Author(s)

This article is also featured in Energy Insights, which reflects a sample of ongoing research across the Center for Energy Studies’ diverse programmatic areas, all addressing the ever-evolving energy challenges across Texas, the U.S., and the globe. Read more from the inaugural edition.

A Need for Critical Minerals

Reaching global net-zero goals by 2050 requires a significant transformation of the energy mix toward cleaner energy sources and technologies. Therefore, it requires greater supplies of critical minerals, which include copper, nickel, cobalt, lithium, and rare earths. Electrifying economies in ways that reduce the use of hydrocarbon fuels supposes not only massive expansion of the electricity transmission networks, but also large deployment of storage and battery technologies and significant presence of electric vehicles (EVs). These changes also require much larger amounts of minerals and materials; for instance, an EV requires six times more minerals than the typical internal combustion energy vehicle.[1]

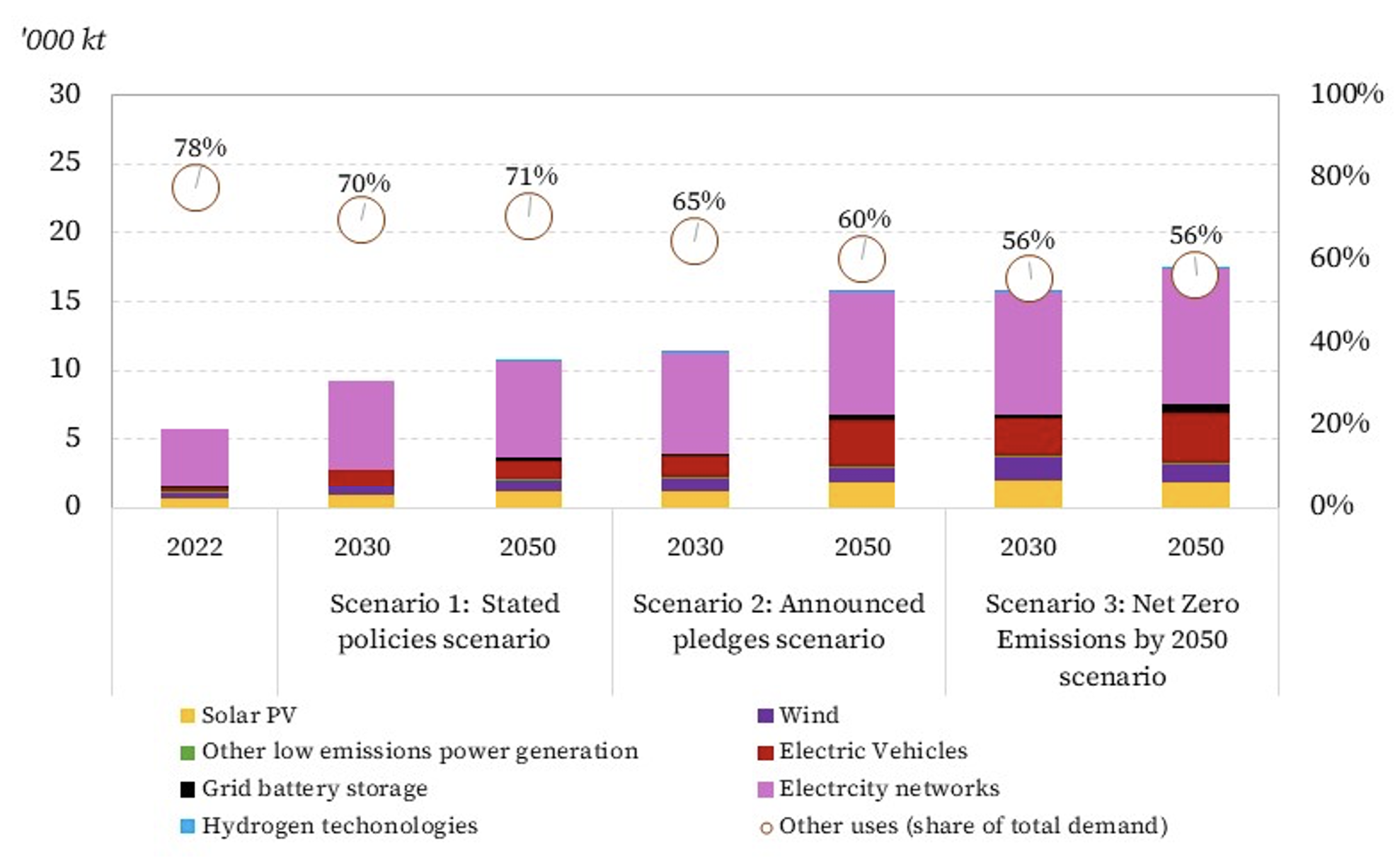

Figure 1 — Expected Copper Demand to 2050 by Scenario

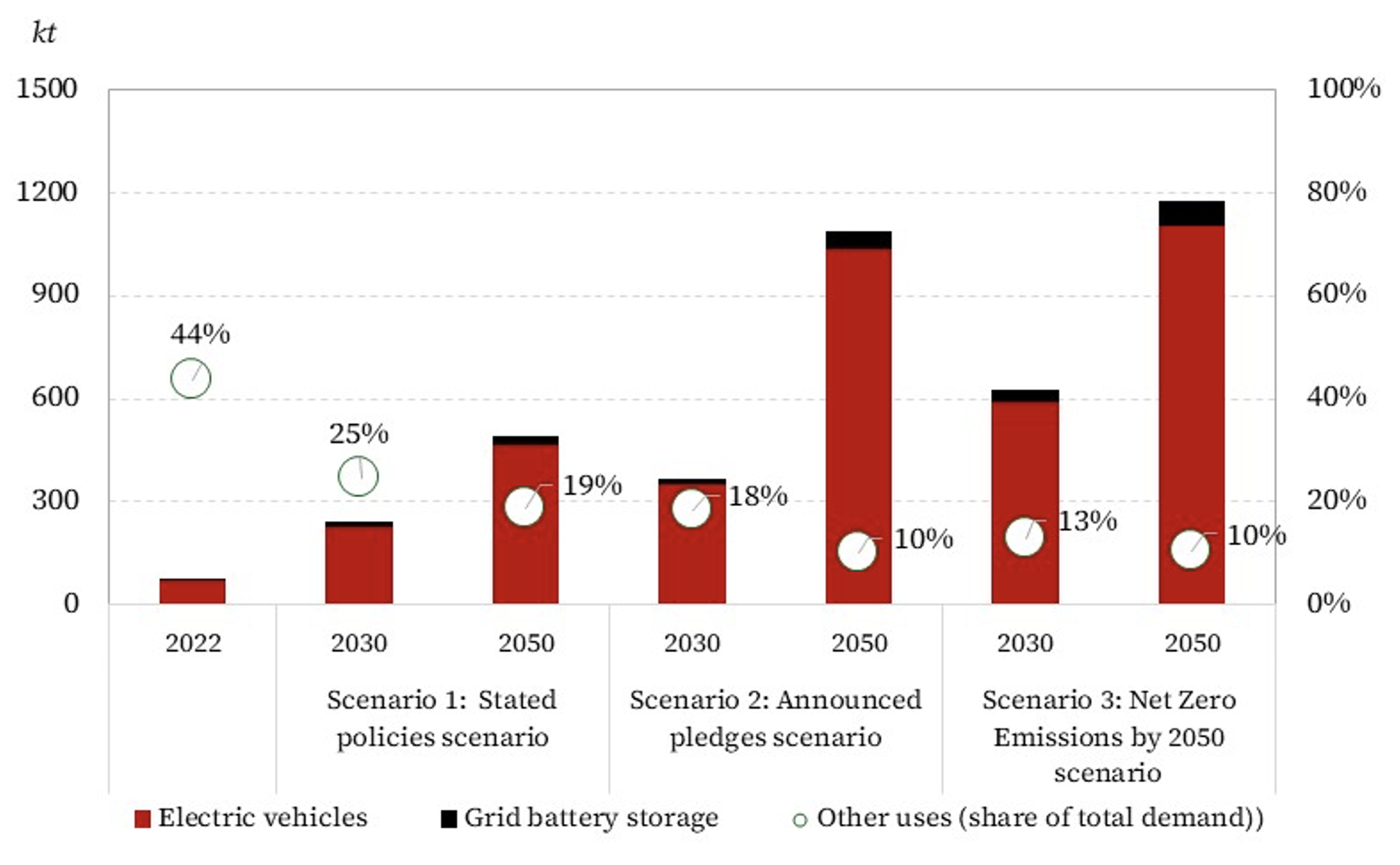

According to the International Energy Agency (IEA), the demand for critical minerals will at least double by 2030.[2] As indicated in Figure 1, global copper production will need to grow dramatically — double or triple its levels in 2022 — to meet the demands of energy transitions. Moreover, the use of copper will shift more heavily toward electricity networks, EVs, and solar photovoltaics (PVs). Even more dramatically, lithium demand is projected to increase anywhere between 5 and 12 times by 2050 relative to 2022 to feed growth in EVs and grid battery storage, depending on the scenario (Figure 2).

