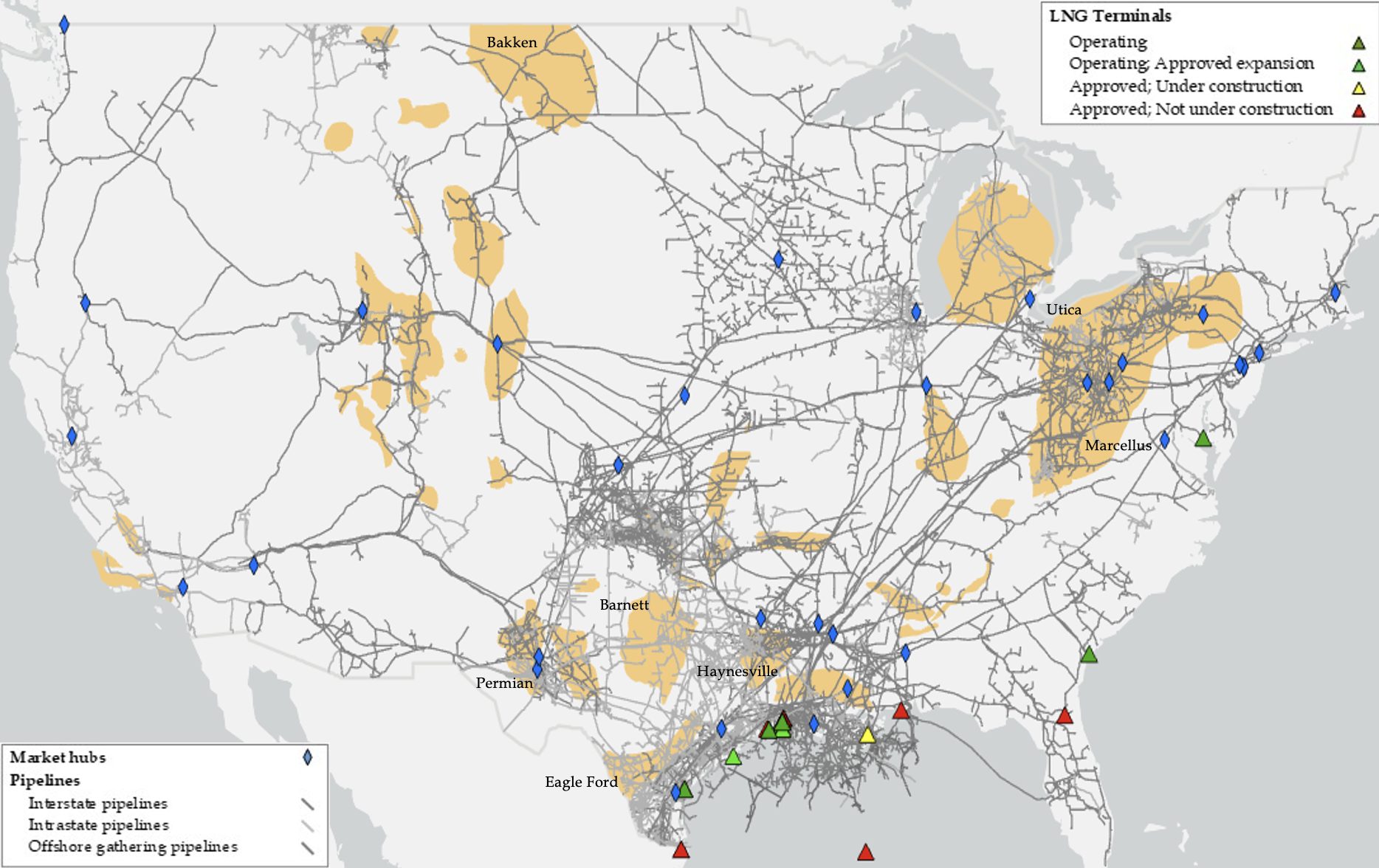

Figure 6 is a map of pipelines, market hubs, shale plays, and operating and approved LNG export terminals in the US Lower-48. This is meant to highlight the location of shales, which have accounted for the majority of domestic production growth, the locus of liquid market pricing locations (hubs), the density of pipeline infrastructure, and the proximity of LNG export terminals (operating and approved) to all of the above. The US Gulf Coast is relatively well-situated to accommodate production growth from shales and access to LNG export terminals – so goes the old adage, “location, location, location.” That stated, pipeline takeaway constraints have been present, as evidenced by negative natural gas prices in the Permian basin and significant gas-flaring associated with oil-directed upstream activities.

Pipeline constraints have been especially evident in the Marcellus and Utica shales in the Mid-Atlantic. Tremendous growth initially resulted in reversals of pipeline flow, but that opportunity is limited. Hence, new infrastructure has been needed to move supplies to other regions. Although not entirely in the purview of US regulators, Canadian supplies are similarly constrained. Altogether, given the locations of existing and proposed LNG export capacity relative to regions of production growth, there is an important need for the North American market to be sufficiently connected from production to storage to market hubs to demand and exports. This may be a “pinch point” for future gas market expansion.

