The coming winter is likely to be the sharpest test yet of the collective will of NATO members and their close partners to contest Russia’s war of conquest against Ukraine.[1] Even amid the warmth and sunshine of mid-summer, energy pain is already manifesting itself across Europe — even leading to impoverishment for some. Much of the eurozone teeters on the brink of recession. European countries have collectively already committed close to $1 trillion to offset high energy costs and bail out commercial firms — a sum larger than the European Union’s COVID-19 recovery fund. Industrial production is stagnating, and companies are looking to offshore their operations to places with lower energy costs.

If summer is already grim, what might winter bring? Mother Nature could deliver another warmer-than-normal winter, and China’s economic engine might not revert to its historic norms (which would require it to import large amounts of liquefied natural gas). Russia might not try to further disrupt energy supplies into Europe. But hope is not a strategy, and at least one of these three possibilities are likely to occur — perhaps all.

Energy challenges at a level not experienced since the 1973 Arab oil embargo plausibly await. Yet many European political and commercial leaders are avoiding critical actions they could take today to keep the lights and heat on (and affordable) this winter and beyond. Tight gas supplies are the danger most imminent, so locking in a more stable arrangement should be among their highest priorities. Yet it is not. Why?

The Gas Grand Canyon: Europe’s Gas Supply Gap

Despite the Kremlin’s history of directly weaponizing gas, most European buyers failed to contract for long-term LNG supplies in the run-up to Russia’s February 2022 invasion of Ukraine. Now, many are active only in the LNG spot market. This lack of forward planning is surprising given that the continent faces a yawning “gas Grand Canyon”[2] that, based on Baker Institute modeling and other physical market assessments, is poised to linger for years to come. The canyon is at this point a structural issue, not a transitory one. In coming decades, wind and solar power, energy efficiency, and various hydrogen-related possibilities may help to bridge the gap, but none will be able to come close to filling Europe’s vast gas supply gap, at least not for many years.

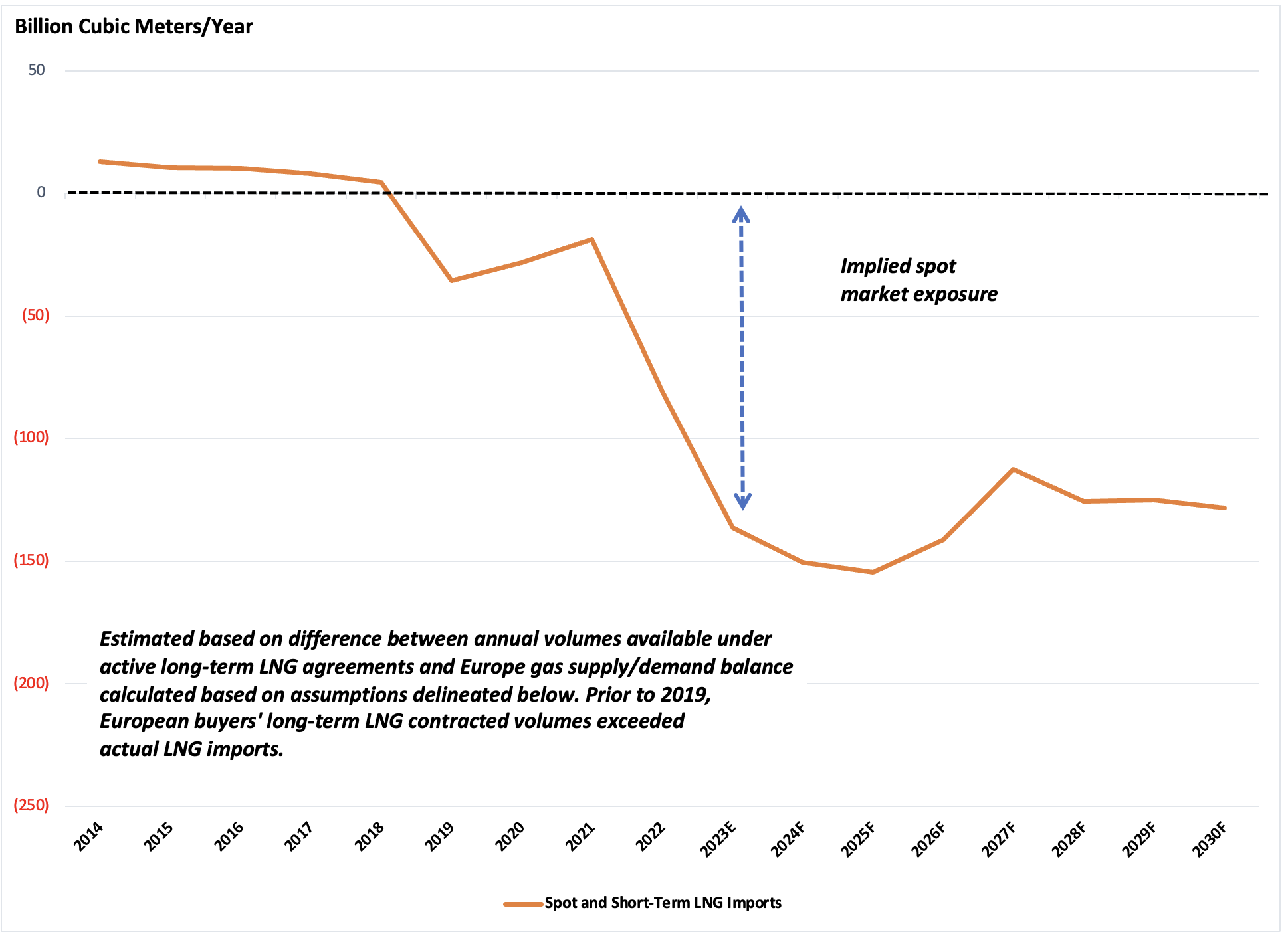

This deficit is over 100 billion cubic meters (bcm) of gas annually and will have global impacts in both the immediate and longer terms (see Figure 1). Depending on one’s preferred yardstick, it is variously 1) on par with the gas use of Bangladesh, Indonesia, Pakistan, and Vietnam combined, 2) nearly 1.5 times larger than India’s entire gas use, or 3) about four times larger than the gas use in all of Western Africa, including powerhouse Nigeria. Additional quantities of natural gas and LNG are supplied via current firm gas supply contracts that are expected to expire in the next few years, which will significantly exacerbate the potential gas supply gap. Altogether, the shortfall has been estimated to be as much as 60% of Europe’s expected LNG demand.

Figure 1— Europe’s Looming LNG Import Grand Canyon

Key Assumptions for 2023-2030: 1) Norwegian pipeline gas exports decline by 2% annually due to falling gas production, 2) Russian pipeline exports to Europe bottom out at 5 bcm/year in 2024 and thereafter gradually recover to 45 bcm/year by 2030, 3) African, Middle Eastern, and other Eurasian pipeline gas exports to Europe remain steady at 32, 25, and 9 bcm/year, respectively, 4) European gas demand declines 2% each year between 2023 and 2030, and 5) European gas production declines 4% annually between 2023 and 2030. Europe’s long-term LNG contracts are based on actual data compiled by the authors as of Aug. 1, 2023.

How We Got Here

For decades, policymakers in Western Europe treated energy security and national security as somehow disconnected. In the years running up to 2020, EU member states collectively allowed Russia’s share of total natural gas supply to nearly double to approximately 40%. At first glance, this might seem logical, given the obvious trade opportunities from a gas-hungry premier global economic bloc situated within pipeline range of one of the world’s largest gas resource bases. But political dynamics also played a significant role for both the exporter and importers. Since the 1990s, Russia has continually and deliberately disrupted energy supply to Ukraine and other customers. It invaded Georgia in 2008 and Ukraine in 2014, and subsequently supported a separatist war in eastern Ukraine[3] that likely claimed more than 14,000 lives from 2014-2021.

Meanwhile, many European countries throttled back on gas infrastructure investments that could have otherwise helped facilitate supply diversification. Data from the EU’s Projects of Common Interest (PCI) list of “key cross border infrastructure projects that link the energy systems of EU countries” show this decline.[4] In 2013, 108 discrete gas infrastructure items made the list, falling to:

- 103 projects in 2015.

