Author(s)

This article is also featured in Energy Insights, which reflects a sample of ongoing research across the Center for Energy Studies’ diverse programmatic areas, all addressing the ever-evolving energy challenges across Texas, the U.S., and the globe. Read more from the inaugural edition.

Recent Developments

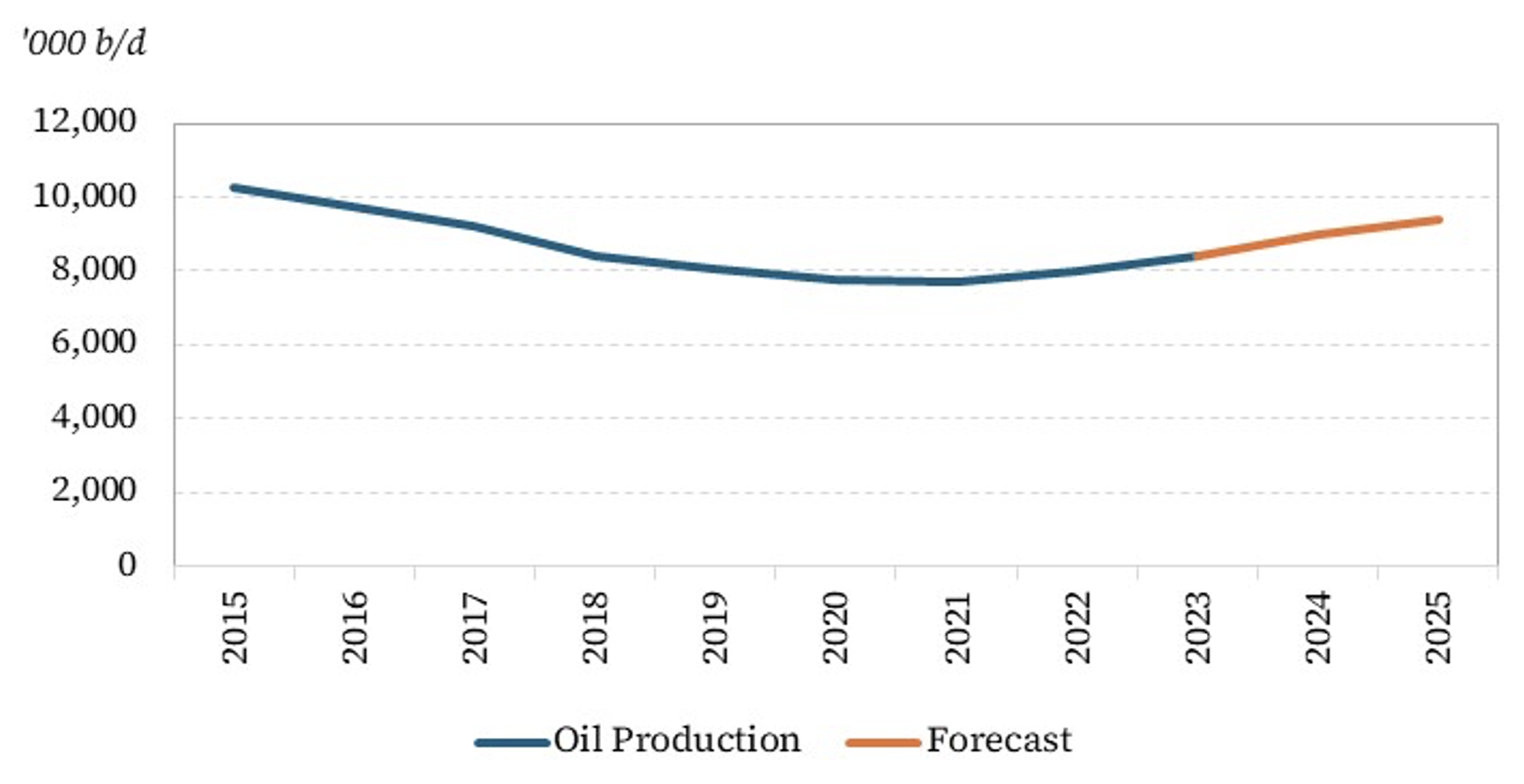

Latin America has massive hydrocarbon resources, second only to the Middle East, but until recently regional production had stagnated or declined, even during the oil price boom of 2004–14. The main obstacles for the development of its potential have been aboveground risks, including regulatory intervention, macroeconomic uncertainty, and expropriation risks — partially rooted in resource nationalism and the dominance of national oil companies. A mix of ideology and opportunistic reneging have thwarted investment and production growth. In contrast to their northern neighbors, the U.S. and Canada, in which production boomed, the region largely wasted the opportunity given by the oil super cycle. According to my own estimates, Latin America could have been producing some 17 million barrels per day (bpd) of crude, if it had the appropriate institutional environment, but instead it was producing close to 9 million bpd in 2023.[1]

However, after seven years of steady decline with an accumulated drop of 25%, the region’s crude production has recovered by more than 9% over the last two years due to significant growth in Guyana and Brazil, with smaller increases in Argentina and Venezuela, more than compensating declines elsewhere in the region.[2] Brazil and Guyana are set to continue their notable upward trajectory in the next few years; the only question is the pace of development in their prolific offshore. Both countries are open to private investment and have a record of respecting property rights.

