Author(s)

This article is also featured in Energy Insights, which reflects a sample of ongoing research across the Center for Energy Studies’ diverse programmatic areas, all addressing the ever-evolving energy challenges across Texas, the U.S., and the globe. Read more from the inaugural edition.

Setting the Stage

For the past 50 years, worldwide reliance on liquified natural gas (LNG) has continuously grown despite regional conflicts, economic recessions, technological shifts, blockades, a global pandemic, climate change-related policies, government taxes, tariffs, price caps, new regulations, and other market interventions. Whether that trend continues will be tested starting in 2024 and continuing over the next few years.

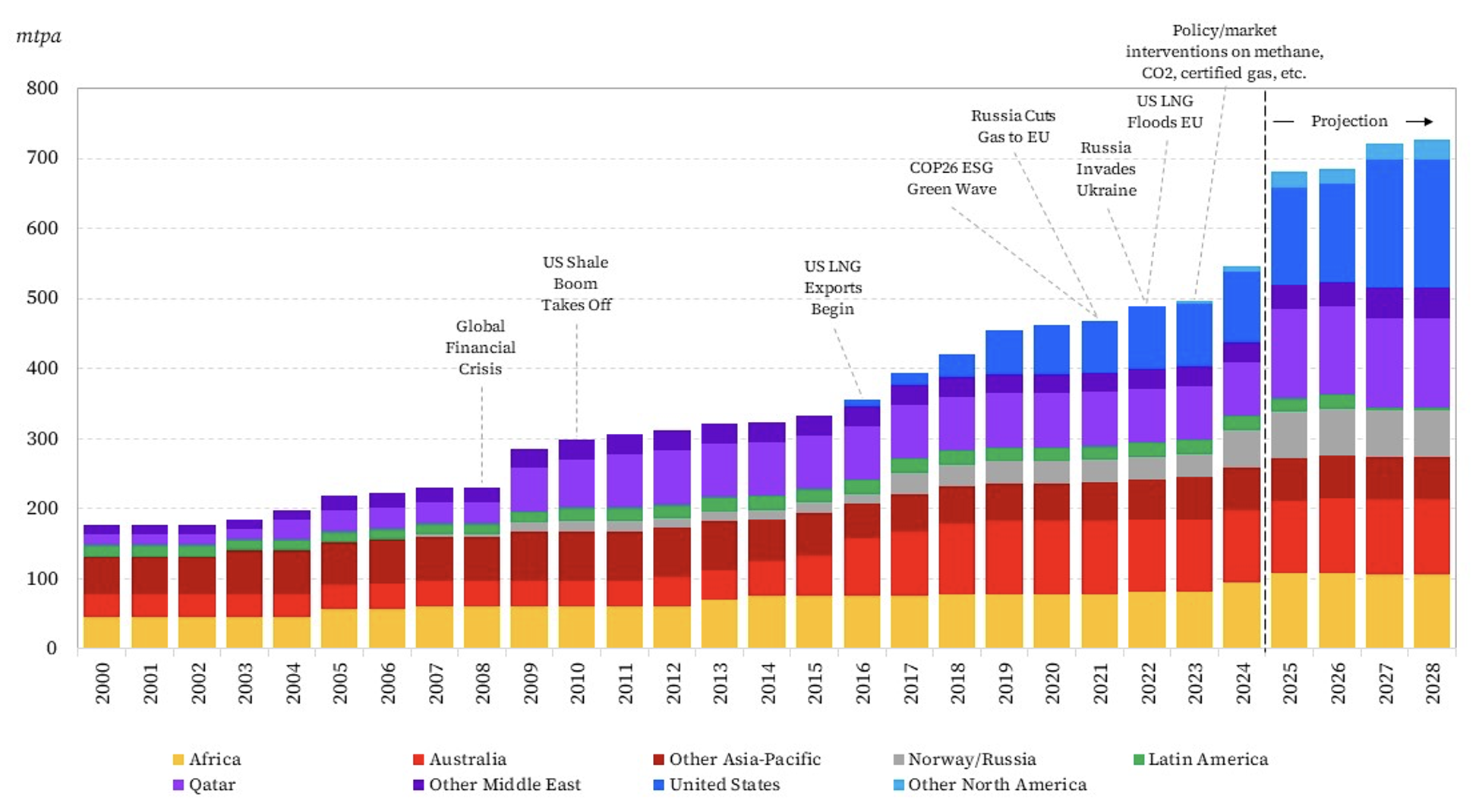

Figure 1 — Global LNG Liquefaction Capacity by Region, 2000–28

As to be expected, given the growth in liquefaction capacity seen in Figure 1, LNG demand has risen significantly since 2000, increasing almost four-fold. Despite such impressive growth, the near-term outlook for LNG is highly uncertain. In fact, LNG market developments over the near term will be influenced by three dominant, intertwined themes — trade and geopolitics, cumulative decarbonization regulations, and the U.S.’s LNG “pause.”[1] The impacts of changes in these three thematic areas will have far-reaching implications that will shape the global LNG market and regional gas markets for years to come.

Trade and Geopolitics: Is the US Preparing To Ban New LNG Sales to China?

For the U.S. LNG export industry, flexibility is a cornerstone of supply agreements. This allows exporters and downstream purchasers to resell or divert cargoes to other destinations without the need for approval from either governments or LNG suppliers. Such contract flexibility makes U.S. LNG supply an attractive option for portfolio players, injects much needed liquidity into the global market, and has altered the global supply portfolio dramatically over the last decade.[2]

U.S. LNG export projects require approval from the U.S. Department of Energy (DOE), as the Natural Gas Act states that LNG exports are deemed to be in the public interest unless otherwise determined by the DOE. With the exception of prohibiting exports to four sanctioned countries — North Korea, Iran, Libya, and Syria — the DOE has never rejected an application for an LNG export permit.

However, in the last sentence of a recent website post that has apparently received scant, if any, notice, the DOE suggested one outcome of its “pause” in issuing new LNG export permits could be to mitigate the risks caused “by selling our energy resources to competitor countries that don’t align with our interests and those of our allies.”[3] Such a criterion has never been part of the public interest standard under the Natural Gas Act to date.

If the Biden administration is preparing to block permits for new LNG exports to China, for example, this would have major repercussions.[4]