- 72 projects in 2017.

- 41 projects in 2019.

- 20 projects in 2021 — with an initial stipulation that no more funding be made available to natural gas infrastructure after the completion of those projects.[5]

When Russia invaded Ukraine on February 24, 2022, most of Europe was caught flat-footed. Gazprom, a company largely owned by Russia, began cutting back on gas supplies to Europe in 2021 and drained the 25% of European gas storage capacity that it controlled in advance of that winter. With the invasion most (though not all) of Russia’s transit routes for pipeline gas were shutdown. Europe lost some 150 bcm/year of Russian gas. Yet, as we wrote some weeks ago, Europe purchased virtually no new long-term LNG supplies in the six-month run-up to the invasion or immediately thereafter, leaving themselves completely dependent on emergency measures, including industrial shutdowns, mandatory cutbacks in electricity usage, billions of euros in subsidies and a flood of LNG spot imports diverted at high cost from other markets. By comparison, China purchased some 24 million metric tons per year (mtpa) of new LNG contracts during the same period, most locked in at much lower Henry Hub-linked prices. Even as of writing, European energy consumers largely remain on the sidelines of the market for long-term LNG supplies, having contracted in the first 16 months after the invasion for less than 15 bcm/year of long-term LNG, compared to total global contracting of about 140 bcm/year during that time. Our analysis suggests that through the same 16-month period had Europe procured LNG under long-term contracts from existing U.S. producers linked to Henry Hub prices, rather than purchasing spot LNG cargoes at TTF-based gas prices, European customers could potentially have saved over $100 billion in energy costs. That amount is poised to continue growing as the forward price curve for TTF continues to exceed that for U.S.-based LNG for at least another couple of years.

Three Possible Rationales for Europe’s Not Filling its Gas Supply Gap

Many of the same energy policies that led to Europe’s gas supply deficit after Russia’s 2022 invasion of Ukraine are now being deployed to rationalize a sequel. Three beliefs appear to underlie Europe’s present justification for relying on such large volumes of uncontracted LNG from unknown and insecure sources at unknowable prices:

- Over the next few years, European buyers can simply outbid everyone to secure gas molecules.

- The war in Ukraine will reach a conclusion “clean” enough to permit a substantial resumption of lower-cost pipeline gas supplies from Russia.

- Europe can reduce gas use by 30% in the next seven years under the Fit for 55 and REPowerEU plans while renewables, over the next five to 10 years, help fill in the gas Grand Canyon described above.

We now sequentially discuss these three possible rationales, concluding with a set of policy ideas with higher potential to deliver an energy secure today and a cleaner, more sustainable tomorrow.

A Strategy of “Outbidding Everyone” for Spot Cargoes Leads to Insecure Supply, Higher and More Volatile Prices, and Energy Transition Reversals

A broad European insistence on purchasing spot LNG cargoes today, rather than investing in supply for the future, has several deleterious impacts, each of which is likely to last for years to come.

Refusal to Invest in New Infrastructure Leads to Insecure Supply

The first signal is straightforward: LNG liquefaction terminals are expensive to build, and project financiers need long-term offtake agreements to defray the risk of projects that can cost billions of dollars and take decades to pay out. If key buyers will not sign long-term agreements, projects will either not get built at all, or else the pace of bringing new supplies to market will slow. At present, one group of large buyers (Europe) needs gas — and likely for longer than they publicly admit they will — but refuses long-term deals, while another large group of buyers (industrial Asia) understands that gas is likely to serve as a multi-decade energy transition bridge fuel and is signing long-term purchase agreements. The result is that Europe is more exposed to a supply disruption than are other LNG buyers. This risk was evidenced by the recent 40% intra-day run-up in prices at the European gas hub, TTF, on the mere mention of a possible labor strike at three of Australia’s ten LNG plants, none of which sell LNG directly to European customers.

European Buyers’ Apparent Readiness to Bid Up Prices Will Lead to More Price Volatility

European buyers’ general avoidance of long-term contracts signals that they will be willing to bid up prices when they need supplies. Paired with its continuing demand for LNG and refusal to meaningfully invest in new infrastructure, Europe’s “outbid everyone” LNG procurement strategy is a recipe for price volatility and higher prices — which the market already saw in 2021 and 2022. Indeed, it was only several months ago that French and German public officials complained of “astronomical prices” for LNG because Europeans were paying prices that were “3-4 times” what the gas cost in the domestic markets of LNG-exporting countries. LNG prices are lower today, but when Europe is relying on uncontracted volumes for potentially up to 60% of its future gas supply needs, price volatility will be a major risk for years to come.

Higher Gas Prices Will Lead Other Users to Double Down on Coal, Undercutting Global Climate Goals

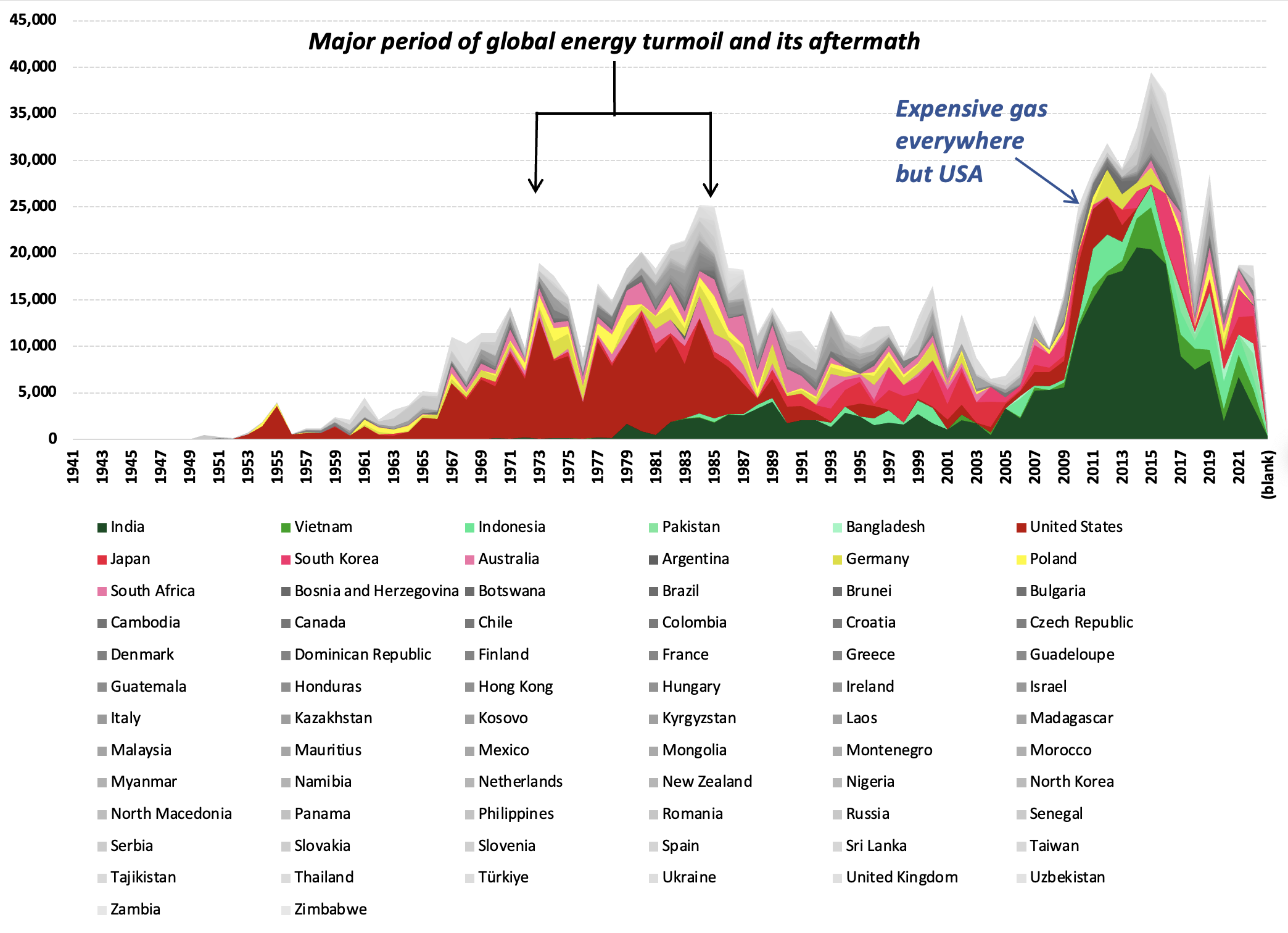

Higher energy prices will lead other energy users to diversify away from gas. Major swathes of the developing world, including the most populous and fastest-growing countries, would like to use more clean natural gas to feed growing energy demand. But while natural gas is a preferred fuel, if the energy services it provides become too expensive, coal generally fills the gap. Approximately 80 years of historical coal plant data from the Global Energy Monitor illustrate the relationship between energy insecurity, high global gas prices, and consumers choosing to double down on coal.