Guyana’s oil production is one of the most remarkable success stories in the last few decades. Offshore oil was discovered by Exxon in 2015. Production started in 2019, and by the end of the first quarter of 2024, it had reached 600,000 bpd. The U.S. Energy Information Administration (EIA) forecasts that Guyana’s production will surpass 800,000 bpd in 2025, adding more than 300,000 bpd in two years.[3] In turn, Brazil’s production is expected to grow by more than 250,000 bpd by 2025.[4] These increases will make Guyana and Brazil, along with the U.S. and Canada, the largest sources of production growth in 2024–25, allowing the production of Latin America to surpass the levels of 2017.

Argentina, despite its macroeconomic difficulties, should continue to grow, although arguably below its potential, due to an extremely attractive unconventional resource base and the probusiness Milei administration. Shale is less vulnerable to political risks, due to its unique characteristics, short cycle, and low sunk costs.[5] In contrast, Colombia, Ecuador, and Mexico are all expected to continue their decline. The recent presidential election in Mexico points toward continuity in the polices that closed private investment opportunities and exacerbated the financial problems of Pemex. In Colombia, the Petro administration has banned fracking and stopped bidding rounds for exploration, making the recovery of production in the next few years unlikely.

Figure 1 — Latin America Oil Production, 2015–25

A Focus on Venezuela: Political Risks and Sanctions

Venezuela, the Latin American country with the largest reserves and significant spare infrastructure, although much deteriorated, has the greatest upside potential. However, political and regulatory risks and U.S. sanctions set a low ceiling to its recovery, unless these constraints are eased. Will the recent sanction flexibilization and political negotiations lead to further investment and production growth?

