Author(s)

The 2024 edition of the Energy Institute’s “Statistical Review of World Energy” was published last week, an annual tradition dating to 1952. As a former project manager for the review, when it was produced by bp, I always look forward to this publication and to my annual commentary.

The review contains objective data on the global energy system — everything from coal demand to lithium production and carbon prices. Its data is freely available for download and is widely used by researchers in industry, government, and the media. I would be doing you a huge disservice if I did not advise you to have a look at its extensive data for yourself!

The Energy Institute and its partners do a good job of summarizing the data and relating the global energy stories of 2023 — as always, the review is a historical document with annual data through last year. So my job here is to bring up a few additional topics, rather than to fully summarize the global energy picture.

And what I see are some new wrinkles, and a lot of continuity — resulting in a mixed message.

Green Energy at Scale and Going Global

So what’s new? To me, one of the biggest stories in global energy last year was that the production of renewable energy sources — primarily wind, solar, and biofuels — accounted for a larger growth increment (measured in exajoules, EJs) than any other energy form (Figure 1).[1] To be fair, this also happened in 2020, but that was the pandemic year, when global energy supply and demand fell sharply. Last year, in contrast, was a growth year for global energy, with total energy, oil and coal production all growing faster than their 10-year average rates. And yet renewables — which grew broadly in line with their historical rate — still saw the largest increase in production (in EJs), showing that they are achieving scale in the global energy system.

Figure 1 — Changes in Energy Production, 2019–23 (Exajoules)