As such, we must ask, “Given the existing pipeline configuration in North America, for a given domestic and international market pull, what is the LNG export potential?”

Figure 6 — US Lower-48 Pipelines, Market Hubs, Shale Plays, and Operating and Approved LNG Export Terminals

B. Is the Past Prelude to the Future?

As can be seen in Figure 7, the US transitioned from a net LNG importer to a net LNG exporter in the middle of last decade. This transition occurred after the Sabine Pass LNG export facility began operations. Prior to then, the US exported LNG from Kenai in Alaska, as well as by truck at a few border crossings. Currently, there are seven LNG export terminals in service in the US Lower 48 – at Sabine Pass, Freeport, Cove Point, Cameron, Elba Island and Corpus Christi, with Venture Global facility in Calcasieu Pass opening at the end of 2021 to round out the current list.

Figure 7 — US LNG Trade, 2000-2021

** - Pictured are exports from Kenai, Sabine Pass, Freeport, Elba Island, Cove Point, Corpus Christi, Cameron, and Other. Other includes 18 border crossings for trucked LNG. Data is available upon request.

Source Data are sourced from the US Energy Information Administration

The rapid growth in exports seen over the last few years has continued through 2022, especially with increased demand from Europe after the Russian invasion of Ukraine and the cut-off of Russian pipeline supplies. In fact, the shock to the global natural gas market has impacted prices everywhere (as seen in Figure 5) and will have lasting repercussions for global LNG trade.

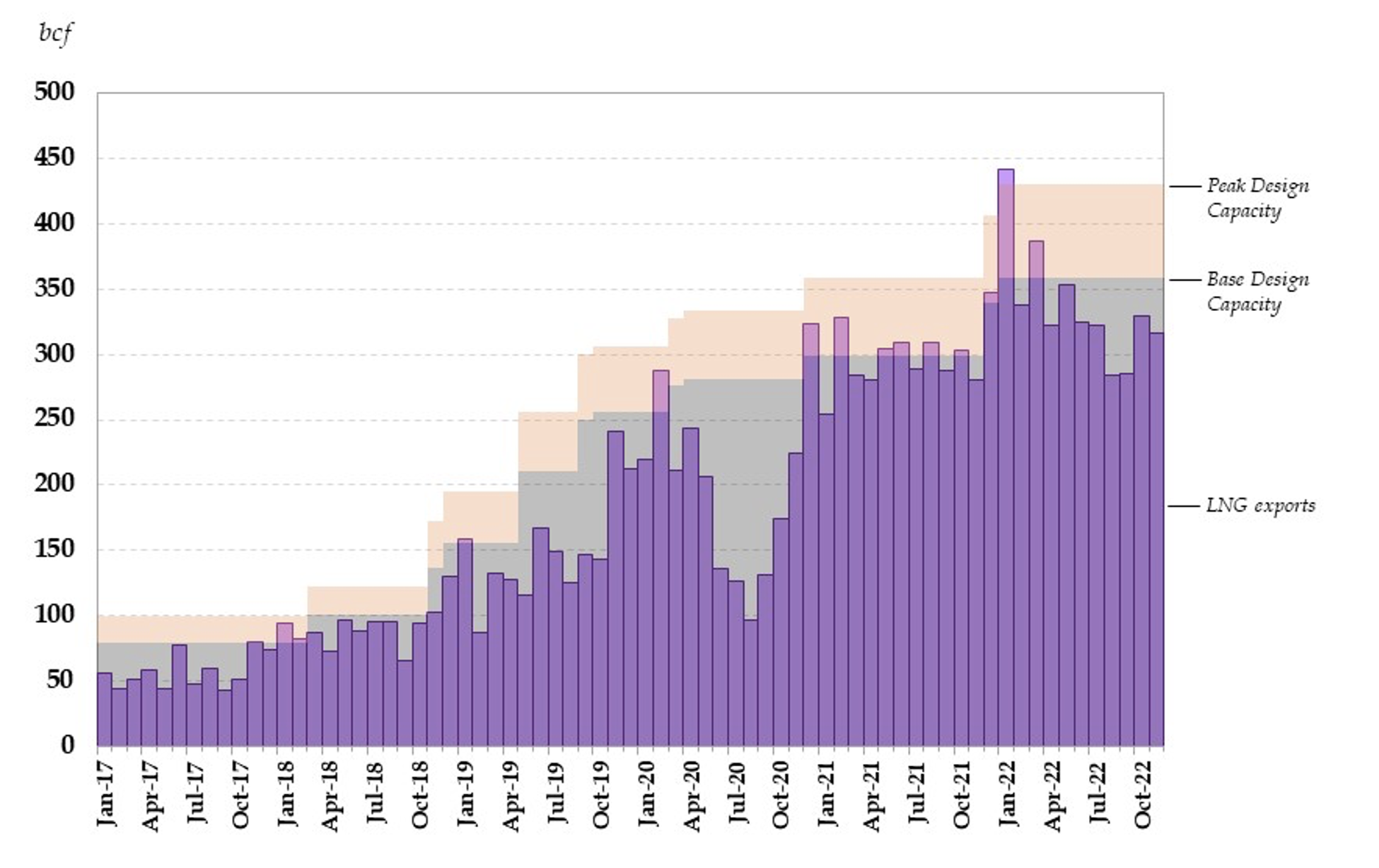

The US already has 14 bcf/d of peak LNG export capacity in operation, an additional 11.2 bcf/d under construction or with limited site work already commenced (Corpus Christi Stage III, Golden Pass, Port Arthur, Plaquemines Phase I, and Driftwood), and non-FTA export licenses granted to another 14.3 bcf/d (see Appendix Table 1). As indicated in Figure 8, LNG export terminals frequently operate at or above base design capacity. This is an indicator of the strong demand for US-sourced LNG in the international market.