- As noted above, the U.S. has never rejected LNG exports to any country unless that country is fully sanctioned for terrorist-supporting activity. Is the Biden administration proposing to sanction all petroleum product sales to China on this basis? If so, what other publicly traded commodities are the U.S. considered banning from export to China? Agricultural products?

- Even if the DOE were merely to give a priority to export applications that named destination countries other than China, such a policy would be of no benefit as U.S. LNG contracts are destination flexible; free to board (FOB) buyers could flip the cargoes back-to-back to buyers who would take them to China. If such an approach is used, the DOE would merely have deprived U.S. LNG project developers from securing long-term contracts, which are vital for securing project financing, from a specific set of customers. Moreover, it would create an arbitrage value between customers in China and customers who are elsewhere that would be captured by others.

- The reaction of China to an announced embargo could potentially be disastrous, as many consider the U.S. embargo of petroleum products to Japan in 1941, for example, to have been.

Figure 2 — LNG Imports in Select Countries, 2013–23

China’s purchases of long-term LNG from the U.S. have been growing, particularly in the run-up to, and immediately following, Russia’s invasion of Ukraine in 2022 (Figure 2).[5] In the six months before the war, China signed contracts for 91% of the firm LNG sold worldwide: most of that from U.S.-based projects using 12 companies, all but one of which were state-owned and nine of which had never purchased LNG previously.[6] Even so, the appropriate policy reaction for the U.S. is not to ban China from buying LNG from the U.S.; rather, it is to stimulate other customers, such as European buyers, to commit to more long-term contracts. Interestingly, even in the immediate wake of the disruption of Russian pipeline supplies, European buyers continued to purchase the majority of LNG on a spot basis rather than signing long-term contracts.[7] While there have been some notable public announcements more recently, this remains true today.

Additional Sources of Uncertainty: Climate Taxes, Tariffs, and Regulation

The last several months have seen a dizzying array of new government initiatives in various countries with the goal of monitoring, measuring, reporting, standardizing, limiting, or taxing carbon dioxide and/or methane in the natural gas and LNG value chain. Some are final; others will likely soon become so; many have garnered public attention; and a few have slipped by in the torrent with little public notice. Some examples include:

- Under the Inflation Reduction Act, a Waste Emissions Charge (methane fee) for certain levels of methane emissions and fugitive methane will be imposed, starting at $900 per metric tons (mt) of CH4 in 2024 and rising to $1,500 per mt for emissions in 2026 and later. The methane fee will be applied to methane reported by emitters under subpart W of the Greenhouse Gas Reporting Program (GHGRP).

