This brief is closely derived from a piece the authors published in Foreign Policy on April 23, 2024, accessible at: https://foreignpolicy.com/2024/04/23/united-states-ban-lng-sales-china.

A low-profile post by the U.S. Department of Energy (DOE) may point to a serious strategic change in U.S. policy in trade, energy, and relations with China. So far, the notice has received little or no public coverage or attention despite its potential ramifications — but, combined with other legislative and political signals, it could be a game-changer in the energy landscape.

The White House and DOE announced on Jan. 26, 2024, a “temporary pause” in reviewing applications to export liquefied natural gas (LNG) to countries with which the U.S. does not have a free trade agreement (“non-FTA countries”). The Natural Gas Act (NGA) requires the DOE to approve applications for the export of LNG to non-FTA countries unless the DOE finds that the export would “not be consistent with the public interest.”

Is the Public Interest Standard for LNG Exports Changing?

In its Jan. 26 announcement, the DOE emphasized that the factors it would consider were the “same” that “DOE has considered when evaluating the public interest of LNG exports for more than a decade”; namely, domestic natural gas prices, economic impact, energy security for the U.S. and its allies, and environmental factors, with an extra dose of climate consciousness. Save for climate, these are long-standing metrics for determining the NGA’s public interest standard.

But on Feb. 23, the DOE posted a new notice to explain the “temporary pause.” It was similar to the Jan. 26 announcement — save for the last paragraph. There, the DOE suggested one outcome of its pause in issuing new LNG export permits could be to take steps that reduce the risks to consumers and manufacturers caused “by selling our energy resources to competitor countries that don’t align with our interests and those of our allies.” The only potential LNG-buying nation that fits that description is the People’s Republic of China.