Figure 8 — US LNG Exports, Monthly Jan2017-Nov2022

Given the disruption of Russian natural gas supplies and stated goals in Europe to diversify away from Russia, the stage is set for US LNG exports to continue to climb. Of course, the extent to which Russian natural gas is re-directed on a long-term basis to other markets, such as China, the depth of the response by other LNG and pipeline gas supplies that can move into Europe, and the degree to which natural gas loses market share in Europe will have bearing on the outcome. Unrelated to Europe and Russia, it is also important to consider the extent to which demand for natural gas will increase in developing nations in Asia and elsewhere. Thus, the future role that US LNG exports could play in global gas market balance will depend heavily on overall market conditions.

Thus, a relevant question to ask is, “What will drive long-term demand for US LNG exports in potential destination markets?”

C. Production, Exports, and the Deep Linkage Trade Theory Would Suggest

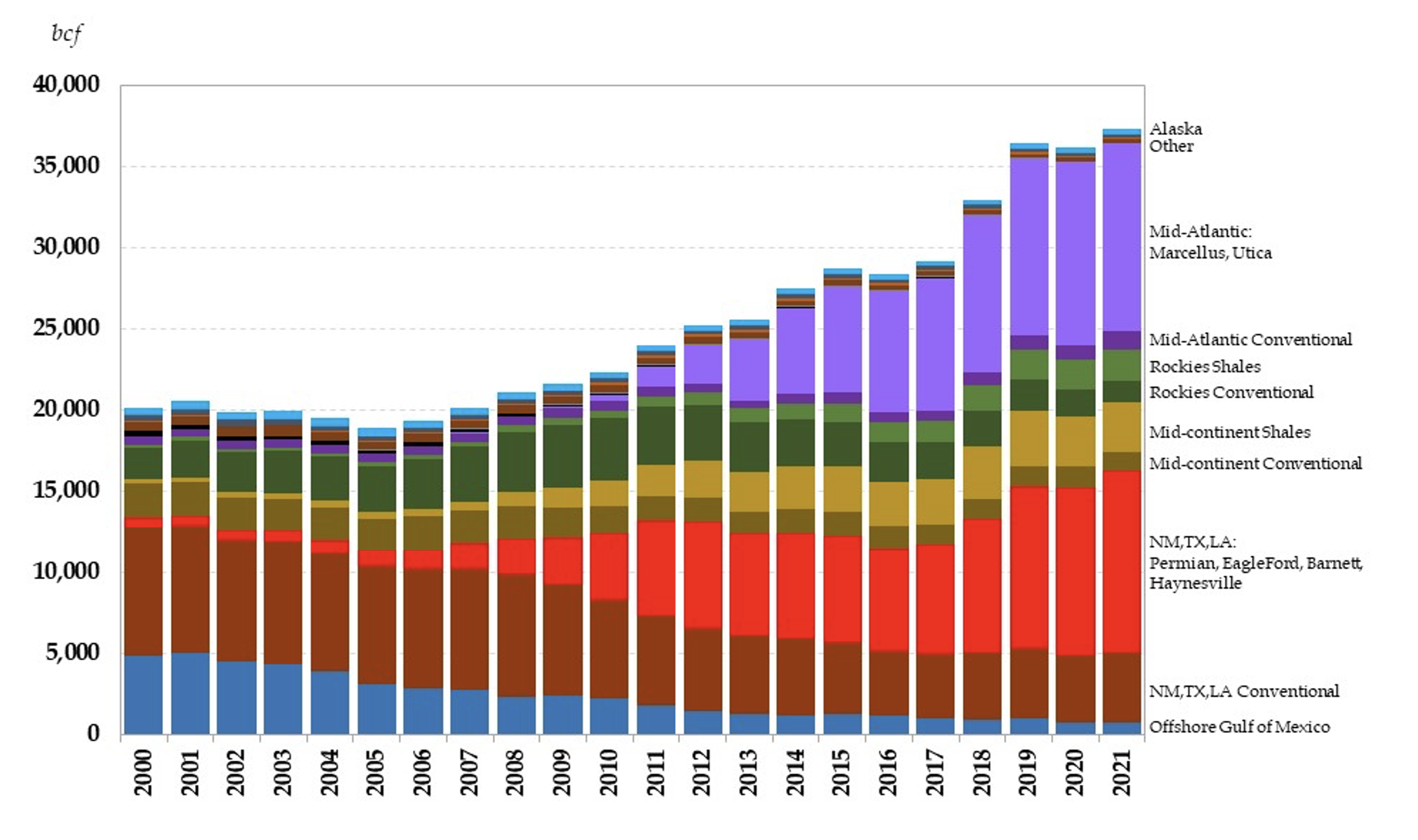

US Lower 48 production growth over the last decade has occurred primarily in shale formations located the Eagle Ford, Permian, Haynesville, Marcellus and Utica shales. In every case, there has been a need for new pipeline capacity and/or reversal of existing pipeline capacity to move volumes from new production areas to market. This fact reveals itself with observed changes in regional prices. For example, the extreme low prices seen at regional market hubs in West Texas and Western Pennsylvania over the last several years are clear market signals that regional supplies are outstripping regional demands. The only way to alleviate the situation is to (1) cut production, (2) grow local demand, and/or (3) add pipeline takeaway capacity to evacuate the region of excess supply. Options (2) and (3) each require investment in new infrastructure, which can be a challenge. Option (3), in particular, will be necessary to connect regional supplies, either directly or by displacement of other supplies, to a regional market or potential LNG liquefaction terminals. If new pipelines cannot be developed, only options (1) and (2) remain.

As indicated in Figure 9, shale production has increased virtually everywhere, but it is most pronounced in the Mid-Atlantic (Marcellus and Utica shales) and in the New Mexico-Texas-Louisiana region (Permian, Eagle Ford, Barnett and Haynesville shales). In the Rockies and Mid-continent regions, shale production growth has largely been offset by decline in conventional production. Altogether, this indicates, rather unsurprisingly, that infrastructure investments to increase takeaway capacity have been the greatest in the Mid-Atlantic and New Mexico-Texas-Louisiana regions. In the latter case, nearby access to ports has prompted greater connectivity with LNG export capacity along the Gulf Coast.

Figure 9 — US Production by Region, 2000-2021

The Mid-Atlantic region has presented a unique and well-publicized challenge. Historically, pipelines carried natural gas from the Gulf Coast, Midcontinent, Rockies, and Canada to consumers in the Upper Midwest, Mid-Atlantic and New England states. However, as production in the Marcellus and Utica regions increased, the need for natural gas from other regions dropped, so much so that prices in the Mid-Atlantic region fell below Henry Hub. As a result, existing pipelines reversed flow to export excess supplies to other regions, which has changed price and volume dynamics everywhere. In fact, if Mid-Atlantic production had not increased, there would likely be less interest in exporting LNG from the Gulf Coast because supplies in Texas and Louisiana would be needed to meet demands in the Mid-Atlantic region.