Figure 2 — Expected Lithium Demand Until 2050 by Scenario

A Role for South America

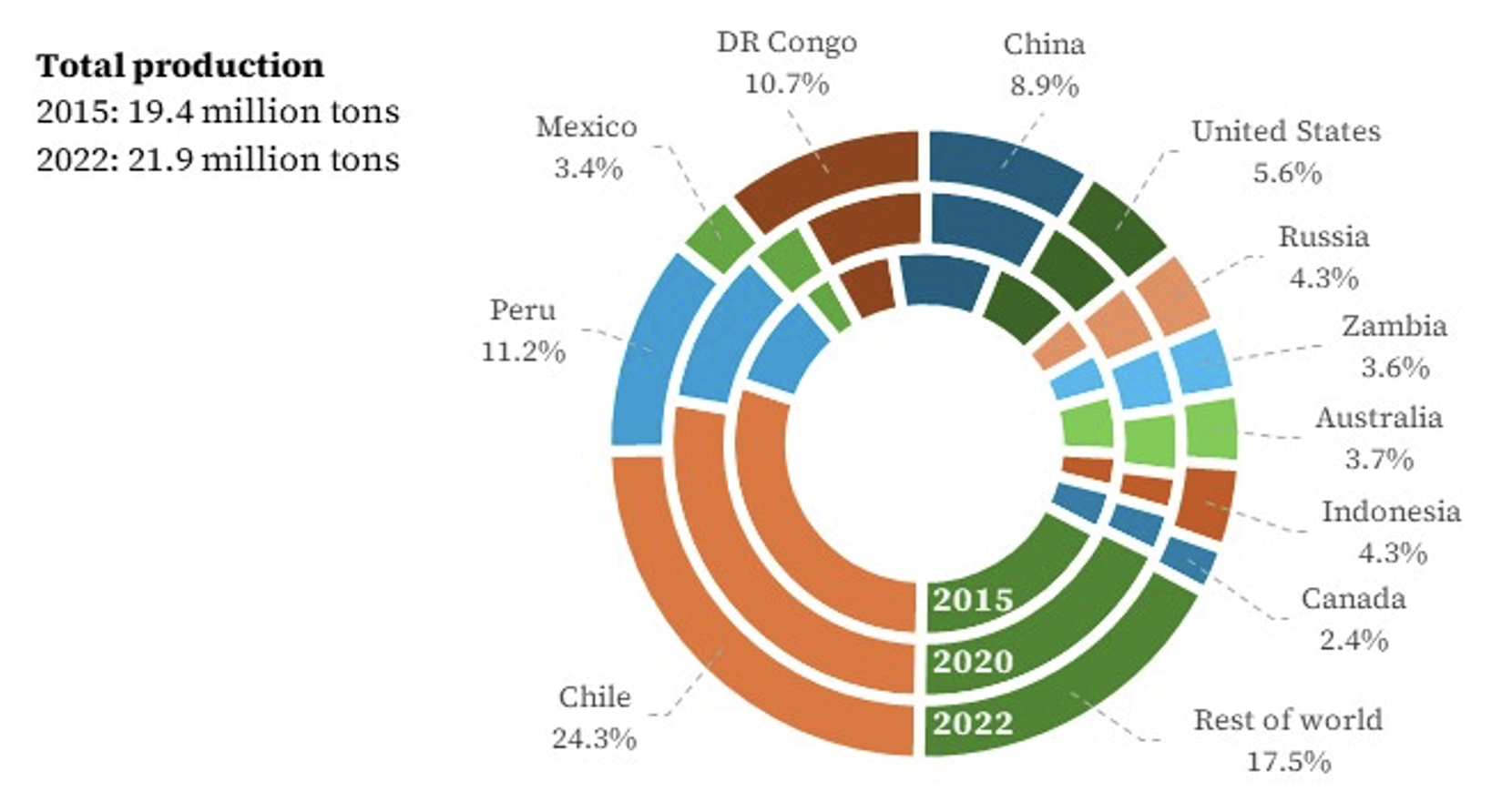

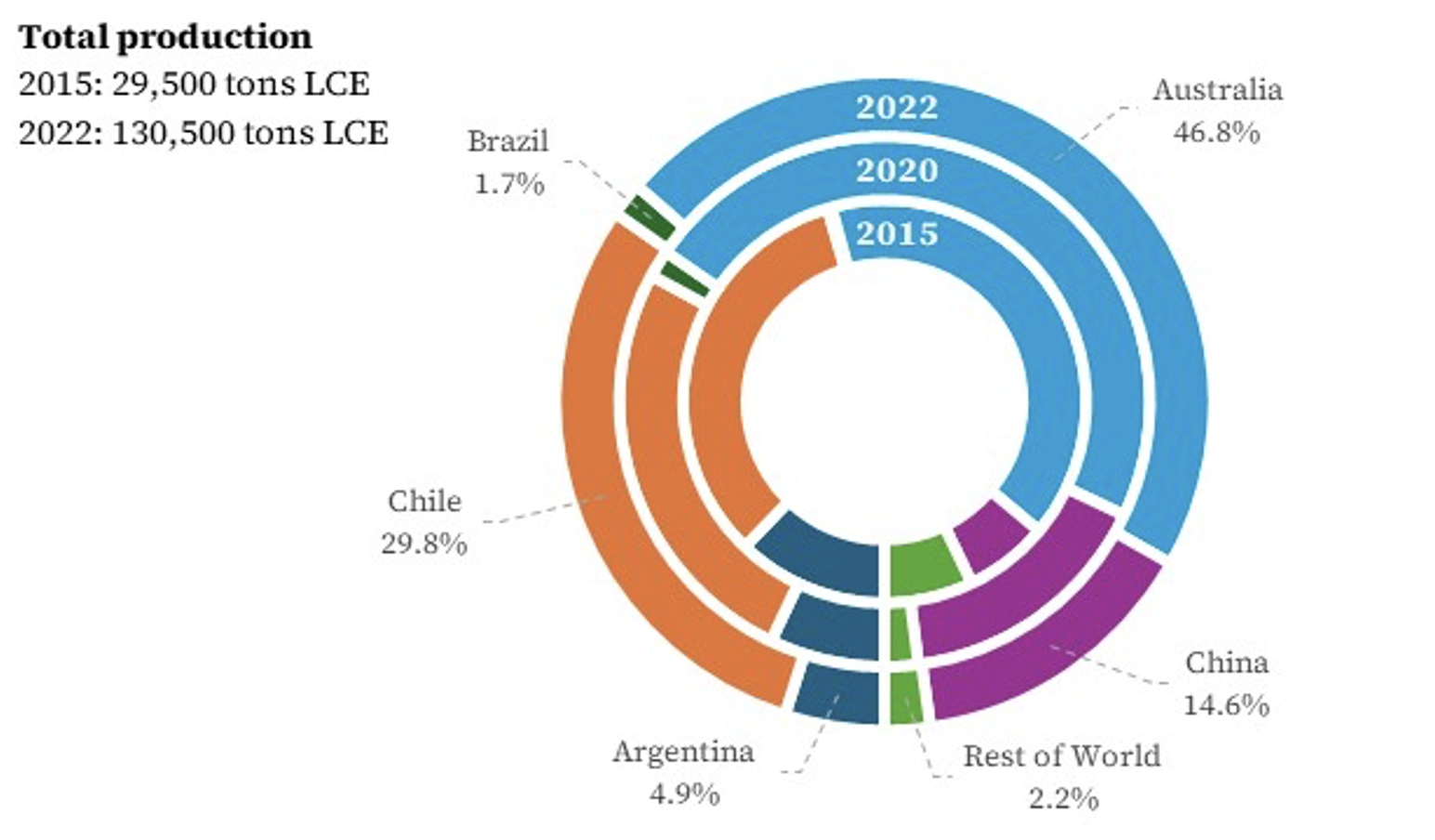

Critical minerals resources are geographically concentrated in a few regions. Chile, Argentina, Peru, Bolivia, and Brazil, to mention some, are of great relevance due to their reserves and current production levels of minerals, such as copper, lithium, zinc, silver, bauxite, etc. Currently, Chile and Peru account for about 35% of global copper production and 31% of global copper reserves (Figure 3). Similarly, Chile, Argentina and Brazil accounted for 37% of global lithium production and 53.2% of global lithium reserves at the end of 2022, excluding Bolivia’s estimated reserves of 23 million tons of lithium (Figure 4).[3] Given the data presented in Figures 1 and 2, it is no surprise that these countries also stand to be significant players in the future of energy.

Figure 3 — Copper Mine Production in 2015, 2020, and 2022

Figure 4 — Lithium Mine Production in 2015, 2020, and 2022