As shown in Figure 2, from 1973 through 1985, the country with the largest additions of coal-fired power plant capacity was the United States (shown in red). This period coincided with great energy insecurity in the United States, including the Arab oil embargo, the Iranian oil embargo, high inflation, declines in domestic oil and gas production, and high prices for imported fuel. The United States did not add comparable amounts of coal-fired capacity at any other time before or after. In comparison, Figure 2 shows that from 2009 to present, India and other Southeast Asian countries (shown in green) have added the largest amounts of coal-fired power capacity (China is not included in this graph, though their addition would probably amplify the observation that Asia was the dominant region for adding coal-fired capacity). This period coincides with minimal access for these countries to domestic natural gas and increasingly higher costs for imported LNG. In short, Figure 2 indicates a direct relationship between high natural gas prices and energy insecurity, on the one hand, and additions of coal-fired power capacity on the other hand.

Figure 2 — Global Coal Power Plant Capacity Additions, Excluding-China (MW annually), 1941-January 2023

Note MW = megawatt (one million watts).

As energy buyers outside of Europe — particularly countries in the Global South with large and growing energy needs but more limited financial means — face the prospect of EU buyers spiking LNG prices throughout the next several years, many will choose coal over energy poverty. Pakistan offers a recent case in point, having announced in February 2023 that it planned to quadruple its domestic coal-fired power capacity because it could not afford LNG in the wake of price run-ups triggered by Russia’s war against Ukraine and the demand of wealthy European and Asian buyers who were willing to pay higher prices for LNG.

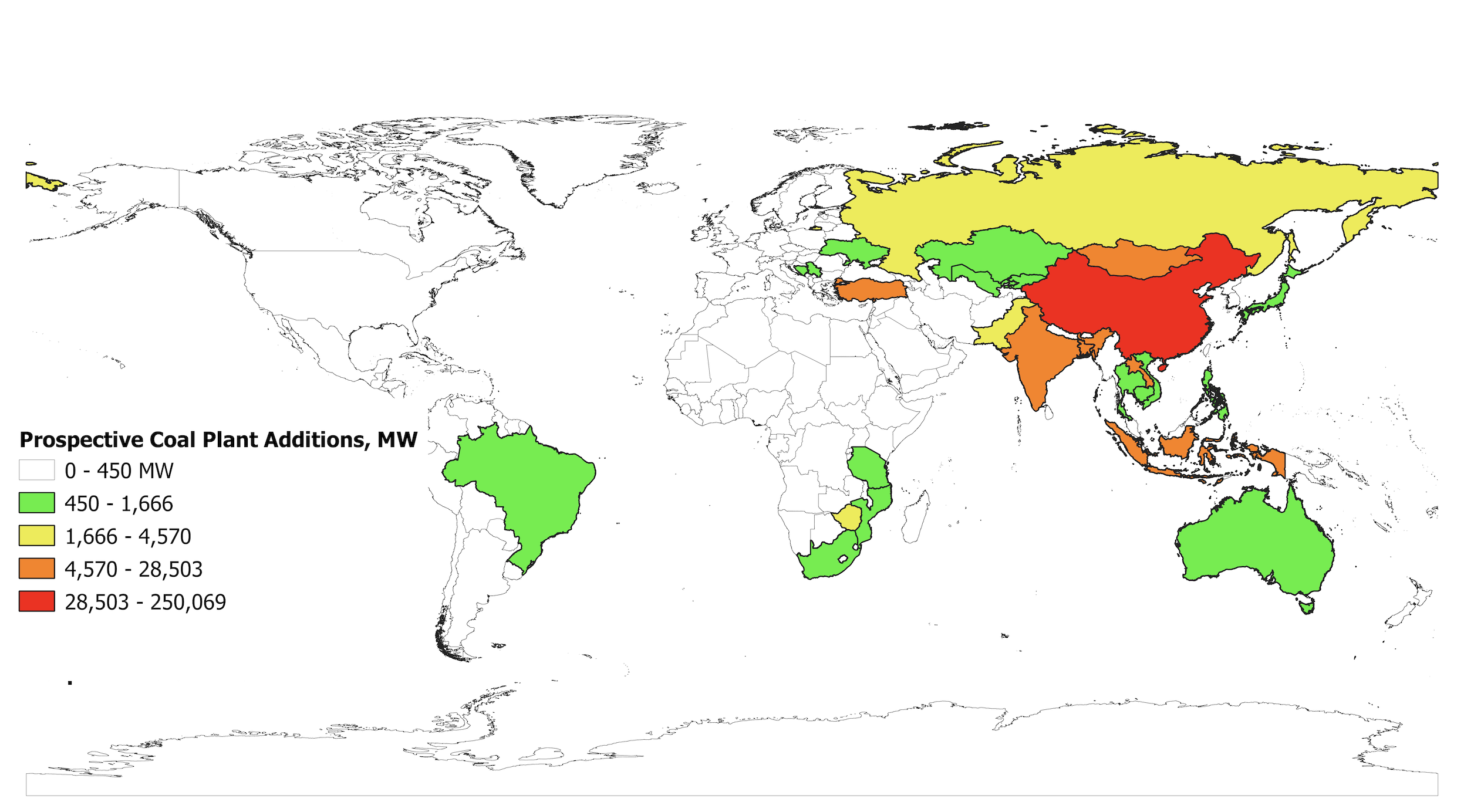

Such decisions are deeply consequential. Coal plants often run for 40-50 years, meaning that if European LNG buyers continue to avoid long-term supply deals, they risk obtaining gas for themselves (at a higher price) while locking in billions of metric tons of additional cumulative coal usage in China, developing Asia, and elsewhere between now and 2060-2070. The prospective coal plants shown in Figure 3 could conceivably be taken off the board if Europe committed to long-term contracts in lieu of secondary market purchases from existing projects, thereby expanding global LNG supplies leading to lower prices worldwide.

Figure 3 — Prospective Coal-fired Power Capacity by Country, in MW

Note Includes projects classified as announced, pre-permit, and permitted.

A “Clean” End to the War in Ukraine Is Unlikely

Some European gas buyers may be quietly assuming that the hostilities will soon end and that they will be able to resume the pre-war pattern of taking low-cost Russian gas through largely amortized pipelines, perhaps with a surcharge attached to help fund Ukraine’s reconstruction.[6] A possible precedent exists in the United Nations Iraq Oil for Food Program. Under such a scenario, Europe might not take the 200 bcm/year it did before the war, but something less — say, 100 bcm/year — with Russian producers knowing that supply cutoffs would face the credible threat of a demonstrated LNG import surge capacity through infrastructure expanded during the war.

For example, assuming annual sales of 100 bcm, a reconstruction surcharge of $50 per 1,000 cubic meters (roughly 25-30% of Gazprom’s pre-war price for customers outside the Commonwealth of Independent States) could raise $5 billion annually for Ukraine. However, that amount pales in comparison to the prospective cost of rebuilding what Russia has destroyed in Ukraine, with the World Bank estimating in March 2023 that the war’s first year alone wrought more than $400 billion in damage. Furthermore, raising a reconstruction surcharge high enough to generate more meaningful revenues would increase Russian natural gas costs to the point at which consumers would likely opt for LNG instead.