In sum, as production increases, adequate pipeline capacity is needed to connect supplies to markets. This is especially true when the production gains are in regions that have historically imported supplies. If pipeline capacity is not available, there is a binding constraint on regional trade. In many ways, the US natural gas market is a microcosm of the global natural gas market. In fact, we can see one relief valve at work as significant production gains from 2016 to 2019 coincided with the opening of US LNG export capacity. Whether or not similar production increases occur as new LNG export capacity comes online remains to be seen. But if there are constraints on developing new pipeline capacity from regions with low-cost natural gas resources, domestic production increases are less likely. In turn, this will negatively impact the competitiveness of US LNG exports, placing new and existing LNG export terminal capacity at risk.

Note, this same dynamic applies to Canadian production. If Canadian natural gas can access the US market with little to no impediment, and even potentially expand, then it will influence price to be lower in North America. In turn, this will improve the competitiveness of US LNG exports, even if Canadian natural gas does not directly access the export locations.

So, it is important to ask, “Will investment in new pipeline capacity be sufficient to support long-term market integration with shifts in regional production and, hence, LNG exports?”

D. The Future of LNG Exports: What the Analyses Tell Us

A number of studies utilizing different approaches have been done to determine the public interest in licensing LNG exports to non-FTA countries. Since 2012, the DOE Office of Fossil Energy has commissioned 5 studies to evaluate the macroeconomic effects of LNG exports.

- “Effect of Increased Natural Gas Exports on Domestic Energy Markets” was performed by the U.S. EIA and published in January 2012.[29]

- “Macroeconomic Impacts of LNG Exports from the United States” was performed by NERA Economic Consulting and published in December 2012.[30]

- “Effect of Increased Levels of Liquefied Natural Gas Exports on U.S. Energy Markets” was performed by the U.S. EIA and published in October 2014.[31]

- “The Macroeconomic Impact of Increasing U.S. LNG Exports” was performed by the Center for Energy Studies (CES) at Rice University’s Baker Institute and Oxford Economics and published in October 2015.[32]

- “Macroeconomic Outcomes of Market Determined Levels of U.S. LNG Exports” was performed by NERA Economic Consulting and published in June 2018.[33]

Each study took a different approach to modeling the implications of greater LNG exports. The two studies performed by EIA utilized the National Energy Modeling System (NEMS) to evaluate the impact of different rates of change in and different levels of exports. The studies found that natural gas prices rise with increasing export volumes and rise faster when exports increase more quickly. Given the nature of the NEMS model, these results are not surprising given that exports effectively act as demand shocks of different proportions. The price implications are that natural gas use in power generation declines in favor of coal and renewables. Both of the EIA studies utilized the then-most recent Annual Energy Outlook as the baseline, but the second study also considered each scenario with different resource base assumptions, finding that a larger resource base reduces the price impact of greater exports. The second study also explicitly evaluated the macroeconomic impact of greater exports, finding that GDP increases with exports.