Global production of raw minerals has been responding to increased clean energy technology. Copper production has increased by 13.2% between 2015 and 2022, while lithium production has increased in 342% in the same period.[4] Moreover, it is estimated that copper production in Peru and Chile will grow by 30% and 15% between 2022 and 2030, respectively.[5] On the other hand, global mineral processing is highly concentrated in one country, China, which is a dominant player of the refined supply of many of key resources. China processes over 90% for manganese, 70% for cobalt, almost 60% for lithium, and approximately 40% for copper.[6]

Meeting the projected increases in demand requires important long-lived investments. For copper and nickel alone, meeting demand growth will require cumulative capital expenditures of $250 billion to $350 billion by 2030.[7] By 2023, Chile and Peru secured portfolios of 31 and 27 copper mining projects worth $65.2 billion and $38.5 billion, respectively. These projects are expected to be developed through 2031.[8] As for lithium projects, as of 2023 Argentina holds an estimated total project investment of $7 billion to be developed through 2032 by Rio Tinto, Arcadium Lithium, Posco, and Gangfeng Lithium, among others.[9] Chile holds a total project investment of $2.3 billion to be developed by Sociedad Química y Minera (SQM), Salado Isolation Mining Contractors (SIMCO), and Minera Salar Blanco. Notably, fiscal terms are likely playing a role in attracting investments, as a royalty of 3% in Argentina for lithium mining is, all else equal, more attractive to private investment that a royalty of 40%, as is the case in Chile.[10]

Challenges Remain

Mineral supplies face heightened risks due to lengthy permitting processes and rising mining conflicts. A longstanding barrier to mining expansion is found in the permitting process, which can take years. The global average to develop mining production from discovery to first production is about 17 years for copper; in the case of lithium, the average is seven years in South America.[11] This may explain why copper mining investment has been largely directed toward brownfield projects — specifically, capacity expansion or replacement — rather than greenfield projects.