The War May Become Another Frozen Russian Conflict

Complicating matters further, a clean and stable World War II-style peace seems increasingly unlikely. Russia’s predilection for frozen conflicts along its periphery and its centuries-long tendency toward subjugating neighboring territories suggest that periodic flaring of conflict, drone and missile strikes, and sabotage is the more probable outcome, along with other forms of intermittent violence. This state of affairs could exist for years: The initial round of fighting is as likely to sow the seeds of follow-on wars as it is to create the foundations of durable peace.

A 2024 U.S. presidential election that resulted in reduced support to Ukraine would further amplify the risks. Unlike Azerbaijan or Georgia, which largely have to accept Russian territorial depredations and harsh unilateral settlements due to vast power disparities, Ukraine, even with less NATO support, would still be a formidable foe that could — and very likely would — fight back for years. Kyiv has the combat experience, motivation, resources, and weapons availability to run a hybrid hot war and insurgency far fiercer than what the Soviets encountered in Afghanistan during the 1980s. Russia would face years of violent resistance even east of the Dnieper River and might never be able to fully pacify areas west of it. Gas and oil pipelines would be inviting targets, as conflict in Colombia has shown.

East-West Conflict in Europe Could Make Complicate the Restoration of Flows

No matter how future violence plays out, it will have major impacts on the resumption of larger-scale gas commerce between Russia and Europe. Several EU members still substantially depend upon Russian gas, but the big question will center on whether Germany and other large Western European buyers might seek to resume imports. Given the low probability of a “clean,” mutually respected end to hostilities in Ukraine, trouble likely awaits. A push for renewed imports would become an especially pressing matter for East-West relations in Europe.

Without support from Poland and the Baltics, it is unlikely that the Nord Stream pipelines would be brought back online. For pipelines across Ukraine, Kyiv would likely attach stringent conditions. Ukrainian Energy Minister German Galushenko recently registered the country’s opposition to the current gas transit deal that allows Gazprom to ship 40 bcm/year through Ukraine, noting: “I believe, by the winter of 2024, Europe will not need Russian gas at all …. If [today’s] profits from Russian gas pay for Russia’s war of aggression against Ukraine and Gazprom’s private army, the only thing they should pay for in the future shall be reparations.”

Among other things, conflict over gas transit would invariably be influenced by an evolving European balance of power. Western Europe still has the largest economies, but they are besieged by high energy prices, gnawing deindustrialization and limited military vigor. Meanwhile, key parties in the East — Poland, the Baltics, and Ukraine among them — are adjusting their energy sourcing and gaining military strength. Eastern capitals may thus be less willing to support Russian gas procurement schemes that they see as emphasizing Western Europe’s economic expediency at the expense of the eastern flank’s hard security. Washington might back them with a renewed sanctions assault on Russian gas export projects, perhaps using the formidable powers contained in the 2017 Countering America’s Adversaries Through Sanctions Act (CAATSA). Indeed, an economic nationalist administration in the U.S. opposed to militarily supporting Ukraine might still see legal interdiction of Russian pipelines as a way to further American LNG exports. Firms that choose to try to resume imports of Russian gas might also find themselves in the crosshairs of private legal actions.[7] We express no opinion as to whether any such claim would be warranted by the facts or justified or sustainable under the law of any jurisdiction.

Emphasizing Renewables Over Long-term Gas Supplies Will Leave European Consumers Wanting — And Its Industries Uncompetitive

The REPowerEU plan promulgated by the European Union in 2022 emphasizes reducing energy consumption through immediate behavioral changes and longer-term structural energy efficiency measures, with a target of reducing gas usage by 30% by 2030. With the EU now more than two years into the gas shortages triggered by Russia, the trends are still preliminary. However, the data thus far strongly suggest that industrial curtailments, rather than true structural efficiency improvements, are thus far a primary driver of realized reductions in gas use.

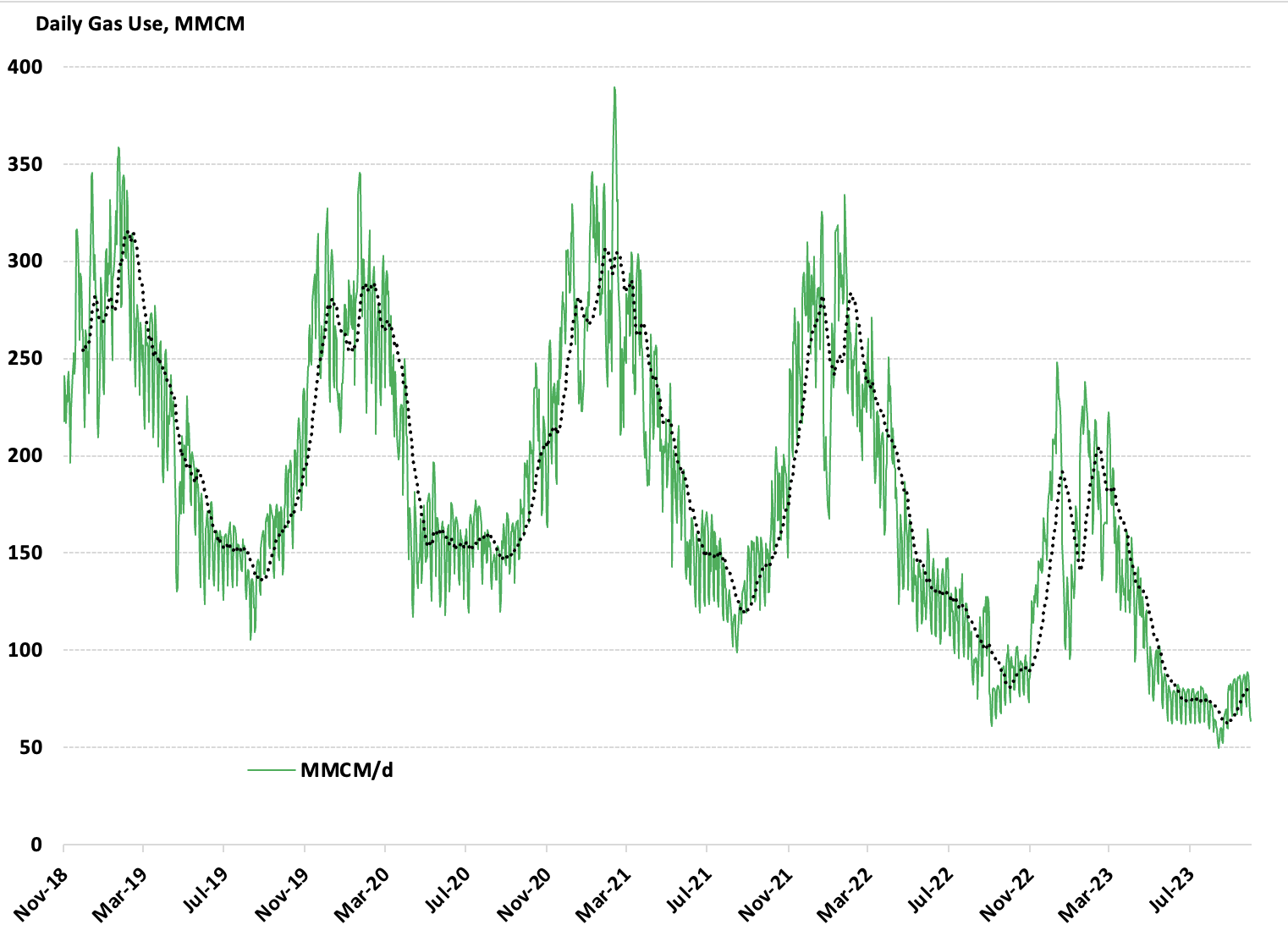

Figures from the Energy Institute’s Statistical Review of World Energy show that only two global regions experienced primary energy use decreases in 2022: Europe and the CIS. (The latter is dominated by a Russia at war and under severe sanctions.) Rapid, acute energy demand decreases, such as those experienced by Europe in 2022, are typically symptoms of a crisis — for instance, the global financial crisis of 2007-2009 or the 2020 pandemic lockdowns. Data show that a step change commenced in Europe in 2021 as Gazprom began cutting supplies and gas prices spiked.[8] Usage by these customers in Belgium, France, Italy, the U.K., the Netherlands, and Luxembourg has not recovered, and as of now sits at its lowest point in at least five years (Figure 4).