The first NERA study, published in 2012, utilized NERA’s Global Natural Gas Model and NewERA macroeconomic model to evaluate the impact of LNG exports under different scenarios. The study found that the net macroeconomic benefits associated with greater LNG exports (up to 12 bcf/d) are positive, meaning there are net welfare gains from trade.

As export license applications continued to come in, the DOE was required to make a public interest determination for LNG export volumes in excess of 12 bcf/d. The study performed by CES and Oxford that was published in 2015 examined a number of different scenarios utilizing the Rice World Gas Trade Model (RWGTM) and Oxford Economics’ Global Economic Model (GEM) and Global Industry Model (GIM). The gas market scenarios were constructed in the RWGTM so that international market demand pull would stimulate greater levels of US LNG exports under different US resource base assumptions. Domestic prices increase in every case, but are motivated by demand pull from abroad where prices are even higher. The GEM and GIM models indicate that the net gains from trade for the US are positive in every case examined, although the benefits vary by scenario. Scenarios with greater resource availability tended to result in greater gains from trade.

The second NERA study, published in 2018, utilized the same models as NERA’s 2012 study. It was the most expansive of all studies to date. Utilizing baseline information from the EIA’s 2017 Annual Energy Outlook and International Energy Outlook, scenarios were constructed to evaluate a wide range of scenarios to capture a wider range of potential uncertainties, including those that eventually phase out all fossil fuels. The analysis finds that most significant factor affecting consumer welfare and US GDP is oil and gas resource availability and technology development, and that greater exports within a single domestic supply scenario are associated with greater welfare gains and higher GDP.

The studies commissioned by DOE to evaluate the public interest in LNG exports identify a net positive benefit associated with trade. Moreover, in what is perhaps an overlooked aspect common to the analyses, the net benefits are greater when resource availability is greater. While this is often framed in context of a larger resource base with more elastic cost-of-supply, it is also informative of the implications of policies that inhibit resource development. Namely, if policies or lack of regulatory action impede the development of infrastructure that market signals support, the net gains from trade are reduced.

The studies published in 2015 and 2018 also reveal another very important point. Namely, each considered scenarios with LNG export volumes well in excess of current, and each demonstrated that market conditions, not licenses to export, will dictate exported volumes. It is certainly true that too few licenses can present a constraint, but too many will not be a binding constraint. We have, in fact, already seen this with LNG imports to the US, where a significant number of licenses were issued but never resulted in imported volumes. Even in cases where developers constructed regasification capacity, the shift in market conditions in the late-2000s rendered that capacity to be of little consequence, so much so that much of it was later converted to export capacity. A license simply avails market participants of the ability to trade, nothing more.

If, however, there are other impediments to developing resources and/or infrastructures needed to support trade, then the gains from trade will not be realized. Given the licenses awarded to date, totaling over 42 bcf/d, it is unlikely that licensed export volumes will be a binding constraint. Rather, other factors are likely to bind, particularly those that inhibit the ability to achieve financing – such as market uncertainties, an inability to secure sufficient contracted offtake, legal challenges, and concerns related to policy and regulatory changes. Policy can address some of these issues, but not all. For example, questioning the benefits of LNG exports and threatening to take action to limit them, despite the depth of analysis already conducted on the matter, is not helpful. Exports will only occur if there is an associated economic value, which is especially true if they originate from an open and competitive market such as the US natural gas market.

It is important to recognize that the gains from trade are “net” not absolute. This arises because some consumers of natural gas are negatively impacted by higher prices that result when exports commence. But the gains elsewhere outweigh the losses. In fact, the 2015 study went to great detail to identify where the gains and losses occurred across the US economy.[34] Moreover, the losses are lower and net gains higher when more low-cost resources are available. This follows from a flatter, longer marginal cost-of-supply curve (a.k.a. more elastic supply) because the increase in demand for domestic resources that results from greater exports has a smaller impact on domestic prices when domestic supply is more elastic. Constraints that limit the ability to develop infrastructure or raise development costs tend to make domestic supply less elastic. Ironically, this has the impact of limiting exports and raising the domestic costs of exports that do occur. In such an outcome, both exports and the net gains from trade are lower.

While the analyses done to date have clear implications, they do not account for potential environmental costs. Recognition of this is what led DOE to consider the aforementioned studies of environmental costs in its review of LNG export licenses. In addition, FERC oversees an environmental analysis in accordance with NEPA prior to awarding its approval. Nevertheless, concerns related to environmental costs, when valid, could offset the net gains from trade identified in the modeling efforts commissioned by DOE. As such, it is incumbent upon the industry to adequately address environmental concerns. Any appearance of impropriety with regard to environmental cost accounting can lead to the erection of legal and regulatory barriers to project development.