Ore grade — the concentration of a desired mineral in mined material — is also important since mineral concentration is negatively correlated to operating costs. Locations with higher ore grades require less material removal during processing, which implies lower energy use and lower environmental impact. Globally, ore grades have been declining, which has caused higher operating and environmental costs. Currently, 0.6% of copper is the average ore grade, which is below the threshold for high grade at 1%. In Chile, average copper ore grades declined from 0.69% in 2015 to 0.59% in 2022.[12]

Socio-environmental conflicts and opposition from local and indigenous communities to mining activities are also barriers to the rapid expansion of mining projects. This opposition is intensified by pervasive social inequities, absence of effective public services, weak environmental protection, and a failing rent distribution system. For example, from 2000 to 2020, mining-associated conflicts in Chile and Peru almost quadrupled.[13]

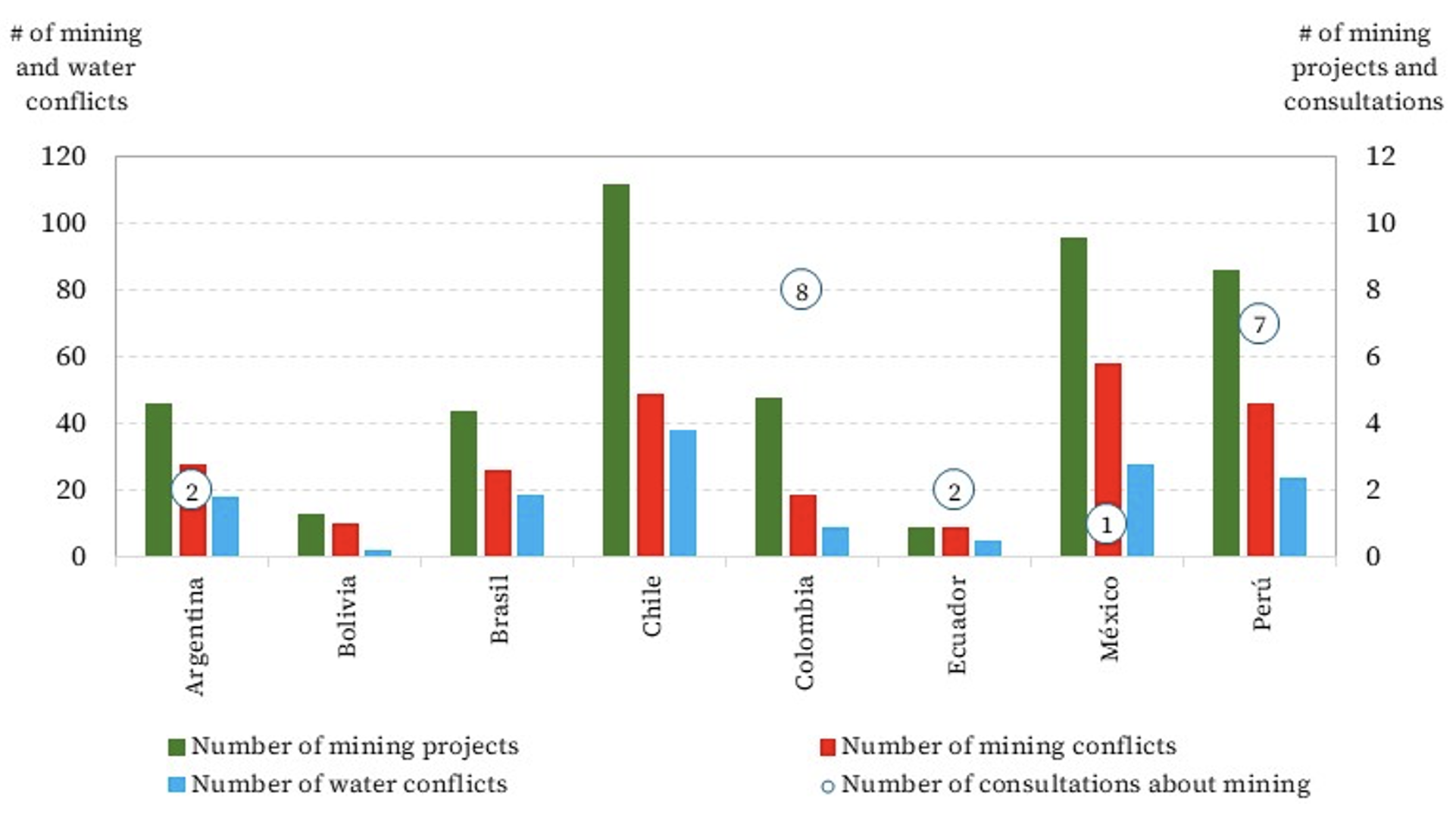

Although a higher level of national government effectiveness is positively associated with income levels and good renewable energy policies and regulation, no clear relationship exists with mining conflicts (Figure 5). This may be explained by the fact that mining projects are usually developed within or close to indigenous communities’ lands, and these communities have been traditionally underrepresented and neglected. Out of a total of 284 mining conflicts registered by the Observatory of Mining Conflicts in Latin American (OCMAL) through 2020, 68% were in South America. Notably, water stress and water pollution concerns that lead to water conflicts are highly associated with mining conflicts, and, of course, mining conflicts increase with the number mining projects. Public consultations with local communities prior to project development seem to be a minor practice across countries in Latin America (Figure 6).

Figure 5 — Government Effectiveness in 2019; Renewable Energy Regulatory Environment Indicator in 2019; and Cumulative Mining Conflicts Through 2021

Note: Bubble size and annotations indicate number of conflicts.

Figure 6 — Mining and Water Conflicts and Prior Consultations in Selected Latin American Countries Through 2021