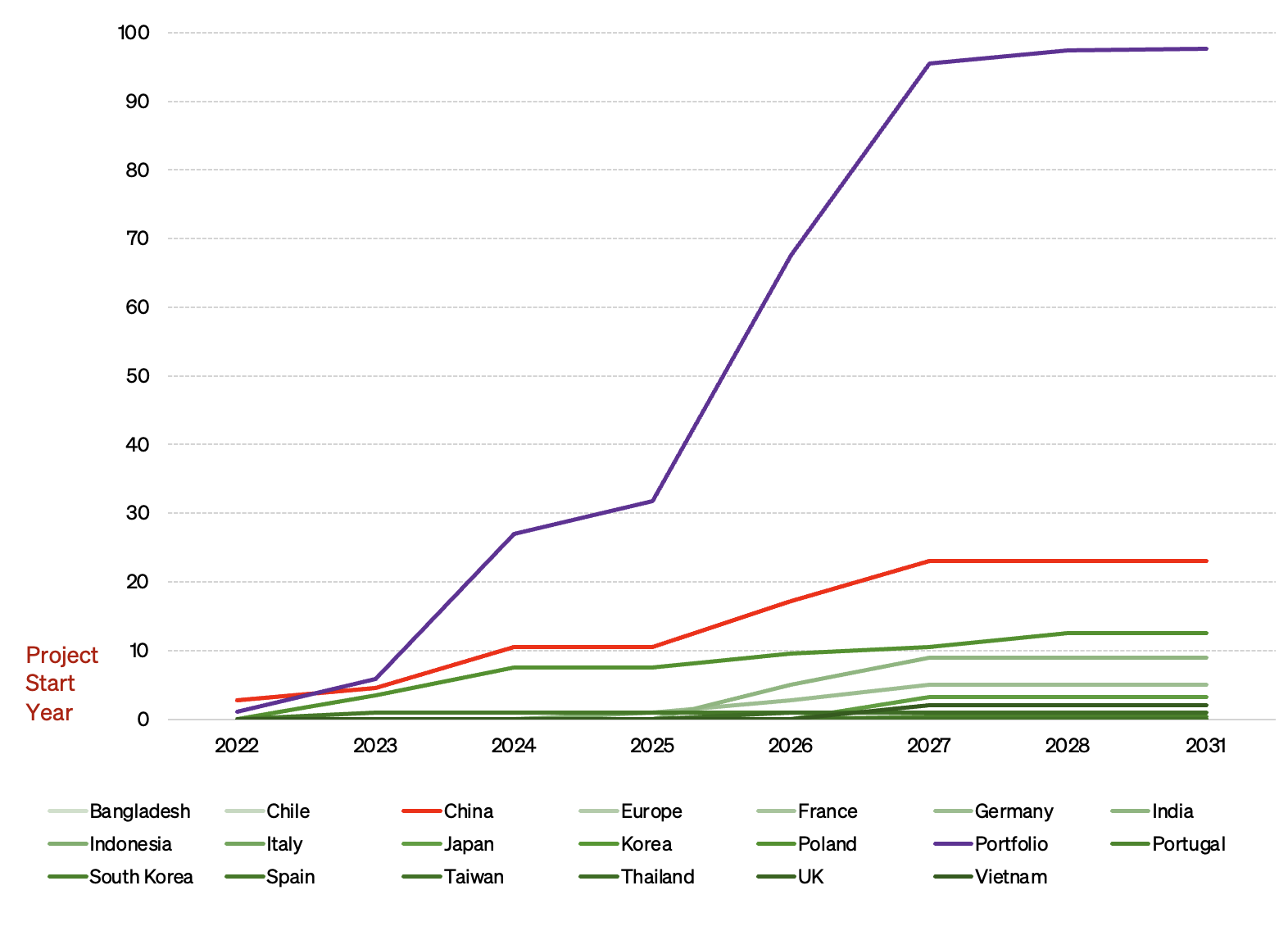

Why would the United States consider restricting LNG sales to China? China accounted for less than 4% of all U.S. LNG exports in 2023, but it is now the largest designated destination by volume under all long-term U.S. LNG contracts, and Chinese buyers account for almost 25% of the volume of long-term contracts entered into by LNG export facilities affected by the DOE’s LNG export pause.[1]

Figure 1: China Buyers Have Helped Anchor US LNG Export Projects

The rapid growth of China’s acquisition of U.S.-sourced LNG under long-term contracts has produced worries about a possible buildup of energy supplies ahead of military aggression, as well as concerns about cheaper Chinese steel, aluminum, and EV cars potentially flooding the U.S. market directly or indirectly through Mexico.

Long-term LNG contracts signed with U.S. project developers have generally been priced lower than LNG from other sources, partly because U.S. natural gas is cheaper than gas elsewhere and partly because of robust competition among U.S. project developers. Denying China access to U.S. LNG, the argument goes, might help keep its exports to the U.S. from being so cheap.

Potential Scenarios

To date, the DOE only prohibits LNG exports (along with bans on the export of many other goods) to North Korea, Cuba, and Iran. Is the United States about to put China in the same basket? Initially, this seemed highly unlikely, particularly as China’s signing of long-term contracts has allowed billions of dollars of capital to flow to several new projects employing many thousands of U.S. construction and other workers.

However, just days after the DOE’s February explanatory posting, four U.S. senators announced they would “introduce legislation banning LNG exports to China.” The bill would ban export of LNG and other petroleum products to China, Russia, Iran, and North Korea; resales of such U.S. products in the secondary market would be prohibited to be delivered to those countries.

Multiple scenarios could play out in the next few weeks and months. These range from no action, to lowering the permitting priority of projects seeking to sell to China, to a ban only on future primary market sales from the U.S. to China, to a full ban on future LNG exports from the U.S. to China from both the primary and secondary markets.

1. No Action

Taking no action now still gives the United States plenty of options. In a military conflict, the U.S. could simply block all shipments of LNG from the U.S. to China; indeed, doing so would be much easier than trying to block shipments of LNG to China from Malaysia, Qatar, or Russia.

With respect to “cheap” Chinese imports, U.S. policymakers can, and should, address any such flood of subsidized goods either through the tariff process, as both former President Donald Trump and incumbent President Joe Biden have pursued, or by imposing a carbon border adjustment to reflect China’s overwhelming use of carbon-emitting coal in its manufacturing processes. Advantages of “no action” include avoiding a trade war with China, including a possible retaliatory ban by China on exports to the U.S. of critical minerals needed for batteries, smartphones, and clean technologies. As noted, China’s purchase contracts also effectively underwrite new and expanded U.S. projects, with economic and employment benefits for the United States.

2. De-Prioritizing Export Applications with China Destinations

If the U.S. takes action against China, the DOE could decide to take a minimalist approach to restricting future exports by de-prioritizing non-FTA LNG export applications that identify China as the primary destination. Given the dramatic lengthening of permit application review from a couple of months to 433 days (and counting) by the Biden administration even before the pause, moving to the end of the queue may be tantamount to rejection of a non-FTA application.

3. Denying New Export Applications that Designate China as Initial Destination

A third alternative would be for the DOE to ban outright new non-FTA LNG export permits that identified China as the initial designated destination. Either the de-prioritization or this stronger version of a ban would produce the same result. LNG portfolio companies, which do not identify any destination or port in their purchase contracts, would step in and replace the Chinese buyers.