Figure 4 — Industrial Gas Deliveries by 14 Selected European Distributors, MCM/Day

Note MCM = million cubic meters of natural gas.

Depressed industrial demand for gas can have circular impacts as higher energy costs lead not only to depressed industrial demand but also to both inflation for individuals and recessionary impacts for the economy. Each of these can further erode industrial output and demand for energy.

Affordability Is Key

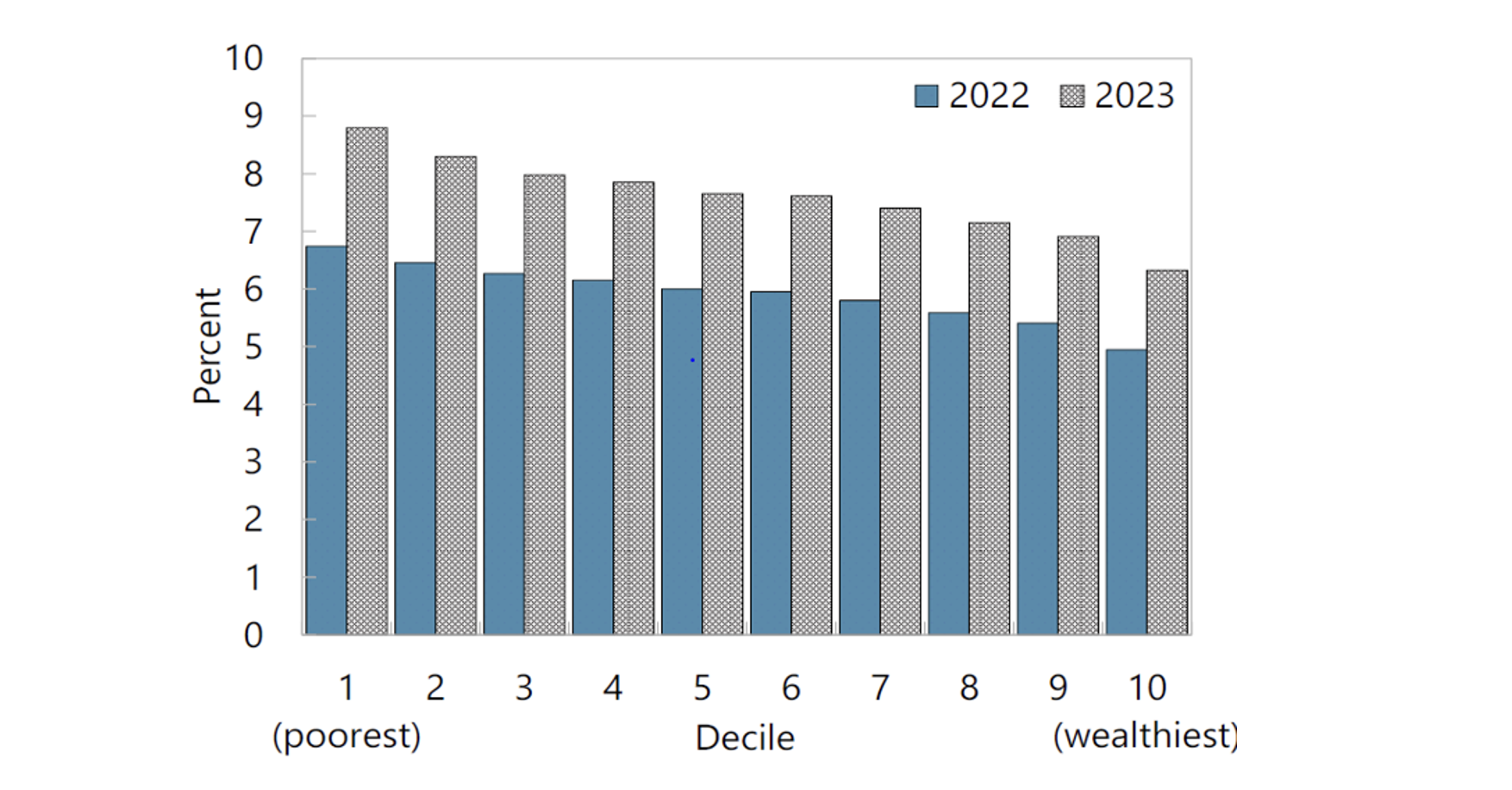

Looking solely at physical availability — as often emphasized by optimistic statements on how full European gas inventories are — neglects the critical dimensions of affordability. The history of commodity markets consistently reveals that for wealthier consumers, true physical unavailability of gas molecules is rare. As shown in Figure 5, the dark underside of that coin is that high costs of energy are borne disproportionately by lower-income individuals, while price-mediated rationing makes those molecules available to the biggest wallets. As this process unfolds, the wallets are left far lighter, and some of those with less means are saddled with the brutal decision of heating or eating.

Figure 5 — Increase in Households’ Cost of Living

Sources Bloomberg, ENTSOE, Eurostat, IMF staff calculations.

In addition to inflated costs and disproportionate impacts on lower-income persons, higher energy costs have recessionary impacts. Economic data suggest a strong association between elevated energy expenditures (equal to 10% of GDP or higher) and recession. The Organization for Economic Cooperation and Development countries — of which the eurozone is a major component — had end-use energy expenditures equal to about 17% of GDP in 2022. Many of the same underlying challenges persist in 2023 and are likely to continue going forward.

Hence, we caution that full inventories and incoming spot LNG cargoes do not reflect a healthy European energy situation.

Shuttered or Offshored Industrial Facilities Are Unlikely to Return Soon

Once industrial facilities shut down or are offshored to areas with lower energy costs like China, the Middle East, or the U.S., they likely are gone for many years, even decades. The only exception is when a formerly disfavored location experiences some type of radical transformation that structurally reduces energy costs. But such “energy input time machines” that can turn back the clock and bring industry back onshore are rare. America’s fracking boom, turning the country from a net energy importer to a leading energy exporter, is a rare exception over the past century.

European policymakers seem to think that by dramatically expanding renewable electricity production and replacing natural gas with hydrogen (itself generated using renewable energy), the continent can turn back the deindustrialization clock, which is now ticking fast. This approach faces substantial hurdles related to timing, scale, and costs associated with system change and intermittency. Accordingly, these will likely involve costs orders of magnitude more expensive than locking in long-term LNG supplies now. Leveraging gas as a bridge fuel while energy transitions can be marshaled in a rational manner will help to keep gas prices lower and could reduce or halt Europe’s slide towards deindustrialization.

Timing and Scale Are Critical

To keep its people warm this winter and to stem the accelerating deindustrialization, Europe needs affordable gas molecules now, six months from now, next year, and throughout the next decade. Otherwise, Europe’s reality risks being one in which gas prices stay higher longer than it can remain industrially competitive and politically solvent.[9] Each day that European companies eschew long-term LNG supply agreements despite consumers needing gas amplifies future supply pressures. Europe’s existing consumption of natural gas remains massive — roughly 23% of the Continent’s total primary energy usage in 2023, according to the Energy Institute’s Statistical Review of World Energy.