The distribution of mining rents from the government is another point of conflict. Even decentralized models of rent distribution that have been implemented in countries such as Peru and Bolivia seem to fail in improving local communities’ well-being. Poor governance at the subnational level, rent-seeking behavior, and corruption may be some of the causes for inefficient public expenditure. Lack of communities’ ownership and lack of their participation in the decision-making process are also relevant factors.[14]

A Path to Solutions

Some institutional improvements have been applied through legislation based on prior consultations in Peru (where they are obligatory and binding) and Chile. Innovative mechanisms to ameliorate risks have been found in roundtables between government and local communities in Peru and in early private-public dialogue in Chile.[15]

Companies are also working toward improving their extraction technology to minimize impacts, as happens with the typically water-intensive lithium extraction process from brines. In Chile, for example, mining companies have been switching to desalinated water sources while also increasingly relying on renewable energy sources. In addition, mining companies from Peru and Chile are collaborating on a binational roadmap for green hydrogen in mining to decarbonize the activity.

A successful path to reducing conflict while capturing the economic opportunity associated with increased mining activities is visible. But collaboration among the relevant stakeholders — government, companies, and communities — is crucial. This is no small task.

Governments must reduce red tape and streamline mining permitting processes while also taking into consideration necessary measures to secure local communities’ well-being and environmental protection. Alongside improved governance that emphasizes transparency and accountability, this can facilitate greater private investment and social welfare, while gaining communities’ trust. In fact, some scholars have found that the social license to operate in mining activities increases with governance capacity.[16]

It is also essential to develop mechanisms that allow larger engagement and participation of indigenous communities in the decision-making process. Only when these communities’ voices are heard will real progress be achievable. In the end, an optimal balance of environmental protection, political stability, and regulation clarity are crucial.

< Previous article | Next article >

Notes

[1] Natural Resource Division of Economic Commission for Latin America and the Caribbean (ECLAC), Lithium Extraction and Industrialization: Opportunities and Challenges for Latin America and the Caribbean (Santiago: United Nations, 2023), https://hdl.handle.net/11362/48965.