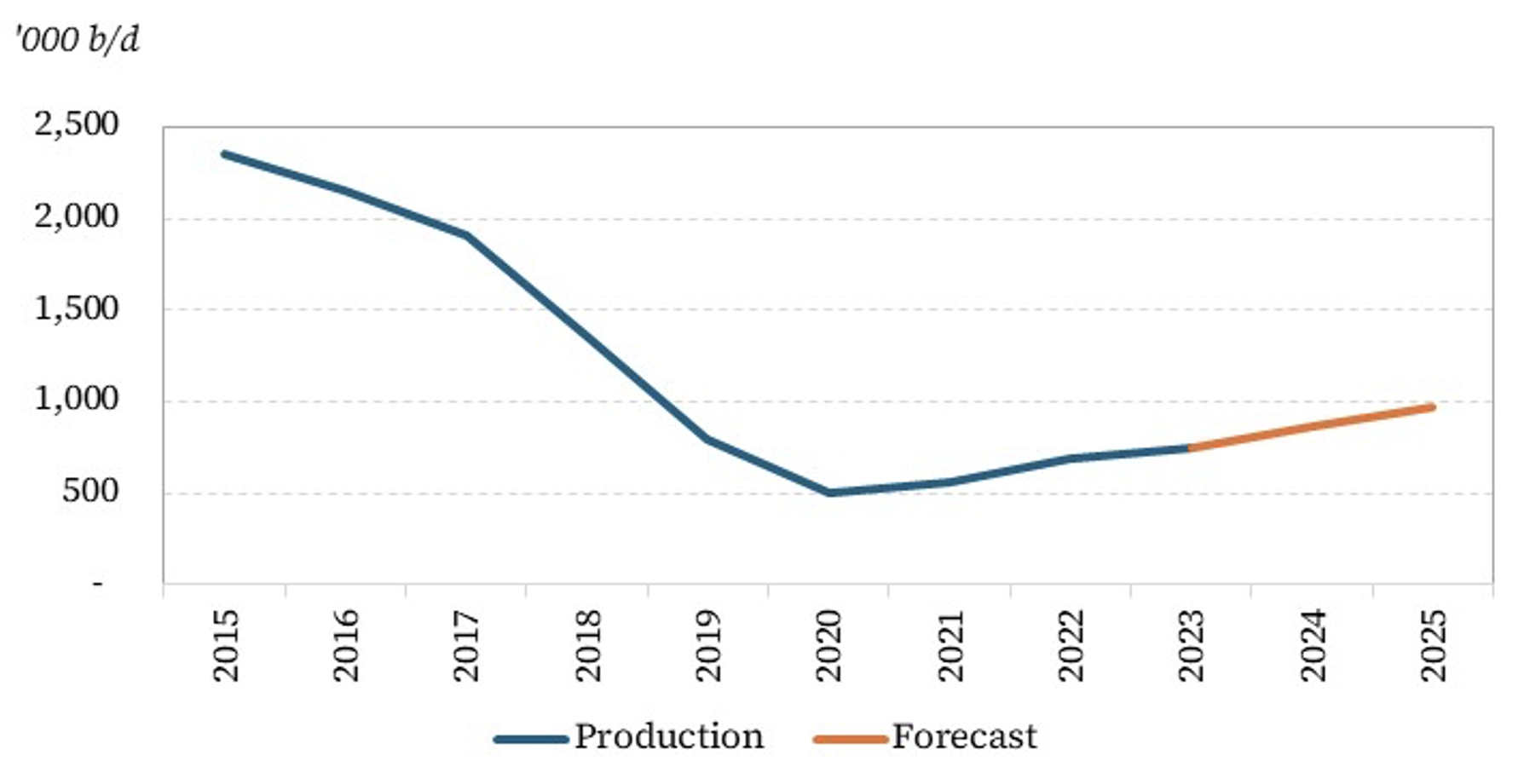

Venezuela represents the biggest question mark in the regional outlook. Forecasts of oil production in the next two years vary widely, from 1.15 million bpd (an increase of 330,000 bpd) to 700,000 bpd (a decrease of 110,000 bpd) by the end of 2025, depending on sanctions’ flexibilization and political developments.[6] For reference, production averaged 812,000 bpd in the first quarter of 2024.

To analyze the outlook for Venezuela, it is important to have some background. The nation’s production fell from 2.3 million bpd in 2015 to 498,000 bpd in 2020. The decline was the result of a combination of lower oil prices, cumulative lack of investment, U.S. sanctions, and 2020 COVID-19-related demand destruction. But the period prior to 2015 witnessed an equally dramatic collapse in the production of Venezuela’s national oil company, Petróleos de Venezuela, S.A. (PDVSA), which shockingly occurred during the price super cycle. Just before Chavez came to power in 1999, Venezuela produced 3.4 million bpd, of which PDVSA operated 3.1 million, and the rest was produced by private operators in service contracts. By 2015 PDVSA produced only 1.2 million bpd, and the joint ventures with foreign companies produced some 1.1 million bpd. PDVSA had taken over the large operations of Exxon and Conoco and some other smaller projects in 2006–07. While its partners in the Organization of the Petroleum Exporting Countries (OPEC) increased oil production by around a third, Venezuela’s total production fell by a third, with PDVSA’s operated production falling by close to two thirds.

Neither the country nor the world paid much attention to the collapse of PDVSA because private companies compensated for a substantial portion of the decline, and the boom in the oil price avoided a decline in oil revenues. Not only did PDVSA’s production collapse but also its debt exploded, including its obligations with partners and contractors. Private operators were regulatorily and fiscally expropriated in the government’s insatiable search for additional revenues.[7] So, when the price of oil declined at the end of 2014, the Venezuelan oil sector’s troubles became painfully evident.