Even with the past 15 years’ massive renewables buildout, gas still supplies about 2.5 times as much primary energy to European consumers as wind and solar combined. This suggests wind and solar projects will not be able to build out fast enough to meaningfully reduce the role of gas as a core electricity fuel source between now and 2030.[10] To that point, multiple metrics paint an inauspicious picture for renewables to rapidly displace gas, as EU policymakers seem to hope for. Siting a large new windfarm in Europe has been estimated to take as long as 10 years. To increase capacity on the scale and timeframe required to avoid major system disruptions, Europe would need to be completing substantially more renewable projects than it currently is. However, with China-related supply chain challenges, critical mineral shortages, public resistance, and other obstacles, it is unlikely to meet its target. In fact, the EU Agency for Cooperation of Energy Regulators (ACER) reported that “orders for wind turbines in 2022 showed a year-on-year drop of total wind turbine orders in Europe by 47%” due to high prices and a shift of investment to other markets.[11] That in turn suggests gas will be far more important at all points during the next decade than popular EU-level political discussions and private sector inaction on long-term LNG contracts would suggest.

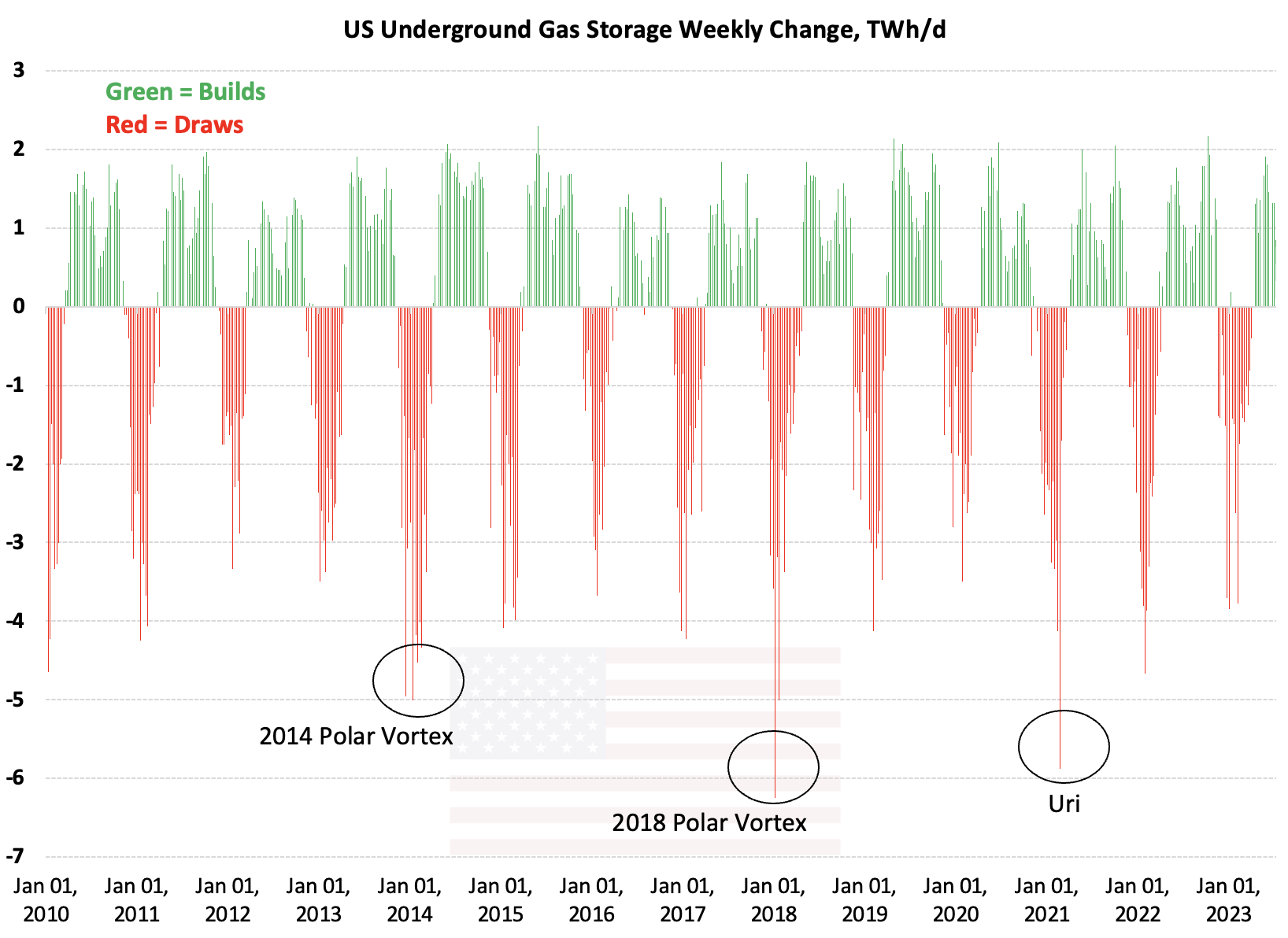

Finally, even if the “green dream” of some EU policymakers were to come to fruition with trillions of euros committed to new windfarms and solar installations, intermittency remains an issue — and its impacts will only be magnified the more deeply Europe seeks to electrify. The more renewables that are deployed, the more important gas will become as a battery to balance the energy system during both normal operations and extreme weather events. Looking at past extreme weather events in the United States (whose energy system is about 25% larger than Europe’s) suggests that at the peak of severe polar vortex and multistate winter storm events, consumers can withdraw 5-6 terawatt-hours (TWh)/day of gas from storage each week on average (see Figure 6).[12] Adjusting that to 4 TWh/d for Europe’s smaller energy system would still invoke an average incremental load of nearly 170 GW (and substantially higher instantaneous demand spikes) against the roughly 52 GW of energy storage capacity available from all sources currently reported operational in the EU.[13]

Figure 6 — Gas Is Currently an Irreplaceable Energy System Balancer

Key Assumptions 1 BCF/d = 0.29 TWh. Gas is burned in peaker power plants with a 42% thermal efficiency rating.

Europe’s current non-fossil battery/non-fossil fuel storage capacity is thus nowhere near what the continent’s economies and consumers would require. “Green” hydrogen has been discussed in the EU as an alternative form of backup power, but is unlikely to reach scale in the next dozen years, as Germany has set 2035 as the date when its LNG receiving terminals and its electric power grid will be ready to replace LNG with hydrogen made from renewable energy. In an era of strained public finances, the vast quantities of capital that will likely be required to incentivize and support the construction of additional wind and solar capacity, plus several non-carbon storage resources, is bound to prove fiscally and politically challenging, at best.

This means that gas will likely continue to be the core system balancer. Whether that gas will be procured at higher spot market prices or lower prices — through long-term agreements that incentivize additional supply by giving gas producers and their shareholders a clearer view of the future — remains to be seen. What is more clear is that even though gas is likely to remain a core transition fuel into 2050 and beyond,[14] many European customers are setting themselves up for a challenging period to come through indecision and not signing long-term contracts To that point, the recent deal that BASF signed with Cheniere for 1.1 bcm/year of LNG, or about 1/3 of the annual needs for its Ludwigshafen complex, bears close observation. [15] It may be a harbinger of things to come as more eurozone businesses conclude that locking in stably-priced gas supplies is an existential matter of business survival.

Conclusion and Policy Recommendations

Given the economic threat caused by the sudden loss of nearly 200 bcm/year of Russian gas, Europe could have used the period from the spring of 2022 to the summer of 2023 to sign long-term LNG supply contracts. To their credit, Europe made impressive strides in building onshore and chartering offshore LNG receiving terminals in several countries, dramatically increasing Europe’s capacity to receive LNG. However, they did not make comparable investments at scale to lock in supplies to bring LNG to those terminals. Doing so would have allowed European buyers to avoid the risk of an interruption or of having to outbid China, Japan, South Korea, and Taiwan for half or more of Europe’s winter cargoes. U.S. and European leaders have met with much publicity, and U.S. LNG sellers and European buyers have talked about contracting for long-term supplies of LNG from the U.S. Our research has revealed, however, that from the date of the invasion through June 2023, less than 15 billion cubic meters per annum (bcma) of new long-term LNG purchase contracts for delivery to Europe were signed — from all suppliers worldwide.