[2] International Energy Agency (IEA), The Role of Critical Minerals in Clean Energy Transitions, IEA Publications, 2021, https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions; IEA, Critical Minerals Market Review 2023, IEA Publications, 2023, https://www.iea.org/reports/critical-minerals-market-review-2023.

[3] According to the Bolivian president, the estimated lithium reserves are 23 million metric tons (Daniel Ramos, “Bolivia Hikes Lithium Resources Estimate to 23 Million Tons,” Reuters, July 20, 2023, https://www.reuters.com/markets/commodities/bolivia-hikes-lithium-resources-estimate-23-mln-tons-2023-07-20/).

[4] On the other hand, global mineral processing is highly concentrated in one country, China, which is a dominant player of the refined supply of many of key resources. China processes over 90% for manganese, 70% for cobalt, almost 60% for lithium, and approximately 40% for copper (International Renewable Energy Agency [IRENA], “Geopolitics of the Energy Transition: Critical Materials,” 2023, https://www.irena.org/Digital-Report/Geopolitics-of-the-Energy-Transition-Critical-Materials).

[5] Benjamin Jones, Francisco Acuña, and Víctor Rodríguez, Cambios en la Demanda de Minerales: Análisis de los Mercados del Cobre y el Litio, y sus Implicaciones para los Países de la Región Andina (Santiago: ECLAC, 2021), https://hdl.handle.net/11362/47136.

[6] IRENA.

[7] Marcelo Azevedo et al., “The Raw-Materials Challenge: How the Metals and Mining Sector Will Be at the Core of Enabling the Energy Transition,” McKinsey & Company, January 10, 2022, https://www.mckinsey.com/industries/metals-and-mining/our-insights/the-raw-materials-challenge-how-the-metals-and-mining-sector-will-be-at-the-core-of-enabling-the-energy-transition. As a reference, around $380 billion is the total investment in climate and energy committed by the U.S. via its Inflation Reduction Act.

[8] S&P Global Market Intelligence, “Chile and Peru’s Copper for Energy Transition,” S&P Global, April 5, 2023, https://www.spglobal.com/esg/insights/featured/special-editorial/chile-and-peru-s-copper-for-energy-transition.

[9] Diana Kinch, “Argentina ‘Most Attractive’ Lithium Triangle Jurisdiction for Brine Projects: Mine Developer,” S&P Global, April 12, 2024, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/metals/041224-argentina-most-attractive-lithium-triangle-jurisdiction-for-brine-projects-mine-developer.

[10] Jack Quinn, “Latin America’s Lithium Sands Are Shifting,” Americas Quarterly, November 6, 2023, https://www.americasquarterly.org/article/latin-americas-lithium-sands-are-shifting/.

[11] IEA, The Role of Critical Minerals in Clean Energy Transitions. In Chile, copper mining permitting process my take 8 to 11 years; while in Peru, it takes 23 years in average.

[12] María Cristina Betancour, “La Caída de la Producción de Cobre y el Desafío del Sector,” Ex-Ante, February 19, 2024, https://www.ex-ante.cl/la-caida-de-la-produccion-de-cobre-y-el-desafio-del-sector-por-maria-cristina-betancour/.

[13] Rafael Poveda Bonilla, Estudio Comparativo de la Gobernanza de los Conflictos Asociados a la Minería del Cobre en Chile, el Ecuador y el Perú (Santiago: ECLAC, 2021), https://hdl.handle.net/11362/47569.

[14] Manuel Glave and Gerardo, “Rent Distribution and Extractive Industry Conflict: The Latin American Approach,” Evidence and Lessons from Latin America (ELLA), January 2012, bit.ly/3Mc1i8D.

[15] Poveda Bonilla.

[16] Lenin H. Balza et al., “The Unwritten License: The Social License to Operate in Latin America’s Extractive Sector,” Inter-American Development Bank (IDB), August 18, 2022, https://ssrn.com/abstract=4188882.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.