PDVSA and the country were at the brink of default, and U.S. financial sanctions in 2017 made debt restructuring unviable. In 2019, sanctions closed the U.S. market, where Venezuela exported more than 500,000 bpd and from which it imported refined products and diluents for its extra-heavy oil production. U.S. secondary sanctions in 2020 forced Venezuelan oil to the black market at heavy discounts, just when COVID-19 pandemic produced a demand and price collapse, making it impossible for PDVSA to sell some 500,000 bpd and prompting production shutdowns. Production bottomed at less than 400,000 bpd in the summer of 2020. With the subsequent price recovery, and the help of Iran in selling on the black market and as a supplier of diluents, production went back up to average 684,000 bpd in 2022, using all the existing spare capacity. But adding production capacity required new investments. Since the middle of 2020, there had been no drilling rigs operating in Venezuela, contrasting with the 60–70 operating when production was stable at around 2.5 million bpd.

Enter the Russian invasion of Ukraine on February 2022, which prompted the U.S. to initiate negotiations with the government of Maduro. That, in turn, led to negotiations between PDVSA and Chevron, the largest foreign investor in the country, resulting in a new contract giving the U.S. major control over the operations and exports of its four join ventures with PDVSA. In November 2022, the U.S. gave a license to Chevron through General License (GL) 41 to operate these joint ventures and export their production to the U.S. market. Chevron investments have lifted its production by more than 100,000 bpd, to around 190,000 bpd by June 2024.

In 2023 the U.S. negotiated a further relaxation of sanctions with Nicolás Maduro in exchange for steps allowing for competitive presidential elections in 2024, as part of the Barbados Agreement. GL 44 of October 2023 suspended sanctions to PDVSA for six months, conditional on electoral guarantees. The license improved the cashflow of PDVSA, by allowing it to sell in the formal market (primarily in India), some of the oil it used to sell in the black market (primarily in China) at lower discounts and costs. However, due to the short-term horizon of six months and the political conditionality, it failed to lead to any relevant additional investments. Production in non-Chevron projects only increased modestly due to increased diluent availability.

On April 17, 2024, the U.S. government announced the nonrenewal of GL 44, due the Venezuelan government’s lack of compliance with its electoral commitments by not allowing the winner of the opposition primaries, María Corina Machado, or her selected substitute to participate in the elections. However, the Biden administration strongly signaled that it would consider applications for individual licenses for companies to operate in Venezuela and do business with PDVSA.

Thus, the current U.S. sanctions policy remains considerably more flexible than the maximum pressure policy set by the Trump administration in 2020. Presumably, sanctions will be fine-tuned according to political developments in Venezuela and U.S. strategic priorities. Chevron’s license GL 41 was reconfirmed. European companies, such as Repsol and Maurel & Prom, obtained a licensed to continue operating in Venezuela. Other possible licensees include the Italian company, Eni, and Indian companies, such as Oil and Natural Gas Corporation Limited (ONGC) for operations and Reliance Industries for the purchase for Venezuelan oil.

Full normalization of relations between Venezuela and the U.S., and the subsequent removal sanctions removal looks improbable, unless there is a return to democracy. Presidential elections in Venezuela are set for July 28, 2024. Presidential elections in Venezuela were held on July 28, 2024. Maduro claimed victory, but there were credible claims of extensive fraud. U.S. elections are set for Nov. 5, 2024. The outcomes of both elections could impact the future of sanctions policy.

It was clear from the outset that Venezuelan elections were not going to be free and fair. Maduro’s approval rating is around 25%. He had bet on his proven strategy of banning some opposition candidates, sponsoring a coopted opposition, encouraging the real opposition’s divisions, and promoting abstention among the opposition voters by discouraging them with electoral abuses and the perspective of outright fraud. The problem is that the opposition became firmly united behind the leadership of Machado, and even though she was banned from running, she maneuvered to stay in the electoral competition by supporting another candidate. So, the country headed for a tumultuous election campaign, with the government losing by large margins in all reputable surveys but unwilling to concede defeat. At the time of this writing, at the end of July 2024, Maduro holds on to power with the support of the military but faces widespread discontent and international condemnation for the fraudulent elections.