The upside is that the present gas quandary can be solved at a relatively low cost. The import infrastructure for LNG already largely exists, as do pipelines, underground storage caverns, and consumer facilities designed for gas use. LNG markets have demonstrated that LNG purchased under long-term sales contracts can be more secure and less volatile than relying solely on the spot market for large quantities over long periods of time. Signing long-term LNG purchase agreements sends signals to the many trillions of dollars in capital around the world still willing to Invest in gas resource development that buyers have given a 20-25 year forward window. Those investors will respond — and respond, we expect, with formidable velocity and effectiveness — just as they have done in Qatar, in Appalachia, in the Permian Basin, on the Northwest Shelf, in East Africa, and in other global gas provinces. Increased supplies should yield lower prices over time and help wean countries and companies off coal.

Diversity and Affordability Are Vital

Winston Churchill counseled on the eve of World War I that “safety and certainty in oil lie in variety and variety alone.” More than a century later, his words aptly describe the solution for gas security (and energy security overall). Diversity and affordability are central to European citizens’ individual well-being in a world of cold snaps and heat waves, as well as to their employers and home countries’ capacity to maintain global industrial competitiveness.

Energy Security Must Be Prioritized

Besides needing to deal with severe weather events and industrial competition, Europe is up against a harsh geopolitical backdrop: While Russia squeezes the continent through energy cutoffs and active warfare, China is working to supplant German and other European concerns at the pinnacle of precision manufacturing with its state-owned enterprises.

The impacts of Europe’s ongoing energy crunch are a “here and now” certainty. As Russia’s weaponization of gas in the run-up to its 2022 invasion of Ukraine strongly suggests, robustly tending to energy security is an essential prerequisite for warding off other types of serious security risks. Energy security is national security. Energy action requires long lead times, and putting off decisions in the hopes of warm winters, technological unicorns, and peaceful adversaries is not a strategy.

References

Abnett, Kate. “Europe's spend on energy crisis nears 800 billion euros.” Reuters. February 13, 2023. https://www.reuters.com/business/energy/europes-spend-energy-crisis-nears-800-billion-euros-2023-02-13/.

ACER. “Assessment of Emergency Measurements in Electricity Markets; 2023 Market Monitoring Report.” July 14, 2023. https://acer.europa.eu/Publications/2023_MMR_EmergencyMeasures.pdf.

“An Act To provide congressional review and to counter aggression by the Governments of Iran, the Russian Federation, and North Korea, and for other purposes.” HR 3364. https://www.govinfo.gov/content/pkg/BILLS-115hr3364enr/html/BILLS-115hr3364enr.htm.

Arregui, Nicolas, Oya Celasun, Dora M Iakova, Aiko Mineshima, Victor Mylonas, Frederik G Toscani, Yu Ching Wong, Li Zeng, and Jing Zhou. “Targeted, Implementable, and Practical Energy Relief Measures for Households in Europe” IMF Working Paper. December 16, 2022. https://www.imf.org/en/Publications/WP/Issues/2022/12/17/Targeted-Implementable-and-Practical-Energy-Relief-Measures-for-Households-in-Europe-526980.

Barnard, Geoff, and Patrice Ollivaud. “Energy expenditures have surged, posing challenges for policymakers.” Ecoscope. January 20, 2023. https://oecdecoscope.blog/2023/01/20/energy-expenditures-have-surged-posing-challenges-for-policymakers/.

Cheniere. “Cheniere and BASF Sign Long-Term LNG Sale and Purchase Agreement.” Press release. August 22, 2023. https://lngir.cheniere.com/news-events/press-releases/detail/284/cheniere-and-basf-sign-long-term-lng-sale-and-purchase.

Collins, Gabriel. 2017. Russia’s Use of the “Energy Weapon” in Europe. Issue brief no. 07.18.17. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/russias-use-energy-weapon-europe.

Collins, Gabriel, and Anna Mikulska. 2018. “Gas Geoeconomics in Europe.” Research paper 05.18. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/sites/default/files/2018-06/import/ces-pub-gasgeoeconeurope-060318.pdf.

Collins, Gabriel, Kenneth B. Medlock III, Anna Mikulska, and Steven R. Miles. 2022. “Send Lawyers, (Gas) And Money: Executive Summary for ‘Strategic Response Options if Russia Cuts Gas Supplies to Europe’.” Research paper 02.11.22. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/strategic-response-options-if-russia-cuts-gas-supplies-europe.

Collins, Gabriel, Anna Mikulska, and Steven Miles. 2022. Winning the Long War in Ukraine Requires Gas Geoeconomics. Research paper no. 08.25.22. Rice University's Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/winning-long-war-ukraine-requires-gas-geoeconomics-0.

Collins, Gabriel and Anna Mikulska. 2020. “Trans-Atlantic Gas Diplomacy 2.0: Molecule-indifferent Gas Geoeconomics, Not Energy Sanctions, are the Best Option to Harden Europe Against Russian Gas Coercion.” Research paper no. 10.01.2020. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/molecule-indifferent-gas-geoeconomics-not-energy-sanctions-are-best-option-harden-europe-against-rus.

Collins, Gabriel, and Steven R. Miles. “China’s Big Gas Bet Raises Questions About Complicity With Russia.” Foreign Policy. June 12, 2023. https://foreignpolicy.com/2023/06/12/china-natural-gas-russia-ukraine-war-energy/.

Cope, Sophia and Cindy Cohn. “Victory! Ninth Circuit Allows Human Rights Case to Move Forward Against Cisco Systems.” Electronic Frontier Foundation. July 12, 2023. https://www.eff.org/deeplinks/2023/07/victory-ninth-circuit-allows-human-rights-case-move-forward-against-cisco-systems.

Department of Defense. “Fact Sheet on U.S. Security Assistance to Ukraine.” July 18, 2023. https://media.defense.gov/2023/Jul/19/2003263170/-1/-1/1/UKRAINE-FACT-SHEET.PDF.

Electric Reliability Council of Texas. “Interval Generation by Fuel Report.” N.d. https://www.ercot.com/files/docs/2023/02/07/IntGenbyFuel2023.xlsx.

Euroindicators. “May 2023 compared with April 2023: Industrial production up by 0.2% in the euro area and by 0.1% in the EU.” Eurostat. 13 July 2023. https://ec.europa.eu/eurostat/documents/2995521/17153235/4-13072023-AP-EN.pdf/7af118ab-e6f3-a316-213f-23c2babc6be6.

European Commission. “Commission proposes new list of Projects of Common Interest for a more integrated and resilient energy market.” Press release. November 19, 2021. https://ec.europa.eu/commission/presscorner/detail/en/IP_21_6094.

“Gasunie Unit Converter,” https://unit-converter.gasunie.nl/.

Gavin, Gabriel. “Ukraine warns key Russian gas supply to Europe will be cut.” Politico. July 12, 2023. https://www.politico.eu/article/ukraine-warns-it-wont-negotiate-new-russian-gas-transit-deal/.

“German Natural Gas Market Balance Dashboard.” N.d. Interactive dashboard developed by Miaomiao Rimmer and Luke (Leelook) Min. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/german-natural-gas-market-balance-dashboard.

Hartley, Peter R., and Kenneth B. Medlock. “Potential Futures for Russian Natural Gas Exports.” The Energy Journal 30 (2009): 73–95. http://www.jstor.org/stable/41323197.

Masterson, Victoria. “How much will it cost Europe to switch to clean energy by 2050?” World Economic Forum. April 27, 2022. https://www.weforum.org/agenda/2022/04/bnef-european-energy-transition-2022.

Medlock, Kenneth Barry. "Modeling the implications of expanded US shale gas production," Energy Strategy Reviews, Volume 1, Issue 1, 2012, Pages 33-41, ISSN 2211-467X, https://doi.org/10.1016/j.esr.2011.12.002.

Miles, Steven R., and Anna Mikulska. 2022. “Who’s To Blame For Exorbitant Natural Gas Prices In Europe? Hint: Maybe Not Who You Think.” Commentary 10.26.22. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/whos-blame-exorbitant-natural-gas-prices-europe-hint-maybe-not-who-you-think.

Miles, Steven R., and Gabriel Collins. 2022. A Bridge Over Troubled Water: LNG FSRUs Can Enhance European Energy Security. Issue brief no. 03.29.22. Rice University’s Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/a-bridge-over-troubled-water-lng-fsrus-can-enhance-european-energy-security.