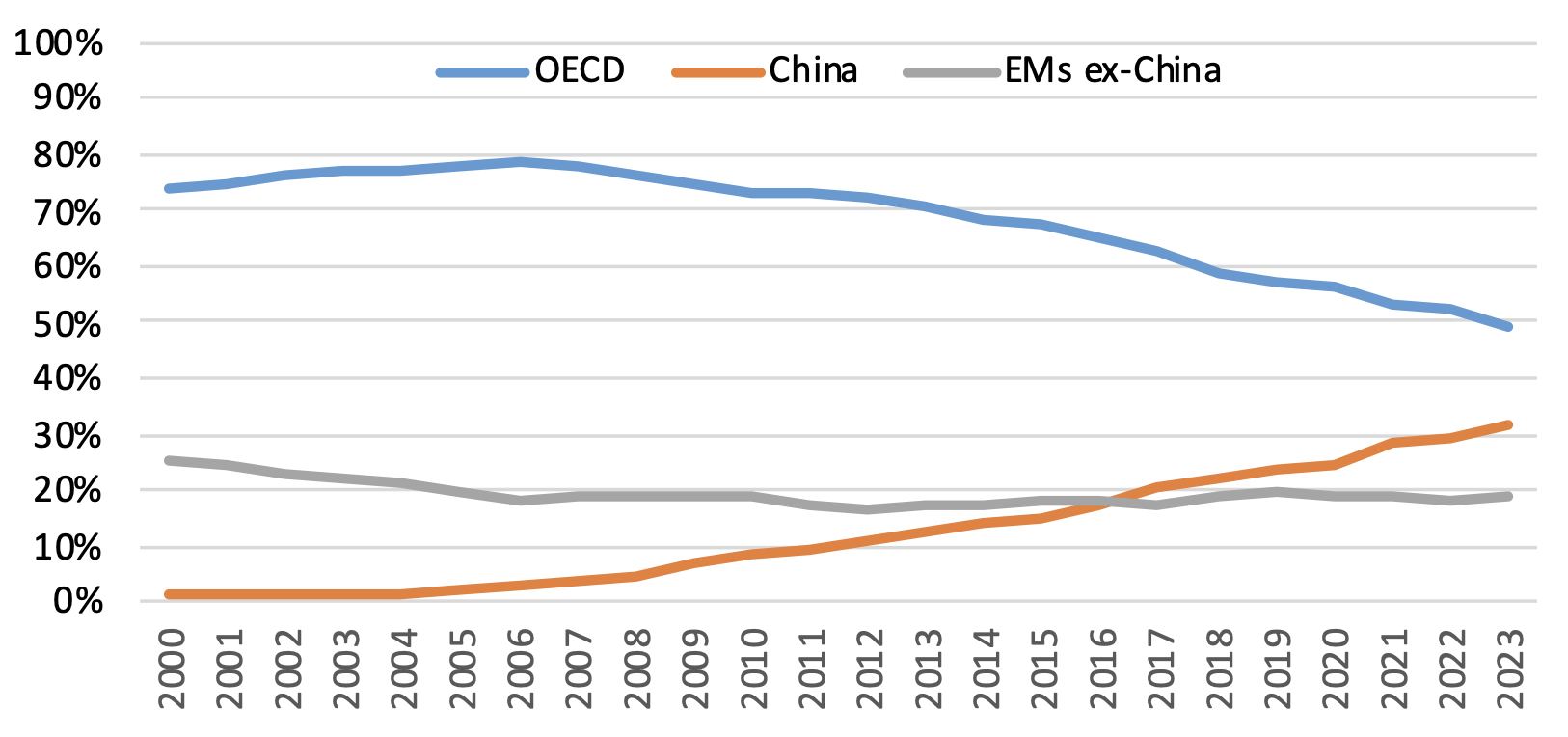

Another important dimension to the renewables story is their increasingly global nature. Last year, for the first time, the majority of renewable energy was produced and consumed outside the mature economies of the Organisation for Economic Co-operation and Development (OECD). And while China dominates this story, accounting for nearly one-third of global renewables use, other emerging economies are increasingly important in the mix. As a group, these countries accounted for 19% of global renewable energy use, and saw a bigger growth increment (in EJs) last year than either the EU or the U.S.

Figure 2 — Shares of Renewable Energy Use

Energy ‘Addition’ Not ‘Transition’

Even as renewables continued to grow rapidly, the 2023 data also shows that oil, natural gas, and coal all grew. Indeed, oil and coal hit all-time records — with gas just slightly below the 2021 peak before Russian supply dropped sharply after the invasion of Ukraine. Globally, fossil fuels continue to account for more than 80% of global energy production and consumption, with (non-hydro) renewables accounting for just 8% of global energy, even with their rapid growth.

And with rising fossil fuel use, CO2 emissions from energy also hit an all-time high, rising by 1.6%, more than double the 10-year average rate. As did overall energy-related CO2-equivalent emissions from “energy, process emissions, methane and flaring,” which, as the Energy Institute notes, surpassed the equivalent of 40 gigatonnes of CO2 last year.

As others have noted, recent experience suggests we live in a world of energy “addition” rather than “transition” — and 2023 data in aggregate reinforced that notion. The rapid growth of renewable energy may be eroding the market share of fossil fuels, but it is not, so far, reducing actual fossil fuel demand or emissions.

Who Is Powering Global Energy Supply Growth? You Might Be Surprised

U.S. energy production continued to grow rapidly in 2023 (+4.2 EJs, or +4.3%, well above the 10-year average growth rate of 2.9%). Domestic oil output saw the largest increase in the world once again, rising by +1.5 million barrels per day (Mb/d) to reach a record 19.4 Mb/d — the highest production of any country in history.[2] Last year’s output was a massive 8 Mb/d higher than the next largest producer, Saudi Arabia. Natural gas output rose by 4.2% (a slightly below-average growth rate) to exceed 100 billion cubic feet per day for the first time. U.S. natural gas production in 2023 was nearly as large as the combined second-, third-, and fourth-largest producers (Russia, Iran, and China).

Overall, U.S. domestic energy production growth exceeded the increase in domestic consumption, making the U.S. an even larger net energy exporter (Figure 3). In 2023, the U.S. surpassed Qatar and Australia to become the world’s largest exporter of liquefied natural gas (LNG) and remained by far the largest exporter of refined petroleum products, and a net exporter of oil — crude and refined products.

Figure 3 — Energy Self-Sufficiency

Note: Domestic production as a share of consumption.