Given the preponderance of evidence found through modeling and analysis, it is relevant to ask, “Are any additional steps needed from government and/or the private sector to ensure net gains from trade are captured? If so, what?”

E. Environmental Concerns

Natural gas has facilitated the displacement of coal in power generation in developed nations, and has the potential to do so in developing nations such as China and India where coal is a domestic staple. However, as attention turns to the greenhouse gas (GHG) footprint of natural gas supply chains, the future of natural gas in the energy mix becomes somewhat clouded.

Flaring and venting is a central concern to the future of natural gas, however neither is a practice deployed during gas-directed upstream activities. Such practices are typically used in oil-directed upstream activities with associated natural gas production, particularly when there is either inadequate takeaway capacity from the production site or the local market cannot make use of the natural gas volumes. While this points to some relatively straight-forward solutions – namely more pipeline takeaway capacity and/or greater local demand through power generation or something else – the economic incentive is not always sufficient, which can be motivation for local regulators to allow flaring to occur. Flaring and venting can also occur for safety and operational reasons to protect personnel and equipment. While a deeper treatise on flaring and venting is beyond the scope of this paper, it is worth noting that flaring and venting is addressed differently in different jurisdictions.[35]

Methane leaks along pipeline transportation and delivery systems is a concern regardless of the upstream source of natural gas. Once produced, either as a primary commodity or associated with oil, natural gas eventually comingles in the intrastate and interstate pipeline network. From there, it moves to a power generator, an industrial customer, a city-gate where a local utility then takes custody of the gas for distribution to a variety of customer types, or to an LNG export facility. Because methane is a much more potent GHG than CO2, if methane leakage along the pipeline network is high enough, then the purported benefits of using natural gas instead of other hydrocarbons, such as coal, disappear.

Prior to the war in Ukraine, LNG buyers in France, Germany, and Ireland had pulled back from supporting LNG imports from certain regions due to concerns about flaring and methane emissions. But the disruption of Russian natural gas supplies coupled with production declines in the EU has revealed a tremendous nascent demand for LNG. Given EU environmental priorities, a focus on verifying that natural gas supply chains have a low GHG footprint will grow. Various aerial survey initiatives and satellite monitoring efforts aimed at tracking methane emissions will bring greater transparency to the environmental impact of the upstream sector.

Government action is already evident. In September 2021, US and EU leadership invited countries to participate in the Global Methane Pledge, and formally launched the initiative at COP26.[36] The pledge is for voluntary action, and a lack of uniform measurement renders any pledge a “soft” target. But greater transparency brought by various measurement efforts will eventually harden methane reduction targets. Proposed methane fees applied to firms with uncontrolled emissions can give teeth to national targets and drive greater compliance.

Industry and regional government action is also evident. For instance, the Oil and Gas Climate Initiative has announced a global average methane emission target as a share of marketed natural gas of 0.25% by 2025.[37] At more regional levels, similar steps are being taken. For example, the Texas Oil and Gas Association and other members of the Texas Methane & Flaring Coalition have announced a commitment to end routine flaring.[38]

We must ask, “What are the pathways for industry to reduce methane leaks and minimize flaring and venting to ensure the long-term viability of natural gas in the energy mix?”

5. Closing Remarks

This paper has sought to elevate a conversation about the future of US natural gas. Broad goals for economic development, environment, and energy security will define the global future of natural gas, and some regions will inevitably chart different courses than others. The future of US LNG exports will be heavily influenced by outcomes beyond US borders, but domestic policies will also have influence.

We began with a discussion of natural gas and the complexities of energy transitions to help motivate a deeper look at the international landscape and its connection to US natural gas and the past, present, and possible future of US LNG exports. In doing so, we noted several critical points.

To begin, the US natural gas market enjoys a legacy and scale that is unrivaled globally. It is also the most liquid regional gas market globally, owing to a regulatory architecture that promotes transparency and competition. Taken together, these factors set the stage for the US to play a prominent role in the future of natural gas in the global market.

Market structure is an advantage. The evolution of the US natural gas market over the last 5 decades has engendered depth and liquidity that provides an advantage to consumers in that they do not need to tie their purchases all the way through the value chain back to the wellhead. Rather, buyers have flexibility to access supplies indexed to regional market hubs. For LNG developers, this reduces the upfront capital commitment, and opens up risk mitigation tools that are not necessarily available in other markets.

Changes in production, consumption, and trade over the last 20 years have motivated a radical shift the US natural gas landscape, with LNG exports taking center-stage in the last 5 years. Periods of significant differences between international and domestic prices has driven a desire to export LNG for commercial gain. Historically, applications for licenses to export increased when regional price differentials were higher. Of course, the process to apply for and receive an export license to non-FTA countries is important for bankability, but it is also arduous and often times lengthy. This can present challenges to the prospects for infrastructure development, particularly as market conditions change. Nevertheless, the rapid growth in LNG exports over the last 5 years and the currently high utilization rates of US LNG export terminals are indicators of the desirability of US-sourced LNG supplies.