Miles, Steven R., Gabriel Collins, and Anna Mikulska. 2022. “US Needs LNG to Fight a Two-Front Gas War.” Report 08.18.22. Rice University's Baker Institute for Public Policy, Houston, Texas. https://www.bakerinstitute.org/research/us-needs-lng-fight-two-front-gas-war.

Oltermann, Philip. “How gas rationing at Germany’s BASF plant could plunge Europe into crisis.” The Guardian. September 15, 2022. https://www.theguardian.com/business/2022/sep/15/gas-rationing-germany-basf-plant-europe-crisis.

Peshimam, Gibran Naiyyar. “Exclusive: Pakistan plans to quadruple domestic coal-fired power, move away from gas.” Reuters. February 13, 2023. https://www.reuters.com/business/energy/pakistan-plans-quadruple-domestic-coal-fired-power-move-away-gas-2023-02-13/.

Rogers, Iain. “Germany to Tender for 8.8 Gigawatts of Hydrogen Power Plants.” Bloomberg. August 1, 2023. https://www.bloomberg.com/news/articles/2023-08-01/germany-to-tender-for-8-8-gigawatts-of-hydrogen-power-plants#xj4y7vzkg.

Skove, Sam. “US paying contractor to quietly supply Bulgarian 155mm shells to Ukraine.” Defense One. July 13, 2023. https://www.defenseone.com/threats/2023/07/us-paying-contractor-quietly-supply-bulgarian-155mm-shells-ukraine/388480/.

Swiss Federal Office of Energy. “Energy Consumption in Switzerland 2022.” N.d. https://www.bfe.admin.ch/bfe/en/home/supply/statistics-and-geodata/energy-statistics/overall-energy-statistics.html/.

“Statistical Review of World Energy” downloadable from “Resources and Data Downloads” page of Energy Institute’s website. Accessed September 5, 2023, https://www.energyinst.org/statistical-review/resources-and-data-downloads.

United Nations Human Rights Office of the High Commissioner, “Conflictrelated civilian casualties in Ukraine,” January 27, 2022, https://bit.ly/3QNQ4uq.

U.S. Energy Information Administration. “Country Analysis Executive Summary: Colombia.” March 31, 2022. https://www.eia.gov/international/content/analysis/countries_long/Colombia/pdf/colombia_exe.pdf.

U.S. Energy Information Administration. “Carbon Dioxide Emissions Coefficients.” October 5, 2022. https://www.eia.gov/environment/emissions/co2_vol_mass.php.

WindEurope, 2023, Wind Turbine Orders Monitoring. 2022 Statistics. https://windeurope.org/intelligence-platform/product/windturbine-orders-monitoring-2022/#interactive-data.

World Bank. “Updated Ukraine Recovery and Reconstruction Needs Assessment.” Press release. March 23, 2023. https://www.worldbank.org/en/news/press-release/2023/03/23/updated-ukraine-recovery-and-reconstruction-needs-assessment.

Yergin, Daniel. “Ensuring Energy Security.” Foreign Affairs 85, no. 2 (2006): 69–82. https://doi.org/10.2307/20031912.

Endnotes

[1] This analysis reflects personal opinions and assessments only. It is not an investment analysis or investment advice. It is also not offering any legal opinion or advice and does not create an attorney-client relationship with any reader or consumer of the information presented herein. Readers rely on the information in this analysis at their own risk.

[2] What do we mean by a “gas Grand Canyon”? We’re referring to a huge deficit in contracted gas supplies over expected demand. An energy crisis was largely avoided over the 2022-23 European winter based on substantial curtailment of industrial demand, the good fortune of warmer-than-normal temperatures, and the sudden redirection and supply of LNG exports, largely from the United States and also Qatar. In the first four months of 2022, 74% of all U.S. LNG production swung to Europe, ultimately seeing the continent into the summer and helping to fill its storage tanks in advance of the winter of 2022.

[3] United Nations Human Rights Office of the High Commissioner, “Conflictrelated civilian casualties in Ukraine,” January 27, 2022, https://bit.ly/3QNQ4uq.

[4] European Commission, “Key cross border infrastructure projects,” https://energy.ec.europa.eu/topics/infrastructure/projects-common-interest/key-cross-borderinfrastructure-projects_en#the-pci-list. Projects of Common Interest can benefit from accelerated planning and permit granting, a single national authority for obtaining permits, improved regulatory conditions, lower administrative costs due to streamlined environmental assessment processes, increased public participation via consultations, increased visibility to investors, and the right to apply for funding from the Connecting Europe Facility (CEF).

[5] A subsequent Projects of Commons Interest list released in November 2021 notes that “No new gas infrastructure project is supported by the proposal. The few, selected gas projects, which have already been on the 4th PCI list, are projects that are necessary to ensure security of supply for all Member States. A strengthened sustainability assessment has led to a number of gas projects being dropped from the list.” See “Commission proposes new list of Projects of Common Interest for a more integrated and resilient energy market,” European Commission, November 19, 2021, https://ec.europa.eu/commission/presscorner/detail/en/IP_21_6094. There is currently a call outstanding for the next round of PCI projects that will close in early September 2023, When that 6th list will be published is currently unclear.

[6] From authors’ private conversations with multiple well-placed European interlocutors, June and July 2023.

[7] See, for instance, Sophia Cope and Cindy Cohn, “Victory! Ninth Circuit Allows Human Rights Case to Move Forward Against Cisco Systems,” Electronic Frontier Foundation, July 12, 2023, https://www.eff.org/deeplinks/2023/07/victory-ninth-circuit-allows-human-rights-case-move-forward-against-cisco-systems. (The judicial opinion is here: https://cdn.ca9.uscourts.gov/datastore/opinions/2023/07/07/15-16909.pdf).

[8] The data was reported by the European Network of Transmission System Operators for Gas (ENTSOG) for deliveries by 14 key gas distributors to industrial customers across Western Europe.

[9] This borrows from John Maynard Keynes’ iconic remarks on financial speculation: “The market can remain irrational longer than you can remain solvent.”

[10] We will be following this report up with another analysis that more deeply examines the prospects for, and challenges faced by, attempts to effectively replace gas with wind and solar energy in Europe.

[11] See ACER, “Assessment of Emergency Measurements in Electricity Markets; 2023 Market Monitoring Report,” 14 July 2023 (acer.europa.eu/Publications/2023_MMR_EmergencyMeasures.pdf), para. 62 & n. 28, citing WindEurope, 2023, Wind Turbine Orders Monitoring. 2022 Statistics. https://windeurope.org/intelligence-platform/product/windturbine-orders-monitoring-2022/#interactive-data.

[12] A terawatt-hour is equivalent to 1,000,000 megawatt-hours (MWh).

[13] For more information see “Database of the European energy storage technologies and facilities,” European Commission, current as of 25 July 2023, https://data.europa.eu/data/datasets/database-of-the-european-energy-storage-technologies-and-facilities?locale=en.

[14] See, for instance: https://www.weforum.org/agenda/2022/04/bnef-european-energy-transition-2022/.

[15] “Cheniere and BASF Sign Long-Term LNG Sale and Purchase Agreement,” Cheniere, August 22, 2023, https://lngir.cheniere.com/news-events/press-releases/detail/284/cheniere-and-basf-sign-long-term-lng-sale-and-purchase. Media report that the Ludwigshafen complex consumes approximately as much gas as Switzerland, which according to Swiss government data consumed 34,029 GWh or 3.48 billion cubic meters in 2021. Philip Oltermann, “How gas rationing at Germany’s BASF plant could plunge Europe into crisis,” The Guardian, September 15, 2022, https://www.theguardian.com/business/2022/sep/15/gas-rationing-germany-basf-plant-europe-crisis; “Energy Consumption in Switzerland 2022,” https://www.bfe.admin.ch/bfe/en/home/supply/statistics-and-geodata/energy-statistics/overall-energy-statistics.html/; converted from GWh to BCM using Gasunie’s eminently helpful online conversion tool “Gasunie Unit Converter,” https://unit-converter.gasunie.nl/.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.