- That methane fee is being applied to LNG producers by the EPA amending subpart W of the GHGRP to require LNG liquefaction project owners to report methane emissions from their acid gas removal units — the major methane emitting components — making them potentially subject to the methane fee.

- DOE has paused processing applications for LNG export permits to assess, among other things, the impact of greenhouse gas emissions due to LNG exports, leaving LNG export applicants to wonder what methane intensity or emission limits might be imposed on applicants.

- The IRS is finalizing rules to determine which types of hydrogen production facilities will qualify for section 45V tax credits, and whether methane intensity will be a factor in allowing some power to be provided by natural gas facilities.

- The Securities and Exchange Commission (SEC) has issued its final rules requiring public disclosure of Scope 1 and 2 emissions, as well as risks due to material climate events. These rules are not equivalent to those imposed by the EU, or by the state of California, and will lead to significant duplication of recordkeeping and reporting costs.

- The EU has extended its carbon tax to include LNG cargoes into Europe starting in 2024. The EU has further agreed to start monitoring methane emissions of countries and companies and to define acceptable limits for fossil-fuel imports across the value chain. A first draft refers to LNG import contracts, but a complete methane tax on all LNG imports exceeding defined methane limits or a new import duty under the EU Carbon Border Adjustment Mechanism (CBAM) are both realistic possibilities. Japan, South Korea, and Canada are among other countries examining various forms of carbon and/or methane taxes or tariffs.