The geographic distribution of production growth in the US has created challenges. Nowhere is this more evident than in the Marcellus and Utica shales in the Mid-Atlantic, where tremendous growth has resulted in new infrastructure requirements to move supplies to other regions, either for consumption or export. A similar dynamic has evolved in the New Mexico-Texas-Louisiana corridor, but location is everything as the nearby Gulf Coast provides an opportunity to feed robust local power generation and industrial demands as well as support LNG exports. In general, additional pipeline takeaway capacity has been needed, which highlights the importance of maintaining a deeply interconnected North American market to ensure regional price dislocations are minimized. Pipelines ensure regional gains from trade are accessible across the US and North America. It was also pointed out that Canadian gas supplies, which have the potential for robust growth, could play an important role in supporting US LNG exports, if market access is not impeded.

We also expounded on the implications of studies commissioned by DOE in support of a public interest determination. It was noted that all studies identified a net gain from trade across a wide range of different scenarios considered. Moreover, the net benefits increase with resource availability. While this is often framed in context of a larger resource base with more elastic cost-of-supply, it also indicates that anything that impedes the development of infrastructure will reduce the net gains from trade. The two most recent studies also reveal that market conditions will dictate traded volumes, not licenses to export.

We then raise environmental concerns that must be addressed, even as DOE and FERC (through NEPA) both consider the environment in their decision-making. We note that methane emissions and natural gas flaring and venting represent a significant source of GHG emissions and resource waste in the supply chain. Reducing flaring, venting and leaks can lock in real, measurable opportunities for LNG trade to be a decarbonization vehicle. Indeed, much of the CO2 emissions reductions seen in the US over the last two decades is a result of natural gas displacing coal in the power generation sector, and this benefit is transferable, if done correctly.

The prospects for US LNG exports are bright as long as market forces can work without impediment. Infrastructure to support regional and international gains from trade is paramount. This does not imply regulations should be lax. Rather, regulation should encourage transparency and competition so that value propositions are identifiable. As global energy markets continue their inexorable transition to a lower GHG future, sources of energy supply that are competitive, accessible, and environmentally favorable will thrive. This is exactly where US natural gas can find its comparative advantage.

Appendix

Appendix Table 1 provides a compilation of information about US LNG export terminals in the Lower 48 states. The vast majority are in Texas (10 sites and 18 licenses totaling 25 bcf/d) and Louisiana (13 sites and 24 licenses totaling 31 bcf/d), with Mississippi, Georgia, Maryland, Pennsylvania, Florida and the Gulf of Mexico accounting for the remainder (9 sites and 9 licenses totaling 10 bcf/d). There is currently 14 bcf/d of capacity in service, with all but 1.1 bcf/d in Texas and Louisiana.

Appendix Table 1

** - According to EIA data, commercial operations typically begin 2-3 months after the facility is brought into service.

*** - Two applications for license were filed, data indicated are for latest application.

Source Data are as of December 16, 2022, are from the US DOE (see https://www.energy.gov/fecm/articles/summary-lng-export-applications-lower-48-states) and US EIA (https://www.eia.gov/naturalgas/data.php#imports), and include only the Lower 48 States. Table does not include 18 applications totaling 18.41 bcf/d that were dismissed, vacated or withdrawn.

Endnotes

[1] The Infrastructure Investment and Jobs Act, 2021 and Inflation Reduction Act, 2022 contain numerous provisions to support a portfolio of options for net CO2 reductions.

[2] Note, this raises important questions about standards for certifying the clean energy credentials of natural gas, and how will they be priced into the commodity as a differentiating feature of natural gas supply chains. It is an ongoing and important area of research (see, for example, Steven Miles, “Low-Carbon Fuels: How to Use U.S. Infrastructure and Exports to Deliver Cleaner Energy to the World,” Baker Institute policy brief, Feb 10, 2021, at https://www.bakerinstitute.org/research/low-carbon-fuels-how-use-us-infrastructure-and-exports-deliver-cleaner-energy-world), but beyond the scope of this paper.

[3] See Hartley, Peter R. and Kenneth B. Medlock, III, “Debt and Optionality in U.S. LNG Export Projects,” The Energy Journal, Vol 44, Iss 2 (forthcoming, 2023).

[4] See, for example, Medlock, K.B. (2021), “China’s Coal Habit will be Hard to Kick,” Barron’s, commentary, available at https://www.barrons.com/articles/chinas-coal-habit-will-be-hard-to-kick-51633462019 and Medlock, K.B., Jaffe, A. and O’Sullivan, M. (2014), “The global gas market, LNG exports and the shifting US geopolitical presence,” Energy Strategy Reviews, available at https://www.sciencedirect.com/science/article/abs/pii/S2211467X14000467.

[5] This is the proverbial “valley of death”.

[6] One can think of this through the lens of real options. Investing in infrastructure is a real option. One only exercises the option when profitable. In the absence of market liquidity, a liquidity premium exists that renders the option value lower, thus reducing investment. Liquidity increases scale.

[7] See Medlock, III, K.B., “The Land of Opportunity? Policy, Constraints, and Energy Security in North America,” Baker Institute research paper, 2014, available at https://www.bakerinstitute.org/research/land-opportunity-policy-constraints-and-energy-security-north-america.