And yet, the U.S. actually lost ground in 2023, in energy terms, to the world’s biggest energy producer — China. China’s dominance of global energy production is largely due to its enormous production of coal. It produces more than half of the world’s coal, more than five times as much as the world’s second-largest producer, India. Chinese energy production grew by 4.6 EJs, or by 3.3% last year, broadly in line with the 10-year average rate. The country accounted for 23% of global energy production last year — far beyond the 16% accounted for by the U.S., the second-largest producer. Chinese production increased for every form of energy except hydro. Like much of the world, China experienced drought conditions last year. Even with increased production, the strength of domestic energy demand (+6.5%, nearly double the 10-year average) meant that Chinese imports of oil, natural gas, and coal all increased, and the country’s overall energy self-sufficiency worsened, breaking a recent improving trend.

Figure 4 — 2023 Energy Production (Exajoules)

Indeed, China and the U.S. combined accounted for roughly two-thirds of global energy production growth last year — as they have on average for the past decade — by far the largest sources of growth on the planet.

Unlike energy production, where the two countries have been growing robustly, the consumption paths have diverged. Chinese energy consumption growth last year accounted for a massive 85% of global growth, while U.S. energy use declined. Over the past decade, Chinese consumption has accounted for roughly 60% of global energy consumption growth, while U.S. consumption has been essentially flat. Indian energy consumption (+2.6 EJs, or +7.3%) recorded the world’s second-largest increase last year — as it has done on average over the past decade. While many analysts expect India to become the leading force for energy demand growth, for now, China remains the engine for global energy demand growth.

Note that while China remained by far the world’s largest importer of fossil energy, the review data also shows that it maintained its dominance of metals and new energy materials in 2023 — materials needed for the much hoped-for transition to a lower-carbon energy system in the future. In addition to leading the world in wind and solar power generation, the data shows that China also led the world in grid-scale battery energy storage systems and production of rare earth metals and graphite. As well as leading in the production of electric vehicles, batteries, wind turbines, solar panels, and the processing and refining of metals, which the review does not report.

Bottom Line: On One Hand … on the Other

At this point, many of you probably feel like Harry Truman famously did about us economists. And yet the data in the “Statistical Review” speaks for itself. While it shows that renewable energy forms continue to grow rapidly, and that their growth is diversifying beyond the OECD, the review also shows that fossil fuels continue to grow, along with CO2 emissions. It shows that China and the U.S. continue to dominate global energy production growth and that China continues to lead the global growth in energy consumption — last year, fueled by rising imports, even in a world with a heightened focus on energy security and domestic supply chains.

As always, the data tells many stories. I have picked a few that seemed important to me, but the power of the review is that you can look for yourself, and tell your own stories. With a spate of recent commentary on the difficulty of finding high-quality data, the service provided by the Energy Institute and its partners is laudable. Like the review, the Baker Institute Center for Energy Studies focuses on rigorous, objective analysis to support energy decision-makers in industry and government — for today’s energy challenges as well as tomorrow’s.

Notes

[1] This analysis excludes hydroelectricity, which the review reports separately. Hydropower does not emit CO2 but involves more mature technology with fewer opportunities for growth. Additionally, while the Statistical Review of World Energy has data on production of each form of energy, it does not aggregate them to track total primary energy production — as it does for total primary energy consumption; the review defines primary energy as comprising “commercially-traded fuels, including modern renewables used to generate electricity” (Energy Institute, Statistical Review of World Energy, 2024, https://www.energyinst.org/__data/assets/pdf_file/0006/1542714/EI_Stats_Review_2024.pdf). In a previous commentary, I explained the process by which I calculate global primary energy production (Mark Finley, “Shock Finding? China Is The World’s Biggest Energy Producer,” Forbes, June 19, 2020, https://www.forbes.com/sites/thebakersinstitute/2020/06/19/todays-quiz-who-is-the-worlds-largest-energy-producer/#4b7e25aa7c13).

[2] The U.S. Energy Information Administration (EIA) also reports that domestic refineries added processing gains of 1 Mb/d in 2023 and that the U.S. also produced 1.3 Mb/d of biofuels, taking total domestic product supplied well above 20 Mb/d (“Monthly Energy Review,” June 2024, https://www.eia.gov/totalenergy/data/monthly/pdf/sec3_3.pdf).

Members of the Baker Institute Center for Energy Studies receive advance access to expert analysis and commentaries. Learn more about becoming a member of the Energy Forum.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.