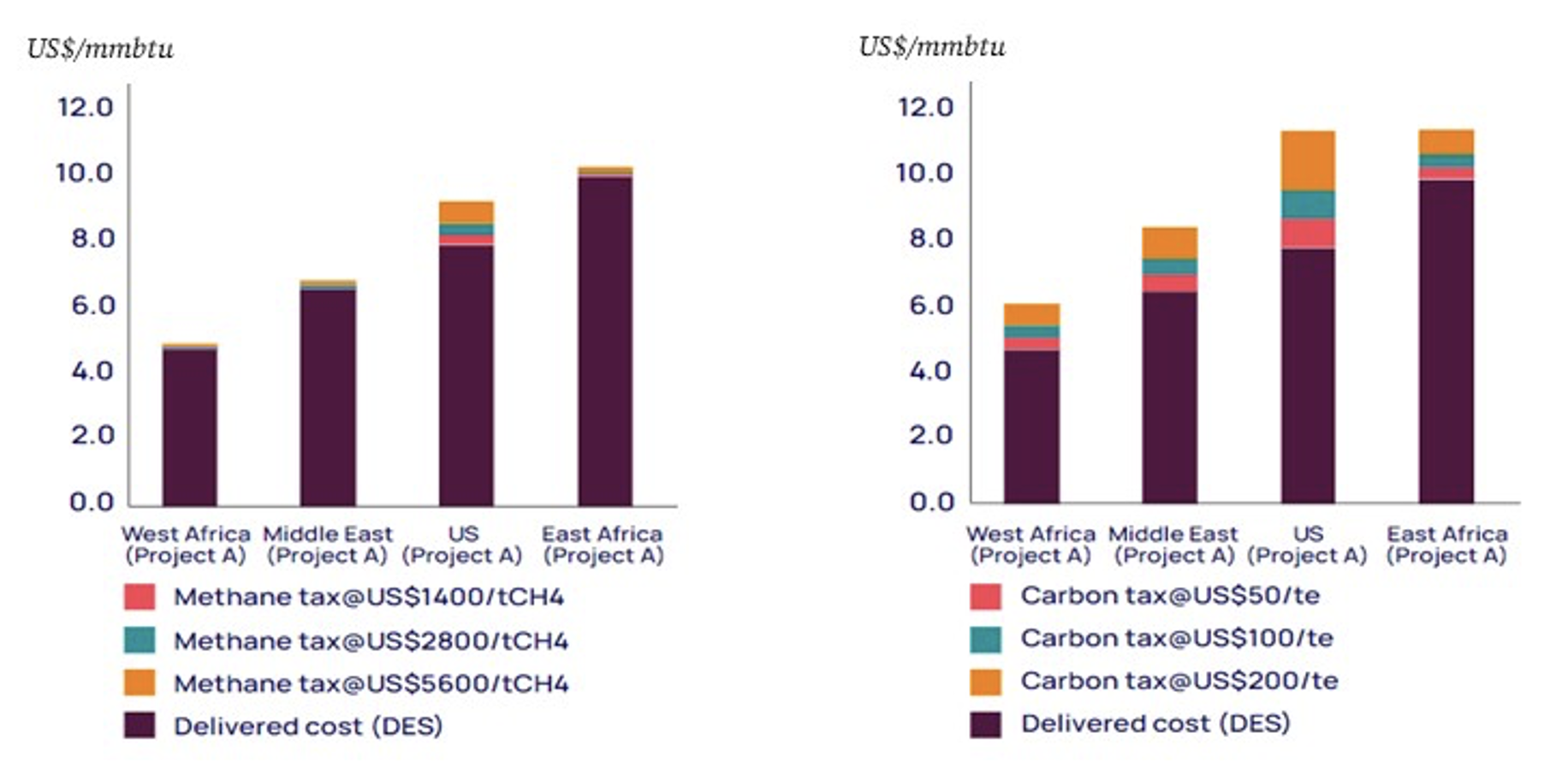

As shown below, an EU carbon tax could be enough to affect the competitiveness of a U.S. LNG project. Taken together, the various taxes, tariffs, and reporting requirements and regulations of the types listed above could have a compounding impact on the U.S. LNG industry. These warrant a close inspection and analysis.

Figure 3 — LNG Delivered Cost to Europe Under Different Methane and CO2 Import Taxes

A Comment on DOE’s LNG “Pause”: Uncertainty Abounds

Much has been written about the DOE’s “pause” in reviewing applications to export LNG to non-free trade countries — except that nothing in the public domain has been written about how DOE should formulate a strategy going forward that will do all it said it plans to accomplish. How does one support free trade, help our allies, protect American consumers, and, perhaps most importantly to the Biden administration, “decarboniz[e] the natural gas value chain to achieve net-zero emissions by midcentury”?[8]

How exactly does one do a full accounting for emissions along the entirety of an LNG value chain? It may seem simple, but it is not (Figure 3).[9] For example, tying upstream emissions to specific producers and gas sales (even assuming measurement technologies can allocate emissions within a field or production area to specific gas producers and streams), and then trying to track those emissions through the mixing bowls of Henry Hub or any of the other major gas transfer hubs requires more estimation than calculation.

Similarly, after the point of title transfer when a cargo is delivered FOB from a liquefaction facility in the U.S. is a challenge, to say the least. LNG becomes blended with the residual heel LNG in the ship, and later blended again with LNG from other sources in the buyer’s receiving terminal storage tanks. It could even be reloaded and reexported, compounding the blending phenomenon. This then begs a very relevant question: How will the emissions accounting be done for the entire lifespan of a given facility? In short, there is enormous uncertainty around measurement and reporting requirements, not to say how assessments will be made prior to a facility receiving an export authorization, which will have significant implications for the growth prospects of the U.S. LNG industry.

What Is Next for LNG?

While the number of uncertainties and intensity of headwinds seems to be mounting for the LNG industry, significant positive signs are present. To begin, the global demand for natural gas continues to grow. As recently noted in the Energy Institute’s annual “Statistical Review of World Energy,” despite global natural gas demand remaining relatively flat in 2023 relative to 2022, global gas demand has increased by 19% since 2013, or roughly 1.7% per year.[10] Moreover, the apparent flattening of global demand over the last couple of years is entirely attributable to the situation in Europe, where demand has fallen by about 10 billion cubic feet per day (bcf/d) since 2021 in the wake of Russia’s invasion of Ukraine, meaning it has grown by a similar amount everywhere else.

In addition, despite the overall natural gas demand reduction seen in Europe, LNG imports to the region have increased by 61.6 billion cubic meters (bcm) from 2021 to 2023 help offset the loss of pipeline imports from Russia.[11] Of course, this growth will not continue, as the situation in Europe is hopefully an aberration driven by the conflict in Ukraine, but the current level of imports will not likely abate substantially in the near-term given the lack of substitutes for natural gas to Europe. Importantly, the declines seen in imports to many other regions over the last couple of years are not likely to persist given the energy needs of developing economies in those regions. Asian buyers, in particular, saw cargoes diverted away to help Europe in 2022; however, those buyers are likely to want to resume their purchases as the crisis in Europe passes and LNG prices moderate.