In recent years, these highly capitalized portfolio companies have become the largest purchasers of long-term LNG from the United States (20 million tons coming online in 2024) and indeed worldwide. Some are large oil and gas companies; others are international commodity traders. The LNG export applicants would amend their DOE applications to remove the references to China. However, an exporter’s LNG portfolio buyers could merely flip the cargoes — as already routinely happens — to a second buyer (or third) who then takes the cargoes to China, none of which would be barred by the DOE action.

4. Banning All Sales to China from Newly-Approved LNG Export Projects

The most draconian option would be a full ban, similar to the current ban on LNG exports to North Korea, Cuba, and Iran, that precluded all sales to China by any person in either the primary or secondary markets. Such a full ban would undercut future U.S. LNG trains’ commercial prospects by limiting the incentive for buyers to sign up for long-term U.S. LNG knowing that it was unlawful to resell the LNG to the world’s largest LNG importer.

With Chinese buyers accounting for almost 25% of the volume of LNG from pending non-FTA LNG applications, a full ban on future sales to China could cause some or all of the proposed LNG export projects and expansions currently waiting for approvals to lose their financing and be delayed or worse. Although the ban might cause significant damage to the U.S. LNG industry, China could still get U.S. LNG from existing projects, either directly or through swaps or the secondary market. And if the DOE attempts to ban sales to China from existing projects or under existing contracts, it risks a legal claim from U.S. exporters, their investors, and lenders that the government has expropriated their assets. Furthermore, politicizing gas exports would place the US on a similar practical and moral plane to Russia, an ironic twist just three years after Gazprom began cutting supplies to Europe, and particularly given the U.S. touting its LNG as rescuing Europe from Russian energy blackmail.

Reviving Russia and Coal

Actions by the U.S. government to restrict China’s access to U.S. LNG will likely send China’s LNG buyers to seek supplies from competing sources — with Russia the most likely candidate. Russia’s Arctic LNG 2 project is capable of producing LNG (with Chinese help) but has yet to ship cargo due to U.S. sanctions. If China concludes that the U.S. is cutting off access to its LNG, that could be enough for China to decide to break U.S. sanctions and inject capital and technical capabilities to help scale up Russia’s LNG industry.

In recent years, Chinese buyers have contracted for approximately 24 million tons per annum (mtpa) of U.S. LNG — almost all of which comes from projects that came online in 2022 or later. As such, U.S. LNG export restrictions that increase China’s appetite for Russian LNG would be a strategic ‘own goal’ because they would boost the revenues available to fund the war in Ukraine and possible future aggression.

Switching power-generating plants from coal to natural gas helped to reduce the U.S.’s carbon intensity in recent years. If the United States bans natural gas sales to China, it will likely be substantially harder to elicit China’s cooperation on other measures to reduce its coal usage. China relies on coal for some 55% of all its primary energy and continues to open new coal-fired power plants and coal mines. In 2022, China’s planned coal-fired capacity increased by 126 GW while the amount of operating and planned coal plants fell in both developed and developing countries (other than China). Climate regulation and policies adopted by the Biden administration and other developed nations will fall short if China continues to rely on coal.

Geostrategic Consequences

Any action could accelerate the Cold War 2.0 now unfolding between the United States and China. In late summer 1941, the Roosevelt administration halted U.S. oil exports to imperial Japan, hastening the slide toward war between the two Pacific powers. As eminent historian Akira Iriye wrote of that situation: “The oil embargo had a tremendous psychological impact upon the Japanese. The ambivalence and ambiguities in their perception of world events disappeared, replaced by a sense of clear-cut alternatives.”

Today is not 1941, but the benefit of historical hindsight affords us an understanding of the nonlinear effects that can arise when one competitor in a strategic rivalry decides to abruptly deny the other access to a vital commodity. China might respond to U.S. LNG export restrictions with reciprocal export bans on critical minerals and other commodities. It would also further encourage Beijing’s already robust instincts to securitize Chinese energy policy, further undermining global climate goals. Now is the time for the United States to emphasize an energy abundance agenda, not politicize energy exports.

Note

[1] Authors’ compilation of liquefied natural gas (LNG) contracts from public sources, including U.S. Department of Energy (DOE) data, Bloomberg, press reports, and other public documents; wherever there was a discrepancy, the authors used DOE data.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.

{kind=link}