[8] https://www.congress.gov/bill/95th-congress/house-bill/5289.

[9] The process of allowing market forces to dictate prices was not completed until the passage of the Natural Gas Wellhead Decontrol Act in 1989. By 1993, all price regulations under the NGPA were eliminated.

[10] Order No. 636 - Restructuring of Pipeline Services | Federal Energy Regulatory Commission (ferc.gov)

[11] This process began with FERC Order 436 (1985), which allowed pipelines to voluntarily offer “open access” transportation services on a competitive basis within a minimum and maximum tariff range. Customers realized a cost savings relative to “take-or-pay” contracted volumes, so customers switched. As take-or-pay contracts were unwound, netback pricing evolved.

[12] According to the Bureau of Transportation Statistics Database, the number of pipeline operators reported as “natural gas transmission” and “natural gas distribution” in 1970 were 420 and 938, respectively. As of 2020, these numbers stood at 1,313 and 1,346, respectively (see www.bts.gov).

[13] Note, the Jones Act prevents waterborne vessel movement of LNG from ports in the US into New England, so imports to the region are sourced from abroad.

[14] Natural gas demand for vehicle fuel has increased at 7.2% per year since 2000, but still only comprises 0.18% or total consumption.

[15] See EIA’s Today in Energy (Dec 7, 2002) https://www.eia.gov/todayinenergy/detail.php?id=54919.

[16] See Medlock, III, K.B., “The Land of Opportunity? Policy, Constraints, and Energy Security in North America,” Baker Institute research paper, 2014, available at https://www.bakerinstitute.org/research/land-opportunity-policy-constraints-and-energy-security-north-america.

[17] See Medlock, K.B., “U.S. LNG Exports: Truth and Consequence,” Baker Institute research paper, 2012, available at https://www.bakerinstitute.org/research/us-lng-exports-truth-and-consequence.

[18] This assumes a 15% weighted average cost of capital, a Henry Hub equivalent feed gas cost, an operating cost of $1.5/mcf, a project book life of 25 years and an LNG export facility size of 1.0 bcf/d. The calculation is meant to be representative as each facility is different.

[19] The extent these stranded costs were rolled into development decisions at different sites is unknown.

[20] This is a requirement of the Natural Gas Act.

[22] https://www.energy.gov/fecm/doe-lng-exports-announcements-may-29-2014.

[23] https://www.energy.gov/fecm/downloads/life-cycle-greenhouse-gas-perspective-exporting-liquefied-natural-gas-united-states.

[24] https://www.energy.gov/sites/prod/files/2014/08/f18/Addendum.pdf.

[25] https://www.energy.gov/sites/prod/files/2020/10/f80/Sabine%20Pass%20-Term%20Ext.%20Order.pdf.

[26] Most proposed LNG export facilities fall into FERC jurisdiction. For deep water export facilities, jurisdiction falls to Maritime Administration (MARAD) and the U.S. Coast Guard (USCG).

[27] See Hartley, Peter, and Kenneth B. Medlock III. "Developments in the LNG Market," Energy in Transition, 7th IAEE Asian Conference, February 12-15, 2020.

[28] Note, 5 of the 22 applications (totaling 4.38 bcf/d) are in various phases of review and development, and application capacity and design capacity do not always match

[29] www.energy.gov/sites/prod/files/2013/04/f0/fe_eia_lng.pdf.

[30] www.energy.gov/sites/prod/files/2013/04/f0/nera_lng_report.pdf

[31] www.eia.gov/analysis/requests/fe/pdf/lng.pdf

[32] www.energy.gov/sites/prod/files/2015/12/f27/20151113_macro_impact_of_lng_exports_0.pdf

[34] Well-organized industries with strong lobbying abilities can successfully influence policy to preserve the status quo and hence market rents, even if the alternative outcome would be welfare improving. This is especially true when the benefits of the alternative outcome accrue to a broader, more diverse, less organized constituency. A relatively recent survey of the literature highlights the difficulties in measuring the welfare impacts of lobbying, see Bombardini, Matilde and Francesco Trebbi, “Empirical Models of Lobbying,” Annual Review of Economics 12:1, pp391-413 (2020). For an example that details different net welfare impacts, see Mohtadi, Hamid and Terry Roe, “Growth, lobbying and public goods,” European Journal of Political Economy, 14:3, pp453-473 (1998). For an example examining the US cellular industry, see Duso, T. “Lobbying and regulation in a political economy: Evidence from the U.S. cellular industry,” Public Choice 122, pp251–276 (2005).

[35] The US DOE’s publication, “Natural Gas Flaring and Venting: State and Federal Regulatory Overview, Trends, and Impacts,” July 2019, provides a nice summary of differences in regulation and technologies to reduce flaring. See https://bit.ly/42BH1zU.

[36] See https://www.globalmethanepledge.org/.

[37] “Oil and Gas Climate Initiative sets first collective methane target for member companies,” OGCI, Sept 24, 2018.

[38] “TXOGA Statement on Railroad Commission Actions to End Routine Flaring,” TXOGA, August 5, 2020.