In total, the global LNG market has grown by 222 bcm since 2013, a pace of 5.3% per year.[12] It is likely to continue to grow, as long as supply is available and as import-dependent economies look for flexible power supply and industrial heating options that have lower carbon intensity than coal. Carbon tariffs in Europe and elsewhere on steel, aluminum, fertilizer, and other products should also begin to tilt the playing field toward imported products made with lower carbon- and methane-producing fuels, favoring LNG.

The longer-term outlook for U.S. LNG exports remains bright, notwithstanding the aforementioned structural uncertainties that could raise costs. But the near term is clouded by the ever-present concerns about adequate investor returns, which are fueled by a lack of clarity on agency interpretations of recent legislation, uncertainties in the political theater about various environmental initiatives in Europe and the U.S., trade tensions between the U.S. and China, and willingness among certain buyers — especially in Europe — to execute long-term offtake agreements amid uncertainties about long-term demand. Suffice it to say that the LNG market is sailing into seas it should be well-adept at navigating — choppy and deep.

< Previous article | Next article >

Notes

[1] Gabriel Collins and Steven R. Miles, “Is the US Preparing to Ban Future LNG Sales to China?” (Houston: Rice University's Baker Institute for Public Policy, April 25, 2024), https://doi.org/10.25613/TA53-BN97.

[2] For more on this, see Peter R. Hartley and Kenneth B. Medlock III, “Debt and Optionality in U.S. LNG Export Projects,” The Energy Journal 44, no. 2 (March 2023), https://doi.org/10.5547/01956574.44.2.phar; and Medlock, “US LNG Exports: Supply, Siting and Bottlenecks,” May 16, 2023, https://www.bakerinstitute.org/research/us-lng-exports-supply-siting-and-bottlenecks, from Energy Futures Initiative (EFI), The Role of U.S. Natural Gas Exports in a Low-Carbon World, April 2023, https://efifoundation.org/topics/the-role-of-u-s-natural-gas-exports-in-a-low-carbon-world/.

[3] U.S. Department of Energy (DOE), Office of Fossil Energy and Carbon Management, “The Temporary Pause on Review of Pending Applications to Export Liquefied Natural Gas,” February 2024, bit.ly/3Mc1cOk.

[4] Collins and Miles.

[5] Figure 2 appears in Stephen Stapczynski, “China’s Taking Control of LNG as Global Demand Booms,” Bloomberg, February 19, 2023, https://www.bloomberg.com/news/articles/2023-02-19/china-s-moving-to-take-control-of-liquefied-natural-gas-as-global-demand-booms.

[6] Miles and Collins, “China’s Big Gas Bet Raises Questions about Complicity with Russia,” Foreign Policy, June 12, 2023, https://foreignpolicy.com/2023/06/12/china-natural-gas-russia-ukraine-war-energy/.

[7] Collins and Miles, “Why Is Europe Not Replacing Russian Pipeline Gas with Long-Term LNG Contracts?” (Houston: Rice University’s Baker Institute for Public Policy, September 13, 2023), https://doi.org/10.25613/3FRC-FA56.

[8] DOE.

[9] Figure 3 appears in Massimo Di Odoardo et al., “Call of Duties: How Emission Taxes on Imports Could Transform the Global LNG Market,” Wood Mackenzie, March 2024, https://www.woodmac.com/horizons/emission-taxes-could-transform-global-lng-market/. The note accompanying the figure reads: “Methane taxes of US$1,400, US$2,800 and US$5,600 per tonne of CH4 have been used, equating to taxes of US$50, US$100 and US$200 per tonne of CO2e, respectively, assuming a global warming potential (100-year GWP) of 28, in line with the IPCC Fifth Assessment Report” (Wood Mackenzie).

[10] Energy Institute (EI), Statistical Review of World Energy, 2024, https://www.energyinst.org/statistical-review.

[11] EI.

[12] EI.

This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and Rice University’s Baker Institute for Public Policy. The views expressed herein are those of the individual author(s), and do not necessarily represent the views of Rice University’s Baker Institute for Public Policy.