In any case, the Biden administration, as well as a potential Harris administration, has incentives to remain in business with Venezuela. Energy geopolitics and immigration issues are two key strategic considerations. A second Trump administration might also prefer a more transactional approach to sanctions than the maximum pressure policy of his previous term. As a result, if Maduro clings to power, the most likely scenario is a world with sanctions but with licenses allowing operations by U.S. and other allied-country companies.

How Quickly Could Venezuela’s Production Recover?

If Venezuela had a regime change, political stability, and an attractive and credible oil investment framework — three big “ifs” — production could increase significantly, by a yearly average 220,000–250,000 bpd with annual investments of around $8–9 billion. While such a scenario is unlikely, it can serve as a benchmark to analyze others.

Figure 2 — Venezuela Oil Production, 2015–25

In a scenario of some normalization of relations with the U.S. along with new Chevron-style contracts and licenses to Western companies, production could increase by 330,000 bpd in 2024 and 2025 to surpass 1.15 million bpd by the end of 2025. As indicated in Figure 2, a status quo scenario, with only the existing contracts and licenses, would add a total of some 210,000 bpd in 2024–25, mainly in Chevron’s projects, to reach just above 1 million bpd by the end of 2025. In the unlikely scenario, in which the U.S. government cancels all licenses in 2024 — e.g. if political conflict escalates due to fraudulent elections and a repressive clampdown on the democratic opposition occurs — production would likely peak below 930,000 bpd in 2024–25 and gradually decline.

Looking Ahead

Latin America is poised to see significant increases in production over the next few years, especially in Guyana and Brazil. The offshore resources in these two countries alone are massive, and the countries’ openness to foreign investment makes them attractive plays. However, the region is also beset with significant uncertainties in other countries, all of which are above ground. Venezuela is at the top of the list in this regard.

Despite having massive resources, low geological risks, and significant brownfields ready for investment, Venezuela’s political risks, deteriorated state capacities and infrastructure, and fraught relations with the U.S. make a large production recovery in the short run unlikely. Rather, Venezuela is most likely to continue to be one of the most significant wild cards in the global market in the next decade.

< Previous article | Next article >

Notes

[1] Unless otherwise noted, the percentages and statistics mentioned are author estimates.

[2] Energy Institute, Statistical Review of World Energy, 2024, https://www.energyinst.org/statistical-review.

[3] Eulalia Munoz-Cortijo and Matias Arnal, “Guyana Becomes Key Contributor to Global Crude Oil Supply Growth,” U.S. Energy Information Administration (EIA), May 21, 2024, https://www.eia.gov/todayinenergy/detail.php?id=62103.

[4] Sean Hill, “Four Countries Could Account for Most Near-Term Petroleum Liquids Supply Growth,” EIA, March 21, 2024, https://www.eia.gov/todayinenergy/detail.php?id=61583.

[5] Gabriel Collins et al., “Shale Renders the ‘Obsolescing Bargain’ Obsolete: Political Risk and Foreign Investment in Argentina’s Vaca Muerta,” Resources Policy 74 (December 2021), https://doi.org/10.1016/j.resourpol.2021.102269. For an earlier version of this paper, see Collins et al., “Shale Renders the ‘Obsolescing Bargain’ Obsolete: Political Risk and Foreign Investment in Argentina’s Vaca Muerta” (working paper, Houston: Rice University’s Baker Institute for Public Policy, February 24, 2020), https://www.bakerinstitute.org/research/political-risk-and-foreign-investment-argentinas-vaca-muerta.

[6] For the upper range estimate, see Rystad Upstream Analytics, “Venezuela Oil Supply Outlook Hangs in Balance with Future of Oil Sanctions Unclear,” February 16, 2024. For the lower range estimate, see IPD Latin America, “Venezuela Production Forecast,” February 2024.

[7] Francisco Monaldi, Igor Hernández, and José La Rosa Reyes, “The Collapse of the Venezuelan Oil Industry: The Role of Above-Ground Risks Limiting Foreign Investment,” Resources Policy 72 (August 2021), https://doi.org/10.1016/j.resourpol.2021.102116.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.